Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 341.48 Billion |

| Market Size (2031) | USD 548.71 Billion |

| Growth Rate (2026 - 2031) | 9.95% CAGR |

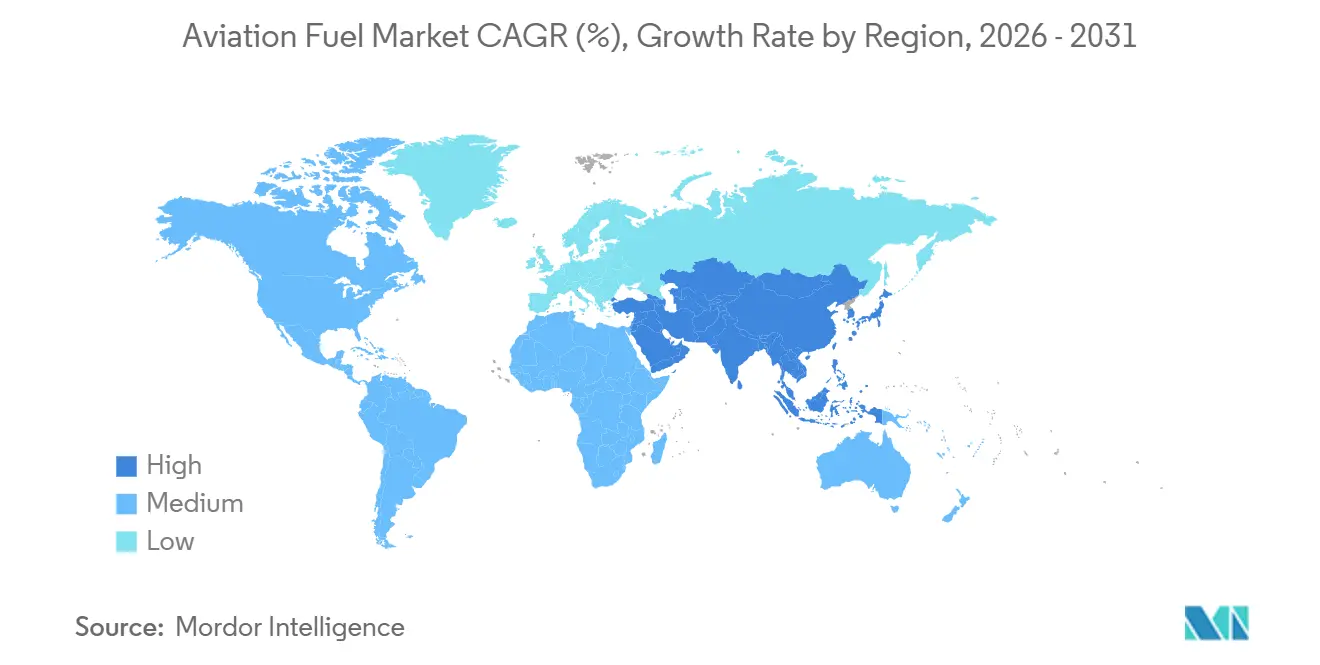

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

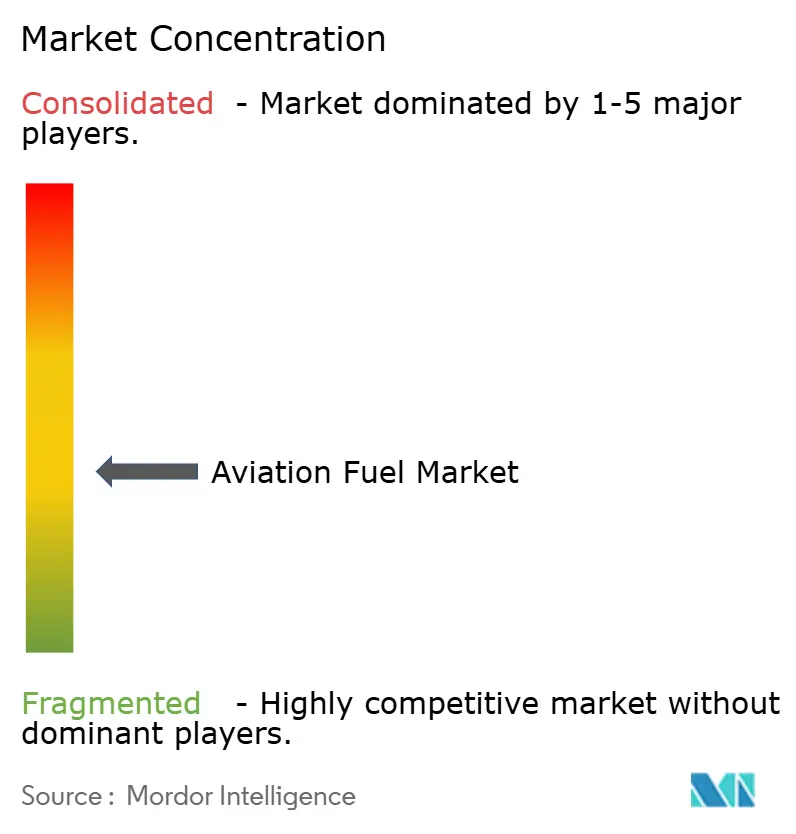

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aviation Fuel Market Analysis by Mordor Intelligence

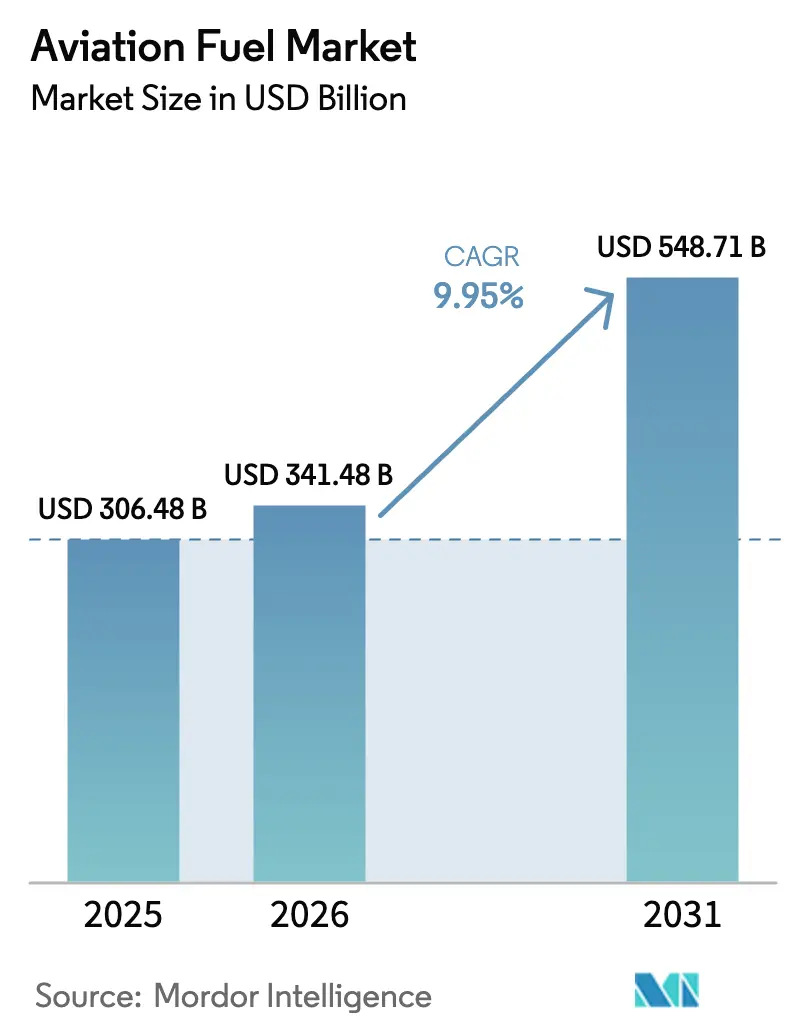

The Aviation Fuel Market size is expected to increase from USD 306.48 billion in 2025 to USD 341.48 billion in 2026 and reach USD 548.71 billion by 2031, growing at a CAGR of 9.95% over 2026-2031.

A rebound in global passenger traffic, rapid e-commerce-led–led air-cargo growth, and intensifying net-zero mandates together propel volume and value, while sustainable aviation fuel (SAF) premiums amplify revenue expansion relative to throughput. Airlines are optimizing load factors, low-cost carriers are widening network footprints, and integrated oil majors are retrofitting hydrotreaters to co-process waste oils, ensuring conventional supply even as SAF penetration rises. Meanwhile, defense modernization cycles and geopolitical tensions lift sortie rates, injecting steady demand from the military segment. Power-to-liquid (PtL) e-kerosene projects poised for startup after 2026 provide a long-run hedge against feedstock scarcity and offer airlines a credible compliance pathway under CORSIA and ReFuelEU Aviation.

Key constraints revolve around volatile crude pricing and SAF feedstock competition with renewable diesel producers, both of which compress refining margins. Engine efficiency gains of 15-20% per seat-mile from LEAP and GTF platforms are tempering incremental volume, yet expanded flight activity offsets per-trip savings. The aviation fuel market, therefore, navigates a structural transition: conventional jet fuel remains the primary volume anchor through the decade, but SAF captures disproportionate value through policy-driven premiums, corporate offtake contracts, and carbon-credit upside. Incumbent refiners that secure reliable waste-lipid supply and accelerate PtL scale-up are positioned to defend share against pure-play SAF entrants, while airports that install dedicated SAF infrastructure early attract wide-body hubs seeking to de-risk compliance exposure.

Key Report Takeaways

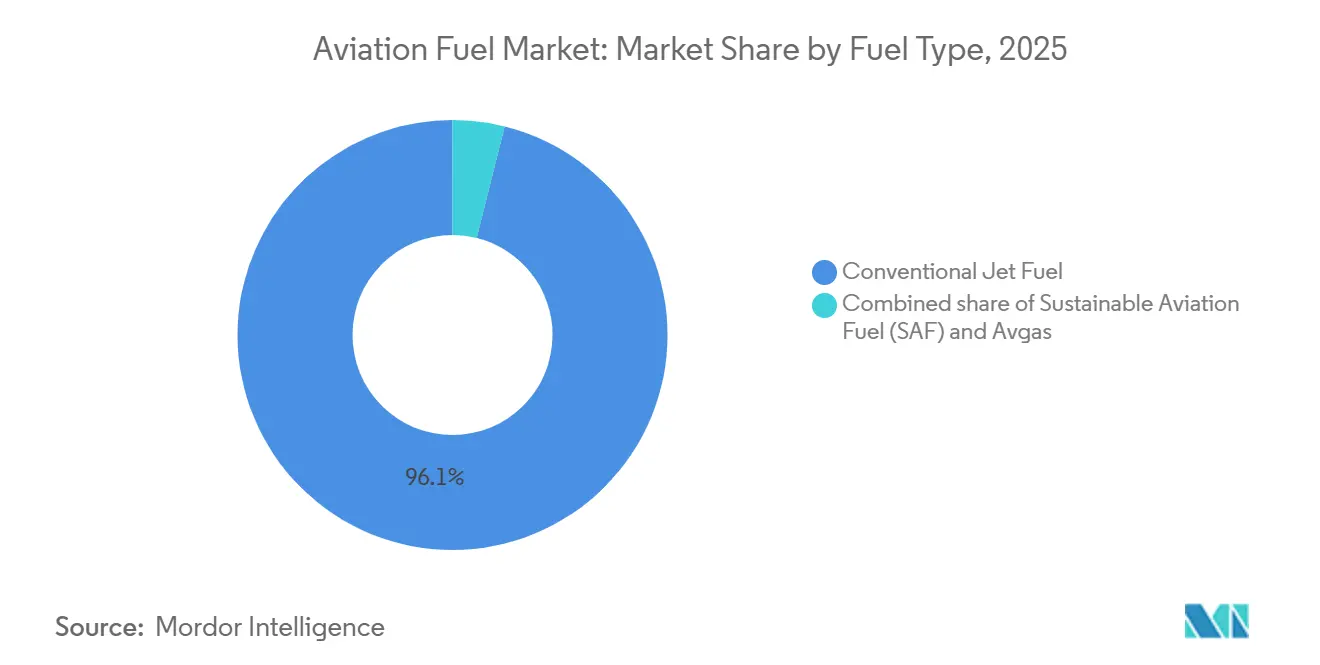

- By fuel type, conventional jet fuel retained a 96.1% aviation fuel market share in 2025, whereas SAF is slated to expand at a 37.0% CAGR through 2031.

- By aircraft type, narrow-body platforms accounted for 60.3% of the aviation fuel market size in 2025, while cargo and freighter operations are on track to grow at a 14.5% CAGR over 2026-2031.

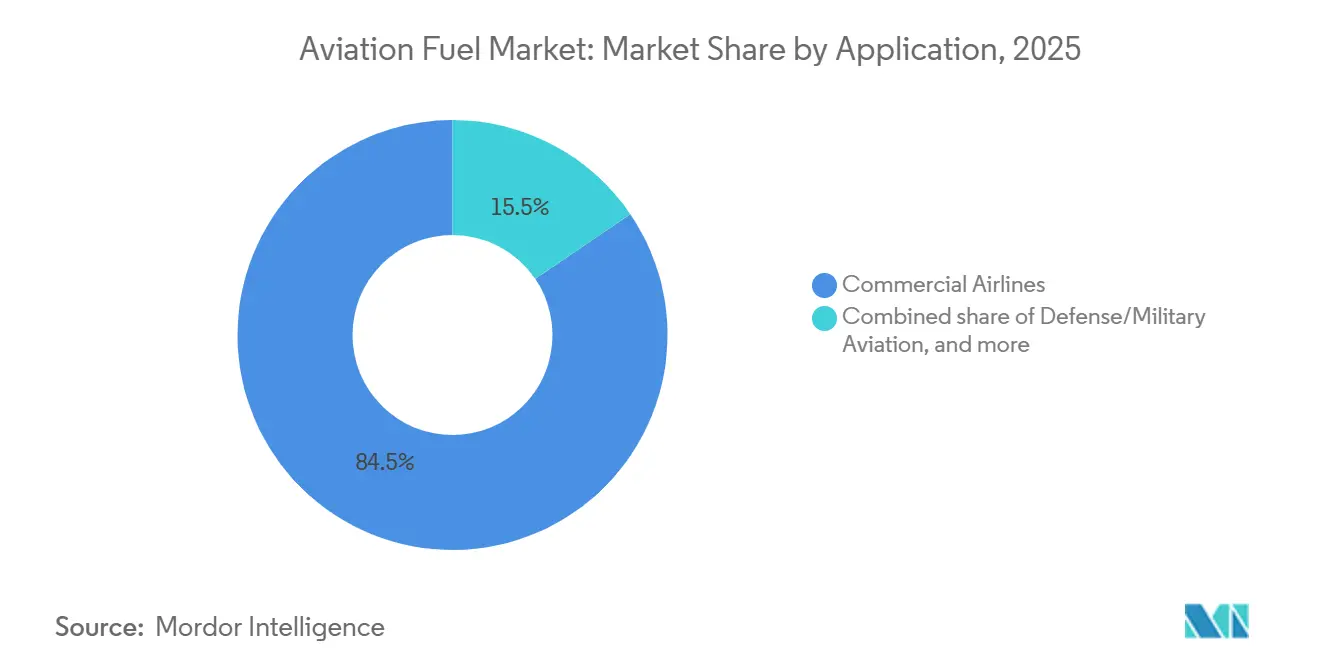

- By application, commercial airlines led with an 84.5% share of the aviation fuel market size in 2025; defense and military aviation exhibits the highest projected CAGR at 13.8% during the forecast window.

