Agricultural Coatings Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

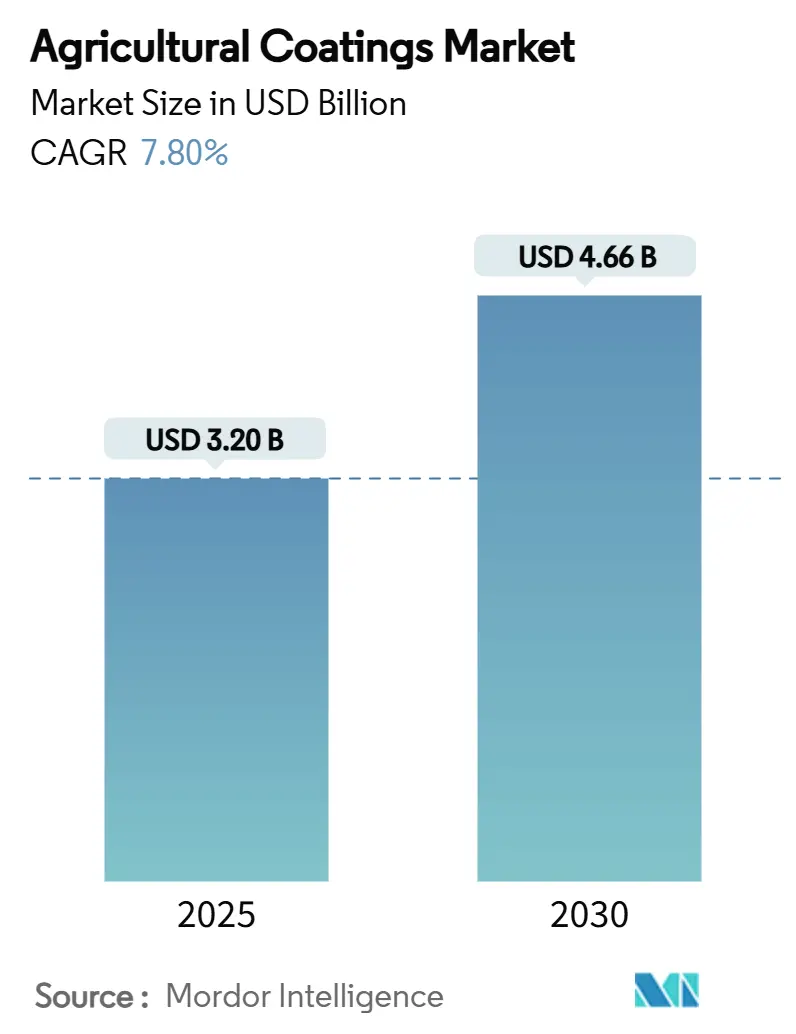

| Market Size (2025) | USD 3.20 Billion |

| Market Size (2030) | USD 4.66 Billion |

| Growth Rate (2025 - 2030) | 7.80% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agricultural Coatings Market Analysis by Mordor Intelligence

The agricultural coatings market size stands at USD 3.2 billion in 2025 and is projected to reach USD 4.66 billion by 2030, advancing at a 7.8% CAGR. Rising pressure to boost resource efficiency, tighter environmental rules, and precision farming adoption are steering demand. Biodegradable polymers, micro-encapsulation, and sensor-responsive release systems are synchronizing nutrient delivery with crop needs, cutting runoff, and maximizing yields. Early commercial successes in microplastic-free seed coatings signal a broad shift toward sustainable inputs, while precision application tools shorten payback periods for coating investments. Strategic alliances between chemical majors and ag-tech startups are accelerating product development timelines and expanding geographic reach.

Key Report Takeaways

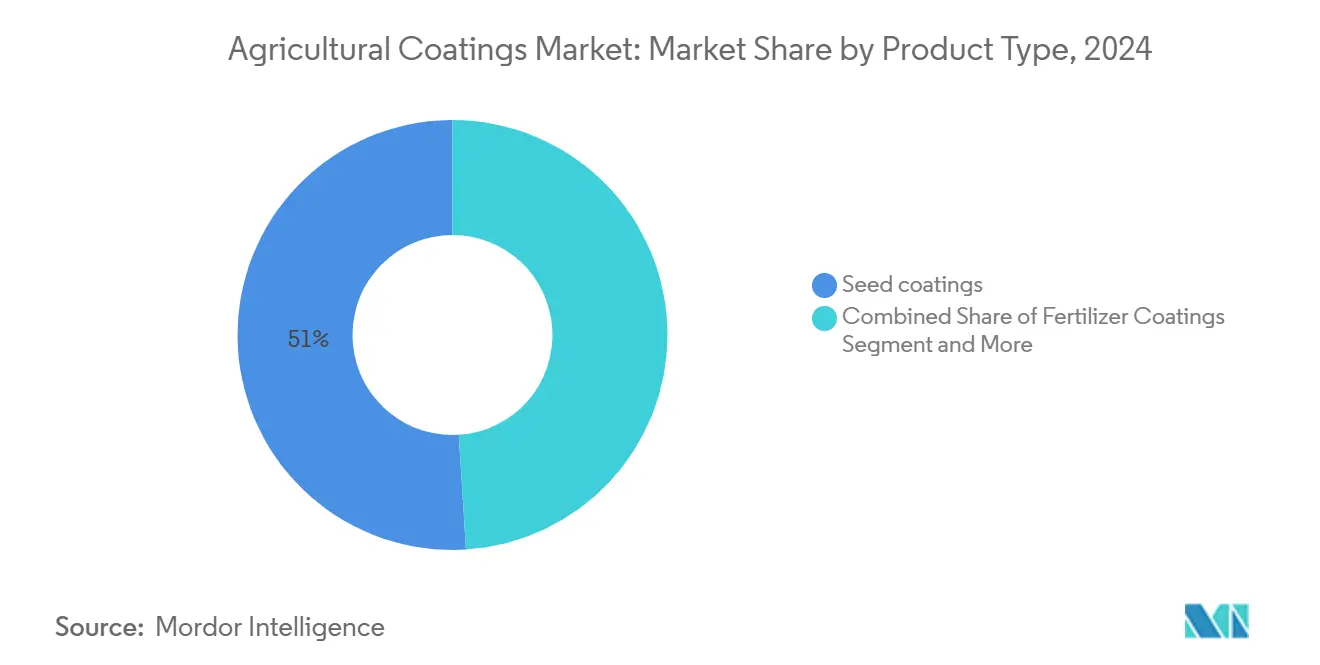

- By product type, seed coatings accounted for 51% of the agricultural coatings market share in 2024, and biodegradable seed coatings are projected to expand at a 11.2% CAGR through 2030.

- By formulation, liquid systems led with 60.2% revenue share in 2024, while micro-encapsulated formulations are projected to grow at 9.7% CAGR to 2030.

- By geography, North America contributed 34.8% of the agricultural coatings market in 2024, while the Asia-Pacific region is poised for the fastest growth, with a 10.0% CAGR through 2030.

- By application method, spray systems commanded a 45.5% share in 2024, and on-farm seed treaters are projected to advance at a 10.2% CAGR to 2030.

- By function, controlled-release nutrition accounted for 55.4% of the agricultural coatings market size in 2024, with seed protection functions projected to grow at a 11.3% CAGR through 2030.

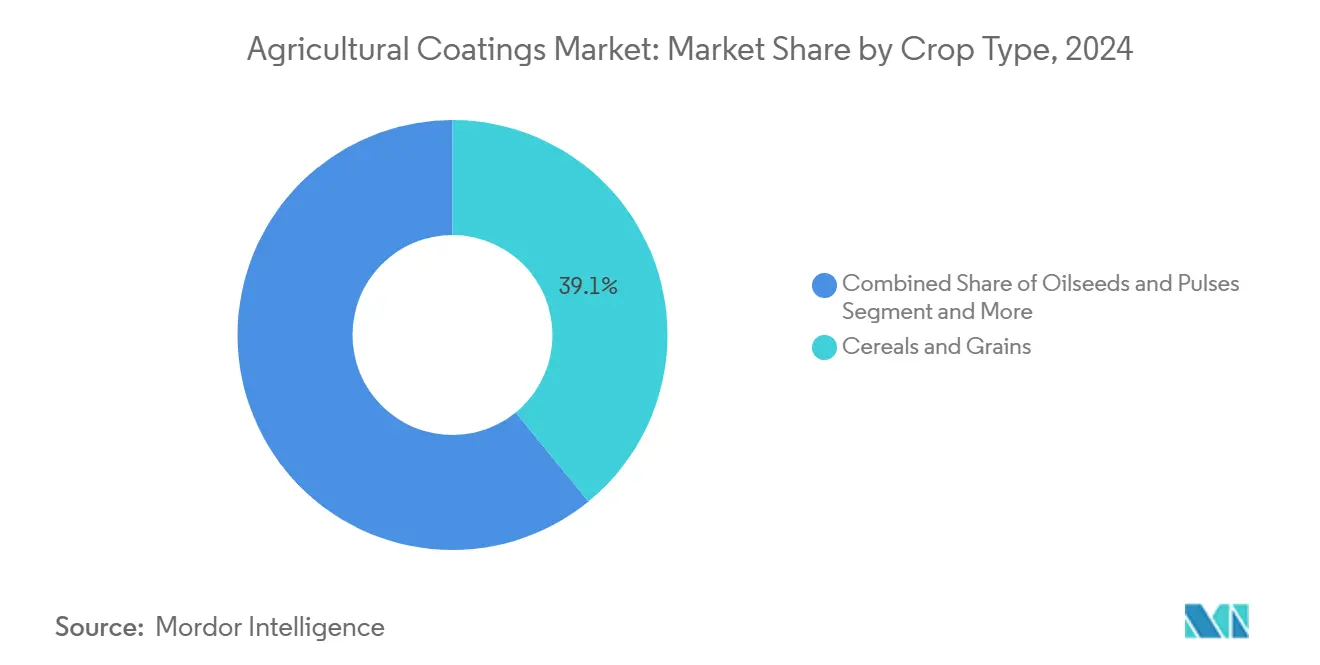

- By crop type, cereals and grains led with a 39.1% share of the agricultural coatings market size in 2024, fruits and vegetables are set to expand at a 9.3% CAGR to 2030.

- The top five companies held 48% of global sales in 2024 of agricultural coatings market share.

Global Agricultural Coatings Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of precision agriculture tools | +1.2% | Global, with North America and Europe leading | Medium term (2-4 years) |

| Rising demand for controlled-release fertilizers | +1.5% | Global, particularly Asia-Pacific and North America | Long term (≥ 4 years) |

| Shift toward biodegradable agro-inputs | +1.8% | Europe is leading, expanding to North America and Asia | Medium term (2-4 years) |

| Regulatory push for reduced agrochemical run-off | +1.1% | Europe and North America, spreading globally | Long term (≥ 4 years) |

| Growth in high-value horticulture crops | +0.9% | Global, concentrated in Asia-Pacific and North America | Medium term (2-4 years) |

| Expansion of seed-treatment capacity in emerging markets | +1.3% | Asia-Pacific, Middle East, and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Precision Agriculture Tools

Smart implements that vary coating rates by zone are showing 20% wheat yield gains and a 10–20% reduction in pesticide use in large United States field trials. BASF and Agmatix co-developed an AI sensor that identifies hot spots for soybean cyst nematodes, protecting approximately USD 1.5 billion in annual yield. Such integrations prompt coating makers to engineer formulations that are compatible with variable-rate nozzles and sensor feedback loops. North America and Western Europe remain launch pads, yet Asia-Pacific growers are quickly embracing low-cost drone sprayers. As capital costs decline, the agricultural coatings market is poised to scale precision-ready products across mid-sized farms.

Rising Demand for Controlled-Release Fertilizers

Polymer-coated granules now supply nutrients for 336 hours, compared with 96 hours for conventional urea, slashing leaching in sandy soils[1]Source: Journal of Agricultural and Food Chemistry, “Extended nutrient release study,” acs.org. Canada’s pledge to curb fertilizer greenhouse gases by 30% by 2030 funnels grants to firms such as Sulvaris, which secured CAD 2.3 million (USD 2.5 million) to advance carbon-based coatings. In Asia-Pacific, rice producers adopting sulfur-coated urea recorded 12% yield lifts and 18% nitrous-oxide cuts. These field outcomes solidify controlled-release nutrition as the performance anchor of the agricultural coatings market.

Shift Toward Biodegradable Agro-Inputs

The European Union REACH Regulation 2023/2055 bans polymer microparticles with a concentration≥0.01% by weight in farm products by 2028[2]Source: European Commission, “REACH restriction on intentionally added microplastics,” europa.eu. Lucent BioSciences responded with Nutreos, a cellulose-based micronutrient coating poised for plants on four continents. Plant-oil polyurethane films now match petroleum coatings for durability, yet fully degrade in soil within 230 days. Seed majors like Incotec are commercializing microplastic-free lines for cereals ahead of regulatory deadlines, advancing the agricultural coatings market toward a polymer-neutral footprint.

Regulatory Push for Reduced Agrochemical Run-Off

The EU targets a 50% pesticide drop by 2030 and has tightened residue limits on neonicotinoids, spurring encapsulation solutions that cut leaching by 45% in corn trials. The United States EPA exempted certain siloxane polymers from tolerance thresholds, signaling acceptance of safer coating matrices[3]Source: Federal Register, “Tetraethoxysilane polymer tolerance exemption,” federalregister.gov. China’s updated pesticide law ties food-safety inspections to input usage, elevating demand for coatings that prove lower drift. Regulatory harmonization is likely to amplify the agricultural coatings market’s pivot to eco-engineered formulations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited farmer awareness in developing nations | -0.8% | Asia-Pacific, Africa, and South America | Medium term (2-4 years) |

| Price sensitivity of smallholder farmers | -0.6% | Global, particularly in emerging markets | Long term (≥ 4 years) |

| Stringent product-registration timelines | -0.4% | Global, with varying regional intensity | Long term (≥ 4 years) |

| Technical challenges in multi-layer coating uniformity | -0.3% | Global manufacturing and quality control | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Farmer Awareness in Developing Nations

Smallholders often depend on informal networks, leaving advanced coatings outside their decision set. Surveys of Kenyan maize growers showed only 27% recognized seed-applied biologicals despite 15% yield advantages. Without extension agents or demo plots, uptake lags even when products are in local supply chains. Multinationals are piloting radio tutorials and village-level field days to address the gap, but scaling such programs requires coordinated public-private funding that remains patchy.

Price Sensitivity of Smallholder Farmers

Upfront coating costs can run 8–12% higher than untreated seed, a hurdle when credit is scarce. BASF’s 0% APR financing for fungicides and 1.99% APR on seed aims to bridge cashflow gaps. Researchers in the Philippines are turning coconut husk fiber into low-cost carriers, trimming per-hectare coating spend by 20% yet preserving efficacy. Success will hinge on localizing raw materials and lowering entry-level pack sizes to meet subsistence-farm budgets, or the agricultural coatings market risks missing the largest grower segment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Biodegradable Innovation Drives Market Evolution

Seed coatings dominated revenue with a 51% share in 2024, underscoring their role in uniform emergence and early-season protection within the agricultural coatings market. Demand is magnified by precision planters that require seeds with consistent size, weight, and flow properties. Fertilizer coatings follow, propelled by growers’ need to align nutrient release with crop uptake and regulatory nitrate caps. Biodegradable seed coatings are pacing growth at an 11.2% CAGR, catalyzed by EU microplastic bans and retailer sustainability pledges. The agricultural coatings market size for biodegradable variants is forecast to climb sharply as companies retrofit factories for plant-based polymers. Post-harvest produce films remain niche but lucrative, delivering price premiums in specialty fruit exports.

Pesticide coatings occupy a smaller share yet hold strategic importance in integrated pest management programs. Natural resin barriers that slow active-ingredient release are registering double-digit gains among orchardists aiming to extend spray intervals. Concurrently, research into nano-structured chitosan films for strawberries showed 28% decay reduction during transit. Such breakthroughs validate the broader shift of the agricultural coatings industry toward multifunctional, residue-reducing formulations.

By Formulation: Liquid Dominance Challenged by Micro-encapsulation

Liquid products controlled 60.2% of 2024 sales, favored for ease of tank-mixing and widespread sprayer compatibility inside the agricultural coatings market. They deliver strong adhesion and can carry higher active loads, aligning with fast-moving planting windows. Yet micro-encapsulated systems are expanding at a 9.7% CAGR, due to precise dose delivery and enhanced shelf stability. The agricultural coatings market size for micro-encapsulation is on track to reach USD 1.1 billion by 2030, buoyed by venture funding into biodegradable shell technologies. Powder forms hold steady demand in cereals, where dry on-farm treaters dominate.

Emerging hydrogel matrices are bridging the gaps between liquid and capsule performance. Starch-based gels loaded with urea delivered 16% nitrogen-use efficiency gains in Thai rice paddies, demonstrating a viable mid-cost alternative. Scaling such materials will hinge on securing regionally abundant starch sources and refining low-energy drying techniques.

By Application Method: On-farm Equipment Gains Momentum

Spray applications led adoption with a 45.5% share in 2024, as most farms already own boom sprayers, minimizing upgrade costs when adopting new coatings. However, on-farm seed treaters are the fastest climbers at 10.2% CAGR, reflecting growers’ preference for just-in-time customization and reduced storage risk. Drum and pan coaters retain relevance for high-value vegetable seeds that command tight tolerances on coat thickness. The agricultural coatings market is witnessing OEM releases of dual-shot systems capable of sequentially layering biologicals and chemicals in one pass, trimming labor times by 30%. As sensing modules integrate with these machines, variable-rate coating at the seed lot level will soon be feasible.

Precision drone sprayers are also entering the mainstream, especially in Southeast Asia’s smallholder rice ecosystems. Early trials showed 40% labor savings and uniform coverage across terraced fields otherwise inaccessible to ground rigs. This momentum suggests application method innovations will remain a prime growth lever.

By Crop Type: Specialty Crops Drive Premium Growth

Cereals and grains contributed 39.1% to 2024 revenue, anchored by vast acreage and mechanized production that scales coating economics. Yet fruits and vegetables, advancing at 9.3% CAGR, are the star performers within the agricultural coatings market. Quality-sensitive export chains justify spending on edible and breathable films that curtail spoilage. Oilseeds and pulses benefit from biological inoculant coatings that enhance nitrogen fixation, yielding 14% protein gains in lentils across Canadian prairies.

Turf and ornamentals, though smaller, demand high-color coatings that ensure uniform germination in golf courses and urban landscaping projects. The diverse crop matrix underscores the need for modular coating platforms adaptable to distinct physiological and market requirements.

By Function: Controlled-Release Nutrition Leads Market Transformation

Controlled-release nutrition captured 55.4% of 2024 revenue, mirroring regulatory and agronomic imperatives to raise nutrient-use efficiency. Fertilizer coatings that stage nutrient delivery over the crop cycle showed 12% maize yield lifts in the United States based University plots while cutting nitrate runoff by a third. Seed protection functions are scaling fastest at 11.3% CAGR as pest pressure rises and neonicotinoid alternatives gain traction. Moisture-barrier coatings safeguard seeds in monsoon regions, while growth-promoting films embedding microbes or phytohormones create dual benefits of protection and vigor.

Multifunctional stacks combining all four roles are emerging. A gellan-based hydrogel infused with an auxin analog and zinc oxide nanoparticles boosted soybean root mass by 18% and reduced seedling disease incidence by 22% in Brazilian research. Such cross-functional advances reinforce the agricultural coatings market’s shift toward holistic performance packages.

Geography Analysis

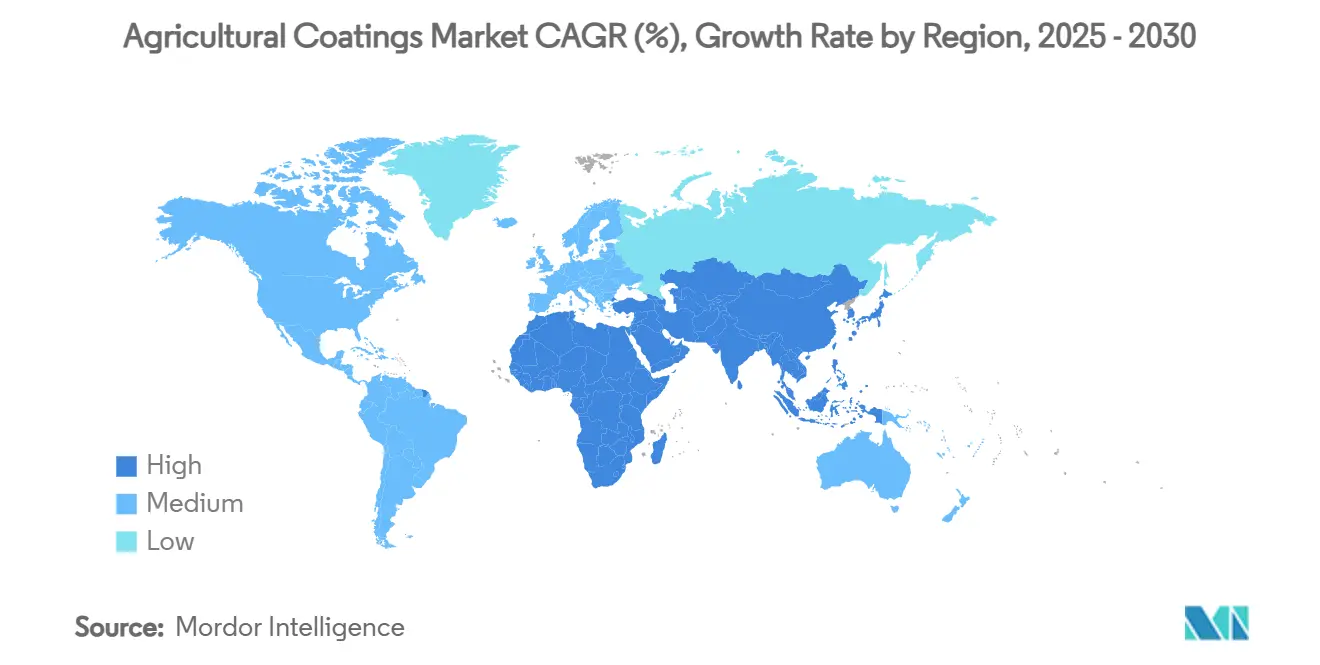

North America accounted for 34.8% of the agricultural coatings market revenue in 2024, driven by sophisticated farm mechanization, early adoption of precision agriculture, and robust regulatory oversight. United States growers have rapidly integrated sensor-guided sprayers, a key pull for formula upgrades. Canada’s 30% fertilizer greenhouse-gas-reduction target accelerates the adoption of controlled-release fertilizers, while Mexico’s modernization funds spur demand for seed treatments along produce export corridors. BASF’s consideration of an Agricultural Solutions IPO by 2027 highlights the region’s strategic importance.

Asia-Pacific is the fastest-growing arena, forecast at a 10.0% CAGR through 2030. China’s push for safer food and reduced pesticide use aligns perfectly with low-drift coatings. India’s booming agrochemical registrations and projected USD 32.4 billion sector size create fertile ground for local contractors. Japan and South Korea, though smaller, favor high-value horticulture coatings, while Australia and New Zealand lean on broadacre controlled-release fertilizers for extensive wheat and pasture systems. Diverse climates and crop portfolios compel suppliers to tailor solutions, broadening the agricultural coatings market footprint across the region.

Europe remains a sustainability leader. REACH Regulation 2023/2055 compels industry to overhaul polymer chemistry, catalyzing a pivot to biodegradables. Germany, France, and the United Kingdom champion precision systems, with data showing larger farms posting greater profitability gains from input reductions. Partnerships such as BASF and Boortmalt’s 90% greenhouse-gas cut in barley illustrate the nexus of eco-goals and coatings innovation. Eastern Europe, meanwhile, offers growth headroom as subsidy frameworks modernize.

Competitive Landscape

The agricultural coatings market exhibits moderate concentration, with the top five manufacturers controlling 48% of global sales. BASF leads with a significant share, supported by USD 1,010.9 million in agricultural research and development spend during 2024. Bayer AG follows, blending digital agronomy with seed traits, while Corteva is one of the leading players with a major share stemming from integrated seed and crop-protection platforms.

Emerging disruptors are carving out a share through sustainability-focused technologies. AgroSpheres secured USD 37 million in Series B funding to commercialize plant-based micro-capsules, and Clariant removed PFAS additives from its portfolio ahead of regulation. Patent filings doubled at Arxada during 2024, underscoring intensifying innovation competition. Strategic collaborations are multiplying as incumbents race to secure next-generation capabilities. Corteva and BASF agreed to co-develop herbicide-tolerant soybean traits slated for early-2030s launch, while Syngenta partnered with Intrinsyx Bio to scale endophyte-based nutrient-efficiency coatings. These alliances illustrate how chemical majors and biotech firms are co-investing to satisfy performance and sustainability mandates.

Regional specialists are also consolidating distribution channels to deepen market reach. Sipcam Oxon’s July 2024 purchase of Phyteurop SA’s distribution assets broadened its Western European footprint, and FMC’s September 2024 pact with Ballagro expanded biological offerings in Brazil. Such localized moves complement global majors’ research and development scale, signaling that targeted mergers and partnerships will remain a key lever for competitive positioning over the next five years.

Agricultural Coatings Industry Leaders

BASF SE

Corteva Agriscience

Clariant AG

Croda International

Bayer AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: BASF and Boortmalt produced the first Verified Impact Units in Europe, cutting greenhouse-gas emissions in barley by 90%. This initiative demonstrates a commitment to sustainable practices to enhance the value of agricultural products and increase demand for coatings designed for sustainability

- January 2025: AgroSpheres raised USD 37 million and secured clearance for AgriCell biodegradable encapsulation is designed for use in agricultural coatings ahead of a 2025 launch.

- January 2025: Syngenta and Intrinsyx Bio formed a pact to develop endophyte-based nutrient-efficiency products influencing the demand for seed treatments and other crop protection products that may utilize coatings.

- December 2024: Corteva and BASF inked agreements to co-develop herbicide-tolerant soy trait stacks. The development of these herbicide-tolerant traits influences the agricultural coatings market, especially in seed coatings.

Global Agricultural Coatings Market Report Scope

| Seed Coatings |

| Fertilizer Coatings |

| Pesticide Coatings |

| Post-harvest Produce Coatings |

| Biodegradable Seed Coatings |

| Liquid |

| Powder |

| Micro-encapsulated |

| Seed Treatment Plants |

| On-farm Seed Treaters |

| Spray Application |

| Drum and Pan Coaters |

| Controlled-Release Nutrition |

| Seed Protection |

| Moisture Barrier |

| Growth-promoting Additives |

| Cereals and Grains |

| Oilseeds and Pulses |

| Fruits and Vegetables |

| Turf and Ornamentals |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Product Type | Seed Coatings | |

| Fertilizer Coatings | ||

| Pesticide Coatings | ||

| Post-harvest Produce Coatings | ||

| Biodegradable Seed Coatings | ||

| By Formulation | Liquid | |

| Powder | ||

| Micro-encapsulated | ||

| By Application Method | Seed Treatment Plants | |

| On-farm Seed Treaters | ||

| Spray Application | ||

| Drum and Pan Coaters | ||

| By Function | Controlled-Release Nutrition | |

| Seed Protection | ||

| Moisture Barrier | ||

| Growth-promoting Additives | ||

| By Crop Type | Cereals and Grains | |

| Oilseeds and Pulses | ||

| Fruits and Vegetables | ||

| Turf and Ornamentals | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the agricultural coatings market?

The agricultural coatings market is valued at USD 3.2 billion in 2025.

How fast is the agricultural coatings market anticipated to grow?

It is forecast to expand at a 7.8% CAGR, reaching USD 4.66 billion by 2030.

Which region leads the agricultural coatings market?

North America tops revenue with a 34.8% share in 2024 due to early precision-agriculture adoption.

Who are the major players in the agricultural coatings market?

BASF, Bayer CropScience, and Corteva Agriscience together account for about 35% of global sales.

How are regulations influencing product development?

The EU’s 2028 microplastic ban and global runoff limits are steering R&D toward biodegradable and controlled-release formulations.

Page last updated on: