Jet Fuel Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 216.59 Billion |

| Market Size (2031) | USD 354.41 Billion |

| Growth Rate (2026 - 2031) | 10.35% CAGR |

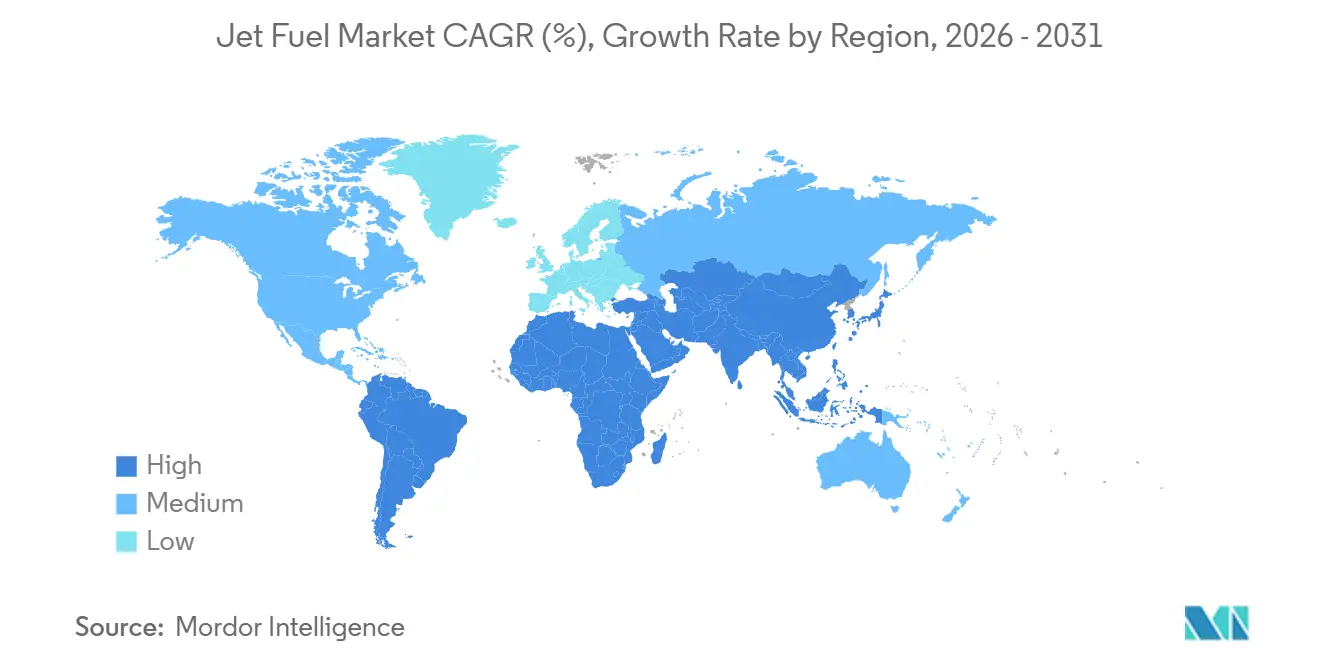

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

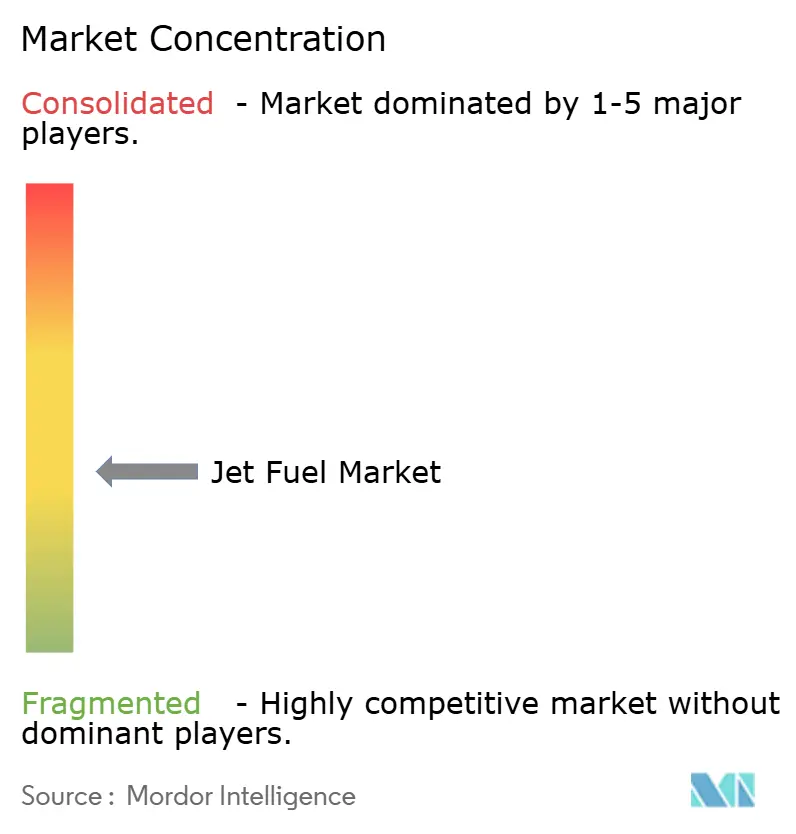

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Jet Fuel Market Analysis by Mordor Intelligence

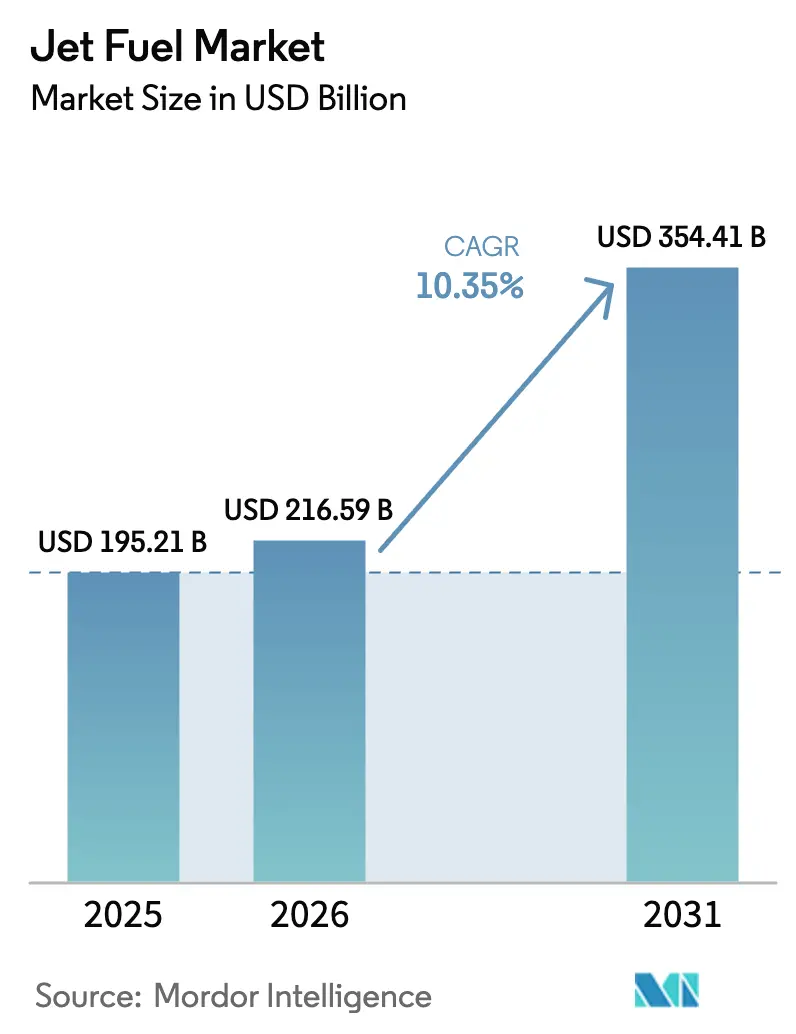

The Jet Fuel Market size is projected to be USD 195.21 billion in 2025, USD 216.59 billion in 2026, and reach USD 354.41 billion by 2031, growing at a CAGR of 10.35% from 2026 to 2031.

Accelerating seat-capacity recovery in Asia-Pacific, sustained wide-body freighter deliveries on trans-Pacific lanes, and regulatory mandates that blend sustainable aviation fuel (SAF) into conventional kerosene collectively underpin this expansion of the jet fuel market. Record-high passenger load factors in January 2025 pushed airlines to up-gauge fleets rather than cap traffic, lifting per-flight fuel uplift even as next-generation aircraft promise lower burn per seat. Concurrently, the European Union’s ReFuelEU Aviation rule compels carriers to use SAF blends that possess slightly lower energy density, so total liters demanded rise despite efficiency gains. Integrated majors that control refineries, pipelines, and airport hydrant rights earn margin resilience as airlines seek one-stop contracts covering both SAF and Jet A-1, while specialist producers such as Neste and LanzaJet capture premiums in the nascent SAF niche.

Key Report Takeaways

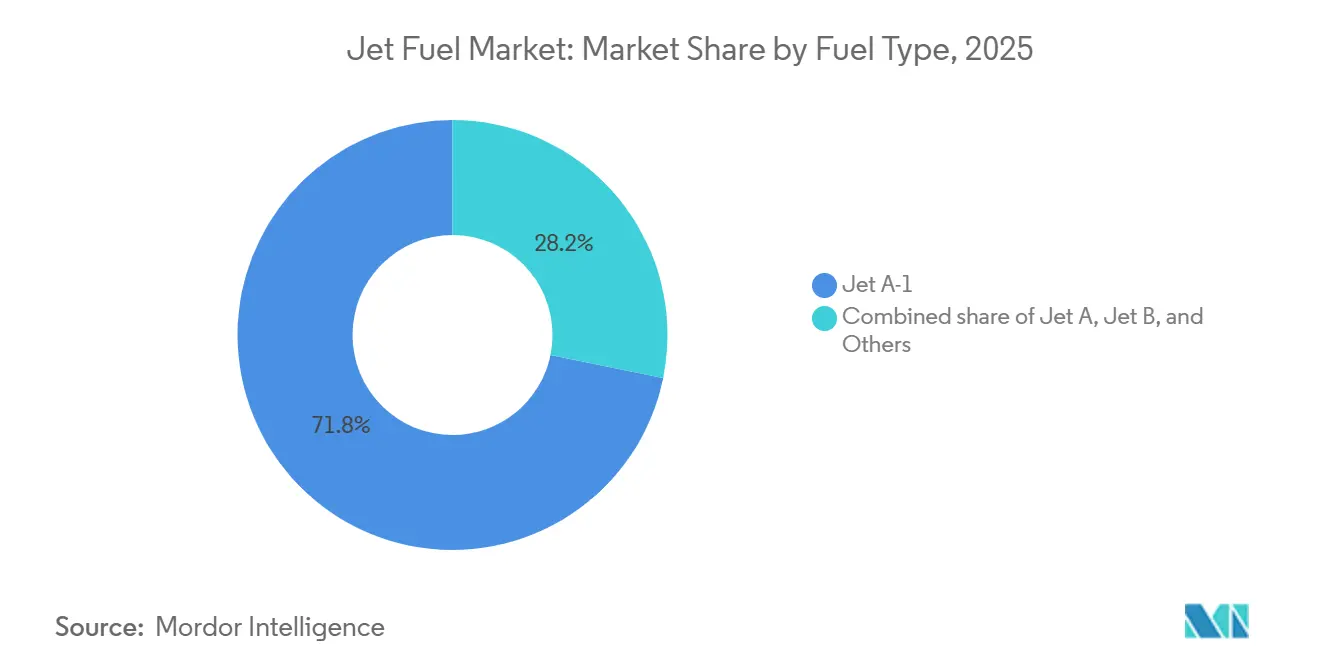

- By fuel type, Jet A-1 held 71.8% of the jet fuel market share in 2025; the “Others” category, led by SAF, is forecast to expand at a 17.4% CAGR through 2031.

- By application, commercial aviation commanded 78.3% of the jet fuel market size in 2025 and is advancing at an 11.1% CAGR to 2031.

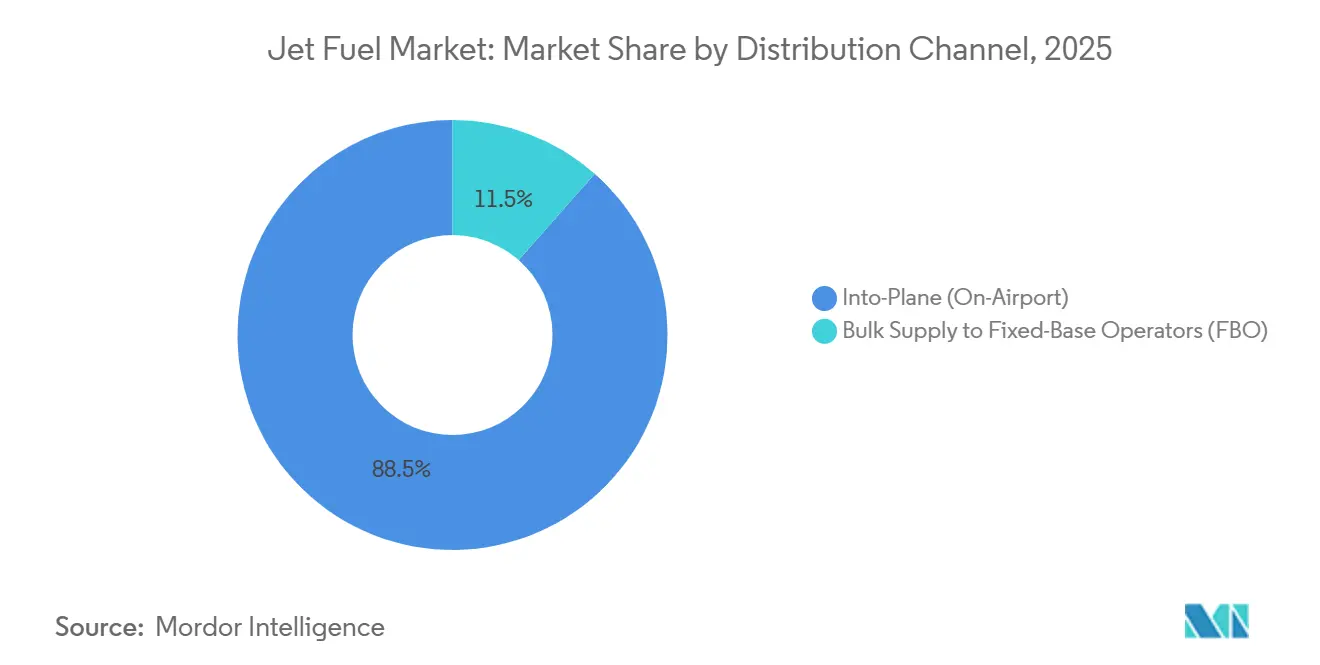

- By distribution channel, into-plane fueling captured 88.5% of the jet fuel market share in 2025, while bulk supply to FBOs posts a lower 8.9% CAGR through 2031.

- By geography, Asia-Pacific held 36.9% of the global jet fuel market share in 2025 and is forecast to grow at an 11.7% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Jet Fuel Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-COVID load-factor rebound lifting Asia Jet A demand | +2.1% | Asia-Pacific core, spillover to Middle East hubs | Short term (≤ 2 years) |

| Expansion of low-cost carriers across Africa & ASEAN | +1.8% | ASEAN, Sub-Saharan Africa, India | Medium term (2–4 years) |

| Surge in wide-body freighter orders on trans-Pacific routes | +1.3% | North America, Asia-Pacific (China, Japan, South Korea) | Medium term (2–4 years) |

| Mega-hub capacity builds and Middle East fuel farm investments | +1.0% | Middle East (UAE, Qatar, Saudi Arabia), connecting traffic to Asia & Europe | Long term (≥ 4 years) |

| Large-scale U.S. & NATO air exercises boosting JP-8 offtake | +0.7% | North America, Europe (NATO member states) | Short term (≤ 2 years) |

| EU 2% SAF blend mandate raising pool volumes via density loss | +0.9% | Europe (EU-27), spillover to UK & Switzerland | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Post-COVID Load-Factor Rebound Lifting Asia Jet A Demand

Asia-Pacific passenger load factors averaged 82.1% in January 2025, a level that obligated carriers to increase flight frequency and deploy larger twin-aisle aircraft, boosting jet fuel market demand.[1]International Air Transport Association, “Air Passenger Market Analysis,” iata.org China’s domestic network recovered to 95% of 2019 capacity by mid-2025, yet international long-haul frequencies stayed 15–20% below pre-pandemic norms, creating latent demand that airlines expect to unlock once visa processing fully normalizes in 2026.[2]Airports Council International, “World Airport Traffic Report,” aci.aero India’s twelve-month passenger growth of 14.2% to March 2025, buoyed by IndiGo’s order for 500 Airbus A320neo-family jets, cements South Asia as a structural growth engine for the jet fuel market. ASEAN low-cost carriers added 87 aircraft in 2024 with high-density layouts that intensify per-turn fuel uplift at primary hubs. Regional passenger traffic is now projected at a 6.3% CAGR to 2028, surpassing the global average and ensuring a double-digit rise in aviation kerosene consumption across India, Bangladesh, and Sri Lanka.

Expansion of Low-Cost Carriers Across Africa & ASEAN

Budget operators in Sub-Saharan Africa and Southeast Asia replicate Southwest Airlines’ single-type, point-to-point playbook but contend with nascent fuel infrastructure. Ethiopian Airlines’ low-cost arm deployed four Boeing 737-800s in 2024 to secondary East-African airports lacking robust hydrant systems, forcing trucked fuel sets that inflate costs by 10–15%. VietJet’s launch of 12 cross-border routes in 2024 under ASEAN open-skies drives episodic fuel shortages, where only one into-plane supplier operates. Boeing forecasts Southeast Asia will require 4,720 new aircraft by 2043, underpinning sustained growth for the jet fuel market. However, in Myanmar, Laos, and Cambodia, limited storage forces carriers to tanker fuel from coastal refineries, compressing the low-cost model’s margin buffer.

Surge in Wide-Body Freighter Orders on Trans-Pacific Routes

Boeing handed over 70 production freighters in 2024, and demand for the 777-8F and Airbus A350F endures as e-commerce reshapes global logistics. FedEx and UPS fleets already exceed 220 dedicated freighters each, and new twin-engine designs burn 15–20% less per tonne-kilometer yet require larger single-sector uplifts owing to extended range. SF Airlines and Cargolux filled order books for 34 Boeing 777-8Fs capable of nonstop Shanghai–Los Angeles lanes that consume up to 100 t of Jet A-1 per trip. IATA’s January 2025 data showed cargo-tonne-kilometers 8.3% higher year on year, with 65% of global freight originating or terminating in Asia-Pacific and North America. Cargo hubs at Anchorage, Memphis, Louisville, and Hong Kong thus lock in durable volume for the jet fuel market.

Mega-Hub Capacity Builds in Middle East Fuel Farm Investments

Dubai International processed 44.9 million travelers in H1 2024 as Emirates’ 260 wide-body fleet uplifted more than 2 million tons of fuel at the airport, ranking it the world’s single largest customer. Qatar Jet Fuel Company added 50 million L of underground storage at Hamad International, enabling simultaneous fueling of 12 Airbus A350-1000s without pressure drops. Saudi Aramco and Saudia invested USD 150 million in a SAF blending terminal targeting 5% blends by 2028, positioning Jeddah as a re-export node to African and South Asian carriers. These expansions safeguard hydrant pressure and inventory, supporting double-digit throughput growth that benefits the jet fuel market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU-ETS Phase IV ticket surcharges curtail leisure flying | -1.4% | Europe (EU-27, UK, Switzerland, Norway) | Short term (≤ 2 years) |

| Fleet renewal toward fuel-efficient aircraft cuts per-flight burn | -1.9% | Global, with fastest adoption in North America, Europe, Asia-Pacific | Medium term (2–4 years) |

| High SAF premium squeezes airline hedging & fuel uplift | -0.8% | Europe, North America (California, Washington), emerging in Asia-Pacific | Medium term (2–4 years) |

| Aromatics-rich crude shortage lowering USGC jet yield | -0.6% | North America (U.S. Gulf Coast refining complex) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EU-ETS Phase IV Ticket Surcharges Curtail Leisure Flying

Phase IV of the EU Emissions Trading System raised carbon prices above EUR 80/t and rescinded free allowances for intra-EU flights, elevating per-sector costs by EUR 700-880 on a London-Barcelona A320neo leg.[3]European Commission, “EU ETS Phase IV Guidelines,” ec.europa.eu Airlines such as Ryanair and easyJet added EUR 5-12 surcharges, and easyJet reported a 4.3% fall in leisure bookings under 1,000 km in Q3 2024. IATA expects a 2-3% annual drop in intra-European passenger-kilometers through 2027, dampening jet fuel market volumes on price-sensitive routes.

Fleet Renewal Toward Fuel-Efficient Aircraft Cuts Per-Flight Burn

The Airbus A320neo saves 20% fuel per seat versus the A320ceo, and Boeing 737 MAX cuts 14–20% against the 737NG, decoupling traffic growth from consumption.[4]Airbus, “Aircraft Characteristics A320 Family,” airbus.com United Airlines’ deployment of 50 MAX 9 jets in 2024 lowered domestic fuel burn by 3.2% despite a 5% seat-mile rise. Fleet retirement cycles imply 40% of today’s 28,000 aircraft will be replaced by 2035, hindering the jet fuel market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fuel Type: SAF Mandates Accelerate “Others” Growth

Jet A-1 retained 71.8% of 2025 volume owing to global standardization outside North America, while Jet A dominates U.S. domestic uplift because its freeze-point, relaxed to −40 °C, suits shorter leg operations. The jet fuel market size for “Others,” comprising TS-1, Jet B, and SAF, is projected to climb at a 17.4% CAGR, the fastest among fuel classes, propelled by binding SAF targets in the EU, UK, and California. Neste’s 1.3 million t Rotterdam expansion and LanzaJet’s 10 million gal Freedom Pines line typify the capital intensity needed to supply mandated volumes.

Market-share growth within the jet fuel industry remains constrained by feedstock scarcity; used cooking oil, tallow, and municipal waste streams cannot yet scale to the multi-million-tonne thresholds regulators envision. Jet B is relegated to extreme-cold markets and faces accelerated retirement as Canadian bush operators modernize fleets. Russia’s TS-1 continues in domestic service, but sanctions freeze technology upgrades, limiting refinery flexibility. CORSIA’s emissions-credit mechanism, nevertheless, should pull an extra 5–8 million t of SAF into circulation by 2030, ensuring the “Others” aggregate captures disproportionate jet fuel market share gains.

By Application: Commercial Dominance versus Defense Resilience

Commercial airlines accounted for 78.3% of 2025 consumption and will sustain an 11.1% CAGR as Asia-Pacific low-cost carriers and Middle East connectors upgauge capacity. Record 82.1% load factors suggest airlines must add frequencies or larger aircraft, both scenarios that lift jet fuel market demand. Defense aviation, representing about 15% of demand, grows at a steadier 7–8% clip; the U.S. Air Force alone took 85 million bbl in FY 2024 as F-35A adoption widens.

General aviation’s 7% slice of the jet fuel market benefits from fractional ownership demand growth of 12–15% flight hours in 2024, yet its disproportionate emissions per passenger attract regulatory scrutiny. The FAA reported increasing adoption of diesel flight-training aircraft that burn Jet A, incrementally lifting segment demand 2–3% annually. Military logistics contracts, often indexed to Brent plus differential, provide a consumption floor when commercial volumes soften, underscoring the application mix’s balancing effect on the jet fuel industry.

By Distribution Channel: Hydrant Infrastructure Consolidates Into-Plane Share

Into-plane fueling supplied 88.5% of world volume in 2025 and is forecast to expand at an 11.0% CAGR during 2026-2031, mirroring hub-airport traffic recovery and airlines’ preference for hydrant-based rapid turns. Dubai, Changi, and Heathrow each dispense 5-8 million t annually through dedicated pipelines, eliminating truck contamination risk and supporting large-scale jet fuel market contracts. Emirates’ USD 6 billion annual Dubai contract showcases oligopolistic supply at mega-hubs, where Shell, BP, and ExxonMobil run joint ventures that bundle SAF options.

Bulk supply to fixed-base operators holds 11.5% share, concentrated at secondary fields where traffic cannot justify hydrants. Signature Flight Support and Atlantic Aviation manage more than 200 U.S. sites but charge 5–10 c/gal mark-ups as storage turns slower. Regional jets’ migration from 50-seat ERJ-145s to 76-seat E175s shifted 15–20% of former FBO volumes into hub hydrant networks, reinforcing in-plane dominance within the jet fuel market.

Geography Analysis

Asia-Pacific commanded 36.9% of 2025 demand and is on track for an 11.7% CAGR through 2031, the fastest worldwide. China’s domestic recovery to 95% of 2019 passenger levels and India’s 14.2% annual traffic surge, propelled by IndiGo’s record 500-aircraft order, anchor regional momentum. ASEAN open-skies lets VietJet and AirAsia add 19 new cross-border sectors in 2024, concentrating fuel uplift where single suppliers control hydrants, boosting regional jet fuel market margins. Japan’s 10% SAF blend goal by 2030 spurs Idemitsu Kosan and ENEOS waste-to-jet investments, positioning the country for possible exports to South Korea and Taiwan.

North America held a roughly 28% share in 2025 and is growing at a 9.2% CAGR through 2031. U.S. consumption of 1.7-1.8 million bpd benefits from trans-Atlantic rebound; United and Delta each logged 18-22% year-on-year international seat-kilometer growth in Q4 2024. Canada’s hub-centric model at Toronto Pearson and Vancouver drives uplift, while Air Canada’s order for 18 Boeing 787-10s lowers per-trip burn 20-25% compared with retiring 767s. Mexico’s 10-12% annual rise ties to nearshoring passenger flows, although limited Pemex refinery investment forces import reliance that tightens jet fuel market supply.

Europe contributed 22% of global demand in 2025, expanding at a slower 8.5% CAGR. EU-ETS surcharges and short-haul rail substitution temper growth, yet density-driven uplift from SAF mandates offsets some volume loss. Heathrow, Charles de Gaulle, and Frankfurt combined moved 12 million t in 2024 through integrated pipelines operated by Shell, BP, TotalEnergies, and ExxonMobil. Ryanair and easyJet carbon add-ons trimmed leisure bookings 4.3% on sub-1,000 km routes, and Russia remains capped at 2019 levels due to sanctions.

The Middle East and Africa share 14% of the demand in 2025. Dubai International’s 44.9 million H1 2024 passengers and Emirates’ 2 million t annual uplift signify enduring hub strength. Qatar Jet Fuel’s 50 million L storage extension secures simultaneous A350 fueling, while Saudi Aramco’s 5% SAF target by 2028 aims at re-export opportunities. Ethiopian Airlines’ route launches into Lusaka and Dar es Salaam highlight Sub-Saharan infrastructure gaps where trucked supply adds 10-15% to costs, yet a 9.5% CAGR through 2031 keeps the jet fuel market attractive. South America’s 6% share concentrates at São Paulo Guarulhos and Rio Galeão, fed by Petrobras Distribuidora pipelines but constrained by slower fleet renewal.

Regulatory Landscape

Sustainable aviation fuel (SAF) blending and emissions-accounting rules are increasingly the binding policy layer for jet-fuel specifications, traceability, and eligible supply. In Europe, ReFuelEU Aviation (Regulation (EU) 2023/2405) applied from 1 January 2025, setting minimum SAF shares for fuel made available at EU airports and formalizing reporting and compliance workflows. EASA reinforced implementation by publishing technical updates to the ReFuelEU Aviation digital reporting tool on 08 April 2026.

Alongside regional mandates, global carbon-accounting alignment is tightening through ICAO CORSIA. In June 2025, the ICAO Council approved amendments covering SAF life cycle assessment (LCA) and indirect land use change (ILUC) values, with updated default values applicable through 31 December 2029. The United Kingdom commenced its SAF mandate in 2025 with an initial 2% obligation for fossil jet fuel supplied, scaling to 10% by 2030 and 22% by 2040, while also signaling pathway governance through a HEFA contribution cap structure in early years. ReFuelEU also embeds a policy review mechanism, including a European Commission consideration by 31 December 2026 on targeted measures addressing carbon leakage and competitive dynamics versus third-country aviation.

Competitive Landscape

The jet fuel market is moderately concentrated: Shell, BP, ExxonMobil, Chevron, and TotalEnergies collectively control near 40% of the into-plane volume at the 50 busiest airports, yet none exceeds 12% global share. Capital-intensive hydrant rights and 5–10-year airline contracts erect barriers, but integrated majors face narrowing margin spreads when crude swings compress refining cracks. Vertical integration lets these firms package fixed-differential pricing, carbon offsets, and SAF blending in single invoices that airlines favor for cost transparency.

Secondary suppliers like Vitol Aviation and World Fuel Services leverage trading agility but lack upstream assets, limiting their ability to hedge price volatility embedded in SAF premiums. Neste’s Rotterdam-scale and LanzaJet’s modular alcohol-to-jet licensing prove nimble specialists can monetize green niches, but the majors approach cautiously. National oil companies, Sinopec, PetroChina, and Indian Oil, retrofit hydrocrackers for 5-10% renewable co-processing, surrendering yield but avoiding greenfield outlay.

Technology plays are accelerating: Shell’s blockchain-based FuelAssure tracking won a 10-year, USD 12 billion exclusive contract at Singapore Changi by certifying end-to-end fuel provenance, a selling point for airlines under tightening ESG audits. Divergent national specifications, Russia’s TS-1 sulfur cap, Japan’s aromatic limits, prevent full commoditization and sustain regional pricing differentials that agile traders exploit to arbitrage the jet fuel market.

Jet Fuel Industry Leaders

Shell PLC

Exxon Mobil Corporation

BP PLC

Chevron Corporation

TotalEnergies SE

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Compliance-led SAF demand and airport fuel logistics upgrades are creating whitespace in certified supply, with book-and-claim style attribute management, plus downstream storage and hydrant distribution. A near-term indicator is the current undersupply in SAF: global SAF production reached 1.9 million tonnes in 2025, roughly 0.6% of global jet fuel consumption. With ReFuelEU Aviation and the UK SAF mandate establishing enforceable minimum SAF shares at airports and for supplied fossil jet fuel, the gap is pulling investment into scalable pathways and traceability infrastructure, including Shell Aviation and partners using the Avelia platform to operationalize SAF environmental-attribute information for corporate buyers.

For conventional jet fuel, the opportunity is more focused on debottlenecking refining and tightening airport-linked distribution to reduce supply tightness and price volatility. ExxonMobil completed the Southampton to London Pipeline project in April 2026, while upgrading facilities at Fawley to increase jet fuel capacity and supply to London airports. In June 2026, Exolum commissioned aviation fuel storage and distribution facilities at Cristiano Ronaldo International Airport (Madeira). In emerging supply hubs, large export-oriented refining and bio-jet investments are moving forward, including Petrobras board approval of the Final Investment Decision in June 2026 for the RPBC Biorefining project in Cubatao (15,000 bpd bio-jet fuel and renewable diesel capacity), along with 2026 steps highlighted around jet fuel export scale and a proposed East African mega-refinery site selection in Lamu, Kenya.

Recent Industry Developments

- June 2026: Shell Catalysts & Technologies signed a technology license agreement with ENGIE to provide Shell XTL1 Process technology (including RWGS and Fischer-Tropsch) for the KerEAUzen e-SAF project in Le Havre, Normandy. The move expands licensed, repeatable e-fuels capability for aviation and supports local European production programs aligned with SAF compliance requirements.

- April 2026: Shell Aviation collaborated with American Express Global Business Travel to extend a long-term corporate agreement with Google for SAF environmental-attribute information using the Avelia platform. This strengthens book-and-claim style procurement at scale, expanding participation beyond physical fuel delivery constraints and connecting corporate demand to airline SAF programs.

- August 2024: BP signed a sustainable aviation fuel deal with China-based Zhejiang Jiaao, as reported by Reuters. The agreement reflects efforts by major operators to secure SAF volumes and diversify supply chains through Asia-based producers amid tightening SAF mandates and traceability requirements.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is counted as the value of jet fuel supplied for aircraft operations, covering conventional turbine fuels (for example Jet A and Jet A-1) and qualifying sustainable aviation fuel blends when they meet jet fuel specifications and are sold for aviation use.

Scope exclusions: We exclude aviation gasoline, non-aviation kerosene uses (such as marine or stationary turbines), carbon-credit instruments, and onboard fuel-management hardware.

Segmentation Overview

- By Fuel Type

- Jet A

- Jet A-1

- Jet B

- Others [TS-1, Sustainable Aviation Fuel (SAF)]

- By Application

- Commercial Aviation

- Defense Aviation

- General Aviation

- By Distribution Channel

- Into-Plane (On-Airport)

- Bulk Supply to Fixed-Base Operators (FBO)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Spain

- Nordic Countries

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Colombia

- Rest of South America

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- Qatar

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building the demand and price context that jet fuel follows closely. We use public aviation traffic and fleet indicators from sources such as ICAO and airport or air-navigation statistics, and fuel price benchmarks from IATA fuel monitoring updates.

Supply-side signals are also tracked so the model stays realistic during refinery or logistics disruptions. Inputs are supported with trade and import-export flows from sources such as UN Comtrade and national customs releases, plus energy balances and refinery output context from sources such as the IEA and EIA. Company filings, investor presentations, and reputable industry press are reviewed to understand capacity changes, fuel-spec shifts, and contract structures. We also use select paid subscriptions for company financials and patent lookups when they help confirm timelines. These sources are used as illustrative inputs, and many other public references are used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to confirm what the desk data cannot show cleanly, especially into-plane pricing behavior, blending practices for sustainable aviation fuel, and how demand varies by route mix and seasonality. We speak with refiners, fuel distributors, airport fueling stakeholders, airline procurement contacts, and sector specialists across APAC, EMEA, and the Americas so assumptions can be checked from more than one viewpoint.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 18% | APAC: 44% |

| Mid tier: 57% | Functional/Unit leaders: 24% | EMEA: 34% |

| Smaller Players: 18% | Managers: 58% | Americas: 22% |

Market-Sizing & Forecasting

Sizing is built using top-down logic where air traffic and fleet activity are converted into a fuel demand pool, then priced to reach a value estimate. To do this, we map indicators such as revenue passenger kilometers and flight departures, active aircraft fleet and utilization trends, typical fuel burn per flight hour, route mix shifts (domestic versus international), and jet fuel benchmark prices with regional spreads.

The totals are then corroborated with selective bottom-up approximations, such as sampled supplier and airport throughput checks, and ASP times volume sense checks from channel discussions. This supports adjustments for gaps where public data is delayed or reported on a different cadence. Forecasting uses scenario analysis with a simple multivariate structure, where future demand is tied to expected air traffic growth, fleet additions, and policy-driven SAF blending, and then reviewed with expert consensus so the final curve remains practical.

Data Validation & Update Cycle

Outputs are validated by comparing modeled consumption and implied prices against independent signals such as aviation activity statistics, refinery output trends, and published jet fuel price monitors. If a region shows an unusual jump, the drivers are re-checked and we may re-contact sources to confirm whether it reflects a real demand change, a price shock, or a timing issue.

Before sign-off, the file goes through stepwise analyst reviews that test formulas, units, and year-over-year movements, followed by variance checks across regions and use cases. The report is refreshed annually, and interim updates are made when material events occur, followed by a final pre-delivery check so clients receive the latest view.

Mordor Intelligence's Jet Fuel Market Size Compared With Other Published Estimates

It is normal to see different market values for jet fuel because publishers do not always count the same fuel scope, the same value point, or the same year assumptions for prices and traffic recovery. The spread also grows when some estimates mix jet fuel with broader aviation fuel categories, or when sustainable aviation fuel is treated as a separate market rather than a blended component.

The biggest gap drivers in this market usually come from what is included in the fuel basket and how the value is defined, such as factory-gate value versus into-plane price paid by aircraft operators, and whether military grades and qualifying SAF blends are counted inside the same total. Differences can also come from using spot prices versus contracted uplift prices, applying one global price curve to all regions, and not refreshing for aviation activity shifts and policy changes, which is why the table below shows meaningful variation, a modeling choice applied by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 195.21 B (2025) | |

| Industry Research Publisher A | USD 212.78 B (2025) | Uses factory-gate value and a broader fuel-type scope that can include alternative aviation fuels beyond kerosene-grade jet fuel, which can lift the total versus an operator-price view. |

| Regional Consultancy B | USD 189.40 B (2024) | Anchors on a different base year and applies a lower growth and price progression path, with SAF treated more as a trend discussion than a consistently priced blended volume in the market total. |

Overall, the spread is mainly explained by value-point selection, year timing, and whether the fuel definition stays tight to certified jet fuel and qualifying blends. When assumptions are tied back to traffic indicators, realistic uplift pricing, and repeatable checks on supply and demand, the estimate becomes easier to audit and update year to year.

Key Questions Answered in the Report

How large is the global jet fuel market in 2026 and what growth is expected by 2031?

The jet fuel market size reached USD 216.59 billion in 2026 and is forecast to expand to USD 354.41 billion by 2031 on a 10.35% CAGR.

Which region leads jet fuel demand growth through 2031?

Asia-Pacific leads, holding 36.9% share in 2025 and expanding at an 11.7% CAGR thanks to traffic rebounds in China, India, and ASEAN.

What impact will SAF mandates have on future fuel volumes?

EU, UK, and California SAF blend rules raise total liters demanded because lower energy density means airlines must uplift extra fuel for the same range.

How are fleet renewals affecting jet fuel consumption?

Next-gen aircraft such as the Airbus A320neo and Boeing 737 MAX cut per-seat burn 14–20%, offsetting part of traffic-driven demand growth.

Who are the major suppliers in the jet fuel market?

Shell, BP, ExxonMobil, Chevron, and TotalEnergies collectively control about 40% of into-plane volume at the world’s busiest airports.

Page last updated on: