Technology, Media and Telecom

5th MayPricing Strategy for Semiconductor Components

3 Min Read

The Separately Excited Motor Market Report is Segmented by Application (Paper Machines, Rolling Units, and More), Voltage (Low Voltage (Below 1 KV), Medium Voltage (1-6 KV), and High Voltage (Above 6 KV)), Power Rating (Below 100 KW, 100-500 KW, and More), End Use Industry (Automotive, Marine, and More), Mounting Type (Foot Mounted, Flange Mounted, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

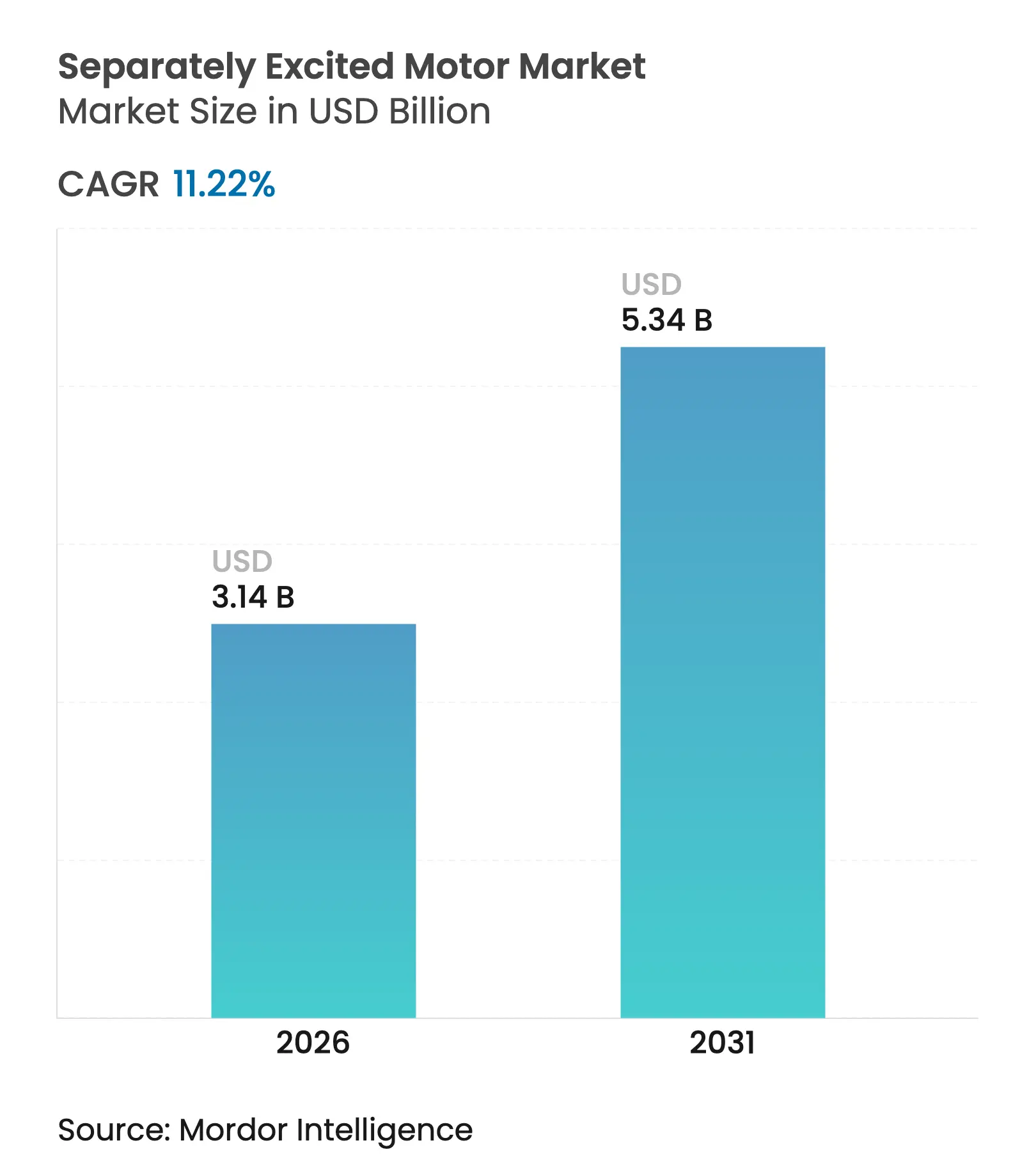

| Market Size (2026) | USD 3.14 Billion |

| Market Size (2031) | USD 5.34 Billion |

| Growth Rate (2026 - 2031) | 11.22 % CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

The separately excited motor market size is expected to grow from USD 2.82 billion in 2025 to USD 3.14 billion in 2026 and is forecast to reach USD 5.34 billion by 2031 at 11.22% CAGR over 2026-2031. Robust demand stems from traction, marine, and heavy-industry users that require wide speed ranges, high starting torque, and independence from rare-earth magnets. The growing electrification of vehicles and ships, along with tightening global efficiency rules and decarbonization programs, anchors long-term momentum for the separately excited motor market. Industrial automation, rising energy costs, and a shift toward total cost of ownership are propelling upgrades to IE4-class wound-field designs that can trim energy bills without sacrificing torque density. Competition centers on integrating proprietary excitation controls, expanding regional manufacturing footprints, and mitigating supply chain risks related to electrical steel, copper, and power electronics.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Growth in automotive vehicle sales Growth in automotive vehicle sales | +2.1% | Global - strong in Asia-Pacific and North America | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+2.1% | Geographic Relevance:Global - strong in Asia-Pacific and North America | Impact Timeline:Medium term (2-4 years) |

Rising demand for energy-efficient traction motors Rising demand for energy-efficient traction motors | +2.8% | EU and North America | Long term (≥ 4 years) | |||

Rapid automation in paper and pulp mills Rapid automation in paper and pulp mills | +1.7% | North America, Europe and select Asia-Pacific markets | Medium term (2-4 years) | |||

Electrification of inland waterways vessels Electrification of inland waterways vessels | +1.9% | Europe, China and North America | Long term (≥ 4 years) | |||

Increasing retro-fit activity in legacy rolling mills Increasing retro-fit activity in legacy rolling mills | +1.4% | Asia-Pacific core; spill-over to Middle East and Africa | Short term (≤ 2 years) | |||

Under-the-radar material handling boom in tier-2 ports Under-the-radar material handling boom in tier-2 ports | +1.6% | Asia-Pacific, Middle East and emerging port markets | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Demand for Energy-Efficient Traction Motors

Mandatory IE4 efficiency rules in the European Union and forthcoming U.S. Minimum Efficiency Performance Standards are expected to amplify the adoption of wound-field designs that allow for precise field weakening, thereby curbing losses at partial load.[1]ABB, “Ecodesign for Motors and Drives,” new.abb.com Wound-field architectures also sidestep rare-earth dependencies, helping OEMs de-risk magnet supply while staying within stringent efficiency classes defined by IEC 60034-30-3. Traction fleets, ranging from rail to forklifts, achieve lifecycle savings that can outweigh the higher upfront cost of the initial stage.

Growth in Automotive Vehicle Sales

Global electric vehicle sales reached 14.1 million units in 2024, accounting for 18% of all light-duty cars, and prompted automakers to shift toward magnet-free propulsion platforms.[2]International Energy Agency, “Global EV Outlook 2024,” IEA.org Separately excited motors are well-suited for shared skateboard architectures and offer wide, constant-power speed ranges, which are crucial for multi-segment vehicle lineups. Controller advances have narrowed complexity gaps with permanent-magnet peers, enabling cost-sensitive mass-volume programs.

Electrification of Inland Waterways Vessels

Hybrid-electric barges trialed under the EU-funded SYNERGETICS project utilize wound-field propulsion for high torque at low speeds and regenerative braking during lock operations.[3]SYNERGETICS Project Consortium, “Hybrid-Electric Inland Waterway Vessels,” synergetics-project.eu Regulatory pressure from the International Maritime Organization to cap CO₂ intensifies demand for electric propulsion, positioning the separately excited motor market as a beneficiary of fleet renewal.

Rapid Automation in Paper and Pulp Mills

Variable-speed paper machines require minimizing torque ripple and achieving fine speed resolution. Separately excited motors on DS Smith lines, delivered by ABB, demonstrate stable tension control across grade changes, boosting throughput while reducing scrap. As mills upgrade to premium packaging and tissue, automation packages rely on field-oriented control to sustain product quality.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Higher cost due to requirement of separate excitation source Higher cost due to requirement of separate excitation source | -1.8% | Global - acute in emerging markets | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-1.8% | Geographic Relevance:Global - acute in emerging markets | Impact Timeline:Short term (≤ 2 years) |

Availability of low-cost brushless DC alternatives Availability of low-cost brushless DC alternatives | -1.3% | Global - notably in consumer and light industry | Medium term (2-4 years) | |||

Supply chain disruptions in rare-earth magnet materials Supply chain disruptions in rare-earth magnet materials | -0.9% | Global - hybrid excitation projects | Short term (≤ 2 years) | |||

Limited technical expertise in emerging economies Limited technical expertise in emerging economies | -0.7% | Asia-Pacific, Middle East and Africa | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Higher Cost Due to Requirement of a Separate Excitation Source

Dedicated power supplies, regulators, and feedback circuits add 10-15% to the bill of materials versus self-excited or brushless designs. Price-sensitive buyers in Africa or Southeast Asia often favor simpler induction motors until energy savings offset the premium. OEM service networks that stock excitation parts and firmware updates can mitigate downtime fears, gradually softening this barrier.

Availability of Low-Cost Brushless DC Alternatives

Volume production of automotive permanent-magnet motors has driven down controller costs, undercutting wound-field propositions below 50 kW. Next-generation brushless drives now incorporate limited field weakening, eroding a key advantage of wound-field drives. Nonetheless, separately excited motors continue to dominate harsh or high-temperature sites where the risk of magnet demagnetization outweighs the price.

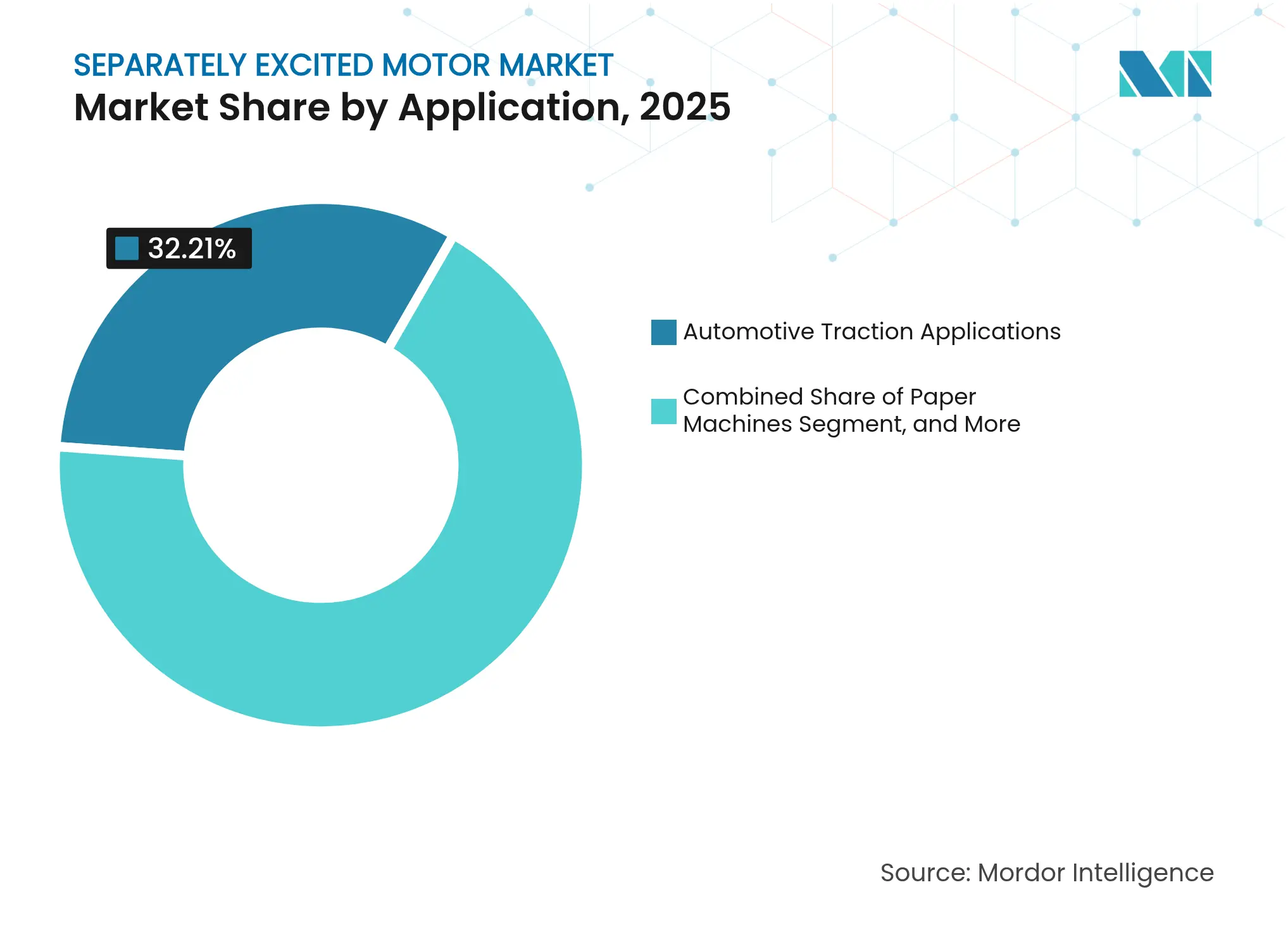

By Application: Automotive Traction Leads Amid Marine Surge

Automotive traction captured a 32.21% revenue share of the separately excited motor market in 2025, reflecting OEM strategies to hedge against fluctuations in magnet prices. Electric ship propulsion, driven by inland waterway retrofits, is forecast to grow at a 11.74% CAGR to 2031, contributing new volumes to the separately excited motor market size. Shipbuilders prefer wound-field machines for regenerative stopping and bidirectional power flow, while automotive platforms leverage the architecture’s tunable field for city-to-highway duty cycles. Rolling mills and paper machines maintain a stable share because tight speed control has a direct influence on product uniformity. Material handling cranes in Tier 2 ports emerge as a niche yet rapidly scaling opportunity as port authorities convert diesel yard equipment.

Paper, pulp, and mill OEMs integrate field-oriented controllers into their distributed control systems, creating a pull-through effect for separately excited motor industry suppliers. Marine installers value the machines’ intrinsic redundancy—if excitation fails, limp-home capability remains via residual magnetism. Automotive C-segment crossover programs in China select wound-field motors to meet cost targets without relying on dysprosium-heavy magnets, underscoring the architecture’s resilience to commodity volatility. Together, these trends sustain application diversity and insulate manufacturers from demand shocks in any single sector.

Note: Segment shares of all individual segments available upon report purchase

By Voltage: Low Voltage Dominates While High Voltage Accelerates

Low-voltage (<1 kV) offerings represented 44.67% of 2025 revenue, owing to standardized inverters and easy certification. However, the 6 kV+ tier is expected to compound at 12.21% from 2026 to 2031, adding significant upside to the separately excited motor market share. High-voltage units excel in desalination plants, pumped-storage hydroelectric facilities, and LNG carriers, where megawatt-scale drives minimize cable losses. IEC 60034-30-3 codified IE4 benchmarks up to 2 MW, giving wound-field suppliers a regulatory springboard. Medium-voltage (1-6 kV) remains essential for brownfield retrofits because existing switchgear often caps the scope of upgrades.

Utilities are increasingly deploying high-voltage wound-field motors in synchronous condenser mode to provide grid inertia as renewable energy penetration rises. In rolling mills, 3.3 kV retrofits improve power factor while retaining existing cabling, thereby maintaining medium-voltage demand. OEM catalog harmonization enables vendors to reuse stator frames across voltage classes, thereby lowering cost curves and encouraging buyers to upgrade to higher ratings. Consequently, the voltage mix is tilting toward larger machines without cannibalizing core low-voltage revenue streams.

By Power Rating: Mid-Range Motors Lead Growth Spectrum

Mid-range 100-500 kW units covered 39.31% of 2025 orders and form the nucleus of steel, paper, and pumping lines worldwide. Motors exceeding 500 kW are projected to grow at a 12.05% CAGR, driving a sizable share of the incremental separately excited motor market size as heavy-industry electrification gains momentum. Increasing conveyor payloads and gigawatt-scale hydrogen plants lift the top-end requirement curve. Sub-100 kW designs see flatter growth because brushless DC alternatives compete aggressively on installed cost.

Shipyards specify 750 kW class wound-field thrusters to achieve ice-class torque at low shaft speeds, reinforcing upside in the top power bracket. Mid-range adoption endures, however, because it aligns with common installed base spare parts. Vendors bundle predictive maintenance analytics to reduce downtime, tipping total cost assessments in favor of wound-field solutions across all power tiers.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

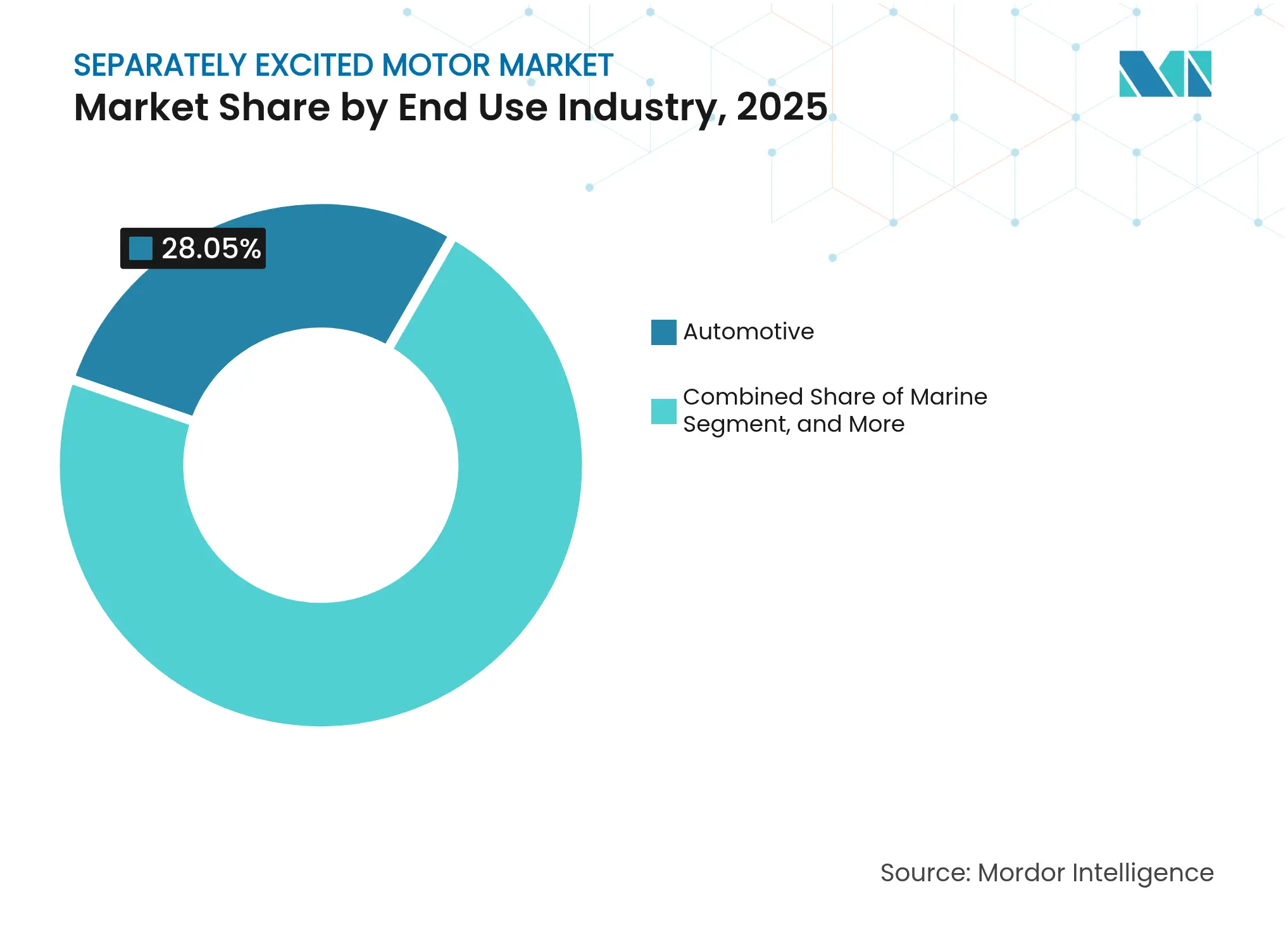

By End Use Industry: Automotive Leads While Marine Gains Momentum

Automotive retained 28.05% revenue share in 2025, but its dominance is narrowing as marine electrification accelerates at an 11.63% CAGR. Ports are ordering electric tugboats and inland barges to comply with Tier III rules, pulling through large frames and excitation packages from the separately excited motor industry. Metals and mining operations rely on high-torque starts for sequential rolling stands, which anchor steady demand in commodity cycles.

Paper and pulp mills retrofit aging DC lines with AC wound-field packages, unlocking energy savings and digital diagnostics. Power generation auxiliaries, such as boiler feed pumps and condensate systems, represent consistent but modest volumes that nonetheless require premium efficiency classifications. Suppliers that can serve both road and sea deliver portfolio synergies, hedging against cyclical slumps in either sector.

Note: Segment shares of all individual segments available upon report purchase

By Mounting Type: Foot-Mounted Configurations Dominate Installation Preferences

Foot-mounted assemblies generated 42.11% of 2025 revenues as legacy plant layouts favor horizontal skid arrangements. Vertical-mounted machines, however, will outpace the market at a 11.86% CAGR, driven by marine shafts, fire-main pumps, and compact process skids, thereby expanding the separately excited motor market. Flange-mounted options retain niche relevance for direct-drive rollers and paper winders, where coaxial alignment helps trim vibration.

Real estate costs and modular plant design encourage engineers to orient motors vertically, especially in retrofit basements with limited floor area. OEMs have refined sump-proof bearings and forced-oil lubrication to tackle deployment hurdles, widening the funnel for vertical sales. Foot-mounted frames remain indispensable for heavy bases that require precise torque anchoring, ensuring that incumbency and familiarity protect their leadership through the decade.

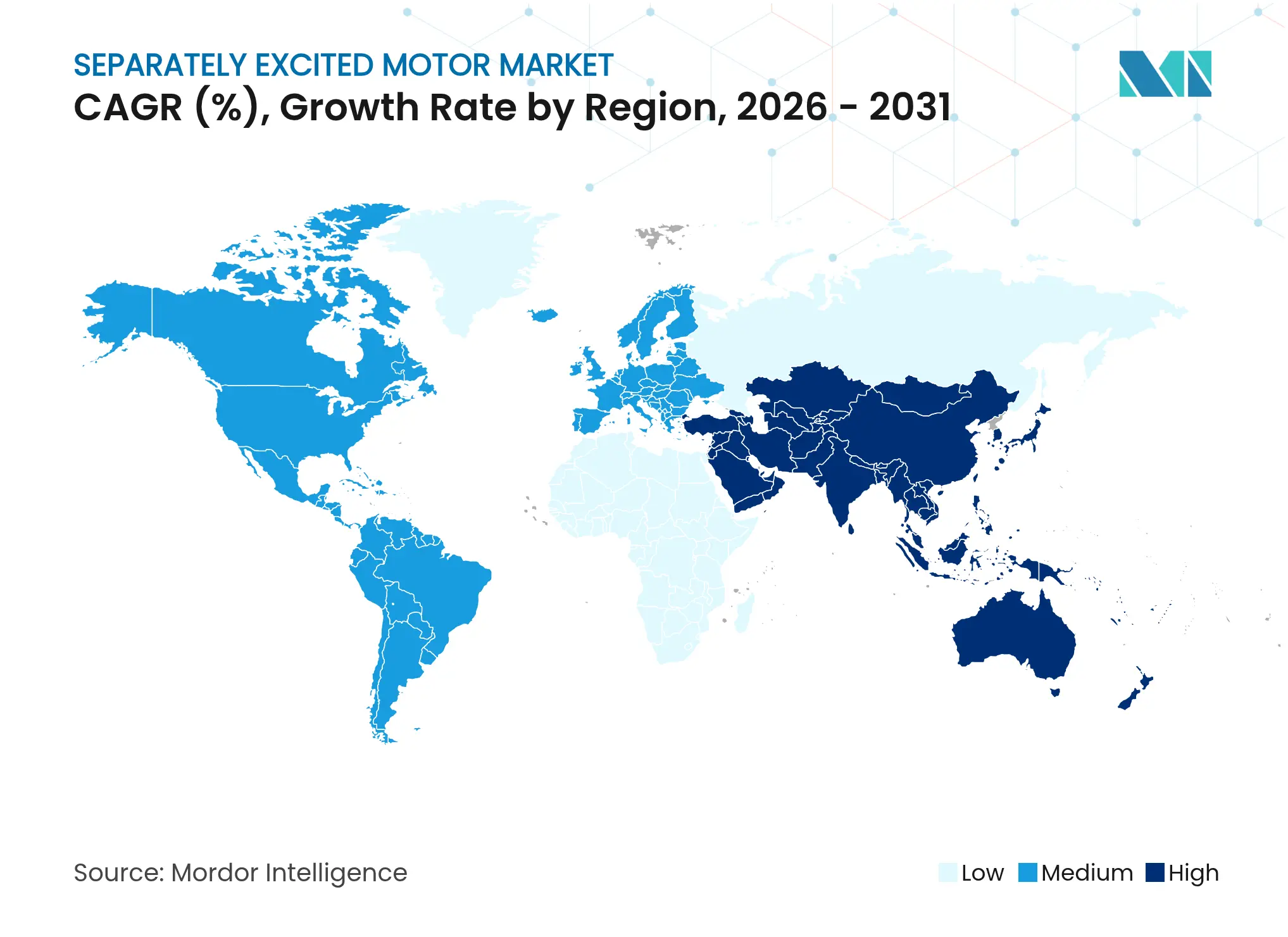

Asia-Pacific held 38.12% of global revenue in 2025, buoyed by China’s extensive manufacturing complex and India’s Production-Linked Incentive program that supports domestic equipment makers. Local champions like CG Power expanded capacity by INR 6.62 billion (USD 79 million) to serve both export and in-country electrification initiatives. Japan advances hybrid wound-field research, while Southeast Asian pulp and textile mills transition from DC to AC wound-field drives.

The Middle East is forecast to grow at a 11.58% CAGR through 2031, as Saudi Arabia’s Vision 2030 and the UAE’s port expansions demand megawatt-class drives for desalination, petrochemical compression, and automated cranes. WEG motors supplied to the Rabigh desalination complex demonstrate early adoption in harsh-salinity environments. Regional grid-modernization plans worth USD 109 billion indirectly stimulate demand for high-efficiency auxiliaries.

Europe and North America are expected to post steady growth, underpinned by IE4 mandates, reshoring incentives, and inland waterway decarbonization. German machine builders integrate wound-field packages into Industry 4.0 retrofits, whereas the U.S. cargo-handling electrification roadmap specifies variable-speed cranes that align with the characteristics of separately excited motors. South America maintains a small but strategic footprint tied to Brazilian shipyards and Chilean copper mines, ensuring globally diversified demand channels.

Market Concentration

The separately excited motor market is moderately fragmented, with the top five vendors accounting for roughly 45% of the revenue. ABB, Siemens, and WEG leverage multi-country manufacturing and service reach to win multi-site framework contracts. WEG’s USD 88 million purchase of Turkey-based Volt Electric Motors expanded access to European and Central Asian markets and added 1 million units of annual output.

Technology differentiation pivots on proprietary excitation algorithms and modular inverter packages that simplify commissioning. ABB released universal HV IE4 packages ahead of IEC deadlines, offering customers future-proof compliance. Siemens integrates predictive analytics into its Sinamics drive stack, aiming to reduce downtime in metals mills.

Regional challengers such as Wolong Electric and Kirloskar Electric emphasize cost-optimized frames for domestic EPC contractors. Nidec and Toshiba focus on specialized traction and pump markets, forming joint ventures with vehicle and process OEMs for co-developed solutions. Supply chain resilience-particularly in copper sourcing and IGBT availability-has emerged as a key tender criterion, with vendors building redundancy into their sub-supplier networks.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

A Separately Excited Motor is a type of DC motor to which the main supply is given separately to the armature and field windings. These motors include some field coils similar to that of shunt-wound type. Separately excited DC motors are often used as actuators in trains and automotive traction applications. The Global Separately Excited Motor Market is segmented By Applications (Paper Machines, Rolling Units, Electric Propulsion of Ships, Automotive Traction Application) and Geography.

Pricing Strategy for Semiconductor Components

3 Min Read

Accelerating Additive Manufacturing Adoption in India

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.