- By geography, North America commanded 37.7% of the aviation fuel market share in 2025, whereas Asia-Pacific is forecast to register the fastest growth at a 12.6% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Aviation Fuel Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging post-pandemic passenger traffic recovery | 2.1% | Global, with Asia-Pacific and Middle East leading recovery | Short term (≤ 2 years) |

| Expansion of low-cost carriers in emerging markets | 1.8% | Asia-Pacific core (India, ASEAN), Latin America, Middle East | Medium term (2-4 years) |

| Fleet modernization & delivery of new fuel-efficient aircraft | 1.5% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Rising defense aviation spending worldwide | 1.4% | North America, Europe (NATO members), Asia-Pacific (Indo-Pacific allies) | Long term (≥ 4 years) |

| Booming air-cargo freighter conversions | 1.2% | North America and Asia-Pacific e-commerce hubs, with spill-over to Europe | Medium term (2-4 years) |

| Build-out of power-to-liquid (PtL) e-kerosene capacity | 0.8% | Europe (Norway, Germany) and North America (Chile projects, US Gulf Coast), early-stage global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Post-Pandemic Passenger Traffic Recovery

Passenger enplanements rebounded to 4.7 billion in 2024, equal to the 2019 peak, and IATA projects 8.8 billion by 2040.[1]International Air Transport Association, “Air Passenger Market Analysis 2025,” iata.org Leisure travel returned first, corporate trips later, yet both segments now outstrip pre-crisis levels on many regional routes. Load-factor optimization is intensifying fuel uplift per cycle because fuller cabins translate every additional seat into extra kerosene uplift despite fleet efficiency gains. Asia-Pacific and the Middle East show double-digit demand growth as rising middle-class incomes intersect with liberalized air-service agreements. China alone added over 100 million domestic passengers in 2024, while India crossed the 200 million mark, underpinning continuous refueling demand at secondary airports.[2]Reuters Staff, “Global Traffic Rebounds to Pre-COVID Levels,” reuters.com Point-to-point networks enabled by long-range narrow-bodies disperse fuel demand beyond mega-hubs, reshaping distributor logistics across the aviation fuel market.

Expansion of Low-Cost Carriers in Emerging Markets

Low-cost carriers (LCCs) rose to 35% of global seat capacity in 2024, up from 30% in 2019, capturing share across India, Southeast Asia, and Latin America.[3]Bloomberg News, “Low-Cost Carriers Lift Emerging-Market Seat Capacity,” bloomberg.com IndiGo operated 370 aircraft in 2025 and ordered another 500 A320neo-family jets, ensuring a decade-long fuel-consumption uptrend.[4]Airbus Communications, “Orders and Deliveries 2024,” airbus.com AirAsia, Volaris, and JetSMART emulate the ultra-low-cost template, stimulating new traffic rather than displacing incumbents. LCC aircraft typically fly 12-14 hours daily, outpacing full-service carriers in utilization and thereby sustaining higher daily fuel demand. Open-skies pacts and incentives such as India’s UDAN scheme reduce route-launch friction, letting LCCs penetrate secondary cities where fuel-farm infrastructure remains limited, compelling suppliers to extend into new geographies within the aviation fuel market.

Fleet Modernization and Delivery of Fuel-Efficient Aircraft

Airbus delivered 766 aircraft in 2024, while Boeing’s 2025-2044 outlook calls for 44,000 deliveries, 70% of them single-aisles. LEAP-powered A320neo and 737 MAX jets cut fuel burn up to 20% versus predecessors, yet rising utilization and route expansion dilute net volume savings. Wide-body innovations like the A350 and 787 trim 25% fuel per seat on intercontinental legs, encouraging airlines to retire 777-200ER and A330 aircraft. Lessors accelerate new-tech orders, guaranteeing a steady pipeline regardless of airline balance-sheet health. Engine technology improvements also tighten fuel-quality specs on sulfur and thermal stability, prompting refiners to invest in additional hydrotreating, thereby changing cost structures within the aviation fuel market.

Rising Defense Aviation Spending, Air-Cargo Freighter Conversions, and PtL E-Kerosene Capacity

The U.S. Department of Defense allocated USD 257 billion for operations and maintenance in fiscal 2025, a material slice of which covers jet fuel. Fighter and tanker flight hours have climbed as NATO members hit 2%-of-GDP spending thresholds. Parallel to defense activity, e-commerce demand drives freighter conversions; Boeing redelivered 116 737-800BCF units in 2024 with backlogs stretching past 2027. PtL pioneers like Norsk e-Fuel and HIF Global are building plants that synthesize drop-in kerosene from renewable hydrogen and captured CO₂, targeting over 300,000 tons of annual capacity by 2028. Though early-stage levelized costs exceed USD 3 per liter, falling electrolyzer prices and carbon-credit monetization signal future cost compression, anchoring long-term demand for high-margin fuels across the aviation fuel market.

Restraints Impact Analysis of Aviation Fuel Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile crude-oil price environment | -0.8% | Global, with highest exposure in regions lacking hedging infrastructure | Short term (≤ 2 years) |

| Carbon-pricing & CORSIA compliance costs | -0.6% | Global under CORSIA; Europe faces additional EU ETS burden | Short term (≤ 2 years) |

| SAF feedstock supply bottlenecks | -0.7% | North America and Europe, where mandates exceed feedstock availability | Medium term (2-4 years) |

| Rapid gains in aircraft/engine energy efficiency | -0.9% | Global, with fastest adoption in North America and Europe fleets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Crude-Oil Pricing and Carbon-Pricing/CORSIA Compliance Costs

Brent prices oscillated between USD 70-90 per barrel through 2024-2025, with each USD 10 swing moving airline operating costs by 3-4%. Jet-fuel crack spreads widened as European capacity closed, magnifying price spikes from geopolitical shocks. CORSIA’s pilot phase began in 2024, obligating carriers to buy carbon credits for growth above 2019 baselines at USD 1-3 per ton, set to rise toward USD 20 by 2027. EU ETS exposure further burdens European operators with allowances near EUR 80 per ton (USD 87) in early 2025. Combined fuel and carbon volatility amplifies margin risk, fueling consolidation and spurring airlines to lock in multiyear SAF deals that stabilize the compliance component of the aviation fuel market.

SAF Feedstock Supply Bottlenecks and Rapid Aircraft/Engine Energy-Efficiency Gains

Global SAF output hit 600 million liters in 2024, under 0.2% of total jet-fuel consumption, constrained by waste-lipid scarcity and capital-intensive conversion capacity. HEFA feedstock prices climbed above USD 1,500 per ton as renewable diesel producers competed for the same pool. ReFuelEU mandates 2% SAF blending in 2025, rising sharply to 70% by 2050, while the U.S. Inflation Reduction Act offers tax credits up to USD 1.75 per gallon but does not solve feedstock access. Parallel efficiency gains from LEAP and GTF engines reduce fuel per flight by 15-20%, limiting volume upside even in growth markets. The twin pressures of constrained supply and moderated demand redirect strategy from volume to margin, forcing suppliers within the aviation fuel market to prioritize high-credit, mandate-driven sales channels.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Aviation Fuel Market Segment Analysis

By Fuel Type:

SAF Mandates Reshape Legacy RefiningConventional jet fuel underpinned 96.1% of volume and revenue in 2025, yet tightening mandates drive SAF to a 37.0% CAGR through 2031, the fastest among all sub-segments.[5]European Commission, “ReFuelEU Aviation Regulation 2025,” ec.europa.eu Neste expanded Singapore capacity to 2.2 million tons per year, locking in long-term offtake with multiple European and Asian carriers. U.S. refiners such as ExxonMobil and Phillips 66 are co-processing waste oils to secure early compliance under Inflation Reduction Act credits. Within the aviation fuel market size, SAF’s dollar share overtakes its volumetric share because premium pricing outweighs blended volumes, supporting margin expansion despite feedstock volatility.

The aviation fuel market size attached to Avgaz remains marginal and trends downward as piston-engine fleets age out and unleaded substitutes progress under the FAA’s EAGLE program.[6]Federal Aviation Administration, “EAGLE Initiative Roadmap 2025,” faa.gov Conventional jet fuel remains indispensable throughout the decade due to installed turbine fleets and global pipeline-to-wing infrastructure, yet its incremental growth moderates. PtL e-kerosene and alcohol-to-jet pathways diversify feedstocks beyond lipid-based HEFA, though commercialization hinges on electrolyzer-cost compression, CO₂-capture infrastructure, and clear lifecycle-emission accounting. Suppliers that balance co-processing retrofits with greenfield PtL investments build optionality, positioning to capture the aviation fuel market share redistribution as mandates accelerate post-2030.

By Aircraft Type:

Cargo Freighters Outpace Passenger PlatformsNarrow-body aircraft absorbed 60.3% of fuel in 2025 because flight frequency on short-to-medium-haul routes outweighs individual flight fuel loads. Cargo freighters, forecast at a 14.5% CAGR, represent the most dynamic slice of the aviation fuel market. Express e-commerce models require time-definite delivery, justifying dedicated airlift despite per-ton-kilometer cost premiums. Boeing’s 737-800BCF and Airbus’s A321P2F conversions extend the economic life of passenger airframes while embedding efficient CFM56-7B and V2500 engines, narrowing per-trip operating cost gaps versus new-build freighters.

Wide-body demand is recovering on transpacific and transatlantic corridors, yet utilization remains below 2019 as corporate travel budgets lag. Next-generation 787 and A350 platforms lower per-seat fuel burn, mitigating absolute volume even as sectors lengthen. Regional jets and turboprops carve a niche in thin markets and remote geographies; ATR and Embraer programs now integrate SAF-compatibility certification as standard, signaling anticipated line-fit demand for blended fuels. Overall, the aviation fuel market size linked to cargo segments is set to outrun passenger growth rates through 2031, with Asia-Pacific generating the steepest trajectory thanks to cross-border e-commerce penetration.

By Application:

Defense Modernization Drives Fastest GrowthCommercial airlines dominated 84.5% of the aviation fuel market size in 2025, mirroring the surge to 4.7 billion passenger enplanements. However, defense and military aviation hold the highest projected CAGR at 13.8% through 2031 as NATO expansion, Indo-Pacific deterrence, and fleet modernization escalate flight hours. F-35, KC-46, and next-gen tanker deployments increase per-sortie fuel draw relative to legacy fleets, translating budget allocations directly into uplift volumes.

General and business aviation remains a premium niche with limited elasticity to fuel prices; Gulfstream’s G800 and Bombardier’s Global 7500 emphasize range and cabin experience, yet incremental fuel demand is capped by fleet size. The U.S. Air Force’s 2024 certification of 100% drop-in SAF proves technical feasibility for military turbines, suggesting that defense demand might catalyze scale-up of high-blend or neat SAF supply chains. Consequently, the aviation fuel market balances civilian volume dominance with defense-driven growth velocity, underpinning a diversified demand profile across the forecast horizon.

Geography Analysis

North America Aviation Fuel Market

North America accounted for 37.7% of global demand in 2025, supported by hub-and-spoke structures, a large general-aviation fleet, and early SAF tax incentives. Integrated majors such as Chevron and Phillips 66 will add more than 500 million gallons of SAF capacity by 2027 through refinery retrofits, anchoring regional supply. Canadian northern-route optimization and Mexican LCC expansion together add incremental uplift, while NextGen air-traffic management trims per-flight fuel burn yet fails to offset aggregate volume tied to rising flight numbers. The aviation fuel market benefits from stable policy, accessible feedstocks, and mature logistics, sustaining moderate growth despite fleet efficiency gains.

APAC Aviation Fuel Market

Asia-Pacific is expected to register a 12.6% CAGR, the fastest regional expansion, as China’s airport-construction spree and India’s domestic boom widen the fuel-demand base. ASEAN liberalization lets carriers open secondary city pairs, decentralizing supply chains and multiplying refueling points. Japan and South Korea focus on SAF R&D and hydrogen demonstrations, hoping to export technology while tackling domestic carbon caps. Australia’s ultra-long-haul plans, such as Qantas Project Sunrise, reinforce demand for high-energy-density fuels, including SAF blends. This diversity of growth engines cements Asia-Pacific as the pivotal contributor to the incremental aviation fuel market size during the outlook period.

EMEA and South America Aviation Fuel Market

Europe operates under the strictest decarbonization regime; ReFuelEU Aviation sets a 2% SAF mandate in 2025, rising steeply thereafter, compelling refiners and airports to build blending and storage infrastructure. Carbon prices above USD 80 per ton accelerate legacy fleet retirements and drive airlines toward long-term SAF contracts with Neste and LanzaJet. The Middle East continues hub-centric expansion; Emirates, Qatar Airways, and Etihad each grow wide-body capacity, while ADNOC invests in SAF capacity to reinforce the UAE’s hub status. South America recovers alongside Brazil’s domestic market, yet wrestles with infrastructure gaps and currency volatility. Africa remains under-penetrated; Ethiopian Airlines leads intra-continental expansion, prompting localized fuel-farm investments. Collectively, these dynamics shape a multipolar aviation fuel market in which policy, capital intensity, and traffic trends vary sharply by region.

Regulatory Landscape

Aviation fuel regulation is increasingly framed around lifecycle-emissions accounting, SAF blending obligations, and standardized reporting across global and regional schemes. ICAO continues to operationalize CORSIA during its first phase (2024-2026), including requirements for states to submit aggregated CO2 emissions data and CORSIA Eligible Fuels information via the CORSIA Central Registry, with the 2025 reporting-year submission due by 31 July 2026. In March 2026, the ICAO Council approved updates to its guidance on policy measures for SAF development and deployment, and it refreshed verifier training content to better address emission-reduction claims linked to CORSIA Eligible Fuels.

Europe is tightening supplier-side obligations through ReFuelEU Aviation (Regulation (EU) 2023/2405), which has applied since 2025 and requires minimum SAF availability at Union airports. This is already shaping blending, logistics, and traceability requirements for fuel suppliers. Switzerland adopted ReFuelEU Aviation from 1 January 2026 for suppliers serving Zurich and Geneva airports, extending alignment beyond the EU. In the United Kingdom, the Sustainable Aviation Fuel Act 2026 received Royal Assent on 5 March 2026 and introduced a revenue-certainty mechanism for SAF producers, including powers to levy aviation fuel suppliers to fund the program, while the UK SAF Mandate applies to fuel passing the duty point from 1 January 2026 through 31 December 2026.

Competitive Landscape

Integrated oil majors, ExxonMobil, Shell, BP, Chevron, TotalEnergies, maintain end-to-end control from refining to wingtip delivery across most major hubs, giving them scale synergies in the aviation fuel market. However, SAF’s emergence fragments competition: Neste, LanzaJet, and Gevo secure premium offtake agreements that bypass traditional suppliers. Airlines such as United and Delta take equity stakes in SAF producers, capturing margin and supply security. National oil companies, notably ADNOC and Indian Oil Corporation, deploy sovereign capital to add regional storage and SAF lines, defending domestic supply chains against import volatility.

Technology differentiation becomes critical; PtL developers owning proprietary catalysts and high-temperature electrolyzer IP can lock in early-mover premiums. Refiners unable to procure waste-lipid feedstocks face margin compression as renewable diesel competes for the same inputs. Volume risk shifts to distributors as engine efficiency trims per-trip consumption, compelling them to diversify into higher-margin services, such as into-plane fueling and fuel-quality analytics. Overall, the aviation fuel market’s competitive landscape rewards asset-heavy incumbents that adapt quickly and specialized newcomers that solve policy-driven pain points, particularly around lifecycle-carbon verification and feedstock traceability.

Aviation Fuel Industry Leaders

Exxon Mobil Corporation

Shell plc

BP plc

Chevron Corporation

TotalEnergies SE

- *Disclaimer: Major Players sorted in no particular order

Aviation Fuel Market Companies Covered in this Report

- Exxon Mobil Corporation

- Shell plc

- BP plc (Air BP)

- Chevron Corporation

- TotalEnergies SE (Air Total)

- Gazprom Neft PJSC

- Phillips 66

- Valero Energy Corporation

- Abu Dhabi National Oil Company (ADNOC)

- Emirates National Oil Company

- Indian Oil Corporation Ltd

- Bharat Petroleum Corp Ltd

- World Fuel Services Corp

- Vitol Aviation

- Neste Oyj

- LanzaJet Inc.

- Gevo Inc.

- Honeywell UOP

- Red Rock Biofuels LLC

- Swedish Biofuels AB

- Allied Aviation Services Inc.

Market Opportunities and Future Outlook

SAF scaling remains the main commercial whitespace as mandates expand faster than near-term supply, which lifts the value of certified low-carbon volumes and the supporting services needed for verification. In 2026, global SAF production is around 2.4 million tonnes, about 0.8% of annual jet fuel consumption, leaving a large gap between policy targets and physical availability. The gap creates room for refiners and independent producers to add HEFA and alcohol-to-jet capacity, while airlines and corporate buyers increasingly use long-tenor offtakes to underwrite projects, including Loganair and ClimaHtech Green Flight announcing a 15-year bio-SAF and e-SAF offtake arrangement in May 2026.

More activity is also emerging around attribute-based procurement models that reduce reliance on physical delivery constraints at specific airports. In April 2026, DSV collaborated with Microsoft, United Airlines, and Phillips 66 to secure 11 million gallons of SAF for a book-and-claim program, and in June 2026 American Airlines and Google agreed to unlock 35 million gallons over three years, broadening demand signals beyond airlines. Over the longer term, technology pathways are widening the opportunity set: in July 2026 Airbus and MTU Aero Engines announced a joint venture to develop fully electric hydrogen fuel cell engines. In parallel, hydrogen combustion and fuel-cell testing milestones reported in 2026 point to continued work that could reshape future fuel specifications, airport energy infrastructure, and the competitive mix across liquid jet fuel, SAF, and emerging low-carbon propulsion options.

Recent Industry Developments in Aviation Fuel Market

- July 2026: Bharat Petroleum Corporation Ltd. (BPCL) signed an MoU with Akasa Air to create a framework for supplying SAF-blended aviation turbine fuel in India and disclosed investment plans for a 61-kilotonnes-per-annum SAF production facility at its Mumbai Refinery. The airline supply alignment combined with a supply-side capital commitment supports domestic availability and can accelerate adoption at Indian airports where blending and logistics are still developing.

- June 2026: Shell Catalysts & Technologies signed a technology license agreement with ENGIE for the KerEAUzen e-SAF project in France, using Shell XTL process technology to produce synthetic aviation fuel from captured biogenic CO2 and green hydrogen. Licensing helps replicate conversion capability beyond Shell-owned assets and supports the power-to-liquid build-out needed for higher-blend mandates.

- September 2024: TotalEnergies signed a long-term agreement with Air France-KLM to supply up to 1.5 million tons of sustainable aviation fuel over a 10-year period ending in 2035. Multi-year offtake volumes at this scale provide demand certainty for producers and encourage investment in dedicated SAF production and airport distribution infrastructure in Europe.

Aviation Fuel Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the aviation fuel market covers revenues linked to fuels used to power aircraft operations worldwide, across civil and defense usage, and across main airport and off-airport supply points.

Scope exclusions: It excludes aircraft lubricants, in-flight consumables, and non-aviation refinery outputs that are not sold as aviation fuel.

Segments Covered in This Report

- By Fuel Type

- Conventional Jet Fuel

- Sustainable Aviation Fuel (SAF)

- Avgas

- By Aircraft Type

- Narrow-body

- Wide-body

- Regional Jets and Turboprops

- Cargo/Freighters

- By Application

- Commercial Airlines

- Defense/Military Aviation

- General and Business Aviation

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- NORDIC Countries

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Australia and New Zealand

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Chile

- Rest of South America

- Middle East and Aafrica

- Saudi Arabia

- United Arab Emirates

- South Africa

- Egypt

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to build the base structure of the model and to keep assumptions tied to verifiable aviation activity. We referenced public aviation traffic and operations statistics such as those from ICAO, IATA, FAA, and Eurostat, along with energy and fuel market indicators from sources such as the IEA and the US EIA.

On the supply and policy side, we reviewed airport and airline sustainability disclosures, government SAF policy notes, and trade and customs statistics where jet fuel movements are visible (imports and exports by product codes). Company filings, investor presentations, and reputable press were also used to understand capacity additions, fuel procurement trends, and pricing pass-through patterns. For select cross-checks, we used paid subscriptions for company financials and intelligence, news and financials, and an import and export shipment-level database. The examples above are illustrative and not exhaustive, and we also consulted other public and paid sources for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and short surveys with participants across the aviation fuel value chain, including refiners and blenders, distributors, airport fuel service providers, airlines, and fleet operators. Respondent input from APAC, EMEA, and the Americas was used to confirm how consumption rebounds after demand swings, how SAF blending trajectories are paced in practice, and how pricing assumptions flow through at the distributor and airport service-provider stages. We then used those answers to close gaps where public statistics lagged or used different definitions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 14% | APAC: 49% |

| Mid tier: 59% | Functional/Unit leaders: 31% | EMEA: 30% |

| Smaller Players: 15% | Managers: 55% | Americas: 21% |

Market-Sizing & Forecasting

Market sizing was built using a top-down and bottom-up logic where global and regional flight activity and fuel-use intensity were used to reconstruct demand, which was then translated into value using observed pricing ranges. When the model was being finalized, selective bottom-up approximations were used as a check, including sampled airport throughput comparisons, supplier and distributor channel checks, and simple volume times average selling price tests, to ensure totals stayed realistic.

Key inputs used in the model include available seat kilometers and passenger traffic recovery indicators, flight departures by region, typical fuel burn per flight hour by aircraft category, SAF blending and mandate timelines, and jet fuel and avgas pricing trends by region and currency timing. Where a data series was missing for a smaller country or an airport cluster, we used proxy variables such as traffic share and route mix to fill the gap, then rechecked the results with interview feedback.

For forecasting, scenario analysis was used to reflect different paths for passenger demand, cargo strength, and SAF adoption, followed by smoothing of year-to-year transitions so the output does not swing unrealistically. Assumptions on fleet utilization, fuel efficiency improvements, and policy-led SAF penetration were reviewed with primary respondents before final forecasts were locked.

Data Validation & Update Cycle

Validation was done by comparing the model output with independent signals such as air traffic recovery, regional jet fuel price movements, and broad refinery and middle-distillate market indicators, and then checking that implied consumption per flight stayed within realistic bands. If a region showed an unexpected jump, we revisited the drivers, rechecked the conversion steps, and re-contacted sources when the variance could not be explained through published data.

Before sign-off, the work goes through multiple analyst reviews so scope, units, and currency treatment stay consistent across all geographies. Reports are refreshed annually, and interim updates are triggered when there are material events such as major demand shocks, policy changes on SAF mandates, or large refinery and supply disruptions. Right before delivery, a fresh pass is done so clients receive the latest updated view.

Mordor Intelligence's Global Aviation Fuel Market Market Estimate Compared With Other Published Estimates

Published market sizes for aviation fuel can look far apart even when they are driven by similar travel and fleet trends, because the underlying counting rules are not always the same. Differences usually come from which fuel products are included, whether values are captured at the point of final sale into aviation versus earlier in the supply chain, and how quickly pricing and traffic inputs are refreshed.

By checking regional jet fuel and avgas price timing and the recovery in flight departures, Mordor Intelligence keeps the estimate tied to aviation consumption and avoids pulling in adjacent middle-distillate value pools that sit outside the aviation fuel market. Another gap driver is SAF treatment, since some estimates count neat SAF only while others include blended volumes at different effective prices, which changes totals quickly. Currency conversion timing and the base-year price deck also matter in a market where value can move sharply even if volumes shift modestly.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 306.48 B (2025) | |

| Trade Publisher A | USD 264.83 B (2025) | Uses a factory-gate style market value concept and often bundles related services, which can understate value captured at airport distribution points and at the final fuel sale step into aviation operators. |

| Global Consultancy B | USD 473.20 B (2025) | Appears to apply a broader value boundary and a higher base-year price deck in 2025, which can inflate totals if wholesale-to-retail markups, taxes, or adjacent fuel revenue elements are counted more than once. |

The spread in the table is mainly explained by how value is defined along the supply chain and how base-year pricing is set during volatile jet fuel cycles. When the scope is kept to aviation fuel sold into aircraft operations and cross-checked against traffic and fuel-intensity signals, the resulting number is easier for us to trace and repeat year to year.

Key Questions Answered in the Report

What is the projected value of the aviation fuel market in 2031?

The aviation fuel market size is expected to reach USD 548.71 billion by 2031, reflecting a 9.95% CAGR from 2026.

Which fuel type is growing fastest within global aviation?

Sustainable aviation fuel is forecast to expand at a 37.0% CAGR through 2031 as mandates and corporate commitments take effect.

Which region will post the highest growth in aviation fuel demand?

Asia-Pacific shows the steepest trajectory, with a 12.6% CAGR driven by China's airport expansion and India's domestic traffic surge.

How significant is cargo activity for aviation fuel suppliers?

Cargo and freighter operations are set to grow at 14.5% annually, outpacing passenger segments and offering premium pricing opportunities.

What are the main risks to aviation fuel supply growth?

Key risks include volatile crude pricing, carbon-compliance costs, and limited SAF feedstock availability amid competing renewable diesel demand.

Page last updated on: