Electronic Clinical Outcome Assessment Solutions (ECOA) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

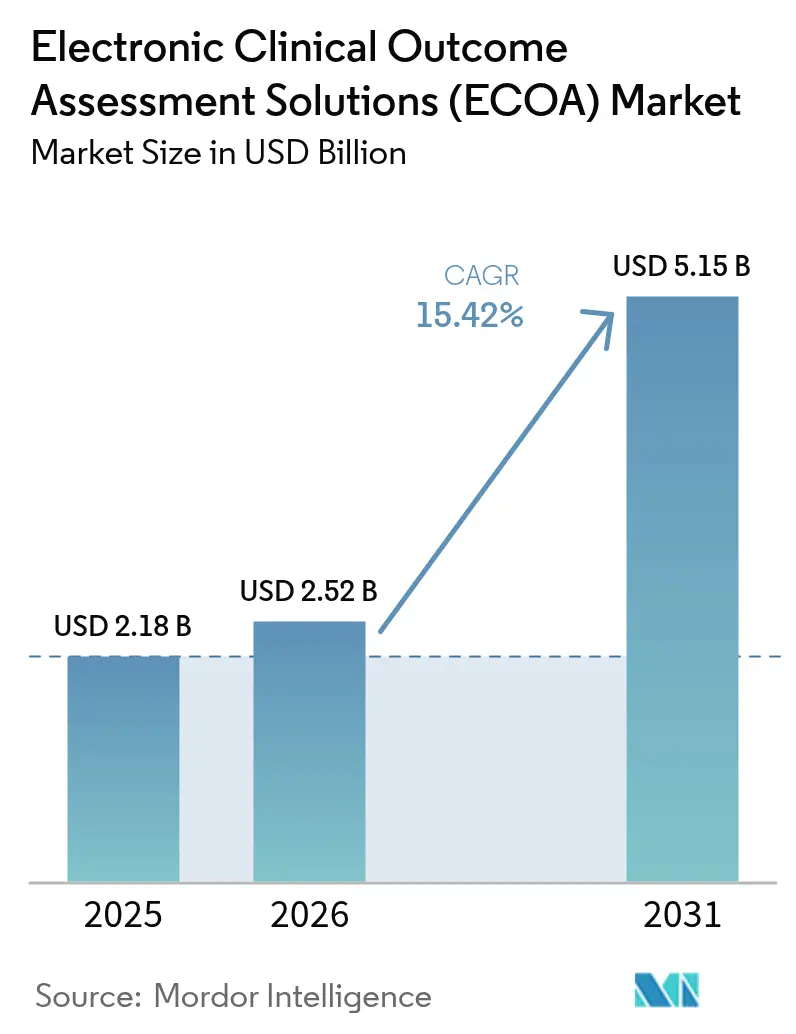

| Market Size (2026) | USD 2.52 Billion |

| Market Size (2031) | USD 5.15 Billion |

| Growth Rate (2026 - 2031) | 15.42% CAGR |

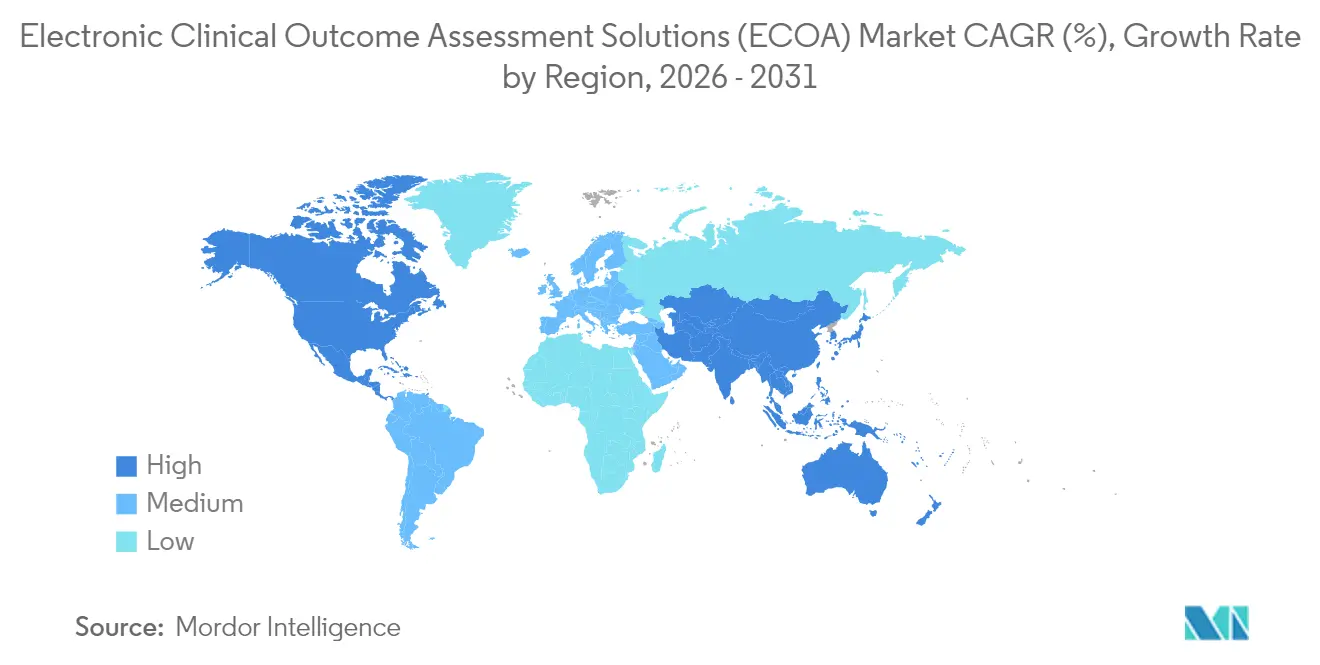

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Electronic Clinical Outcome Assessment Solutions (ECOA) Market Analysis by Mordor Intelligence

The electronic clinical outcome assessment solutions market size is expected to grow from USD 2.18 billion in 2025 to USD 2.52 billion in 2026 and is forecast to reach USD 5.15 billion by 2031 at 15.42% CAGR over 2026-2031. Intensifying regulatory focus on patient-centric evidence, rapid migration to cloud-native eClinical stacks, and the widespread adoption of decentralized trial models are accelerating platform demand [1]Center for Drug Evaluation and Research, “Electronic Systems in Clinical Investigations,” FDA.gov . Pharmaceutical sponsors view these systems as the primary mechanism for collecting high-integrity patient-reported, clinician-reported, observer-reported, and performance outcomes data that inform labeling and reimbursement. Mature vendors keep broadening their suites through acquisitions, while niche players differentiate with artificial-intelligence decision support and integrated payment capabilities. Emerging economies add further tailwinds by offering cost advantages that encourage multi-regional trial execution.

Key Report Takeaways

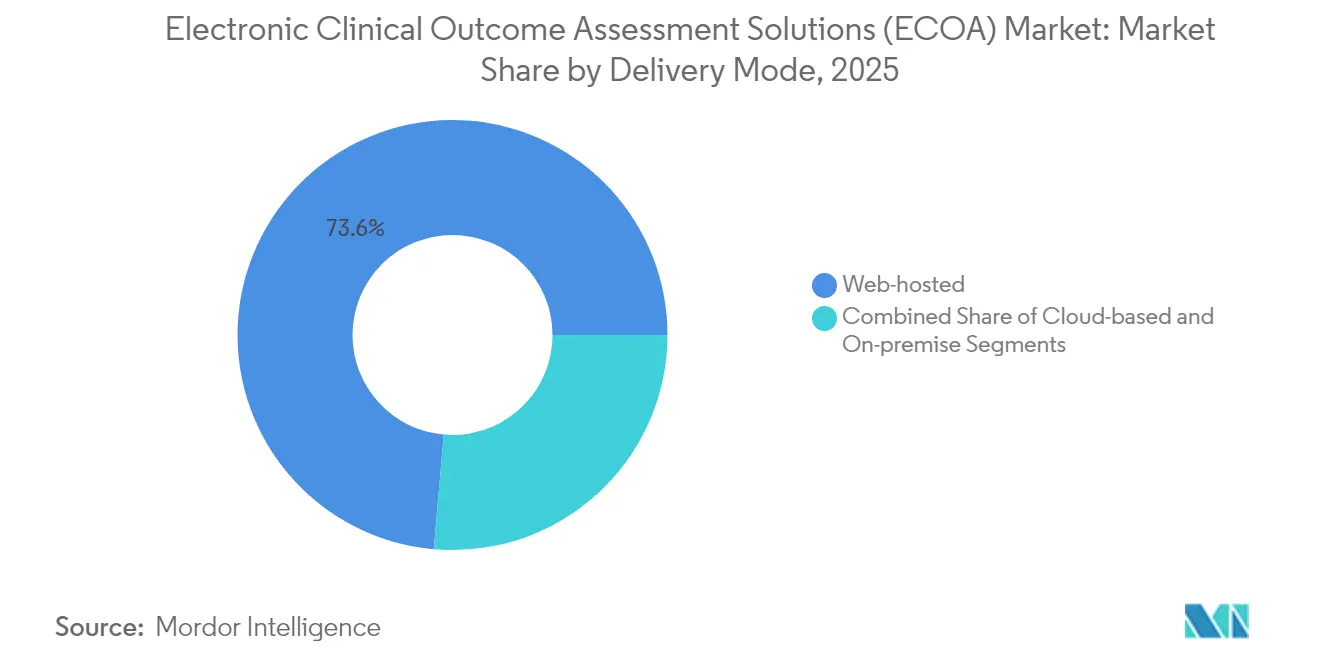

- By delivery mode, web-hosted solutions led with 73.61% revenue share in 2025; cloud-based platforms are forecast to expand at a 15.98% CAGR through 2031.

- By approach, patient-reported outcomes captured 48.45% of electronic clinical outcome assessment solutions market share in 2025; clinician-reported outcomes are advancing at a 16.05% CAGR to 2031.

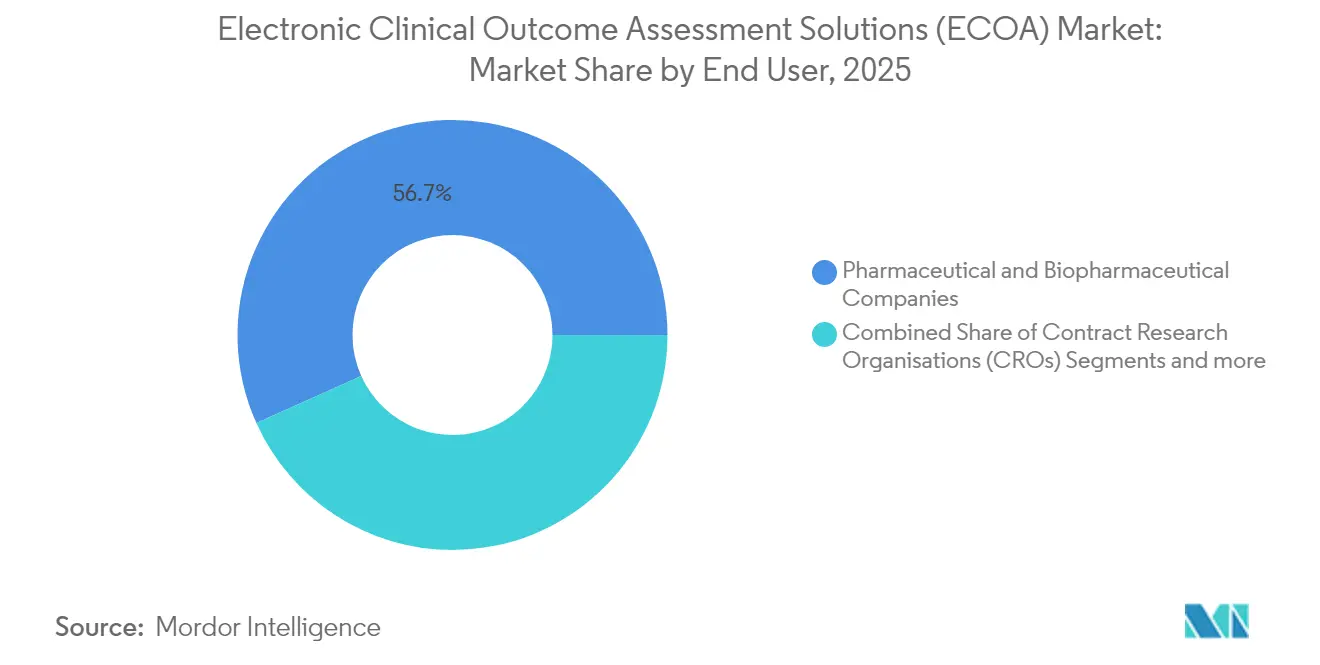

- By end user, pharmaceutical companies accounted for 56.72% of electronic clinical outcome assessment solutions market size in 2025, while contract research organizations are poised for 16.02% CAGR growth to 2031.

- By geography, North America commanded 41.76% share of the electronic clinical outcome assessment solutions market size in 2025, whereas Asia-Pacific is projected to post the highest regional CAGR at 16.29% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Electronic Clinical Outcome Assessment Solutions (ECOA) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing outsourcing of clinical trials by pharma & biotech sponsors | +2.8% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Expansion of cloud/SaaS-based eClinical stacks | +3.1% | Global, led by North America, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Regulatory push for patient-focused drug development | +2.5% | Global, with FDA and EMA leadership | Long term (≥ 4 years) |

| Accelerating shift to decentralized & BYOD trial models | +3.4% | North America & Europe core, spill-over to Asia-Pacific | Medium term (2-4 years) |

| BYOD-enabled wearables lower device costs & boost compliance | +1.9% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| AI-driven adherence coaching lifts PRO data quality | +1.8% | North America & Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Outsourcing of Clinical Trials by Pharma & Biotech Sponsors

Contract research organizations handle an expanding share of trial execution because sponsors prioritize core discovery activities. In the United States, the biopharmaceutical CRO market is projected to reach USD 19.75 billion by 2033, a signal of enduring outsourcing appetite. CROs now adopt turnkey electronic clinical outcome assessment solutions platforms, offering sponsors unified data capture, randomization, and patient engagement services at scale. Consolidation, exemplified by the Suvoda–Greenphire merger, creates integrated ecosystems spanning eCOA, payments, and supply chain functions [2]Suvoda LLC, "Suvoda and Greenphire to merge creating a technology platform optimizing clinical trial processes and streamlining the patient journey," suvoda.com. Post-pandemic staffing shortages—Clinical Research Associate turnover rates exceed 25%—reinforce the preference for external partners capable of supplying trained digital-trial personnel [3]Grace Parrish, "CRA Turnover Within Contract Research Organizations Post-COVID-19: A Cross-Sectional Study," Clinical Researcher, acrpnet.org.

Expansion of Cloud/SaaS-Based eClinical Stacks

Cloud deployments outpace legacy web-hosted models as sponsors seek elasticity, automated validation, and lower total cost of ownership. FDA’s Computer Software Assurance guidance supports risk-based verification, reducing barriers to cloud adoption while preserving 21 CFR Part 11 requirements. Major providers such as Microsoft Azure meet SOC 1, SOC 2, and ISO/IEC 27001 standards, giving life-science teams out-of-the-box security frameworks. Specialized firms like USDM automate patch management and maintain continuous audit readiness, enabling multi-regional compliance for sponsors running concurrent studies.

Regulatory Push for Patient-Focused Drug Development

The FDA’s patient-focused drug development program mandates systematic capture of patient experience measures during pivotal studies, making fit-for-purpose eCOA platforms indispensable. October 2024 guidance on core patient-reported outcomes in oncology supplies standardized instrument templates, reducing method-qualification uncertainty. Parallel EMA recommendations on computerized systems produce trans-Atlantic alignment that lowers implementation complexity for global trials. Digital end-point qualification—such as stride velocity for Duchenne muscular dystrophy—illustrates regulators’ openness to novel outcome measures that depend on real-time sensor feeds.

Shift Toward Decentralized & BYOD Trial Models

Decentralized designs achieve 10% faster recruitment and improved demographic diversity compared with site-centric models. September 2024 FDA guidance clarifies operational expectations for trials incorporating home visits, telemedicine, and direct-to-patient IMP shipping, cementing DCT legitimacy. Bring-your-own-device strategies cut provisioning costs and raise adherence because participants use familiar smartphones, but they require rigorous equivalence testing across operating systems. Government support, evidenced by BARDA’s five-year agreement with Allucent to scale decentralized infrastructure, further legitimizes the model.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-security & privacy-breach concerns | -1.7% | Global, with heightened EU focus under GDPR | Short term (≤ 2 years) |

| High upfront implementation & validation costs | -2.1% | Global, greater impact on smaller biotech | Medium term (2-4 years) |

| Shortage of eCOA-skilled clinical-ops workforce | -1.4% | North America & Europe primarily | Medium term (2-4 years) |

| Device heterogeneity risks measurement equivalence | -1.2% | Global, with regulatory focus in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-Security and Privacy-Breach Concerns

The FDA now requires a software bill of materials for connected medical technologies, compelling eCOA vendors to maintain robust vulnerability monitoring programs. Europe’s GDPR adds strict data-transfer constraints, forcing sponsors to deploy regional data-residency controls and layered encryption. Enforcement actions—such as the FDA’s 2024 warning letter to Exer Labs—underscore the financial and reputational hazards of inadequate cybersecurity. Rising scrutiny of algorithmic transparency leads 72% of healthcare organizations to favor government oversight of AI-driven predictive models, putting pressure on vendors to explain machine-learning logic in plain language.

High Upfront Implementation and Validation Costs

Phase III trials already absorb the bulk of development budgets, and validating eCOA software across devices, languages, and demographic subgroups adds further expense. The eCOA Consortium stresses that sensor-based data streams must undergo fit-for-purpose evaluation, prolonging project timelines. Wearable validation studies reveal inter-site variability, obliging sponsors to fund extensive standardization and monitoring infrastructure. Although the Computer Software Assurance framework lightens some paperwork, sponsors still need specialized quality engineers and statisticians—resources in short supply among early-stage biotech firms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Delivery Mode: Cloud Migration Gains Momentum

Web-hosted deployments held 73.61% of electronic clinical outcome assessment solutions market share in 2025 because many sponsors rely on established data-center contracts. The model’s familiarity and proven audit readiness sustain near-term preference, particularly for late-phase portfolios where continuity outweighs innovation. However, cloud-native platforms are expanding at a 15.98% CAGR to 2031, reflecting sponsors’ drive for elastic capacity, real-time analytics, and automated regulatory updates. Microsoft Azure’s security certifications and FDA-endorsed risk-based validation create confidence that cloud infrastructure can satisfy data-integrity mandates.

Sponsors shift workloads incrementally, often starting with early-phase or observational studies before migrating pivotal trials once internal policies mature. Hybrid architectures that tether legacy web-hosted databases to cloud analytics services help firms manage transition risk. As a result, cloud solutions are projected to capture a growing slice of electronic clinical outcome assessment solutions market size, while on-premise instances retreat to niche scenarios demanding maximal data control, such as defense-funded infectious-disease projects.

By Approach: PRO Dominance Meets ClinRO Acceleration

Patient-reported outcomes accounted for 48.45% of electronic clinical outcome assessment solutions market size in 2025, anchored by longstanding FDA labeling precedents and patient-focused drug development policy. Clinician-reported outcomes are on track for a 16.05% CAGR, propelled by embedded eSource modules that let investigators enter scores directly within electronic health-record environments. Observer-reported measures retain specialized use in pediatrics and dementia, while performance outcomes rise alongside validated digital biomarkers.

Natural-language processing now transforms unstructured narrative fields into structured ClinRO variables, reducing time burdens and error rates for busy physicians. Signant Health’s electronic clinician rating modules exemplify how decision-support prompts standardize scoring while preserving clinical nuance. As wearable companies qualify additional digital biomarkers—gait speed, heart-rate variability—performance outcomes will transition from exploratory endpoints to co-primary status, broadening demand for multi-modal eCOA suites that seamlessly ingest sensor data.

By End User: CRO Demand Outpaces Sponsor Investment

Pharmaceutical and biopharmaceutical firms represented 56.72% of electronic clinical outcome assessment solutions market share in 2025, reflecting direct accountability for registrational data integrity. Nevertheless, contract research organizations are advancing at a 16.02% CAGR, mirroring the broader outsourcing wave that sees sponsors externalize operational complexity. Leading CROs bundle eCOA capability with site payments, eConsent, and randomization to offer unified digital trial blueprints. The Suvoda–Greenphire merger typifies how service providers combine complementary assets to streamline study start-up and investigator remuneration.

Academic medical centers and government agencies, although smaller consumers, fuel innovation by piloting novel digital endpoints in rare-disease cohorts where commercial incentives are limited. The expanding public-private partnership model, supported by the NIH’s Decentralized Trial Innovation Network, introduces open-source toolkits that lower adoption barriers for resource-constrained institutions, indirectly nurturing expertise that later migrates to CRO and sponsor teams.

Geography Analysis

North America dominates the electronic clinical outcome assessment solutions market with 41.76% share, driven by stringent yet well-defined FDA regulations, sophisticated clinical research infrastructure, and early deployment of patient-centric metrics. Continuous FDA guidance, including the Computer Software Assurance framework, underpins sponsor confidence by clarifying validation expectations. The United States accounts for most regional revenue, with Canada contributing specialized day-1 access programs for rare diseases and Mexico offering cost-effective Phase I units.

Asia-Pacific records the fastest regional expansion at 16.29% CAGR, reflecting harmonized trial policies, rising domestic R&D investment, and the promise of lower per-patient costs. China’s streamlining of clinical-trial approval timelines, India’s digital-health mission, and South Korea’s telemedicine pilots collectively foster a receptive environment for decentralized study designs that require robust eCOA backbones. Nevertheless, divergent data-localization policies and language complexity demand that vendors deliver multi-tenant architectures with configurable sovereignty controls.

Europe, supported by EMA alignment and national eHealth agendas, remains a stable adopter. Germany’s hospital digitalization budget and the UK’s Medicines and Healthcare products Regulatory Agency sandbox stimulate uptake of sensor-driven outcomes in oncology and neurology. Meanwhile, GDPR compliance costs push smaller biotech to partner with established vendors holding pre-certified hosting zones, ensuring uninterrupted flow of electronic clinical outcome assessment solutions market transactions across the continent.

Competitive Landscape

The market shows moderate concentration. Medidata, Signant Health, and Clario together hold a sizeable portion, yet numerous mid-tier and emerging suppliers exploit specialty niches. Medidata extends its leadership by integrating eCOA into its unified clinical platform and by launching the Site Insights Program, which feeds site feedback into study design. Signant Health collaborates with IQVIA on the One Home for Sites framework, consolidating investigator portals and electronic source to enhance workflow efficiency. Clario bolstered its portfolio by acquiring WCG’s eCOA unit, widening geographic reach and deepening expertise in complex therapeutic areas.

New entrants differentiate through artificial-intelligence modules. Kayentis mines adherence patterns to trigger personalized nudges, while Medable Studio allows drag-and-drop configuration of multilingual instruments to reduce build time. Oracle and Veeva Systems position enterprise-grade data lakes that merge operational and clinical signals, promising real-time risk-based monitoring. Midsize players specialize further: some focus on pediatric endpoints, others on integration of high-frequency wearable feeds.

Amid consolidation, white-space remains in low-resource settings where local language support, offline functionality, and ruggedized hardware are essential. Vendors able to meet those requirements stand to capture incremental electronic clinical outcome assessment solutions market share as sponsors extend trials into Africa and Latin America.

Electronic Clinical Outcome Assessment Solutions (ECOA) Industry Leaders

-

Kayentis

-

IQVIA Inc.

-

Parexel International Corporation

-

Signant Health

-

WIRB-Copernicus Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Clario acquired the electronic clinical outcome assessment business from WCG, enhancing its ability to deliver comprehensive solutions for global trials.

- March 2025: Medidata Solutions launched the Site Insights Program to elevate site engagement and embed study design feedback directly into its unified platform.

- January 2025: Suvoda and Greenphire announced a merger to form a combined clinical-trial technology suite covering randomization, supply management, eConsent, eCOA, and patient payments.

- August 2024: Medable introduced Medable Studio, an all-in-one environment for configuring and validating multicomponent eCOA deployments.

Global Electronic Clinical Outcome Assessment Solutions (ECOA) Market Report Scope

As per the scope of this report, electronic clinical outcome assessment (eCOA) uses technology, such as smartphones, tablets, and computers, to allow patients, caregivers, and doctors to directly report the outcomes of clinical trials. eCOA produces highly accurate data that allows for a better understanding of the patient experience in clinical trials and ultimately helps simplify the path to approval.

The electronic clinical outcome assessment solutions (eCOA) market is segmented by delivery mode, approach, end user, and geography. By delivery mode, the market is segmented as web-hosted and cloud-based. By approach, the market is segmented by patient-reported outcome (PRO), clinician-reported outcome (ClinRO), observer-reported outcome (ObsRO), and performance outcome (PerfO). By end user, the market is segmented as pharmaceutical and biopharmaceutical companies, contract research organizations, and other end user. By geography, the market is segmented as North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD) for the above segments.

| Web-hosted |

| Cloud-based |

| On-premise |

| Patient-Reported Outcome (PRO) |

| Clinician-Reported Outcome (ClinRO) |

| Observer-Reported Outcome (ObsRO) |

| Performance Outcome (PerfO) |

| Pharmaceutical and Biopharmaceutical Companies |

| Contract Research Organisations (CROs) |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Delivery Mode | Web-hosted | |

| Cloud-based | ||

| On-premise | ||

| By Approach | Patient-Reported Outcome (PRO) | |

| Clinician-Reported Outcome (ClinRO) | ||

| Observer-Reported Outcome (ObsRO) | ||

| Performance Outcome (PerfO) | ||

| By End User | Pharmaceutical and Biopharmaceutical Companies | |

| Contract Research Organisations (CROs) | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving the strong CAGR in the electronic clinical outcome assessment solutions market?

Expansion of decentralized trials, regulatory mandates for patient-focused evidence, and accelerated cloud adoption collectively underpin a 15.42% CAGR through 2031.

Which delivery mode is growing the fastest?

Cloud-based platforms are advancing at 15.98% CAGR, outpacing web-hosted and on-premise models as sponsors seek scalable, compliance-ready infrastructure.

Why are CROs gaining electronic clinical outcome assessment solutions market share?

Sponsors outsource trial execution to CROs to offset workforce shortages and leverage specialized digital expertise, fueling a 16.02% CAGR for CRO adoption.

Which region offers the largest growth opportunity?

Asia-Pacific is projected to post a 16.29% CAGR, helped by regulatory harmonization and cost-efficient patient recruitment.

What are the main barriers to wider platform adoption?

Data-security concerns under stringent privacy regimes and high validation costs remain key obstacles, especially for smaller biotechnology firms.

How is artificial intelligence influencing platform differentiation?

Vendors integrate machine-learning modules for adherence coaching, outcome prediction, and automated data-quality checks, enhancing value to sponsors and sites.

Page last updated on: