Industrial Bearings Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

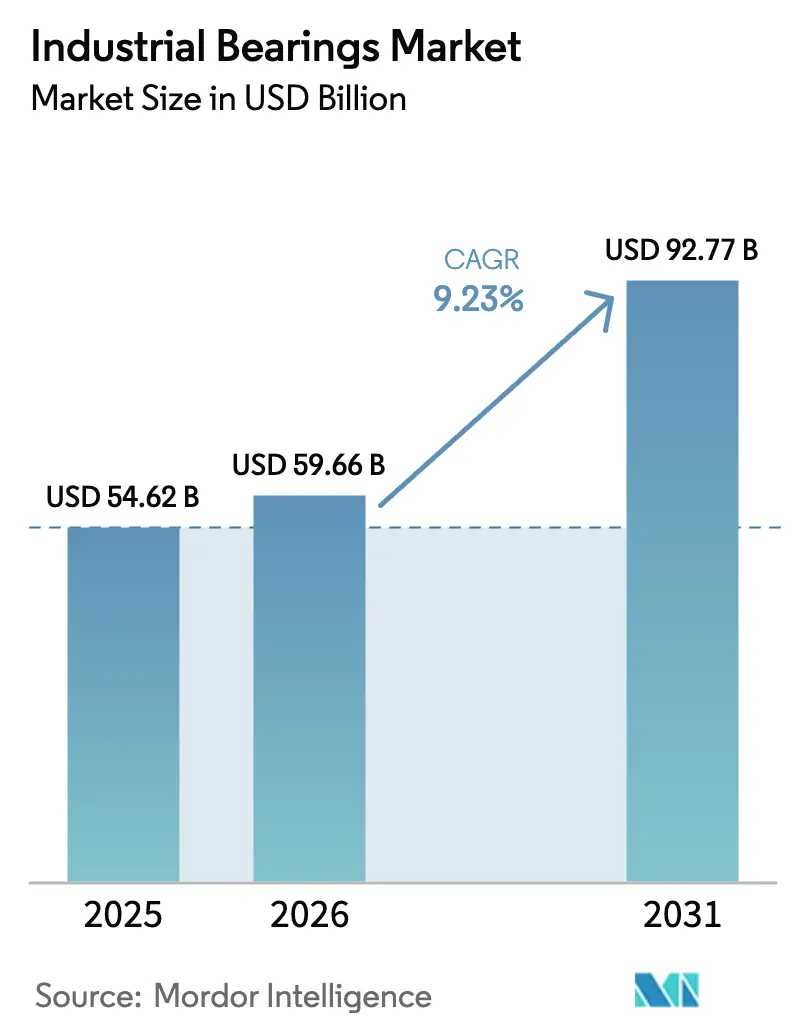

| Market Size (2026) | USD 59.66 Billion |

| Market Size (2031) | USD 92.77 Billion |

| Growth Rate (2026 - 2031) | 9.23% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Bearings Market Analysis by Mordor Intelligence

The industrial bearings market size is projected to be USD 54.62 billion in 2025, USD 59.66 billion in 2026, and reach USD 92.77 billion by 2031, growing at a CAGR of 9.23% from 2026 to 2031. Strong demand from electric-vehicle drivetrains, on-shore wind installations, and sensor-equipped smart bearings is widening the revenue base. Hard-to-substitute large-diameter slewing rings for 5 MW turbines, higher-value e-axle and wheel-hub units in battery-electric cars, and digitally enabled uptime contracts are lifting the average selling price across the industrial bearings market. Regional re-shoring programs in North America and near-shoring to Mexico are shortening supply chains, while hydrogen-compressor pilots in Europe and the Middle East are opening a niche for magnetic and ceramic variants. Suppliers with vertically integrated steel forging and heat-treatment lines are absorbing alloy price volatility better than mid-tier competitors and are using their cost advantage to defend market share in the industrial bearings market.

Key Report Takeaways

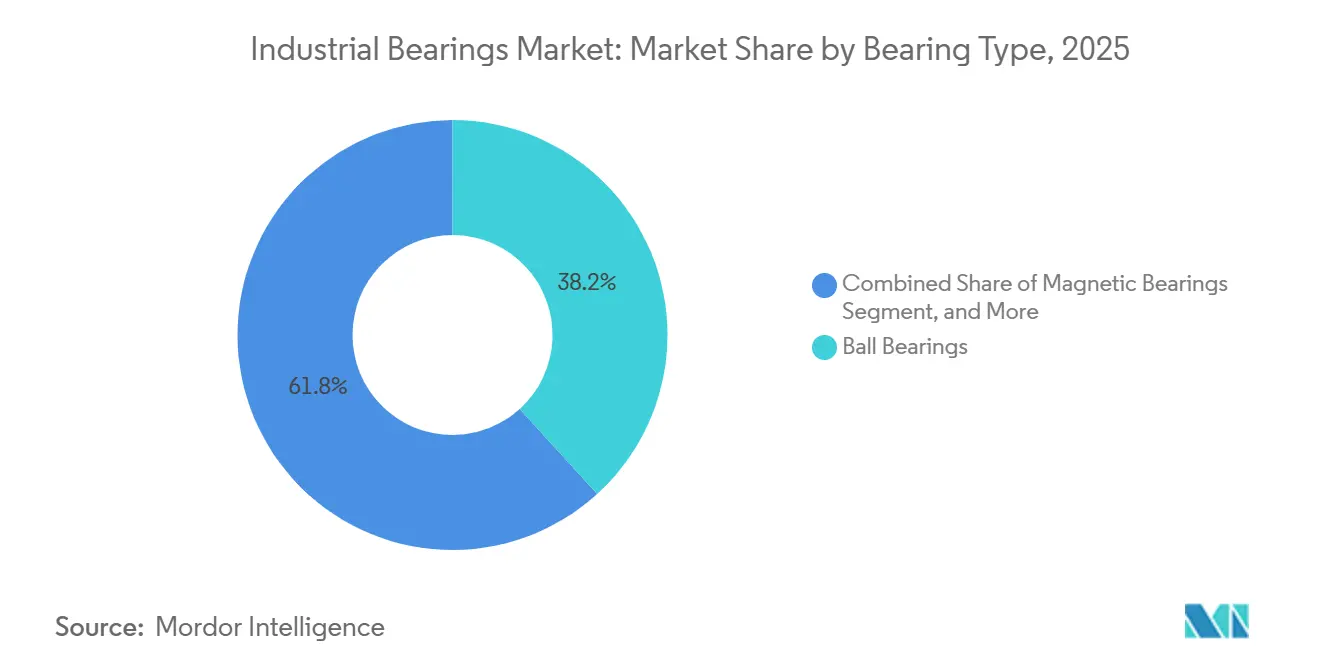

- By bearing type, ball bearings led with 38.24% of the industrial bearings market share in 2025; magnetic bearings are forecast to expand at a 10.21% CAGR through 2031.

- By material, alloy steel captured 49.22% of the industrial bearings market in 2025, while ceramic materials are advancing at a 9.93% CAGR through 2031.

- By end-user, automotive accounted for 29.63% of revenue in 2025; the energy segment is projected to record the highest CAGR of 10.89% through 2031.

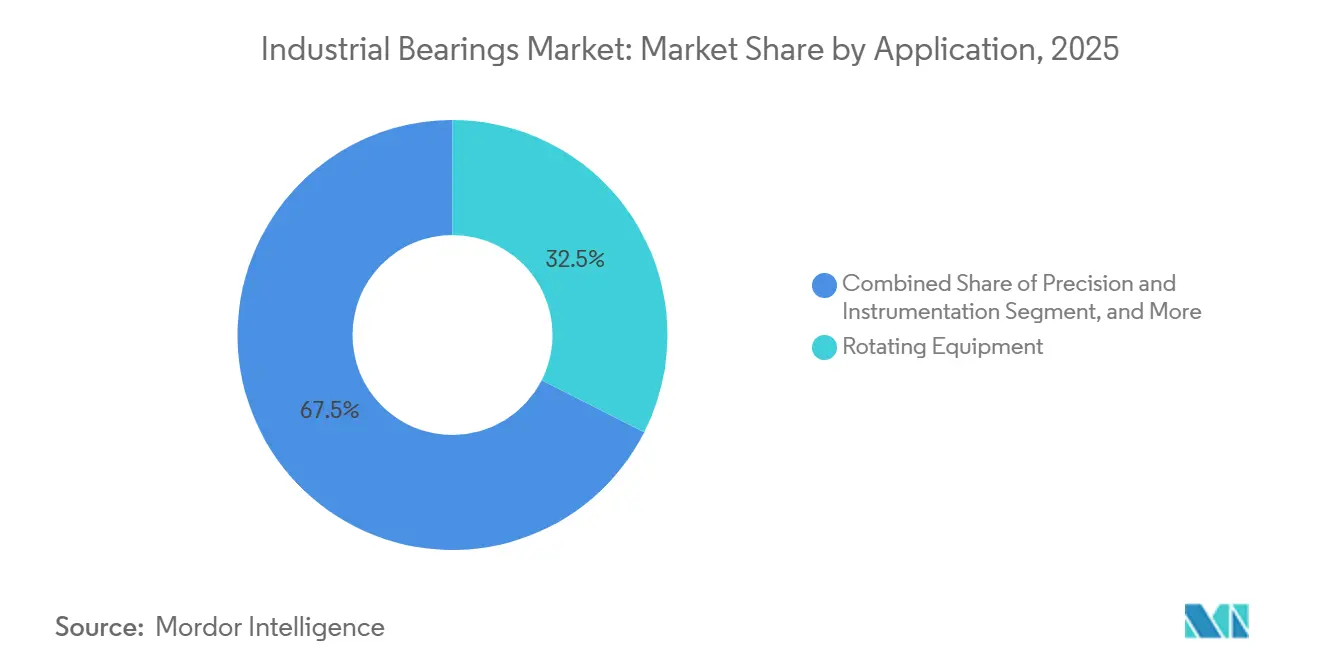

- By application, rotating equipment accounted for 32.47% of the industrial bearings market in 2025, and precision and instrumentation is projected to grow at a 10.24% CAGR through 2031.

- By sales channel, OEMs accounted for 66.79% of 2025 revenue; aftermarket and MRO are set to grow at a 9.67% CAGR through 2031.

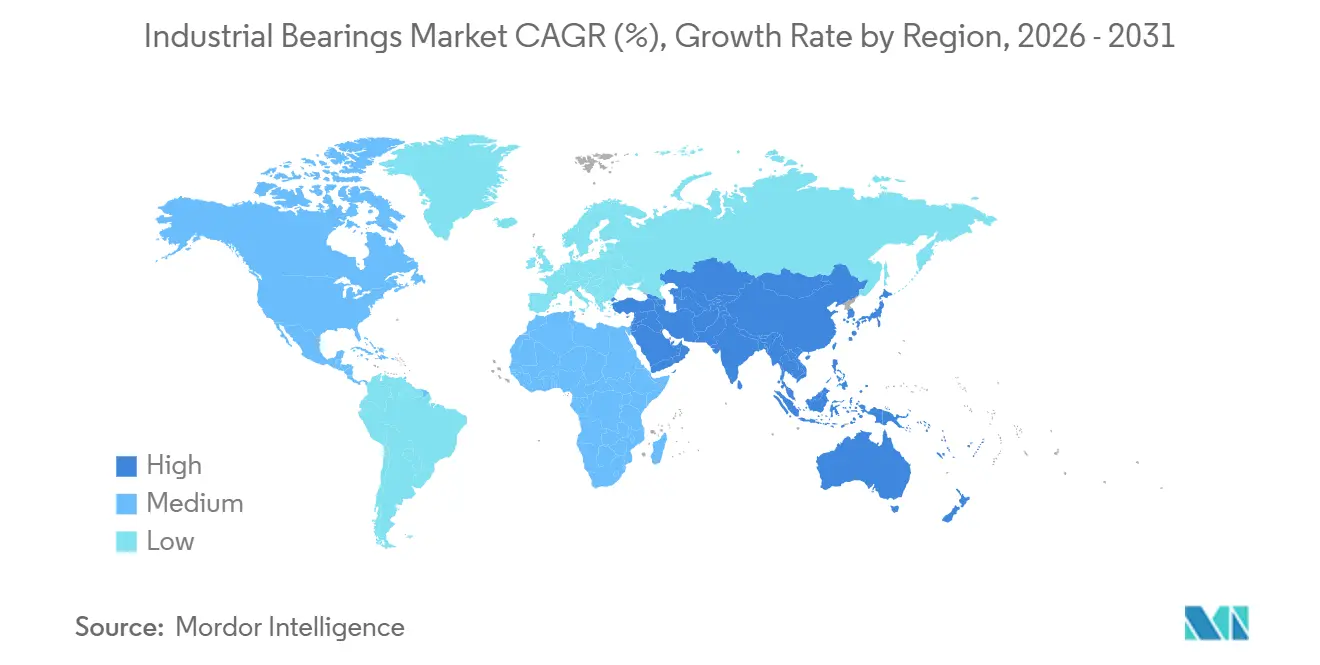

- By geography, Asia-Pacific commanded a 53.21% share of the industrial bearings market in 2025, whereas the Middle East is expected to post a 10.29% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Industrial Bearings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Automotive and EV Production Rebound | +1.8% | Global (China, India, United States) | Medium term (2-4 years) |

| Rapid Adoption of Predictive-Maintenance-Ready Smart Bearings | +1.5% | North America and Europe, spillover to Asia-Pacific | Long term (≥ 4 years) |

| Expansion of On-Shore Wind Turbines in Asia-Pacific and Europe | +1.3% | Asia-Pacific core, Europe | Medium term (2-4 years) |

| Re-Shoring of Industrial Equipment Supply Chains in North America | +0.9% | North America, selective near-shoring to Mexico | Medium term (2-4 years) |

| Niche Demand for Magnetic and Ceramic Bearings in Hydrogen Compressors | +0.6% | Europe, Middle East, pilot projects in Asia-Pacific | Long term (≥ 4 years) |

| Surge in Robotics and Cobots Requiring Low-Friction Miniature Bearings | +0.7% | Global, led by Asia-Pacific electronics plants | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Automotive and EV Production Rebound

Global light-vehicle output rebounded to 88 million units in 2025 as electrification lifted the average bearing content per wheel-end and introduced new e-axle designs that must tolerate higher torque loads.[1]International Energy Agency, “Global EV Outlook 2025,” iea.org Ceramic-hybrid wheel-hub bearings that cut rolling resistance by 15% and match battery warranties illustrate how the industrial bearings market is monetizing efficiency gains. Indian passenger-vehicle builds grew 8% in 2025, and two-wheeler electrification added incremental demand for small-diameter ball bearings. North American commercial-vehicle production rose 6%, adding larger tapered-roller sets for heavy e-trucks. Together, these shifts are steering capital toward high-load, sensor-integrated designs that defend margins within the industrial bearings market.

Rapid Adoption of Predictive-Maintenance-Ready Smart Bearings

Sensorized housings that stream vibration and temperature data are turning bearings into IIoT nodes capable of flagging failures 4-6 weeks ahead and triggering just-in-time replacements.[2]SKF Group, “Enlight Predictive Maintenance Platform,” skf.com SKF’s Enlight deployments in 2025 reduced unplanned downtime by 22% across paper mills, while NSK’s cloud-linked spherical-roller units cut regreasing intervals from 500 to 1,200 hours. Subscription-based uptime contracts are shifting revenue from upfront sales to recurring service, rewarding incumbents with broad installed bases and eroding the price advantage of low-cost entrants. As industrial IoT penetration reached 34% in 2025, predictive-maintenance use cases became the largest share of sensor rollouts.

Expansion of Onshore Wind Turbines in Asia-Pacific and Europe

Onshore wind additions hit 110 GW in 2025, with each multi-megawatt turbine incorporating 40-50 bearings, many exceeding 4 m in diameter.[3]Global Wind Energy Council, “Global Wind Report 2025,” gwec.net Slewing-ring unit value rises 30-40% on 5 MW platforms versus legacy 2 MW models. Schaeffler’s newly expanded German line machines ring up to 5 m, underlining the premium segment’s localization trend. Repowering of 15-year-old European farms is creating a parallel aftermarket, while India and Vietnam have redirected delayed offshore budgets to faster onshore builds, sustaining double-digit growth in the industrial bearings market.

Reshoring of Industrial Equipment Supply Chains in North America

Announced North American reshoring investment reached USD 427 billion during 2021-2025, with heavy-equipment assembly accounting for 18%. Timken added 25% forging capacity in Ohio to secure domestic tapered-roller supply for Class 8 axles. RBC Bearings acquired a Connecticut precision grinder to support aerospace contracts subject to Buy America thresholds. Lead times for Asian imports once at 16 weeks, have fallen to 8 weeks for regional supply, giving local producers a time-to-market edge that is translating into share gains across the industrial bearings market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Alloy and Energy Prices Squeezing Margins | -1.2% | Global, acute in Europe and North America | Short term (≤ 2 years) |

| Automotive ICE-to-EV Transition Reducing Engine-Related Bearing Volumes | -0.9% | Global, led by Europe and China | Medium term (2-4 years) |

| IP-Driven Import Restrictions on Chinese Bearings in United States and EU | -0.6% | United States, European Union | Medium term (2-4 years) |

| Additive-Manufactured Bushings Replacing Small Roller Bearings in Aerospace | -0.4% | North America, Europe clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Alloy and Energy Prices Squeezing Margins

Chrome-steel surcharges climbed 12% in H1 2025 after ferrochrome exports from South Africa tightened and EU electricity rates spiked, trimming mid-tier manufacturers’ gross margins by up to 300 basis points. Energy-intensive heat treatment accounts for nearly 20% of production costs, so regional gas price volatility is quickly reflected in quotes. Larger players with captive steel mills are absorbing swings, while smaller shops are shifting to polymer substitutes for non-critical uses, a pattern that could limit price pass-through in the industrial bearings market.

Automotive ICE-to-EV Transition Reducing Engine-Related Bearing Volumes

Battery-electric architectures cut bearing counts from roughly 180 units per vehicle to nearer 90 by eliminating crankshaft and transmission locations. European diesel and gasoline registrations fell to 68% of total sales in 2025, while Chinese EV penetration reached 38%, accelerating the decline. Engine-bearing revenue at legacy suppliers slid 7% in 2025, even as e-mobility product lines rose 22%. This substitution gap means that overall unit growth in the industrial bearings market will increasingly come from higher-value wheel-end and e-axle sets rather than engine components.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Bearing Type: Magnetic Variants Gain Traction in Contact-Free Applications

Ball bearings retained a 38.24% share of the industrial bearings market in 2025, buoyed by high-speed electric motors, appliances, and automotive wheel hubs. Roller bearings followed in heavy-load niches such as mining-truck axles and wind-turbine main shafts, while plain bearings filled oscillating roles in construction equipment. Although still a small base, magnetic bearings are forecast to post a 10.21% CAGR, lifted by hydrogen compressors and high-speed turbomachinery that demand oil-free operation. Sensor integration is now standard: SKF and NSK embed accelerometers in spherical- and tapered-roller housings to feed cloud diagnostics.

Carbide-coated roller races extend life 40% in dusty mines, and hybrid ceramic-steel ball bearings cut weight 30% in electric-vehicle hubs. Igus uses 3D-printed polymer cages that reduce wear by 25% in collaborative robot joints. Adoption barriers for magnetic units, chiefly control-system costs, are easing as maintenance-free lifecycles offset higher capex, positioning them for faster penetration into the industrial bearings market over the forecast horizon.

By Material: Ceramic and Hybrid Composites Address Extreme Environments

Alloy steel accounted for 49.22% of revenue in 2025, thanks to its strength-to-cost profile, yet ceramic grades are projected to grow at a 9.93% CAGR through 2031, driven by silicon-nitride balls for electric-vehicle wheel hubs and zirconia rings for MRI scanners. Polymer composites meet food-processing mandates for lubrication-free operation, and ceramic-steel hybrid rolling-element bearings prevent electrical pitting in wind-turbine generators.

Silicon-nitride hybrids cut rolling resistance by 15% and align grease life with 150,000-km EV service windows. Polymer bearings are displacing bronze in FDA-regulated conveyors, while diamond-like carbon coatings on steel races help defend incumbent volumes by extending hardness without premium material cost. Together, these advances diversify material mixes and protect margins across the industrial bearings market.

By End-User Industry: Energy Sector Outpaces Automotive in Forecast Growth

Automotive accounted for 29.63% of 2025 demand, yet the energy segment is set to register a 10.89% CAGR as wind-turbine repowering, hydrogen infrastructure, and oil-and-gas upgrades lift value content per unit. Even at lower production volumes, aerospace applications necessitate the use of AS9100-traceable bearings, which are critical for ensuring the reliability and safety of flight-critical actuators and landing gear. This requirement contributes to a premium pricing mix within the industry.

Hydrogen compressors specify magnetic and ceramic units that command multiples of traditional steel prices, while mining uses reconditionable large-bore spherical-roller bearings that can be refurbished three times, lowering lifecycle cost in copper and lithium projects. Automotive volumes will gradually migrate from engine to wheel-hub and e-axle designs, limiting downside, but energy’s share of the industrial bearings market will expand the fastest through 2031.

By Application: Precision Instrumentation Driven by Robotics and Medical Miniaturization

Rotating equipment accounted for 32.47% of the 2025 revenue in the industrial bearings market, covering motors, pumps, and compressors that benefit from standardized interfaces. Linear-motion systems in semiconductor plants and machine tools require micron-level repeatability and vacuum-grade lubricants. Engine and driveline bearings remain relevant in commercial trucks, while chassis and wheel hubs gain importance in EVs due to integrated sensor rings.

Precision and instrumentation applications are poised for a 10.24% CAGR, the segment’s strongest pace, as collaborative robots and medical imaging demand miniature bearings with sub-10-micron tolerances. Hybrid ceramics mitigate electrical stress from variable-frequency drives in motors, while dental drills now achieve sub-50-dB noise levels using ultra-quiet miniature ball bearings. These trends elevate average unit value and reinforce premium niches inside the industrial bearings market.

By Sales Channel: Aftermarket Growth Reflects Sealed Bearing Proliferation

OEM contracts accounted for 66.79% of 2025 sales because designs are locked in years before volume production. However, aftermarket and MRO streams are projected to rise at a 9.67% CAGR as sensor alerts shift replacement toward condition-based cycles. In 2025, e-commerce platforms, including Applied Industrial Technologies, provided enhanced real-time inventory visibility, thereby accounting for 28% of the total aftermarket purchases.

Sealed bearings increase the interval duration by approximately 25%. However, their higher unit value offsets the slower turnover rate, thereby contributing to revenue growth. The consolidation of distributors enhances their leverage with suppliers and expands the scope of next-day delivery services. Additionally, regional reshoring efforts have significantly reduced lead times from 16 weeks to 8 weeks. These factors are expected to sustain the upward trajectory of the aftermarket's share within the industrial bearings market through 2031.

Geography Analysis

Asia-Pacific dominated the industrial bearings market with 53.21% of global revenue in 2025 as China assembled roughly 30 million vehicles and added 65 GW of onshore wind capacity, while India’s two-wheeler and commercial-vehicle builds expanded 8% year on year. Japan and South Korea contributed high-value precision bearings for robotics, semiconductor equipment, and machine tools, where unit prices can exceed USD 500 because tolerances sit in the single-micron range. Southeast Asia became a secondary hub for grinding and assembly, with Vietnam and Thailand attracting new plants that benefit from lower labor costs and trade-preference agreements. Regional suppliers also diversified sourcing to buffer against tariff uncertainty, expanding the industrial bearings market footprint beyond China without diluting scale efficiencies.

The Middle East is projected to post a 10.29% CAGR through 2031 as transport megaprojects in the United Arab Emirates and Saudi Arabia specify corrosion-resistant wheel-hub, axle-box, and pump bearings for high-speed rail, metro extensions, and desalination plants. Saudi Arabia’s NEOM and Red Sea programs require stainless-steel and polymer units that withstand seawater exposure, lifting average selling prices. North America’s reshoring wave compressed lead times from 16 to 8 weeks when Timken and RBC Bearings expanded domestic forging and heat-treatment capacity, satisfying Buy America content rules and stabilizing supply for agricultural-equipment and mining-truck OEMs. Europe shows mixed signals: shrinking engine-bearing volumes in cars are offset by repowering of aging wind farms, which need slewing rings exceeding 2 m in diameter and miniature precision sets for industrial automation cells.

South America’s demand remains modest, driven mainly by Brazil’s agricultural-equipment aftermarket and mining spares for copper and iron-ore operations. Africa’s volumes concentrate in South African and Zambian mines, where refurbishable spherical-roller bearings reduce downtime in crushers and mills, and in Egypt’s metro expansions along the Suez corridor that use axle-box designs originally qualified for European commuter trains. OEMs continue to diversify procurement across Mexico, Eastern Europe, and Southeast Asia to hedge geopolitical risk, a trend that spreads tooling investment across multiple low-cost jurisdictions. This geographic diversification strengthens supply resilience but also heightens competition for new grinding lines, keeping the industrial bearings market both regionally balanced and strategically fluid.

Competitive Landscape

Four incumbent suppliers, SKF, NSK, Schaeffler, and Timken, controlled a mid-40% share of the industrial bearings market in 2025, reflecting moderate concentration bolstered by decades of process know-how and captive steel or heat-treatment assets. Vertical integration lets these firms absorb alloy-price spikes that trimmed mid-tier competitors’ margins when chrome-steel surcharges climbed 12% in early 2025. Their size also supports multi-year co-engineering agreements with automotive, wind, and aerospace OEMs, locking in share over an entire product life cycle. Digital-service bundles are the new differentiator: NSK’s cloud-connected bearings extend regreasing intervals by 140% and generate subscription revenue, while SKF’s Enlight platform cuts unplanned downtime by 22% in cement and paper mills.

Emerging disruptors are carving out niches. Honeywell’s additive-manufactured aerospace housings integrate bearing seats and eliminate small roller sets in actuators, trimming part count by 40% and weight by 15%. Polymer-composite leader igus shifted from plain bushings to 3D-printed ball-bearing cages, reducing wear by 25% in robotic pick-and-place joints. Ceramic-hybrid specialists are winning orders for electric-vehicle wheel hubs and wind-turbine generators that require electrical-pitting immunity, while magnetic-bearing startups are targeting hydrogen compressors, where contact-free rotation eliminates the risk of oil contamination. These challengers rarely threaten the incumbents’ core automotive volumes but do pressure margins at the performance edge of the industrial bearings market.

Strategic moves in 2025 underscored the pivot toward higher-value segments. NSK bought a European steering-system bearing line to deepen electric-power-steering content, Schaeffler committed EUR 150 million (USD 161 million) to expand 5-m slewing-ring heat treatment in Germany, and SKF spun off its India automotive arm to unlock valuation multiples tied to aftermarket growth. Timken named a Chief Technology Officer in January 2026 to accelerate digital-twin analytics across its portfolio, signaling software’s rising weight in competitive positioning. Compliance barriers remain high. ISO 281 life testing, AS9100 audits, and 3-A sanitary approvals favor incumbents with in-house labs and field-failure databases. Yet the window for differentiation is shifting from sheer scale to mastery of materials science and data services, keeping rivalry intense and ensuring continuous innovation within the industrial bearings market.

Industrial Bearings Industry Leaders

Aktiebolaget Svenska Kullagerfabriken

NSK Ltd.

NTN Corporation

The Timken Company

Schaeffler AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Timken appointed a Chief Technology Officer to accelerate digital-twin development and predictive-analytics capabilities across its bearing portfolio.

- October 2025: SKF completed the demerger of its India automotive arm into a standalone entity to focus investment on EV wheel-hub bearings and sensor-integrated designs.

- September 2025: NSK acquired a steering-systems bearing portfolio from a European supplier, strengthening its electric-power-steering actuator range.

- March 2025: NSK rolled out reconditionable large-size tapered-roller bearings for mining haul trucks, designed for three refurbishment cycles.

Global Industrial Bearings Market Report Scope

The Industrial Bearings Market Report is Segmented by Bearing Type (Ball Bearings, Roller Bearings, Plain Bearings, Magnetic Bearings, Other Bearing Types), Material (Alloy Steel, Ceramic, Polymer/Composite, Hybrid), End-User Industry (Automotive, Aerospace, Energy, Mining and Metals, Construction and Heavy Equipment, Food and Beverage, Material Handling and Logistics, Other End-User Industries), Application (Rotating Equipment, Linear Motion Systems, Engine, Transmission and Driveline, Chassis and Wheel Hubs, Precision and Instrumentation), Sales Channel (OEM, and Aftermarket/MRO), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Ball Bearings |

| Roller Bearings |

| Plain Bearings |

| Magnetic Bearings |

| Other Bearing Types |

| Alloy Steel |

| Ceramic |

| Polymer / Composite |

| Hybrid |

| Automotive |

| Aerospace |

| Energy |

| Mining and Metals |

| Construction and Heavy Equipment |

| Food and Beverage |

| Material Handling and Logistics |

| Other End-User Industries |

| Rotating Equipment |

| Linear Motion Systems |

| Engine, Transmission and Driveline |

| Chassis and Wheel Hubs |

| Precision and Instrumentation |

| OEM |

| Aftermarket / MRO |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Bearing Type | Ball Bearings | ||

| Roller Bearings | |||

| Plain Bearings | |||

| Magnetic Bearings | |||

| Other Bearing Types | |||

| By Material | Alloy Steel | ||

| Ceramic | |||

| Polymer / Composite | |||

| Hybrid | |||

| By End-User Industry | Automotive | ||

| Aerospace | |||

| Energy | |||

| Mining and Metals | |||

| Construction and Heavy Equipment | |||

| Food and Beverage | |||

| Material Handling and Logistics | |||

| Other End-User Industries | |||

| By Application | Rotating Equipment | ||

| Linear Motion Systems | |||

| Engine, Transmission and Driveline | |||

| Chassis and Wheel Hubs | |||

| Precision and Instrumentation | |||

| By Sales Channel | OEM | ||

| Aftermarket / MRO | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the global industrial bearings space likely to be by 2031?

Total value is projected to reach USD 92.77 billion by 2031, expanding at a 9.23% CAGR from 2026.

Which bearing design is expected to post the fastest growth over the next five years?

Magnetic, contact-free units are forecast to grow at roughly 10.21% a year, helped by hydrogen-compression and high-speed turbomachinery adoption.

Why are ceramic and hybrid bearings gaining traction in electric vehicles?

Silicon-nitride rolling elements cut rolling resistance by about 15% and extend grease life to match 150,000 km service windows, improving drivetrain efficiency.

What role does predictive maintenance play in aftermarket replacement timing?

Sensorized bearings can flag failure four to six weeks in advance, enabling condition-based ordering that reduces unplanned downtime by more than 20%.

Which region is set to contribute the most incremental revenue through 2031?

Asia-Pacific remains the largest contributor due to EV production and wind-turbine installs, while the Middle East shows the highest growth rate at 10.29% CAGR.

How are alloy-price swings influencing supplier strategies?

Vertically integrated producers with in-house forging absorb cost volatility better, while mid-tier firms are turning to polymer or lower-alloy substitutes in non-critical uses.

Page last updated on: