Seed Coating Ingredients Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

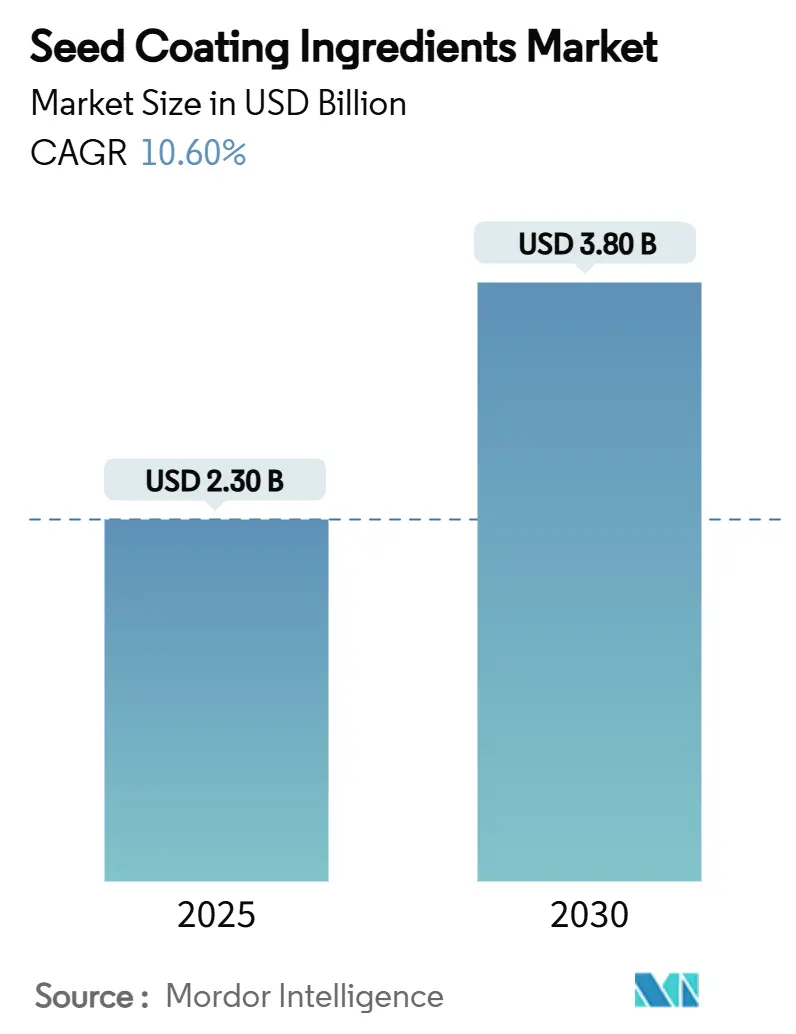

| Market Size (2025) | USD 2.30 Billion |

| Market Size (2030) | USD 3.80 Billion |

| Growth Rate (2025 - 2030) | 10.60% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Seed Coating Ingredients Market Analysis by Mordor Intelligence

The seed coating ingredients market size reached USD 2.3 billion in 2025 and is forecast to reach USD 3.8 billion by 2030, advancing at a CAGR of 10.6% during 2025-2030. Robust seed technology investments, tighter residue-level rules, and the need to improve field-level seedling vigor continue to steer demand for specialized coating ingredients. Capital inflows toward advanced multi-layer polymers enhance coating functionality while bio-derived carriers help growers comply with lower synthetic chemical thresholds. Financial incentives for climate-smart agriculture intensify adoption among hybrid vegetable and specialty crop producers. Meanwhile, precision planters with automated dosing units bolster usage rates by guaranteeing accurate seed-to-ingredient ratios and by curbing wastage.

Key Report Takeaways

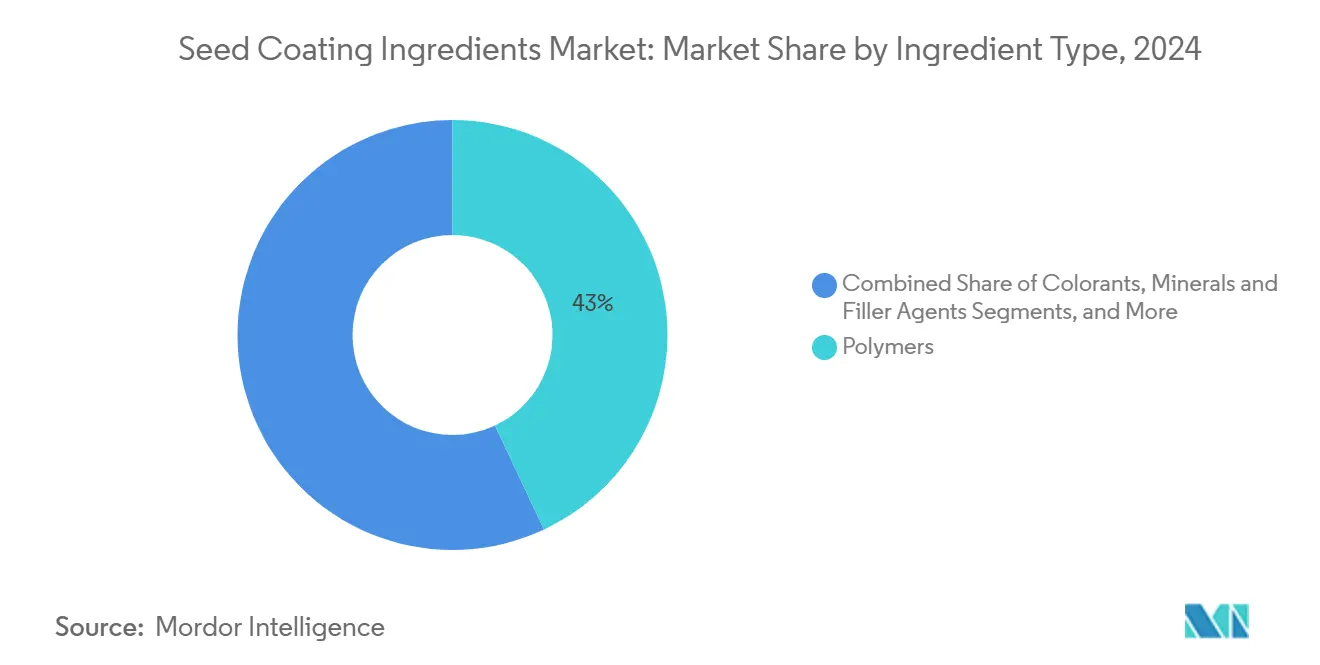

- By ingredient type, polymers led with 43.0% of the seed coating ingredients market share in 2025 biologicals are projected to post a 13.4% CAGR through 2030.

- By coating formulation, film coating accounted for 48.5% of the seed coating ingredients market size in 2025, whereas multi-layer advanced formulations will expand at a 14.2% CAGR between 2025-2030.

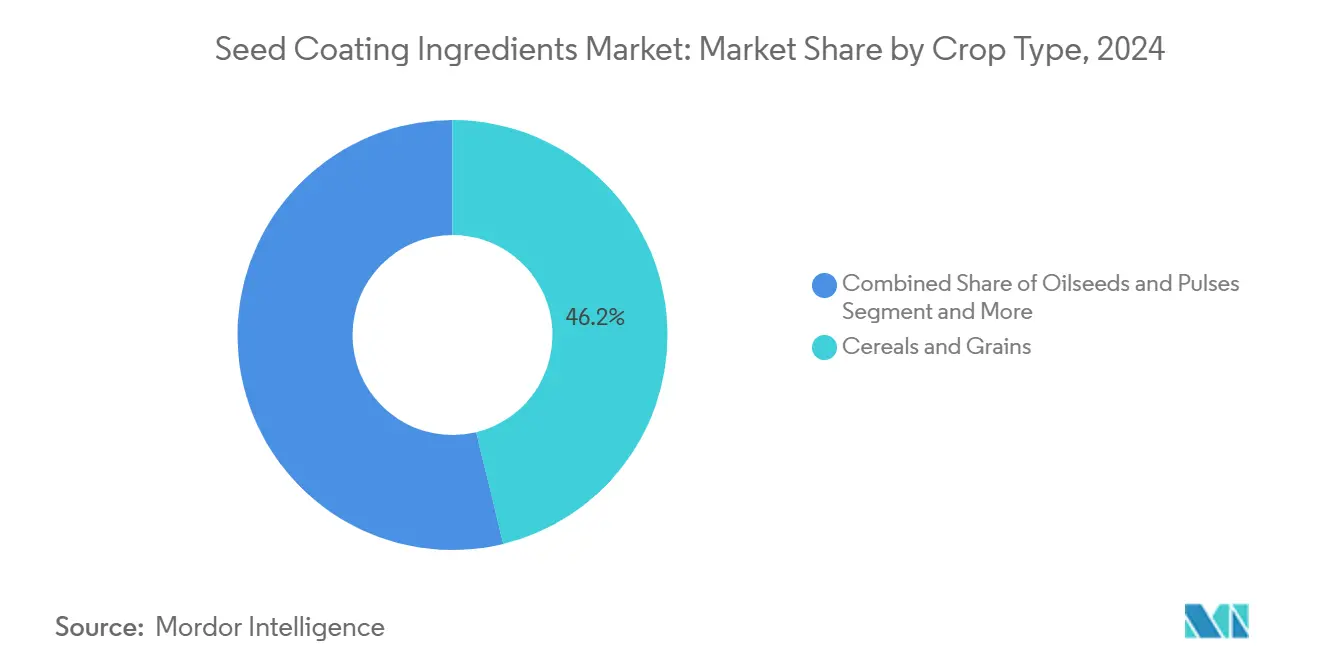

- By crop type, cereals and grains held 46.2% revenue share in 2025 fruits and vegetables are set to register a 12.8% CAGR to 2030.

- By function, protection captured 51.0% of the seed coating ingredients market share in 2025, while enhancement is forecast to progress at a 14.6% CAGR during 2025-2030.

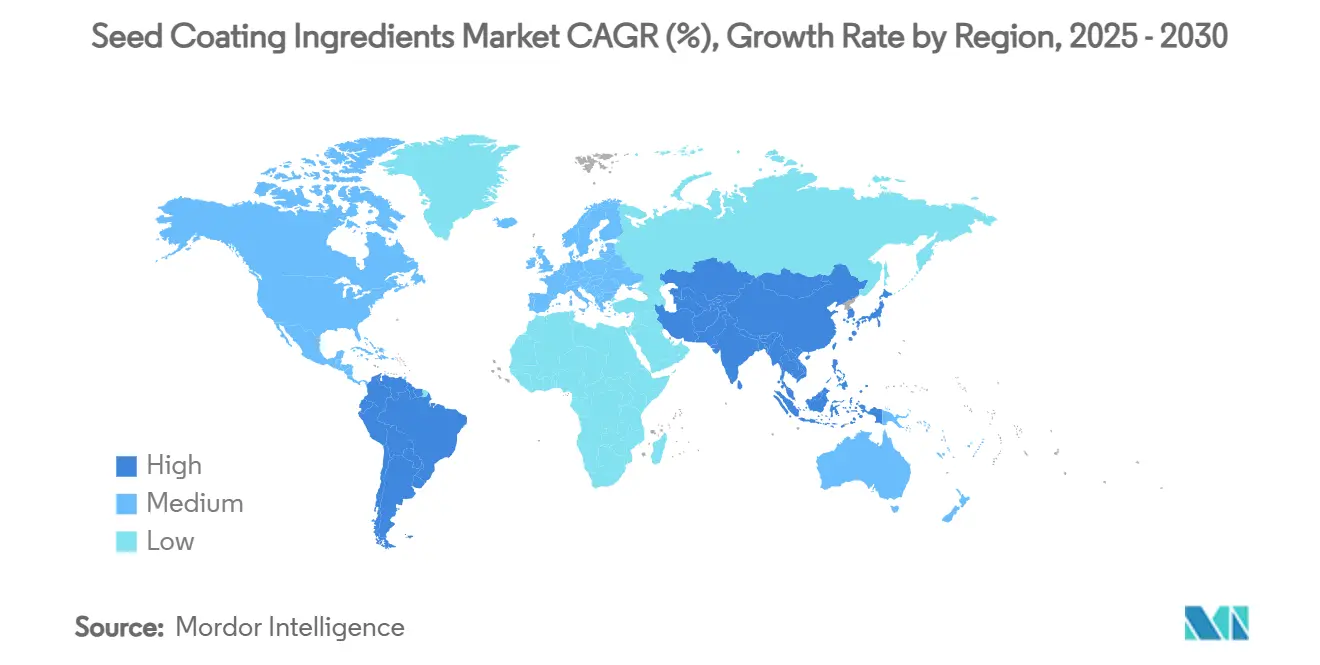

- By geography, Asia-Pacific is the largest region with a market share of 30.8%, and it is also the fastest with 12.1% CAGR.

Global Seed Coating Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainability push for reduced agro-chemical inputs | +2.1% | Global, with strongest impact in Europe and North America | Medium term (2-4 years) |

| Rising adoption of precision planting equipment | +1.8% | North America and Europe core, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Demand for biological inoculant integration | +1.6% | Global, with early adoption in South America and Asia-Pacific | Medium term (2-4 years) |

| Growth of hybrid vegetable and specialty seeds | +1.4% | Asia-Pacific core, spill-over to North America and Europe | Long term (≥ 4 years) |

| Accelerated regulatory approvals for micro-polymers | +1.2% | North America and Europe, expanding globally | Short term (≤ 2 years) |

| R&D tax incentives for novel coating technologies | +0.9% | United States, Brazil, and India with national focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sustainability Push for Reduced Agro-chemical Inputs

European and North American regulators now enforce stringent active-ingredient cutbacks that prompt seed companies to migrate to lower-volume delivery systems. Film and multi-layer coatings that host micronized actives comply with residue-level rules, reducing field applications and overall carbon footprints. Incentive programs under the European Union Green Deal reward growers for adopting bio-based polymers, which deliver controlled release of inoculants and micronutrients. Parallel mandates in Canada and selected United States states have tightened emission caps on seed treatment plants, strengthening the commercial case for compliant coatings. Collectively, these policy levers heighten long-run procurement of sustainable carrier chemistries.

Rising Adoption of Precision Planting Equipment

Digital planters equipped with variable-rate meters enable accurate dispensing of coated seeds, minimizing skips and doubles across the seedbed. Equipment vendors collaborate with coating ingredient suppliers to calibrate polymer viscosity and surface tension for seamless passage through high-speed vacuum disks. North American and Australian growers report 5% reductions in seeding rates after switching to precision planters, freeing budget for premium ingredient blends. Regional pilot projects funded by agriculture ministries demonstrate yield upticks when uniform seed spacing is paired with functional coatings. This equipment-driven usage boost manifests in medium-term volume gains for specialty polymers and colorants.

Demand for Biological Inoculants Integration

Rhizobial and mycorrhizal formulations embedded in seed coatings deliver early-stage root colonization that improves phosphorus and nitrogen uptake. South American soybean growers incorporate biological carriers to comply with limits on chemical seed dressings set by national health agencies. Ingredient vendors introduce encapsulation matrices that maintain microbial viability for more than 12 months under tropical temperatures, addressing previous shelf-life barriers. European horticulture firms adopt similar inoculant carriers to support organic-certified seedlings, driving incremental sales of biopolymers. The aggregate pull for microbial compatibility strengthens medium-term market momentum.

Growth of Hybrid Vegetable and Specialty Seeds

Seed houses increase production of hybrid tomato, cucumber, and chili cultivars tailored for protected cultivation. These high-value seeds demand multi-layer coatings for property preservation, including abrasion resistance and visual differentiation. Chinese protected-farming clusters show double-digit growth in hybrid adoption, and commercial nurseries in the Gulf region follow similar paths to counter arid-zone stresses. Specialty segments, such as turfgrass and ornamentals, also adopt breathable polymer forms that modulate moisture uptake. Heightened production of high-value seeds thereby injects near-term demand for advanced seed coating ingredients.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent residue-level limits in Europe | -1.8% | Europe core, with regulatory spillover to North America and Asia-Pacific | Short term (≤ 2 years) |

| Volatile prices of high-grade biopolymers | -1.4% | Global, with particular impact on premium segments in North America and Europe | Medium term (2-4 years) |

| Limited field data on multi-layer formulations | -1.2% | Global, with strongest impact in North America and Asia-Pacific | Medium term (2-4 years) |

| Channel resistance from traditional seed distributors | -1.0% | South America core, with significant impact in emerging markets across Asia-Pacific and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stringent Residue-level Limits in Europe

Revised Maximum Residue Levels for several fungicidal actives demand extensive reformulation of coating recipes. Compliance costs escalate as ingredient suppliers must conduct fresh toxicological dossiers and re-engineer polymer matrices. Seed companies temporarily defer coating upgrades while awaiting clear guidance on updated thresholds, slowing procurement cycles in the region. Certification audits under the Sustainable Use Regulation also impose testing fees that squeeze smaller regional coaters. These procedural burdens impede mid-term European demand despite positive sustainability intent.

Volatile Prices of High-grade Biopolymers

Supply disruptions in carrageenan, alginate, and cellulose derivative feedstocks raise average input prices by 18% between 2024 and 2025. Chinese polysaccharide processors grapple with energy curbs that restrict output, while Scandinavian pulp mills face higher freight charges. Ingredient buyers without long-term contracts experience spot-price surges, limiting inventory restocking. Though polymer makers pass partial costs to seed companies, end-user price sensitivity caps overall invoice growth. This volatility places short-term stress on profitability for both formulators and distributors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient Type: Polymers Dominate while Biologicals Accelerate

Polymers commanded 43.0% of the seed coating ingredients market size in 2024, driven by their versatility across grain and vegetable crops. Vinyl acetate ethylene, polyvinyl alcohol, and acrylic copolymers ensure strong adhesion and rapid drying that suit high-speed treating lines. Their longer field record and compatibility with diverse actives sustain top-line share. The biological sub-segment, encompassing carriers for beneficial microbes and botanical extracts, records the fastest 13.4% CAGR through 2030 as pressure for residue-free farming intensifies. Regional certification bodies in South America and Europe endorse microbial coatings for soil health enhancement, prompting incremental investment in fermentation facilities.

Innovations accelerate biological penetration. Encapsulated Bacillus strains in alginate beads withstand mechanical stress during pneumatic planting, bridging a past performance gap versus synthetic polymers. Joint development agreements between biological producers and seed companies shorten registration timeframes. Cost parity trends emerge because carbon-tax-adjusted prices for petro-derived polymers inch upward, narrowing the premium for biopolymers. These shifts widen adoption in fruits, vegetables, and pulses, fortifying long-term volume gains for biological carriers in the seed coating ingredients market.

By Coating Formulation: Film Types Lead but Multi-layer Variants Surge

Film coatings represented 48.5% of the seed coating ingredients market share in 2024, owing to their established processing lines and lower material usage. They deliver color differentiation, minimal dust, and thin-layer protection suitable for cereals, soybeans, and cotton. However, multi-layer advanced coatings show a 14.2% CAGR to 2030 as growers seek multifunctional benefits. Layered architectures segregate micronutrients from microbial inoculants, preventing antagonistic interactions while ensuring staged release. Precision seeders can handle these bulkier seeds without singulation issues, widening compatibility.

R&D roadmaps highlight moisture-responsive outer layers paired with core polymer binders that unlock nutrients under field conditions. Asia-Pacific rice breeders adapt multi-layer technology to deliver zinc and silicon boosters against abiotic stress. Though per-unit cost runs 12% above film coatings, yield gains and input savings validate the premium. Consequently, advanced formulations progressively displace traditional films in high-margin hybrid seed categories, raising both value and volume contributions to the seed coating ingredients market.

By Crop Type: Cereals And Grains Remain Pivotal while Fruits And Vegetables Gain Pace

Cereals and grains held 46.2% revenue share in 2024, reflecting large corn, wheat, and rice acreages that consistently adopt polymer and colorant coatings for mechanized planting. Seed majors embed systemic fungicides plus micronutrients within single-layer films, ensuring broad coverage across extensive farm operations. Government seed-quality schemes in India and China further institutionalize coating prescriptions in certified cereal seed supply chains, reinforcing segment dominance.

Fruits and vegetables exhibit a 12.8% CAGR during 2025-2030 as greenhouse and protected cropping expand in Asia-Pacific and the Middle East. High-value seeds of tomato, pepper, cucumber, and leafy greens justify costlier multi-layer coatings integrating growth promoters and biostimulants. Color coding and pelletizing aid automated transplanting systems, reducing labor costs in hydroponic nurseries. As consumer diets tilt toward nutrient-dense produce, commercial seed suppliers respond with coated specialty hybrids, raising the segment’s proportional lift within the seed coating ingredients market.

By Function: Protection Leads while Enhancement Outpaces

Protection-oriented coatings, which house fungicides, insecticides, and nematicides, commanded 51.0% of the seed coating ingredients market share in 2024. Disease-prone geographies such as Brazil and parts of Sub-Saharan Africa rely on these actives to secure early stand establishment. Strong regulatory scrutiny along with active-ingredient phase-outs in Europe drives continual reformulation, yet the protection function persists due to the agronomic necessity to curb soil-borne pathogens.

Enhancement-focused coatings, delivering micronutrients, plant growth regulators, and biostimulants, expand at a 14.6% CAGR through 2030. They mitigate abiotic stresses like drought and salinity, aligning with climate adaptation strategies. National crop-insurance schemes in Australia and the United States recognize these enhancements within carbon-smart crop packages, providing partial premium rebates. As a result, ingredient suppliers position integrated nutrient-plus-biological solutions to widen enhancement uptake across diverse crop portfolios.

Geography Analysis

Asia-Pacific contributed the largest share of 30.8% to revenue in 2024 and is projected to clock a 12.1% CAGR through 2030. China, India, and Australia scale up precision planting acreage, backed by subsidy programs that reimburse up to 30% of equipment costs [1]Source: Ministry of Agriculture and Rural Affairs China, “Mechanization Subsidy Scheme 2024,” moa.gov.cn. Domestic polymer plants in Jiangsu province guarantee price stability for local seed treaters, motivating higher inclusion rates. Rising protected horticulture in China and Japan boosts demand for multi-layer coatings with micronutrient boosters, amplifying regional uptake.

South America showcased a growth outlook, led by Brazil’s soybean corridor expansions across Mato Grosso and Pará. Seed technologists integrate rhizobial inoculants into coatings to comply with MAPA rules limiting on-farm liquid inoculation volumes [2]Source: Ministry of Agriculture Brazil, “Inoculant Regulations for Soybean Seeds,” agricultura.gov.br. Argentine corn growers adopt film-formers with cold-start polymers that improve germination under early-spring sowing, adding incremental volume. Chilean fruit exporters favor enhancement coatings loaded with trace elements to secure uniform orchard establishment under water-constrained conditions.

North America and Europe represent mature yet steady markets. North America shows mid-single-digit growth as United States seed firms push advanced biological carriers for regenerative farming packages. Canadian canola producers adopt low-dust colorants that satisfy transport regulations and maintain grain-handling safety standards [3]Source: Government of Canada, “Transportation of Agricultural Dusts Guidelines,” canada.ca . Europe faces lower growth given residue constraints, yet demand for bio-derived ingredients rises. The seed coating ingredients market size within Germany and France benefits from Horizon Europe grants supporting bio-polymer R&D. Eastern Europe, particularly Poland and Romania, grows faster due to the modernization of cereal seed infrastructure.

Competitive Landscape

The top five companies, BASF SE, Clariant, Croda, Solvay, and Sensient Technologies Corporation, held a significant combined share of global revenue in 2024, underscoring a moderately concentrated structure. BASF SE leads through a broad portfolio of polymer binders and continuous-flow film-coating lines. Clariant strengthens its position in colorants and flow-improvers by opening a USD 35 million capacity expansion in Germany in 2024. Croda pivots to bio-based carriers by integrating Algae-derived lipids into enhancement coatings. DSM-Firmenich pushes nutritive micro-encapsulates that carry zinc and boron for horticultural seeds.

Strategic alliances shape technology pipelines. In 2024, BASF SE and a Japanese equipment manufacturer co-developed a smart-coating module that links polymer viscosity data to real-time drum speed adjustments, thereby improving coating uniformity. In the same year, Clariant licensed a United States start-up’s nano-silica platform to formulate moisture barriers for paddy rice. Investments in South America remain prominent. Croda inaugurated a biologics competence center in São Paulo to localize microbial carrier development for soybean coatings.

Portfolio diversification toward biologicals intensifies. BASF SE filed patents for enzymatic polymer degradation to ensure end-of-life residue breakdown, anticipating stricter disposal norms. Across the seed coating ingredients market, these moves reflect a pivot from commodity film-formers to specialty multi-functional systems that command premium pricing and widen customer lock-in.

Seed Coating Ingredients Industry Leaders

Croda International plc

Solvay

Sensient Technologies Corporation

Clariant

BASF SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: The ICAR-Indian Institute of Oilseeds Research (IIOR) signed a memorandum of understanding with Kurnool Seeds Pvt. Ltd. and Cynora Crop Science Pvt. Ltd. to commercialize its patented biopolymer-based seed coating technology. This technology protects nutrient-mobilizing microbes during seed treatment, increasing crop yields by 25% to 30%.

- June 2024: Syngenta Group initiated seed processing at its Enkhuizen facility in the Netherlands, focusing on small-seeded vegetables such as peppers and tomatoes. The company aims to eliminate microplastics from all European seed processing operations by the end of the year, transitioning to 100% biodegradable seed coatings to reduce environmental impact.

- October 2023: In Canada, Corteva Agriscience introduced Straxa, a fungicide seed treatment that provides farmers with a ready-to-use formulation to control major seed and soil-borne diseases in cereal crops.

Global Seed Coating Ingredients Market Report Scope

| Polymers |

| Colorants |

| Minerals and Filler Agents |

| Biologicals (Inoculants, Biostimulants) |

| Film Coating |

| Encrusting |

| Pelleting |

| Multi-layer Advanced |

| Cereals and Grains |

| Oilseeds and Pulses |

| Fruits and Vegetables |

| Turf and Ornamentals |

| Protection (Fungicide, Insecticide) |

| Nutrition (Micronutrients) |

| Enhancement (Growth Promoters) |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Ingredient Type | Polymers | |

| Colorants | ||

| Minerals and Filler Agents | ||

| Biologicals (Inoculants, Biostimulants) | ||

| By Coating Formulation | Film Coating | |

| Encrusting | ||

| Pelleting | ||

| Multi-layer Advanced | ||

| By Crop Type | Cereals and Grains | |

| Oilseeds and Pulses | ||

| Fruits and Vegetables | ||

| Turf and Ornamentals | ||

| By Function | Protection (Fungicide, Insecticide) | |

| Nutrition (Micronutrients) | ||

| Enhancement (Growth Promoters) | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the forecast value for the Seed Coating Ingredients Market by 2030?

The market is projected to reach USD 3.8 billion by 2030.

Which ingredient type currently holds the largest share?

Polymer binders lead with 43.0% share.

Which formulation is anticipated to grow fastest?

Multi-layer advanced coatings will expand at a 14.2% CAGR through 2030.

Why are biological carriers gaining traction?

Regulatory limits on chemical residues and demand for soil health benefits drive adoption of microbial carriers.

Which region shows the strongest growth outlook?

Asia-Pacific is forecast to advance at a 12.1% CAGR due to mechanization subsidies and protected farming expansion.

How concentrated is the competitive landscape?

The top five suppliers hold 54% of revenue, indicating moderate concentration with active innovation competition.

Page last updated on: