Process Analytical Instrumentation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

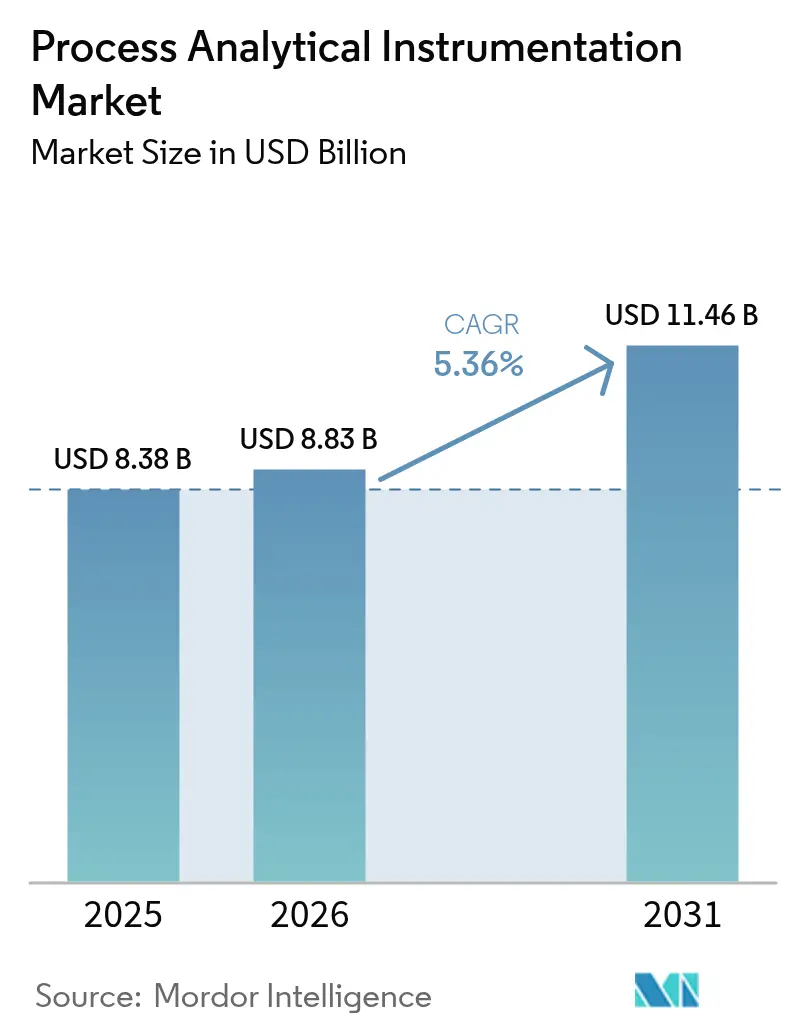

| Market Size (2026) | USD 8.83 Billion |

| Market Size (2031) | USD 11.46 Billion |

| Growth Rate (2026 - 2031) | 5.36% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Process Analytical Instrumentation Market Analysis by Mordor Intelligence

The process analytical instrumentation market size is expected to grow from USD 8.38 billion in 2025 to USD 8.83 billion in 2026 and is forecast to reach USD 11.46 billion by 2031 at 5.36% CAGR over 2026-2031. Strong adoption of real-time monitoring, ever-tighter global regulations, and data-driven operational strategies keep propelling the process analytical instrumentation market, even as industries grapple with rising system complexity and cybersecurity risks. Convergence of operational and information technology has converted formerly stand-alone analyzers into digital nodes that feed broader Industry 4.0 ecosystems, allowing high-fidelity feedback loops and predictive maintenance routines that shrink downtime and waste. This technology shift is reinforced by capital-intensive projects in hydrocarbon processing, biopharmaceutical continuous manufacturing, and green-hydrogen electrolyzer build-outs, all of which demand robust in-line analytics. Asia-Pacific’s push to align with North American and European emission rules is reshaping supplier footprints, while global helium scarcity continues to influence chromatograph procurement decisions.

Key Report Takeaways

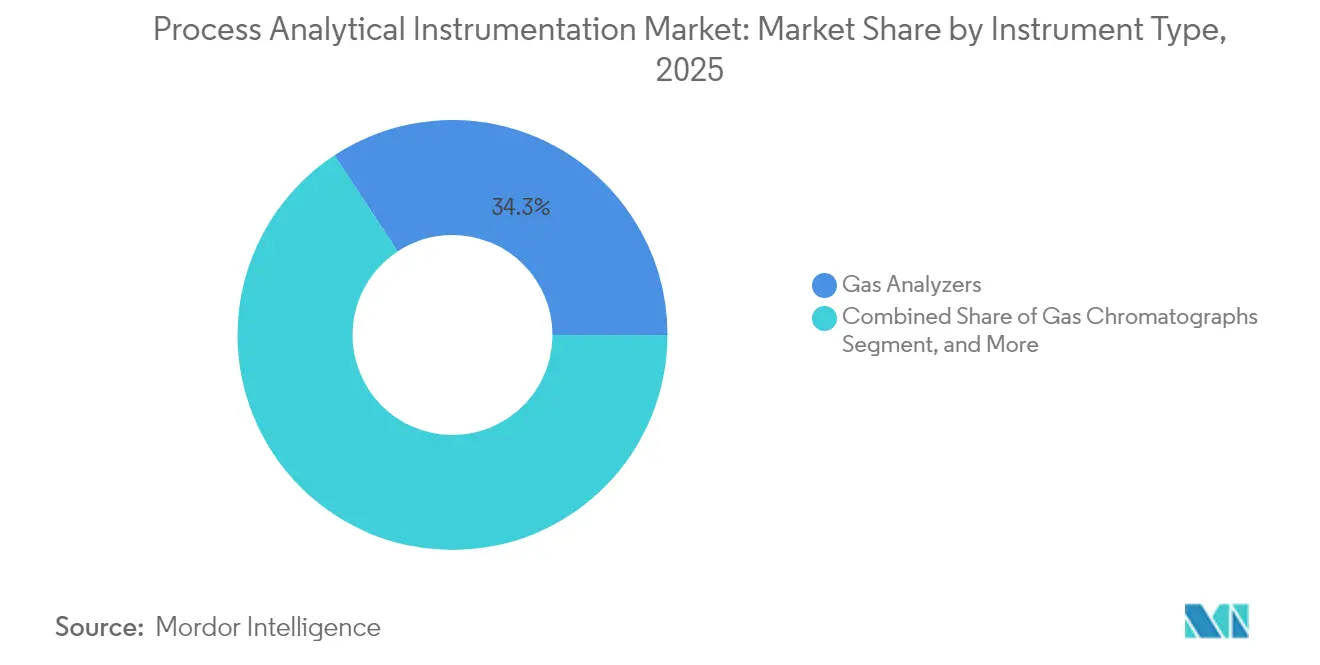

- By instrument type, gas analyzers held 34.25% of the process analytical instrumentation market share in 2025, whereas spectrometers are advancing at a 6.38% CAGR through 2031.

- By component, hardware captured 51.35% revenue share in 2025; software is projected to expand at a 6.55% CAGR to 2031.

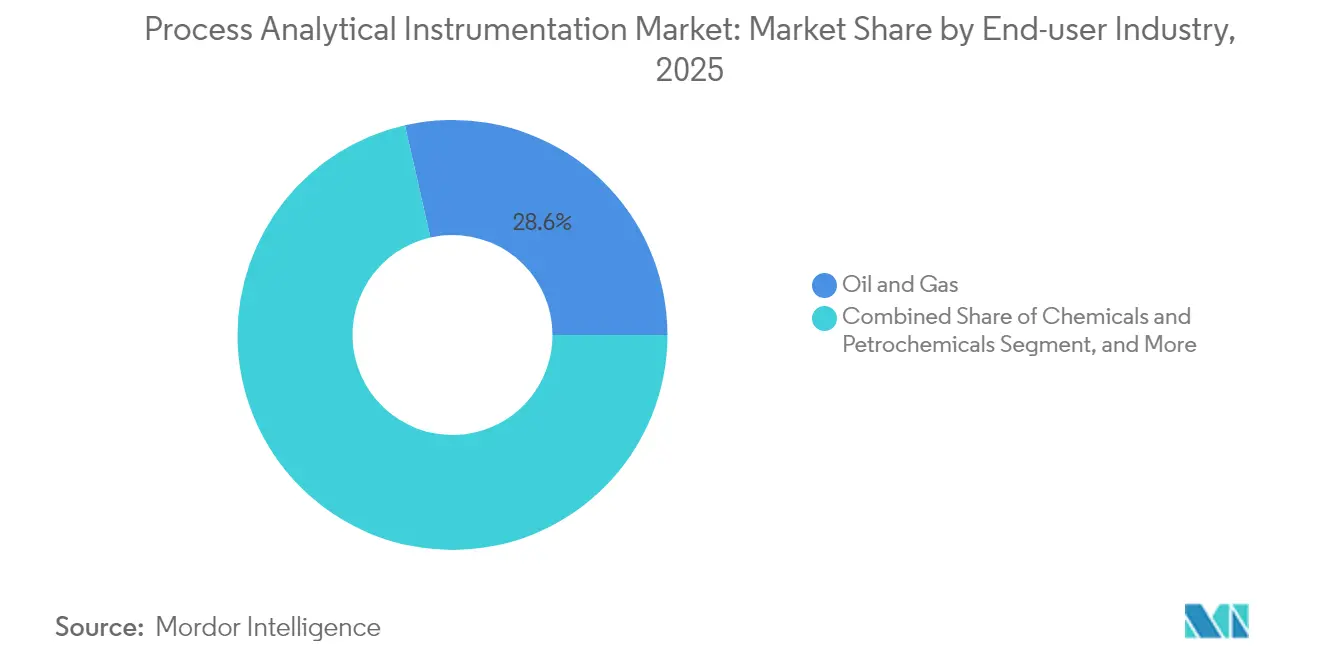

- By end-user industry, oil and gas accounted for 28.55% of the process analytical instrumentation market size in 2025, while pharmaceutical and biotechnology applications posted the fastest 7.84% CAGR forecast.

- By installation type, in-line/on-line configurations commanded a 54.85% share of the process analytical instrumentation market size in 2025 and are growing at a 7.42% CAGR through 2031.

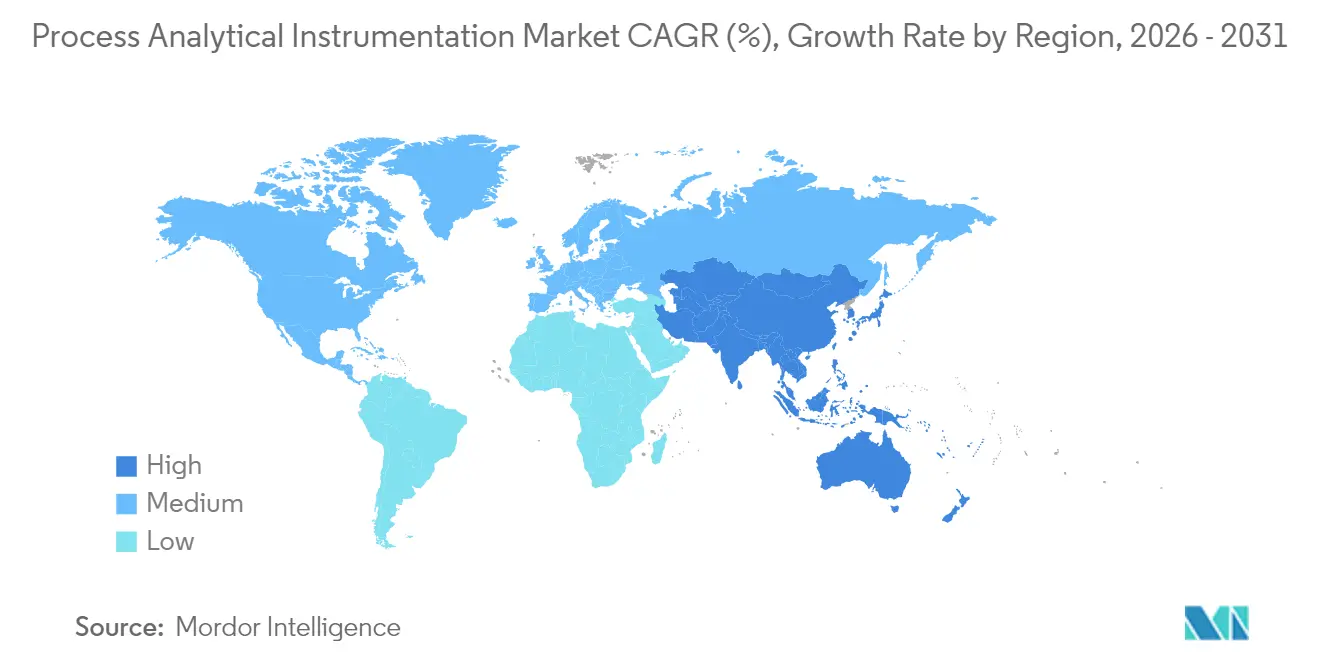

- By geography, North America led with 41.05% market share in 2025; Asia-Pacific is scaling with an 8.21% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Process Analytical Instrumentation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory push for in-process quality and emission compliance | +1.20% | Global, with emphasis on North America and Europe | Medium term (2-4 years) |

| Digitalization and Industry 4.0 adoption across process industries | +1.50% | Global, led by North America and Asia-Pacific | Long term (≥ 4 years) |

| Rising demand for real-time analytics in oil, gas and petrochemicals | +0.90% | Global, concentrated in Middle East, North America, and Asia-Pacific | Short term (≤ 2 years) |

| Rapid expansion of biopharma continuous manufacturing lines | +0.80% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Green-hydrogen electrolyzer build-outs needing high-purity gas analysis | +0.60% | Europe and Asia-Pacific, emerging in North America | Long term (≥ 4 years) |

| Deployment of digital-twin models requiring high-fidelity inline data | +0.70% | Global, led by advanced manufacturing regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory push for in-process quality and emission compliance

A wave of fresh environmental statutes is forcing continuous monitoring across smokestacks, flares, and bioreactors, immediately enlarging the addressable base of the process analytical instrumentation market.[1]TSI Editorial, “The New EU Ambient Air Quality Directive,” TSI Resources, Jan 1, 2025, tsi.com The EU’s Ambient Air Quality Directive of 2024 compels ultrafine-particle counting, while Canada’s CEMS code tightens calibration cycles for SO₂, NOx, and CO probes. Similar rulemaking in Asia is closing historical enforcement gaps, moving thousands of plants toward mandatory continuous emission monitoring. Vendors able to supply analyzers pre-certified to ISO 17025 and EN 15267 standards shorten customers’ route to compliance. Beyond environmental stacks, the same regulatory intent is seeping into pharmaceutical GMP and food safety standards, where inline analytics mitigate batch rejection costs.

Digitalization and Industry 4.0 adoption across process industries

As cloud-native SCADA platforms and industrial IoT gateways proliferate, the process analytical instrumentation market gains new connectivity mandates, compelling instrument makers to embed OPC UA, MQTT, and secure IP stacks.[2]ABB Newsroom, “ABB Reports Strong Q4 2024 Results and Provides 2025 Guidance,” ABB News, Jan 1, 2025, abb.com Plants pairing analyzers with digital twins derive multivariate insights, such as feed-quality drift or catalyst aging, well before the product degrades. Software vendors’ AI-enhanced chemometric engines now automate spectrum interpretation, expanding advanced analysis beyond PhD-level specialists. However, network exposure heightens cyber-risk, so firms promoting IEC 62443-certified appliances gain competitive credibility. This dual connectivity-and-security requirement propels recurring software and service revenues, tilting value creation from hardware toward digital offerings.

Rising demand for real-time analytics in oil, gas and petrochemicals

Hydrocarbon producers deploying inline spectrometers and chromatographs quantify blend ratios, sulfur content, and vapor pressure in minutes rather than hours, unlocking millions in annual yield improvement.[3]AspenTech Analysts, “Petrochemical Fuel Reduction Case Study,” AspenTech Resources, Jan 1, 2025, aspentech.com Case studies from Cenosco report USD 2.35 million yearly savings, while other refiners achieve USD 9.3 million in uplift by linking analyzer data to advanced process control loops. In upstream gas treatment, real-time dew-point monitors avert glycol overuse, trimming operating expenses and flare volumes. These quantifiable wins accelerate capital approval for analyzer projects, offsetting helium-supply concerns in gas chromatography by driving uptake of micro-GC and hydrogen carrier systems.

Rapid expansion of biopharma continuous manufacturing lines

Regulators encourage drug makers to shift from batch to continuous production, provided real-time release testing verifies quality every second.[4]BioProcess International Editors, “Continuous Manufacturing PAT Adoption,” BioProcess International, Jan 1, 2025, bioprocessintl.com Raman and NIR probes now thread through crystallizers and dryers, capturing critical quality attributes with sub-second latency. Pharmaceutical majors record double-digit throughput gains and six-figure annual material savings, as seen in Valtris Champlor’s EUR 90,000 (USD 96,300) reduction in solvent usage. Clear EU Pharmacopoeia guidelines for handheld Raman tools simplify validation, leveling barriers for smaller biotech firms. This sustained investment stream reinforces the long-term growth vector of the process analytical instrumentation market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and lifecycle costs of sophisticated analyzers | -0.80% | Global, particularly impacting emerging markets | Short term (≤ 2 years) |

| Shortage of skilled calibration and maintenance personnel | -0.60% | Global, acute in North America and Europe | Medium term (2-4 years) |

| Cyber-security vulnerabilities in networked analyzers | -0.40% | Global, critical in regulated industries | Short term (≤ 2 years) |

| Global helium scarcity impacting GC operations | -0.50% | Global, severe impact on analytical laboratories | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High capital and lifecycle costs of sophisticated analyzers

Complete CEMS platforms or triple-quadrupole mass spectrometers require outlays that exceed USD 500,000, with annual service costs reaching 20% of the purchase price. Emerging economies face currency volatility, import duties, and a dearth of local service hubs that inflate delivered pricing. In continuous-process plants where downtime penalties are brutal, redundancy becomes mandatory, doubling capital requirements. These economics delays analyzer adoption among small-scale chemical, food, and specialty-materials producers.

Shortage of skilled calibration and maintenance personnel

Multidisciplinary expertise, spanning spectroscopy, electronics, software, and compliance, is scarce and aging out of the workforce.[5]BioProcess International Editors, “Continuous Manufacturing PAT Adoption,” BioProcess International, Jan 1, 2025, bioprocessintl.com Plants in remote basins struggle to retain analysts willing to work rotating shifts under safety-critical conditions. Limited academic programs for process analytical technology exacerbate the pipeline problem. Vendor-run remote diagnostics and augmented-reality field tools offer partial relief, yet cannot fully replace on-site technicians, tempering the growth trajectory of the process analytical instrumentation market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Instrument Type: Gas analyzers cement leadership as spectrometers accelerate

Gas analyzers held a 34.25% process analytical instrumentation market share in 2025, underpinned by universal emission-monitor mandates and pervasive process-optimization routines across refineries, chemical crackers, and power boilers. Their share advantage stems from the necessity of continuous SO₂, NOx, CO, and CO₂ readouts to comply with environmental permits and carbon-pricing schemes. Spectrometer demand, while smaller, is climbing at a 6.38% CAGR to 2031 as portable XRF and handheld Raman devices push elemental and molecular identification to loading docks and utility skids.

In the second half of the decade, utilities retrofitting hydrogen co-firing lines and electrolyzer OEMs will widen the gas-analyzer installed base, yet spectrometers may erode share in biotech and battery-materials lines where real-time impurity tracking becomes critical. Micro-GC architectures, hydrogen carrier gases, and smart valve ovens counter helium shortages while preserving separation performance. The combined evolution sustains hardware sales yet shifts value toward application-specific chemometrics, reinforcing the strategic importance of software inside the process analytical instrumentation market.

By Component: Hardware is still dominant, software captures velocity

Hardware contributed 51.35% to 2025 revenue, mirroring large sensor counts and the mechanical complexity of sample-conditioning systems that make up each analyzer skid. Sophisticated optics, ruggedized gas-cells, and explosion-proof enclosures keep average selling prices high. The process analytical instrumentation market size for software, however, is posting a 6.55% CAGR because embedded AI engines translate raw spectra into actionable set-point changes. Suppliers such as Bruker, integrating the SciY data platform across its portfolio, are packaging subscription-based chemometrics that boost gross margin and create annuity revenue.

Service contracts wrap calibration, validation, and cyber-patching into multi-year agreements; Emerson alone booked USD 4.06 billion from measurement & analytical services in 2024. The industry’s skills gap elevates service intensity, giving vendors that maintain global field networks a structural advantage. As predictive-maintenance algorithms mature, software-as-a-service offerings will likely outgrow hardware capital sales beyond 2030.

By End-User Industry: Oil and gas retains scale, pharma gains momentum

Oil and gas operations accounted for 28.55% of 2025 revenue, making the sector the single largest consumer of continuous gas chromatography, mass-spectrometry, and tunable-diode laser absorption setups. Refiners depend on octane and sulfur loop analytics to prove fuel compliance, while LNG terminals deploy fast spectrometers for custody-transfer calorific calculations.

Pharmaceutical and biotech lines are recording an 7.84% CAGR, driven by continuous manufacturing cells and regulatory backing for real-time release testing. Inline Raman verifies polymorph ratios, and NIR models quantify moisture without sampling, compressing batch-release times from days to minutes. Water & wastewater operators, metals & mining concentrators, and food & beverage processors each enlarge addressable niches by turning to analyzers for effluent compliance and ingredient integrity.

By Installation Type: In-line supremacy reflects real-time imperative

In-line assemblies commanded a 54.85% share in 2025, and the process analytical instrumentation market size for in-line solutions is set to grow 7.42% annually as users switch from lab-based assays to continuous quality assurance. Spectroscopic probes now screw directly into reactors or pipelines, enabling closed-loop control that removes manual sampling drag. Multiplexers allow a single spectrometer to supervise up to six positions, spreading capex while widening insight bandwidth.

At-line carts still thrive in sectors needing frequent but not continuous QC; for example, pulp-and-paper mills park near-infrared benches beside coaters, running five-minute checks on brightness. Central laboratories persist for forensic tasks, trace-level heavy-metal determinations, or method-development cycles, yet their relative footprint inside the process analytical instrumentation market is shrinking as sensors penetrate plant floors.

Geography Analysis

North America held a 41.05% share in 2025 as the U.S. EPA’s 40 CFR Part 60/75 rules and OSHA exposure limits necessitated continuous analyzers across refineries, chemical parks, and power plants. Ample capital budgets, established service infrastructures, and long-tenured workforces allow quick integration of AI-supported chemometrics. Persistent helium tightness and labor shortages do temper replacement cycles, but vendor-managed service agreements buffer downtime risk.

Asia-Pacific is growing 8.21% per year, making it the fastest-scaling geography in the process analytical instrumentation market. China’s reinforced pollution-control ordinances, India’s consent-to-operate mandates, and Japan’s JAIMA-led standardization initiatives collectively open sizeable order backlogs. Continuous analyzers are being embedded not only in mega-refineries and steelworks but also in smaller specialty-chemical parks keen to meet export-market QC demands. Regional suppliers partner with global OEMs to localize service, easing import-duty burdens and language barriers.

Europe maintains steady expansion anchored to the October 2024 Ambient Air Quality Directive, which compels ultrafine-particle measurement across 27 member states. Petrochemical clusters along the Rhine and in Iberia replace legacy opacity meters with modern FTIR cells to satisfy CO₂ taxation reporting. Simultaneously, green-hydrogen electrolyzer projects in Germany and Spain demand high-purity oxygen and hydrogen validation, catalyzing analyzer uptake. Eastern European processors, eager to secure REPowerEU funding, adopt Western emission standards, adding incremental volume for vendors.

Competitive Landscape

A moderate level of consolidation characterizes the process analytical instrumentation market, with ABB, Siemens, Emerson, and Endress+Hauser controlling a sizable installed base that grants cross-selling leverage. These incumbents embed AI crime-resistant firmware and OPC UA servers into new product lines, differentiating through secure integration with plant-wide DCS and MES layers. Multiple tuck-in acquisitions, such as ATS Corporation’s 2024 purchase of Heidolph, illustrate a strategy of filling application gaps, especially in biotech and spatial-chemistry niches.

Mid-tier challengers intensify competition by rolling out cyber-hardened portable analyzers that reach maintenance technicians and field engineers otherwise underserved by fixed-installation OEMs. Fortive, for instance, aligns internal data-science teams to monetize post-deployment analytics subscriptions, aiming for USD 100 million in AI service revenue by 2030. Investor enthusiasm remains robust; KPMG reports 21.1× EV/LTM EBITDA multiples for instrumentation companies, encouraging serial acquisitions that extend geographic footprints and widen installed service bases.

Start-ups focusing on helium-free micro-GC modules, battery-materials spectrometers, and cloud-delivered chemometrics exploit niche white spaces. Yet they often partner with larger distributors to overcome qualification hurdles in heavily regulated verticals. Intellectual-property accumulation, evident from rising IEEE industrial-automation cybersecurity filings, reinforces barriers to entry and underscores the premium placed on standards-body participation within the process analytical instrumentation market.

Process Analytical Instrumentation Industry Leaders

ABB Ltd

Siemens AG

Emerson Electric Co.

Endress+Hauser Group Services AG

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: European Pharmacopoeia updated handheld Raman guidance, simplifying GMP validation. Strategy: lowers adoption barriers, expanding pharma inline analytics TAM.

- March 2025: Agilent’s Q1 FY2025 sales hit USD 1.68 billion, buoyed by LC-MS platform refreshes, signaling continued demand for lab-adjacent real-time assays that bridge to process lines. Strategy: leverage analytical method continuity from lab to plant, easing customer validation.

- February 2025: Honeywell recorded USD 10.051 billion Industrial Automation revenue in 2024 despite a 7% organic dip but kept R&D spend above USD 1.5 billion to accelerate secure analyzer integration. Strategy: maintain innovation cadence to defend regional share against niche cyber-hardened entrants.

- January 2025: Bruker posted Q4 2024 revenue of USD 979.6 million, up 14.6% year-over-year, and outlined a spatial-biology expansion strategy to deepen application reach in cell-factory analytics. Strategy: bolsters portfolio breadth, locking in cross-platform service contracts.

Global Process Analytical Instrumentation Market Report Scope

Process analytical technology falls under analyzers, monitors, and other instruments used for industrial purposes by oil, gas, chemical, petrochemical, pharmaceutical, semiconductor, factory automation, and other process industries. These products are often utilized parallel with various oil field instruments, infrared temperature measurement devices, subsea and ultra-deepwater fluid, flow measurement equipment, and specialized sampling, extraction, transport, and conditioning systems.

The process analytical instrumentation market is segmented by type (gas chromatographs, gas analyzers, liquid analyzers, and spectrometers), end-user industry (oil & gas, chemicals & petrochemicals, pharmaceutical & biotechnology, metal & mining, water & wastewater, and other end-user industries), and geography (North America, Europe, Asia-Pacific, and Rest of the World). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Gas Chromatographs |

| Gas Analyzers |

| Liquid Analyzers |

| Spectrometers |

| Hardware |

| Software |

| Services |

| Oil and Gas |

| Chemicals and Petrochemicals |

| Pharmaceutical and Biotechnology |

| Metals and Mining |

| Water and Wastewater |

| Food and Beverage |

| Power Generation |

| In-line/On-line |

| At-line |

| Laboratory |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Instrument Type | Gas Chromatographs | ||

| Gas Analyzers | |||

| Liquid Analyzers | |||

| Spectrometers | |||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By End-user Industry | Oil and Gas | ||

| Chemicals and Petrochemicals | |||

| Pharmaceutical and Biotechnology | |||

| Metals and Mining | |||

| Water and Wastewater | |||

| Food and Beverage | |||

| Power Generation | |||

| By Installation Type | In-line/On-line | ||

| At-line | |||

| Laboratory | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the process analytical instrumentation market and its growth outlook?

The process analytical instrumentation market size is USD 8.83 billion in 2026 and is expected to reach USD 11.46 billion by 2031, registering a 5.36% CAGR over 2026-2031.

Which region is growing fastest in process analytical instrumentation adoption?

Asia-Pacific leads with an 8.21% CAGR driven by industrialization and stricter environmental regulations.

Which instrument type dominates global demand?

Gas analyzers hold the largest share at 34.25% in 2025 due to universal emissions monitoring requirements.

Why are in-line installations favored over laboratory analyzers?

In-line setups deliver real-time data that supports immediate process adjustments, raising yield and lowering rejection rates.

How is the pharmaceutical sector influencing market expansion?

Continuous manufacturing and real-time release testing are pushing pharma to adopt Raman and NIR probes, driving an 7.84% CAGR for the segment.

What major challenge could slow market growth?

High capital costs and shortages of skilled calibration personnel jointly constrain rapid deployment, particularly in emerging markets.

Page last updated on: