Hammocks Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

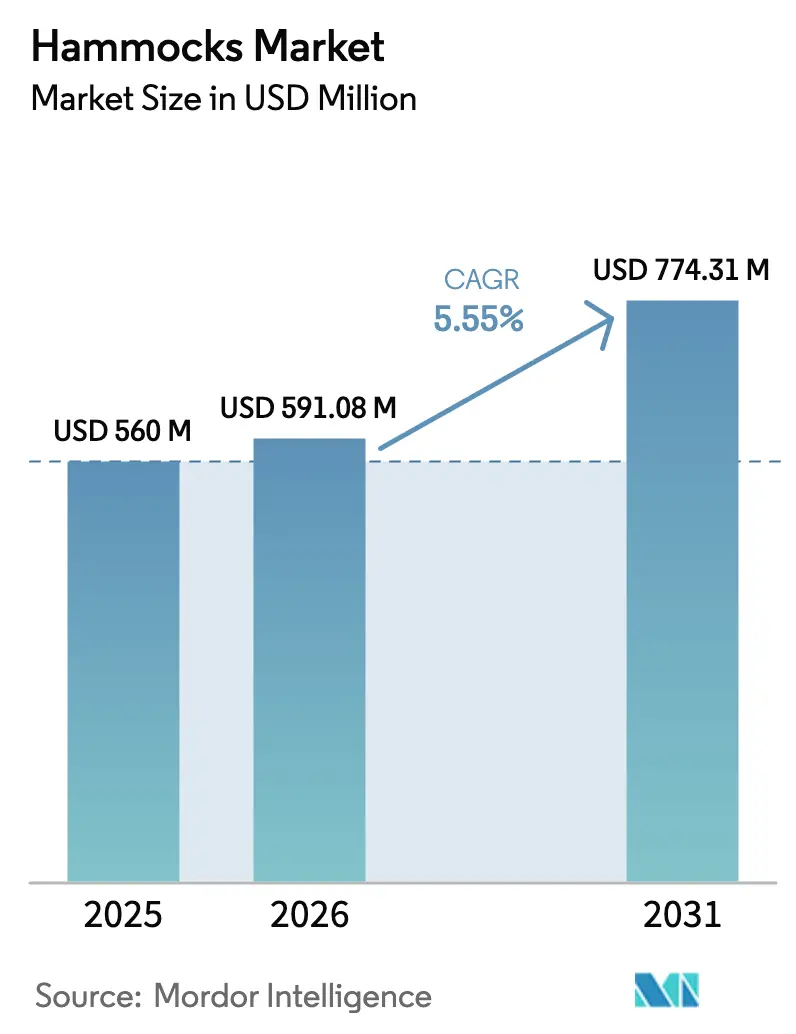

| Market Size (2026) | USD 591.08 Million |

| Market Size (2031) | USD 774.31 Million |

| Growth Rate (2026 - 2031) | 5.55% CAGR |

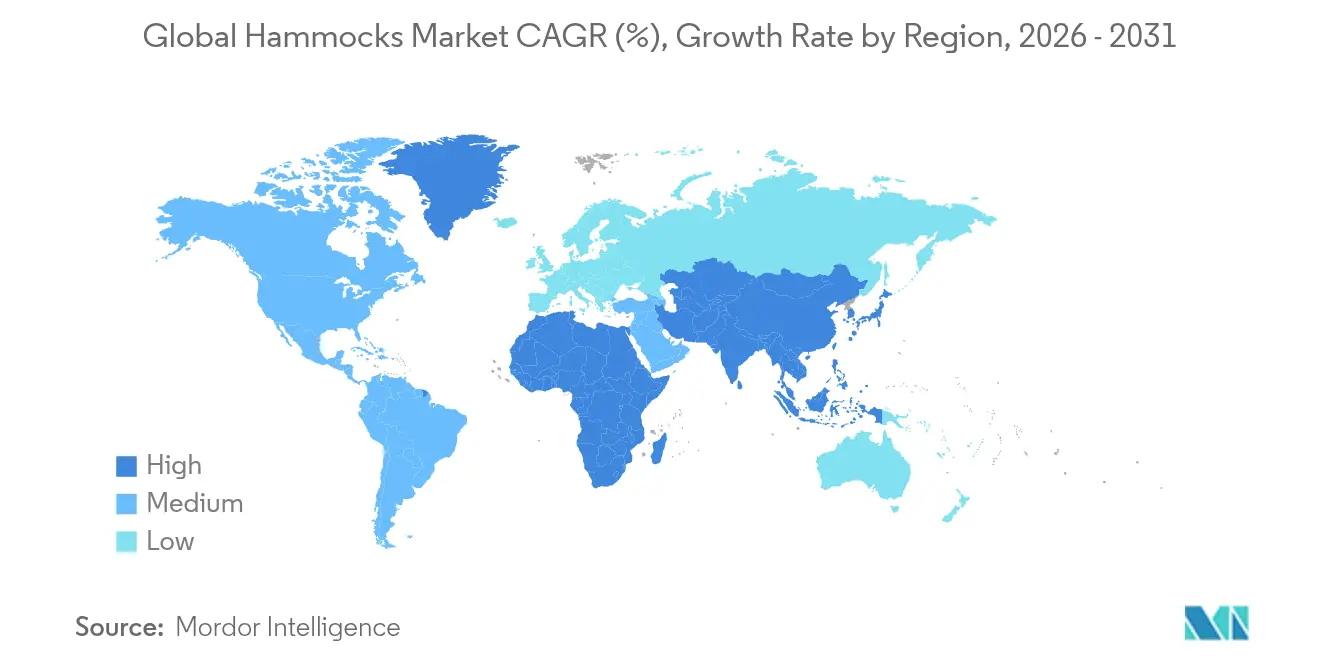

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

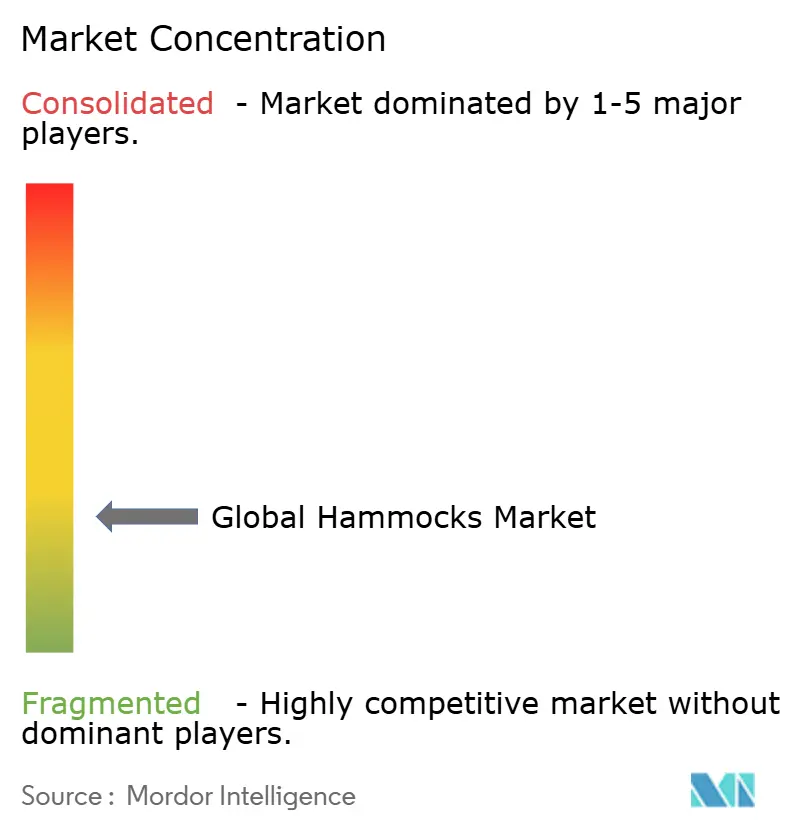

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hammocks Market Analysis by Mordor Intelligence

The hammocks market size is expected to grow from USD 560 million in 2025 to USD 591.08 million in 2026 and is forecast to reach USD 774.31 million by 2031 at 5.55% CAGR over 2026-2031. Robust participation in outdoor recreation, rising wellness spending, and steady e-commerce penetration are sustaining growth despite tariff pressure and raw-material inflation. Portable designs that serve both camping and indoor relaxation needs widen the user base, while sustainability credentials support premium pricing. Manufacturers increasingly pair technical fabrics with heritage aesthetics to target casual consumers seeking comfort as well as committed adventure travelers. Urban buyers account for a rising share of sales, encouraged by compact mounting systems that fit apartments and balconies, and this pattern is likely to keep the hammocks market on a steady expansion path.

Key Report Takeaways

- By product, rope hammocks led with 29.30% of the hammocks market share in 2025; Brazilian hammocks are forecast to grow at a 6.1% CAGR to 2031.

- By material, cotton captured 39.40% share of the hammocks market size in 2025, while nylon is projected to post a 6.41% CAGR through 2031.

- By purpose, outdoor applications accounted for 64.10% of revenue in 2025; indoor uses are advancing at a 5.43% CAGR to 2031.

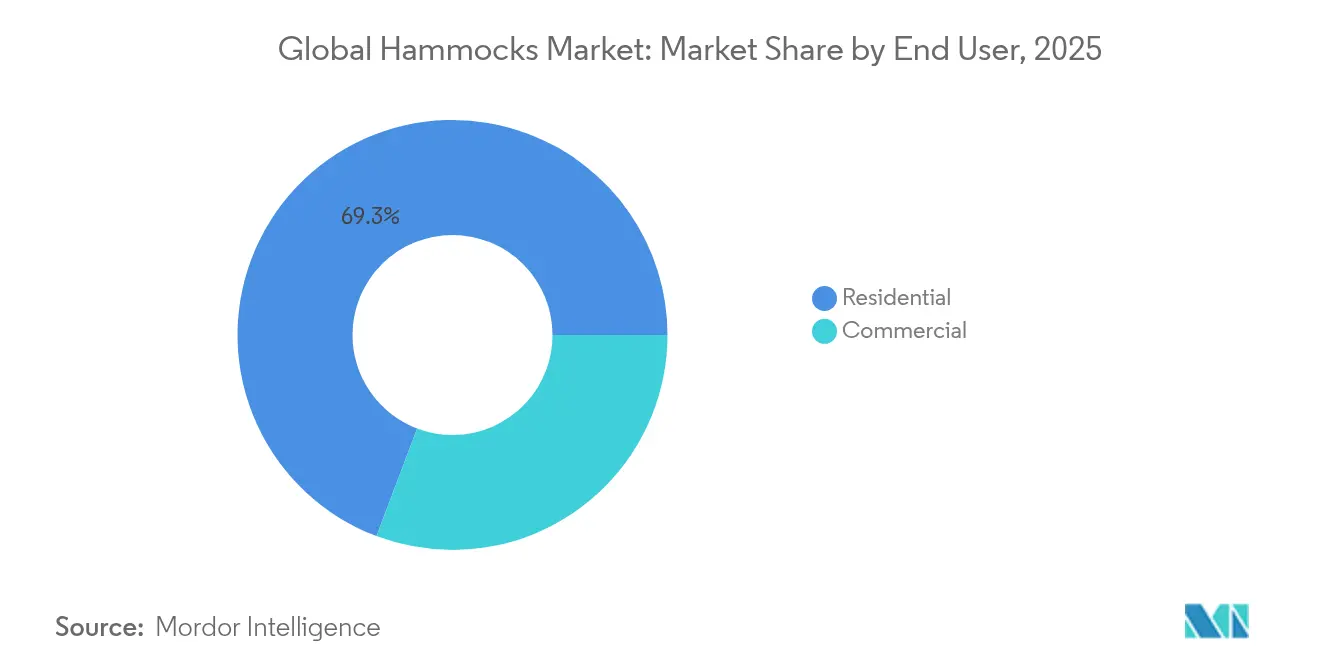

- By end user, the residential segment held 69.25% of the hammocks market share in 2025, whereas commercial demand is set to rise at a 6.7% CAGR through 2031.

- By distribution channel, home centers retained a 34.20% share in 2025; online sales are expanding at a 7.12% CAGR to 2031.

- By geography, North America represented 29.70% of revenue in 2025, but Asia-Pacific is projected to grow fastest at a 6.9% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hammocks Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global participation in outdoor recreation and camping activities post-COVID-19 | +1.5% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Growth of adventure tourism and experience-based leisure spending worldwide | +0.8% | Developed markets and tourism hubs | Long term (≥ 4 years) |

| Increasing urban demand for space-efficient relaxation and wellness furniture | +1.2% | Major metropolitan areas worldwide | Short term (≤ 2 years) |

| Rapid expansion of cross-border e-commerce enabling direct-to-consumer sales | +0.9% | Asia-Pacific and Latin America | Short term (≤ 2 years) |

| Sustainability certifications and ethical sourcing are boosting the preference for organic and fair-trade hammocks | +0.7% | Primarily developed economies, spreading to emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Participation in Outdoor Recreation and Camping Activities Post-COVID-19

Outdoor recreation remained popular after travel restrictions eased, with more than half of the Americans aged 6 and older taking part in at least one activity in 2024 [1]Outdoor Industry Association, “2024 Outdoor Participation Trends Report,” outdoorindustry.org. Similar enthusiasm is visible in China, where government policy promotes outdoor sports. Such structural tailwinds translate into sustained demand for versatile entry-level hammocks that offer comfort without technical complexity. Suppliers respond with lightweight cotton and nylon blends that pack small yet support heavier loads. Retail promotions now span all seasons, reflecting steady rather than cyclical buying.

Growth of Adventure Tourism and Experience-Based Leisure Spending Worldwide

Millennials and Gen Z allocate more income to experiential travel, driving glamping resorts and eco-lodges to install premium hammock lounges that complement nature immersion. Operators prefer Brazilian styles that balance aesthetics and durability, often sourced through fair-trade collectives to reinforce a sustainability narrative. Brand collaborations with tour providers deliver bundled gear plus curated travel itineraries, extending visibility across multiple touchpoints. The linkage between adventure tourism and the hammock market is expected to deepen as demand shifts from basic shelter to value-added comfort.

Increasing Urban Demand for Space-Efficient Relaxation & Wellness Furniture

Compact dwellings encourage homeowners to seek furnishings that provide restorative benefits without occupying floor space. Indoor hammock chairs and ceiling-mounted nets meet this requirement while aligning with mindfulness trends that emphasize micro-breaks and stress reduction. Developers integrate hammock zones in co-living apartments and wellness-focused offices, reinforcing year-round revenue streams beyond the traditional summer surge. Cotton quilted formats are popular indoors because they pair a soft feel with eye-catching patterns that match contemporary interiors.

Rapid Expansion of Cross-Border E-commerce Enabling Direct-to-Consumer Sales of Premium Hammocks

Social platforms such as TikTok showcase setup tutorials that shorten the learning curve and stimulate impulse purchases. Direct-to-consumer brands leverage logistics partners to offer duty-free delivery worldwide, allowing niche categories—such as Nicaraguan hand-woven hammocks—to access affluent buyers previously out of reach. The e-commerce boom also supports subscription-based accessory sales, from suspension straps to seasonal weather covers, improving customer lifetime value.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying price competition from low-cost manufacturers | -1.8% | Price-sensitive markets worldwide | Short term (≤ 2 years) |

| Seasonality of demand in temperate zones causing volatile sales cycles | -0.6% | North America and Europe | Medium term (2-4 years) |

| Availability of substitute portable seating options (camping chairs, inflatable loungers) | -0.4% | Urban markets and casual outdoor segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intensifying Price Competition from Low-Cost Manufacturers

Tariffs on Chinese and Vietnamese imports raise costs, yet competing factories in Southeast Asia absorb part of the increase to maintain export volumes. Established brands, therefore, face shrinking gross margins, especially in mainstream cotton hammock categories. Some counter pressure by shifting to recycled nylon and value-added accessories, supporting premium price points that limit direct comparison with budget entries. Others explore near-shoring to insulate against currency swings and freight volatility, highlighting domestic manufacturing as a quality cue.

Seasonality of Demand in Temperate Zones Causing Volatile Sales Cycles

Spring and summer quarters still generate the majority of hammock sell-through across North America and Europe. Extended logistics lead times force vendors to place production orders months ahead, risking overstocks if rain-heavy seasons suppress camping trips. Retailers mitigate the swing with indoor SKUs and cross-selling of stands and suspension kits, yet markdowns remain a feature of late summer clearance events. Better demand forecasting and flexible manufacturing aim to smooth revenue peaks over the forecast period.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Brazilian Popularity Expands Consumer Choice

Brazilian formats are projected to register a 6.1% CAGR through 2031, reflecting recognition of hand-loom techniques that create dense, supportive weaves favored for extended lounging. Rope variants held 29.30% of the hammocks market size in 2025, underpinned by broad retail distribution and competitive price points. Manufacturers promote improved cord tension and weather-treated finishes to refresh an otherwise mature sub-segment. Emerging designs such as inflatable models incorporate insulated air chambers that regulate temperature, signaling convergence between traditional fabric hammocks and technical camping mats. Brazilian offerings increasingly feature organic cotton yarns and artisan branding, reinforcing storytelling that resonates with lifestyle buyers seeking authenticity over generic mass production.

Growth prospects for quilted, Nicaraguan, and camping-specific lines rely on niche positioning around distinct use cases. Quilted versions, often paired with spreader bars, appeal to resort operators keen on poolside aesthetics. Camping models integrate bug nets and suspension straps to attract backpackers who reject heavier ground tents. The product mix demonstrates that the hammock market continues to broaden from a single outdoor leisure item into a multi-faceted category that satisfies relaxation, décor, and sport applications, ensuring future diversification.

By Material: Nylon Challenges Cotton Leadership

Cotton retained 39.40% of the hammock market size in 2025, owing to comfortable hand feel and wide style choices. Brands differentiate through organic certifications that justify premiums among eco-conscious shoppers. Nevertheless, nylon’s 6.41% forecast CAGR signals accelerating substitution, driven by weight savings and moisture resistance prized by trekkers. Hybrid weaves combine nylon warp threads with cotton weft to balance feel and strength, illustrating how fabric innovation defends share while reducing reliance on a single fiber type.

Wood and plastic remain ancillary, typically used in stands and spacer bars rather than sling fabrics, yet advances in bio-composites promise lower weight and reduced environmental impact. Cellulosic yarns such as Naia™ Renew, debuted by Eastman in 2025, showcase recyclable inputs and hypoallergenic performance. Such developments highlight a material race where comfort, durability, and environmental profile converge to shape purchasing decisions in the hammock market.

By Purpose/Application: Indoor Adoption Accelerates

Outdoor use still represented 64.10% of revenue in 2025, anchored by campground, beach, and backyard installations. That dominance will moderate as city dwellers add hammocks to living rooms, balconies, and home offices. Indoor demand is rising at a 5.43% CAGR, buoyed by wellness and mindfulness routines that encourage micro-napping and meditation. Designers tailor softer color palettes and plush padding to match interior décor, and simplified anchor hardware eases landlord concerns about structural damage.

Year-round indoor sales counterbalance climate-driven dips in outdoor demand, offering suppliers steadier cash flow and higher margins. Embedded smart-home sensors that adjust height or gently rock the occupant are in early piloting stages, signalling potential crossover with health-tech markets. The hammocks market, therefore, benefits from use-case diversity that limits over-dependence on any single season or consumer segment.

By End User: Commercial Buyers Gain Momentum

Residential buyers accounted for 69.25% of global revenue in 2025, confirming hammocks’ roots as personal leisure items. Nevertheless, hotels, spas, coworking spaces, and healthcare facilities collectively propel a 6.7% CAGR in the commercial channel. Hospitality operators install premium Brazilian and quilted models to create Instagram-friendly relaxation corners, while offices adopt stand-mounted lounge nets in wellness rooms to encourage micro-breaks and boost productivity. Bulk orders often mandate flame retardancy, weight certification, and quick-dry fabrics, prompting specialized SKUs.

Several airports now pilot nap pods incorporating suspended hammocks to enhance traveler comfort during layovers. Such deployments validate the product’s utility beyond recreation and position it within the broader experience economy. As commercial penetration mounts, suppliers scale professional-grade after-sales services covering maintenance and installation, thereby capturing annuity revenue in the hammocks market.

By Distribution Channel: Online Expansion Reshapes Sales Mix

Home centers held 34.20% of revenue in 2025 and remain key for tactile trials during peak outdoor-living promotions. Retailers curate interactive displays that let shoppers test sling depth and stand stability, helping close sales on impulse. Even so, online platforms are forecast to grow 7.12% annually as consumers value doorstep delivery and broad assortments unavailable in brick-and-mortar aisles. Paid search and influencer marketing drive product discovery, while augmented-reality apps allow virtual placement in living spaces, narrowing the experiential gap once exclusive to stores.

Supermarkets and hypermarkets cater to budget-conscious families via seasonal aisles, although limited assortment confines upselling opportunities. Specialized outdoor boutiques differentiate through expert staff and demo events, remaining influential among gear enthusiasts seeking high-performance nylon systems. The evolving channel mix underscores how direct digital engagement builds loyalty and grants brands first-party data pivotal to long-term positioning in the hammocks market.

Geography Analysis

North America commanded 29.70% of the hammock market size in 2025, sustained by deep camping culture, high disposable incomes, and broad retailer networks. Tariff shifts temper imports yet may favor domestic sewing operations that champion locally sourced wood and fabric, providing differentiation for made-in-USA labels. Ongoing wellness trends spur indoor adoption in colder months, partially offsetting seasonal sales troughs. Municipal park improvements and campground reservations remain robust, supporting consistent baseline demand.

Asia-Pacific is the fastest-growing region at a 6.9% CAGR through 2031. Chinese consumer enthusiasm extends beyond professional outdoor sports to casual lifestyle use, aided by government infrastructure spending and social-media influencers who normalize hammock lounging in urban green spaces. Rising disposable income in India, Thailand, and Indonesia further widens the addressable customer pool. Brands often collaborate with online marketplaces to manage cross-border fulfillment and align with local payment preferences, accelerating market entry.

Europe shows steady yet moderate growth. Environmental sensitivity encourages uptake of organic cotton and recycled nylon varieties, allowing premium pricing that compensates for slower volume gains. Southern Europe’s warmer climate broadens the usage window, whereas northern markets rely on indoor SKUs to navigate shorter summers. Brexit-related trade adjustments add cost uncertainty for UK distributors, spurring exploration of EU manufacturing to streamline customs procedures. Elsewhere, South America and the Middle East & Africa present attractive but volatile prospects. Economic cycles, currency swings, and infrastructural gaps require region-specific risk mitigation, though early adopters report strong brand loyalty once local presence is established.

Competitive Landscape

The hammock market remains fragmented, giving regional artisans space to flourish alongside global outdoor giants. Few players exceed double-digit shares, and top brands compete on sustainability claims, design aesthetics, and integrated ecosystems that bundle stands, tarps, and accessories. Eagles Nest Outfitters broadened its portfolio in 2025 with festival-oriented kits that include solar-powered lights and quick-deploy rainflies [2]Eagles Nest Outfitters, “Product Catalog 2025,” eaglesnestoutfitters.com. Tentsile continues tree-planting campaigns exceeding 1 million saplings, reinforcing environmental credentials while courting eco-tourism resorts [3]Tentsile, “One Million Trees Planted Milestone,” tentsile.com.

Strategic mergers characterize scale seekers. Fenix Outdoor’s 65% stake in Devold of Norway adds premium wool expertise, paving the way for cold-weather hammock insulation layers. Gathr Outdoors’ acquisition spree unites multiple gear brands under one logistics roof, amplifying shelf presence and cross-selling potential.

Product development emphasizes lightweight yet durable fabrics, modular stands, and simplified setup. Brands explore embedded IoT sensors for movement-activated rocking or sleep-quality tracking, aiming to secure wellness-tech partnerships. Overall, competitive dynamics favor companies able to integrate sustainability, digital engagement, and customer experience into cohesive strategies within the hammock market.

Hammocks Industry Leaders

Eagles Nest Outfitters Inc. (ENO)

The Hammock Source (Pawleys Island Hammock)

Grand Trunk

Wise Owl Outfitters

Kammok

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Tensa Outdoor released the Tensa4 portable stand supporting 350 lb loads and 12-ft hammocks, catering to users lacking adequate tree anchors.

- June 2024: New Atlas spotlighted an inflatable hammock design featuring insulated air gaps for improved temperature control during camping trips.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global hammocks market as retail revenue generated from portable woven or fabric slings that hang between two fixed points and are primarily used for leisure or sleep across residential yards, campsites, beaches, hospitality decks, and similar relaxation venues.

Scope Exclusion: Freestanding swing chairs, infant cradles, and enclosed hanging tents are not covered.

Segmentation Overview

- By Product

- Rope Hammock

- Quilted Hammock

- Brazilian Hammock

- Other Products (Nicaraguan Hammock, Camping Hammock, etc.)

- By Material

- Cotton

- Nylon

- Wood

- Plastic

- Other Materials

- By Purpose / Application

- Outdoors

- Indoors

- By End User

- Residential

- Commercial

- By Distribution Channel

- Supermarkets and Hypermarkets

- Home Centers

- Online

- Other Distribution Channels

- By Geography

- North America

- Canada

- United States

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- Rest of Europe

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Middle East & Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East & Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews and web surveys were conducted with outdoor gear buyers, specialty retail managers, online marketplace sellers, and fabric suppliers across North America, Europe, and Asia. Their insights on channel mix, average selling prices, and seasonality patterns closed data gaps and grounded model assumptions.

Desk Research

We begin by assembling baseline signals from tier-1 public sources such as the U.S. Outdoor Industry Association participation survey, Eurostat textile trade records, UN Comtrade HS-6306 shipment data, and campground occupancy reports issued by national tourism boards, which together outline usage, production, and cross-border flows. Mordor analysts then refine value estimates through brand-level revenue clues in company 10-Ks housed on D&B Hoovers, price scans in retailer flyers captured by Dow Jones Factiva, and patent filings accessed via Questel that flag material innovations. These examples illustrate our secondary source mix; many additional publications and datasets support fact checks and clarifications.

Market-Sizing & Forecasting

Our model starts with a top-down reconstruction that layers global outdoor-living spend, regional camping participation rates, and trade volumes for hammocks. Results are stress-tested through selective bottom-up checks, weighted average price multiplied by estimated units for leading brands, to lock in a base value. Forecasts flow from five key variables: per-capita disposable income, e-commerce share in home goods, urban green-space additions, cotton and nylon input prices, and vacation days per adult. A multivariate regression projects these drivers, while scenario analysis adjusts for sudden policy or material shifts. Country splits are apportioned using outdoor-recreation expenditure where direct data are thin.

Data Validation & Update Cycle

Outputs pass three layers of variance checks, and anomalies trigger rapid re-contact with experts before sign-off. Reports refresh every twelve months, with interim updates issued when currency swings, trade tariffs, or major product recalls materially alter demand.

Why Mordor's Hammocks Baseline Commands Reliability

Published estimates often diverge because firms select different product bundles, price ladders, and refresh timelines. Our disciplined scope, transparent variables, and annual update ritual narrow those gaps for decision makers.

Key divergence factors include whether swing chairs are counted, the baseline year chosen, average price methodologies, and recognition of post-pandemic outdoor-leisure acceleration.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 560 million (2025) | Mordor Intelligence | - |

| USD 462 million (2025) | Global Consultancy A | Omits resort installations and applies one global average price |

| USD 387.2 million (2023) | Industry Data Firm B | Uses pre-pandemic baseline and rolls forward with fixed CAGR |

| USD 4.75 billion (2024) | Regional Research Group C | Bundles swing chairs and large canopy daybeds, inflating scope |

These comparisons show that when scope, inputs, and update cadence vary, outcomes shift widely. Mordor's stepwise approach, anchored in verifiable trade and retail indicators, delivers a balanced, repeatable baseline that clients can trace back to clear data points and documented assumptions.

Key Questions Answered in the Report

What is the current value of the global hammocks market?

The hammocks market was valued at USD 591.08 million in 2026 and is projected to grow steadily through 2031.

Which product type holds the largest revenue share?

Rope variants led with 29.30% of the hammocks market share in 2025, benefiting from broad availability and competitive pricing.

Why is Asia-Pacific the fastest-growing region?

Rising disposable incomes, supportive government policies for outdoor sports, and strong social-media influence contribute to a 6.9% CAGR in Asia-Pacific.

How are sustainability trends influencing material choices?

Organic cotton and recycled nylon blends gain traction as consumers favor eco-credentials, while innovations like Naia™ Renew fiber add recyclable options to the mix.

What drives commercial demand for hammocks?

Hotels, spas, coworking spaces, and airports adopt premium models to enhance guest or employee experiences, pushing the commercial segment toward a 6.7% CAGR.

Which sales channel is expanding fastest?

Online platforms are forecast to grow at 7.12% annually as direct-to-consumer models leverage global shipping, influencer marketing, and augmented-reality tools for virtual setup previews.

Page last updated on: