Gaming Chair Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

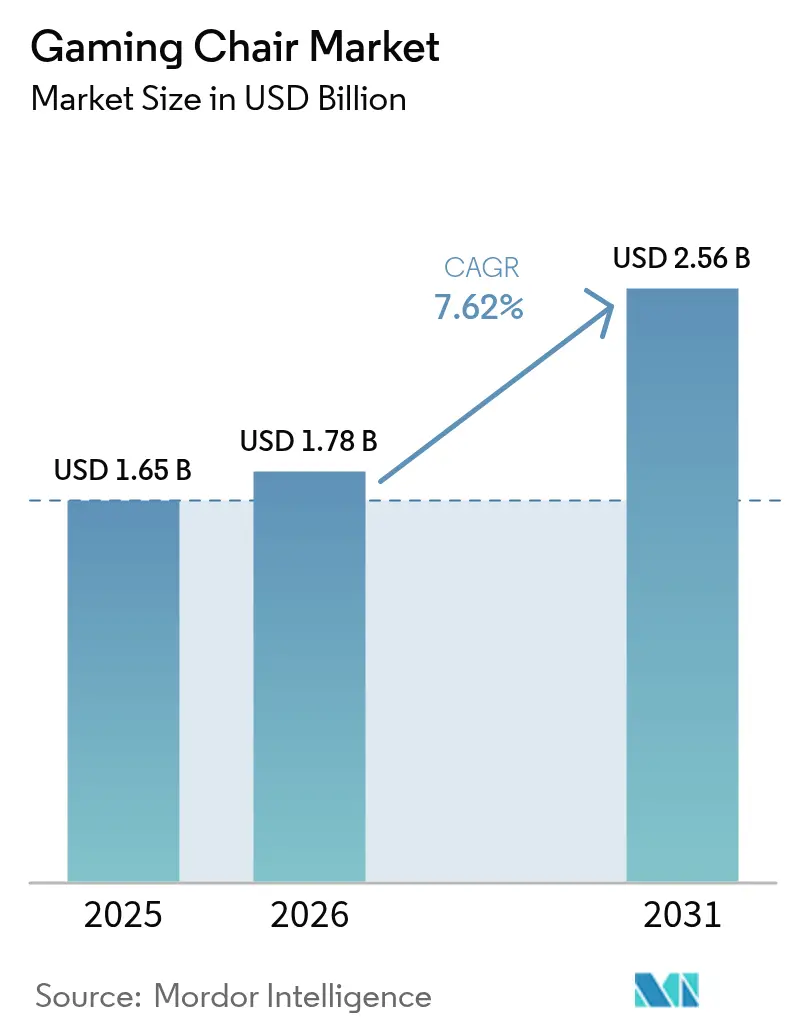

| Market Size (2026) | USD 1.78 Billion |

| Market Size (2031) | USD 2.56 Billion |

| Growth Rate (2026 - 2031) | 7.62% CAGR |

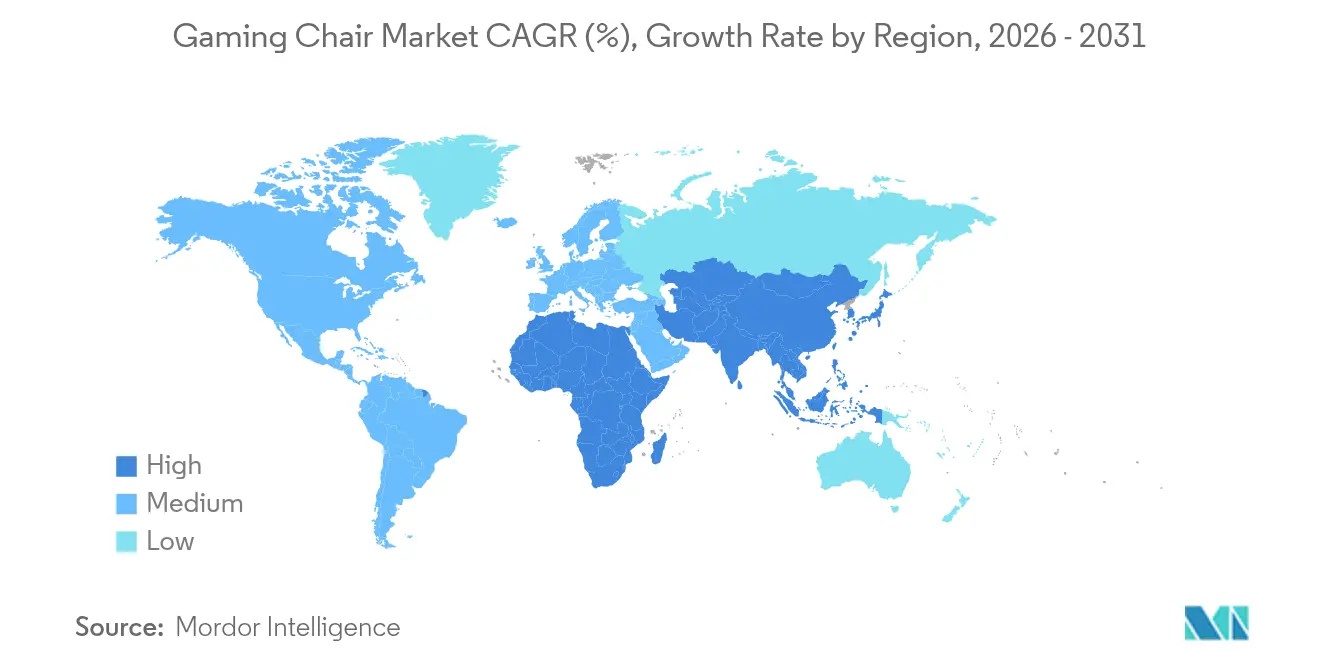

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Gaming Chair Market Analysis by Mordor Intelligence

The gaming chair market size is expected to grow from USD 1.65 billion in 2025 to USD 1.78 billion in 2026 and is forecast to reach USD 2.56 billion by 2031 at 7.62% CAGR over 2026-2031. Robust growth aligns with e-sports expansion, hybrid work adoption, and rising ergonomic awareness among digital natives. Professional tournaments now treat high-performance seating as requisite equipment, while corporate buyers recognize gaming chair as productivity assets that appeal to younger personnel. Bulk orders from gaming cafés in Asia-Pacific and sustained premiumization in North America further expand the addressable base. Competitive intensity revolves around ergonomic innovation, smart-feature integration, and sustainable materials, allowing both value and premium brands to thrive.

Key Report Takeaways

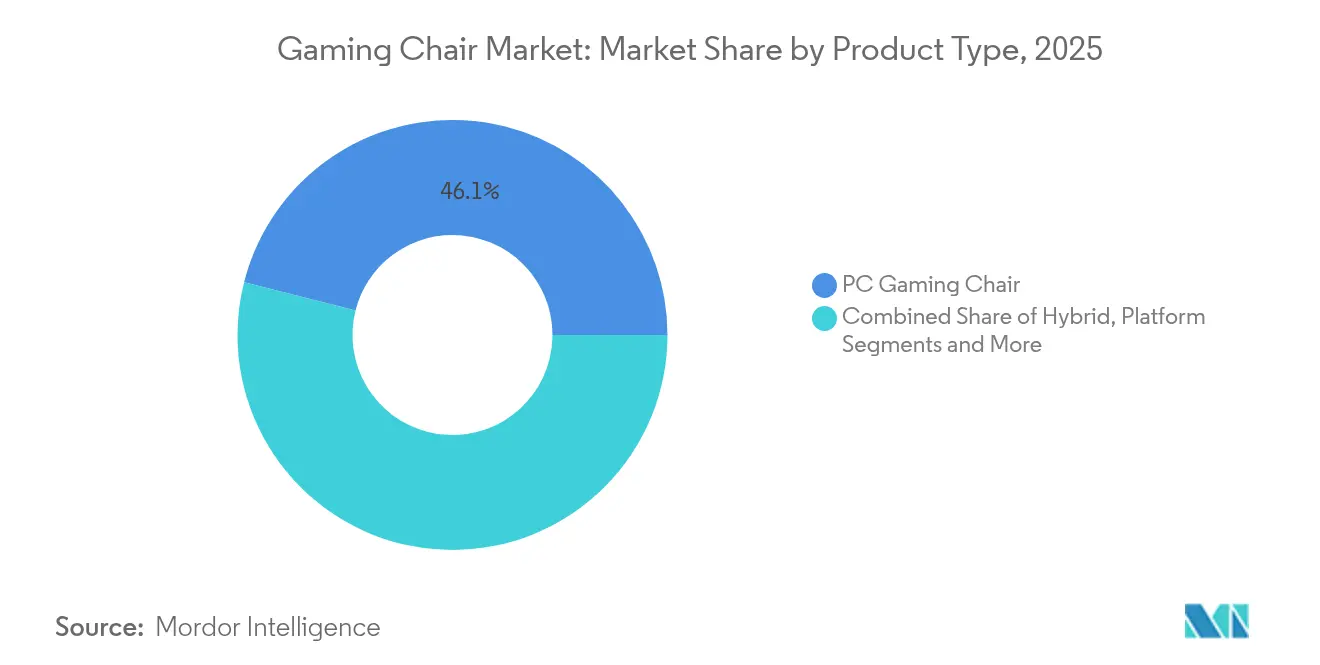

- By product type, PC Gaming Chair led with 46.05% of the gaming chair market share in 2025, while Hybrid Gaming Chair is projected to advance at a 8.72% CAGR through 2031.

- By material, PU Leather commanded 52.12% share of the gaming chair market size in 2025; Fabric/Mesh is poised to grow at 8.31% CAGR to 2031.

- By distribution channel, B2C outlets held 71.35% revenue share in 2025, whereas B2B channels are forecast to rise at an 8.12% CAGR through 2031.

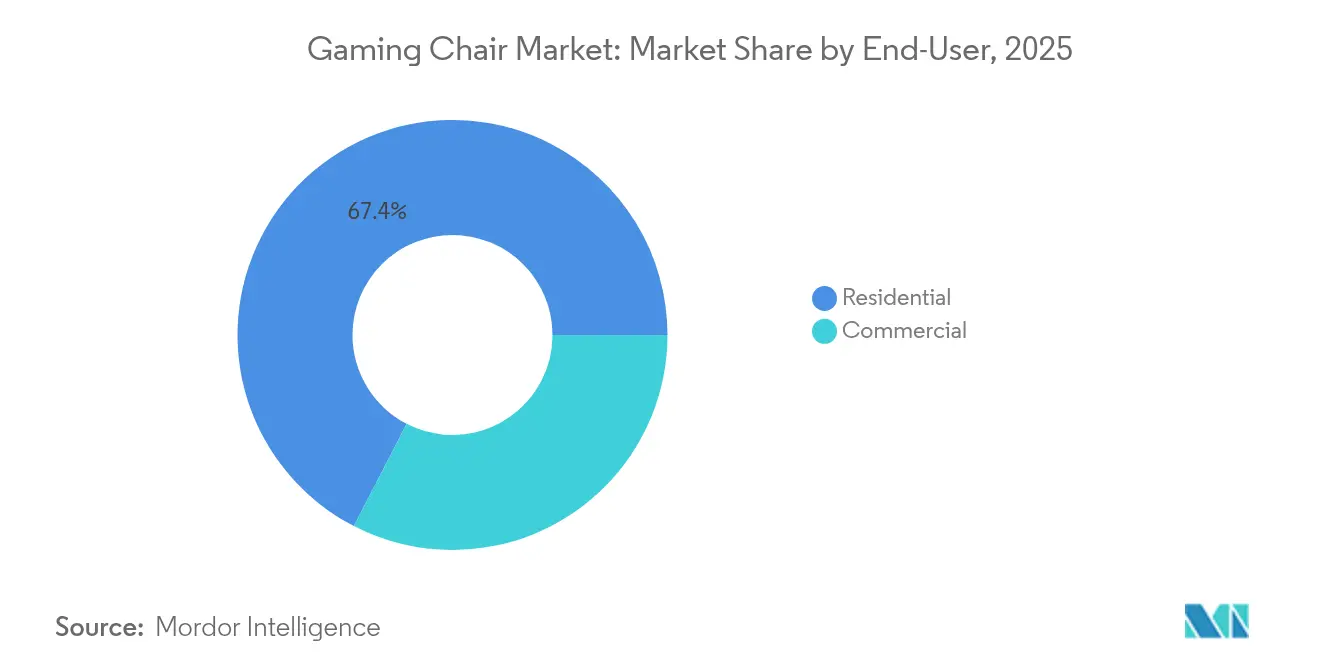

- By end-user, Residential applications accounted for 67.42% of the gaming chair market size in 2025, while the Commercial segment is moving at an 8.55% CAGR through 2031.

- By geography, North America occupied 40.78% share in 2025, while Asia-Pacific is slated to accelerate at a 8.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Gaming Chair Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive growth of global e-Sports prize pools | +1.8% | Global, with concentration in North America, South Korea, China | Medium term (2-4 years) |

| Rising average daily gaming hours among Gen-Z and Millennials | +1.5% | Global, particularly strong in Asia-Pacific and North America | Long term (≥ 4 years) |

| Continuous ergonomic product innovation and patent activity | +1.2% | North America and Europe leading innovation, Asia-Pacific manufacturing | Medium term (2-4 years) |

| Corporate adoption of gaming chairs in hybrid office setups | +1.0% | North America and Europe primarily, expanding to urban Asia-Pacific | Short term (≤ 2 years) |

| Livestream-centric "showpiece" furniture demand by influencers | +0.8% | Global, with strong influence in North America and developed Asia markets | Short term (≤ 2 years) |

| Expansion of gaming cafés across Tier-2/3 Asian cities | +0.9% | Asia-Pacific core, particularly India, Southeast Asia, and China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Explosive Growth of Global E-sports Prize Pools

Prize money escalation has reframed chairs from accessories to performance tools, elevating demand across professional and aspirational tiers. Sponsorship deals place branded seating on global broadcasts, reinforcing perceptions that premium ergonomics create a competitive edge. Amateur players emulate idols seen practicing in a branded chair during high-stakes finals. Manufacturers capitalize by tailoring models to team preferences, then releasing consumer versions bearing identical specifications. This virtuous cycle directly feeds volume gains in the gaming chair market[1]Source: Jeffrey Rousseau, “Global Games Market Grew to USD 86.6 Billion in 2024,” gamesindustry.biz. The trend has particular momentum in regions with established e-sports infrastructure, where gaming chairs have become status symbols within gaming communities and markers of serious competitive intent. The correlation between prize pool growth and gaming chair demand reflects the broader legitimization of gaming as a serious competitive pursuit requiring dedicated equipment investments. This trend has particular momentum in regions with established e-sports infrastructure, where gaming chairs have become status symbols within gaming communities and markers of serious competitive intent.

Rising Average Daily Gaming Hours Among Gen-Z and Millennials

Cross-platform engagement stretches play sessions well beyond traditional leisure windows, intensifying physical stress on back and neck muscles. Prolonged digital immersion has raised user expectations for adjustable lumbar, multi-tilt mechanics, and breathable upholstery. Older Gen-X gamers, with higher discretionary budgets, now pursue premium seating that merges comfort with mature aesthetics. Extended use cases move the gaming chair market beyond teenage bedrooms into shared household spaces. Sustained playtime keeps replacement cycles brisk, reinforcing steady revenue inflow. The convergence of longer gaming sessions and demographic maturation has fundamentally shifted gaming chairs from teenage bedroom furniture to adult lifestyle products requiring sophisticated design and premium materials.

Continuous Ergonomic Product Innovation and Patent Activity

Patent filings in gaming chair technology have accelerated significantly, with innovations extending beyond traditional ergonomics to incorporate biometric monitoring, thermal regulation, and smart connectivity features that position gaming chairs as health and performance optimization platforms[2]Source: United States Patent and Trademark Office, “Smart Sport Chair Patent US 11,488,118,” uspto.report. FDA-registered models such as the Anthros chair underscore medical-grade aspirations, supporting premium price points. Collaboration between furniture engineers and university biomechanics labs provides peer-reviewed validation that feeds marketing claims. Smart features differentiate offerings in a crowded gaming chair market, sustaining margins despite rising raw-material costs. Rapid prototyping and Asia-Pacific manufacturing scale convert lab concepts into retail units within a single season. The patent landscape increasingly emphasizes multifunctional capabilities that address both gaming performance and general health outcomes, reflecting the market's evolution toward sophisticated wellness-oriented furniture rather than simple comfort enhancement.

Corporate Adoption of Gaming Chair in Hybrid Office Setups

Tech firms and design studios outfit hot-desking zones with gaming chairs to attract talent accustomed to esports aesthetics. Procurement teams cite lower absenteeism and higher coding productivity when ergonomic adjustments match varied body types. Color-toned variants with subdued branding blend into conference backdrops, easing executive approval. Bulk orders shorten payback periods for manufacturers and lift the gaming chair market in the B2B channel. Workplace validation further normalizes gaming designs for mainstream buyers. The aesthetic evolution of gaming chairs toward more professional appearances has facilitated corporate acceptance, with manufacturers developing models that maintain ergonomic gaming features while adopting subdued color schemes and refined designs suitable for video conferencing. This corporate adoption trend has particular momentum in technology companies and creative industries where gaming culture intersects with professional identity, creating new market segments and distribution channels.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium pricing vs. conventional office chairs | -1.1% | Global, particularly pronounced in price-sensitive emerging markets | Medium term (2-4 years) |

| High influx of low-cost counterfeit products | -0.9% | Asia-Pacific manufacturing regions, global distribution impact | Short term (≤ 2 years) |

| Stricter eco-material standards raising PU costs | -0.7% | Europe and North America primarily, expanding to Asia-Pacific | Medium term (2-4 years) |

| Low ergonomic awareness in price-sensitive economies | -0.8% | Emerging markets in Asia-Pacific, Africa, and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Premium Pricing vs. Conventional Office Chair

An authentic gaming chair can cost triple a basic task chair, limiting first-time adoption for budget buyers. Price sensitivity is most acute in emerging markets, where consumer focus remains on core PC hardware. Corporate finance teams often question added spend unless ROI is demonstrated via health-related metrics. Brands respond by launching entry lines that retain signature contours but drop non-essential extras. Value-engineering helps protect the gaming chair market from severe discount erosion. The "showpiece" demand has driven premiumization trends, with high-end gaming chairs serving dual purposes as functional seating and visual status symbols within streaming communities. This trend has global reach but shows particular strength in regions with established streaming cultures and high social media engagement, where gaming chairs function as both performance equipment and lifestyle accessories for digital content creation.

High Influx of Low-Cost Counterfeit Products

Imitators crowd online marketplaces with visually similar designs that cut corners on foam density and frame integrity. Counterfeits tarnish brand reputations when early wear or safety failures occur, prompting costly warranty claims against genuine makers. Manufacturers deploy QR-code authentication and dealer blacklists to safeguard consumers. Legal enforcement remains challenging across multiple jurisdictions, sustaining a background drag on the gaming chair market. Education campaigns stressing the long-term health risks of knock-offs aim to shift buyer behavior. The commercial durability requirements for gaming café chairs have driven product innovations in materials and construction, with manufacturers developing models specifically designed for high-usage commercial environments. This expansion trend has created new distribution channels and bulk purchasing opportunities, with gaming café operators increasingly viewing chair quality as a competitive differentiator in attracting and retaining customers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Hybrid Models Bridge Gaming and Professional Use

PC Gaming Chair held 46.05% of the gaming chair market size in 2025, reflecting their entrenched role in desk-based esports setups. Demand endures as streamers showcase recognizable bucket-seat silhouettes that signal pro status. Hybrid models, however, are gaining at the fastest clip given their subdued palettes and fold-away footrests that suit video calls. Manufacturers now cross-list hybrid units under both gaming and office catalogs to broaden reach. R&D teams refine synchro-tilt mechanisms that transition seamlessly between recline for gaming and upright posture for typing. Sim-racing and platform chair remain niche yet lucrative due to specialized hardware mounts. Corsair’s acquisition of Fanatec validates the segment’s appeal to peripheral giants. A diversifying product map underpins steady ASPs across the gaming chair market. Branding strategies increasingly tailor messaging to use-case personas—creator, coder, racer—rather than one-size-fits-all gamers. Continual refresh cycles keep model lineups aligned with evolving ergonomic science.

PC gaming chair benefit from the established desktop gaming infrastructure and the visual prominence of gaming setups in streaming and content creation, maintaining their position through continuous feature enhancement and brand partnerships with gaming peripheral manufacturers. Platform Gaming Chair face challenges from the shift toward mobile gaming in many regions, but maintain relevance through console gaming growth and specialized applications like VR gaming that require unique seating configurations. The product type landscape suggests continued segmentation as gaming applications diversify and user needs become more specialized, with successful manufacturers likely to develop targeted solutions for specific gaming contexts rather than pursuing one-size-fits-all approaches.

By Material: Sustainability Challenges Traditional PU Dominance

PU Leather retained 52.12% share of the gaming chair market in 2025, valued for its wipe-clean surface and bold color blocking. Regulatory scrutiny over petro-based synthetics and consumer interest in eco-credentials, however, propel Fabric/Mesh options at an 8.31% CAGR. Breathable weaves mitigate sweat build-up during marathon sessions, improving thermal comfort in humid regions. Brands experiment with recycled polyester yarns and plant-based coatings to align with ESG targets. Genuine leather remains limited to flagship SKUs aimed at affluent hobbyists seeking luxury status cues. Hybrid fabrics pair mesh centers with soft-touch bolsters, balancing airflow and edge-wear resistance. Material selection now factors in end-of-life recyclability, influencing procurement policies at large enterprises. Sustainability storytelling differentiates entrants crowded out of pure price competition in the gaming chair market.

PU Leather's continued dominance reflects its established supply chains, aesthetic appeal, and durability advantages, but manufacturers are investing in bio-based and recycled PU alternatives to address sustainability concerns while maintaining material performance. The material segmentation increasingly influences brand positioning, with eco-conscious manufacturers leveraging sustainable materials as competitive differentiators in crowded gaming chair markets. Genuine leather maintains premium positioning but faces ethical sourcing challenges and higher costs that limit market penetration, while hybrid materials attempt to balance sustainability, performance, and cost considerations. The material landscape suggests continued innovation in sustainable alternatives as environmental regulations tighten and consumer awareness increases, with successful manufacturers likely to develop proprietary material solutions that address both performance and sustainability requirements.

By End-User: Commercial Adoption Transforms Market Dynamics

Residential buyers still constitute 67.42% of sales, reflecting pandemic-era home-office upgrades and core gamer passion. However, the Commercial cohort is expanding at 8.55% CAGR, fueled by wellness-centric HR policies in technology and media firms. Corporate specifications emphasize neutral colorways and replaceable cushions to maximize fleet lifespan. Schools and universities deploy gaming chairs in esports labs, exposing younger audiences to premium ergonomics early. Chairs with certification badges—FDA registered or endorsed by physiotherapy associations—ease procurement hurdles. Commercial uptake stabilizes volume demand and shortens replacement cycles, providing baseline revenue for the gaming chair market even during consumer spending lulls.

Commercial buyers increasingly demand certifications and compliance documentation that residential consumers typically ignore, driving manufacturers to invest in testing and certification programs that support corporate sales initiatives. The end-user evolution suggests gaming chairs are becoming mainstream ergonomic furniture rather than specialized gaming products, with successful manufacturers developing products that serve both segments without compromising core gaming chair characteristics. Educational institutions represent an emerging commercial segment as gaming and e-sports programs expand in schools and universities, creating new bulk purchasing opportunities and product requirements for institutional environments.

By Distribution Channel: B2B Growth Signals Corporate Adoption Acceleration

B2C e-commerce remains the primary route at 71.35% share, thanks to influencer unboxings and generous return policies that ease remote furniture purchases. Yet B2B orders are set to outpace, growing 8.12% each year as offices refresh workstations for hybrid routines. Facility managers demand ANSI/BIFMA-certified gaming models that pass rigorous durability tests. Brick-and-mortar specialty outlets showcase sample units where shoppers verify fit before committing, bolstering premium attachment rates. Home centers court first-time buyers with budget SKUs, expanding the gaming chair market to casual console players. Manufacturers provide AR configurators that let corporate teams visualize colorways in floor layouts. Gaming cafés form an institutional sub-channel, often ordering dozens of identical units per location backed by maintenance contracts. Direct-to-consumer brands dabble in pop-up showrooms to boost tactile engagement without carrying heavy retail overhead.

The distribution landscape suggests continued channel diversification as gaming chairs serve broader market segments, with successful manufacturers developing channel-specific strategies that address unique buyer needs and purchasing processes. Specialty retailers provide valuable services for premium gaming chair sales, offering ergonomic assessments and customization options that online channels cannot replicate, maintaining relevance despite online growth. The channel evolution indicates gaming chairs are following broader furniture industry trends toward omnichannel distribution while maintaining gaming-specific retail characteristics and customer service requirements.

Geography Analysis

North America retained a 40.78% share in 2025, supported by mature esports ecosystems, high disposable income, and strong brand loyalty toward premium seating. Continuous streamer content originating from the United States amplifies chair visibility across global audiences. Canada mirrors U.S. trends, but regional distributors focus on cold-weather fabric variants that counteract PU stiffness. Asia-Pacific is the fastest-growing territory at a 8.98% CAGR through 2031, underpinned by USD 86.6 billion in regional game revenues recorded in 2024. China’s mobile-first market funnels new gamers into accessory purchases once they upgrade to PC rigs. India’s 16 million gamer base and NVIDIA-backed plan to open 100 cafés in 2024 create bulk chair orders that boost the gaming chair market.

Southeast Asia and MENA markets grew by 5.3% and 4.2% respectively, in 2024, with Saudi Arabia leading MENA growth at 8.5%, indicating broad-based regional momentum beyond traditional gaming strongholds. The regional growth patterns reflect varying stages of gaming culture development, with established markets focusing on premiumization while emerging markets prioritize accessibility and volume adoption. North America's market leadership reflects mature e-sports infrastructure, high disposable income among gaming demographics, and established gaming chair brand presence, though growth rates suggest other regions are rapidly closing the gap through infrastructure investment and demographic shifts. Europe maintains steady growth supported by established gaming culture and corporate adoption of gaming chairs in hybrid office environments, with regulatory frameworks around sustainable materials influencing product development and market positioning. The geographic segmentation increasingly reflects economic development patterns rather than pure gaming culture, with affluent regions driving premium product adoption while emerging markets focus on value and accessibility. Gaming café expansion across tier-2 and tier-3 Asian cities creates bulk demand that differs from individual consumer purchasing patterns in developed markets, requiring manufacturers to develop commercial-grade products and distribution strategies. The regional dynamics suggests continued market expansion as gaming infrastructure develops and disposable income rises in emerging markets, with successful manufacturers likely to adapt products and strategies to local preferences and economic conditions.

Regulatory Landscape

Gaming chairs are governed mainly through general upholstered seating and office or institutional seating requirements rather than a gaming-specific regime. In the United States, upholstered gaming chairs sold at retail commonly follow the federal upholstered furniture flammability framework that aligns with California Technical Bulletin 117-2013 (TB 117-2013), which makes material selection and supplier test documentation important for importers and private-label sellers. For performance and safety, commercial and institutional buyers often reference ANSI/BIFMA seating standards such as ANSI/BIFMA X5.1-2017 (R2022) when specifying durability, stability, and strength for high-usage environments like offices, universities, and gaming cafes.

Trade policy and product classification also affect compliance and landed cost. Gaming chairs are typically classified under Harmonized System headings for seats (for example, upholstered metal-frame seats or swivel seats), and tariff treatment is determined by construction attributes (frame, upholstery, swivel or height adjust) rather than marketing claims. This classification logic influences sourcing decisions and has encouraged manufacturers to diversify production footprints while maintaining traceable bills of materials to manage country-specific duty exposure and documentation needs for cross-border shipments.

Value Chain Analysis

The gaming chair value chain begins with upstream inputs such as steel or aluminum for frames and mechanisms, foam and upholstery (PU leather, fabric or mesh), casters and bases, and gas lifts that are often procured to meet contract-grade seating expectations (including BIFMA-aligned component testing for B2B tenders). Manufacturing is concentrated in Asia, where specialized furniture clusters support integrated capabilities across metal fabrication, molding and foam, sewing or upholstery, finishing, and final assembly. Brands and ODM or OEM partners then move product through packaging and export logistics, followed by regional importers or distributors and omnichannel retail, with B2C e-commerce leading volumes while B2B serves offices, esports labs, and gaming cafes through bulk ordering and service requirements.

Downstream, last-mile delivery, returns, and warranty support are key cost centers because chairs are bulky, high-dimensional weight items with higher reverse-logistics exposure than smaller peripherals. In 2026, furniture logistics disruption and higher freight volatility have pushed brands toward resilience tactics such as buffering inventory, splitting production across multiple countries, and adding regional warehousing to support faster replenishment for commercial accounts. Counterfeit and gray-market listings in online channels also add pressure, prompting more authentication measures and tighter control over authorized dealer networks.

Competitive Landscape

Secretlab, Herman Miller × Logitech G, and DXRacer anchor the premium tier, leveraging proprietary foam formulas, community engagement, and esports sponsorships. Middle-price challengers focus on value-rich bundles that include memory-foam pillows and extended warranties. Patent volumes spike as Nike’s smart chair blueprint introduces biometric feedback loops that may define the next frontier of the gaming chairs industry. Sustainable material innovators differentiate through recycled mesh and bio-PU, capturing eco-conscious millennials.

The competitive landscape increasingly emphasizes technological differentiation, with companies investing in smart features, biometric integration, and sustainable materials to justify premium pricing and differentiate from commodity alternatives. White-space opportunities exist in specialized segments like sim racing chairs, as demonstrated by Corsair's USD 110 million acquisition of Fanatec, indicating potential for niche market development and premium positioning[4]Source: Corsair Gaming, “Investor Presentation Q3 2024,” corsair.com. Emerging disruptors focus on direct-to-consumer sales models and sustainable materials, challenging traditional distribution channels and manufacturing approaches while appealing to environmentally conscious consumers. Technology integration has become a critical competitive factor, with companies developing proprietary features like RGB lighting, wireless charging, and mobile app connectivity to create ecosystem lock-in and justify premium pricing in increasingly commoditized markets.

The competitive dynamics suggest successful companies must balance gaming culture authenticity with mainstream appeal, as gaming chairs expand beyond core gaming demographics into corporate and professional environments. Market leaders typically maintain strong community engagement through sponsorships, influencer partnerships, and gaming event presence, recognizing that brand credibility within gaming communities drives purchasing decisions across all market segments. The fragmented nature of gaming sub-segments limits market consolidation opportunities, as different gaming applications require specialized features and aesthetic preferences that prevent one-size-fits-all solutions. Competitive intensity varies by region, with established markets emphasizing brand differentiation and premium features while emerging markets focus on value positioning and accessibility, requiring manufacturers to develop region-specific strategies and product portfolios. The competitive landscape suggests continued innovation investment and brand building will determine market leadership, as gaming chairs evolve from simple seating solutions to sophisticated ergonomic and technological platforms that serve diverse user needs and applications.

Gaming Chair Industry Leaders

Secretlab

DXRacer

Herman Miller

Noblechairs

GT Omega

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A clear whitespace sits at the intersection of gaming aesthetics and office-grade ergonomics, where buyers want multi-tilt mechanisms, adjustable lumbar support, and durable components without overtly aggressive styling. Secretlab expanding into a task-focused ergonomic chair with the Secretlab Atlas (June 2026) shows demand adjacency and supports procurement conversations beyond core gamers, including hybrid work users and corporate facilities teams that already ask for standardized durability and safety performance (often framed around ANSI/BIFMA). Product roadmaps that combine ergonomic credibility with easier-to-spec configurations (size ranges, replaceable wear parts, and subdued palettes) also align with the commercial segment growth reflected in the report context.

Materials and compliance support another differentiation pathway. Regulatory attention on upholstered furniture flammability compliance in the United States, alongside rising sustainability scrutiny on petro-based synthetics, is driving experimentation with fabric or mesh and alternative coatings. This connects directly to the report finding that PU leather held 52.12% share in 2025 while fabric or mesh is the faster-growing material segment. Brands that can document flammability compliance (TB 117-2013 aligned) and build a credible sustainability story around recycled textiles or lower-impact coverings are better positioned for enterprise purchasing and education esports labs, where procurement increasingly requests compliance documentation alongside ergonomic claims.

Recent Industry Developments

- July 2026: Secretlab scheduled the final drop of 100 units of its McLaren MonoCell Edition gaming chair for July 13, 2026. The limited-run strategy reinforces premium positioning and keeps high-visibility motorsport collaborations in the product cycle, supporting brand pull in a crowded mid-to-premium market.

- October 2025: Herman Miller Gaming introduced two new colorways, Ignite and Nova, for the Embody Gaming Chair. The refresh extends the lifecycle of a flagship SKU while giving retailers and direct channels a new merchandising hook without changing the core ergonomic platform.

- June 2024: Herman Miller Gaming updated the Vantum Gaming Chair with new colorways and a redesigned headrest. The change targets comfort and creator use cases, helping the brand address long-session ergonomics while maintaining a distinct gaming line under the MillerKnoll portfolio.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the gaming chair market covers revenue earned from chairs that are designed and marketed for gaming comfort and posture support, and sold through consumer and business purchase channels across major regions.

Scope exclusions: office chairs not positioned for gaming, generic seating without gaming-focused design cues, and second-hand resale are excluded from the market value.

Segmentation Overview

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with building the demand story and identifying what can be measured in public data. We refer to sources such as the United Nations Comtrade database for trade direction, national statistics offices for consumer spending signals, and customs or tariff schedules that help classify seating imports and exports. Regulatory and standards bodies for furniture safety references are used as supporting context, and peer-reviewed ergonomics and occupational health journals are reviewed for posture and comfort claims that influence buying decisions.

To size the commercial landscape, we also review company annual reports, investor presentations, and product catalogs to understand price ladders and feature positioning. News and financial coverage is used to track new launches, channel shifts, and major distribution moves, and paid subscription sources for company financials and intelligence help with private company context where public filings are limited. The desk sources listed above are illustrative, and we use additional public references to collect, cross-check, and clarify data points.

Primary Interviews and Surveys

Primary work is used to pressure test assumptions that desk sources cannot settle, including typical selling prices by material, the split between residential and commercial buying, and whether demand is driven more by replacement or first-time setup. We speak with a mix of brands, distributors, specialty retailers, corporate procurement contacts, and informed industry experts across APAC, EMEA, and the Americas, so the regional splits and channel shares we apply remain realistic.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 15% | APAC: 47% |

| Mid tier: 58% | Functional/Unit leaders: 25% | EMEA: 33% |

| Smaller Players: 17% | Managers: 60% | Americas: 20% |

Market-Sizing & Forecasting

Sizing is built using top-down and bottom-up logic so the final value remains tied to real-world buying signals. On the top-down side, we use furniture and seating production, trade flows, and consumer durable spending indicators to reconstruct the addressable chair pool, then narrow it to gaming-design demand using penetration and mix assumptions that are checked against interview feedback. After the demand pool is formed, it is translated into value using price ladders that reflect common price bands and material premiums.

To keep the totals practical, we then run selective bottom-up checks using sampled price points across online and offline channels, plus shipment and assortment checks from distributors where available. Inputs that frequently move the model include average selling price by material (PU leather, PVC leather, and fabric or mesh), the share of online versus offline sales, the weight of residential versus commercial purchases, replacement cycle assumptions, and regional e-sports and gaming participation signals that affect new setups. When a bottom-up view is incomplete, gaps are handled by applying conservative ranges from comparable regions, then re-testing those ranges with channel participants.

For forecasting, scenario analysis is used so growth reflects different paths for gaming participation, hybrid work setups, and price inflation by region. A short list of drivers is projected forward, and then the final forecast is aligned to what primary respondents consider reasonable for near-term pricing and volume momentum.

Data Validation & Update Cycle

Validation is done through several passes that look for values that do not fit broader market reality. We compare model outputs against independent signals such as furniture trade direction, visible pricing trends, and channel feedback on demand strength, then investigate sharp variances before locking the numbers. If a mismatch appears, assumptions are revisited and follow-up outreach is triggered to confirm whether the issue is timing, pricing, channel mix, or geography weighting.

Before sign-off, a separate analyst reviews the work for logic consistency, unit alignment, and currency conversions. Reports are refreshed annually, and interim updates are made when material events affect demand or pricing. Immediately prior to delivery, a final quick scan is performed so clients receive the latest updated view.

Mordor Intelligence's Gaming Chair Market Sizing Compared With Other Published Estimates

Published market sizes for gaming chairs can vary even when the topic sounds identical, because different studies do not always count the same products, years, and buying channels. The spread usually comes from scope choices, price assumptions, and how carefully totals are checked against real market signals.

The main gap comes from whether an estimate treats gaming chairs as a narrow product category sold for gaming setups, or as a wider ergonomic seating bucket. In this area, Mordor Intelligence counts value only when the chair is positioned and sold as a gaming chair across both B2C and B2B channels, using ASP ladders and region splits that are re-checked with interview feedback.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.78 B (2026) | |

| Global Consultancy A | USD 1.80 B (2025) | Uses a different base year and can fold adjacent ergonomic seating into the count, which pushes the value upward even when gaming-specific design and positioning are not consistently filtered. |

| Industry Portal B | USD 1.45 B (2024) | Anchors the market in an earlier year and relies more on a straight forecast curve, with fewer stated checks on price progression by material and on channel mix changes across regions. |

Across the figures, the differences align with year selection, what qualifies as a gaming chair, and how pricing and channel shares are treated. By keeping the scope tied to gaming-positioned chairs and then sanity-checking totals with trade, pricing, and interview inputs, the estimate stays traceable to clear assumptions that can be reviewed and updated.

Key Questions Answered in the Report

What is the forecast CAGR for the gaming chair market to 2031?

The market is projected to grow at an 7.62% CAGR between 2026 and 2031.

Which region will grow fastest in gaming chair demand through 2031?

Asia-Pacific is expected to register the quickest expansion, at a 8.98% CAGR.

Which product segment currently leads unit sales?

PC Gaming Chairs hold the largest share at 46.05% of 2025 revenues.

What is the market size in 2026?

USD 1.78 billion in 2026.

Which material is gaining favor for sustainability reasons?

Fabric and mesh upholsteries are advancing at an 8.31% CAGR as consumers seek breathable, eco-friendly options.

Page last updated on: