Pressure Vessel Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 63.52 Billion |

| Market Size (2031) | USD 79.23 Billion |

| Growth Rate (2026 - 2031) | 4.52% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pressure Vessel Market Analysis by Mordor Intelligence

The Pressure Vessel market size is expected to grow from USD 60.77 billion in 2025 to USD 63.52 billion in 2026 and is forecast to reach USD 79.23 billion by 2031 at 4.52% CAGR over 2026-2031.

Energy-infrastructure modernization, Asia-Pacific nuclear construction, and hydrogen-economy investments are reshaping demand profiles. Composite overwrapped pressure vessels (COPVs) lead the technology shift because weight-to-strength advantages enable hydrogen mobility and space applications. Ultra-high-pressure ratings above 100 bar expand quickly as fuel-cell vehicles and supercritical chemical processing become mainstream. The pressure vessel market also benefits from tougher safety standards such as ASME, PED, and API 510, which accelerate replacement cycles and favor certified manufacturers. At the same time, volatile steel prices, skilled-labor shortages, and lengthy certification cycles weigh on profitability, nudging producers toward composites and automation.

Key Report Takeaways

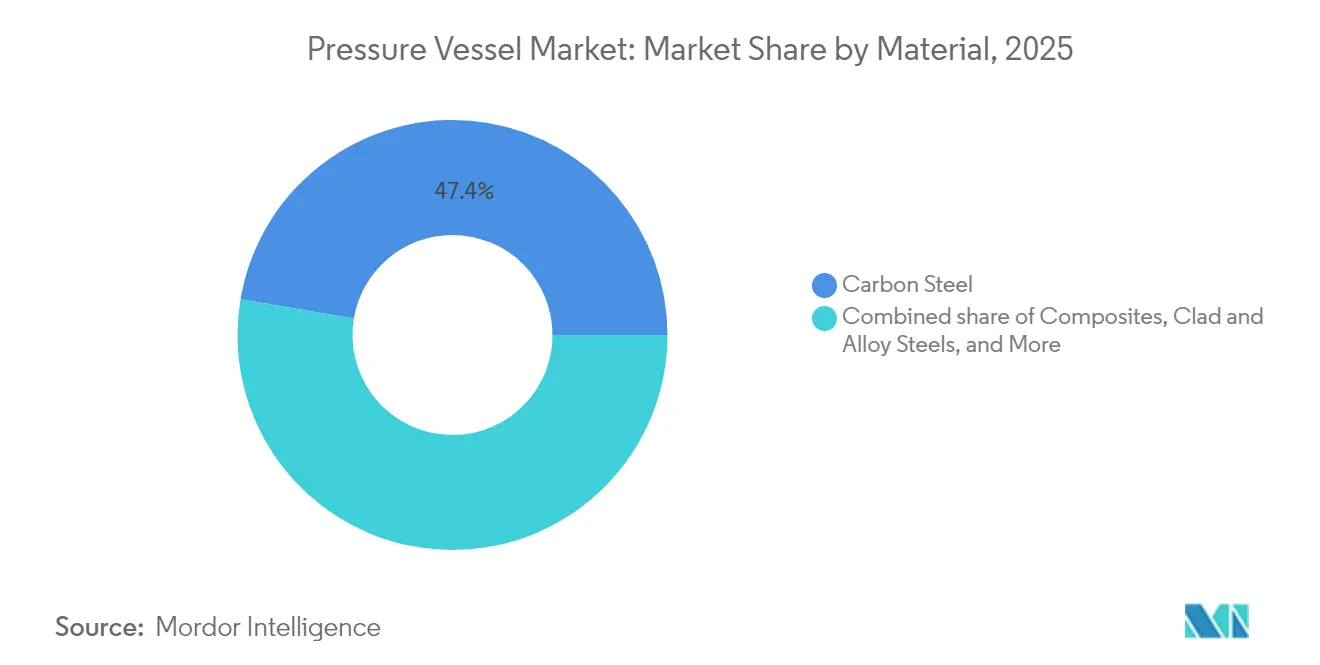

- By material, carbon steel held 47.35% pressure vessel market share in 2025, while composites recorded the highest projected CAGR at 7.05% through 2031.

- By pressure rating, the 0 to 10 bar (low) segment captured the largest share of 40.60% in 2025, while vessels above 100 bar captured 7.20% of incremental growth, eclipsing all other brackets between 2025 and 2031.

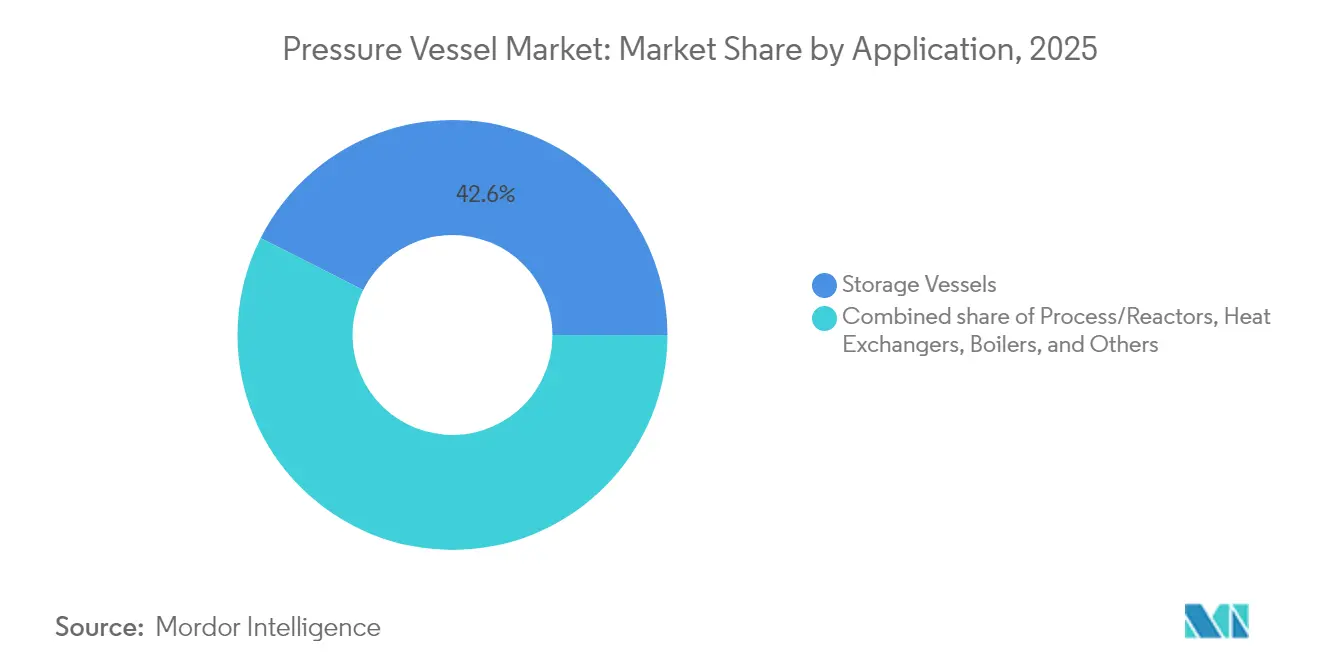

- By application, storage accounted for 42.55% of the pressure vessel market size in 2025, yet the specialty “Others” category is set to expand at a 6.85% CAGR to 2031.

- By end-user, oil and gas mid/downstream retained 33.45% revenue share in 2025, whereas pharmaceutical and biotech uses are advancing at 7.05% CAGR through 2031.

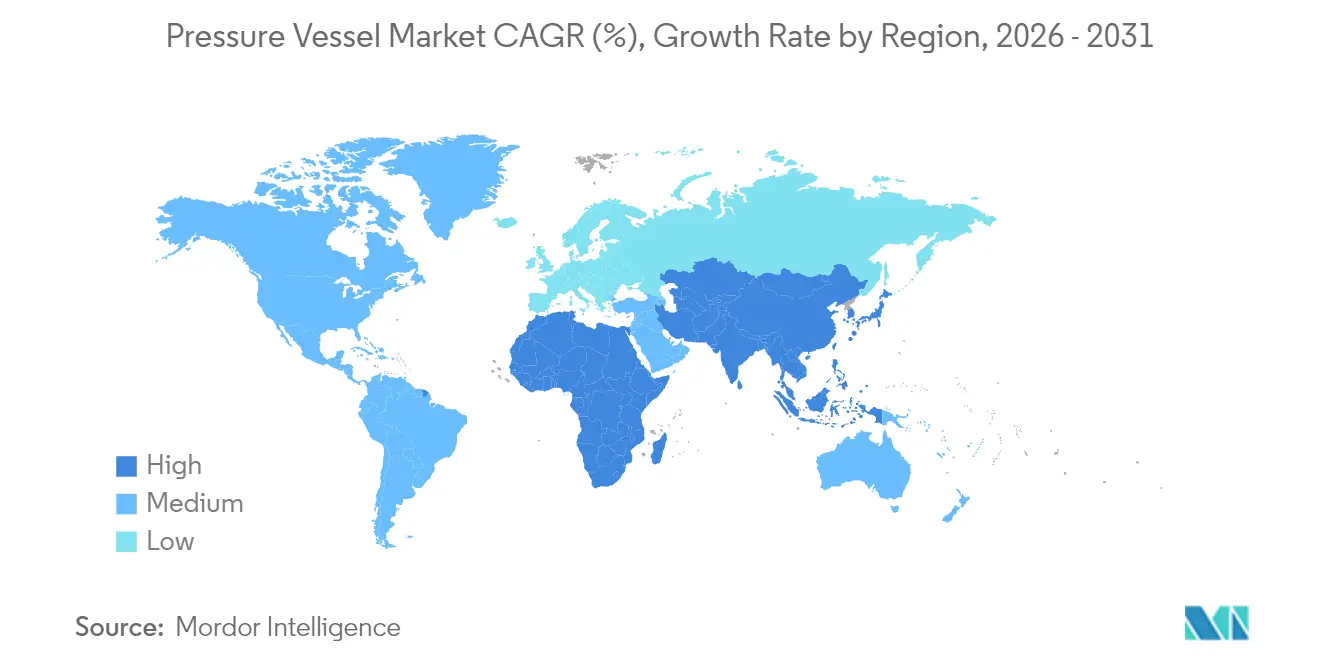

- Asia-Pacific commanded 44.62% of the pressure vessel market in 2025, and it posts the strongest regional CAGR at 6.05% over the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pressure Vessel Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy infrastructure upgrades in emerging economies | +1.20% | Asia-Pacific, Middle East & Africa, South America | Medium term (2-4 years) |

| Rising global LNG trade and associated cryogenic storage demand | +0.90% | Global, focus on North America & Asia-Pacific | Long term (≥ 4 years) |

| Nuclear new-build resurgence in Asia | +0.80% | Asia-Pacific core, spill-over to Europe | Long term (≥ 4 years) |

| Stricter workplace safety regulations | +0.60% | Global | Short term (≤ 2 years) |

| COPV adoption in hydrogen mobility | +0.70% | North America & Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Modular small-scale chemical processing skids | +0.50% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Energy Infrastructure Upgrades in Emerging Economies

Asia-Pacific governments accelerate refinery, petrochemical, and power-generation projects that require large quantities of certified vessels; Dongfang Electric’s supply of domestic reactor pressure vessels for Taishan 2 underscores the shift from imports to local fabrication.(1)World Nuclear News, “Construction Milestone at Taishan 2 EPR,” world-nuclear-news.org Industrial parks across India and Southeast Asia specify standardised vessels for combined-cycle plants and LNG terminals, redistributing orders away from traditional Western suppliers. Funding from national development banks shortens project cycles and boosts volume guarantees for regional fabricators. Lower labour costs complement burgeoning technical skills, enabling price-competitive products that comply with ASME and PED codes. This geographic capacity migration adds manufacturing resilience and cost pressure within the pressure vessel market.

Rising Global LNG Trade and Associated Cryogenic Storage Demand

Canada’s first Pacific-coast export cargo to Asia shows North American LNG flows demand hundreds of double-walled stainless-steel vessels that maintain −162 °C temperatures under variable loading. The USD 40 billion LNG Canada plant illustrates the scale, with tanks engineered to manage boil-off gas and cyclic thermal stresses. Vessel complexity grows when integrating onto LNG-fuelled ships and heavy-duty trucks, where weight reduction and vacuum insulation become mission-critical. These technical barriers favour incumbents with proven cryogenic know-how, consolidating market share among specialised suppliers. Long-term offtake contracts reduce volume risk, enabling large backlog visibility for cryogenic vessel manufacturers.

Nuclear New-Build Resurgence in Asia

Japan Steel Works controls 80% of global large-forging capacity used in reactor pressure vessels, anchoring Asia-Pacific leadership.(2)Japan Steel Works, “Nuclear Component Orders Bolster JSW Results,” jsw.co.jp Mitsubishi Heavy Industries has expanded reactor production at Kobe to support domestic restarts and export orders, while Russia’s Atommash now produces four full nuclear-island sets per year after its relaunch. Advanced small modular reactors leverage factory fabrication, standardising vessel designs to cut site labour and schedule risk. Each reactor order commands tens of millions of dollars for a single pressure vessel, making nuclear the highest-value segment of the pressure vessel market. New-build pipelines across China and India, therefore, underpin long-duration demand visibility.

Stricter Workplace Safety Regulations (API 510, PED, ASME)

API 510 inspections require periodic wall-thickness and flaw assessments, prompting early replacement of ageing refinery vessels. The European Pressure Equipment Directive streamlines compliance across 27 member states, but documentation burdens and notified-body audits raise costs that smaller fabricators struggle to absorb. ASME code revisions now include creep-strength-enhanced ferritic steels and additive-manufactured components, widening design options while keeping safety margins ASME.ORG. Firms advertising full-scope compliance gain tender advantages as asset owners treat safety credentials as selection criteria. Collectively, regulation transforms safety from a cost centre into a competitive differentiator within the pressure vessel market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile steel prices squeezing OEM margins | -0.80% | Global | Short term (≤ 2 years) |

| Lengthy certification & compliance cycles | -0.60% | North America & Europe | Medium term (2-4 years) |

| Slow commercialisation of Generation IV designs | -0.40% | Global | Long term (≥ 4 years) |

| Scarcity of skilled welders & inspectors | -0.70% | Global, acute in North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Steel Prices Squeezing OEM Margins

European apparent steel consumption shrank for the fourth year in 2024, and new US import tariffs have intensified cost swings.(3)Financial Times, “Tariffs Hit Steel Market Hard as Recession Persists,” ft.com Pressure vessel makers negotiate fixed-price delivery contracts months before plate mills settle quarterly surcharges, creating negative margins when spot prices spike. Some producers accelerate substitution toward composites or duplex stainless grades to mitigate exposure, but code approvals limit rapid changeovers. Working-capital burdens also rise because mills demand quicker payment during tight supply cycles. Thus, price volatility directly constrains profitability in the pressure vessel market.

Lengthy Certification & Compliance Cycles

Document packages for nuclear reactors exceed 2,000 pages and require multi-year review by regulators such as the NRC and EURATOM, delaying revenue recognition for vessel suppliers. Pharmaceutical bioreactors undergo validation testing that can last 18 months before lot release. Smaller entrants find audit costs prohibitive, reinforcing incumbent dominance. Harmonisation efforts between ASME and PED progress slowly, so OEMs must still tailor product dossiers per jurisdiction. These protracted cycles stretch cash flows and restrict new-technology uptake across the pressure vessel market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Composites Challenge Steel Dominance

Carbon steel retained 47.35% share of the pressure vessel market in 2025, thanks to low cost and broad code coverage. However, the composites' pressure vessel market size is projected to rise 7.05% CAGR to 2031 as hydrogen mobility scales production volumes. Stainless steel maintains an evergreen role in food, pharmaceutical, and biotech services, where corrosion resistance justifies its premium price. Clad and alloy steels address high-temperature petrochemical reactors, and aluminium occupies weight-sensitive niches. Composite overwrapped pressure vessels achieve 60% weight reduction at 700 bar service, expanding adoption into transport and stationary storage.

The pressure vessel market responds by retooling filament-winding lines and securing carbon-fibre supply agreements to capture the emerging composite opportunity. Steel fabricators defend their share by adding electropolishing lines and duplex alloys to meet stringent hygiene codes. Material diversification, therefore, intensifies competition, with regulatory approvals acting as both barrier and catalyst. Certifications for composite liners in nuclear service remain elusive, keeping steel dominant in that premium segment but not halting composite encroachment elsewhere.

By Pressure Rating: Ultra-High Pressure Drives Innovation

Low-pressure vessels between 0 and 10 bar held 40.60% of the pressure vessel market share in 2025 across bulk storage and water treatment. The pressure vessel market size for ultra-high-pressure units above 100 bar will rise at a 7.25% CAGR to 2031 because hydrogen tanks and supercritical reactors require extreme ratings. Medium (10-50 bar) and high (50-100 bar) segments provide steady replacements in refining and chemical plants. Hydrogen fuel cell vehicles store at 350-700 bar, so Type 4 tanks become the design default.

Manufacturers targeting this segment invest in autofrettage presses, precision winding, and in-house burst-test rigs to comply with ISO 19881. Cost-per-kilogram of stored hydrogen becomes the competitive metric, driving thinner liners and advanced fibers. Conversely, low-pressure producers focus on modular tank farms and automated rolling lines to preserve margin in commodity markets. This bifurcation underscores how emerging technologies redefine competitive clusters within the pressure vessel market.

By Application: Storage Dominance Faces Specialty Growth

Storage vessels captured 42.55% revenue in 2025, serving LNG terminals, industrial gases, and petrochemical storage. The “Others” category, including modular chemical-processing skids and cryogenic dewars, expands 6.85% CAGR to 2031, outpacing mainstream reactors and boilers. Cryogenic designs need multilayer insulation and vacuum jackets to manage heat ingress, whereas modular skid vessels prioritise compact footprints and integrated instrumentation.

The pressure vessel market capitalises on this divergence by offering customised skids under framework agreements, capturing design-for-manufacture fees and after-sales spares. High-volume storage suppliers accelerate robotic welding and digital quality records to maintain cost leadership. Over time, knowledge from specialty vessels feeds into standard offerings, fostering incremental innovation across the application spectrum.

By End-User Industry: Pharma Biotech Accelerates Growth

Oil and gas mid/downstream retained 33.45% of revenue in 2025, but pharmaceutical and biotech segments will log a 7.05% CAGR to 2031 as single-use bioreactor scales surpass 4,000 litres. Pressure vessel market size for nuclear power will also rise, given new reactor build programmes, while chemical and petrochemical users sustain baseline demand. Food and beverage applications rely on 300-series stainless steel with mirror finishes to mitigate biofilm, providing steady replacements.

Biotech’s stringent cleaning validation demands electropolished interiors and documentary traceability, raising average selling prices. Vendors, therefore, bundle validation support and GMP audit packages, strengthening lock-in. Conversely, oil and gas customers impose rigid cost disciplines, pressuring margins. The mixed portfolio cushions cyclicality, reinforcing diversified positioning among leading pressure vessel market participants.

Geography Analysis

Asia-Pacific held 44.62% of the pressure vessel market in 2025 and is forecast to expand at a 6.05% CAGR through 2031. China’s localisation of nuclear island components and India’s refinery build-outs underpin large order books. Japan Steel Works and Mitsubishi Heavy Industries supply reactor forgings globally, reinforcing regional dominance in high-specification segments. South Korea leverages shipbuilding expertise to produce LNG tanks, and ASEAN economies invest in hydrogen refuelling stations that use 700 bar COPVs. These projects embed long-term manufacturing ecosystems across the region. North America represents a mature yet opportunity-rich landscape. The US aims to raise nuclear capacity from 100 GW in 2024 to 300 GW by 2050, implying that sizable reactor-grade vessel demand and export terminals along the Gulf Coast and British Columbia require cryogenic storage, sustaining specialised vessel orders. Replacement cycles in refineries and stricter OSHA rules create recurring domestic demand, although fabricators face competition from Asian imports on commodity tanks.

Europe prioritises decarbonisation, channelling funds into hydrogen infrastructure and small modular reactors. PED harmonisation simplifies cross-border sales but raises compliance thresholds. Steel price volatility and energy costs challenge margins, prompting consolidation among medium-sized fabricators. Scandinavia and Germany pilot Power-to-X plants, adding ultra-high-pressure vessels to local wish lists. Overall, European customers pay premiums for traceable supply chains and carbon-footprint disclosures.

Emerging regions such as South America, the Middle East, and Africa show divergent growth arcs. Brazil’s pre-salt fields extend downstream infrastructure, Mexico retrofits refineries, and Argentina eyes shale monetisation. Gulf petrochemical clusters in Saudi Arabia and the UAE commission mega-scale reactors and heat exchangers. African nations pursue modular fertiliser and gasification units, leaning on foreign EPC contractors that bundle imported vessels. Collectively, these areas inject volume upside into the global pressure vessel market, albeit from smaller bases.

Competitive Landscape

The pressure vessel market is fragmented in overall revenue terms but exhibits pockets of high concentration. Nuclear reactor vessels, for instance, are produced by a handful of ASME-certified suppliers led by Japan Steel Works, which controls 80% of large-diameter forgings. Babcock & Wilcox and Westinghouse focus on boilers and nuclear pressure boundaries, leveraging long-term utility partnerships. By contrast, storage tanks for chemicals and water are served by thousands of regional fabricators that compete largely on price.

Competitive strategies depend on segment focus. Legacy steel shops invest in advanced plasma cutting, robotic welding, and ERP-linked traceability to bolster productivity. Composite specialists develop proprietary resin systems and high-speed towpreg winding to outrun learning curves. Several incumbents acquire composite start-ups to hedge bets, while others form joint ventures in Asia-Pacific to secure local content mandates. Software for digital twin simulations now accompanies vessel bids, offering predictive maintenance as a service, deepening customer stickiness.

Regulatory credentials remain a crucial entry barrier. Nuclear suppliers must meet N stamp, RCC-M, and KTA codes, which take years to achieve. Pharmaceutical vendors maintain ISO 9001 and cGMP certifications audited by regulators. Cryogenic vessel players hold EN 13458 and ADR approvals for transport. The capital and time needed to obtain these badges explain the persistence of established brands in the upper tiers of the pressure vessel market even as new materials widen the field.

Pressure Vessel Industry Leaders

Babcock & Wilcox Enterprises Inc

Doosan Heavy Industries & Construction

Alfa Laval AB

Andritz AG

Larsen & Toubro Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Babcock & Wilcox Enterprises posted Q1 2025 revenue of USD 181.2 million, with its Thermal segment up 25% as customers upgraded boilers and pressure vessels, lifting backlog to USD 526.8 million.

- March 2025: Westinghouse Electric and Shawflex signed an MoU to strengthen nuclear pressure-vessel supply chains for AP1000, AP300, and eVinci reactors, with each AP1000 unit expected to add nearly USD 1 billion to Canadian GDP.

- March 2025: Babcock & Wilcox reported 2024 full-year bookings up 39% to USD 889.6 million, highlighting progress on its BrightLoop hydrogen project that relies on specialised vessels for chemical looping.

- July 2024: The Netherlands mapped EUR 56-69 billion in electrolyser and offshore wind investments, triggering demand for hydrogen-storage pressure systems.

Global Pressure Vessel Market Report Scope

A pressure vessel is a container designed to hold gases or liquids at a pressure substantially different from the ambient pressure and is primarily used in thermal power generation, refineries, petrochemical plants, and other end-user industries.

The Pressure Vessel Market is segmented by application, end-user industry, and geography. By application, the market is segmented into processing vessels, storage vessels, and others. By end-user industry, the market is segmented into oil and gas, chemical and fertilizers, power, and others. The report also covers the market size and forecasts for the Pressure Vessel Market across major regions. For each segment, the market sizing and forecasts have been done based on revenue (USD Billion).

| Carbon Steel |

| Stainless Steel |

| Clad and Alloy Steels |

| Composites |

| Aluminium and Others |

| 0 to 10 bar (Low) |

| 10 to 50 bar (Medium) |

| 50 to 100 bar (High) |

| Above 100 bar (Ultra-high) |

| Storage Vessels |

| Process/Reactors |

| Heat Exchangers |

| Boilers |

| Others (Custom vessels, Specialty vessels, Expansion vessels) |

| Oil and Gas Upstream |

| Oil and Gas Mid/Downstream |

| Chemical and Petrochemical |

| Power Generation |

| Food and Beverage |

| Pharmaceuticals and Biotech |

| Water and Wastewater |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Material | Carbon Steel | |

| Stainless Steel | ||

| Clad and Alloy Steels | ||

| Composites | ||

| Aluminium and Others | ||

| By Pressure Rating | 0 to 10 bar (Low) | |

| 10 to 50 bar (Medium) | ||

| 50 to 100 bar (High) | ||

| Above 100 bar (Ultra-high) | ||

| By Application | Storage Vessels | |

| Process/Reactors | ||

| Heat Exchangers | ||

| Boilers | ||

| Others (Custom vessels, Specialty vessels, Expansion vessels) | ||

| By End-User Industry | Oil and Gas Upstream | |

| Oil and Gas Mid/Downstream | ||

| Chemical and Petrochemical | ||

| Power Generation | ||

| Food and Beverage | ||

| Pharmaceuticals and Biotech | ||

| Water and Wastewater | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the pressure vessel market?

The pressure vessel market is valued at USD 63.52 billion for 2026 and is expected to reach USD 79.23 billion by 2031, growing at a 4.52% CAGR.

Which region leads the pressure vessel market and why?

Asia-Pacific leads with 44.62% share due to nuclear new-build activity, refinery expansion, and emerging hydrogen infrastructure.

Which material category is growing fastest?

Composite overwrapped pressure vessels are advancing at 7.05% CAGR because their weight savings make them ideal for hydrogen mobility.

How does steel price volatility impact the industry?

Unpredictable steel costs compress OEM margins under fixed contracts, prompting material diversification and composite substitution.

What are the top growth applications?

Ultra-high-pressure hydrogen tanks, cryogenic LNG storage, and modular chemical-processing skids exhibit the highest growth trajectories.

Why are certification cycles considered a restraint?

Nuclear, pharmaceutical, and pressure-code compliance reviews can last multiple years, delaying revenue and raising entry barriers for newcomers.

Page last updated on: