Intelligent Motor Control Centers (IMCC) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

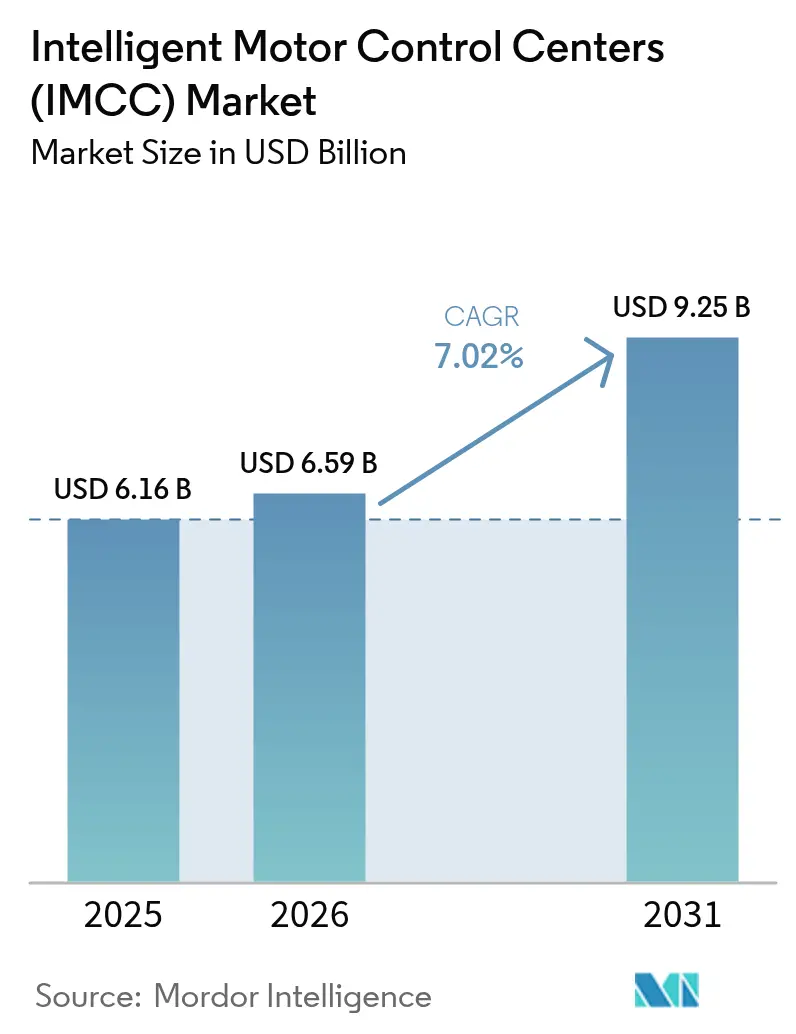

| Market Size (2026) | USD 6.59 Billion |

| Market Size (2031) | USD 9.25 Billion |

| Growth Rate (2026 - 2031) | 7.02% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players_Market_-_Major_Players.webp) *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Intelligent Motor Control Centers (IMCC) Market Analysis by Mordor Intelligence

The intelligent motor control centers (IMCC) market size is expected to grow from USD 6.16 billion in 2025 to USD 6.59 billion in 2026 and is forecast to reach USD 9.25 billion by 2031 at 7.02% CAGR over 2026-2031. Rising digitalization of process plants, stringent energy-efficiency mandates, and demand for predictive maintenance continue to shift investment away from passive starters toward network-aware intelligent systems that help operators curb unplanned downtime and participate in tariff-based load management programs. Low-voltage solutions retained the bulk of installed capacity in 2024; however, medium-voltage variants are now attracting the fastest capital growth, as mining, desalination, and bulk-water projects require arc-flash mitigation and remote diagnostics. Variable speed drives (VSDs) are the standout component because they unlock real-time energy arbitrage and enable compliance with IE3-plus efficiency rules. Meanwhile, the Asia Pacific’s infrastructure build-out and manufacturing reshoring programs keep the region at the top of the demand curve, while North America and Europe register steady upgrade cycles focused on cybersecurity and efficiency standards. Competitive dynamics remain vigorous, with the top five suppliers accounting for approximately 60% of the market share. However, regional specialists maintain pricing pressure by tailoring retrofit kits that integrate with legacy control architectures.

Key Report Takeaways

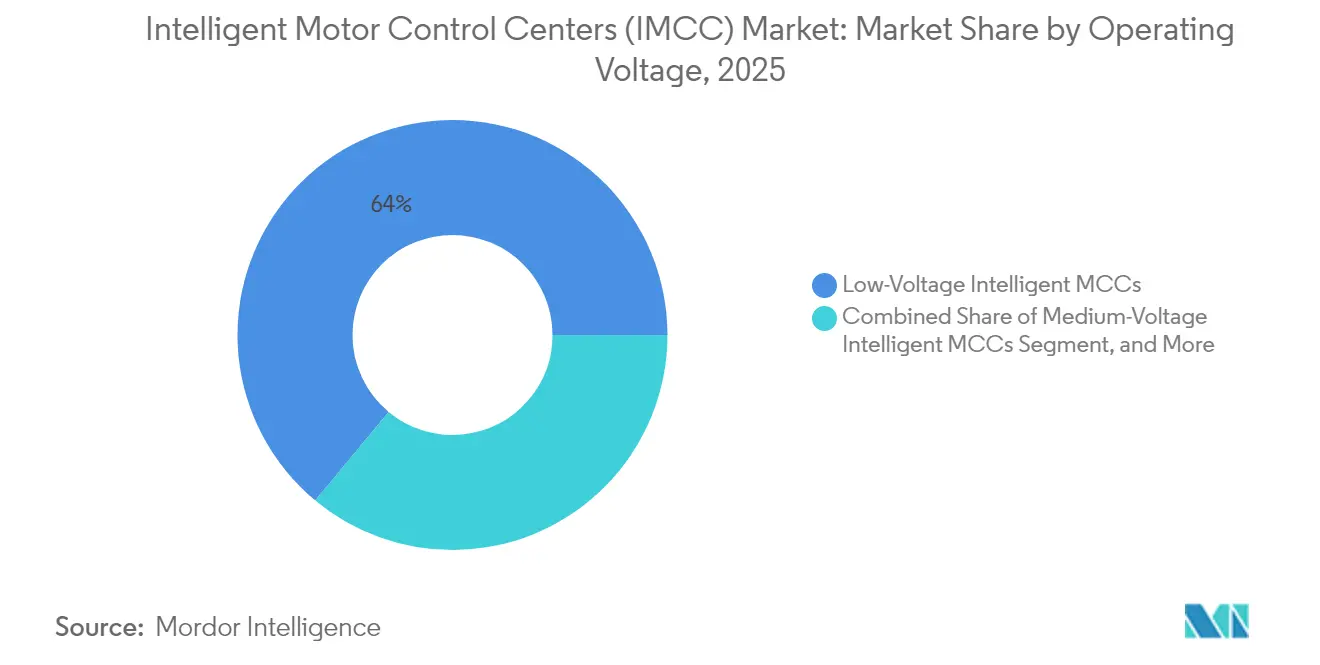

- By operating voltage, medium-voltage intelligent solutions are projected to expand at a 8.96% CAGR from 2025 to 2026 and remain the fastest-growing segment through 2031.

- By component, VSDs captured the highest growth rate, with a 9.62% CAGR through 2031, whereas busbars retained 24.05% of the intelligent motor control center market share in 2025.

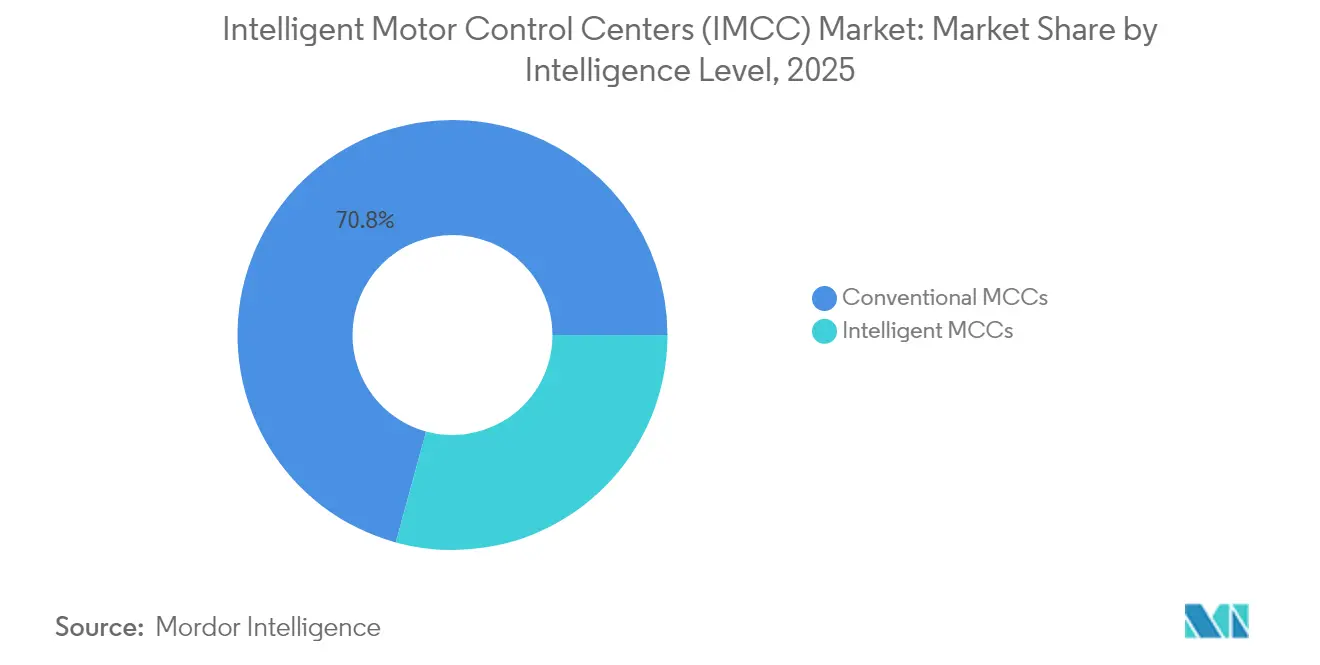

- By intelligence level, intelligent variants are forecast to accelerate at 12.15% CAGR through 2031, while conventional counterparts will continue to lose share.

- By end-user, the food and beverage sector is projected to grow at a 9.07% CAGR to 2031, surpassing industry growth projections, whereas the oil and gas sector maintained a 24.76% revenue lead in 2025.

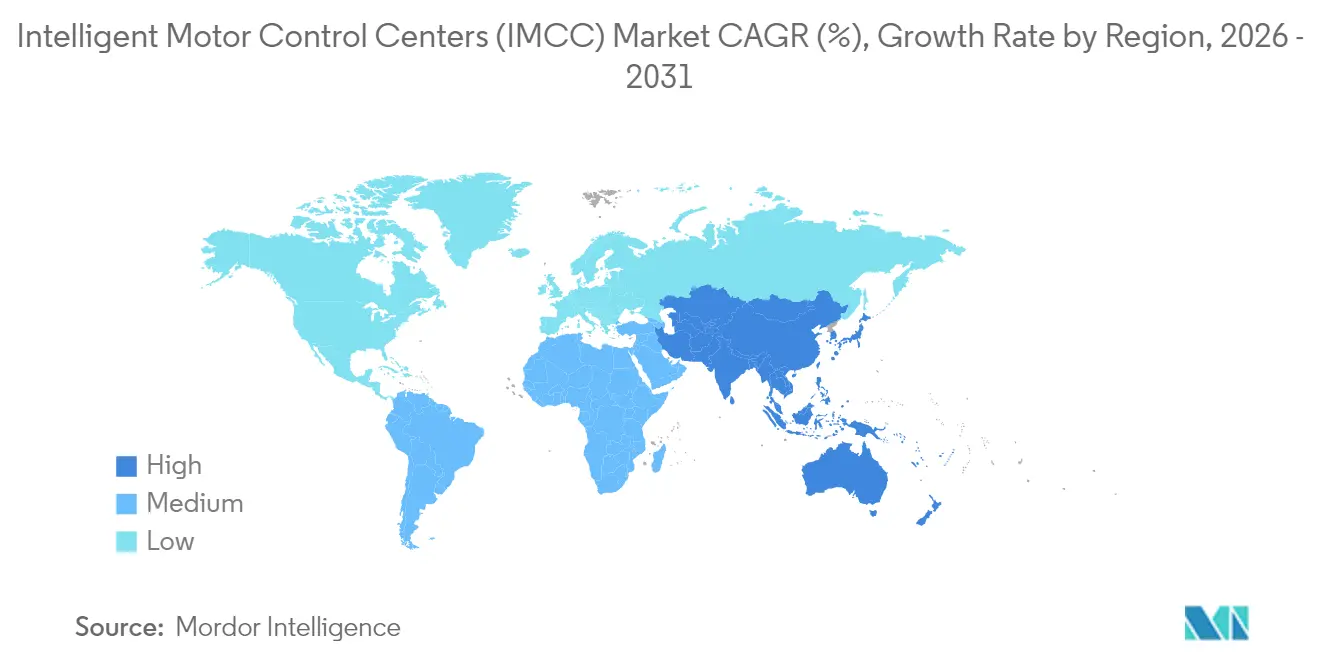

- By geography, the Asia Pacific region dominated with 38.12% of 2025 revenue and is expected to grow at an 8.21% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Intelligent Motor Control Centers (IMCC) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of Industrial Automation and Industry 4.0 Initiatives | +1.8% | Global, led by Germany, China, United States | Medium term (2-4 years) |

| Energy Efficiency Regulations Driving Smart Motor Control Adoption | +1.5% | EU, North America, China | Short term (≤ 2 years) |

| Superior Diagnostics and Predictive Maintenance Capability | +1.3% | Global, early gains in oil and gas, mining | Medium term (2-4 years) |

| Integration of Digital Twins for Virtual Commissioning and Lifecycle Optimization | +0.9% | North America, Western Europe, Asia Pacific | Long term (≥ 4 years) |

| Rising Demand for Cybersecure Motor Control Centers in Critical Infrastructure | +0.7% | North America, EU, Middle East | Medium term (2-4 years) |

| Modular Retrofit Solutions Targeting Aging Brownfield Plants | +1.1% | North America, Europe, India | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Proliferation of Industrial Automation and Industry 4.0 Initiatives

Factory-floor digitalization positions intelligent MCCs as edge nodes that aggregate real-time telemetry and publish OPC UA data streams directly to cloud historians, eliminating round-trip latency to remote SCADA servers. Siemens reported that by 2024, more than 3,200 plants had adopted TIA Portal-based MCC configurations, resulting in a 30% reduction in commissioning labor. ABB rolled out Edgenius retrofit modules that transform legacy low-voltage panels into smart assets, compatible with IEC 61131-3 programming, resulting in a 25–30% price reduction compared to full replacement.[1]ABB Ltd., “ABB Ability Edgenius Retrofit Modules,” abb.com Policy incentives amplify the trend: China’s Made in China 2025 program earmarked RMB 45 billion (USD 6.2 billion) for intelligent motor upgrades across state-owned petrochemical complexes. Modular, software-defined control now enables operators to quickly reconfigure production cells, a crucial advantage as product varieties and life cycles become increasingly shorter. Equipment suppliers respond by incorporating cybersecurity features into new product lines to help plants meet IEC 62443 audit requirements.

Energy Efficiency Regulations Driving Smart Motor Control Adoption

Regulators now price inefficiency, effectively taxing conventional starters in favor of VSD-based schemes. The EU Ecodesign Regulation 2019/1781 banned direct-on-line starters for most motors above 0.75 kW beginning July 2023, steering capital toward integrated MCCs with embedded metering. Schneider Electric monitored 1,800 European facilities in 2024 and achieved electricity savings of 12-18% after implementing intelligent MCC retrofits, reducing payback periods to under 24 months.[2]Schneider Electric, “EcoStruxure Power Monitoring Data 2024,” se.com In December 2024, the U.S. Department of Energy adopted tighter low-voltage motor rules that incentivize soft starters and VSDs. India’s Bureau of Energy Efficiency introduced a five-star scheme in March 2024 that bundles accelerated depreciation and goods and services tax relief for intelligent motor systems. These frameworks create a compliance floor that legacy panels struggle to meet, tilting lifecycle economics toward intelligent variants.

Superior Diagnostics and Predictive Maintenance Capability

Embedded condition monitoring converts MCCs into diagnostic hubs that detect bearing wear, insulation decay, and harmonic distortion, allowing for early detection of potential failures weeks before catastrophic failure. Rockwell Automation’s analytics stack captures 10 kHz current signatures to pinpoint rotor-bar cracks, helping automotive suppliers cut unplanned downtime by 35%.[3]Volkswagen AG, “Sustainability Report 2024,” volkswagenag.com Eaton’s Brightlayer suite combines vibration sensors with cloud models that predict faults 14 days ahead with 85% accuracy. In high-value sectors like oil and gas, where an hour of downtime can exceed USD 500,000, the incremental USD 15,000-25,000 cost of an intelligent MCC is trivial. Insurers reinforce adoption by offering 5-10% premium discounts to plants running certified predictive-maintenance programs anchored on intelligent MCCs.

Integration of Digital Twins for Virtual Commissioning and Lifecycle Optimization

Digital-twin technology enables engineers to simulate control logic and stress-test fault scenarios before installation. Siemens’ SIMIT environment cuts onsite startup time by up to 50% on greenfield lines. ABB’s System 800xA aligns physical MCCs with cloud models, enabling virtual testing of demand-response strategies, which resulted in a 7% annual reduction in energy costs for a European chemical plant. Digital twins maintain their value after commissioning by continually updating predictive models and maintenance schedules, thereby forming a closed feedback loop. Automotive OEMs utilize digital twins to recalculate motor loads for new battery chemistries without interrupting production, a practice highlighted in Volkswagen’s 2024 sustainability report.[4]Rockwell Automation Inc., “FactoryTalk Analytics Performance Study,” rockwellautomation.com Regulators now recognize virtual arc-flash studies, further easing compliance burdens for risk-averse sectors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Capital Expenditure and Hidden Installation Costs | -0.9% | Global, acute in price-sensitive SMEs | Short term (≤ 2 years) |

| Availability of Low-Cost Conventional Motor Control Alternatives | -0.6% | South Asia, Africa, Latin America | Medium term (2-4 years) |

| Cybersecurity Skill Shortage Hindering Connected MCC Deployments | -0.5% | Global, severe in developing markets | Medium term (2-4 years) |

| Fragmented Communication Standards Complicating Interoperability | -0.4% | Global, multi-vendor environments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Expenditure and Hidden Installation Costs

Even as component prices fall, intelligent MCCs still demand a 25-40% capital premium over conventional panels, and turnkey costs can double once network switches, firewalls, and software subscriptions are factored in. A typical 400 kW low-voltage smart panel costs USD 45,000-60,000, compared to USD 18,000-25,000 for a basic contactor-based unit, with an additional USD 15,000-20,000 required for Ethernet cabling and SCADA integration. Annual cloud analytics fees of USD 5,000-10,000 increase operating expenses, and mandatory cybersecurity audits can add USD 10,000-15,000 per site. Many SMEs, therefore, postpone upgrades, particularly in markets where labor is inexpensive and energy tariffs are low. Financing constraints also matter: smaller firms face higher borrowing costs and shorter payback thresholds, which favor incremental retrofits over full intelligent conversions.

Availability of Low-Cost Conventional Motor Control Alternatives

Low-cost producers in China, India, and Turkey retail conventional MCCs at up to 60% below Western-brand intelligent options. For stable loads, such as pumps and fans, the functional gap can appear narrow, encouraging budget-sensitive buyers to stick with legacy gear. Chinese vendors such as Chint Electric price a 400 kW panel at USD 8,000-12,000 and meet IEC 61439 standards, enabling quick procurement for municipal utilities and textile mills. This ample supply of affordable alternatives sustains a massive installed base that in turn supports a broad spare-parts ecosystem—making migration to intelligent platforms even less urgent for plants with minimal downtime penalties.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Operating Voltage: Medium-Voltage Variants Capture Electrification Upside

Medium-voltage intelligent solutions are projected to expand at a 8.96% CAGR through 2031, driven by electrification projects in mining haul-truck charging, large-scale pumping stations, and LNG liquefaction. Anglo American’s Quellaveco mine deployed 18 medium-voltage panels to manage conveyor and grinding motors, resulting in a 12% reduction in downtime in year one. Low-voltage units continue to dominate the intelligent motor control center market, retaining a 63.98% share in 2025, primarily due to their widespread use in discrete manufacturing and commercial buildings. High-voltage models above 11 kV remain a niche market, suited to applications such as pumped-storage and offshore platforms.

The medium-voltage segment also aligns with decarbonization: battery-electric haul trucks require 3-5 MW chargers, whose load spikes must be balanced in real-time. Intelligent MCCs orchestrate charging cycles without destabilizing site power systems, a capability BHP credited with enabling 24/7 electric-truck fleets. Low-voltage panels continue to post solid 6-7% growth, driven by modular retrofits and distributed manufacturing trends that favor compact footprints.

By Component: Variable Speed Drives Monetize Energy Arbitrage and Grid Services

VSDs are expected to log the fastest expansion at a 9.62% CAGR to 2031, as utilities roll out dynamic tariffs and demand-response programs. Schneider Electric’s Altivar Process drives let wastewater operators shift pumping to off-peak hours, saving up to USD 100,000 per plant annually. Busbars, although mature, held 24.05 of % intelligent motor control center market share in 2025 due to their universal presence in MCC construction.

Growth in communication gateways, power-quality filters, and power meters underscores the shift toward intelligence-enabling hardware. Soft starters gain traction where VSDs would be overengineered, offering 60-70% of the energy benefit at 40% of the cost, an attractive ratio for agricultural cooperatives and municipal water boards.

By Intelligence Level: Greenfield Projects and Regulatory Pressure Accelerate Intelligent Adoption

Intelligent variants are projected to grow at a 12.15% CAGR, thanks to embedded analytics in new plants and compliance mandates that conventional gear struggles to meet. An Eaton lifecycle study concluded that savings from downtime avoidance yielded positive NPV within 30-36 months in continuous-process sectors. The intelligent motor control center market share will therefore expand steadily as insurers reward predictive maintenance and regulators enforce higher motor system efficiency.

Conventional MCCs persist in low-criticality applications and budget-sensitive regions, yet their long-term relevance wanes as intelligent components become more commoditized and interoperability improves. Retrofit kits that preserve busbars and enclosures accelerate conversion by slashing shutdown windows, making upgrades palatable even in brownfield sites with tight maintenance schedules.

By End-user Industry: Food and Beverage Leads Growth on Traceability and Hygienic Mandates

Food and beverage facilities must comply with stringent hygienic-design and batch-traceability rules that favor stainless-steel enclosures and embedded diagnostics. Nestlé allocated USD 1.2 billion for factory automation in 2024, specifying IP69K-rated intelligent panels that can withstand high-pressure washdowns. Oil and gas remains the largest vertical, with a 24.76% share in 2025, due to motor-intensive refining and pipeline operations.

Water and wastewater follow closely as municipalities modernize their aging assets to reduce energy costs and support remote operations. Mining, chemicals, and power generation also rely on intelligent MCCs to integrate renewable sources and manage variable loads. The automotive, pulp and paper, and cement industries focus on modular retrofits to maintain uptime while transitioning toward predictive operations. Mission-critical sites such as data centers and airports are emerging pockets of demand driven by high interruption costs and cybersecurity mandates.

Geography Analysis

The Asia Pacific led the intelligent motor control centers (IMCC) market with 38.12% revenue share in 2025 and is projected to grow at an 8.21% CAGR through 2031. China’s State Grid committed RMB 520 billion (USD 72 billion) in 2024 to industrial power-distribution upgrades that include demand-responsive MCCs. India’s Production-Linked Incentive schemes are catalyzing the development of greenfield factories that specify intelligent panels from the outset, while local suppliers, such as Larsen & Toubro, deliver faster than their Western counterparts.

North America held a just under 30% share in 2025 and is expected to grow at a 6-7% CAGR as reshoring initiatives and the Inflation Reduction Act channel capital into automated lines. Updated DOE efficiency rules and CISA cybersecurity advisories reinforce the case for intelligent starters. Europe commands a 22-24% share in 2025 and grows more modestly at a 5-6% CAGR, but strict energy and cybersecurity directives keep retrofit activity stable. The Middle East and Africa together account for 8-10% of 2025 revenue. Petrochemical megaprojects in Saudi Arabia and the UAE are projected to drive a 7-8% CAGR for medium-voltage solutions. Africa’s 4-5% growth reflects limited capital access and preference for lower-cost conventional panels. South America, led by Brazil and Argentina, is expected to register a 6-7% CAGR in mining and lithium extraction projects, supported by local vendors such as WEG.

Competitive Landscape

The intelligent motor control centers (IMCC) market shows moderate concentration. ABB, Siemens, Schneider Electric, Eaton, and Rockwell Automation collectively controlled approximately 60% of the 2024 revenue. Their vertically integrated portfolios create switching costs that translate into recurring revenue from software and services. Differentiation now centers on edge analytics and cybersecurity certifications; for example, Schneider Electric’s EcoStruxure models predict failures 10-14 days in advance, supporting price premiums of 15-20%.

Regional specialists dilute global dominance by offering modular retrofit kits that mesh with incumbent DCS architectures at roughly half the replacement cost. Eaton’s NXR kit installs in under a week and preserves existing busbars, an attractive proposition for food processors that cannot afford extended shutdowns. Software-centric entrants like Augury threaten hardware margins by attaching cloud diagnostics to commodity contactors.

Standardization across OPC UA, IEC 61850, and TSN weakens proprietary protocols, allowing users to pursue multi-vendor ecosystems. As a result, profit pools migrate toward analytics subscriptions, lifecycle services, and cybersecurity consulting.

Intelligent Motor Control Centers (IMCC) Industry Leaders

General Electric Co.

ABB Limited

Schneider Electric SE

Eaton Corporation

Siemens AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Siemens commissioned a EUR 12 million (USD 13 million) intelligent MCC line in Amberg, Germany, featuring AI-driven quality inspection.

- December 2024: ABB landed a USD 45 million order for medium-voltage MCCs at Rio Tinto’s Oyu Tolgoi expansion in Mongolia.

- November 2024: Schneider Electric partnered with Microsoft to embed Azure IoT Edge in EcoStruxure panels for real-time analytics.

Global Intelligent Motor Control Centers (IMCC) Market Report Scope

The Intelligent Motor Control Centers (IMCC) Market is Segmented by Operating Voltage (Low, Medium, High), Component (Busbars, Circuit Breakers, Relays, VFDs, Soft Starters, Others), Intelligence Level (Intelligent, Conventional), End-user (Automotive, Chemicals, Food and Beverage, Mining, Pulp and Paper, Power, Oil and Gas, Water, Cement, Others), and Geography (North America, South America, Europe, Asia Pacific, Middle East, Africa). Market Forecasts are in Value (USD).

| Low-Voltage Intelligent MCCs |

| Medium-Voltage Intelligent MCCs |

| High-Voltage Intelligent MCCs |

| Busbars |

| Circuit Breakers and Fuses |

| Overload Relays |

| Variable Speed Drives |

| Soft Starters |

| Others |

| Intelligent MCCs |

| Conventional MCCs |

| Automotive |

| Chemicals and Petrochemicals |

| Food and Beverage |

| Mining and Metals |

| Pulp and Paper |

| Power Generation |

| Oil and Gas |

| Water and Wastewater |

| Cement Manufacturing |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Operating Voltage | Low-Voltage Intelligent MCCs | ||

| Medium-Voltage Intelligent MCCs | |||

| High-Voltage Intelligent MCCs | |||

| By Component | Busbars | ||

| Circuit Breakers and Fuses | |||

| Overload Relays | |||

| Variable Speed Drives | |||

| Soft Starters | |||

| Others | |||

| By Intelligence Level | Intelligent MCCs | ||

| Conventional MCCs | |||

| By End-user Industry | Automotive | ||

| Chemicals and Petrochemicals | |||

| Food and Beverage | |||

| Mining and Metals | |||

| Pulp and Paper | |||

| Power Generation | |||

| Oil and Gas | |||

| Water and Wastewater | |||

| Cement Manufacturing | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the intelligent motor control centers (IMCC) market in 2031?

The market is set to reach USD 9.25 billion by 2031.

Which region leads revenue and growth in intelligent MCC demand?

The Asia Pacific region accounted for 38.12% of 2025 revenue and is forecast to expand at an 8.21% CAGR through 2031.

Which component records the fastest growth inside intelligent MCCs?

Variable speed drives are projected to post the highest CAGR at 9.62% through 2031, driven by efficiency and demand-response benefits.

Which end-use sector shows the strongest growth momentum?

Food and beverage plants are projected to lead with a 9.07% CAGR through 2031.

Why are medium-voltage intelligent MCCs gaining traction?

The electrification of mining haul-truck charging and large water projects drives adoption, as these panels provide arc-flash mitigation and remote diagnostics.

How do insurers influence intelligent MCC adoption?

Many insurers offer 5-10% premium discounts for facilities that run certified predictive-maintenance programs anchored on intelligent MCCs.

Page last updated on: