Synchronous Motor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

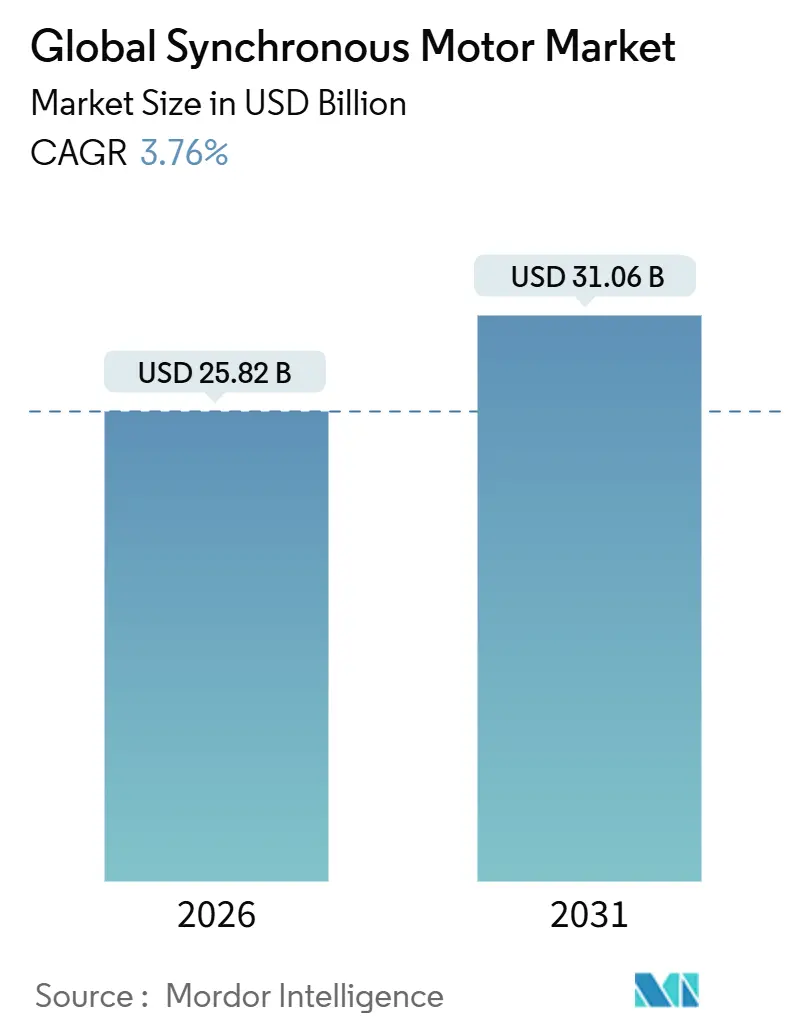

| Market Size (2026) | USD 25.82 Billion |

| Market Size (2031) | USD 31.06 Billion |

| Growth Rate (2026 - 2031) | 3.76% CAGR |

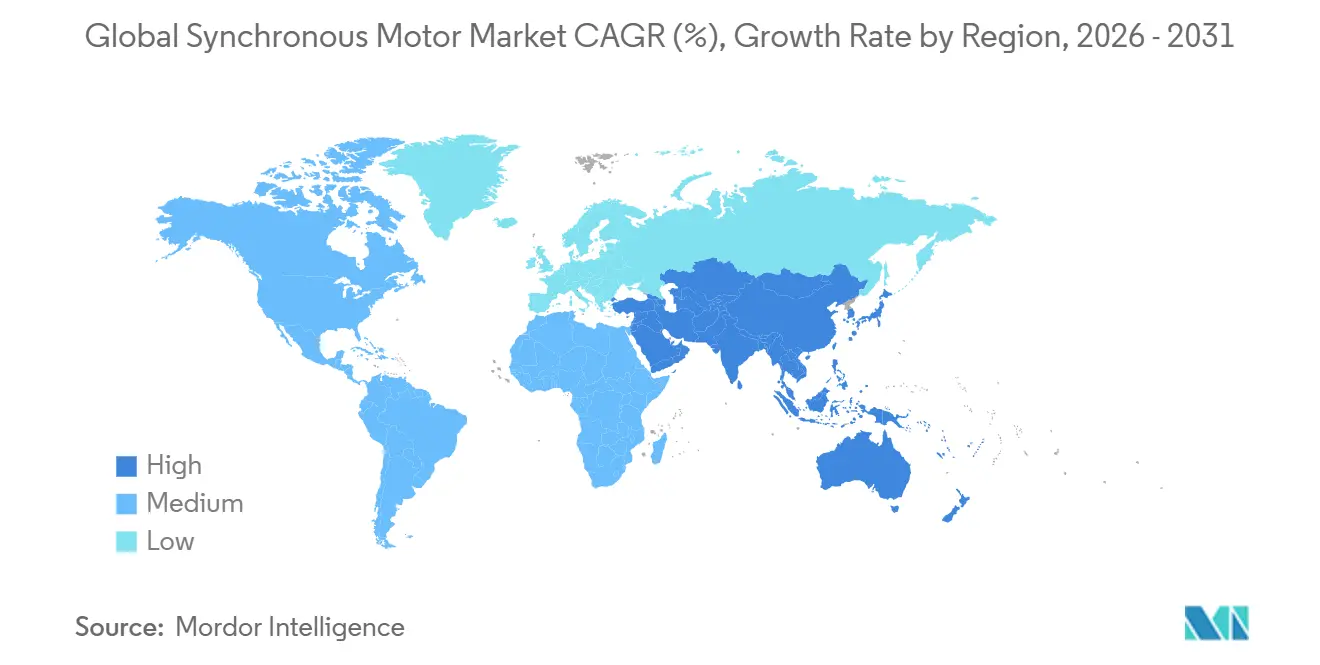

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia Pacific |

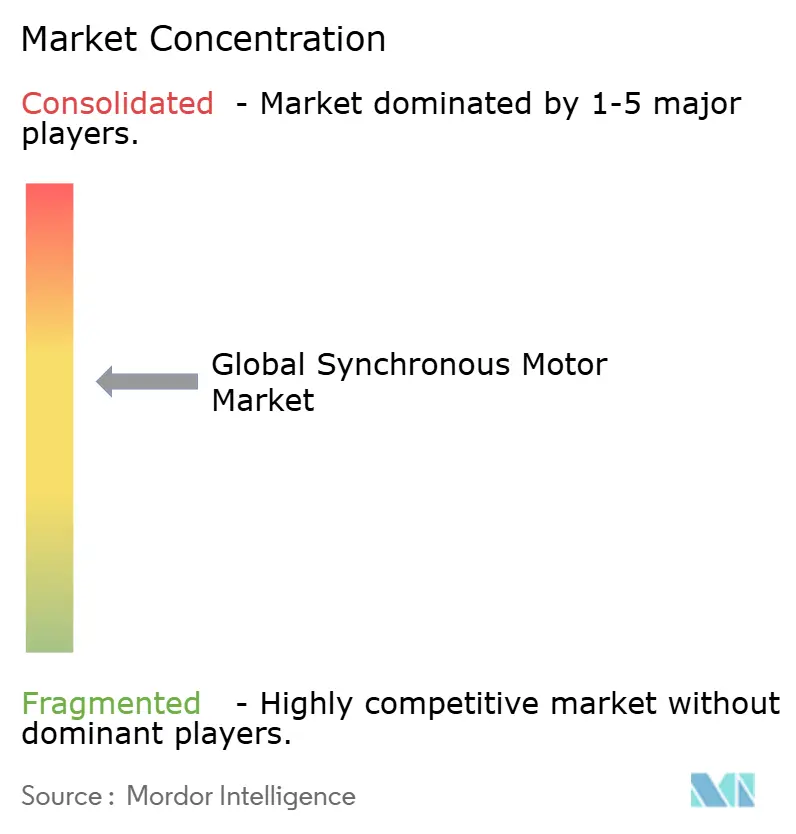

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Synchronous Motor Market Analysis by Mordor Intelligence

The synchronous motor market size stood at USD 25.82 billion in 2026 and is projected to reach USD 31.06 billion by 2031, reflecting a 3.76% CAGR across the forecast horizon. Demand is pivoting from rare-earth permanent-magnet rotors toward reluctance-based alternatives, while traction and propulsion requirements are reshaping power-rating preferences in the synchronous motor market. Regulatory efficiency mandates, the electrification of transport, and distributed manufacturing are widening the addressable opportunity, but supply-chain turbulence for rare earths and thermal-management limits temper short-term adoption curves. Market participants continue to divest low-margin induction portfolios and consolidate intellectual property around synchronous technologies, positioning themselves to capitalize on efficiency-driven retrofit cycles and greenfield renewable-energy investments. With Asia-Pacific enforcing stricter performance standards and serving as both a manufacturing hub and an end-use center, regional dynamics will heavily influence competitive strategy in the synchronous motor market.

Key Report Takeaways

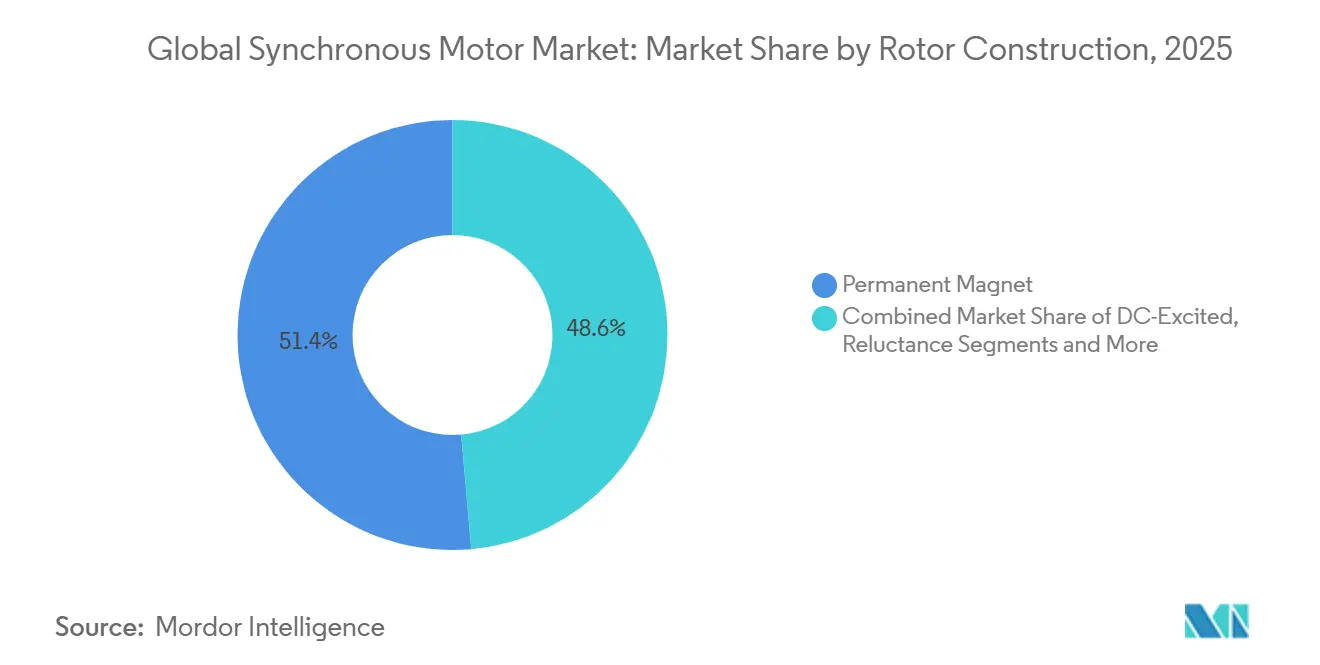

- By rotor construction, permanent-magnet designs led with 47.80% revenue share in 2025, while reluctance variants are poised for an 11.80% CAGR to 2031.

- By power rating, the 1-10 megawatt tier captured 38.50% of synchronous motor market share in 2025, yet the sub-1 megawatt tier is forecast to expand at a 10.40% CAGR.

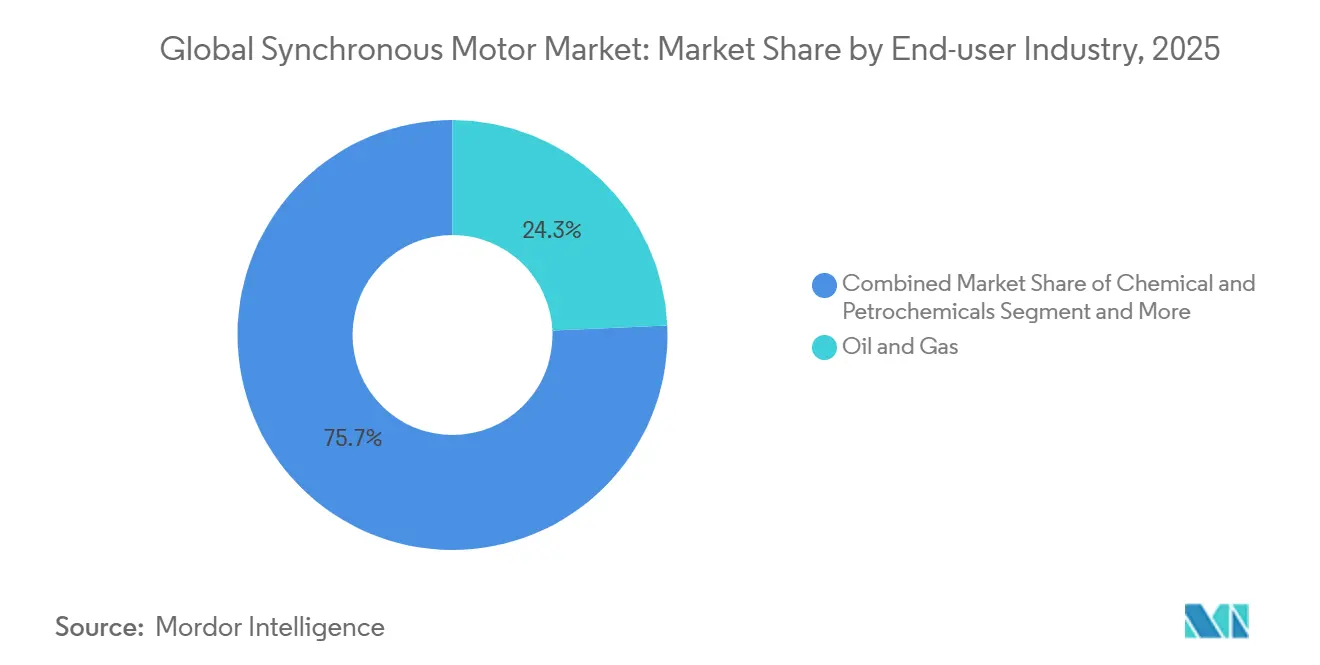

- By end-user industry, oil and gas held 24.30% of 2025 revenue, whereas electric-vehicle OEM demand is projected to rise at a 13.50% CAGR through 2031.

- By application, pumps accounted for 29.10% of 2025 installations, but traction and propulsion uses are advancing at a 14.20% CAGR.

- By geography, Asia-Pacific commanded 34.80% of 2025 revenue, and it is expected to maintain the fastest regional growth at 12.10% annually.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Synchronous Motor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent IE3/IE4 Energy-Efficiency Mandates | +1.2% | Global, with early enforcement in EU, China, and select US states | Medium term (2-4 years) |

| Expansion of HVAC and Industrial Automation | +0.9% | North America, Europe, Asia-Pacific industrial corridors | Medium term (2-4 years) |

| Surge in Electric Vehicle and Traction Motor Demand | +1.5% | Asia-Pacific core, spill-over to North America and Europe | Long term (≥ 4 years) |

| Grid-Scale Renewable Projects, Hydro-Pumped Storage | +0.7% | Europe, China, India, select Middle East markets | Long term (≥ 4 years) |

| Rare-Earth-Free Synchronous Reluctance Motor Adoption Momentum | +1.1% | Global, concentrated in Europe and Asia-Pacific | Medium term (2-4 years) |

| High-Speed Magnetic Bearing Micro-Turbines | +0.3% | North America, Europe, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent IE3/IE4 Energy-Efficiency Mandates

Efficiency regulations anchored in IEC 60034-30-1 and codified into European Union Ecodesign Regulation 2019/1781 have tightened procurement specifications, pushing buyers toward synchronous technologies that readily achieve IE4 and IE5 grades without copper-rotor complexity[1]Source: International Electrotechnical Commission, “IEC 60034-30-1: Efficiency Classes of Line Operated AC Motors,” IEC.CH. China enacted a parallel leap under GB 18613-2020 during 2025, spurring local OEM capacity expansions and accelerating the replacement of legacy induction stock[2]Source: ABB Ltd., “ABB Expands IE5 SynRM Motor Production to Meet Growing Demand,” ABB.COM . Utility and industrial operators with energy expenditures above 40% of total operating cost now see compliance-driven retrofits delivering sub-three-year paybacks, fueling recurrent upgrade cycles across water utilities and petrochemical plants. Market-wide, these mandates lift the synchronous motor market by expanding both baseline volumes and premium-efficiency price points.

Expansion of HVAC and Industrial Automation

Building-code revisions such as ASHRAE Standard 90.1-2022 compel variable-speed control on motors above 10 horsepower, positioning synchronous motors as the preferred choice for rooftop units and chillers that run at part-load most of the year. Equipment launched by Danfoss and Trane in 2025 integrates synchronous reluctance rotors with intelligent drives, documenting 15%–25% electricity savings in field pilots. Parallel gains in factory automation emerge through servo-grade synchronous motors that enable rapid acceleration, regenerative braking, and predictive health analytics via edge-connected drives like Siemens Sinamics S210. These combined HVAC and automation pull-through effects widen the synchronous motor market footprint in both commercial buildings and discrete manufacturing.

Surge in Electric Vehicle and Traction Motor Demand

Automotive electrification is the fastest-growing vector, elevating propulsion-specific design requirements in the synchronous motor market. BorgWarner’s 800-volt permanent-magnet traction platform, awarded by a top Chinese automaker in 2024, typifies the move toward higher-voltage stacks that slim copper cross-sections and enable rapid charging. Concurrently, IEEE-published studies confirm that ferrite-assisted synchronous reluctance rotors achieve 92%-plus drive-cycle efficiency, removing rare-earth constraints without ceding performance. NASA’s 2025 validation of SynRM for regional e-aircraft underscores cross-sector synergies that accelerate R&D investments and volume scaling. As electric vehicles, rail, and marine applications align around high-torque, low-weight architectures, they create multi-year ordering visibility and raise the design-complexity barriers for new entrants.

Rare-Earth-Free Synchronous Reluctance Motor Momentum

Chinese export controls on neodymium and dysprosium compounds tightened in 2024, triggering material-cost spikes and extended lead times that eroded the cost advantage of permanent-magnet machines. European Parliament assessments flagged rare-earth dependence as a strategic vulnerability, promoting investment in ferrite-based or magnet-free rotors. ABB and WEG responded by scaling IE5-rated synchronous reluctance lines across Finland, India, and Brazil, with ABB investing INR 140 crore (USD 17 million) in 2025 capacity. Adoption momentum now spans pumps, fans, and compressors where reluctance rotors offer quick procurement and stable pricing, sustaining double-digit growth inside the synchronous motor market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Up-Front Cost of Permanent-Magnet Rotors | -0.8% | Global, acute in price-sensitive emerging markets | Short term (≤ 2 years) |

| Rare-Earth Supply Volatility | -0.6% | Global, concentrated in Asia-Pacific and Europe | Medium term (2-4 years) |

| Thermal-Management Limits at High Power Density | -0.4% | Global, critical in EV and aerospace traction applications | Long term (≥ 4 years) |

| Induction-VFD Efficiency Parity Pressure | -0.5% | North America, Europe, select Asia-Pacific markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Up-Front Cost of Permanent-Magnet Rotors

Permanent-magnet synchronous units carry a 20%–40% price premium over induction counterparts, magnified in emerging markets where capital budgets are tight, and payback expectations hover under three years[3]Source: London Metal Exchange, “Rare Earth Prices,” LME.COM. Volatile spot prices for neodymium-praseodymium oxide, ranging from USD 48,000–68,000 per metric ton in 2025, translate into USD 8–12 per kilogram of sintered magnet and elevate bill-of-materials costs for every high-end motor. Municipal utilities and small manufacturers therefore defer replacements despite long-run energy savings, slowing near-term volume expansion in the synchronous motor market.

Rare-Earth Supply Volatility

Export-license regimes enacted by China in 2024 introduced supply-chain uncertainty for neodymium, dysprosium, and terbium, pressuring motor OEMs reliant on these inputs. The European Critical Raw Materials Act sets ambitious diversification targets, yet few mining projects have reached scale, keeping supply tight and prices erratic. While this volatility accelerates the pivot to reluctance architectures, the interim redesign costs and performance compromises weigh on profitability and adoption timing within the synchronous motor market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Rotor Construction: Reluctance Designs Accelerate Amid Supply-Chain Hedging

Permanent-magnet rotors retained 47.80% share of 2025 revenue, anchoring high-torque and traction roles where their density justifies cost. However, reluctance designs are forecast to grow at an 11.80% CAGR, driven by ABB’s IE5 and forthcoming IE6 lines and WEG’s 2025-launched W50 platform, which incorporates Regal Rexnord intellectual property. Europe’s regulatory push toward IE5, combined with the scarcity of rare earths, is driving demand for magnet-free or ferrite-assisted options in pumps, fans, and compressors. DC-excited machines remain relevant in hydro-pumped storage and marine propulsion because their field-winding flexibility provides reactive power and voltage support. Hysteresis rotors remain niche, serving precision lab equipment and timing devices where ultra-smooth torque is prized.

Reluctance adoption momentum is especially sharp in Asia-Pacific and Europe, where OEMs report reduced lead times and 20%-plus unit-cost savings versus permanent-magnet equivalents. IEEE research during 2024 confirmed ferrite-assisted synchronous reluctance efficiencies topping 94%, narrowing any practical gulf with neodymium designs and slicing material costs by about one-third. As traction vehicles, HVAC OEMs, and food processors validate these systems, rotor-type balances will realign by 2031, driving fresh competition and technical road-maps inside the synchronous motor market.

By Power Rating: Sub-Megawatt Growth Signals Distributed Adoption

The 1-10 megawatt band dominated with 38.50% of 2025 installations, aligning with centrifugal compressors, chiller drives, and mid-scale industrial automation projects. Yet the sub-1 megawatt class is projected to post a 10.40% CAGR, fueled by distributed manufacturing, modular water treatment, and food processing upgrades, where right-sizing motors trims energy waste. Schneider Electric’s 2024 Altivar Process drive, coupled with 0.75–500 kilowatt synchronous motors, brings cloud-based predictive analytics that help plant managers slash downtime.

Industrial users participating in the United States Better Buildings Initiative logged 15%–30% power savings when oversized induction units were swapped for optimized synchronous machines, with rebate programs pulling payback under two years. While motors exceeding 10 megawatts stay entrenched in wind turbines and large hydro units, the swelling sub-megawatt base indicates that small-horsepower innovation will underpin the next leg of expansion for the synchronous motor market size.

By End-User Industry: EV OEMs Overtake Traditional Heavy Industry Momentum

Oil and gas held 24.30% of 2025 demand, sustained by compressor and pump fleets along pipelines and liquefied natural-gas plants. Electric-vehicle OEMs, however, represent the fastest rising customer pool with a 13.50% CAGR, mirroring global passenger-EV penetration and 800-volt drivetrain architectures. Chemicals, water utilities, and metals together comprise roughly one-third of revenue, exploiting variable-speed synchronous motors for agitators, blowers, and grinding mills.

Food and beverage plants increasingly specify stainless-steel IP-rated synchronous units for hygienic conveyors and refrigeration compressors. Discrete manufacturing, especially automotive and electronics assembly, deploys servo-grade synchronous motors across robotic arms and CNC stages, guided by Mitsubishi Electric and Yaskawa control ecosystems. This diverse uptake underscores that the synchronous motor market is no longer monolithic, but rather a mosaic of high-growth e-mobility users and steady-state industrial stalwarts.

By Application: Traction and Propulsion Outpace Stationary Loads

Pumps remained the largest slice at 29.10% in 2025, reflecting massive installed bases in water utilities and chemical processing. Yet traction and propulsion applications are accelerating at a 14.20% CAGR, driven by electric cars, e-buses, rail, and marine electrification. Siemens Mobility’s Velaro Novo high-speed train employs permanent-magnet drives that cut traction power by 30% while retrieving up to 15% energy during braking. Fans, blowers, compressors, and material-handling equipment together anchor roughly half of total installations.

Marine adopters favor synchronous podded drives for cruise ships and ferries, citing tighter maneuverability and silent operation advantages. As mobile use cases spread, rotor topology, cooling systems, and integration software are tuned for lighter, thermally-efficient assemblies, further diversifying the synchronous motor market.

Geography Analysis

Asia-Pacific, holding 34.80% of 2025 revenue, is on track for a 12.10% CAGR through 2031 as China, India, and Southeast Asian nations raise minimum efficiency thresholds and expand factory automation. Chinese producers such as Wolong Electric funneled CNY 500 million (USD 70 million) into Zhejiang facilities in 2025 to scale IE3 and above units, while India’s Production-Linked Incentive scheme spurred Kirloskar Electric’s new Maharashtra plant capable of 50,000 high-efficiency motors annually. Japan’s Nidec posted 18% synchronous revenue growth in fiscal 2024, benefitting from traction-motor design wins in China and Europe.

North America and Europe combined to capture about 45% of 2025 value. In the United States, Industrial Assessment Centers documented that motor-system upgrades accounted for 22% of recommended efficiency projects, with synchronous equipment specified in more than one-third of replacements. Europe’s Green Deal Industrial Plan earmarked EUR 3 billion (USD 3.3 billion) to back domestic clean-tech manufacturing, financing new motor lines in Poland and Spain. The Middle East pursues large synchronous pump motors for desalination, yet regional share stays below 5%.

South America centers on Brazil, where WEG’s Jaraguá do Sul complex produced more than two million units in 2024, increasingly synchronous as energy costs bite. African demand skews toward mining clusters in South Africa and the Copperbelt, leveraging ABB and Siemens high-horsepower solutions for grinding mills and ventilation. Across regions, the synchronous motor market tracks a two-tier pattern: mature economies retrofit for higher efficiency, while developing markets leapfrog directly to premium-grade synchronous options amid new industrialization.

Competitive Landscape

The synchronous motor market exhibits moderate concentration, with ABB, Siemens, WEG, Nidec, and Toshiba commanding an estimated 40%–45% of 2025 revenue. Vendors are differentiating through rotor technology, integrated drives, and digital-service ecosystems that embed condition monitoring and energy analytics. ABB’s 2025 rollout of expanded IE5 reluctance production across Finland, India, and China reinforces its bet on rare-earth-free platforms, while Siemens leverages its TIA Portal software stack to bind drive and automation layers together.

Mergers and acquisitions accelerate the pivot away from commoditized induction portfolios toward high-margin synchronous offerings. WEG finalized the USD 1.7 billion purchase of Regal Rexnord’s motor division in 2024, gaining reluctance IP and expanding U.S. and Mexican footprints. EBARA’s planned 2026 closure of Mitsubishi Electric’s three-phase motor business deepens integration around pump-motor packages for water utilities. Smaller specialists such as SEVA-tec and Dunkermotoren thrive in servo and micro-motor niches, offering customized rotors and embedded encoders where incumbent mass-production models lack agility.

Standards harmonization under the forthcoming IEC 60034-30-2 revision will tighten verification protocols, curbing efficiency over-statement and sharpening price-performance competition. In parallel, next-generation applications in electric aviation and high-speed micro-turbines entice both incumbents and start-ups, hinting at future market fragments that reward thermal-management and rotor-topology breakthroughs. The interplay of consolidation, R&D realignment, and regulatory scrutiny sets the stage for an increasingly innovation-driven synchronous motor market.

Synchronous Motor Industry Leaders

ABB Ltd.

Siemens AG

WEG S.A.

Nidec Corporation

Toshiba Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: EBARA confirmed regulatory clearance steps for its acquisition of Mitsubishi Electric’s three-phase motor operations remain on schedule for completion during 2026.

- November 2025: EBARA announced the Mitsubishi Electric deal valued at an undisclosed sum, transferring plants and IP for motors up to 500 kilowatts.

- September 2025: ABB expanded IE5 synchronous reluctance capacity in Finland, India, and China, with a capital outlay of INR 140 crore (USD 17 million).

- July 2025: Schneider Electric introduced Altivar Process ATV600 drives that natively control synchronous motors from 0.75 to 500 kilowatts.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the synchronous motor market as all newly manufactured alternating-current machines whose rotor speed is locked to the supply frequency through either direct excitation, permanent magnets, or reluctance designs. Units sold as complete motors for industrial, infrastructure, mobility, and utility drive duties are counted in value terms.

Stand-alone synchronous condensers, stepper motors, refurbished or rewound units, and generator retrofits are excluded.

Segmentation Overview

- By Rotor Construction

- DC-Excited

- Permanent Magnet

- Reluctance

- Hysteresis

- By Power Rating

- ≤1 MW

- 1-10 MW

- >10 MW

- By End-User Industry

- Oil and Gas

- Chemicals and Petrochemicals

- Power Generation

- Water and Wastewater

- Metals and Mining

- Food and Beverage

- Discrete Manufacturing

- HVAC and Refrigeration

- By Application

- Pumps

- Compressors

- Fans and Blowers

- Conveyors and Hoists

- Traction/Propulsion

- Other Applications

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with OEM engineers, motor distributors, EPC contractors, and energy auditors across Asia-Pacific, North America, and Europe validated service-level price spreads, typical replacement cycles, and upcoming IE5 compliance deadlines. Feedback from purchasing managers re-grounded our volume estimates where secondary data were thin.

Desk Research

We built the baseline with open data streams such as UN Comtrade HS-8501 shipment values, the International Energy Agency's efficiency policy tracker, Eurostat industrial production indices, and national motor standards from the IEC and DOE. Company 10-Ks, investor decks, and reputable trade journals filled cost and pricing gaps, while patent analytics from Questel highlighted technology diffusion trends. D&B Hoovers supplied segment revenue splits that helped map vendor footprints across voltage classes. Many additional public and subscription sources were also consulted to cross-check facts and refine assumptions.

Market-Sizing & Forecasting

A top-down reconstruction of global production and trade flows (HS-8501) was first performed, then selectively balanced with bottom-up snapshots, supplier roll-ups, and sampled ASP × volume checks for high-volume frame sizes. Key model drivers include industrial value-added growth rates, grid-connected renewable capacity additions, mandated IE4/IE5 adoption timelines, average rare-earth magnet cost, and electric-vehicle traction motor penetration. Forecasts to 2030 rely on multivariate regression blended with scenario analysis to capture policy and commodity price uncertainty. Gaps from incomplete customs codes are bridged through region-specific penetration ratios validated by primary calls.

Data Validation & Update Cycle

Outputs pass two independent analyst reviews; variance thresholds trigger re-work, and anomalous year-on-year shifts are re-checked with respondents. Models refresh yearly, with interim revisions if major policy or supply-chain shocks emerge. A final pre-publication sweep ensures clients receive the latest view.

Why Mordor's Synchronous Motor Baseline Earns Decision-Makers' Trust

Published figures often differ because firms pick dissimilar voltage bands, include generator retrofits, or roll motors and condensers together.

By anchoring on clear scope rules, using current-year customs data, and refreshing annually, Mordor Intelligence delivers a dependable midpoint that boards can reference with confidence.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 24.87 B (2025) | Mordor Intelligence | - |

| USD 22.80 B (2024) | Regional Consultancy A | Narrow voltage scope; older base year; traction motors omitted |

| USD 26.06 B (2025) | Global Consultancy A | Aggregates AC motor categories, risking double counting |

| USD 27.98 B (2025) | Industry Association B | Includes condensers and servo motors; PPP currency conversion inflates value |

Taken together, the comparison shows that deviations stem chiefly from scope creep and currency methods, while Mordor's disciplined, annually refreshed approach provides a balanced, transparent baseline that can be replicated and stress-tested by clients.

Key Questions Answered in the Report

What was the synchronous motor market size in 2026, and how fast is it growing?

The synchronous motor market size reached USD 25.82 billion in 2026 and is forecast to grow at a 3.76% CAGR to USD 31.06 billion by 2031.

Which region leads current demand for synchronous motors?

Asia-Pacific led with 34.80% revenue share in 2025 and is expected to grow fastest at 12.10% annually through 2031.

Which rotor technology is expanding quickest?

Reluctance-based rotors are projected to register an 11.80% CAGR, outpacing permanent-magnet designs due to rare-earth supply concerns and regulatory pressure.

How are electric vehicles influencing synchronous motor demand?

Electric-vehicle OEMs form the fastest-growing end-user segment at 13.50% CAGR as they deploy high-voltage permanent-magnet and reluctance traction motors.

Page last updated on: