Computerized Physician Order Entry (CPOE) Systems Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

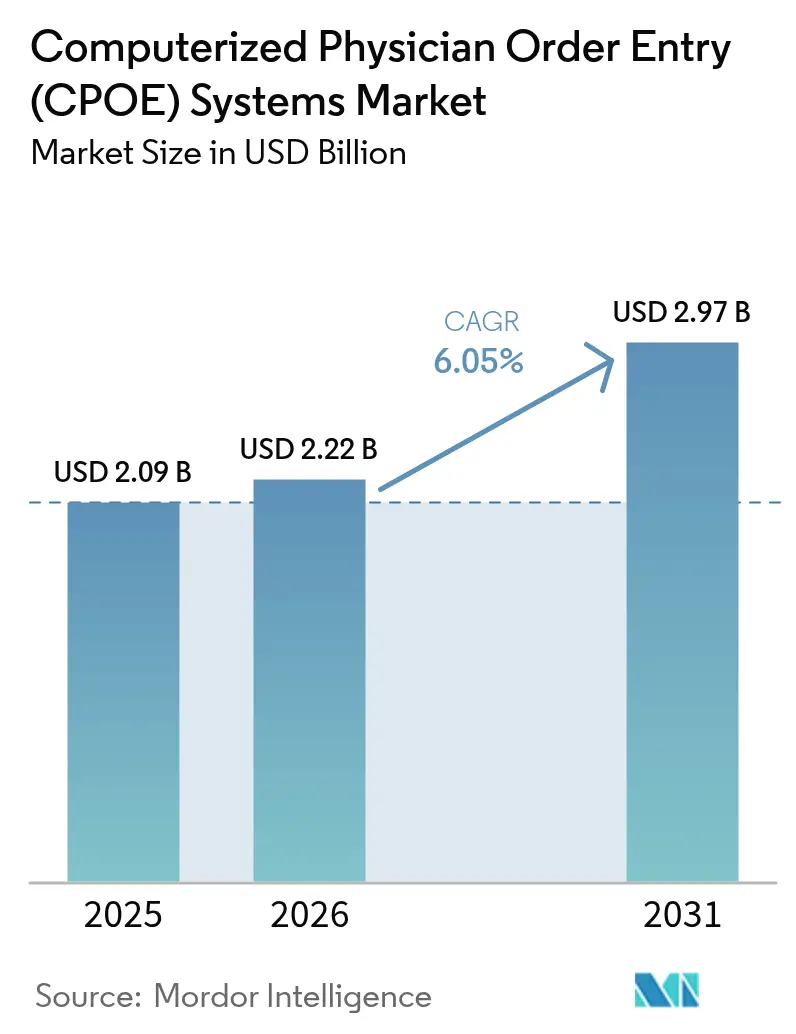

| Market Size (2026) | USD 2.22 Billion |

| Market Size (2031) | USD 2.97 Billion |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

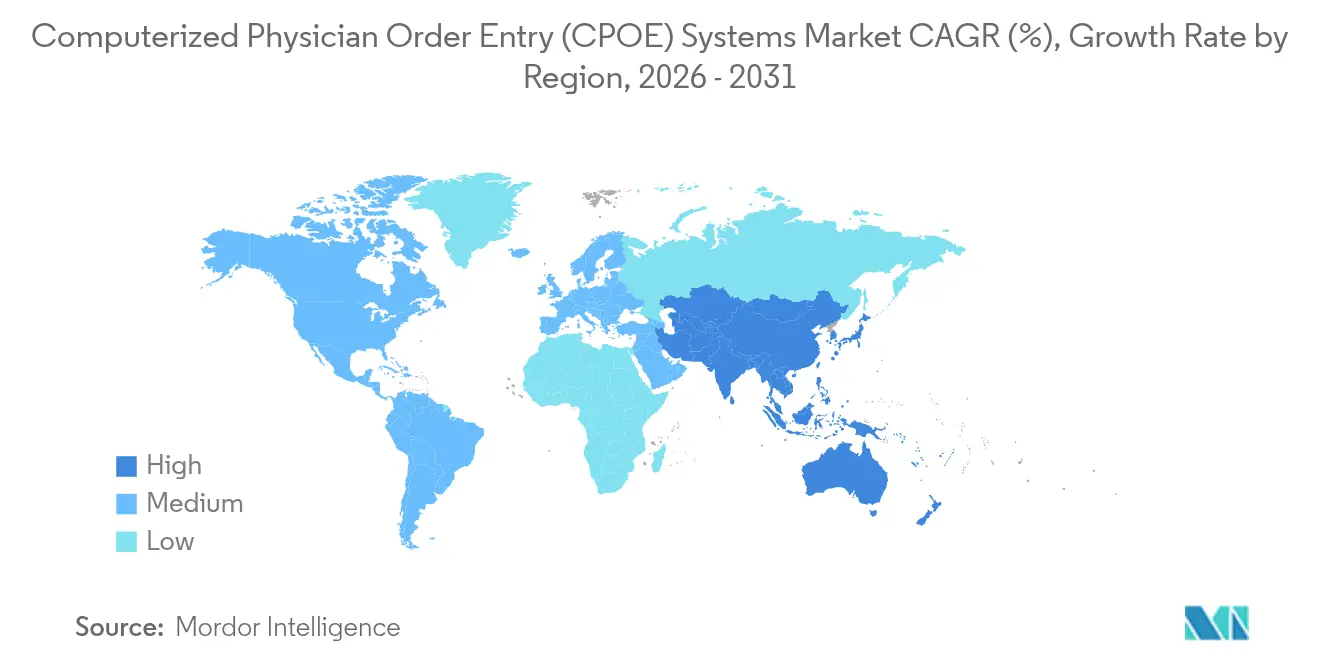

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

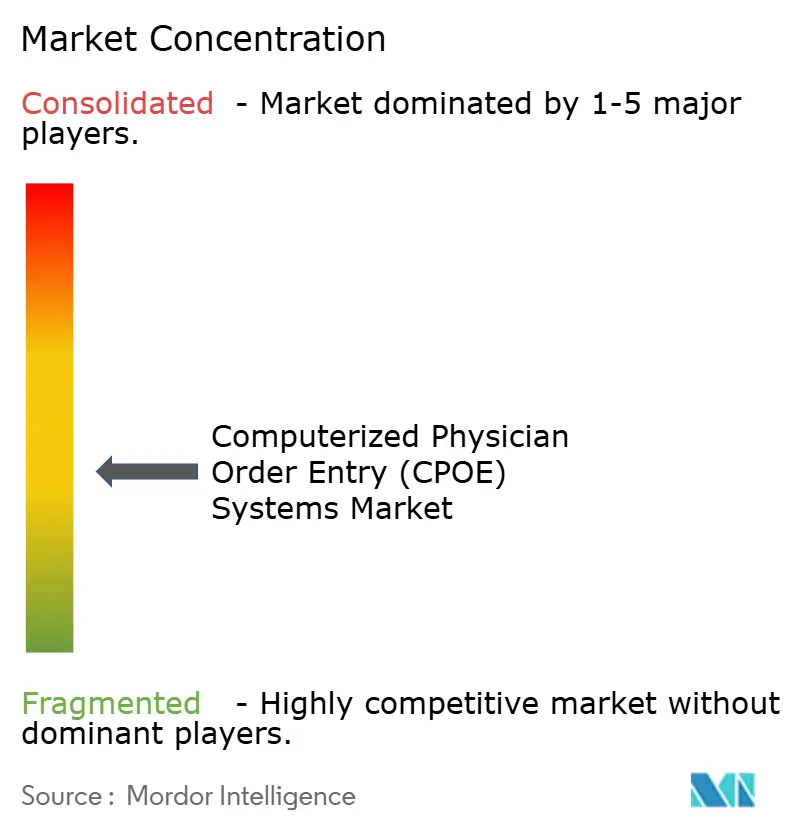

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Computerized Physician Order Entry (CPOE) Systems Market Analysis by Mordor Intelligence

Computerized Physician Order Entry (CPOE) Systems market size in 2026 is estimated at USD 2.22 billion, growing from 2025 value of USD 2.09 billion with 2031 projections showing USD 2.97 billion, growing at 6.05% CAGR over 2026-2031. Robust federal mandates, expanding accountable-care arrangements, and fast-maturing artificial-intelligence decision engines are together accelerating adoption across inpatient and ambulatory settings. Epic Systems’ plan to link every client site with the Trusted Exchange Framework and Common Agreement by year-end 2024 sets a new baseline for interoperability expectations, while Oracle Health’s struggle to stem a 25.06% to 23.1% ambulatory share slide illustrates the competitive repercussions of lagging data-exchange performance. The push toward value-based care, coupled with cloud-native deployment models that ease implementation burdens, keeps investment levels high even among cost-pressured providers. Across oncology, cardiology, and infectious-disease workflows, AI-curated order sets are reducing error rates and driving measurable quality gains, reinforcing the perception of CPOE as a strategic rather than purely transactional asset.

Key Report Takeaways

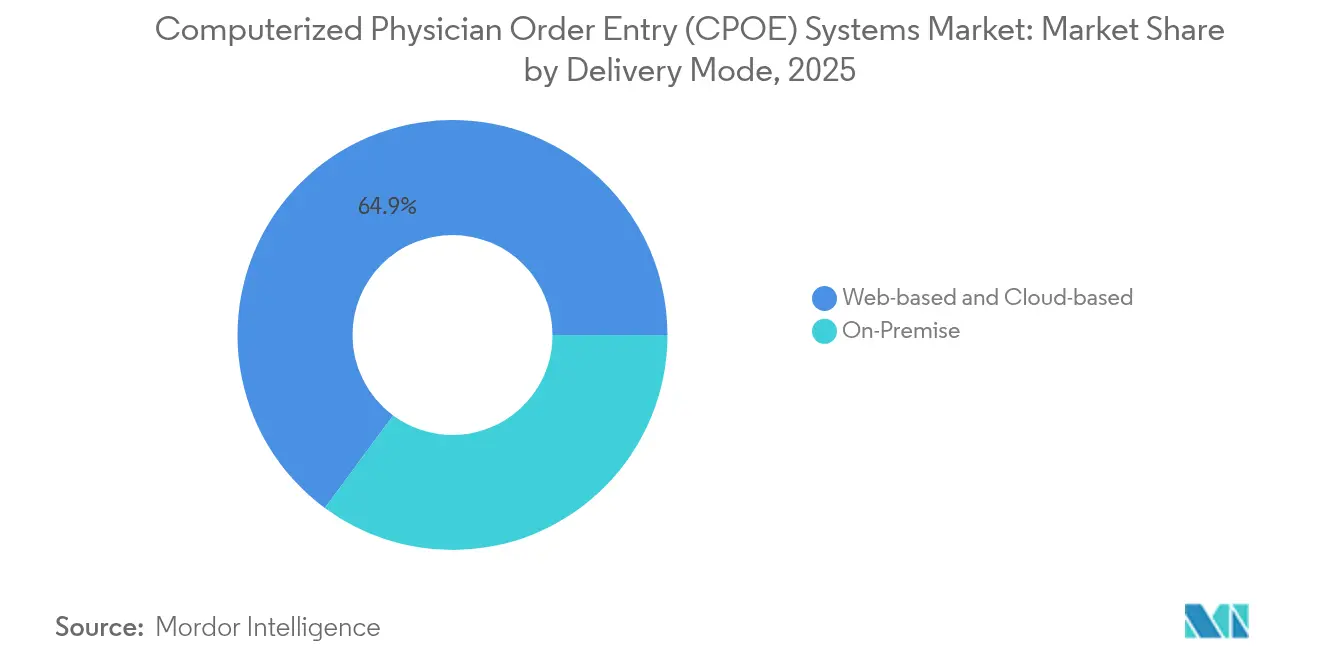

- By delivery mode, web-based and cloud platforms held 64.88% of the Computerized Physician Order Entry (CPOE) Systems market share in 2025, while on-premise deployments are expanding at a 6.78% CAGR through 2031.

- By component, software dominated with 51.02% share of the Computerized Physician Order Entry (CPOE) Systems market size in 2025, yet services are growing the fastest at 6.91% CAGR.

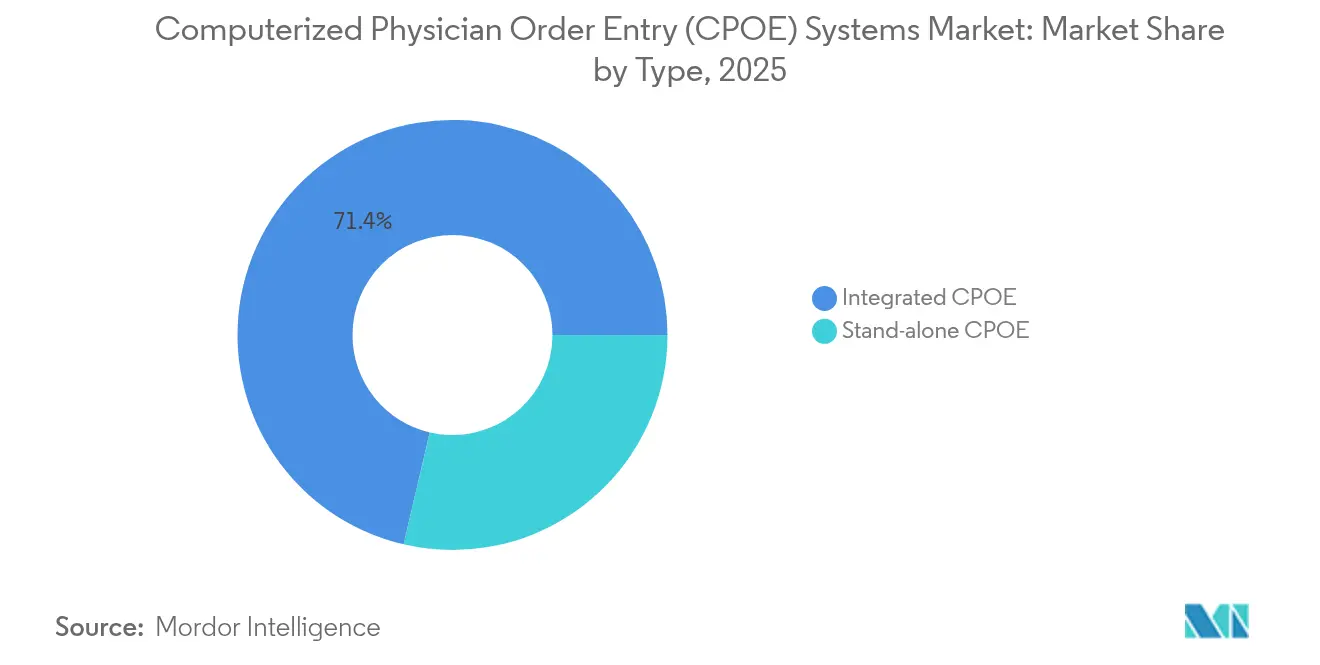

- By type, integrated solutions commanded 71.35% share of the Computerized Physician Order Entry (CPOE) Systems market size in 2025; stand-alone platforms are advancing at a 6.92% CAGR.

- By end user, hospitals and clinics accounted for 77.58% of the Computerized Physician Order Entry (CPOE) Systems market size in 2025, while ambulatory surgical centers post the quickest climb at 6.97% CAGR.

- By geography, North America contributed 42.10% of Computerized Physician Order Entry (CPOE) Systems market share in 2025; Asia-Pacific is projected to lead growth at a 7.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Computerized Physician Order Entry (CPOE) Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Federal mandates & reimbursement penalties | +1.8% | North America, with spillover to global markets | Short term (≤ 2 years) |

| Cloud-first EHR modernization waves | +1.2% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Rise of value-based care & ACO consolidation | +1.0% | North America core, expanding to APAC | Long term (≥ 4 years) |

| AI-driven medication-error prediction engines | +0.9% | Global, with advanced deployment in developed markets | Medium term (2-4 years) |

| Oncology-specific order set libraries | +0.4% | Global, concentrated in major cancer centers | Short term (≤ 2 years) |

| Sovereign health-data hosting laws boosting local cloud nodes | +0.3% | EU, with emerging requirements in APAC & MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Federal Mandates & Reimbursement Penalties

Federal rules now link reimbursement directly to electronic ordering and clinical-decision-support usage, pushing even reluctant providers to deploy compliant systems. The Medicare Promoting Interoperability Program withholds up to 4% of payments from hospitals that fail to demonstrate meaningful CPOE use. Simultaneously, the 21st Century Cures Act bars information blocking, forcing vendors to publish standardized APIs that let third-party tools pull structured data at the point of order. Because compliance deadlines cluster within 24 months, many health systems accelerate contracting cycles, favoring suppliers with proven audit trails and TEFCA connectivity. Large groups also negotiate enterprise-wide licenses to streamline attestation across multiple facilities, reinforcing the scale advantages already enjoyed by the incumbent leaders in the Computerized Physician Order Entry (CPOE) Systems market.

Cloud-First EHR Modernization Waves

Providers are shedding on-premise hardware in favor of subscription models that shift capital outlays toward predictable operating expenses. Epic’s recently launched fully managed-hosting option enables hospital chains to deploy the complete order-entry stack without building their own data centers. Oracle Health likewise pivoted its portfolio to a multi-tenant cloud after high-profile implementation setbacks. Cloud architectures eliminate lengthy version-upgrade cycles, let suppliers roll out security patches in hours, and open the door to micro-service add-ons such as specialty-specific order-set libraries. The same infrastructures underwrite national-level health-information exchanges, exemplified by InterSystems’ cloud-native IntelliCare network that shares medication orders across disparate facilities. As cyber-risk insurers increasingly require up-to-date software and immutable backups, CIOs frame cloud adoption as a resilience necessity rather than a discretionary project, boosting bookings across nearly every sub-segment of the Computerized Physician Order Entry (CPOE) Systems market.

Rise of Value-Based Care & ACO Consolidation

Accountable-care organizations expanding to cover 30 million beneficiaries insist on analytics-ready order data that proves adherence to evidence-based pathways. Modern CPOE modules therefore ship with population dashboards, cost-prediction curves, and shared-savings drill-downs, turning the order screen into a real-time risk-management console. Larger ACO networks are standardizing formularies and diagnostic panels to smooth contract performance across multiple hospitals, prompting highway-size order-set libraries. Vendors that integrate outcomes measurement—rather than merely capturing orders—secure multi-year renewals and position themselves as partners in reimbursement optimization. The trend spills into Asia-Pacific, where fledgling capitation pilots in Japan and Singapore already list CPOE data feeds as mandatory technical criteria in request-for-proposal documents.

AI-Driven Medication-Error Prediction Engines

Machine-learning algorithms that flag potential drug-patient mismatches or dose anomalies before final sign-off are cutting reported error rates by more than 70% at early-adopter sites. Some centers overlay computer-vision modules on infusion pumps to authenticate barcodes, while others embed large-language-model “copilots” that translate genomic reports into dose adjustments. Epic has quietly activated over 100 production AI workflows, from ambient speech capture that auto-populates order fields to predictive sepsis warnings in the CPOE timeline. Competitive positioning now hinges on the depth of proprietary training data, with oncology-specific vendors licensing National Comprehensive Cancer Network chemotherapy templates to accelerate system accuracy [1]David Chen, "Large language models in oncology: a review," BMJ Oncology, bmjoncology.bmj.com. Global health systems regard these AI interventions as workforce multipliers, boosting nursing productivity and reducing malpractice-related expenses, intensifying demand within the broader Computerized Physician Order Entry (CPOE) Systems market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront integration & workflow redesign costs | -1.4% | Global, with acute impact in resource-constrained markets | Short term (≤ 2 years) |

| Alert-fatigue-induced clinician pushback | -0.8% | Global, particularly in high-volume acute care settings | Medium term (2-4 years) |

| Cyber-resilience & ransomware insurance hurdles | -0.6% | Global, with heightened concern in North America & EU | Short term (≤ 2 years) |

| Shortage of HL7 FHIR integration talent in emerging markets | -0.4% | APAC, MEA, and Latin America emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Integration & Workflow Redesign Costs

Despite falling server expenditures, the human-capital intensity of mapping legacy processes, reconciling formularies, and training multidisciplinary teams keeps total project budgets daunting for small or rural institutions. Many organizations stagger roll-outs across departments to soften cash-flow strain, yet staged go-lives elongate realization of safety benefits and complicate interface maintenance. Limited pools of HL7-FHIR specialists further inflate consulting rates and extend timelines, particularly in emerging markets with nascent health-IT labor forces. Commercial lenders still view large-scale CPOE conversions as risky, so hospital boards often seek joint-purchasing alliances or public-grant co-funding to bridge financing gaps [2]Ramesh Pingili, "HOW WORKFLOW OPTIMIZATION IMPROVES PATIENT CARE," International Journal of Research In Computer Applications and Information Technology (IJRCAIT), iaeme.com. These financial and resource hurdles slow penetration among the “long-tail” of providers and shave incremental points from the otherwise robust growth outlook for the Computerized Physician Order Entry (CPOE) Systems market.

Alert-Fatigue-Induced Clinician Pushback

An intensive-care nurse can receive dozens of medication alerts per shift, and repeated exposure erodes responsiveness to truly critical warnings. Studies show nearly 68% of administrations involve workarounds that bypass at least one safety feature because users perceive the notification stack as noise. Hospitals that deployed AI-based tuning engines cut non-actionable alerts by up to 75% within 12 months. Still, optimal threshold calibration is dynamic, varying by specialty and staffing ratios, which means continuous governance is required. Burnout surveys place alarm fatigue among the top three IT complaints, ranking alongside poor single-sign-on performance and excessive documentation clicks [3]Brenda A. Nyarko, "Nurses’ alarm fatigue, influencing factors, and its relationship with burnout in the critical care units: A cross-sectional study," Australian Ciritcal Care, australiancriticalcare.com. Vendors now embed user-specific learning loops that adjust prompts in real time, yet definitive proof of sustained clinician satisfaction remains limited, tempering near-term adoption in high-acuity wings of the Computerized Physician Order Entry (CPOE) Systems market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Delivery Mode: Cloud Momentum Outpaces But Does Not Obsolete On-Premise Needs

Cloud and web-hosted solutions generated 64.88% of 2025 revenue, reinforcing the primacy of elastic architectures in the Computerized Physician Order Entry (CPOE) Systems market. Hospitals emphasize scalable capacity for seasonal surges and automatic patching, while multi-site IDNs appreciate unified governance dashboards that span geographies. In contrast, on-premise contracts, though a diminished share, clock the quickest 6.78% CAGR as data-sovereignty statutes push some European and Gulf providers to retain sensitive information within national borders. French Health-Data-Hosting rules effective November 2024 compel facilities to verify that production databases never exit the EEA, sustaining a niche for private-cloud or hybrid models that tether analytics nodes to local racks.

A hybrid topology—front-end order screens streamed over public cloud yet mirrored to an in-house archive for legal holding—emerges as a common compromise. Vendors respond with containerized micro-services that can flip between modes without code forks, minimizing validation overhead. These flexible deployment blueprints lower vendor-selection barriers for mid-market hospitals previously locked into aging monoliths, broadening the total reachable Computerized Physician Order Entry (CPOE) Systems market.

By Component: Service Engagements Close Capability-Gaps Left by Software Licenses

Software retained 51.02% of 2025 spending, owing to perpetual license renewals and incremental module upgrades that keep feature sets current. Yet service lines—implementation, optimization, user-experience redesign—advance 6.91% per year as executives realize that configuration choices, not core code, often dictate measurable outcome gains. Chief medical information officers increasingly budget for quarterly alert-governance reviews, antimicrobial-stewardship order-set tuning, and AI bias audits, turning services into an annuity.

Hardware demand now centers on mobile carts, rugged tablets, and Wi-Fi 6E network gear that ensure uninterrupted bedside access. Because cloud adoption removes local server rooms, facilities redirect capital from racks to endpoint devices, which in turn raises the bar for user-interface responsiveness. The service-heavy delivery model improves stickiness, motivating suppliers to bundle evergreen consulting in multi-year subscription tiers, a shift that inflates lifetime customer value across the Computerized Physician Order Entry (CPOE) Systems market.

By Type: Integrated Suites Leverage Data Liquidity, While Stand-Alone Tools Find Niche Buyers

Fully integrated platforms captured 71.35% revenue in 2025, pairing order entry with documentation, billing, and revenue cycle analytics in a single database. The seamless context lets physicians cascade an accepted medication order into financial authorization checks and inventory pulls without extra clicks, compressing length of stay and uncovering charge-capture leakage. Hospital chains undergoing merger activity value this uniformity, citing faster clinician onboarding and lower interface maintenance as decisive factors.

Stand-alone applications, though representing a minority, rise 6.92% annually by targeting ambulatory and outpatient surgical centers whose procedure mixes differ sharply from inpatient caseloads. Vendors emphasize lighter footprints, curated specialty order sets, and subscription tiers priced for single-location groups. Some specialists use the thinner client as a “bolt-on” to a legacy practice-management system, extracting targeted efficiency with minimal workflow disruption. This two-speed demand landscape ensures neither product archetype monopolizes growth, but integrated suites still anchor the lion’s share of the Computerized Physician Order Entry (CPOE) Systems market.

By End User: Hospitals Dominate Today, Yet Ambulatory Centers Set the Growth Pace

Hospitals and clinics represented 77.58% of total receipts in 2025, reflecting their complex needs spanning emergency, inpatient, and critical-care pathways. Multi-disciplinary governance committees prioritize enterprise-grade cybersecurity, pediatric weight-based dosing logic, and extended analytics pipelines, all favoring established mega-vendors.

Ambulatory surgical centers are the fastest climbers at 6.97% CAGR as payers push low-risk orthopedic and gastrointestinal procedures to lower-cost sites. Many ASCs procure modular CPOE suites that slot into anesthesia information systems, avoiding the overhead of full EHR rewrites. Because the share of procedures handled by ASCs is projected to hit 44 million by 2034, this user tier will meaningfully enlarge its slice of the Computerized Physician Order Entry (CPOE) Systems market.

Geography Analysis

North America commands 42.10% of 2025 revenue, attributable to stringent Medicare incentives, mature broadband connectivity, and deep vendor footprints. The Computerized Physician Order Entry (CPOE) Systems market size for the region is projected to close 2031 at USD 1.27 billion, sustaining leadership through AI-rich module upgrades that lock customers into multi-cycle relationships. Continuous TEFCA rollouts provide a “nationwide health-IT backbone,” allowing smaller community hospitals to interoperate with tertiary centers without bespoke interfaces.

Asia-Pacific logs the quickest 7.05% CAGR, underwritten by large public-sector digitization grants such as India’s Ayushman Bharat Digital Mission, which now links 300 million longitudinal health records. Singapore’s concerted IoT strategy places secure Wi-Fi endpoints inside every public ward, paving the way for wireless order entry on handhelds. Thailand’s rural tele-pharmacy kiosks automatically transmit physician orders to provincial warehouses, showcasing how CPOE functionality can leapfrog physical-infrastructure constraints. This inclusive expansion lifts total regional spending even where per-facility budgets remain modest.

Europe, the Middle East, Latin America, and Africa together provide steady mid-single-digit growth. Sovereign-cloud mandates in the EU and GCC energize local hosting partners that integrate with multinational suites. The Middle East’s plan to allocate USD 7.9 billion to health-IT upgrades by 2028 directs a significant tranche to e-prescribing and order-set engines within new tertiary campuses. Latin American ministries negotiate concessional financing with multilateral banks to fund CPOE rollouts inside public hospital rebuilds, a pipeline that could accelerate the Computerized Physician Order Entry (CPOE) Systems market once macro-economic headwinds ease.

Competitive Landscape

The market remains moderately concentrated around a handful of incumbents that pair deep R&D budgets with long maintenance track records. Epic added 29,399 inpatient beds in 2024 and broadened its artificial-intelligence roadmap to encompass ambient note capture and real-time medication-adjustment advisories. Oracle Health relinquished ambulatory share yet invested heavily in voice-activated order entry and facial-recognition authentication, seeking to recover lost momentum. InterSystems deployed its IntelliCare platform across multi-state IDNs, staking a claim on mid-tier institutions desiring vendor-neutral data fabrics.

Strategic acquisitions illustrate the race to fuse analytics, payer connectivity, and specialty content into one package. Cotiviti’s February 2025 pact to absorb Edifecs gives the claims-integrity specialist native HL7-FHIR pipes, smoothing prior-authorization workflows that intersect the ordering process. Veradigm channeled USD 140 million into ScienceIO to embed language-model summarization inside its CPOE layer, compressing manual chart reviews for oncologists evaluating complex chemotherapy regimens. On the intellectual-property front, filings relating to dynamic alert-threshold engines rose 12% year-over-year, signaling sustained emphasis on clinician-experience optimization within the Computerized Physician Order Entry (CPOE) Systems market.

Niche vendors thrive by focusing on underserved segments. MEDITECH secured “Best in KLAS” for small-hospital EHRs for an eleventh straight year, leveraging rapid, template-driven go-lives that resonate with 100-bed rural facilities. Several cloud-native start-ups supply “CPOE-as-a-Service” bundles, bundling alert fatigue analytics and antimicrobial-stewardship reports in a single per-user monthly fee, although scaling such models beyond national borders remains challenging in the face of divergent privacy codes. Overall, competitive tension centers on who can unify decision support, specialty depth, and cross-enterprise interoperability at the lowest total ownership cost, a calculus that will define share migration through the current decade.

Computerized Physician Order Entry (CPOE) Systems Industry Leaders

-

Athenahealth, Inc.

-

CliniComp International

-

Epic Systems Corporation

-

Veradigm

-

Oracle Health (Cerner)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Epic Systems debuted an enterprise resource-planning suite that natively exchanges charge codes and supply-chain data with CPOE orders, promising a single financial-clinical backbone.

- March 2025: InterSystems launched IntelliCare, an AI-enabled EHR that offers note generation and predictive analytics options across cloud, on-premise, and SaaS modes.

- February 2025: Cotiviti reached an agreement to purchase Edifecs, creating an end-to-end interoperability platform spanning payers and providers.

- December 2024: HEALWELL AI finalized its USD 165 million acquisition of Orion Health, integrating advanced clinical-decision-support capabilities into its AI portfolio.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the computerized physician order entry (CPOE) systems market as the revenue generated from new licenses, subscription fees, and implementation support for software that lets physicians and allied staff enter medication, laboratory, imaging, and treatment orders directly into an electronic record. The scope tracks integrated and stand-alone platforms across hospitals, ambulatory centers, and emergency facilities worldwide.

Scope Exclusions: Hardware such as workstation terminals and barcode scanners is tracked only for context and is not valued in the market totals.

Segmentation Overview

-

By Delivery Mode

- Web-based and Cloud-based

- On-Premise

-

By Component

- Software

- Hardware

- Services

-

By Type

- Integrated CPOE

- Stand-alone CPOE

-

By End User

- Hospitals and Clinics

- Ambulatory Surgical Centers

- Others

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed hospital IT directors, pharmacy informaticists, and regional EHR integrators in North America, Europe, Asia-Pacific, and the Gulf. These conversations clarified live price points, implementation timelines, and the share of beds running integrated versus stand-alone CPOE, allowing us to reconcile secondary indicators with field reality.

Desk Research

We began with publicly available health-IT sources such as the US Office of the National Coordinator, the Centers for Medicare & Medicaid Services, Eurostat eHealth files, and Japan's MHLW datasets, which supply adoption rates, reimbursement rules, and spending baselines. Trade bodies, including the Healthcare Information and Management Systems Society and the American Hospital Association, helped us follow hospital digitization budgets, while peer-reviewed journals in PubMed outlined medication-error prevalence that underpins CPOE demand. To size vendor revenues, we mined 10-K filings and earnings calls, then validated headline numbers through paid repositories like D&B Hoovers and Dow Jones Factiva. The sources above illustrate our mix; many additional open and paid references supported data cleaning and cross-checks.

Market-Sizing & Forecasting

First, a top-down reconstruction converted national hospital-bed inventories and average per-bed CPOE license fees into base-year value. That result was then stress-tested through limited bottom-up supplier roll-ups and channel checks. Key variables like EHR penetration, average selling price progression, medication-error incidence, Meaningful Use incentive levels, and cloud migration share drive the model each year. We forecast 2025-2030 values using multivariate regression that links spending to GDP per capita growth and policy incentives, blended with ARIMA smoothing for recent uptake spikes. Where hospital counts or fee curves were patchy, ratio imputation and regional analogs filled gaps before the final calibration.

Data Validation & Update Cycle

Every run is peer-reviewed inside Mordor; anomalous jumps trigger re-contact with sources. Outputs are reconciled against independent metrics such as eRx transaction volumes. Reports refresh annually, and material events, like major vendor pricing shifts, prompt an interim update so clients always receive our latest view.

Why Mordor's Computerized Physician Order Entry (CPOE) Systems Baseline Commands Reliability

Published figures differ because firms vary in what they count, how often they refresh numbers, and which price assumptions they prefer.

By tying value to licensed software revenue only, using current currency conversions, and refreshing each year, Mordor avoids both over-inflated 'total solution' values and dated baselines.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.09 B (2025) | Mordor Intelligence | - |

| USD 2.07 B (2024) | Global Consultancy A | mixes maintenance hardware with software fees |

| USD 2.11 B (2025) | Industry Portal B | applies uniform ASP, ignores regional discounts |

Together, the comparison shows that while totals appear close, differences arise from peripheral inclusions or pricing shortcuts. By centering on verified license revenue and tested variables, Mordor delivers a transparent, repeatable baseline decision-makers can trust.

Key Questions Answered in the Report

What is the forecast growth rate for the Computerized Physician Order Entry (CPOE) Systems market?

The market is projected to progress at a 6.05% CAGR from 2026 to 2031, moving from USD 2.22 billion to USD 2.97 billion.

Which delivery mode leads current adoption?

Web-based and cloud deployments account for 64.88% of 2025 revenue, signaling a clear industry preference for scalable, remotely managed platforms.

Why are ambulatory surgical centers considered a high-growth user segment?

Payer site-neutral policies are shifting elective surgeries away from hospitals, and ASCs need tailored order-entry systems, driving a 6.97% CAGR for this group.

How do federal mandates influence purchasing decisions?

Medicare programs tie reimbursement eligibility to meaningful CPOE use and interoperability compliance, making certified solutions a financial imperative for US hospitals.

What role does artificial intelligence play in current CPOE deployments?

AI modules predict medication errors, personalize alert thresholds, and automate data entry, raising clinical-quality metrics and differentiating advanced vendors.

Are on-premise solutions disappearing?

No; sovereign-data laws and legacy-infrastructure investments keep on-premise installations relevant, though growth is slower than in cloud segments.

Page last updated on: