Spacer Fluid Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

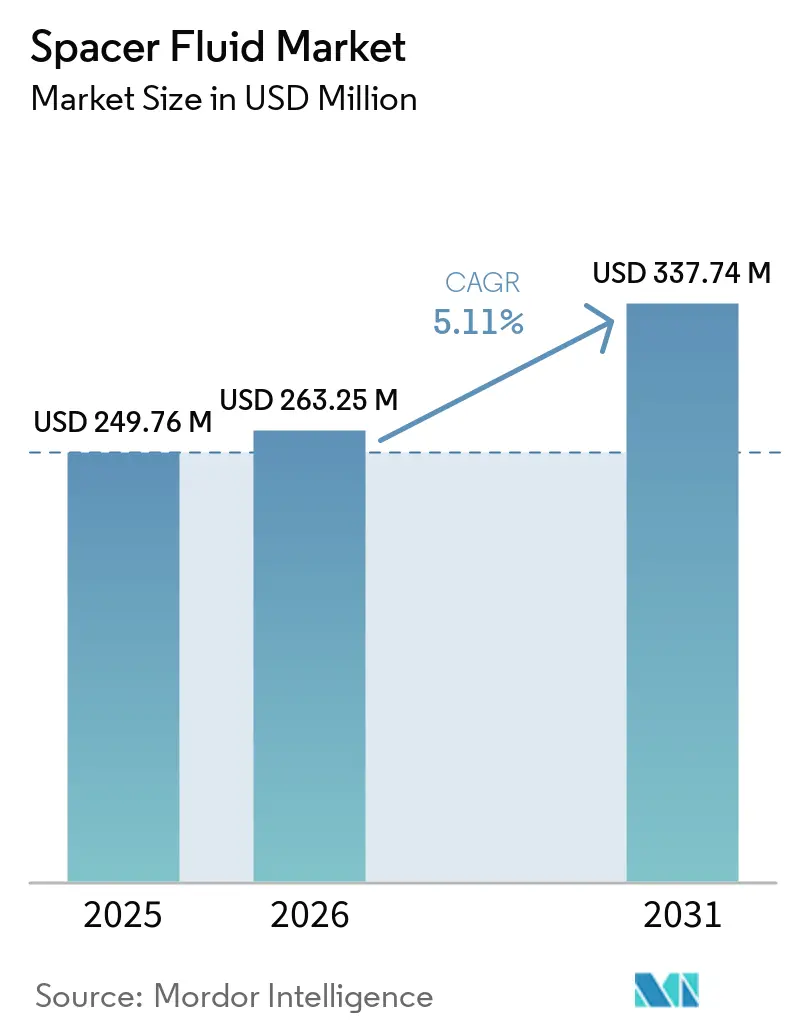

| Market Size (2026) | USD 263.25 Million |

| Market Size (2031) | USD 337.74 Million |

| Growth Rate (2026 - 2031) | 5.11% CAGR |

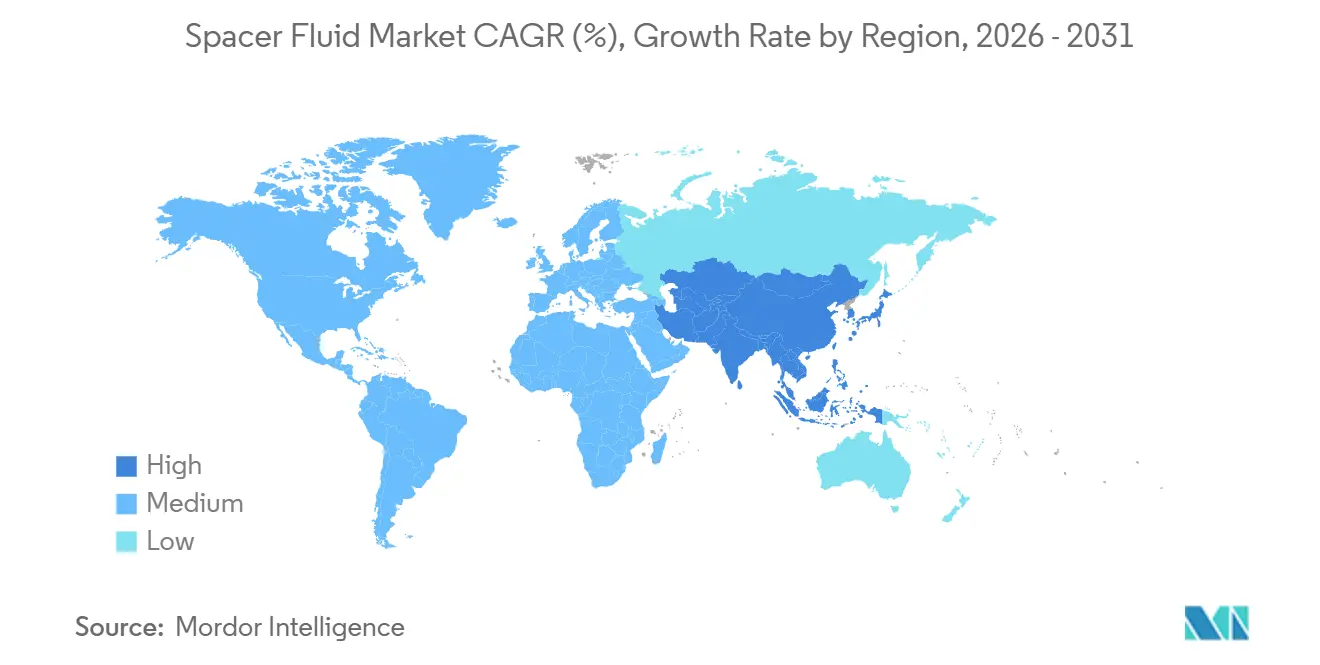

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spacer Fluid Market Analysis by Mordor Intelligence

The Spacer Fluid Market size was valued at USD 249.76 million in 2025 and is estimated to grow from USD 263.25 million in 2026 to reach USD 337.74 million by 2031, at a CAGR of 5.11% during the forecast period (2026-2031). In the near term, regulatory pressure on methane‐leak mitigation and the pivot toward geothermal and carbon-capture wells are reshaping demand patterns. Operators continue to buy low-cost water-based products for vertical onshore wells, yet growth is fastest for polymer-rich switchable and nanoparticle-enhanced systems that withstand HPHT conditions. Digital well planning now optimizes rheology in real time, cutting volumes by up to 15% and shifting pricing power from traditional service companies to software-centric players. At the same time, local-content mandates in the Middle East and Asia-Pacific are forcing international suppliers to add regional blending capacity, which is fragmenting supply chains but anchoring demand growth locally. Competitive intensity is moderate: the three largest providers command a majority share of global revenue, but smaller specialists are gaining traction in geothermal and CCUS retrofits, where track records are still thin.

Key Report Takeaways

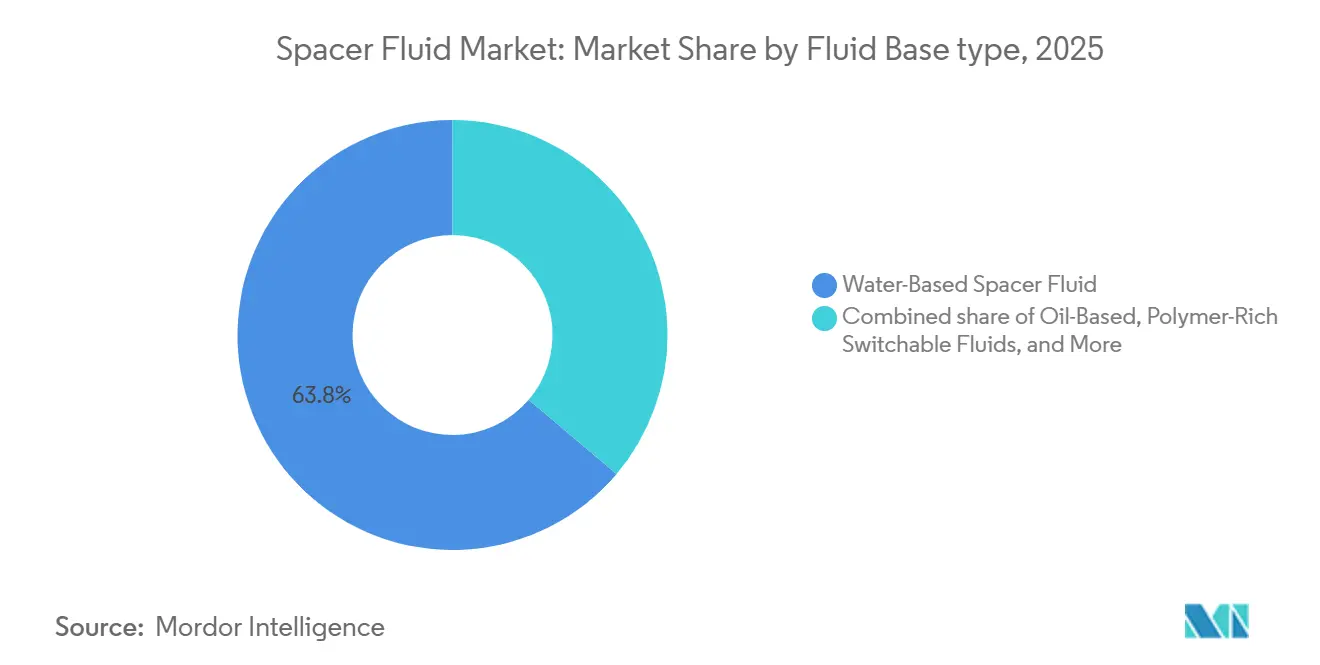

- By fluid base, water-based products led with 63.8% of the spacer fluid market share in 2025, while polymer-rich switchable fluids are projected to grow at a 7.3% CAGR through 2031.

- By additive chemistry, viscosifiers & rheology modifiers led with 34.5% of the spacer fluid market share in 2025, while nanoparticle-enhanced systems are projected to grow at a 7.5% CAGR through 2031.

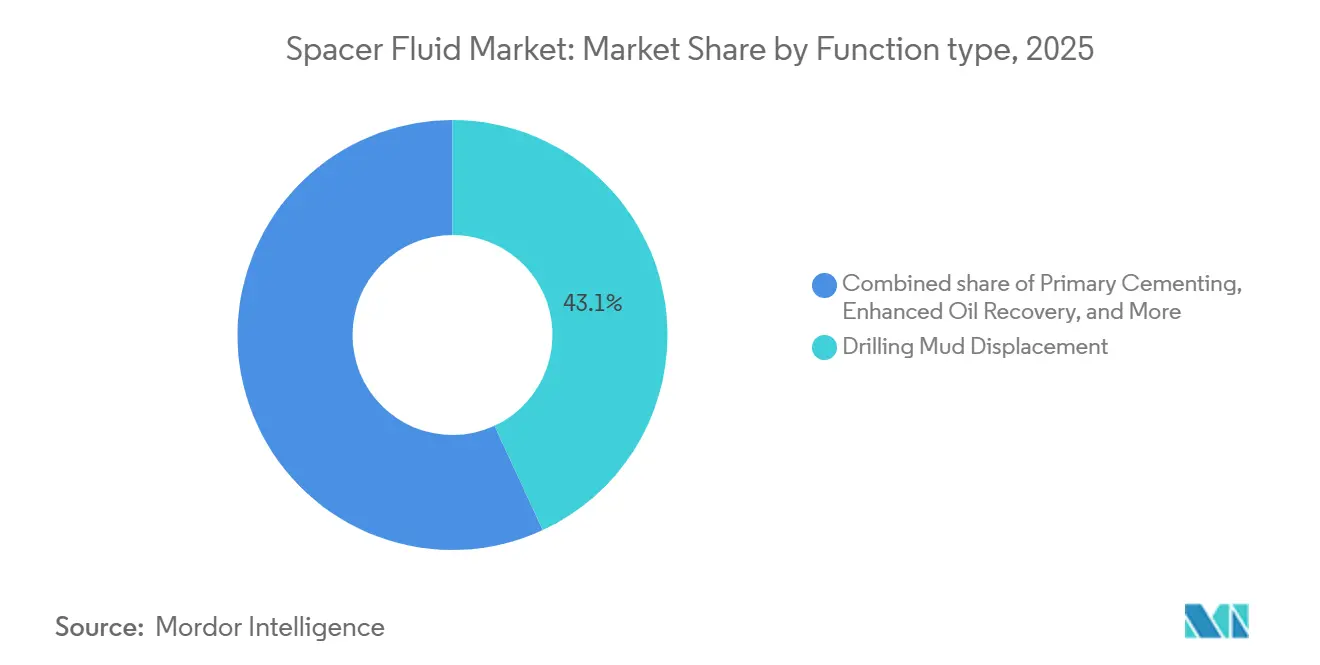

- By function, drilling mud displacement captured 43.1% of the spacer fluid market size in 2025, and enhanced oil recovery is advancing at a 7.8% CAGR to 2031.

- By reservoir type, sandstone led with 43.7% of the spacer fluid market share in 2025, while the naturally fractured type is projected to grow at a 6.1% CAGR through 2031.

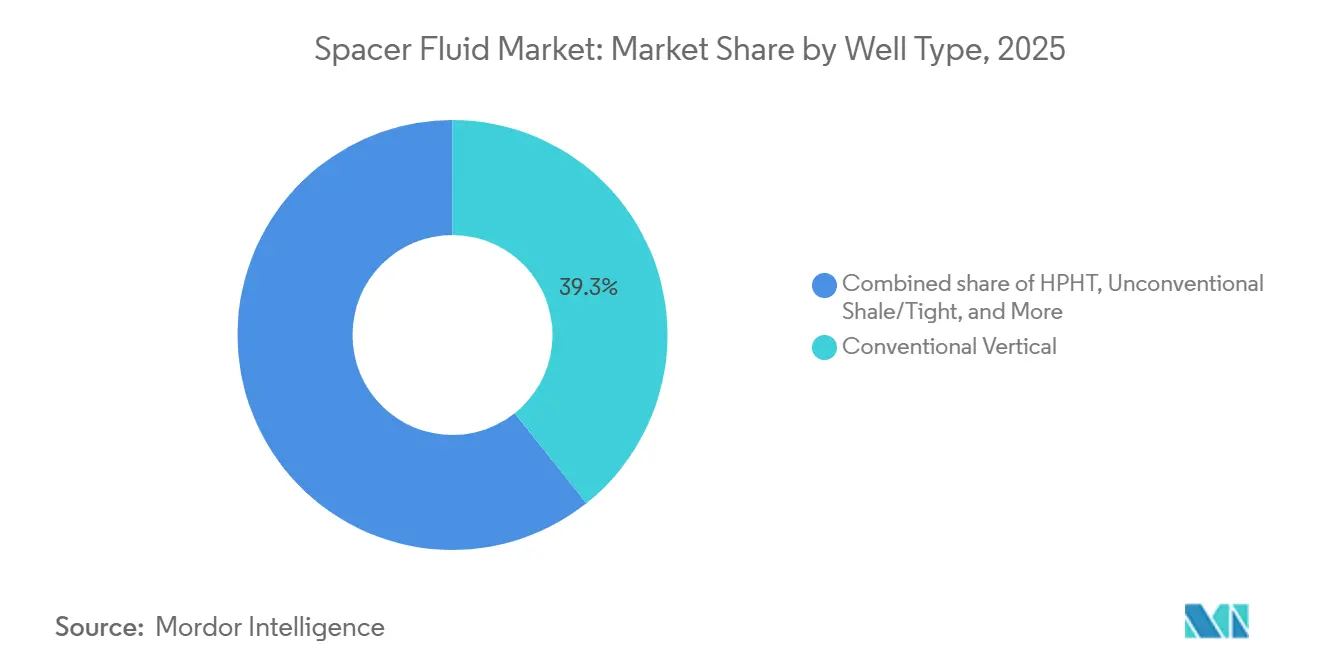

- By well type, conventional vertical led with 39.3% of the spacer fluid market share in 2025, while geothermal well type is projected to grow at a 8.1% CAGR through 2031.

- By location, onshore led with 73% of the spacer fluid market share in 2025, while offshore locations are projected to grow at a 6.4% CAGR through 2031.

- By geography, North America led with 36.9% of the spacer fluid market share in 2025, while Asia-Pacific is projected to grow at a 6.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Spacer Fluid Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ESG‐driven methane-leak reduction mandates | +1.2% | North America, European Union | Medium term (2-4 years) |

| Surge in HPHT & ultra-deepwater projects | +1.5% | Gulf of Mexico, Brazil, West Africa, Asia-Pacific | Long term (≥ 4 years) |

| Rising shale re-fracturing programs in North America | +0.9% | United States, Canada | Short term (≤ 2 years) |

| Digitally designed rheology-tunable spacer formulations | +0.7% | Global, early adoption in North America & Middle East | Medium term (2-4 years) |

| CCUS well retrofits requiring novel spacer chemistries | +0.6% | United States, Canada, Norway, United Kingdom, Australia | Long term (≥ 4 years) |

| National oil company local-content rules (MENA, APAC) | +0.5% | Saudi Arabia, UAE, India, China, Indonesia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

ESG-driven methane-leak reduction mandates

Global climate policy is reshaping spacer specifications toward gas-migration prevention. The U.S. EPA’s 2024 rule introduced a Waste Emissions Charge that rises to USD 1,500 per metric ton in 2026, compelling tighter density windows and surfactant packages that wet casing surfaces and curb micro-annulus formation.[1]U.S. Environmental Protection Agency, “EPA Issues Final Rule to Reduce Methane and Other Harmful Pollution from Oil and Natural Gas Operations,” epa.gov The European Union’s Methane Regulation went live in 2024, extending liability to imported gas and elevating demand for ISO 13503-certified fluids. SLB’s CemCRETE LiteCRETE polymer spacer, deployed in the Permian, cut gas migration by 40% relative to bentonite fluids.[2]SLB, “CemCRETE LiteCRETE System Reduces Gas Migration in Permian Basin,” slb.com Operators increasingly insist on density tolerances of ±0.2 lb/gal to ensure annular seal integrity, especially in horizontal shale wells where pressure spikes can dislodge unset cement. In parallel, digital leak-detection platforms flag anomalies within minutes, forcing rapid remediation and further boosting premium spacer uptake.

Surge in HPHT and ultra-deepwater projects

Multi-billion-dollar deepwater complexes are moving the spacer fluid market toward synthetic and oil-based systems. Chevron’s Anchor and Shell’s Whale projects each operate beyond 20,000 psi and 350 °F, demanding thermally stable viscosifiers and densities up to 18 lb/gal.[3]Chevron, “Anchor Project,” chevron.com Petrobras awarded SLB a USD 430 million contract in 2024 covering 28 wells where nanoparticle-enhanced spacers maintain fluid-loss below 50 ml/30 min at 15,000 psi.[4]SLB, “CemCRETE LiteCRETE System Reduces Gas Migration in Permian Basin,” slb.com Nanoparticles such as graphene oxide form impermeable cakes that safeguard zonal isolation while lowering formation damage. HPHT and ultra-deepwater demand is therefore tilting procurement toward synthetic-base fluids that biodegrade within discharge limits yet survive extreme bottomhole environments, underpinning long-cycle growth for premium chemistries.

Rising shale re-fracturing programs in North America

Economic re-fracs of legacy shale wells need spacers that displace residual slickwater and scale before new proppant stages. BKV Corporation achieved 30%-50% higher initial rates in the Barnett by using hybrid water-based spacers with friction reducers and scale inhibitors. Diamondback and Pioneer (now ExxonMobil) use ResFrac simulation to design spacer trains that shorten pump time and save 15% in fluid cost. Spacer budgets of USD 15,000-30,000 per well equal 5%-8% of total re-frac spend, so formulators able to cut volume but retain displacement efficiency are winning share. High TDS produced water, often >200,000 ppm, drives adoption of synthetic polymers with salinity resilience.

Digitally designed rheology-tunable spacer formulations

Machine-learning platforms optimize density, viscosity, and flow rate in real time. Halliburton’s iCruise and DecisionSpace 365 adjust spacer chemistry on downhole data, trimming volumes by up to 15% in the Haynesville. Baker Hughes’ Leucipa does the same in the North Sea, while SLB’s Delfi digital twin allows engineers to specify minimum effective volumes. These tools commoditize legacy water-based products and shift margins toward software services. Rheology-tunable systems also switch from Newtonian to non-Newtonian behavior via pH triggers, crucial for horizontal wells where turbulent-to-laminar transitions prevent rock failure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile pricing of specialty biopolymers | -0.8% | Global, acute in India/Pakistan-dependent regions | Short term (≤ 2 years) |

| Stricter discharge limits on surfactant toxicity | -0.6% | Gulf of Mexico, North Sea, Australia, SE Asia | Medium term (2-4 years) |

| Supply bottlenecks for food-grade xanthan/guar post-El Niño | -0.4% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| AI-based mud-in-place simulators lowering spacer volumes | -0.5% | Global, concentrated in North America & Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile pricing of specialty biopolymers

Xanthan hit USD 2,760 per metric ton in Jan 2026, up 10% year-on-year, after Chinese fermenters faced higher energy costs. Guar output fell 15% in India’s 2024 kharif season due to erratic monsoon, then faced 10%-50% import duties, lifting costs for service companies reliant on Indian supply. Synthetic polymers offer consistency but raise environmental flags under EU REACH, limiting their ability to fully replace biopolymers. Spacers make up 5%-8% of total well costs, so cost spikes translate quickly into budget overruns, especially for re-frac and abandonment programs with tight economics.

Stricter discharge limits on surfactant toxicity

The EPA’s NPDES GMG290000 permit achieved an 86% pass rate since 2023; failures cost up to USD 50,000 per day and delay rig schedules, prompting operators to adopt biodegradable alkyl-polyglucosides that cost 25% more than nonylphenol ethoxylates. OSPAR and NOPSEMA enforce similar offshore limits, effectively phasing out diesel-based thinners and zinc inhibitors. Smaller service firms often cannot fund the new toxicity tests, raising entry barriers and concentrating spacer fluid market share among incumbents.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fluid Base: Switchable Polymers Challenge Water-Based Dominance

Water-based formulations held 63.8% of the spacer fluid market share in 2025, thanks to low cost and easy handling. Yet polymer-rich switchable fluids are growing 220 basis points faster than the overall spacer fluid market, advancing at 7.3% CAGR to 2031 as pH-triggered gelling improves zonal isolation in horizontals. Oil-based products remain vital for HPHT and deepwater wells. Synthetic-base fluids favored in discharge-sensitive basins like the Gulf of Mexico, biodegrade within 28 days, a nd meet toxicity limits. Foamed and ultralight systems enable operations in depleted or low-pressure zones by cutting density to 6 lb/gal without losing viscosity.

Switchable fluids trim cement contamination by forming in-situ gels at pH 12 and above, a function that saved 10% spacer volume per well in Fervo Energy’s 400-well geothermal program. Synthetic bases, often esters or polyalphaolefins, survive 450 °F for 12 hours, meeting geothermal and CCUS needs. Together, these premium niches are eroding the historical dominance of low-specification water-based systems, redefining the spacer fluid market size distribution.

By Additive Chemistry: Nanoparticles Disrupt Viscosifier Incumbency

Viscosifiers and rheology modifiers captured 34.5% of additive demand in 2025, but nano-enhanced systems are set to expand 7.5% CAGR through 2031, improving fluid-loss control by 30%-40% under HPHT conditions. Surfactants and wettability agents driven by the shift to biodegradable chemistries that meet NPDES toxicity tests. Lost-circulation materials and bridging fibers remain essential for naturally fractured reservoirs.

Silica nanoparticle spacers rolled out by Baker Hughes achieved fluid-loss below 50 ml/30 min at 350 °F, outclassing xanthan systems. Graphene oxide loading raised cement compressive strength by 15% in lab tests, supporting adoption in HPHT completions. The additive mix is therefore pivoting from bulk rheology modifiers to engineered nano-additives that elevate performance while nudging unit costs upward.

By Function: EOR Applications Outpace Primary Cementing

Drilling mud displacement represented 43.1% of functional demand in 2025, but EOR spacer usage is advancing 7.8% CAGR as polymer floods spread across China’s Daqing and Shengli fields. Primary cementing stayed, tracking global drilling, while remedial and P&A work on North Sea wells were near the end-of-life. The balance comes from wellbore cleanup and expandable liners.

Spacer fluid market size for EOR is rising because chemical floods rely on low-IFT surfactant spacers to clear residual oil and enable polymer injectivity. In Brazil’s Campos Basin, Petrobras aims for 15,000 bpd incremental output by 2027 via surfactant-polymer floods, driving region-specific demand. Hence, EOR has become the fastest-growing functional slice, even though drilling mud displacement remains numerically larger.

By Reservoir Type: Fractured Carbonates Demand Tailored Chemistries

Sandstones held 43.7% share in 2025, yet naturally fractured formations are growing 6.1% CAGR as tight carbonates in Jafurah and North American shales require bridging particles between 100-500 microns. Spacer fluids for fractured carbonates often include graphite and calcium carbonate to stem losses; Saudi Aramco’s early production wells confirmed this strategy.

With unconventional shale also under “Others,” salinity-tolerant spacers remain crucial. The Montney and Duvernay, supplying Canadian LNG exports, require additives that function in sour-gas environments exceeding 10% H₂S. These technical needs diversify product lines and raise average selling prices.

By Well Type: Geothermal Surge Reshapes Demand Mix

Conventional vertical wells fell to 39.3% of activity in 2025. Geothermal, growing 8.1% CAGR, now represents the fastest-expanding slice as closed-loop designs like Eavor-Loop demand 450 °F stability and corrosion inhibition. HPHT wells driven by Gulf of Mexico and West Africa projects, while unconventional horizontals and directionals filled the balance.

Fervo Energy’s Cape Station specifies synthetic polymers with silicate inhibitors to survive 12 hours at 450 °F, underscoring why geothermal is redrawing spacer fluid market demand patterns. The shift to ultra-high temperatures privileges suppliers with advanced polymer science, limiting effective competition.

By Location: Offshore Complexity Drives Premium Pricing

Onshore held 73% share in 2025, yet offshore is growing 6.4% CAGR thanks to ultra-deepwater developments. Petrobras alone will drill 28 pre-salt wells with synthetic-base spacers that biodegrade in 28 days to meet Brazilian rules, anchoring Latin American offshore growth. ExxonMobil’s Stabroek block relies on oil-based spacers for 12,000 psi reservoirs.

Offshore regulations, from NPDES to OSPAR, boost demand for green surfactants and close-loop cuttings systems, adding 20%-30% to fluid costs. These added compliance outlays widen the price gap between onshore and offshore formulations, fortifying revenue streams for suppliers with robust environmental portfolios.

Geography Analysis

North America commanded 36.9% spacer fluid market share in 2025 on the back of 12,000 horizontal shale wells drilled in 2024, consuming 15 million barrels of completion fluids. Yet growth here moderates as capital pivots to re-fracs; Barnett campaigns showed 30%-50% production uplifts using hybrid spacers that cost USD 15,000-30,000 per well. Canada’s Montney, buoyed by LNG export demand, needs sour-gas compatible spacers for H₂S-rich wells.

Asia-Pacific is the fastest-growing region at 6.2% CAGR through 2031. India’s 60% local-content rule for drilling chemicals by 2027 is spurring domestic xanthan fermentation and guar processing. CNOOC awarded USD 1.2 billion in drilling contracts requiring China-made spacers, while Indonesia’s SKK Migas targets 50% local content by 2030, compelling multinationals to partner or build blending plants.

Europe reflects a dual focus on new developments like Johan Sverdrup and large-scale P&A. The UK regulator expects 2,000 North Sea wells to be abandoned by 2030, lifting demand for 16 lb/gal high-density spacers. South America, at 12%, is dominated by Brazil’s pre-salt, where high-pressure wells use synthetic bases. The Middle East & Africa benefit from the Jafurah unconventional gas ramp-up and Ghasha ultra-sour gas, both favoring lost-circulation and corrosion-inhibited formulations.

Competitive Landscape

The global spacer fluid market is moderately concentrated. SLB, Halliburton, and Baker Hughes are leading players, anchored by bundled drilling-fluids and cementing contracts. SLB’s Q4-2024 revenue hit USD 9.3 billion, with digital up 24% to USD 1.4 billion as its Delfi platform automated spacer optimization. Halliburton logged USD 5.7 billion that quarter, expanding capacity in the Middle East. Baker Hughes’ Leucipa integrated analytics trimmed spacer volumes by 10%-15% on North Sea wells.

Smaller specialists such as Impact Fluid Solutions and Petrochem Performance Chemicals target geothermal and CCUS niches with 450 °F-stable synthetic polymers. Regulatory toxicity testing costs favor consolidation, but white space remains for innovators in nanotechnology and switchable polymers. AI-driven volume reduction constrains top-line growth for commodity products, pushing service companies to pivot toward premium chemistries and digital subscriptions.

Spacer Fluid Industry Leaders

Halliburton Company

SLB (Schlumberger)

Baker Hughes Company

Weatherford International

TETRA Technologies Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: SLB secured a USD 430 million drilling-services contract with Petrobras for 28 Santos Basin wells that will use synthetic-base spacers biodegradable in 28 days.

- February 2025: Argent LNG selected Baker Hughes as technology provider for proposed 24 MTPA LNG export facility in Port Fourchon, Louisiana, utilizing NMBL™ modularized LNG solution and LM9000 gas turbines with a multi-year services plan including iCenter™ digital solutions. Construction is expected to begin in 2026 with commercial operations by 2030.

- January 2025: Baker Hughes launched SureCONNECT™ FE, the first commercially available downhole fiber-optic wet-mate system designed for high-pressure, high-temperature environments, enabling real-time monitoring and electric intelligent completion systems without intervention.

- November 2024: Baker Hughes opened Namibia's largest liquid mud plant and cement bulk facility at Walvis Bay Port, holding 15,000 barrels of fluids to support offshore oil and gas operations in the Orange Basin.

Global Spacer Fluid Market Report Scope

A spacer fluid is a specialized viscous liquid utilized in the oil and gas industry to separate and prevent the mixing of two incompatible fluids, typically drilling mud and cement slurry, during wellbore completion. Direct contact between drilling fluids and cement, which are chemically incompatible, can result in severe gelation, thickening, or inadequate bonding, potentially compromising well integrity.

The spacer fluid market is segmented into fluid base, additive chemistry, function, reservoir type, well type, location, and geography. By fluid base, the market is segmented into water-based, oil-based, synthetic-based, polymer-rich switchable, and other fluid bases. By additive chemistry, the market is segmented into viscosifiers and rheology modifiers, surfactants and wettability agents, LCM/bridging fibers, and nanoparticle-enhanced systems. By function, the market is segmented into primary cementing, remedial/plug and abandon, drilling mud displacement, EOR, wellbore cleanup, and other uses. By reservoir type, the market is segmented into carbonate, sandstone, naturally fractured, and other reservoir types. By well type, the market is segmented into conventional vertical, HPHT, unconventional shale/tight, directional/horizontal, and geothermal wells. By location, the market is segmented into onshore and offshore. The report also covers the market size and forecasts for the spacer fluid market across major regions, including North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Water-Based Spacer Fluid |

| Oil-Based Spacer Fluid |

| Synthetic-Based Spacer Fluid |

| Polymer-Rich Switchable Fluids |

| Others (Foamed, Ultralight, etc.) |

| Viscosifiers and Rheology Modifiers |

| Surfactants and Wettability Agents |

| LCM/Bridging Fibers |

| Nanoparticle-Enhanced Systems |

| Primary Cementing |

| Remedial/Plug and Abandon |

| Drilling Mud Displacement |

| Enhanced Oil Recovery (EOR) |

| Wellbore Cleanup and Other Uses |

| Carbonate |

| Sandstone |

| Naturally Fractured |

| Others |

| Conventional Vertical |

| HPHT |

| Unconventional Shale/Tight |

| Directional/Horizontal |

| Geothermal |

| Onshore |

| Offshore |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Fluid Base | Water-Based Spacer Fluid | |

| Oil-Based Spacer Fluid | ||

| Synthetic-Based Spacer Fluid | ||

| Polymer-Rich Switchable Fluids | ||

| Others (Foamed, Ultralight, etc.) | ||

| By Additive Chemistry | Viscosifiers and Rheology Modifiers | |

| Surfactants and Wettability Agents | ||

| LCM/Bridging Fibers | ||

| Nanoparticle-Enhanced Systems | ||

| By Function | Primary Cementing | |

| Remedial/Plug and Abandon | ||

| Drilling Mud Displacement | ||

| Enhanced Oil Recovery (EOR) | ||

| Wellbore Cleanup and Other Uses | ||

| By Reservoir Type | Carbonate | |

| Sandstone | ||

| Naturally Fractured | ||

| Others | ||

| By Well Type | Conventional Vertical | |

| HPHT | ||

| Unconventional Shale/Tight | ||

| Directional/Horizontal | ||

| Geothermal | ||

| By Location | Onshore | |

| Offshore | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| NORDIC Countries | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will global demand for spacer fluids be by 2031?

The spacer fluid market size is forecast to reach USD 337.74 million by 2031, growing at a 5.11% CAGR from 2026.

Which fluid base is growing fastest?

Polymer-rich switchable spacer fluids are projected to expand at 7.3% CAGR through 2031 as pH-triggered gelling improves zonal isolation.

Why are nanoparticles gaining popularity in spacer formulations?

Nanoparticles such as graphene oxide and silica cut fluid loss by up to 40% and enhance cement strength, supporting adoption in HPHT completions.

What impact do methane regulations have on spacer demand?

EPA and EU methane rules push operators to specify spacers with tighter density windows and gas-migration control, boosting premium product sales.

Which region offers the strongest growth prospects?

Asia-Pacific is set to grow at 6.2% CAGR to 2031, driven by local-content mandates in India, China, and Indonesia that spur domestic additive production.

How are digital tools changing spacer usage?

Platforms like SLB's Delfi and Halliburton's DecisionSpace 365 optimize rheology in real time, trimming spacer volumes by up to 15% and shifting value toward software services.

Page last updated on: