Prostate Cancer Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 25.73 Billion |

| Market Size (2031) | USD 38.33 Billion |

| Growth Rate (2026 - 2031) | 8.29% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Prostate Cancer Market Analysis by Mordor Intelligence

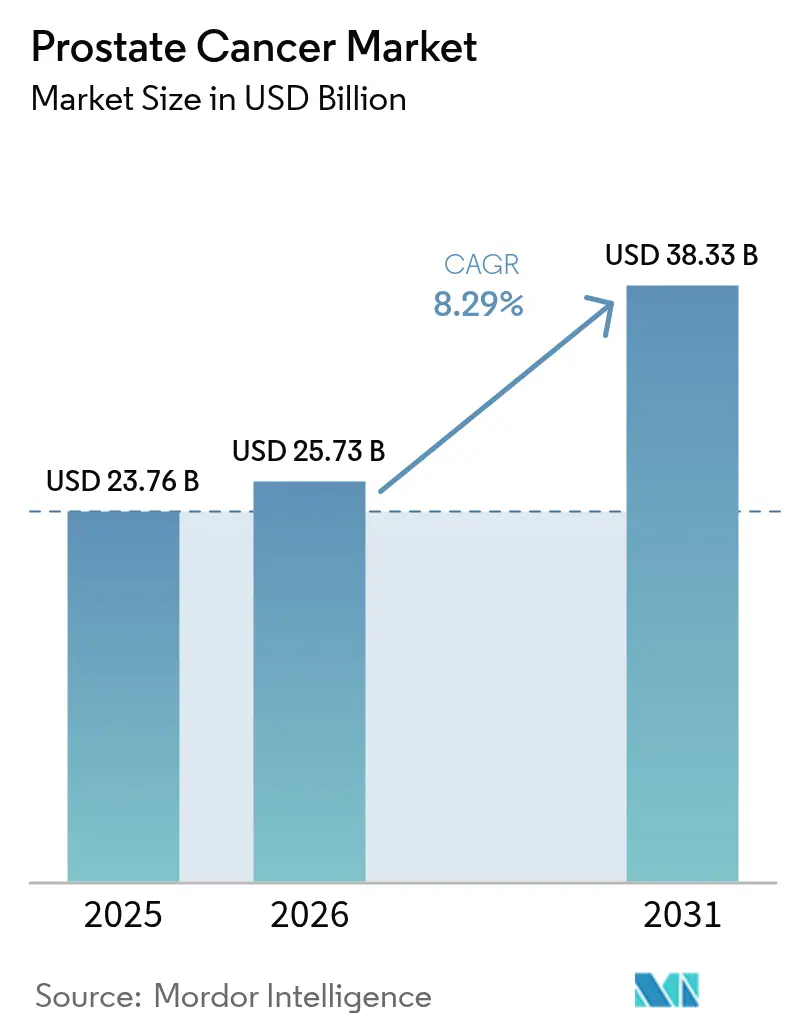

Prostate Cancer market size in 2026 is estimated at USD 25.73 billion, growing from 2025 value of USD 23.76 billion with 2031 projections showing USD 38.33 billion, growing at 8.29% CAGR over 2026-2031. Demographic ageing, rapid uptake of precision-medicine workflows, and steady therapeutic innovation collectively underpin this expansion. Robust reimbursement for next-generation imaging such as PSMA-PET, coupled with broader Medicare coverage for multi-gene urine and blood tests, is accelerating early detection in high-income settings.[1]Source: Centers for Medicare & Medicaid Services, “Bone Density Evaluation for Patients With Prostate Cancer and Receiving Androgen Deprivation Therapy,” cms.gov The Asia-Pacific region supplies additional momentum as China, India, and Japan modernize their oncology infrastructure, which raises diagnostic volumes and broadens access to advanced hormone and radioligand therapies. Competitive strategies center on the roll-outs of radioligand therapy, biomarker-guided drug-diagnostic combinations, and cross-border licensing deals that secure regional footholds. At the same time, payers continue to scrutinize high-ticket regimens, favouring technologies that shorten diagnostic cascades or delay transition to costly late-line treatments.

Key Report Takeaways

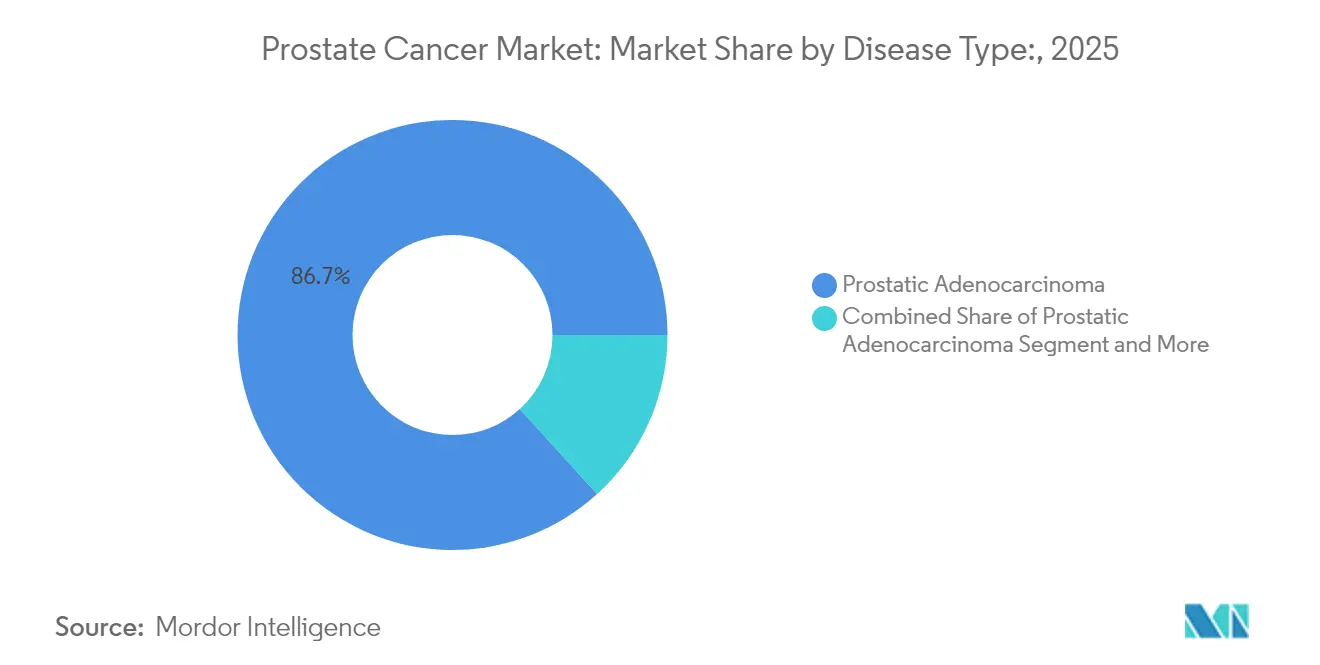

- By disease type, prostatic adenocarcinoma accounted for 86.74% of the Prostate Cancer market share in 2025, whereas small cell carcinoma is projected to advance at a 6.78% CAGR through 2031.

- By stage, localized T1–T2 disease accounted for a 61.08% share of the Prostate Cancer market size in 2025, while distant/metastatic cases are expected to expand at an 8.57% CAGR through 2031.

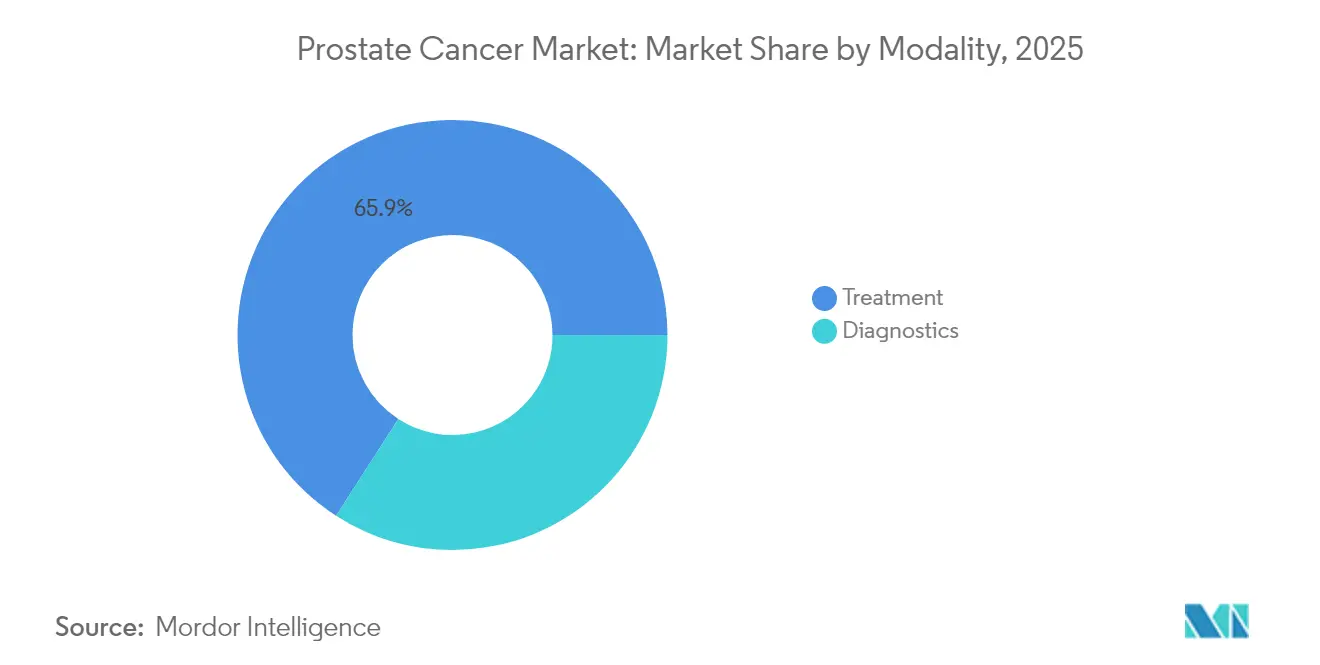

- By modality, treatment activities captured 65.89% of the revenue in 2025; diagnostics remain the fastest-growing segment, registering a 9.27% CAGR through 2031.

- By end user, hospitals led the Prostate Cancer market with 48.21% of the market value in 2025; however, specialty cancer centers are projected to record the highest CAGR at 8.95% through 2031.

- By geography, North America led with a 41.88% share in 2025; the Asia Pacific is expected to register the highest 10.08% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Prostate Cancer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Aging Population and High Prevalence Rate of Prostate Cancer | +2.1% | Global, with highest impact in North America & Europe | Long term (≥ 4 years) |

| Growing Adoption of Precision-Medicine Workflows & Companion Diagnostics | +1.8% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Technological Advances in Minimally-Invasive Surgery and Image-Guided Radiotherapy | +1.5% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Increasing Government Initiatives for Prostate Cancer Awareness | +1.2% | APAC core, spill-over to MEA and Latin America | Short term (≤ 2 years) |

| Robust R&D Pipeline of Prostate Cancer Therapies | +1.4% | Global, concentrated in North America & Europe | Long term (≥ 4 years) |

| Shift Toward Personalized Medicine and Relevant Improved Patient Experience | +1.3% | North America & EU, gradual expansion globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Ageing Population and High Prevalence

Longevity gains have lifted global male life expectancy, creating larger cohorts at risk for prostate malignancy. Incidence now varies more than 13-fold between regions, with the highest rates in Australia/New Zealand, North America, and Northern Europe. Mortality remains disproportionately high across sub-Saharan Africa and parts of Latin America, where de novo metastatic presentations exceed 20%, underscoring gaps in screening infrastructure. Over the past five years, 11 middle-income countries have reported double-digit growth in incidence, reflecting both improved PSA testing coverage and demographic aging. These structural shifts sustain baseline demand for the prostate cancer market worldwide. Health ministries in the Middle East are reevaluating age-based screening cut-offs to curb the presentation of advanced stages, signaling regulatory tailwinds for the widespread adoption of diagnostics.

Growing Adoption of Precision-Medicine Workflows & Companion Diagnostics

Regulatory approvals for biomarker-guided treatments, notably olaparib plus abiraterone for BRCA-mutated metastatic disease, have validated the routine use of genomic testing. Economic models place germline BRCA screening at USD 26,657 per quality-adjusted life year, which is well within the acceptability thresholds for high-income systems. Medicare reimbursement for urine-based MyProstateScore 2.0 and 18-gene panels is cutting avoidable biopsy rates, thereby curbing downstream overtreatment costs. The Prostatype P-score further enhances active-surveillance triage, delivering incremental QALY gains at a lower overall spend.[2]Source: Persson S., “Prostatype P-Score Biomarker Approach,” Springer, springer.com Collectively, these tools bolster physician confidence in individualized care, accelerating revenue growth for the prostate cancer market within the diagnostics segment.

Technological Advances in Minimally-Invasive Surgery and Image-Guided Radiotherapy

Robotic platforms and focal-therapy devices are redefining the standard of care. MR-guided transurethral ultrasound ablation yielded an incremental cost-effectiveness ratio of EUR 12,193 per QALY compared to robot-assisted radical prostatectomy, thereby bolstering payer acceptance. Transperineal biopsy under local anaesthetic halves procedural costs while matching diagnostic accuracy, a benefit keenly valued by outpatient centers. PSMA-PET/CT integration into equivocal MRI pathways delivers superior localization; however, broader adoption hinges on the contraction of radiotracer costs. These innovations differentiate providers and fortify procedure volumes, further energizing the prostate cancer market.

Robust R&D Pipeline of Prostate Cancer Therapies

Pipeline density spans hormone-therapy reformulations, PARP inhibitors, radioligands, and immune-cell engagers. The FDA accepted a three-month leuprolide depot with 97.9% testosterone suppression, targeting August 2025 approval. Darolutamide’s March 2025 label expansion into metastatic castration-sensitive disease extends its addressable cohort and sets up direct competition with enzalutamide. Early-phase bi-specific T-cell engagers targeting PSMA and PSCA are tackling antigen-escape resistance, although toxicity management remains a development hurdle. The breadth of modalities promises sustained innovation flow, supporting medium-term revenue acceleration for the prostate cancer market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Aggregate Cost of Diagnosis-To-Treatment Pathway Strains Payers and Patients | -1.9% | Global, with highest impact in emerging markets | Short term (≤ 2 years) |

| Limited Accessibility of Advanced Imaging and Genomic Testing in Low-Resource Settings | -1.4% | Sub-Saharan Africa, Latin America, rural APAC | Long term (≥ 4 years) |

| Stringent Regulatory Requirements & Lengthy Clinical Development Timelines for Novel Agents | -1.1% | Global, with varying impact by regulatory jurisdiction | Medium term (2-4 years) |

| Concerns Regarding Drug Resistance and Relapse | -0.8% | Global, particularly affecting advanced disease management | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Aggregate Cost of Diagnosis-to-Treatment Pathway

Cost-of-illness studies in Iran pegged the average per-patient expenditure at USD 2,613, while national burden estimates reached USD 217 million, figures that strain payer budgets in resource-stressed settings.[3]Source: Behzadifar M., “Economic Burden of Prostate Cancer in Iran,” biomedcentral.com In Germany, 177Lu-PSMA-617 radioligand therapy adds EUR 27,200 per patient, nudging the cost-utility ratio toward EUR 69,418 per QALY, a level only marginally within negotiated thresholds. Caribbean hospitals experience sharp spikes in out-of-pocket costs for surgical care, often steering patients toward suboptimal hormone monotherapy. Generic abiraterone in Mexico has reduced costs by USD 6,251 per case, illustrating how pricing reforms can expand therapeutic access. Persistently high aggregate spending dampens the near-term uptake of cutting-edge modalities, tempering the velocity of the prostate cancer market, especially in low- and middle-income economies.

Limited Accessibility of Advanced Imaging and Genomic Testing in Low-Resource Settings

Diagnostic capacity across 58 African urology centres shows 53.4% readiness for radical prostatectomy and 86.2% access to radiotherapy, yet only a minority offer PSMA-PET or high-density biopsy services. Kenyan focus groups attribute diagnostic delay to symptom misattribution, stigma, and direct-payment barriers, underlining the importance of culturally attuned awareness campaigns. Even where equipment is present, consumable supply chains and radio-pharmaceutical logistics remain fragile, leading to backlog-driven wait times that push clinical staging toward T3-T4 categories. Consequently, care deferral perpetuates advanced-stage dominance, capping addressable procedure volumes for the prostate cancer market in these zones.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disease Type: Adenocarcinoma Consolidation Supports Scale Efficiencies

Prostatic adenocarcinoma continues to dominate, holding 86.74% of the prostate cancer market value in 2025, buoyed by standardized care pathways and robust evidence-based guidelines. Precision biomarker panels are refining risk stratification within this broad cohort, enabling more granular treatment roadmaps and sustaining diagnostic test growth. Small cell carcinoma, although accounting for only a small portion of the overall incidence, is experiencing a 6.78% CAGR as genomic profiling and targeted chemotherapeutic regimens improve survival in this aggressive phenotype. The Prostate Cancer Diagnostics and Therapy industry has responded by earmarking R&D budgets for rare histologies, anticipating reimbursement differentiation that rewards specialized therapeutics. Benign prostatic hyperplasia remains clinically distinct yet exerts an indirect influence on imaging volumes when PSA levels trigger further work-up, fostering cross-referral synergies within comprehensive urology centers.

Heightened recognition of transitional cell and sarcomatoid variants, coupled with academic-centre registry initiatives, forecasts an incremental lift in niche subsegments. However, the sheer scale of adenocarcinoma anchors manufacturing economies across hormone-therapy APIs and biopsy devices, conferring cost advantages that smaller-scale indications struggle to replicate. This volume dynamic reinforces the central role of adenocarcinoma management in the target market.

By Stage: Divergent Growth between Early and Advanced Presentations

Localized T1–T2 disease delivered 61.08% of 2025 procedure volumes, reflecting widespread PSA screening and insurance-funded MRI triage in North America and parts of Europe. Yet distant/metastatic tumours outpaced all others with an 8.57% CAGR forecast, propelled by improved imaging sensitivity that converts biochemical recurrence into earlier metastatic confirmation. The prostate cancer market size for metastatic interventions is projected to grow in the coming years, mirroring escalating use of novel hormonal combinations and radioligand therapies.

Regional T3 disease sits between these poles, benefiting from dose-escalated image-guided radiotherapy and MR-targeted focal ablation that preserves functional outcomes. Data from the Mexican Can.Prost registry confirms that early detection programs elevate radical treatment eligibility to 67%, shrinking future metastatic burden. Conversely, Middle Eastern registries cite de novo metastatic rates above 20%, signalling lost screening opportunities that inflate high-cost systemic therapy demand. Such contrasts illustrate how stage migration dictates revenue mix inside the prostate cancer market

By Modality: Diagnostics Accelerate While Therapies Hold Revenue Lead

Treatment modalities retained 65.89% revenue share in 2025, anchored by surgery, radiation, and systemic drugs that command premium pricing across disease stages. The prostate cancer market size for diagnostic technologies is, however, expanding at 9.27% CAGR, underscoring the fiscal logic of catching disease earlier and tailoring therapy precisely. In vivo imaging with PSMA-PET and MRI fusion biopsy platforms is swelling capital-equipment pipelines as community hospitals seek competitiveness.

On the therapeutic side, robotic surgery delivers marketing cachet and shorter length-of-stay, but cost-conscious payers are evaluating bundled payments that could compress margins. Radioligand agents poised for adjuvant trials may shift some revenue from operating theatres toward nuclear medicine departments. Meanwhile, decentralized liquid biopsy testing promises to recalibrate follow-up pathways, keeping diagnostics firmly in double-digit growth terrain and rebalancing modality mix within the prostate cancer market.

By End User: Specialty Centres Challenge Hospital Supremacy

Hospitals still accounted for 48.21% of 2025 spending, supported by broad service portfolios, integrated imaging suites, and payer contracts that funnel complex cases. Yet specialty cancer centres are registering a 8.95% CAGR, capitalizing on highly focused clinical teams and multidisciplinary tumour boards that draw referral traffic nationwide. The Prostate Cancer Diagnostics and Therapy industry recognises these hubs as early-adopter sites for PSMA-targeted PET tracers and radioligand therapies, often partnering for post-marketing evidence generation.

Diagnostic laboratories, equipped with high-throughput NGS platforms, leverage growing biomarker panel volumes to cement lucrative send-out contracts. Tele-urology networks and outpatient surgical facilities are emerging fringe players, riding cost-minimization mandates and patient convenience trends. Collectively, the evolving provider ecosystem diversifies revenue channels, enhancing resilience across the prostate cancer market.

Geography Analysis

North America dominated with a 41.88% share of 2025 global revenues, reflecting universal coverage of guideline-endorsed diagnostics, early integration of PSMA-PET, and rapid uptake of androgen receptor pathway inhibitors. Medicare’s expansion of molecular test reimbursement has amplified biopsy triage accuracy, while the Veterans Affairs system continues to refine active-surveillance protocols to guard against overtreatment. United States oncology networks employ health-technology assessments to align formulary inclusion with real-world outcomes, generating data transparency that sustains payer confidence. Canada reinforces fiscal discipline through sequence-based cost-effectiveness models that optimize therapy order and duration. As a result, market growth in the region is driven more by innovation cycling than demographic expansion. Yet, absolute spend per patient remains at the global peak, anchoring manufacturer launch strategies inside the prostate cancer market.

Europe leverages harmonized screening frameworks under European Commission guidance, providing consistent baseline demand despite heterogeneous reimbursement climates. Germany’s Federal Joint Committee rigorously evaluates cost-utility profiles, yet approved radioligands and advanced imaging quickly secure DRG-linked payment once value is demonstrated. Eastern European states, however, face higher mortality and lower PSA screening coverage, pointing to inequities that represent latent growth pockets. Collaborative procurement for radiotracers and genomic kits is gaining momentum, promising cross-border volume aggregation that could narrow access gaps.

Asia-Pacific supplies the fastest regional CAGR at 10.08% through 2031, underpinned by ageing demographics and health-system modernization. China’s tiered hospital reform is funnelling complex oncology procedures to tertiary centres where PSMA-PET scanners and linear accelerators cluster, rapidly lifting diagnostic and radiotherapy volumes. Japan’s national insurance already lists darolutamide and olaparib combinations, aiding swift diffusion of premium therapeutics. In India, private urology groups partner with tele-pathology providers to extend biomarker testing beyond metros. Rezvilutamide’s favourable USD 26,657 per QALY profile has swayed Chinese payers, illustrating readiness to reimburse cost-effective innovations. Strong growth therefore reflects both rising incidence and escalating technology penetration, cementing Asia-Pacific as the pivotal demand engine for the market.

Competitive Landscape

Johnson & Johnson’s Erleada maintains lead share within the androgen receptor inhibitor class, yet Pfizer-Astellas’ Xtandi challenges via extensive real-world dataset publications that underscore broader sequencing optionality. AstraZeneca’s USD 2.4 billion acquisition of Fusion Pharmaceuticals provides it with immediate radioligand manufacturing capacity, positioning the firm for next-generation combinations that integrate diagnostic isotopes with alpha-emitting therapeutics. Bayer capitalized on ARANOTE trial success to secure FDA approval of Nubeqa for metastatic castration-sensitive disease, effectively opening a new prescriber base outside traditional non-metastatic segments.

Diagnostic disruptors such as Paige are scaling FDA-cleared digital pathology suites that halve slide-review time and normalize Gleason grading across community labs. Interoperability initiatives, such as USCDI+ Cancer, foster FHIR-based data exchange, drawing electronic health record vendors into oncology workflow integration and potentially lowering onboarding friction for new diagnostic algorithms. The competitive field now favours firms capable of bundling therapy and companion diagnostics under value-based contracts, a model gaining traction in high-volume US centres and select EU early-adopter regions.

White-space opportunities persist in affordability solutions for emerging markets, where generic formulations, modular imaging kits, and mobile biopsy vans can break logistical bottlenecks. Intellectual-property cliffs for first-generation hormone therapies spur biosimilar ventures, while academic-industry alliances explore PSMA-targeted bispecifics to surmount resistance. Overall, the prostate cancer market rewards differentiated science coupled with access-minded pricing, keeping competitive intensity at a moderate yet rising level.

Prostate Cancer Industry Leaders

Bayer AG

AstraZeneca PLC

Sanofi-Aventis

Thermo Fisher Scientific

F. Hoffmann-La Roche Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Novartis’ Pluvicto secured FDA expansion for earlier treatment lines, broadening radioligand therapy reach.

- January 2025: Bayer confirmed third indication launch plans for darolutamide in 2025 after positive ARANOTE data.

- January 2025: The FDA assigned an Aug 29 2025 PDUFA date to the three-month leuprolide mesylate depot formulation.

- September 2024: Veracyte reported that its Decipher Prostate Genomic Classifier predicts chemotherapy benefit in metastatic settings.

Global Prostate Cancer Market Report Scope

As per the scope of the report, prostate cancer begins when normal cells in the prostate begin to multiply uncontrollably. The scope of the study is limited to revenue generated by various diagnostic and therapeutic products used in the management of benign prostatic hyperplasia, prostatic adenocarcinoma, and small cell carcinoma, among other types of prostate cancer. The prostate cancer market is segmented by Type (Benign Prostatic Hyperplasia, Prostatic Adenocarcinoma, Small Cell Carcinoma, and Other Types), Modality (Diagnosis and Treatment), and Geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above-mentioned segments.

| Benign Prostatic Hyperplasia |

| Prostatic Adenocarcinoma |

| Small Cell Carcinoma |

| Other Types |

| Localized (T1–T2) |

| Regional (T3) |

| Distant/Metastatic (T4 & M1) |

| Diagnostics | Tissue Biopsy | |

| Transrectal Ultrasound | ||

| Clinical Laboratory Examination | Prostate-specific Antigen Testing | |

| Urine Biomarker Testing | ||

| Diagnostic Imaging | ||

| Treatment | Surgery (Radical, Laparoscopic, Robotic) | |

| Radiation Therapy (EBRT, Brachytherapy) | ||

| Therapeutics | Hormone / Androgen-Deprivation Therapy | |

| Chemotherapy | ||

| Immunotherapy / Targeted Therapy | ||

| Other Treatments (HIFU, Cryotherapy) | ||

| Hospitals |

| Specialty Cancer Centers & Clinics |

| Diagnostic Laboratories |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Disease Type | Benign Prostatic Hyperplasia | ||

| Prostatic Adenocarcinoma | |||

| Small Cell Carcinoma | |||

| Other Types | |||

| By Stage | Localized (T1–T2) | ||

| Regional (T3) | |||

| Distant/Metastatic (T4 & M1) | |||

| By Modality | Diagnostics | Tissue Biopsy | |

| Transrectal Ultrasound | |||

| Clinical Laboratory Examination | Prostate-specific Antigen Testing | ||

| Urine Biomarker Testing | |||

| Diagnostic Imaging | |||

| Treatment | Surgery (Radical, Laparoscopic, Robotic) | ||

| Radiation Therapy (EBRT, Brachytherapy) | |||

| Therapeutics | Hormone / Androgen-Deprivation Therapy | ||

| Chemotherapy | |||

| Immunotherapy / Targeted Therapy | |||

| Other Treatments (HIFU, Cryotherapy) | |||

| By End User | Hospitals | ||

| Specialty Cancer Centers & Clinics | |||

| Diagnostic Laboratories | |||

| Other End Users | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large is the Prostate Cancer Therapy market in 2026?

The prostate cancer market size reached USD 25.73 billion in 2026 and is on track for USD 38.33 billion by 2031.

What is the expected growth rate through 2031?

The market is forecast to expand at an 8.29% CAGR between 2026 and 2031.

Which region is growing fastest?

Asia-Pacific posts the highest regional CAGR at 10.08%, propelled by expanding diagnostic access and rising incidence.

Which disease stage segment is expanding most quickly?

Distant/metastatic presentations are advancing at an 8.57% CAGR thanks to improved imaging and novel systemic therapies.

Who are the key therapy innovators to watch?

Bayer, Johnson & Johnson, AstraZeneca, and Novartis lead late-stage pipelines, while startups like Paige drive diagnostic innovation.

How are costs influencing adoption in emerging markets?

High aggregate treatment costs remain a restraint, but generic hormone therapies and modular imaging solutions are improving affordability.

Page last updated on: