Terahertz Technologies Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

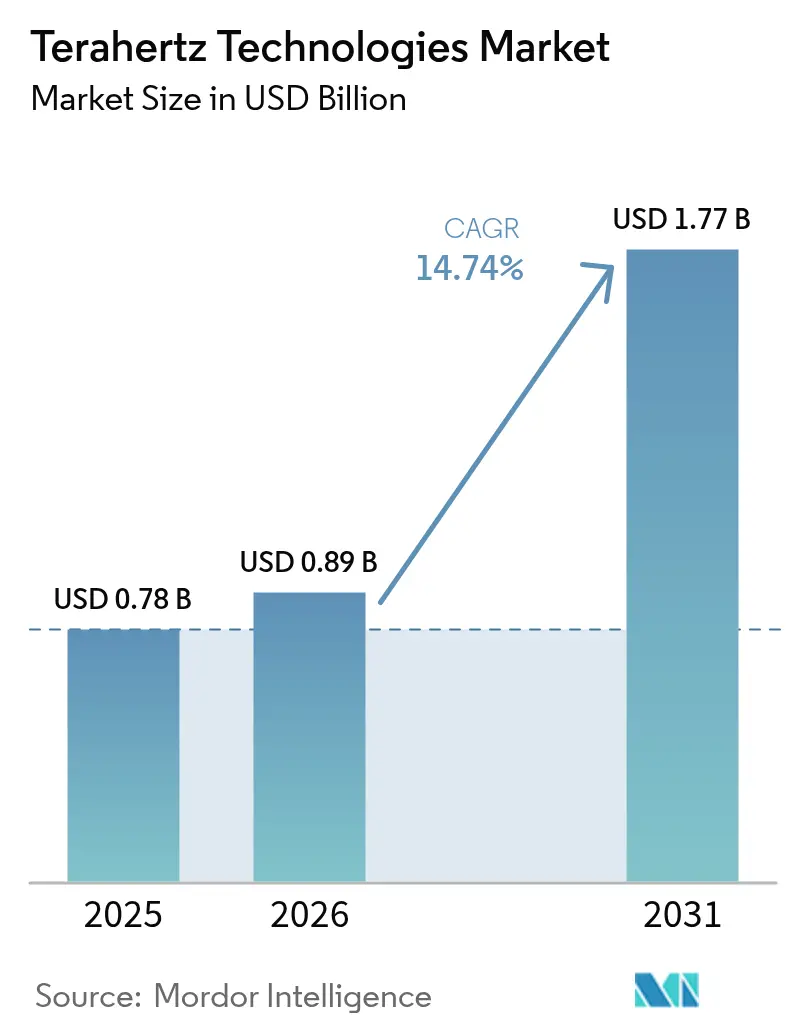

| Market Size (2026) | USD 0.89 Billion |

| Market Size (2031) | USD 1.77 Billion |

| Growth Rate (2026 - 2031) | 14.74% CAGR |

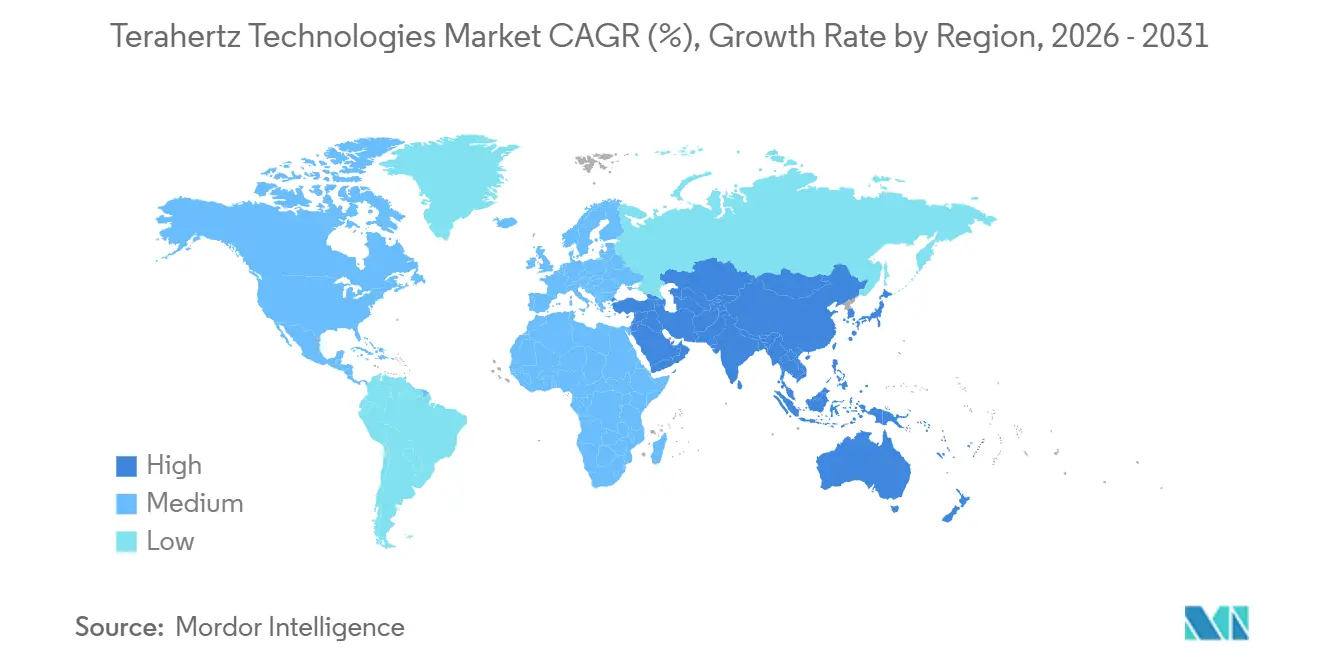

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Terahertz Technologies Market Analysis by Mordor Intelligence

The terahertz technologies market size was valued at USD 0.78 billion in 2025 and estimated to grow from USD 0.89 billion in 2026 to reach USD 1.77 billion by 2031, at a CAGR of 14.74% during the forecast period (2026-2031). Strong momentum behind photonic-integrated sources, expanding 6G proof-of-concept backhaul links, and rising healthcare adoption are moving the terahertz technologies market from research labs into high-volume production lines. Component manufacturers have shifted investment toward chip-level assemblies that lower system cost and simplify field deployment, while end users prioritize turnkey platforms that bundle machine-learning analytics with quantum-cascade lasers or photomixing modules. Regulatory support for process analytical technology in pharmaceuticals and aggressive public funding for 6G research consortia further reinforce demand. Competition now centers on reducing cryogenic-cooling overhead, securing design slots in inline quality-control installations, and achieving long-term reliability targets that match those of incumbent optical and microwave solutions.

Key Report Takeaways

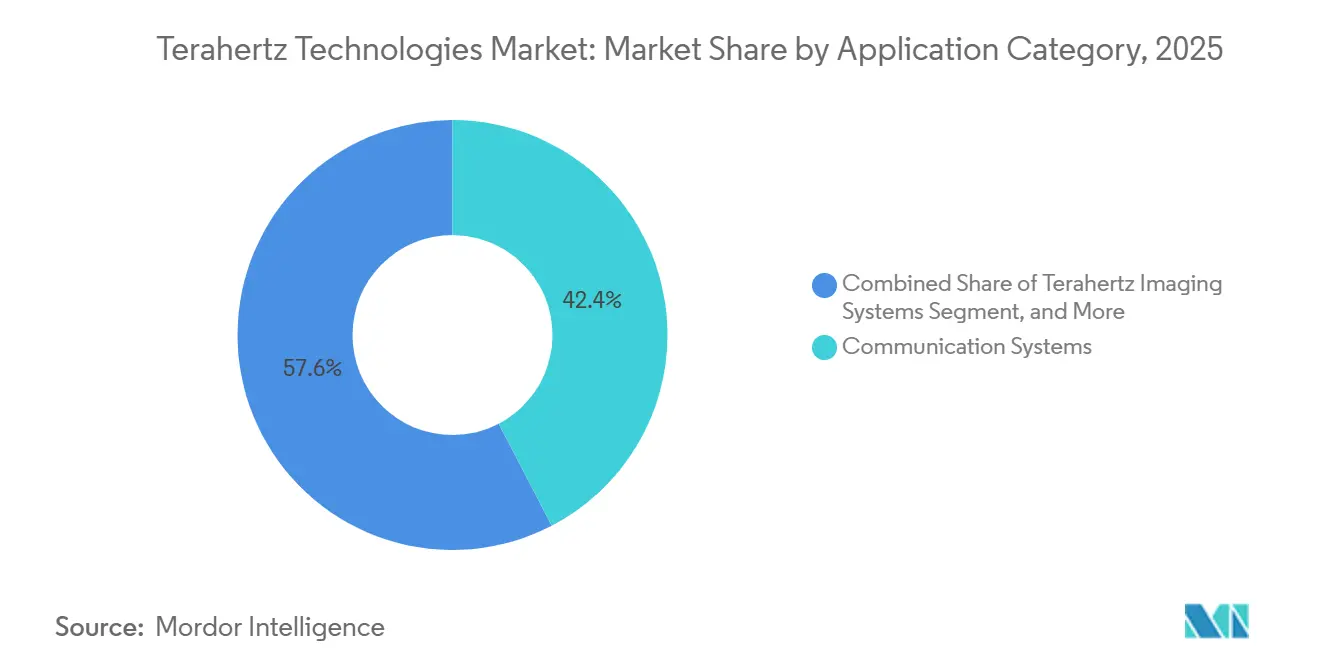

- By application category, communication systems led with 42.36% of the terahertz technologies market share in 2025, whereas terahertz imaging systems are forecast to advance at a 15.32% CAGR through 2031.

- By frequency range, mid-frequency platforms held 47.93% terahertz technologies market share in 2025 and are projected to grow at a 15.37% CAGR between 2026-2031.

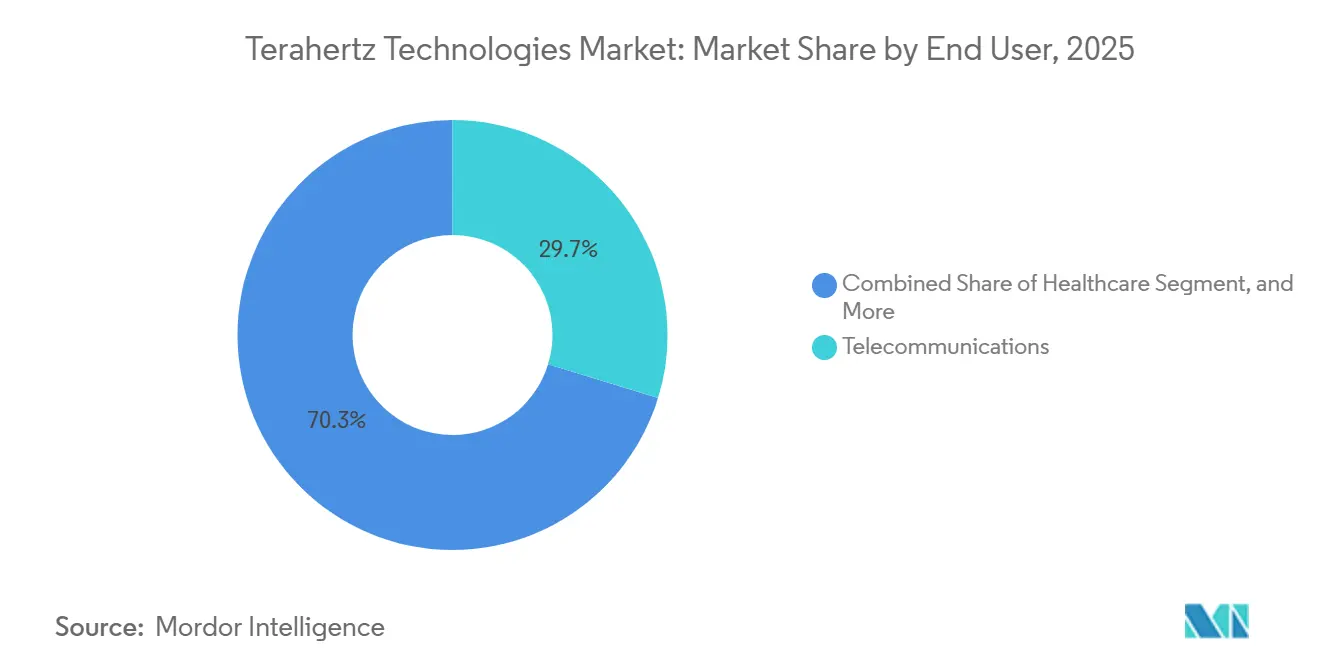

- By end user, telecommunications accounted for 29.74% of 2025 revenue, while healthcare applications are poised to expand at a 16.11% CAGR through 2031.

- By component type, terahertz sources accounted for 34.59% of spending in 2025; systems and software are expected to post a 15.56% CAGR during 2026-2031.

- By geography, Asia-Pacific accounted for 38.23% of 2025 revenue and is set to grow at a 15.79% CAGR, outpacing all other regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Terahertz Technologies Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advances in Compact Photonic-Integrated THz Sources | +3.2% | Global, with early commercialization in North America and Asia-Pacific | Medium term (2-4 years) |

| Surge in 6G-Backhaul Proof-of-Concept Installations | +2.9% | Asia-Pacific core, spill-over to North America and Europe | Short term (≤ 2 years) |

| Rising Adoption in Inline Pharmaceutical QA/QC | +2.4% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Defense Demand for mm-Resolution Passive Standoff Scanners | +1.8% | North America and Middle East, selective adoption in Europe | Long term (≥ 4 years) |

| Standardization of THz EUV Lithography Mask Metrology | +1.3% | Asia-Pacific (Taiwan, South Korea), North America (United States) | Long term (≥ 4 years) |

| Funding for THz Cultural Heritage Preservation Analysis | +0.6% | Europe, selective projects in North America and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Advances in Compact Photonic-Integrated THz Sources

Photonic integration is shrinking terahertz emitters from bench-top optical assemblies to millimeter-scale chips that drop directly into handheld instruments. Thin-film lithium niobate modulators now achieve difference-frequency mixing efficiencies approaching 1%, providing continuous-wave output above 1 THz without cryogenic mirrors or bulky alignment hardware.[1]Alan Wong, “Lithium-Niobate Photonic THz Generation,” Optica Publishing Group, opg.optica.org Commercial foundries have licensed more than 40 university patents since 2024, bringing the technology to 200 mm silicon photonics lines that cut part counts and lead times by more than half. Unit cost is falling below USD 10,000 for mid-power sources, opening up price-sensitive segments such as food inspection and cultural heritage conservation. The combination of a lower price and a field-ready form factor underpins the projected 15.32% growth in imaging systems through 2031.

Surge in 6G-Backhaul Proof-of-Concept Installations

Telecom operators completed over 25 terahertz backhaul pilots in dense urban corridors during 2025, targeting multi-gigabit links where trenching fiber exceeds USD 1 million per kilometer. Japan’s NICT validated a 100 Gbps, 300 GHz connection over 500 m in downtown Tokyo, meeting 6G latency and packet-error requirements under real traffic conditions.[2]Kenji Yamamoto, “100 Gbps 300 GHz Field Trial in Tokyo,” National Institute of Information and Communications Technology, nict.go.jp South Korea’s ETRI achieved 50 Gbps at 220 GHz with adaptive beam steering that compensated for building sway and pedestrian blockage, demonstrating robustness for small-cell aggregation. Capital budgets for 2026 now include terahertz radios alongside microwave and optical backhaul gear, confirming the segment’s transition from research to deployment. These pilots explain why communication systems retained 42.36% market share in 2025.

Rising Adoption in Inline Pharmaceutical QA/QC

Continuous-manufacturing tablet lines in North America and Europe embedded terahertz time-domain spectroscopy to monitor coating thickness and polymorphic form in real time, replacing destructive offline sampling.[3]United States Food and Drug Administration, “PAT Guidance for Industry,” fda.gov Each inline sensor inspects up to 200,000 tablets per hour and flags deviations that correlate with dissolution-rate failures, a capability near-infrared tools lack due to limited penetration depth. The technology aligns with regulatory initiatives to enable real-time release testing, reducing batch-hold inventory and shortening production cycles. Falling hardware prices driven by photonic integration allow plants to equip multiple lines rather than a single pilot system. These factors support the forecast 16.11% CAGR for healthcare applications through 2031.

Defense Demand for mm-Resolution Passive Standoff Scanners

Defense and security agencies are procuring passive terahertz imagers that capture millimeter-scale detail at standoff ranges of 10 m or more, enabling non-invasive detection of concealed threats. The United States TSA evaluated next-generation portals that improve spatial resolution and reduce false-alarm rates compared with legacy millimeter-wave units. Middle Eastern ministries signed contracts totaling more than USD 50 million in 2025 for vehicle-mounted passive scanners for high-risk checkpoints where proximity screening is unsafe. Passive architectures avoid export-control restrictions tied to high-power active transmitters, streamlining cross-border sales. Although defense spending grows more slowly than healthcare or telecom, these high-value systems anchor a stable revenue base for suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Atmospheric Transmission Windows for Outdoor Links | -1.4% | Global, acute in humid tropical and subtropical regions | Short term (≤ 2 years) |

| Cryogenic Cooling Cost for High-Power QCL Sources | -1.1% | Global, particularly North America and Europe where labor and energy costs are elevated | Medium term (2-4 years) |

| Scarcity of Volume-Manufacturable Low-Loss THz Packaging | -0.8% | Global, with acute supply constraints in Asia-Pacific and North America | Medium term (2-4 years) |

| Absence of Harmonised Global EMC and Health Exposure Limits Above 275 GHz | -0.6% | Global, fragmented regulatory landscape across North America, Europe, and Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Atmospheric Transmission Windows for Outdoor Links

Water vapor creates attenuation peaks above 100 dB km⁻¹ at many terahertz frequencies, restricting reliable outdoor service to narrow windows near 300 GHz and 350 GHz. Humid tropical climates experience two-to-three times higher losses, forcing operators to oversize link budgets or confine deployments to dry seasons. Rainfall above 10 mm h⁻¹ can drop link availability below carrier standards, pushing networks to retain microwave or fiber overlays for resiliency. These environmental limits cap the long-term share of terahertz in backhaul architectures despite technical successes in pilot trials. Investment, therefore, shifts toward indoor, short-range, or point-to-point campus links where atmospheric effects are minimal.

Cryogenic Cooling Cost for High-Power QCL Sources

Quantum-cascade lasers that deliver multi-milliwatt terahertz output require cooling below 200 K, adding USD 15,000–50,000 in cryocooler hardware plus 200–500 W continuous power draw. Five-year ownership can exceed USD 100,000 once maintenance and energy are included, a barrier for cost-sensitive industries such as food processing. Labor rates above USD 100 h⁻¹ in North America and Europe further inflate service costs, creating regional adoption gaps. Vendors are racing to commercialize room-temperature photomixing sources that trade output power for lower complexity. Until those alternatives mature, cryogenic overhead will limit terahertz penetration in mass-market inspection lines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application Category: Imaging Systems Gain Momentum

Terahertz imaging systems are projected to grow at a 15.32% CAGR between 2026-2031, closing in on communication platforms that commanded 42.36% of the terahertz technologies market share in 2025. The terahertz technologies market for imaging will benefit from falling hardware prices as photonic-integrated sources reach sub-USD 10,000 unit costs and enable routine non-destructive testing on pharmaceutical lines and composite-material parts. Active imagers that couple quantum-cascade lasers with fast detectors dominate tablet-coating inspection and aerospace defect mapping, while passive arrays lead airport screening by avoiding export-control limits on high-power emitters.

The expanding use cases in dermatology clinics, dental practices, and cultural-heritage conservation are driving demand beyond research labs. Hybrid instruments that overlay spectral fingerprints on high-contrast images allow a single platform to shift between quality control, security, and medical diagnostics through software updates rather than hardware swaps. As these multipurpose systems mature, integrators bundle AI analytics that reduce operator training time and standardize results across sites. Together, these factors underpin sustained double-digit growth for imaging despite communication remaining the largest revenue generator through mid-decade.

By Frequency Range: Mid-Band Platforms Dominate

Mid-frequency solutions spanning roughly 0.5-1.5 THz held 47.93% of 2025 revenue, the largest slice of the terahertz technologies market share, and are expected to expand at a 15.37% CAGR to 2031. In this band of the terahertz technologies market, 1 THz spectroscopy can effectively resolve 5 µm coating layers, providing high precision in material analysis. At the same time, atmospheric attenuation and component costs remain manageable for field systems, making it an optimal range for practical applications in various industries, including healthcare, security, and telecommunications.

Low-frequency gear below 0.5 THz propagates farther and operates at room temperature, making it well-suited for point-to-point links and through-wall sensing, but millimeter-scale resolution limits its appeal for precision QA. Above 1.5 THz, sub-millimeter imaging is used for EUV mask metrology, although stronger water-vapor absorption and higher detector noise keep such units largely laboratory-bound. Mid-band designs, therefore, remain the default for pharmaceutical, telecom, and security users that need balanced performance without cryogenic overhead or severe weather constraints.

By End User: Healthcare Surges Ahead

Telecommunications accounted for 29.74% of terahertz revenue in 2025, yet healthcare applications are forecast to grow at a 16.11% CAGR through 2031, the fastest among end users. Dermatology practices adopted handheld scanners that delineate carcinoma margins in real time, reducing re-excision rates and justifying capital costs near USD 200,000 per unit. Pharmaceutical manufacturers, encouraged by real-time release regulations, embedded inline spectroscopy across multiple coating lines, each screening up to 200,000 tablets per hour.

Dental, ophthalmic, and point-of-care settings follow, drawn using radiation-free imaging that aligns with pediatric and outpatient workflows. Defense and security procure passive standoff arrays for concealed-weapon detection, though lengthy procurement cycles temper growth. The industrial and food sectors are exploring moisture sensing and composite inspection, but remain sensitive to system prices above USD 50,000. As vendors roll out photonic-integrated sources and AI analytics that shrink the total cost of ownership, healthcare’s share is set to narrow the gap with telecom by the end of the forecast window.

By Component Type: Systems and Software Capture Value

Terahertz sources represented 34.59% of 2025 spending, led by high-price quantum-cascade lasers, yet systems and software are on track for a 15.56% CAGR, the fastest within the stack. As emitter costs decline and detectors become commoditized, the focus of value creation is shifting towards comprehensive turnkey platforms. These platforms seamlessly integrate hardware, analytics, and data management that is ready for regulatory compliance.

Integrators now embed convolutional neural networks trained on thousands of spectra or images, automating pass-fail calls and trimming operator training from weeks to hours. Compliance features such as 21 CFR Part 11 electronic records support pharmaceutical buyers, while SNMP interfaces let telecom operators integrate terahertz radios into existing network management suites. Passive optics remain a stable but slower-growing slice, with innovation centering on 3D-printed lenses and metamaterial flats that ease handheld design. As a result, the terahertz technologies market size tied to software subscriptions and algorithm updates will climb steadily, even as component ASPs decline.

Geography Analysis

Asia-Pacific captured 38.23% of global revenue in 2025, the highest regional share, and is projected to expand at a 15.79% CAGR through 2031. China’s Ministry of Science and Technology allocated CNY 2.1 billion (USD 290 million) in 2025 to 6G terahertz consortia that develop indigenous sources and detectors. Japan’s National Institute of Information and Communications Technology demonstrated a 100 Gbps, 300 GHz link across 500 m of central Tokyo in late 2025, validating sub-terahertz reliability under dense urban conditions. South Korea’s ETRI field-tested a portable 220 GHz transceiver that delivered 50 Gbps on Seoul streets in mid-2025, further cementing regional leadership in pilot deployments. Together, these initiatives position the region to dictate future component cost curves and performance benchmarks.

North America ranked second in revenue, buoyed by DARPA grants for passive standoff scanners and widespread pharmaceutical rollout of inline spectroscopy. The terahertz technologies market in North America is forecast to grow steadily, though the region’s CAGR trails Asia-Pacific as telecom operators pursue measured 6G backhaul expansion. Europe’s contribution remains significant thanks to research hubs such as Fraunhofer IAF, which advanced thin-film lithium-niobate photomixers that enable room-temperature sources. Fragmented spectrum policy and more conservative capital expenditure, however, slow cross-border deployments. As a result, Europe is expected to yield incremental share to faster-moving Asian markets through the forecast window.

South America stands at an evaluation stage, with Brazil’s agricultural agencies testing terahertz moisture sensors for coffee and soybean quality control. Mexico’s automotive sector pilots non-destructive testing of composite panels, yet import duties and limited local manufacturing constrain volume adoption. In the Middle East and Africa, airport security screening and border-control orders generate periodic but high-value sales, while the absence of an indigenous component supply curbs scale. Collectively, these emerging regions hold less than 10% of the terahertz technologies market share today and are expected to remain single-digit contributors until falling Asia-Pacific price points broaden accessibility.

Regulatory Landscape

Terahertz commercialization is shaped by uneven spectrum allocations and evolving compliance guidance above 95 GHz. Under ITU-R Radio Regulations, global allocations are well defined up to 275 GHz, while study and compatibility work extends into higher sub-THz/THz ranges. This includes agenda-driven analyses heading toward WRC-27 under ITU-R Resolution 663 for radiolocation and related coexistence topics across 231.5-275 GHz and 275-700 GHz bands, which creates different time-to-market profiles for communication systems near 300 GHz versus higher-frequency imaging and metrology platforms that often operate under less harmonized rules.

In the United States, the FCCs December 2025 KDB 800303 D01 guidance for emission measurements above 95 GHz helps standardize test approaches for EHF equipment and reduces uncertainty during device certification as more sub-THz radios and instruments move beyond lab demonstrations. On the standards side, IEEE Std 802.15.3-2023 supports 300 GHz physical and MAC layer operation for high data rate links, while ETSI workstreams relevant to automated networks (including ZSM architecture publications such as ETSI GR ZSM 021 V1.1.1 released in May 2026) and harmonized equipment standards in adjacent ultra short range bands (ETSI EN 305 550-5 for 57-260 GHz) provide reference points for interoperability and deployment models around edge terahertz use cases.

Value Chain Analysis

The terahertz technologies value chain starts with specialty materials and device fabrication, spanning III-V semiconductors and photonics processes used for sources (including quantum-cascade lasers, photomixers, and photodiodes) as well as for sensitive detectors. It then moves into packaging, module assembly, and system integration. A key upstream-to-midstream dependency is heterogeneous integration and thermal management, where material bonding and low-loss packaging determine achievable output power, stability, and cost at scale. In June 2025, OKI and NTT Innovative Devices Corporation reported progress toward mass production technology for high-power terahertz devices using crystal film bonding of InP photodiodes onto SiC substrates, illustrating how substrate selection, bonding yield, and InP area efficiency affect manufacturability.

Downstream, value concentrates in turnkey systems and software, where vendors combine terahertz hardware with analytics, compliance-ready data handling, and automation interfaces for telecom, pharmaceutical QA/QC, and security workflows. Distribution commonly runs through direct enterprise sales and specialized integrators that tailor inline inspection cells, imaging portals, or backhaul radio enclosures, with calibration, maintenance, and application support as recurring revenue drivers. Bottlenecks remain concentrated in volume-manufacturable low-loss packaging, production test and metrology for sub-THz/THz modules, and precision passive components, including advanced optics where additive manufacturing trade-offs can limit surface finish and material choice, which collectively influence lead times and system pricing.

Competitive Landscape

The terahertz technologies market is moderately fragmented, with the five largest suppliers controlling roughly 60% of worldwide revenue. Established spectroscopy leaders such as Bruker Corporation and Menlo Systems rely on decades of materials analysis expertise to maintain premium positioning. Photonics startups licensing university patents introduce thin-film lithium-niobate emitters that operate without cryogenic cooling, targeting cost-sensitive industrial buyers. Defense integrators, including Northrop Grumman and Lockheed Martin, repurpose millimeter-wave radar experience to develop passive scanners for threat detection. Competition, therefore, spans optical, radiofrequency, and security domains rather than a single technology silo.

Mergers, acquisitions, and partnerships accelerated in 2025 as firms sought vertical integration. Bruker purchased a German Schottky-diode foundry, cutting detector lead times by 30% and safeguarding margins in high-volume pharmaceutical deals. Menlo Systems signed a joint development pact with a major telecom OEM to embed 300 GHz radios into weather-sealed base-station enclosures. TOPTICA Photonics launched a photonic-integrated source module priced below USD 10,000, pressuring rivals dependent on more expensive quantum-cascade lasers. Virginia Diodes secured a USD 18 million DARPA contract to advance passive scanners, leveraging non-dilutive funding to move prototypes toward production.

Patent filings for photonic-integrated emitters climbed more than 30% during 2024-2025, shortening innovation cycles and eroding proprietary advantage. Software is emerging as the key differentiator, with suppliers bundling machine-learning classifiers that reduce false positives and trim operator training from weeks to hours. As detector and source prices fall, recurring revenue shifts toward firmware updates and cloud analytics tied to multi-year service contracts. Vendors capable of delivering turnkey, compliance-ready solutions are positioned to capture greater wallet share as buyers consolidate around fewer full-stack partners.

Terahertz Technologies Industry Leaders

ADVANTEST Corporation

Luna Innovations Incorporated

TeraView Limited

TOPTICA Photonics AG

HÜBNER GmbH and Co. KG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term whitespace is emerging where terahertz hardware, automation software, and standards activity overlap, particularly around sub-THz/THz communications architectures and integrated sensing-and-communications (ISAC) concepts. ETSI ISG THz provides a structured forum for industrial and academic entities to align channel models, candidate bands, and system assumptions, while the ITU-R 6G standardization timeline, with requirements and evaluation criteria defined during 2024-2027 and technology specification activities starting in 2027, creates an organizing window for suppliers to harden modules, packaging, and orchestration features that telecom buyers can validate in pilots.

Publicly funded R&D programs are also generating a pipeline of application prototypes that can translate into procurement-led deployments in later phases. EU-backed initiatives such as TERRAMETA (reconfigurable intelligent surfaces for THz wireless) and 6G-TERAFIT (THz wave bands for heterogeneous wireless networks, supported under Marie Sklodowska-Curie Actions) point to continued work on hardware development, propagation-aware optimization, and test methodologies that narrow the gap between lab demonstrators and field-ready nodes. For suppliers, the opportunity is focused on compact, room-temperature source modules, robust packaging qualified for outdoor and industrial environments, and software layers that fuse sensing outputs with link management, reflecting buyer preference for deployable platforms rather than standalone components.

Recent Industry Developments

- June 2026: Advantest announced a partnership with OpenLight to develop silicon photonics test solutions aimed at high-volume manufacturing. The collaboration targets scalable validation and characterization workflows for photonic devices that increasingly sit alongside sub-THz/THz signal paths in advanced communications and compute hardware. Strengthening automated test capability supports higher throughput and tighter tolerances, which are prerequisites for broader deployment of terahertz-enabled modules.

- December 2025: Japans National Institute of Information and Communications Technology (NICT) reported a 100 Gbps, 300 GHz wireless link over 500 m in central Tokyo. The field result showed sub-terahertz performance under dense urban conditions, shifting the discussion from controlled labs toward operational link engineering. It also reinforced vendor focus on weather-aware design, beam management, and integration into telecom backhaul planning.

- October 2024: IEEE maintained momentum around terahertz connectivity through the evolution of high-frequency wireless standards, with IEEE Std 802.15.3-2023 providing a reference for 300 GHz PHY and MAC operation for fixed and portable devices. This standards baseline helps developers align device behavior, interoperability assumptions, and test plans as prototypes transition into productized radios. A clearer technical framework supports earlier engagement with regulators and certification labs for sub-THz equipment.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the terahertz technologies market is defined as revenues generated from terahertz sources, detectors, related optics or passive components, and integrated systems used to generate, detect, or analyze terahertz radiation for imaging, spectroscopy, and communications across end users.

Scope exclusions: We exclude non-terahertz imaging or sensing platforms and general RF or microwave equipment that does not operate as a terahertz technology offering.

Segmentation Overview

- By Application Category

- Terahertz Imaging Systems

- Active Systems

- Passive Systems

- Terahertz Spectroscopy Systems

- Time-Domain

- Frequency-Domain

- Communication Systems

- Terahertz Imaging Systems

- By Frequency Range

- Low-Frequency Terahertz

- Mid-Frequency Terahertz

- High-Frequency Terahertz

- By End User

- Healthcare

- Defense and Security

- Telecommunications

- Industrial

- Food and Agriculture

- Laboratories

- Other End Users

- By Component Type

- Terahertz Sources

- Terahertz Detectors

- Optics and Passive Components

- Systems and Softwares

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Italy

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the outer boundaries of the model and to keep unit assumptions realistic before we spoke to industry participants. We reviewed public research and statistics such as ITU material on spectrum and telecom evolution, NIST references on measurement science, and IEEE and Optica (OSA) publications that track photonics and device progress.

We also used sources such as the USPTO patent database, US FDA public device databases where applicable to screening and imaging uses, and defense and security procurement notices for directional demand signals. Annual reports, investor presentations, and press releases helped us understand product readiness, shipment timing, and pricing movement, while a paid subscription for company financials and a patent dataset helped us speed up cross-checks. These desk sources are illustrative, and we also used additional public references to collect inputs, validate assumptions, and clarify gaps.

Primary Interviews and Surveys

Primary work focused on validating what actually gets purchased in the terahertz stack, and when it gets booked as revenue, which is where desk sources can be thin. We spoke with a mix of component suppliers, system makers, labs and integrators, and end-user buyers across APAC, EMEA, and the Americas to pressure-test adoption timelines, typical pricing behavior, and where pilots are turning into repeat orders.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 16% | APAC: 48% |

| Mid tier: 51% | Functional/Unit leaders: 25% | EMEA: 30% |

| Smaller Players: 17% | Managers: 59% | Americas: 22% |

Market-Sizing & Forecasting

Sizing started with a top-down approach where addressable spending was reconstructed from end-use demand pools for imaging, spectroscopy, and communications use cases, then split by component and system value captured in terahertz solutions. To keep the totals grounded, we corroborated them through selective bottom-up approximations such as sampled supplier revenue splits, channel checks, and an ASP times volume sanity check for key system categories.

Inputs were built around practical variables that can be checked year to year, including R&D and procurement cycles in defense and labs, pilot to production conversion rates in industrial inspection, device cost-down trends from chip-level assemblies, and the pace of 6G backhaul proof-of-concept activity that influences communications demand. Forecasting relied mainly on scenario analysis, where adoption speeds and price erosion were adjusted based on interview consensus, then smoothed to avoid one-time spikes from project-based orders. When bottom-up signals were missing for smaller niches, we filled gaps using proxy shares from similar end-use patterns and then revisited them during expert follow-ups.

Data Validation & Update Cycle

Model outputs were checked against independent signals, such as patent intensity shifts, public program funding direction, and reported product launch cadence, and then compared across regions to catch unrealistic step changes. If variances looked too wide, we reopened assumptions and triggered a second round of expert confirmation, especially for pricing curves and adoption timing.

Before sign-off, the file goes through multi-step analyst reviews where formulas, unit logic, and currency handling are checked again, followed by a last pass for any material news that may change near-term demand. Reports are refreshed annually, and interim updates are made when major events occur that can alter forecast paths.

Mordor Intelligence's Terahertz Technologies Market Size Compared With Other Published Estimates

Published terahertz market numbers can look far apart because each source draws the market boundary differently, and each one also selects its own year and pricing logic. The table makes the spread easy to see, and it also highlights how scope choices, currency timing, and whether pilots are treated versus scaled deployments can move the total.

The table shows a tighter 2025 value versus some larger figures, and in Mordor Intelligence's model the market is counted around terahertz specific components and systems used for imaging, spectroscopy, and communications, rather than folding in broad adjacent RF, sensing, or downstream service revenues. When a source uses factory-gate only rules or stretches the definition into wider electronics categories, the reported market size can shift even if the underlying adoption story is similar.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.78 B (2025) | |

| Global Publisher A | USD 0.84 B (2025) | Uses a factory-gate framing and bundles several service and related goods descriptions, which can change what is counted as market revenue compared to a components-plus-systems focus. |

| Industry Publisher B | USD 1.27 B (2025) | Applies a broader solution scope and a higher assumed commercialization pace, which typically pulls more adjacent electronics and faster ramp assumptions into the 2025 base. |

Overall, the comparison indicates that most differences come from where the revenue boundary is drawn and how quickly early deployments are assumed to scale. By tying inputs to repeatable demand indicators and then checking the totals with interview-led pricing and adoption sanity checks, the resulting number stays traceable and practical for planning.

Key Questions Answered in the Report

What is the projected value of the terahertz technologies market by 2031?

The market is forecast to reach USD 1.77 billion by 2031.

How fast is the terahertz technologies market expected to grow?

It is projected to register a 14.74% CAGR during 2026-2031.

Which region is likely to lead future terahertz deployments?

Asia-Pacific is set to expand fastest, with a 15.79% CAGR driven by strong 6G and R&D funding.

Why are mid-frequency terahertz platforms popular?

They balance spatial resolution, atmospheric transmission, and component readiness, capturing nearly half of 2025 revenue.

Which end-user segment is growing quickest?

Healthcare applications are forecast to grow at 16.11% annually, outpacing telecommunications.

What major challenge limits outdoor terahertz backhaul links?

Water-vapor absorption narrows transmission windows, requiring high link budgets or limiting service to dry conditions.

Page last updated on: