Angioplasty Balloons Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.91 Billion |

| Market Size (2031) | USD 3.47 Billion |

| Growth Rate (2026 - 2031) | 3.57% CAGR |

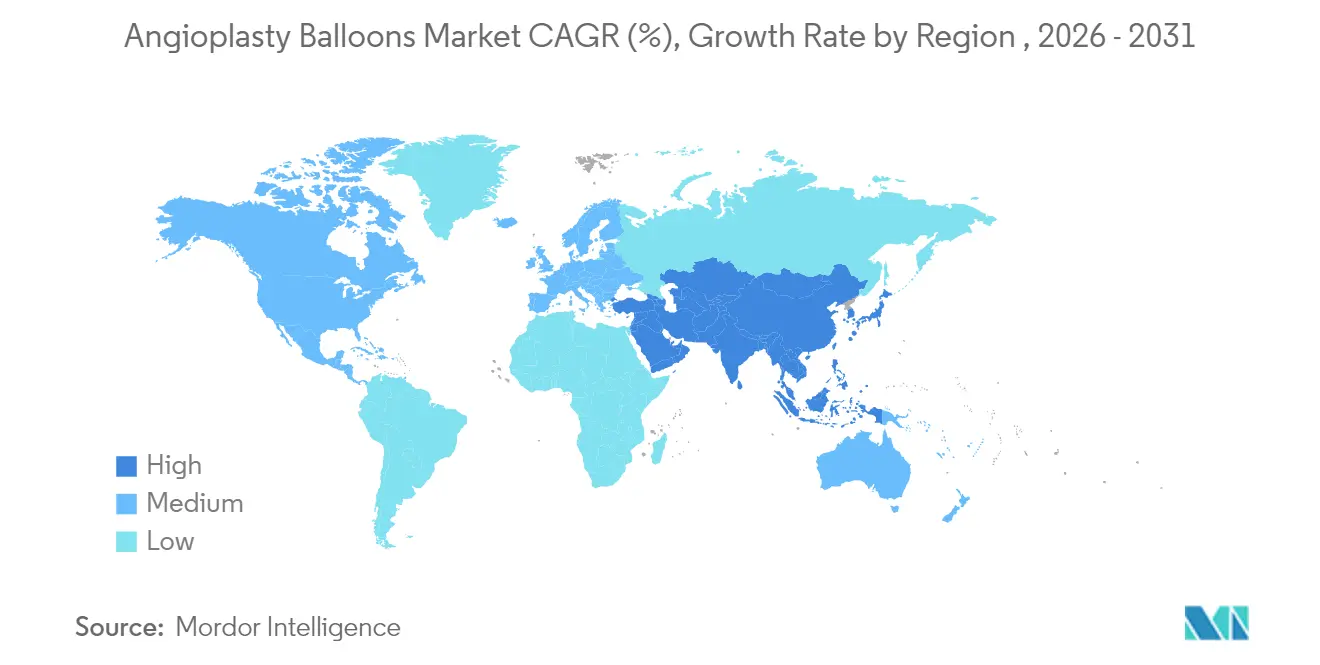

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

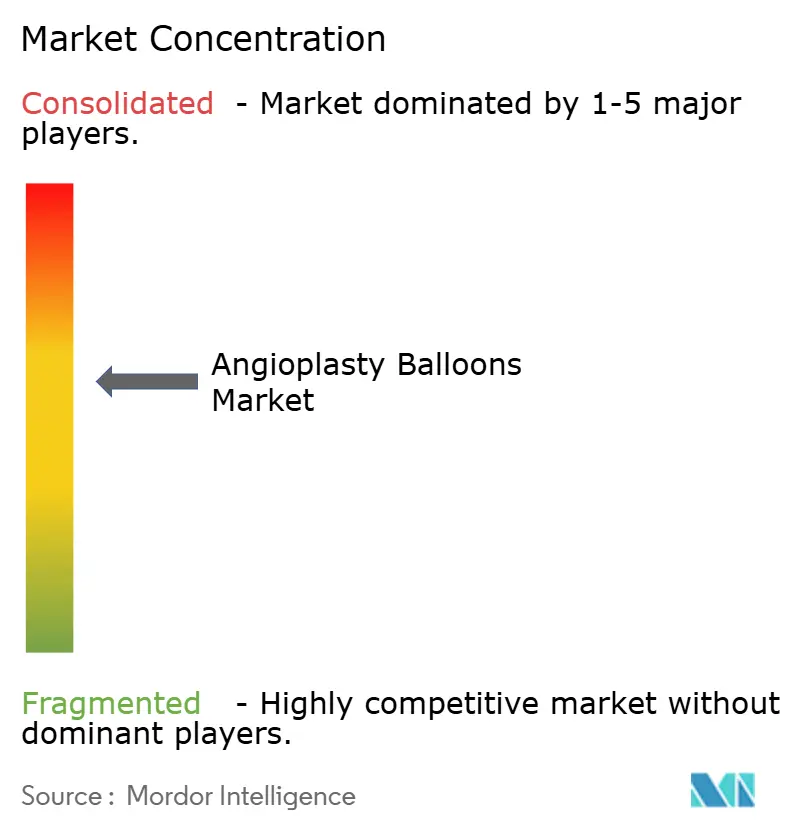

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Angioplasty Balloons Market Analysis by Mordor Intelligence

The angioplasty balloons market size is expected to grow from USD 2.81 billion in 2025 to USD 2.91 billion in 2026 and is forecast to reach USD 3.47 billion by 2031 at 3.57% CAGR over 2026-2031. This outlook confirms that the angioplasty balloons market continues to mature in a cardiovascular care environment where device sophistication must counterbalance modest procedure growth in developed regions. Demand remains firmly rooted in a large and aging cardiovascular patient pool—127.9 million Americans aged 20 and older live with heart disease today, and coronary artery disease prevalence remains close to 4.6%–4.9%. Growing clinician preference for minimally invasive percutaneous coronary intervention (PCI) sustains core procedure volumes, while recent approvals for drug-coated balloons (DCBs) validate a “leave-nothing-behind” treatment strategy that reduces reliance on permanent metallic implants. Normal balloons still dominate routine PCI, yet specialized scoring and drug technologies are gaining share as lesion complexity rises and pay-for-performance models reward durable outcomes.

Key competitive and regional shifts underpin medium-term upside. North America retains the largest regional position with 39.68% of the angioplasty balloons market in 2024 thanks to advanced infrastructure and reimbursement that now covers PCI in ambulatory surgical centers (ASCs). Asia-Pacific is the fastest-growing territory, expanding at 4.53% CAGR, supported by rapid procedure adoption amid demographic aging and investments in cath-lab capacity. At the care-delivery level, angioplasty balloons market growth tilts toward outpatient centers; ASC-based PCI volumes climbed from 0.01 to 0.87 per 10,000 Medicare beneficiaries between 2018 and 2022, pointing to 4.67% CAGR for this setting. On the product front, normal balloons held 41.54% share in 2024, but scoring balloons are pacing 4.32% CAGR as clinicians seek plaque-modification efficiency. Meanwhile, Boston Scientific’s 2024 FDA clearance for the AGENT coronary DCB, which cut target-lesion revascularization risk by 50% versus plain balloons, signals a decisive regulatory green light for drug-coated platforms.

Key Report Takeaways

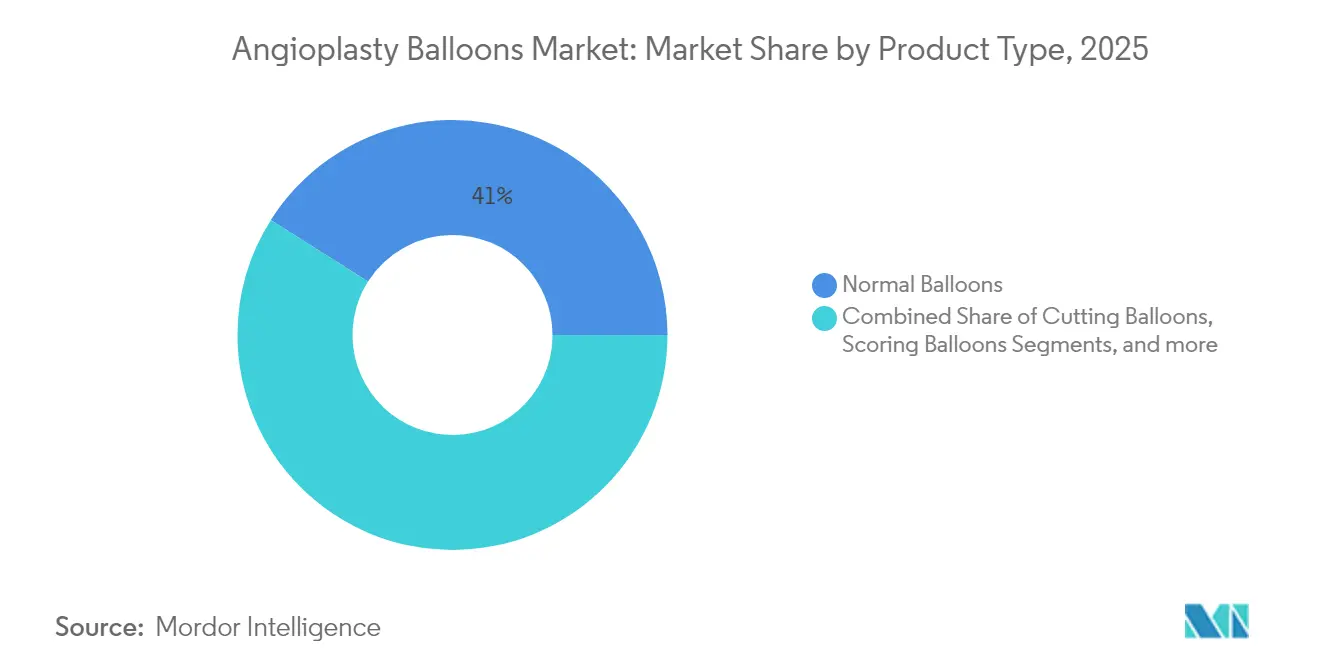

- By product type, normal balloons led with 41.02% of angioplasty balloons market share in 2025, while scoring balloons are forecast to register the highest 4.26% CAGR through 2031.

- By application, coronary angioplasty accounted for 56.30% of the angioplasty balloons market size in 2025; peripheral angioplasty is projected to expand at 4.05% CAGR to 2031.

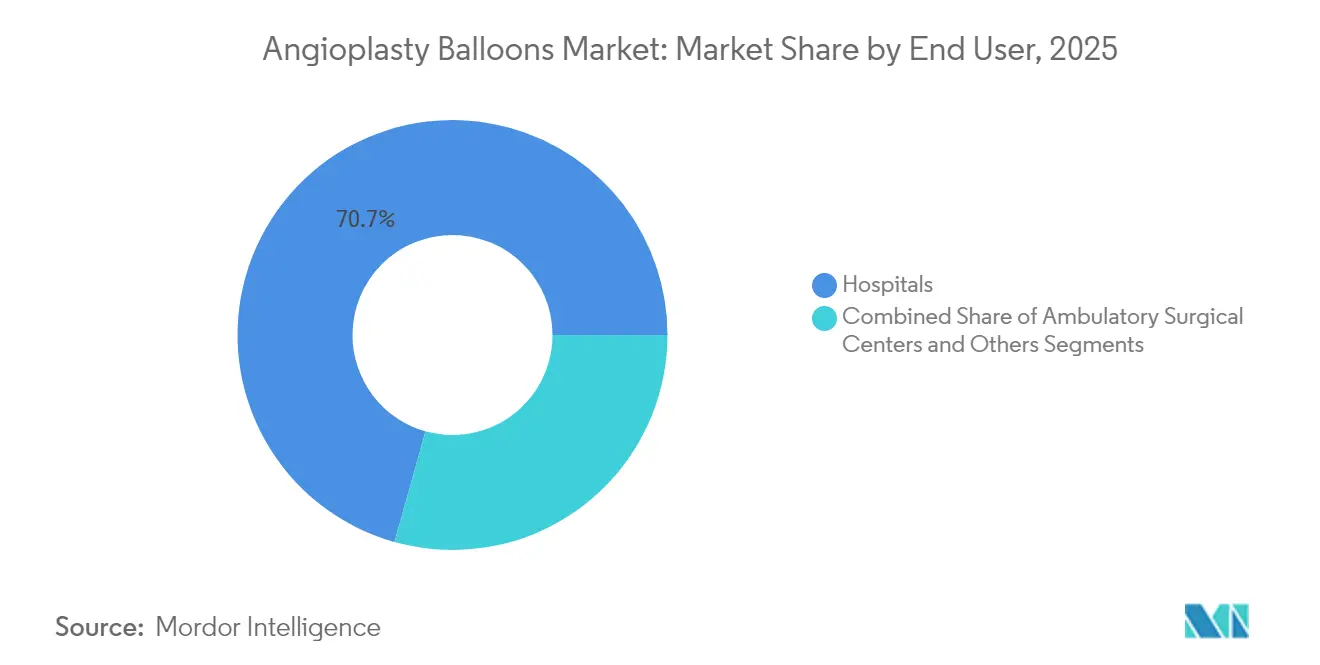

- By end user, hospitals held 70.65% revenue share of the angioplasty balloons market in 2025, whereas ambulatory surgical centers are on track for the fastest 4.58% CAGR to 2031.

- By region, North America captured 39.25% angioplasty balloons market share in 2025; Asia-Pacific is expected to post the quickest 4.45% CAGR over the forecast horizon.

- Boston Scientific, Abbott, Medtronic, and Teleflex collectively exceeded 54.62% of 2025 global angioplasty balloons market share, reflecting continued consolidation around premium technology portfolios.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Angioplasty Balloons Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising cardiovascular disease prevalence | +0.9% | Global, strongest in North America & Europe | Long term (≥ 4 years) |

| Shift toward minimally invasive PCI & technology advances | +0.8% | North America & Europe, spreading to Asia-Pacific | Medium term (2-4 years) |

| Expanding geriatric PAD pool in emerging economies | +0.6% | Asia-Pacific core, spill-over to Latin America | Long term (≥ 4 years) |

| Breakthroughs in bio-resorbable and ultra-high-pressure polymers | +0.5% | Global innovation hubs | Medium term (2-4 years) |

| Normal-pressure balloons remain hospital workhorse | +0.3% | Global, Strongest in price-sensitive market | Medium term (2-4 years) |

| Migration of angioplasty to outpatient cath-lab settings | +0.1% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Cardiovascular Disease Prevalence

The number of adults living with clinical cardiovascular disease is projected to top 45 million in the United States alone by 2050. Hypertension, diabetes, and obesity rates all continue to climb, reinforcing a long-run need for catheter-based revascularization. Although coronary mortality dropped markedly between 2000 and 2020, it has plateaued in recent years, keeping demand for balloon angioplasty stable. Hospitalizations linked to heart disease cost USD 108 billion in 2021, and forecasts point to USD 131.3 billion by 2030, highlighting the economic imperative for cost-effective minimally invasive solutions[1]American Heart Association, “Heart Disease and Stroke Statistics 2025 Update,” heart.org.

Shift toward Minimally-invasive PCI & Technology Advances

Clinical practice now favors percutaneous catheter approaches that shorten recovery and curb facility costs. Standardized endpoints for coronary DCB trials released in 2025 have legitimized drug-coated balloons, which posted 17.9% target-lesion failure at 1 year versus 28.6% with plain balloons. Intravascular lithotripsy is gaining momentum, using acoustic pressure waves inside the balloon to fracture calcium and improve luminal gain. These technologies collectively strengthen the angioplasty balloons market outlook by enhancing outcomes without leaving permanent metal behind[2]Boston Scientific, “AGENT IDE Trial Results,” bostonscientific.com.

Expanding Geriatric PAD Pool in Emerging Economies

Peripheral artery disease (PAD) incidence is climbing sharply in many Asian and Latin American populations as life expectancy rises and Western lifestyle risk factors spread. Longer balloon lengths, dedicated drug coatings, and deliverability improvements have made femoropopliteal and below-the-knee interventions more practical in resource-constrained settings. Five-year data from the IN.PACT Global Study showed 69.4% freedom from clinically driven target-lesion revascularization for DCBs in femoropopliteal disease, bolstering adoption in these high-volume markets.

Breakthroughs in Bio-resorbable & Ultra-high-pressure Polymers

Material science continues to redefine performance. Abbott’s Esprit BTK Everolimus-Eluting Resorbable Scaffold gained FDA approval in 2024, demonstrating a viable dissolving device for critical limb ischemia. Separately, ultra-high-pressure balloons such as OPN NC now withstand inflation pressures above 40 atm, enabling treatment of heavily calcified lesions that once required surgery. Drug-delivery innovations, including nano-encapsulated sirolimus, promise safer and more durable antirestenotic effects[3]Abbott Laboratories, “Esprit BTK Resorbable Scaffold System Receives FDA Approval,” abbott.com.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High procedure and device cost compared with stenting bundles | -0.7% | Global, most acute in price-sensitive markets | Short term (≤ 2 years) |

| Regulatory scrutiny over paclitaxel DCB safety signals | -0.5% | North America & Europe, cascading worldwide | Medium term (2-4 years) |

| Supply-chain tightness for high-grade nylon & PET films | -0.2% | Global | Medium term (2-4 years) |

| Periprocedural complications (recoil, restenosis) | -0.1% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Procedure & Device Cost versus Stenting Bundles

Healthcare payers remain cautious when balloon-only strategies appear more expensive than bundled stent packages that include follow-up imaging and medication plans. Despite Medicare approval, ASCs still perform only 1.8% of outpatient PCIs in the United States, signaling persistent economic hesitation. Premium pricing on drug-coated balloons tightens purchasing decisions, especially where supply-chain inflation has lifted input costs to 20% of device revenues.

Regulatory Scrutiny on Paclitaxel DCB Safety Signals

Although the FDA lifted restrictions, lingering concern regarding late mortality in paclitaxel-based DCBs slows adoption. Labels for leading paclitaxel platforms include explicit warnings mandating patient discussions, and post-market surveillance obligations raise compliance costs. These uncertainties are driving interest in sirolimus-coated alternatives and in next-generation trial designs that more clearly delineate mortality risk[4]U.S. Food & Drug Administration, “Premarket Approval AGENT Drug-Coated Balloon,” fda.gov.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Scoring Balloons Drive Specialized Growth

Scoring balloons held the fastest growth trajectory at 4.26% CAGR through 2031, a pace that reflects their role in plaque-modification strategies for calcified or fibrotic lesions. The angioplasty balloons market size for scoring systems is rising as studies such as Naviscore’s first-in-man series reported 94% procedural success in moderate-to-severe calcification. Normal balloons still dominate everyday PCI with 41.02% 2025 share because they remain indispensable for routine pre- and post-dilation steps.

Drug-coated balloons gained decisive momentum after Boston Scientific’s AGENT approval, which showed a 50% reduction in repeat revascularization compared with conventional angioplasty. Cutting balloons preserve a niche for in-stent restenosis and small-vessel work, with meta-analysis indicating a 33% reduction in target-lesion revascularization risk. Ultra-high-pressure variants, now exceeding 40 atm, extend percutaneous treatment to hard fibro-calcific plaques, expanding the angioplasty balloons market both procedurally and technologically.

By Application: Peripheral Angioplasty Accelerates Growth

Peripheral interventions are forecast to post 4.05% CAGR to 2031, reflecting surging PAD prevalence amid aging demographics and lifestyle changes. Freedom-from-revascularization rates of 69.4% at 5 years for drug-coated balloons validate durability in the femoropopliteal segment, anchoring demand outside the coronary arena. Coronary angioplasty still delivered 56.30% of 2025 revenue and remains the most common procedure; however, secondary prevention initiatives and optimized medical therapy cap its growth.

Emerging tools, including dissolving scaffolds for below-the-knee disease, further broaden therapeutic reach. Intravascular lithotripsy integration with long peripheral balloons improves luminal expansion in diffuse calcified lesions. The peripheral trend diversifies the angioplasty balloons market, helping balance plateauing coronary volumes and giving manufacturers new avenues for innovation.

By End User: Ambulatory Centers Reshape Care Delivery

Hospitals retained 70.65% of global revenue in 2025 because of comprehensive cardiac services and readiness for complex or emergent cases. Still, the angioplasty balloons market is experiencing a pronounced site-of-care shift. Ambulatory surgical centers are on a 4.58% CAGR trajectory through 2031 because Medicare now reimburses PCI outside hospital walls. Recent claims data confirm that ASC PCI volume, while still small, is accelerating quickly.

Cost efficiency and patient-experience gains serve as key ASC advantages, although stringent patient-selection protocols remain essential. New ASC-only C codes for diagnostic catheterization and PCI elevate reimbursement predictability, nudging cardiology groups to develop freestanding labs. Quality-outcome benchmarks and standardized discharge criteria will further support outpatient expansion, sustaining angioplasty balloons market growth in this setting.

Geography Analysis

North America led with 39.25% angioplasty balloons market share in 2025, supported by broad insurance coverage, established cath-lab networks, and early adoption of premium devices. The region’s regulatory environment favors innovation, evidenced by the 2024 clearance of the AGENT coronary DCB. CMS policy changes permitting ASC-based PCI have begun to reshape volume distribution, yet hospitals keep the bulk of complex procedures. Persistent supply-chain turbulence has forced local manufacturers to absorb double-digit logistics and raw-material inflation, heightening focus on digital inventory control. Consolidation remained active, highlighted by Teleflex’s EUR 760 million acquisition of BIOTRONIK’s vascular unit, which enriched its drug-coated balloon and stent offerings.

Asia-Pacific registers the swiftest expansion at 4.45% CAGR. Population aging, urbanization, and infrastructure build-out are unlocking cath-lab demand. Government moves to harmonize device approvals and encourage domestic manufacturing continue to reduce time-to-market for new balloons. Regional clinical guidelines now recommend DCBs for small-vessel disease and in-stent restenosis, aligning therapy choices with global standards. Growth, however, is tempered by price sensitivity, which pushes buyers toward cost-effective platforms and accelerates local production of basic balloons even as demand for high-end scoring and drug-coated variants climbs.

Europe delivers steady but measured gains as economic pressures constrain premium device uptake in some public-health systems. The Medical Device Regulation (MDR) framework, while rigorous, provides clarity that helped Terumo secure CE marks for several vascular-closure solutions in 2024, sustaining procedural ecosystems. Cordis’s SELUTION SLR sirolimus-eluting balloon posted 81.5% three-year patency in Japan and 91.1% freedom from target-lesion revascularization in European trials, reinforcing drug-coated platforms. Clinical collaboration through groups such as the Drug-Coated Balloon Academic Research Consortium promotes evidence-based adoption across the continent, maintaining Europe’s role as a bellwether market for next-generation balloons.

Competitive Landscape

The angioplasty balloons market displays moderate concentration as diversified device companies reinforce portfolios via targeted mergers while smaller innovators carve out high-performance niches. Boston Scientific’s USD 664 million purchase of Bolt Medical gave it proprietary lithotripsy balloon capability, complementing its AGENT DCB and deepening its plaque-modification arsenal. Teleflex invested EUR 760 million to buy BIOTRONIK’s vascular intervention franchise, broadening access to drug-eluting technology and strengthening its structural-heart cross-selling strategy. Johnson & Johnson followed with a USD 1.1 billion move for V-Wave, signaling that large players see value in specialized cardiovascular platforms.

Technology differentiation centers on coating science, burst pressure engineering, and material innovation. Boston Scientific leverages its TransPax platform to deliver paclitaxel more predictably, achieving 50% lower revascularization versus plain balloons in in-stent restenosis. Abbott focuses on bio-resorbable constructs that dissolve after drug delivery, solving long-term metal-implant drawbacks. Cordis drives sirolimus-based balloons that aim to mitigate paclitaxel safety debate. Medtronic’s Prevail DCB pivotal trial, approved in October 2024, will compare head-to-head with AGENT across 65 centers, underscoring the premium suppliers place on randomized evidence.

Operational resilience has become a competitive theme as geopolitics and raw-material costs lift supply-chain exposure. Leading manufacturers are investing in additive manufacturing, real-time inventory analytics, and smart extrusion lines to safeguard production. Smaller entrants focus on single-use specialty balloons and regional distribution alliances, often licensing coating or polymer IP to larger firms. The overall competitive narrative points to a mix of consolidation among giants and agile innovation among specialists, jointly propelling the angioplasty balloons market forward.

Angioplasty Balloons Industry Leaders

Medtronic

Boston Scientific Corporation

Terumo Corporation

BIOTRONIK

Terumo Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Teleflex announced the acquisition of BIOTRONIK’s vascular intervention business for about EUR 760 million (USD 820 million), enhancing its interventional cardiology lineup with DCBs and drug-eluting stents.

- January 2025: Boston Scientific entered the intravascular lithotripsy segment via its USD 664 million Bolt Medical acquisition, adding acoustic-pressure balloon technology for calcified arterial disease.

- October 2024: Medtronic secured FDA investigational-device-exemption approval to launch the Prevail DCB pivotal trial, comparing outcomes directly with Boston Scientific’s AGENT platform across 65 global centers.

- August 2024: Johnson & Johnson revealed plans to purchase cardiovascular specialist V-Wave for up to USD 1.1 billion, aiming to expand its interventional cardiology presence.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our analysis defines the angioplasty balloons market as the worldwide sales value of single-use catheter-based balloons, normal, cutting / scoring, and drug-eluting, deployed to widen coronary or peripheral arteries during percutaneous transluminal angioplasty procedures. These figures exclude bundled stent kits and inflation pumps, so the addressable value reflects the balloon device alone, expressed in constant 2024 US Dollars.

Scope Exclusions: The study excludes balloon inflation devices, guide wires, vascular stents, and post-dilation service revenues.

Segmentation Overview

- By Product Type

- Normal Balloons

- Cutting Balloons

- Scoring Balloons

- Drug-Eluting Balloons

- By Application

- Coronary Angioplasty

- Peripheral Angioplasty

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Others

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- Turkey

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor's team interviewed interventional cardiologists, cath-lab managers, sourcing heads at hospitals and ambulatory surgical centers, plus regional distributors across North America, Europe, Asia-Pacific, and Latin America. Insights on procedure mix shifts, preferred balloon types, and current ASP discounting filled information gaps and validated secondary signals before numbers were finalized.

Desk Research

We started with structured desk work, mapping regulatory and care-delivery baselines from tier-1 public sources such as the American Heart Association, Centers for Medicare & Medicaid Services, OECD Health Statistics, Eurostat hospital discharge files, and Japan's MHLW procedure registry. Device import-export codes were checked through UN Comtrade, while safety notices were reviewed in the U.S. FDA 510(k)/MAUDE databases. Company revenues from D&B Hoovers and news flows in Dow Jones Factiva helped anchor average selling prices. These references illustrate, not exhaust, the wider body of literature consulted by Mordor analysts.

Market-Sizing & Forecasting

A top-down reconstruction converts country-level PCI and peripheral angioplasty volumes into balloon demand pools, applying average balloons-per-case factors that our experts validated. Supplier roll-ups and sampled ASP × volume checks provide a selective bottom-up lens that fine-tunes totals. Key variables inside the model include primary PCI incidence rates, reimbursement rule changes, coronary-to-peripheral case mix, drug-eluting balloon penetration, average selling price erosion, and cath-lab capacity expansion. Multivariate regression, supported by scenario analysis for regulatory or recall shocks, projects each driver through 2030. Missing datapoints are bridged through closely correlated proxies such as cardiac catheterization bed additions.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated variance scans, peer analyst audits, and senior sign-off. Deviations beyond preset bands trigger re-contacts with interviewees. We refresh the database each year and issue interim updates if material recalls, reimbursement shifts, or major acquisitions alter market dynamics.

Why Mordor's Angioplasty Balloons Baseline Commands Reliability

Published estimates often differ because firms choose dissimilar device baskets, price assumptions, and refresh rhythms. By selecting a narrowly defined balloon scope and validating every input against live cath-lab feedback, Mordor delivers numbers that decision-makers can trace back to observable variables.

Key gap drivers include divergent scope, as some publishers blend accessories or focus solely on drug-coated balloons, older base years rolled forward with flat CAGRs, and limited ASP triangulation. Our annual refresh and mixed-method model help neutralize these issues.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.81 B (2025) | Mordor Intelligence | - |

| USD 2.70 B (2024) | Global Consultancy A | Wider device basket; parallel-import volume estimates lack ASP checks |

| USD 2.20 B (2022) | Regional Consultancy B | Older base year; fixed growth ignores post-pandemic cath-lab rebound |

| USD 0.64 B (2022) | Industry Journal C | Focuses only on drug-coated balloons, excluding normal and scoring variants |

In sum, the disciplined scope selection, dual-lens modeling, and annual validation cycle ensure that Mordor Intelligence provides a balanced, transparent baseline suited to budgeting, portfolio planning, and investment screening.

Key Questions Answered in the Report

What is the current angioplasty balloons market size and expected growth?

The angioplasty balloons market size is USD 2.91 billion in 2026 and is forecast to reach USD 3.47 billion by 2031 at a 3.57% CAGR.

Which region leads the angioplasty balloons market?

North America holds the lead with 39.25% market share in 2025, supported by broad reimbursement and early technology adoption.

Why are drug-coated balloons gaining attention?

FDA-approved drug-coated balloons such as AGENT reduce repeat revascularization by 50% versus plain balloons, supporting a leave-nothing-behind strategy.

How fast is the ambulatory surgical center segment growing?

ASC-based PCI is projected to register a 4.58% CAGR through 2031 as reimbursement and patient-experience benefits shift procedures out of hospitals.

What are the main restraints facing the angioplasty balloons market?

High device costs relative to bundled stent strategies and ongoing regulatory scrutiny of paclitaxel safety remain the chief adoption barriers.

Which product type is expanding the quickest?

Scoring balloons lead growth at 4.26% CAGR because they improve plaque modification in complex calcified lesions.

Page last updated on: