Pharmaceutical E-commerce Market Size and Share

Market Overview

| Study Period | 2025 - 2031 |

|---|---|

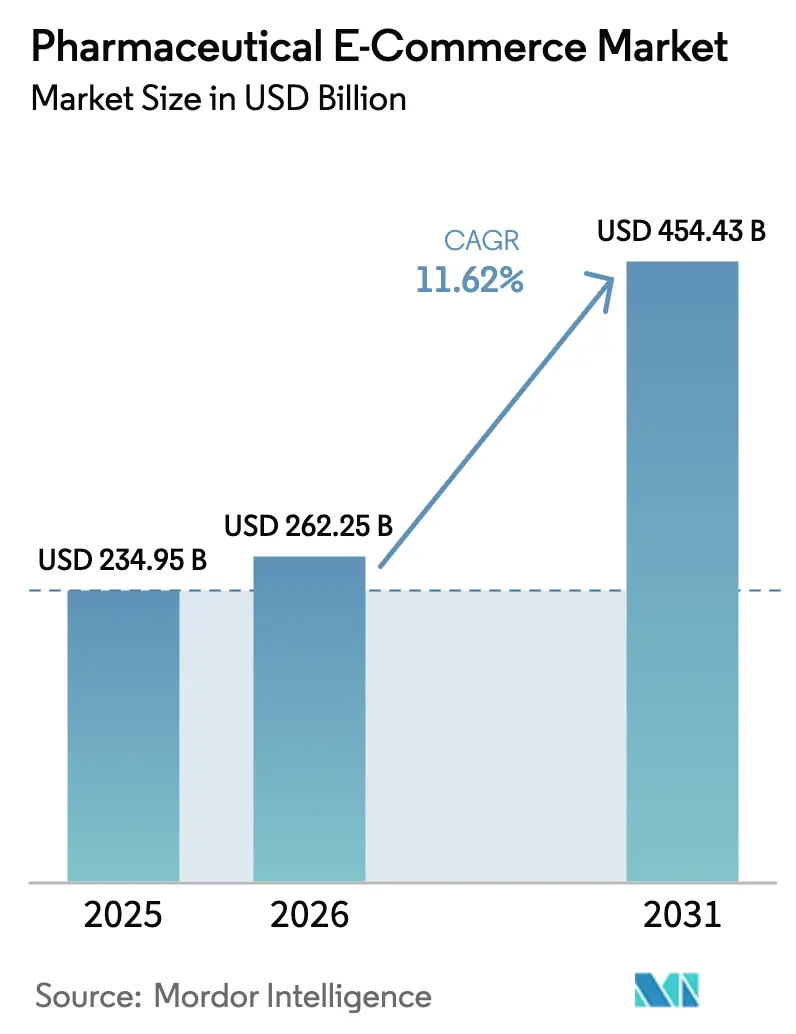

| Market Size (2026) | USD 262.25 Billion |

| Market Size (2031) | USD 454.43 Billion |

| Growth Rate (2026 - 2031) | 11.62% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pharmaceutical E-commerce Market Analysis by Mordor Intelligence

Pharmaceutical E-commerce Market size in 2026 is estimated at USD 262.25 billion, growing from 2025 value of USD 234.95 billion with 2031 projections showing USD 454.43 billion, growing at 11.62% CAGR over 2026-2031. The double-digit growth reflects sustained migration from in-store dispensing to digital-first fulfillment, a shift reinforced by telemedicine expansion, wider broadband coverage, and streamlined e-prescription rules in key jurisdictions. Ongoing investment in cold-chain logistics and cloud-based pharmacy management platforms has lowered distribution costs while extending reach into underserved areas. Aging populations, the rising prevalence of chronic diseases, and heightened consumer familiarity with on-demand delivery also elevate baseline demand, positioning the Pharmaceutical E-commerce Market as an indispensable channel within the broader USD 1.48 trillion global pharmaceutical sector. Competitive dynamics remain fluid as technology firms, pharmacy chains, and drug manufacturers race to embed seamless digital experiences that integrate diagnosis, dispensing, and adherence support.

Key Report Takeaways

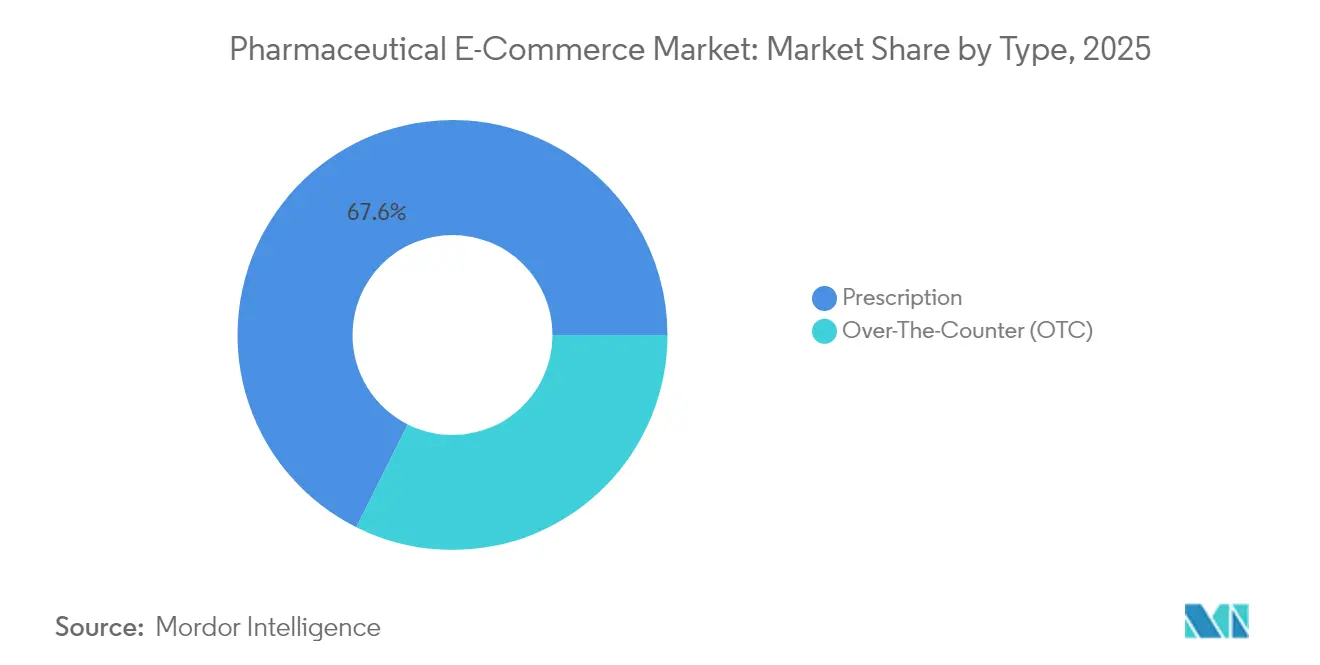

- By product category, prescription medicines accounted for 67.62% of Pharmaceutical E-commerce Market share in 2025, while over-the-counter products are projected to expand at a 14.12% CAGR through 2031.

- By product type, general medicines led with 43.71% revenue share in 2025; vaccines are forecast to grow at a 15.32% CAGR to 2031.

- By therapeutic area, diabetes treatments commanded 18.12% share of the Pharmaceutical E-commerce Market size in 2025, yet cancer therapies are advancing at a 15.06% CAGR over the same horizon.

- By Platform, third-party marketplaces captured 36.78% of revenue in 2025, whereas manufacturer-owned portals are projected to grow at a CAGR of 13.88%.

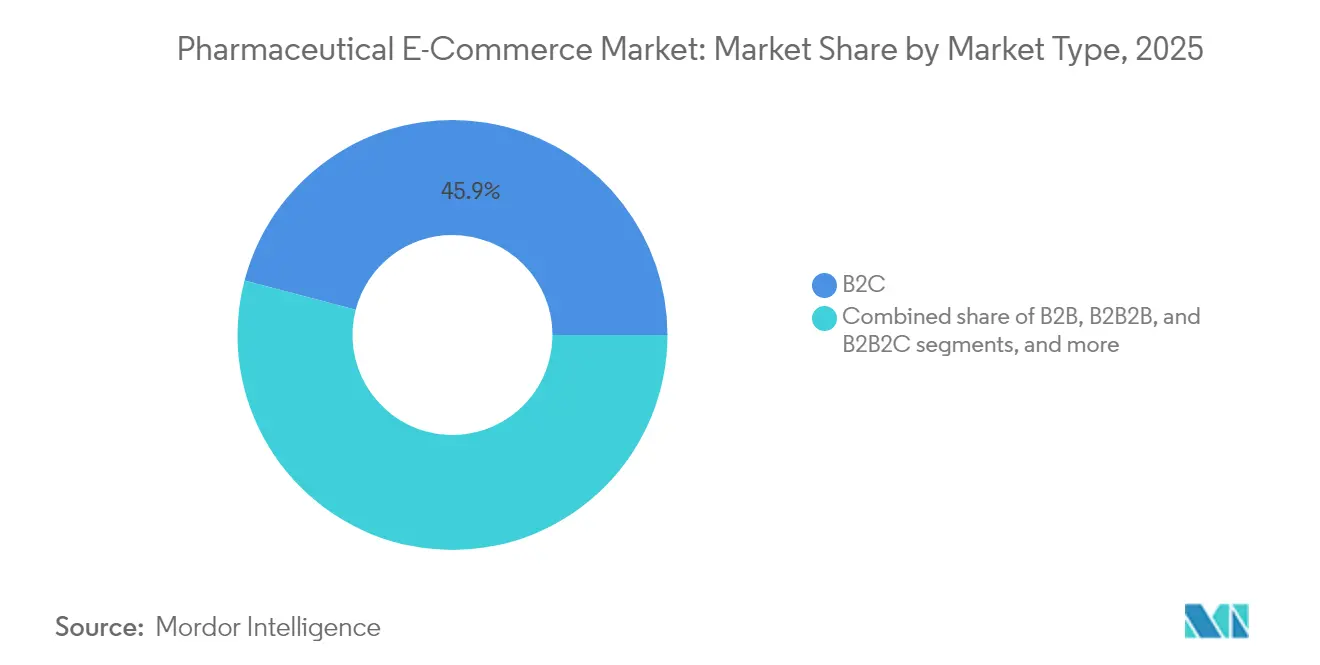

- By business model, the B2C segment held 45.92% of the Pharmaceutical E-commerce Market share in 2025, while B2B2C models record the highest projected CAGR at 14.41% through 2031.

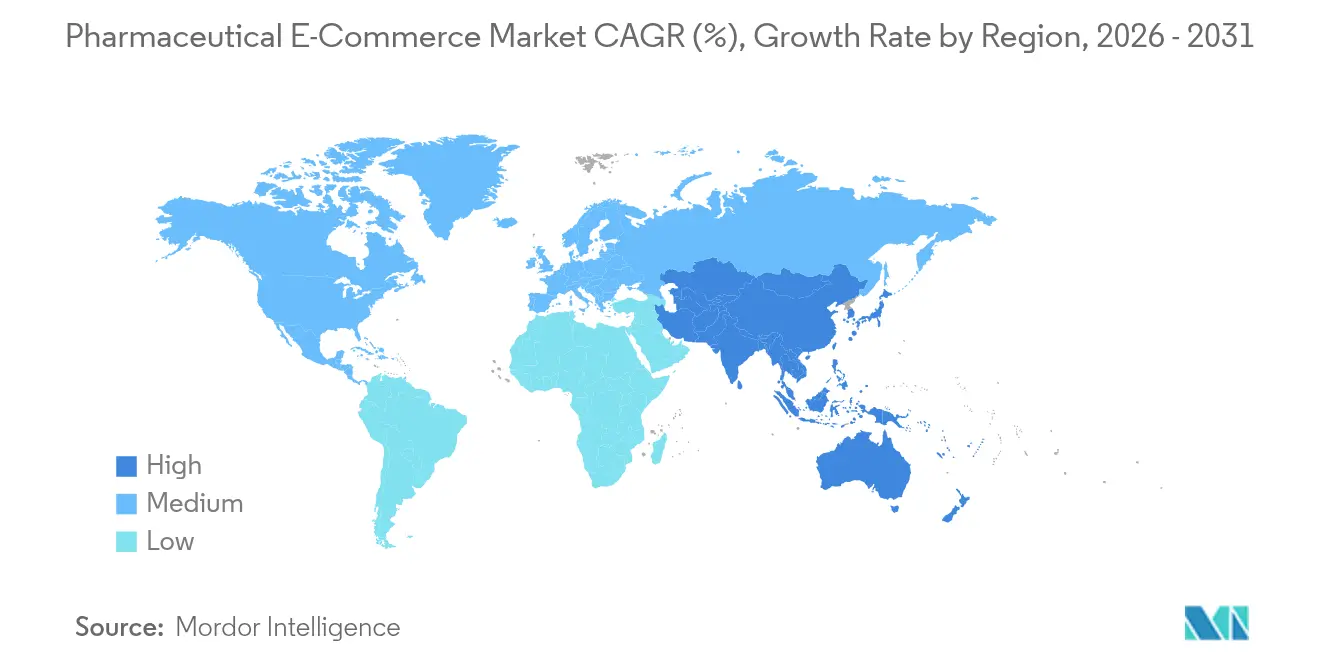

- By region, North America captured 39.71% revenue share in 2025; Asia-Pacific is on track for a 13.12% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pharmaceutical E-commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of digital health infrastructure | +2.8% | Global; strongest in North America and Asia-Pacific | Medium term (2-4 years) |

| Rising adoption of telemedicine and e-prescription services | +2.1% | North America and EU lead; Asia-Pacific scaling | Short term (≤ 2 years) |

| Growing consumer preference for convenient home delivery | +1.9% | Urban centers worldwide | Short term (≤ 2 years) |

| Increasing burden of chronic diseases and aging population | +1.7% | Global; higher in developed markets | Long term (≥ 4 years) |

| Government initiatives promoting online pharmaceutical sales | +1.4% | Asia-Pacific core; spill-over to Middle East & Africa | Medium term (2-4 years) |

| Venture capital investment fueling e-pharmacy platforms | +1.2% | North America and EU; expanding in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Digital Health Infrastructure

Digital health infrastructure now links electronic medical records, payment gateways, and cloud-based inventory systems in real time, enabling frictionless prescription validation and fulfillment. Amazon’s plan to open 20 additional on-site pharmacies in 2025 will extend same-day delivery to 45% of U.S. households, demonstrating how infrastructure spending quickly scales market access. Global logistics providers such as UPS Healthcare have added GDP/GMP-compliant cold-chain capacity across 220 countries, simplifying cross-border shipments of temperature-sensitive biologics. Improved connectivity cuts dispensing errors, reduces lead times, and expands specialty drug coverage to rural zones that previously relied on infrequent deliveries. The net result is an ecosystem where early movers lock in supply-chain efficiencies that are difficult for late entrants to replicate.

Rising Adoption of Telemedicine and E-Prescription Services

Telemedicine platforms eliminate the gap between consultation and dispensing by routing e-prescriptions directly to partnered online pharmacies. Updated DEA regulations now permit controlled-substance prescribing via telehealth under a Special Registration framework, removing a major barrier to digital fulfilment[1]DEA, “Diversion Control Special Registration for Telemedicine,” dea.gov. Eli Lilly’s LillyDirect integrates virtual visits with direct-to-home shipment of diabetes, obesity, and migraine drugs through Amazon Pharmacy, offering a unified experience that boosts adherence and reduces travel time. In rural areas where clinician shortages persist, telemedicine-e-pharmacy linkages reduce clinical inertia and ensure timely therapy initiation. This synergy also lowers payer costs by minimizing emergency visits tied to medication lapses.

Growing Consumer Preference for Convenient Home Delivery

Consumers accustomed to one-click shopping now expect the same convenience for prescription refills. Walmart’s same-day delivery service, live in 49 states as of January 2025, bundles Rx items with grocery orders, reaching 86% of U.S. households via its store network. Subscription models are also gaining traction: Amazon’s RxPass offers unlimited access to 60 generic drugs for USD 5 monthly, incentivizing chronic-disease patients to consolidate purchases on a single platform. Automated refill reminders, transparent pricing, and doorstep delivery create tangible time savings for patients balancing work and caregiving responsibilities, reinforcing loyalty to the Pharmaceutical E-commerce Market leader that offers the smoothest experience.

Increasing Burden of Chronic Diseases and Aging Population

Chronic metabolic and cardiovascular conditions drive repeat prescription volumes that align perfectly with automated e-commerce workflows. Diabetes alone accounts for 18.65% of the Pharmaceutical E-commerce Market size, underscoring the significance of refill-based revenue streams. Older adults, once reluctant digital adopters, have embraced online health services as mobility constraints intensify. Immunization gaps among adults remain wide, suggesting that convenient online scheduling and home delivery of vaccines could unlock new sales. Specialty therapies for oncology and neurodegenerative diseases also transition to self-administration, further enlarging the addressable base for e-pharmacies equipped with cold-chain and remote-monitoring capabilities.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent and fragmented regulatory frameworks | -1.8% | Global; most acute in cross-border operations | Long term (≥ 4 years) |

| Prevalence of counterfeit and substandard medicines online | -1.2% | Global; heightened in emerging markets | Medium term (2-4 years) |

| Limited cold-chain logistics capability for temperature-sensitive drugs | -1.5% | Emerging markets and remote regions | Medium term (2-4 years) |

| Digital literacy gaps among elderly and rural populations | -1.1% | Rural areas in both developed and developing markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent and Fragmented Regulatory Frameworks

Compliance complexity rises when state, federal, and supranational rules evolve at different speeds. The FDA ended its stabilization period for enhanced drug-distribution security in November 2024, compelling all large pharmacies to meet end-to-end traceability standards, while small outlets remain exempt until late 2026. Simultaneously, the European Union’s first sweeping pharmaceutical-legislation overhaul in two decades introduces new digital-dispensing requirements, challenging platforms that operate across multiple member states[2]EMA, “Common Logo for EU Online Pharmacies,” ema.europa.eu. Such divergence inflates legal costs and slows cross-border scaling, favoring well-capitalized players that can absorb documentation, auditing, and serialization expenses.

Prevalence of Counterfeit and Substandard Medicines Online

Illicit vendors exploit lax domain registration and cross-border shipping to sell unapproved drugs, undermining trust in legitimate operators. The FDA estimates that only 5% of roughly 35,000 sites offering prescription medicine to U.S. consumers comply with national law[3]FDA, “Online Pharmacies and Counterfeit Threat,” fda.gov. High-profile criminal cases, such as the conviction of Antoine Kolias for marketing counterfeit pills on mainstream retail platforms, expose enforcement blind spots and trigger tighter verification protocols. Regulatory bodies like the U.K. MHRA advise consumers to verify the official common-logo badge before purchasing, adding friction that can deter first-time digital shoppers. Failure to stem counterfeits risks stricter universal-authentication mandates that could slow the overall Pharmaceutical E-commerce Market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Prescription Dominance Faces OTC Disruption

Prescription drugs held 67.62% of Pharmaceutical E-commerce Market share in 2025, reflecting entrenched clinical oversight and reimbursement pathways tied to physician authorization. Over-the-counter items, however, expand at a 14.12% CAGR through 2031, signaling consumer willingness to self-treat common ailments without clinician visits. The FDA’s Additional Conditions for Nonprescription Use (ACNU) Final Rule, effective January 2025, creates a pathway for digital self-selection tools that could reclassify select chronic-disease therapies as nonprescription, accelerating OTC substitution.

The segment outlook suggests that platform operators able to layer decision-support algorithms on product pages will capture growth as consumers consult apps before checkout. Subscription refills tied to OTC vitamins, allergy treatments, and pain relievers further diversify revenue and offset seasonal revenue dips. Meanwhile, prescription dominance persists where insurance mandates prior authorization, yet telehealth reduces friction by converting video consultations into instant electronic prescribing. The resulting convergence blurs categorical lines, reinforcing the Pharmaceutical E-commerce Market as a single continuum rather than two siloed segments.

By Product Type: General Medicines Yield to Vaccine Innovation

General medicines contributed 43.71% of revenue in 2025, encompassing high-volume categories such as antihypertensives and antibiotics. Vaccines, though lower in base revenue, are set to climb at a 15.32% CAGR, driven by mRNA innovation and expanded adult-immunization initiatives. Lab teams have demonstrated microneedle printers capable of producing thermostable COVID-19 mRNA doses, potentially reducing cold-chain dependence and unlocking wider postal delivery.

As national immunization programs widen catch-up schedules for shingles, HPV, and pneumococcal shots, online pharmacies that integrate appointment booking with doorstep delivery or in-home administration gain an edge. Specialty cold-chain couriers continue to refine box-level temperature trackers that maintain 2-8 °C for 35 hours, a milestone that broadens viable shipping windows. General medicines remain the revenue anchor, but platform branding increasingly highlights immunization convenience, enhancing user acquisition during seasonal flu campaigns.

By Therapeutic Area: Diabetes Leadership Challenged by Cancer Growth

Diabetes treatments account for 18.12% of the Pharmaceutical E-commerce Market size, reflecting large chronic-care populations that value automatic refill services. Oncology therapies, although traditionally hospital-centric, now log the fastest growth at 15.06% due to rising availability of orally administered and antibody-drug conjugate formulations. Eli Lilly’s direct-shipment model for GLP-1 agents, distributed through Amazon Pharmacy, showcases how manufacturers bypass legacy wholesalers to expedite therapy initiation.

For oral oncology regimens, online channels streamline medication access and enable adherence monitoring via connected pill dispensers. Chronic comorbidities such as cardiovascular diseases and neurodegenerative disorders also benefit from integrated e-commerce plus remote-monitoring bundles, suggesting future cross-selling opportunities. The therapeutic-area diversification confirms that the Pharmaceutical E-commerce Market is not limited to high-volume generics but increasingly serves high-value specialty categories.

By Market Type: B2C Dominance Meets B2B2C Innovation

In 2025, business-to-consumer models accounted for 45.92% of total revenue. Direct patient engagement through user-friendly portals reduces intermediaries, captures first-party data, and enables personalized adherence nudges that boost lifetime value. Yet B2B2C structures, expanding at a 14.41% CAGR, blend manufacturer scale with trusted retail-pharmacy footprints, permitting patient-centric outreach without forsaking legacy trade relationships. PfizerForAll, for instance, operates as a virtual clinic while routing fulfillment to networked pharmacies, balancing direct engagement with regulatory compliance.

Concurrently, traditional B2B wholesale channels digitize purchase orders and invoicing to defend share among clinics and long-term-care facilities. Hybrid models that combine bulk institutional supply with patient-level micro-fulfillment further blur boundaries. Success hinges on robust APIs that synchronize inventory, pricing, and shipment status across stakeholders, ensuring that the Pharmaceutical E-commerce Market continues integrating multiple sales paths rather than converging on a single archetype.

By Platform: Third-Party Marketplaces Face Manufacturer Competition

Third-party marketplaces captured 36.78% revenue in 2025, capitalizing on enormous traffic, embedded payment wallets, and cross-category purchase bundling. Amazon Pharmacy alone is projected to hit USD 2 billion in Rx sales for 2024, with customer interest rising sharply among Prime members. Manufacturer-owned portals, advancing at a 13.88% CAGR, increasingly position themselves as hubs for disease-specific education, telehealth access, and refill reminders—services that differentiate beyond price alone.

Distributors and wholesalers run white-label storefronts that leverage existing licensure and storage accreditations, giving smaller community pharmacies a turnkey pathway to e-commerce participation. Retail chains employ omnichannel tactics such as click-and-collect, enabling instant pickup for urgent therapies while still reaping online basket-building advantages. Competitive equilibrium will depend on who best orchestrates a full-journey offering that starts with symptom assessment and ends with long-term adherence support, reaffirming that the Pharmaceutical E-commerce Market rewards tight end-to-end integration.

Geography Analysis

North America held 39.71% of global revenue in 2025, benefiting from mature broadband penetration, widespread e-prescription mandates, and consumer familiarity with doorstep delivery. Amazon’s forthcoming 20 brick-and-mortar pharmacies and Walmart’s same-day Rx coverage across 49 states highlight how existing logistics grids translate into pharma dominance. Policy harmonization—illustrated by the DEA’s Special Registration for telehealth prescribing—further reduces friction for cross-state dispensing. Yet consolidation pressures remain: Walgreens’ pending USD 23.7 billion leveraged buy-out aims to accelerate digital rebuilding outside public market scrutiny.

Asia-Pacific is the fastest-growing territory, forecast at a 13.12% CAGR through 2031. China lifted pilot restrictions on online prescription drug sales, India expanded its Unified Payments Interface to facilitate secure health-service payments, and Japan is legalizing most OTC e-sales by 2025, establishing fertile regulatory soil. Rising middle-class income and mobile-first habits speed adoption. Health-ministry drives in Saudi Arabia and the UAE back large-scale e-health implementations, suggesting spill-over demand for e-pharmacy in neighboring Gulf Cooperation Council states.

Europe maintains steady, mid-single-digit momentum as the common logo for registered online pharmacies improves consumer confidence. National rules still diverge on cold-chain shipping and advertising, however, moderating upside. South America and parts of Africa present earlier-stage opportunities; Brazil’s e-commerce-friendly payment innovations and Nigeria’s last-mile logistics start-ups offer templates but infrastructure and regulatory gaps persist. Collectively, these trends ensure the Pharmaceutical E-commerce Market evolves at different speeds, requiring region-specific compliance and service models.

Competitive Landscape

The competitive field is moderately concentrated and intensifying as retailers, tech giants, and drugmakers invest in overlapping capabilities. Amazon wields unmatched fulfillment breadth, pressuring incumbents to adopt similar delivery guarantees or pivot toward specialty niches. CVS responded by purchasing Signify Health for USD 8 billion, stitching home-diagnostics and care navigation directly into its pharmacy and insurance ecosystem.

Strategic postures divide into three camps. Platform aggregators leverage scale to offer wide selections and low prices. Vertically integrated insurers own the care-delivery chain, using pharmacy assets as data-collection nodes to manage population health. Focused specialists like Hims & Hers target discrete conditions such as weight management, leveraging celebrity marketing and subscription refills for stickiness.

Regulatory tech adaptability is emerging as a success marker. The FDA proposal to expand National Drug Codes from 10 to 12 digits requires systemic labeling and IT revamps. Entities that upgrade early will avoid shipping disruptions and gain a reputational edge. Meanwhile, advanced serialization and blockchain pilots aim to curb counterfeit risk, offering co-branded assurance labels that may soon become de facto market entry tickets. Together these factors underscore a Pharmaceutical E-commerce Market where agility, trust, and data orchestration outweigh pure scale.

Pharmaceutical E-commerce Industry Leaders

CVS Health

DocMorris

Giant Eagle, Inc

Walgreens Boots Alliance

Amazon Pharmacy

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Walgreens Boots Alliance agreed to a USD 23.7 billion leveraged buy-out by Sycamore Partners to accelerate digital transformation outside shareholder glare.

- January 2025: The FDA finalized the ACNU Final Rule that permits tech-enabled self-selection for certain OTC medicines.

- January 2025: Walmart scaled same-day prescription delivery to 49 states, linking pharmacy refills with grocery shipments.

- December 2024: Amazon Pharmacy forecast USD 2 billion in Rx revenue for 2024, confirming rapid penetration among Prime members.

- October 2024: Amazon detailed plans to open 20 new pharmacies in 2025 to extend same-day drug delivery coverage.

- August 2024: Pfizer debuted PfizerForAll, a direct-to-consumer virtual-health platform integrating medication supply with telehealth.

Global Pharmaceutical E-commerce Market Report Scope

As per the report's scope, pharmaceutical e-commerce refers to the online buying and selling of pharmaceutical products, including prescription and over-the-counter medications, through digital platforms and websites. It enables consumers to conveniently purchase medications, access healthcare information, and receive home delivery of their orders. The Pharmaceutical E-commerce Market is segmented by type, product type, therapeutic area, market type, platform, and geography. By type, the market is segmented into prescription and over-the-counter (OTC). By product type, the market is segmented into vaccines, specialty care, general medicines, and consumer healthcare. By therapeutic area, the market is segmented into diabetes, immune-system diseases, cancer, neurodegenerative diseases, cardiovascular diseases, and other therapeutic areas. By market type, the market is segmented into B2B, B2B2B, B2B2C, and B2C. By platform, the market is segmented into manufacturer-owned digital commerce, distributor/wholesaler-owned digital commerce, manufacturer-owned marketplace, third-party marketplace, and retail. The report also covers the market sizes and forecasts for the Pharmaceutical E-commerce Market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Prescription |

| Over-The-Counter (OTC) |

| Vaccines |

| Specialty Care |

| General Medicines |

| Consumer Healthcare |

| Diabetes |

| Immune-System Diseases |

| Cancer |

| Neurodegenerative Diseases |

| Cardiovascular Diseases |

| Other Therapeutic Areas |

| B2B |

| B2B2B |

| B2B2C |

| B2C |

| Manufacturer-Owned Digital Commerce |

| Distributor/Wholesaler-Owned Digital Commerce |

| Manufacturer-Owned Marketplace |

| Third-Party Marketplace |

| Retail |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Prescription | |

| Over-The-Counter (OTC) | ||

| By Product Type | Vaccines | |

| Specialty Care | ||

| General Medicines | ||

| Consumer Healthcare | ||

| By Therapeutic Area | Diabetes | |

| Immune-System Diseases | ||

| Cancer | ||

| Neurodegenerative Diseases | ||

| Cardiovascular Diseases | ||

| Other Therapeutic Areas | ||

| By Market Type | B2B | |

| B2B2B | ||

| B2B2C | ||

| B2C | ||

| By Platform | Manufacturer-Owned Digital Commerce | |

| Distributor/Wholesaler-Owned Digital Commerce | ||

| Manufacturer-Owned Marketplace | ||

| Third-Party Marketplace | ||

| Retail | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the Pharmaceutical E-commerce Market?

The Pharmaceutical E-commerce Market size stands at USD 262.25 billion in 2026.

How fast is the Pharmaceutical E-commerce Market expected to grow?

Market revenue is projected to climb at a 11.62% CAGR, reaching USD 454.43 billion by 2031.

Which region dominates pharmaceutical e-commerce sales today?

North America leads with 39.71% revenue share, supported by robust digital infrastructure and supportive regulation.

Which segment is expanding fastest within pharmaceutical e-commerce?

Vaccines are the fastest-growing product type, expected to post a 15.32% CAGR through 2031.

How are regulations affecting cross-border pharmaceutical e-commerce?

Divergent serialization and licensing rules raise compliance costs, slowing expansion for platforms lacking deep regulatory resources.

What strategic moves are incumbents making to stay competitive?

Players like CVS are buying care-navigation firms, while manufacturers such as Pfizer are launching direct-to-consumer portals to keep control of patient data and engagement.

Page last updated on: