Global PTA Balloon Catheter Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

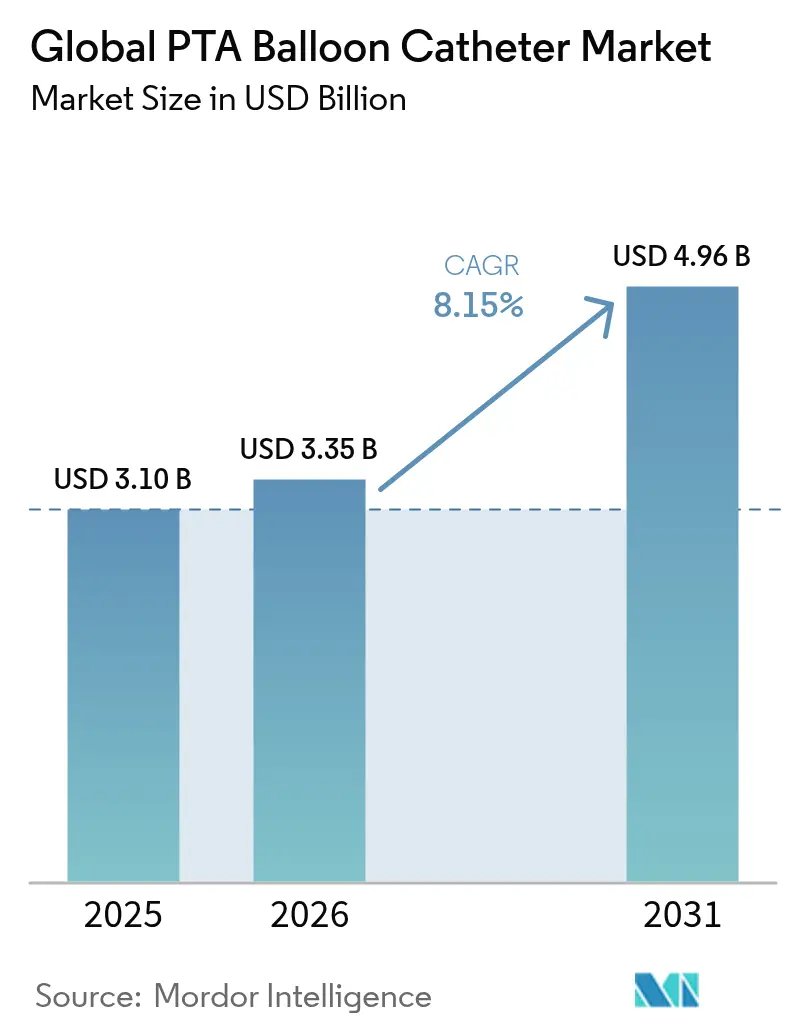

| Market Size (2026) | USD 3.35 Billion |

| Market Size (2031) | USD 4.96 Billion |

| Growth Rate (2026 - 2031) | 8.15% CAGR |

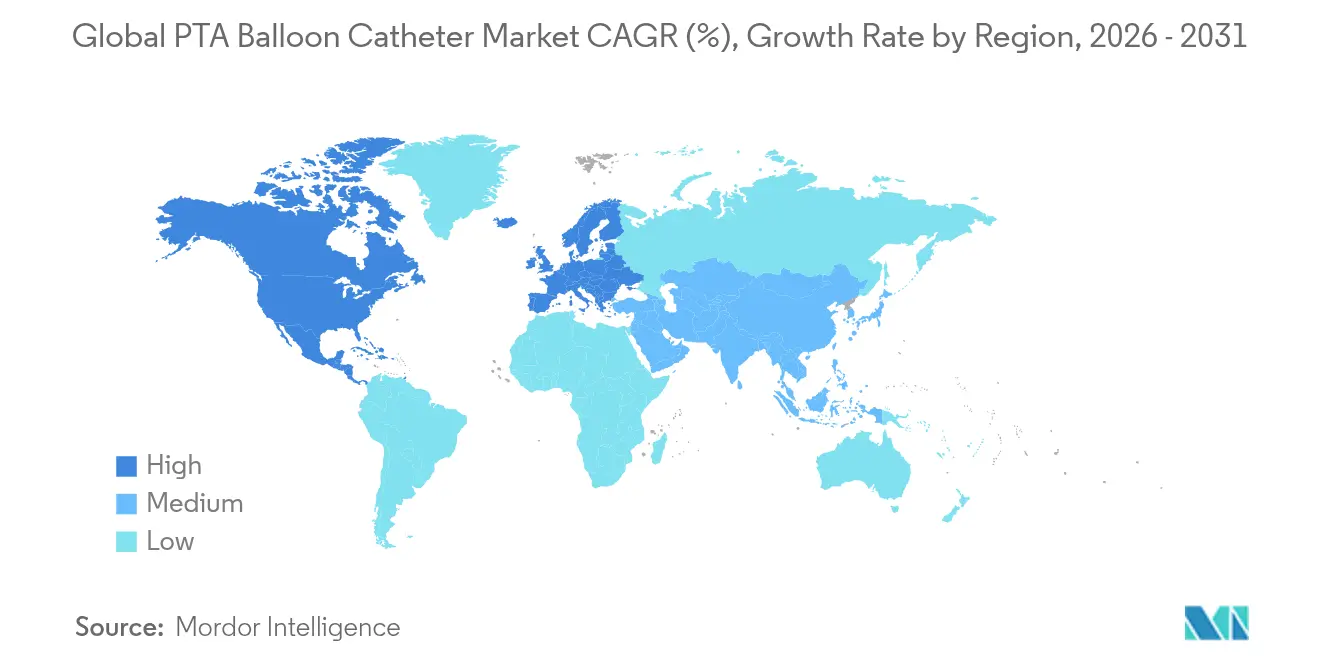

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global PTA Balloon Catheter Market Analysis by Mordor Intelligence

The PTA balloon catheter market size is expected to grow from USD 3.10 billion in 2025 to USD 3.35 billion in 2026 and is forecast to reach USD 4.96 billion by 2031 at 8.15% CAGR over 2026-2031. Rapid growth stems from the global surge in coronary and peripheral artery diseases, broader clinical use of minimally invasive angioplasty, and breakthroughs such as artificial-intelligence-guided vessel sizing that improve precision and outcomes. High adoption rates for semi-compliant balloons, deeper penetration of drug-coated platforms, and strong demand from aging populations collectively steer volume growth. At the same time, cost containment pressures, sustainability mandates, and the emergence of complementary technologies—including intravascular lithotripsy—shape purchasing decisions and competitive strategies. Intensifying consolidation highlights the premium investors place on differentiated balloon portfolios, illustrated by Teleflex’s EUR 760 million purchase of BIOTRONIK’s vascular intervention business in 2025.

Key Report Takeaways

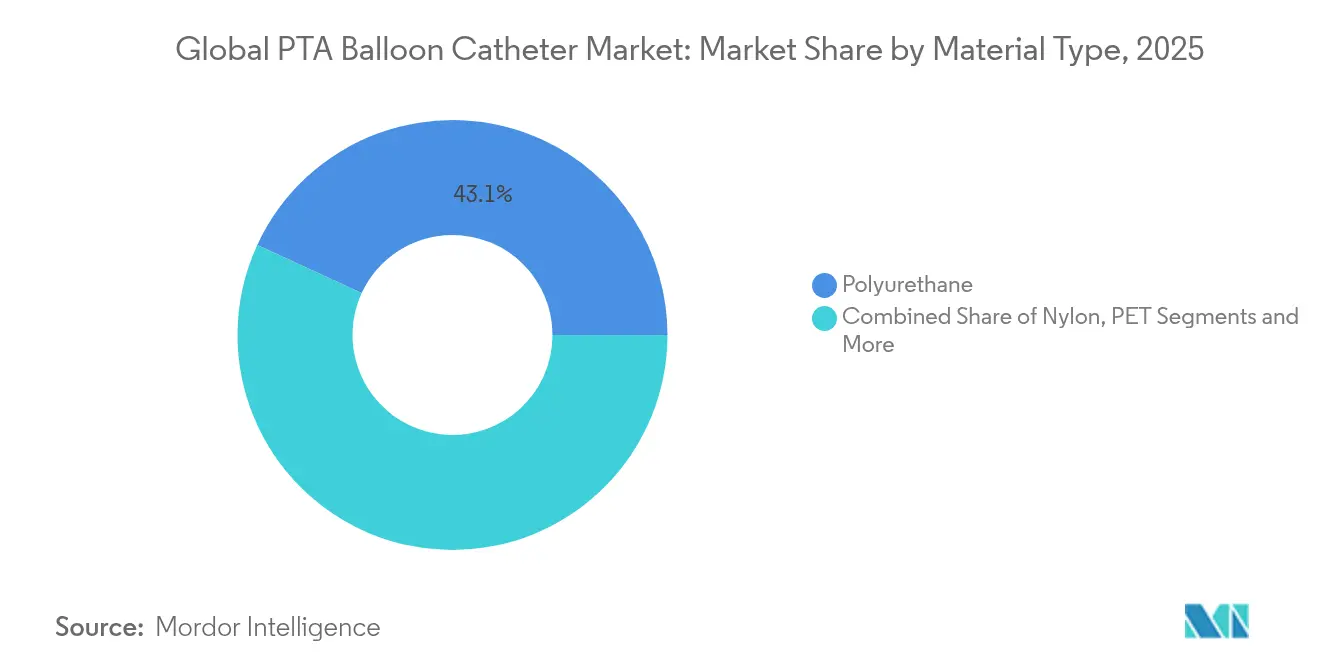

- By material type, polyurethane led with 43.12% of PTA balloon catheter market share in 2025, while advanced Pebax polymers are forecast to expand at a 9.11% CAGR to 2031.

- By coating type, plain non-coated balloons held a 57.66% revenue share in 2025; drug-coated paclitaxel balloons are the fastest-growing segment at a 8.97% CAGR through 2031.

- By compliance level, semi-compliant balloons captured 45.88% share of the PTA balloon catheter market in 2025; compliant balloons are projected to grow at 8.69% CAGR.

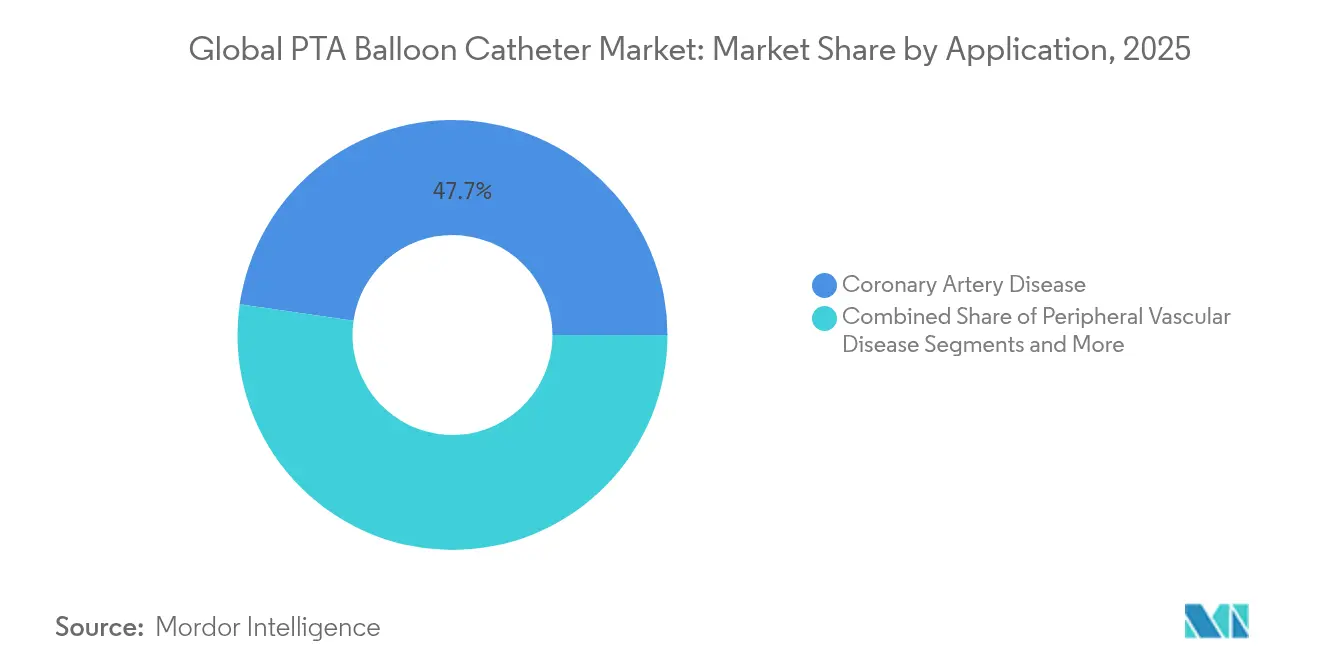

- By application, coronary artery disease accounted for 47.72% of PTA balloon catheter market size in 2025, while peripheral vascular disease is advancing at a 9.28% CAGR through 2031.

- By end user, hospitals commanded 64.75% share in 2025; ambulatory surgical centers record the highest projected CAGR at 9.47% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global PTA Balloon Catheter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Of Coronary & Peripheral Artery Diseases | +2.1% | Global, with highest impact in North America & Europe | Long term (≥ 4 years) |

| Shift Toward Minimally-Invasive Endovascular Procedures | +1.8% | Global, led by developed markets | Medium term (2-4 years) |

| Growing Geriatric Population With Comorbidities | +1.5% | North America, Europe, Japan | Long term (≥ 4 years) |

| Expedited Approvals & Coverage For Drug-Coated Balloons In Mid-Income Markets | +1.2% | Asia-Pacific, Latin America | Medium term (2-4 years) |

| Outpatient Payment Reforms Favoring Day-Case Angioplasty | +0.9% | North America, with spillover to Europe | Short term (≤ 2 years) |

| AI-Based Vessel Sizing Boosting PTA Balloon Utilization | +0.7% | Global, concentrated in advanced healthcare systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Coronary & Peripheral Artery Diseases

Escalating cardiovascular disease has enlarged the addressable patient pool for angioplasty. Coronary artery disease affects more than 200 million people, and peripheral artery disease impacts roughly 230 million worldwide, with incidence tripling beyond age 65 [1]Sofia-Cruz et al., “Calcified Coronary Lesions in Contemporary Practice,” Frontiers in Cardiovascular Medicine, frontiersin.org. Balloon angioplasty is used in 85% of coronary revascularization procedures, and calcified lesions now comprise 40% of interventional cases—conditions that increasingly require specialized cutting or scoring balloons. Diabetes further fuels demand, as drug-coated balloons lower restenosis rates in diabetic vessels. This epidemiologic base anchors sustained utilization even during economic downturns.

Shift Toward Minimally-Invasive Endovascular Procedures

Endovascular therapy now represents 78% of all vascular interventions in developed markets, reflecting shorter recovery times and lower complication rates. Design advances such as ultra-low crossing profiles let physicians treat anatomies once deemed inoperable, while robotic catheter systems cut radiation exposure and improve precision. COVID-19 accelerated the pivot as hospitals prioritized quick, low-risk care. Five-year follow-up from the IN.PACT Global Study shows 69.4% freedom from target lesion revascularization with drug-coated balloons, reinforcing long-term durability.

Growing Geriatric Population With Comorbidities

The global population aged ≥ 65 is rising 3.1% each year. Elderly patients present tortuous arteries and multiple comorbidities that favor balloon-based approaches over open surgery. Registry data confirm better outcomes with drug-coated balloons in patients > 75 years, especially for peripheral applications where durable patency is critical. Medicare has expanded outpatient angioplasty coverage, thereby aligning reimbursement with demographic realities [2]Medicare Payment Advisory Commission, “Report to the Congress: Medicare Payment Policy,” medpac.gov.

Expedited Approvals & Coverage for Drug-Coated Balloons in Mid-Income Markets

China’s NMPA and other regulators have cut review times for high-value cardiovascular devices, approving Boston Scientific’s AGENT drug-coated balloon in 2024. Health technology bodies in India and Brazil now acknowledge 35-40% fewer repeat procedures versus plain balloons, easing reimbursement hurdles. WHO assessments show stronger regulatory capacity across the Western Pacific, smoothing market entry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost Of Drug-Coated Balloons & Reimbursement Gaps | -1.4% | Global, most pronounced in emerging markets | Medium term (2-4 years) |

| Procedural Complications (Restenosis, Dissection) | -0.8% | Global, higher impact in complex lesion cases | Short term (≤ 2 years) |

| Environmental Restrictions On Paclitaxel Supply Chain | -0.6% | Global, concentrated in regulated markets | Medium term (2-4 years) |

| Rise Of Alternative Therapies (Atherectomy, Lithotripsy) | -0.5% | North America & Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Drug-Coated Balloons & Reimbursement Gaps

Drug-coated balloons cost 3-4 times more than conventional options, at USD 800-1,200 per unit in many emerging markets. Uneven reimbursement forces physicians to navigate prior-authorization delays, curbing uptake. Producers face higher manufacturing expenses due to paclitaxel handling and quality controls, passing costs to providers. Value-based frameworks that credit lower reintervention rates are still nascent, limiting penetration despite clinical advantages.

Procedural Complications (Restenosis, Dissection)

Plain balloons see 25-35% restenosis within a year, and 15-20% of angioplasties show some vessel dissection. Complex lesions—heavy calcification or chronic occlusions—raise these risks and occasionally trigger conversion to surgery. Competing modalities such as atherectomy and intravascular lithotripsy increasingly address calcified lesions, partly displacing balloons in select patients.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Advanced Polymers Drive Performance Innovation

Polyurethane commanded 43.12% of PTA balloon catheter market share in 2025, reflecting mature production lines and proven biocompatibility. Pebax and other advanced polymers are expanding at 9.11% CAGR, owing to their kink resistance and multi-durometer flexibility, which improve trackability in tortuous vessels. Nylon remains favored for cost-sensitive applications, and PET supports high-pressure balloons designed for rigid lesions. Saint-Gobain’s medical-grade Pebax blends enable balloons that flex without losing burst strength. Duke Extrusion’s custom Pebax tubing and emerging PEEK substitutes that avoid PFAS demonstrate how sustainability considerations are steering material selection.

Clinical complexity underpins polymer substitution trends. Operators are tackling more calcified and below-the-knee lesions, requiring materials that combine pushability with low crossing profiles. The PTA balloon catheter market continues to reward suppliers that tailor polymer grades for precise compliance and inflation response, supporting higher technical success in difficult anatomy. As value analysis committees scrutinize product differentiation, proven procedural benefits help premium polymers secure formulary acceptance.

By Coating Type: Therapeutic Delivery Platforms Transform Treatment Paradigms

Plain non-coated balloons retained 57.66% revenue share in 2025, underlining their role as baseline therapy for lesion dilation. Drug-coated paclitaxel balloons, however, are growing at 8.97% CAGR, buoyed by randomized trials showing 11.1% fewer adverse events compared with uncoated devices following FDA approval of Boston Scientific’s AGENT balloon in 2024. Specialty hydrophilic coatings serve small niches where low friction benefits outweigh added cost.

The PTA balloon catheter market benefits from maturing drug-transfer science. The AGENT platform’s 2 µg/mm² paclitaxel dose maintains efficacy while reducing systemic exposure. Large-scale registry data from Sweden confirm better outcomes for in-stent restenosis with drug-coated balloons versus plain angioplasty. As guidelines evolve, facilities factor reduced reintervention into total-cost-of-care models, supporting wider formulary adoption of therapeutic coatings.

By Compliance Level: Engineering Precision Meets Clinical Versatility

Semi-compliant balloons led with 45.88% share in 2025 because their controlled expansion suits most routine angioplasty. Compliant balloons, advancing at 8.69% CAGR, excel in complex lesion preparation and post-dilation when vessel conformity matters. Non-compliant balloons remain indispensable for high-pressure applications that demand precise sizing. Manufacturers adjust wall thickness and polymer blends to tune compliance, creating nuanced portfolios that match lesion subtype and procedural step. Novel spherical-tip non-compliant balloons achieved 98.9% technical success in complex coronary cases, illustrating how incremental engineering raises success rates.

Growing lesion complexity makes tailored compliance a procurement priority. Centers serving elderly or diabetic populations lean on compliant balloons to reduce dissection risk, whereas facilities treating chronic total occlusions stock non-compliant devices for aggressive post-stent expansion. Interventionalists increasingly request mixed assortments to align compliance with real-time lesion assessment.

By Application: Peripheral Vascular Expansion Drives Market Evolution

Coronary artery disease held 47.72% of PTA balloon catheter market size in 2025, anchored by well-established procedural volumes. Peripheral vascular disease is the fastest-growing segment at 9.28% CAGR, buoyed by broader indications, favorable reimbursement, and devices tailored to long lesions. Below-the-knee and infrapopliteal angioplasty volumes are rising because aging and diabetes enlarge the high-risk cohort. Renal artery stenosis, neurovascular aneurysm repair with balloon-assisted coiling, and AV fistula maintenance in dialysis patients add incremental demand.

Peripheral growth stems from guideline updates that position minimally invasive therapy ahead of surgical bypass for many limbs-threatening cases. Drug-coated balloons lower restenosis, making endovascular first-line care even more attractive. The PTA balloon catheter market therefore evolves from coronary centric to multi-territory, with device makers broadening size ranges and shaft lengths to suit distal vessels.

By End User: Ambulatory Care Revolution Reshapes Service Delivery

Hospitals owned 64.75% of 2025 volume, reflecting complex case management and round-the-clock emergency capability. Ambulatory surgical centers, expanding at 9.47% CAGR, capture routine and same-day PCI as Medicare coverage widens. Comparable outcomes between ASC and hospital outpatient PCI confirm safety, and lower facility fees enhance payer appeal. Specialty cardiac centers and office-based labs carve smaller yet growing niches.

ASC expansion reshapes inventory strategy: clinicians prefer all-in-one balloon kits that expedite workflow and minimize shelf requirements. Vendors that bundle balloons with guidewires or drug-delivery accessories gain traction in outpatient settings, where procedure time and cost vigilance are intense. As more vascular work migrates outside hospitals, supply chains adjust to just-in-time stocking and smaller batch orders.

Geography Analysis

North America commanded 44.92% revenue share in 2025, nourished by robust reimbursement, deep clinical expertise, and first-in-class approvals like the AGENT drug-coated coronary balloon in February 2024. ASC-based PCI sites doubled from 2019 to 2023 as payment rules favored outpatient care, generating fresh volume outside hospital walls . Canadian and Mexican markets add incremental gains via modernization of cath-lab infrastructure and broader insurance coverage.

Asia-Pacific is the fastest-growing region at 9.71% CAGR. China’s NMPA granted marketing authorization to AGENT in 2024, signaling a friendlier stance toward novel cardiovascular devices. India’s updated device code and increased public-private hospital spending uplift demand, while Japan’s super-aged society drives high utilization of premium balloons. WHO reports cite stronger regulatory oversight across the Western Pacific, removing bottlenecks that once delayed launches. Rising middle-class income and private insurance adoption further enlarge the patient base.

Europe sustains substantial volume through established clinical research networks and harmonized procurement processes. Evidence such as the IN.PACT Global Study underpins payer acceptance of drug-coated balloons. The Medical Device Regulation framework safeguards quality without stifling innovation. Green-procurement policies promote reprocessing programs, influencing disposable-versus-reusable calculus and potentially lowering life-cycle costs. Eastern European countries, meanwhile, lean on EU cohesion funds to upgrade cath-lab equipment, adding pockets of high growth within a mature overall landscape.

Competitive Landscape

Competitive intensity is moderate, with scale and technology leadership conferring advantage. Medtronic, Boston Scientific, and Abbott focus on drug-coated innovations and AI-enabled delivery systems to defend share. Teleflex’s EUR 760 million acquisition of BIOTRONIK’s vascular intervention division in 2025 bolstered its PTA balloon catheter market footprint through the Pantera Lux platform. Boston Scientific acquired Bolt Medical for up to USD 664 million, adding lithotripsy technology that can complement or substitute balloons in calcified lesions.

White-space competition comes from niche players tackling neurovascular, pediatric, or high-pressure segments. Companies integrating AI-driven vessel measurement into balloon selection workflows are first to market with precision-guided systems that promise shorter procedure times. Sustainability pressures spur R&D toward fluorine-free coatings and recyclable polymers, potentially resetting brand preferences. Consolidation is likely to continue as firms seek cost synergies in manufacturing, regulatory submissions, and global sales networks.

Regulatory track record and supply assurance remain core differentiators. Hospitals favor vendors that can guarantee consistent paclitaxel supply amid environmental controls and geopolitical risk. Partnerships between balloon manufacturers and atherectomy or imaging companies foreshadow integrated therapeutic suites that displace single-modality buying.

Global PTA Balloon Catheter Industry Leaders

Medtronic plc

Terumo Corporation

Boston Scientific Corporation

Natec Medical

Cardinal Health

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2024: Cook Medical declared that its Slip-Cath Beacon Tip hydrophilic selective catheter is available for use in the United States and Canada.

- June 2023: Cook Medical announced broader availability of its Advance Serenity hydrophilic PTA balloon catheter line in new sizes and geographies.

- March 2023: BrosMed secured CE MDR approval for its Tiche 0.035 High-Pressure PTA Balloon Dilatation Catheter targeting heavily calcified peripheral disease cases in Europe.

Global PTA Balloon Catheter Market Report Scope

As per the scope of this report, percutaneous transluminal angioplasty (PTA) balloon catheter has an inflatable 'balloon' at its tip, which is used during a minimally invasive catheterization procedure. This procedure is used to enlarge the narrowed vessel opening. The deflated balloon is positioned in the narrowed space and inflated for a short period of time, and deflated again to be removed. The PTA Balloon Catheter market is segmented by Material Types (Polyurethane, Nylon), By Application (Coronary Artery Disease, Peripheral Vascular Disease), By End User (Hospitals or Clinics, Ambulatory Surgery Centers, and Others), and Geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| Polyurethane |

| Nylon |

| PET |

| Pebax & Other Advanced Polymers |

| Plain (Non-coated) |

| Drug-Coated – Paclitaxel |

| Specialty Hydrophilic Coatings |

| Compliant |

| Semi-Compliant |

| Non-Compliant |

| Coronary Artery Disease |

| Peripheral Vascular Disease |

| Renal Artery Disease |

| Neurovascular Disease |

| AV Fistula Stenosis |

| Hospitals |

| Ambulatory Surgical Centers |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Material Type | Polyurethane | |

| Nylon | ||

| PET | ||

| Pebax & Other Advanced Polymers | ||

| By Coating Type | Plain (Non-coated) | |

| Drug-Coated – Paclitaxel | ||

| Specialty Hydrophilic Coatings | ||

| By Compliance Level | Compliant | |

| Semi-Compliant | ||

| Non-Compliant | ||

| By Application | Coronary Artery Disease | |

| Peripheral Vascular Disease | ||

| Renal Artery Disease | ||

| Neurovascular Disease | ||

| AV Fistula Stenosis | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current Global PTA Balloon Catheter Market size?

The PTA balloon catheter market size reached USD 3.35 billion in 2026 and is forecast to attain USD 4.96 billion by 2031.

Who are the key players in Global PTA Balloon Catheter Market?

Medtronic plc, Terumo Corporation, Boston Scientific Corporation, Natec Medical and Cardinal Health are the major companies operating in the Global PTA Balloon Catheter Market.

Which is the fastest growing region in Global PTA Balloon Catheter Market?

Asia-Pacific leads with a forecast 9.71% CAGR owing to regulatory harmonization, infrastructure investment, and rising healthcare expenditure.

How do drug-coated balloons improve outcomes?

Randomized studies show drug-coated balloons reduce target lesion failure by 11.1% versus plain balloons and cut repeat procedures by up to 40%.

Page last updated on: