Supervisory Control And Data Acquisition (SCADA) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

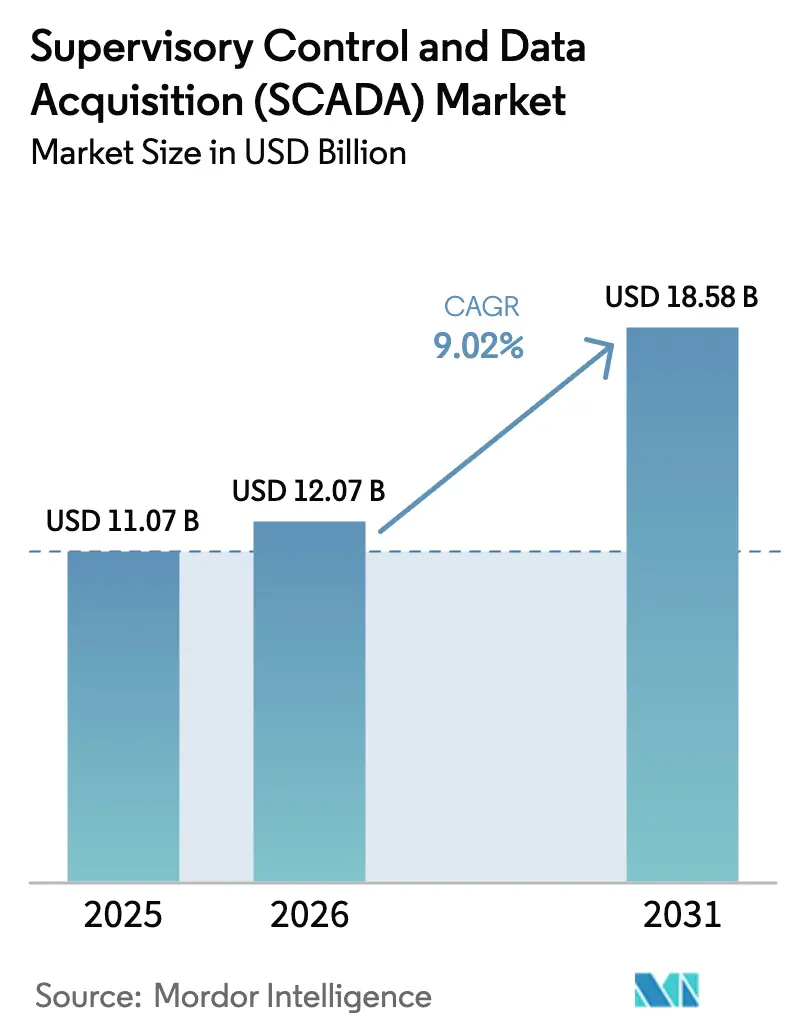

| Market Size (2026) | USD 12.07 Billion |

| Market Size (2031) | USD 18.58 Billion |

| Growth Rate (2026 - 2031) | 9.02% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Supervisory Control And Data Acquisition (SCADA) Market Analysis by Mordor Intelligence

The supervisory control and data acquisition market size was valued at USD 11.07 billion in 2025 and estimated to grow from USD 12.07 billion in 2026 to reach USD 18.58 billion by 2031, at a CAGR of 9.02% during the forecast period (2026-2031). This sustained expansion reflects the global push for digital transformation in critical infrastructure, tighter safety rules in energy pipelines, and the spread of private 5G in factories.[1]Pipeline and Hazardous Materials Safety Administration, “Valve Rule Overview,” phmsa.dot.gov Edge computing, cloud-native architectures, and managed cybersecurity services are now core design elements rather than optional upgrades. Asia-Pacific leads adoption because of large-scale Industry 4.0 programs, while cloud migration in European utilities and renewable megaprojects in the Gulf states add new demand streams. Private wireless connectivity and AI-enabled maintenance analytics are reshaping platform roadmaps, pushing vendors to deliver modular, service-centric offerings that lower total cost of ownership and simplify compliance.

Key Report Takeaways

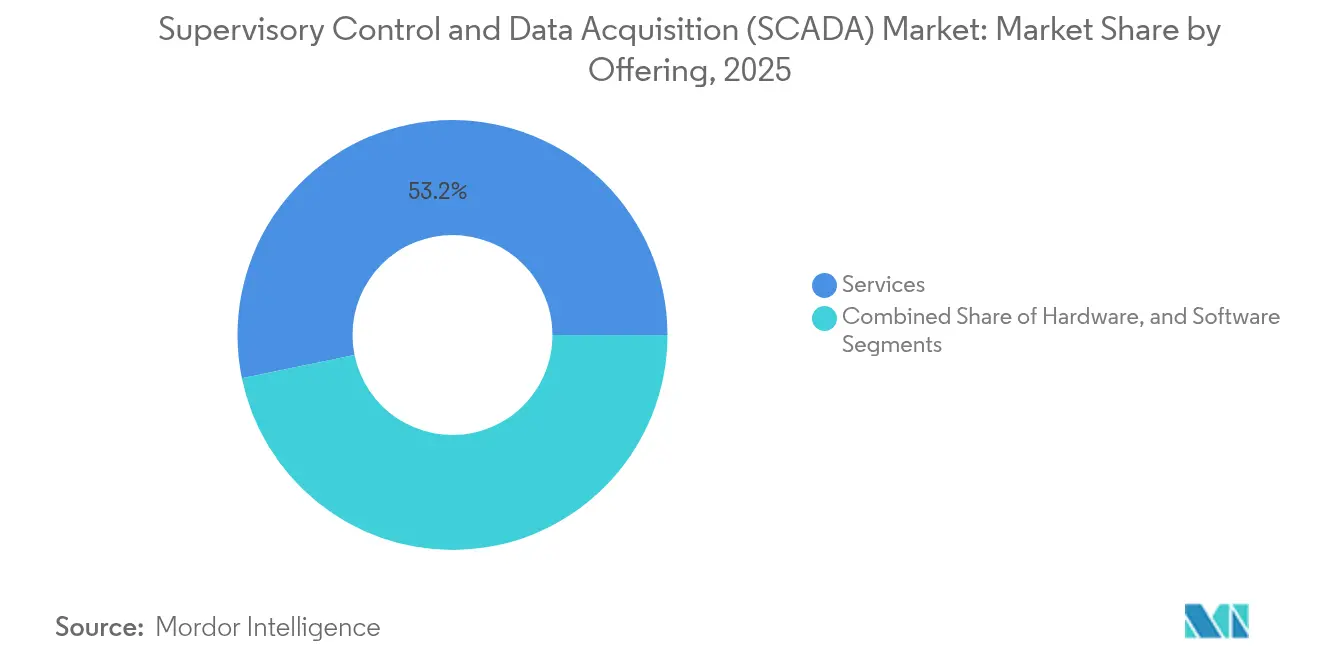

- By offering, Services led with 53.22% of supervisory control and data acquisition market share in 2025, and the segment is projected to expand at a 9.08% CAGR through 2031.

- By component, Programmable Logic Controllers held 30.65% revenue share in 2025, while Communication Systems are on track for the highest 9.41% CAGR to 2031.

- By deployment mode, On-premise solutions accounted for 77.05% of the supervisory control and data acquisition market size in 2025, but Cloud platforms are set to grow fastest at 12.58% CAGR.

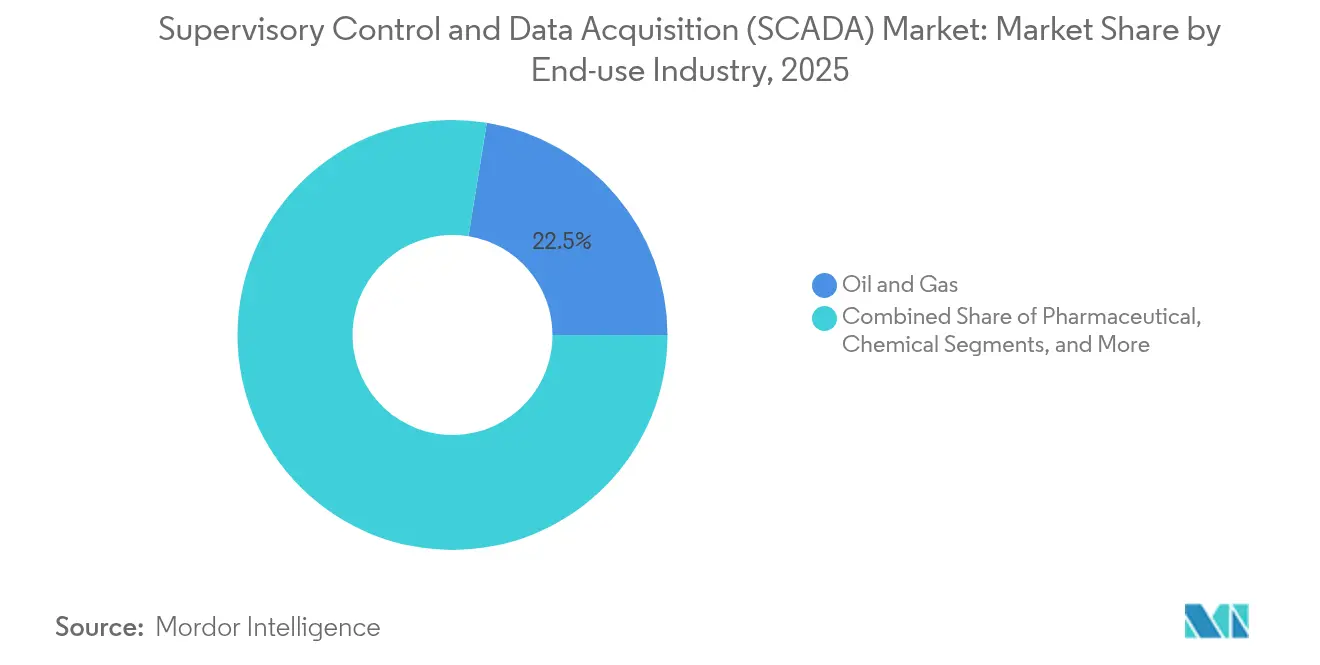

- By end-use industry, Oil and Gas captured 22.45% of supervisory control and data acquisition market share in 2025; Water and Wastewater utilities will likely post the quickest 10.08% CAGR to 2031.

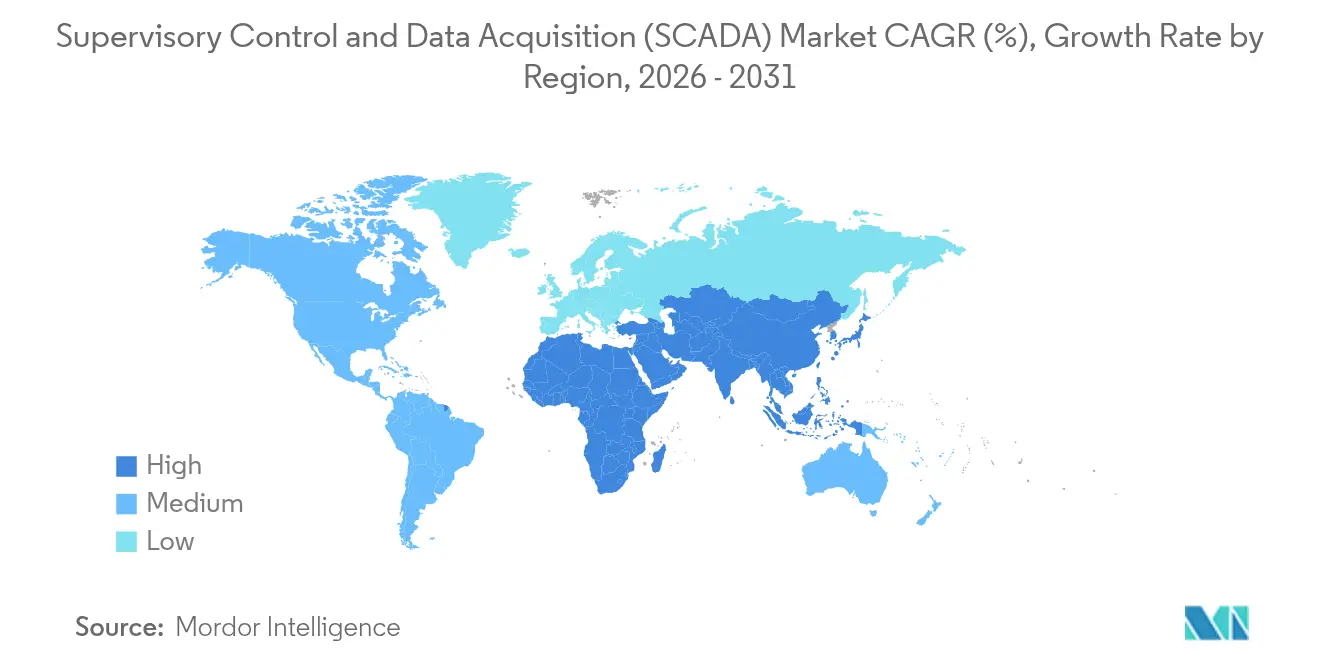

- By geography, Asia-Pacific dominated with 33.85% revenue share in 2025, whereas the Middle East and Africa region is forecast to record a 9.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Supervisory Control And Data Acquisition (SCADA) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Deployment of Edge Computing-enabled SCADA in North American Power Grids | +1.8% | North America, with spillover to Europe | Medium term (2-4 years) |

| Mandatory Pipeline Safety and Integrity Regulations Driving SCADA Upgrades in United States Oil and Gas | +1.5% | United States, with regulatory influence in Canada and Mexico | Short term (≤ 2 years) |

| Rapid Integration of 5G and Private LTE Networks in Asia-Pacific Smart Manufacturing | +2.1% | Asia-Pacific core, with early adoption in China, Japan, and South Korea | Medium term (2-4 years) |

| Rising Adoption of Cloud-native SCADA for Water and Wastewater Utilities in Europe | +1.2% | Europe, with early gains in UK, Germany, and Nordic countries | Long term (≥ 4 years) |

| Cyber-secure Remote Operations Post-COVID-19 Boosting Managed SCADA Services | +1.4% | Global, with strongest demand in developed markets | Short term (≤ 2 years) |

| Government-backed Renewable Energy Megaprojects in Middle East Requiring Utility-Scale SCADA | +1.7% | Middle East and Africa, concentrated in UAE, Saudi Arabia, and Egypt | Long term (≥ 4 years |

| Source: Mordor Intelligence | |||

Accelerated Deployment of Edge Computing-enabled SCADA in North American Power Grids

Utilities in the United States and Canada are embedding micro-data-centers at substations to process real-time control loops locally. Latency drops to sub-millisecond levels, which is essential for balancing renewable generation and maintaining frequency stability.[2]Rockwell Automation, “How Edge Computing Enhances HMI/SCADA Solutions,” rockwellautomation.com Edge nodes also run predictive maintenance models that detect asset failure risk without relying on a central cloud. Southern Linc’s migration of 20,000 SCADA devices to a dedicated LTE backbone shows how telecom upgrades and edge analytics work in tandem.[3]Ericsson, “Keeping the Lights On with Dedicated LTE,” ericsson.com Utilities see cost savings from reduced truck rolls and improved power-quality compliance. The shift positions edge computing as a baseline requirement for next-generation grid modernization.

Mandatory pipeline safety and integrity regulations in the United States oil and gas

Security Directives Pipeline-2021-01D and 02E compel operators to install real-time threat monitoring, rupture-mitigation valves, and 30-minute response protocols that legacy SCADA cannot support. These mandates directly trigger multiyear capital programs for cybersecurity-enabled upgrades and automated emergency shutdown logic. Operators now integrate advanced intrusion detection with control room systems so that physical and cyber events receive the same automated workflow. The regulation also influences Canadian and Mexican pipelines that connect with U.S. networks, spreading demand for compatible platforms. Suppliers offering pre-certified compliance templates gain a procurement advantage.

Rapid integration of 5G and private LTE in Asia-Pacific smart manufacturing

China, Japan, and South Korea are rolling out private 5G networks across brownfield and greenfield plants to enable mobile robots and high-definition machine vision. Midea’s Shunde factory already saved RMB 32 million yearly and lifted productivity by 15-20% through 5G-connected industrial IoT.[4]GSMA, “Industrial IoT,” gsma.com Deterministic wireless links meet sub-10 ms latency targets, which is critical for supervisory control and data acquisition market applications in discrete assembly lines. Certification work by Rockwell Automation, Ericsson, and Qualcomm confirmed EtherNet/IP traffic integrity over 5G slices. As more plants adopt agile production, communication infrastructure shifts from wired fieldbuses to spectrum-controlled wireless cells.

Rising use of cloud-native SCADA for European water utilities

Utilities in the UK, Germany, and Nordic nations migrate supervisory control and data acquisition market workloads to multi-tenant cloud platforms that scale with asset expansions and regulatory reporting needs. Veolia’s AQUAVISTA Plant delivered 20-50% savings by optimizing chemical dosing and energy usage via cloud-hosted analytics. United Utilities adopted Itron’s Temetra cloud meter data solution for 1.6 million meters, gaining rapid billing accuracy and customer transparency. Centralized patching and zero-trust gateways improve cybersecurity posture, which satisfies emerging EU regulations. Long-term, cloud adoption reduces dependency on ageing control room hardware and frees budgets for network renewal.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy Infrastructure Lock-in Hindering Cloud Migration in Brownfield Plants | -1.3% | Global, with highest impact in North America and Europe | Long term (≥ 4 years) |

| Shortage of OT-Cybersecurity Talent Limiting Modernization in South America | -0.8% | South America, with spillover effects in Central America | Medium term (2-4 years) |

| High TCO for Real-time Redundant SCADA in Municipal Water Districts | -0.9% | Global, particularly affecting smaller municipalities | Short term (≤ 2 years) |

| Fragmented Interoperability Standards Slowing Vendor-neutral Implementations in Africa | -0.6% | Africa, with limited impact on established markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy infrastructure lock-in hindering cloud migration in brownfield plants

Chemical, pulp, and steel sites often run proprietary distributed control hardware that lacks open interfaces, forcing phased upgrades that extend over many budget cycles. Full rip-and-replace strategies risk long outages and production losses. Operators therefore keep hybrid architectures that stretch cybersecurity teams thin and dilute cloud benefits. The resulting inertia slows service revenue growth for vendors and postpones subscription transitions.

Shortage of OT-cybersecurity talent in South America

Sixty-four percent of Latin American public managers report skill gaps that delay technology projects, especially in industrial control systems. Universities produce general IT graduates, yet few understand protocol stacks such as Modbus or DNP3. Companies rely on external consultants, raising project costs and extending commissioning timelines. The talent deficit constrains near-term supervisory control and data acquisition market rollouts in fast-growing mining and oil regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services reshape automation economics

Services generated 53.22% of revenue in 2025 and will expand at a 9.08% CAGR, underlining the market shift from one-time license sales to outcome-based engagements. Managed cybersecurity, remote diagnostics, and predictive analytics contracts lower entry barriers for mid-tier utilities that lack in-house expertise. Vendors provide monthly subscription bundles covering software updates, vulnerability scans, and compliance reporting, easing budget approvals for regulated industries.

Cloud-delivered dashboards and AI models need constant tuning, so recurring service streams outweigh hardware margins. This trend elevates partner ecosystems that can deliver regional support, language localization, and sector-specific advisory. The supervisory control and data acquisition market therefore pivots toward value-added services that improve asset uptime and regulatory readiness.

By Component: Communication Systems gain momentum

Programmable Logic Controllers still hold 30.65% share, yet Communication Systems are set to grow the fastest at 9.41% CAGR thanks to private 5G, Wi-Fi 6E, and TSN-ready Ethernet. Deterministic wireless removes cabling limits and supports mobile robots, drones, and wearable AR devices on factory floors. Hardware vendors integrate firewalls and zero-trust features at the network edge to meet IEC 62443 benchmarks.

As bandwidth needs rise, plant managers invest in redundant fiber backbones and software-defined WANs that connect multiple sites. Edge gateways translate legacy protocols so that machineto-machine traffic feeds cloud analytics without data loss. The shift realigns capital budgets from controllers to connectivity, reinforcing the importance of spectrum licensing strategies.

By Deployment Mode: Cloud adoption accelerates, hybrid remains dominant

On-premise deployments commanded 77.05% of the supervisory control and data acquisition market size in 2025, but cloud instances should grow at 12.58% CAGR. Europe’s water sector leads conversions; Thames Water’s modular rollout across 50 sites shows how phased migration can meet strict cybersecurity rules while reducing life-cycle cost.

Hybrid topologies remain popular because mission-critical loops often stay local for deterministic control while data lakes and AI services run in regional clouds. Over time, infrastructure refresh cycles and stricter patching requirements make cloud OPEX models more attractive than periodic CAPEX spikes.

By End-use Industry: Water utilities outpace hydrocarbons

Oil and Gas retained 22.45% revenue share in 2025 due to federally mandated leak detection and cybersecurity upgrades. However, Water and Wastewater utilities will post the fastest 10.08% CAGR. Ageing networks and stricter environmental discharge rules push operators to automate pump scheduling, chemical dosing, and non-revenue water analytics. Veolia and other operators report double-digit savings when deploying cloud-native optimization services.

Meanwhile, renewable-heavy power grids, food processing, and semiconductor fabs also expand SCADA footprints to secure supply chains and energy efficiency targets. Each sector requests templates pre-aligned with its own regulations, steering vendors toward verticalized solutions.

By Application: Process automation keeps the lion’s share

Process automation continues to dominate platform spending because of continuous operations in refining, chemicals, and power. Infrastructure automation gains pace through smart grid and smart city projects that need resilient, distributed control. Remote monitoring surged during pandemic lockdowns, making secure VPN gateways and role-based access standard features.

Asset performance management leverages machine learning to optimize maintenance intervals and extend equipment life, feeding data back into enterprise resource planning systems. As a result, decision makers increasingly view supervisory control and data acquisition market platforms as a central data hub rather than a stand-alone control layer.

Geography Analysis

Asia-Pacific held 33.85% revenue share in 2025, underpinned by China’s nationwide Industry 4.0 subsidies and the region’s leadership in private 5G deployments. Japanese and South Korean firms emphasize robotics integration, demanding low-latency control across multi-vendor equipment. India’s smart city and electronics manufacturing push adds a growing customer base for mid-tier SCADA offerings. Regional suppliers benefit from government incentives that localize production of controllers and IIoT gateways.

The Middle East and Africa region is forecast to grow at 9.18% CAGR as Gulf Cooperation Council states scale solar and wind farms to meet net-zero pledges. The UAE’s USD 6 billion round-the-clock renewable energy complex and Saudi Arabia’s 2 GW Sadawi project rely on utility-grade automation for grid stability. Dubai Electricity and Water Authority’s USD 1.9 billion smart grid plan highlights the demand for automated restoration and distributed energy resource management. African adoption is uneven because of interoperability issues, yet mining in South Africa and utility spending in Egypt create pockets of high growth.

North America remains a technology incubator, driven by strict pipeline safety rules and a rise in edge deployments for renewable integration. Federal directives on valve automation and threat monitoring oblige pipeline operators to modernize SCADA in short order. Canada attracts battery and electrification investments, including Siemens’ CAD 150 million AI manufacturing R&D center, which will rely on advanced automation labs. Mexico benefits from nearshoring electronics and automotive sectors, boosting demand for flexible SCADA platforms that can scale with new lines.

Competitive Landscape

The supervisory control and data acquisition market is moderately concentrated. Siemens, Schneider Electric, and ABB leverage decades-old installed bases yet now focus on AI tooling, low-code engineering, and cybersecurity certification to fend off niche entrants. Hardware commoditization forces these firms to emphasize software ecosystems, subscription support, and marketplace partnerships.

Specialist vendors such as Nozomi Networks, Claroty, and Dragos attract investment by offering deep OT-security analytics, prompting traditional automation houses to partner or invest. Nozomi’s USD 100 million Series E round with Mitsubishi Electric and Schneider Electric participation illustrates the convergence of control and security segments. NVIDIA teams with Rockwell Automation and Siemens to embed GPU-accelerated vision and AI inference into plant-floor systems, signaling a blurring line between IT and OT domains.

Managed services create a fresh arena where telecom operators, cloud hyperscalers, and engineering firms compete to run end-to-end OT stacks. Amazon Web Services collaborates with Rockwell Automation to bundle secure cloud gateways and analytics pipelines, aiming at companies that prefer OPEX models. Vendors able to certify against IEC 62443 standards gain procurement preference in heavily regulated sectors.

Supervisory Control And Data Acquisition (SCADA) Industry Leaders

Rockwell Automation Inc.

Honeywell International Inc.

Emerson Electric Company

Schneider Electric SE

ABB Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Siemens announced a CAD 150 million investment to establish a Global AI Manufacturing Technologies R&D Center for battery production in Canada.

- March 2025: Schneider Electric detailed plans to invest more than USD 700 million in U.S. facilities by 2027, adding over 1,000 jobs.

- March 2025: Siemens committed over USD 10 billion to expand American manufacturing and AI infrastructure, including new plants in Texas and California.

- March 2025: Nozomi Networks raised USD 100 million in Series E funding to boost its OT/IoT security platform.

- February 2025: Rockwell Automation and AWS unveiled a strategic tie-up to combine Rockwell OT software with AWS cloud services for scalable automation.

Global Supervisory Control And Data Acquisition (SCADA) Market Report Scope

SCADA, which stands for supervisory control and data acquisition, is a control system architecture that utilizes networked data communications, computers, and graphical user interfaces to provide advanced processing capabilities for supervisory management. It enables organizations to efficiently monitor, gather, and process real-time data in order to make informed decisions.

The supervisory control and data acquisition (SCADA) market is segmented by offering (hardware, software, and services) by component (human-machine interface (HMI), remote terminal unit (RTU), programmable logic controller (PLC), communication system, and others), by end user (automotive, semiconductor & electronics, oil and gas, pharmaceutical, food & beverage, chemical, power, telecommunication, and others), by geography (North America, Europe, Asia-Pacific, and Rest of the World). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Hardware |

| Software |

| Services |

| Human-Machine Interface (HMI) |

| Remote Terminal Unit (RTU) |

| Programmable Logic Controller (PLC) |

| Communication System |

| Others |

| On-premise |

| Cloud |

| Hybrid |

| Oil and Gas |

| Power and Energy |

| Water and Wastewater |

| Automotive |

| Semiconductor and Electronics |

| Food and Beverage |

| Pharmaceutical |

| Chemical |

| Metals and Mining |

| Transportation and Logistics |

| Telecommunication |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Nordics | ||

| Rest of Europe | ||

| South America | Brazil | |

| Rest of South America | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Offering | Hardware | ||

| Software | |||

| Services | |||

| By Component | Human-Machine Interface (HMI) | ||

| Remote Terminal Unit (RTU) | |||

| Programmable Logic Controller (PLC) | |||

| Communication System | |||

| Others | |||

| By Deployment Mode | On-premise | ||

| Cloud | |||

| Hybrid | |||

| By End-use Industry | Oil and Gas | ||

| Power and Energy | |||

| Water and Wastewater | |||

| Automotive | |||

| Semiconductor and Electronics | |||

| Food and Beverage | |||

| Pharmaceutical | |||

| Chemical | |||

| Metals and Mining | |||

| Transportation and Logistics | |||

| Telecommunication | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Nordics | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Rest of South America | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the supervisory control and data acquisition market?

The supervisory control and data acquisition market is valued at USD 12.07 billion in 2026 and is projected to reach USD 18.58 billion by 2031.

Which region holds the largest market share?

Asia-Pacific leads with 33.85% revenue share, supported by extensive Industry 4.0 and private 5G rollout

Which segment is growing the fastest by deployment mode?

Cloud deployment is expanding at a 12.58% CAGR as utilities and manufacturers overcome legacy constraints and adopt scalable, secure architectures.

Why are services becoming dominant in the supervisory control and data acquisition market?

Managed cybersecurity, predictive analytics, and outcome-based contracts lower operational complexity and align spending with measurable performance gains.

How are new safety regulations impacting SCADA investment in North America?

U.S. pipeline directives mandate real-time threat monitoring and automated valve response, triggering immediate upgrades of control systems and cybersecurity layers.

What is the key restraint slowing cloud migration in brownfield plants?

Legacy proprietary hardware and custom protocols create vendor lock-in, making wholesale replacement risky and costly, which leads many operators to maintain hybrid systems

Page last updated on: