Goat Milk Formula Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

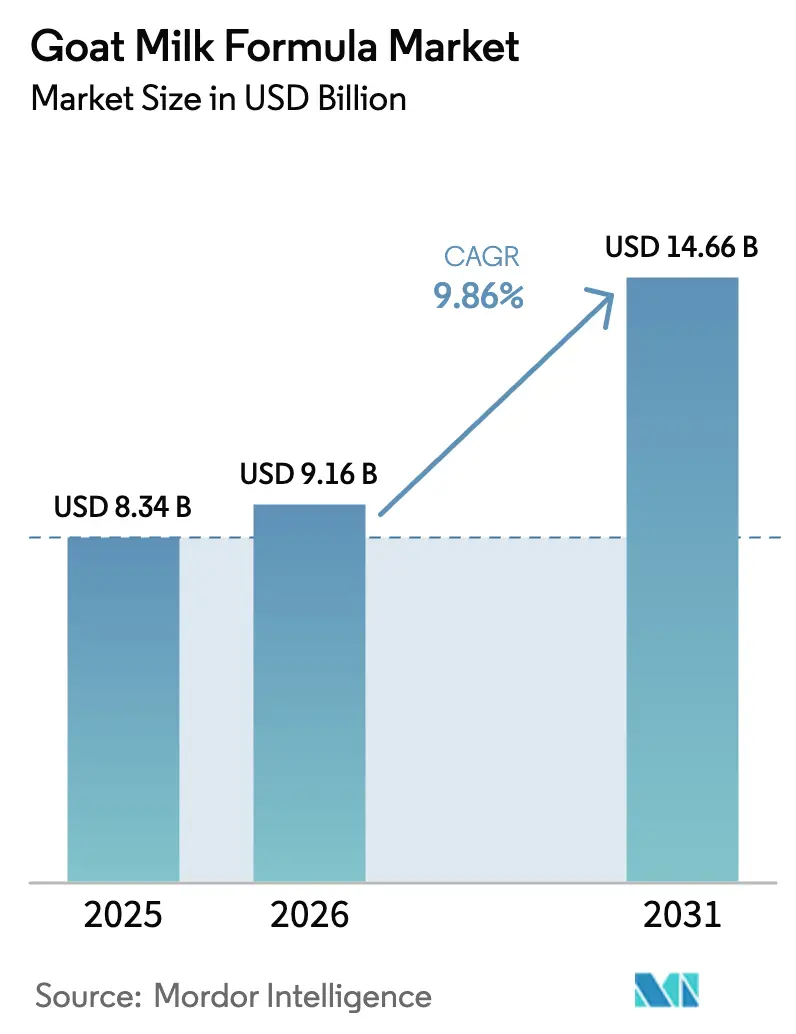

| Market Size (2026) | USD 9.16 Billion |

| Market Size (2031) | USD 14.66 Billion |

| Growth Rate (2026 - 2031) | 9.86% CAGR |

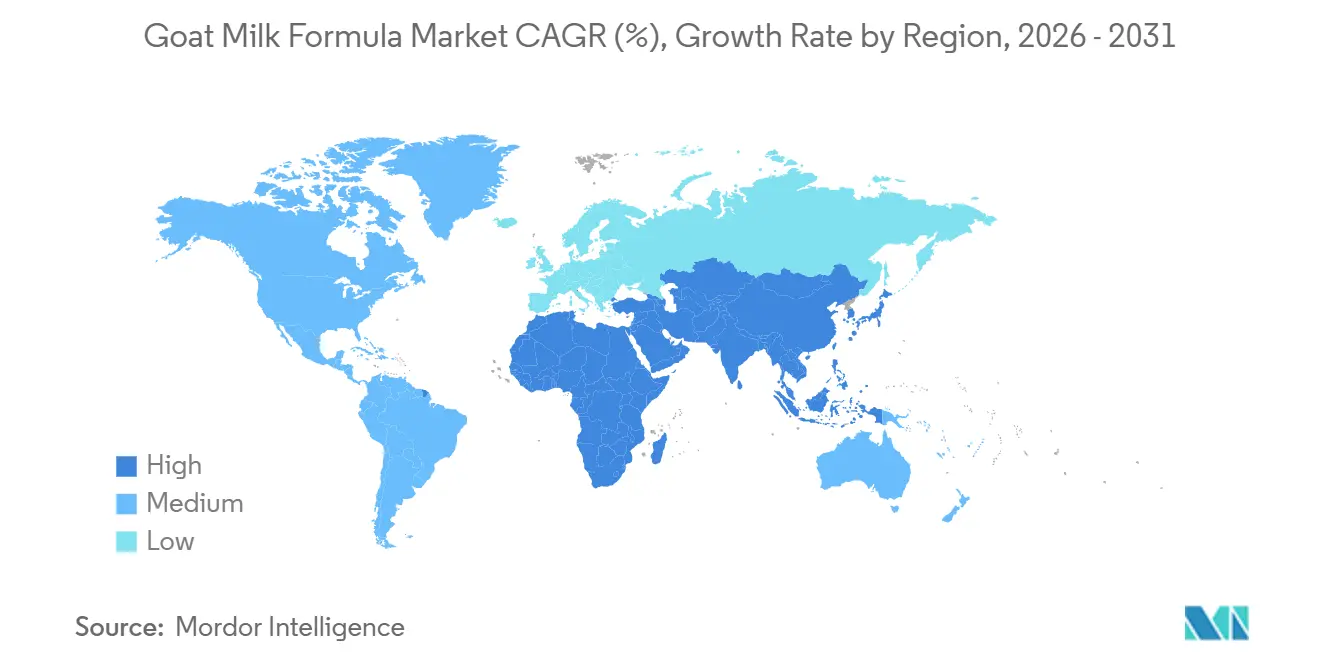

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Goat Milk Formula Market Analysis by Mordor Intelligence

The goat milk formula market size is expected to increase from USD 8.3 billion in 2025 to USD 9.16 billion in 2026 and reach USD 14.66 billion by 2031, growing at a CAGR of 9.86% over 2026-2031. This expansion is driven by improved regulatory clarity in the United States, a growing number of parents opting for hypoallergenic nutrition, and the premium positioning of specialist brands. Although Asia-Pacific remains the leading regional contributor, cross-border e-commerce is shifting sales toward North America and the Middle East. Powdered formats continue to dominate due to their compatibility with traditional dairy infrastructure, but liquid ready-to-feed variants are experiencing faster growth, particularly in affluent urban areas. Retail dynamics are also evolving, with supermarkets maintaining shelf leadership while online platforms expand rapidly, supported by cross-border regulations favoring direct-to-consumer imports.

Key Report Takeaways

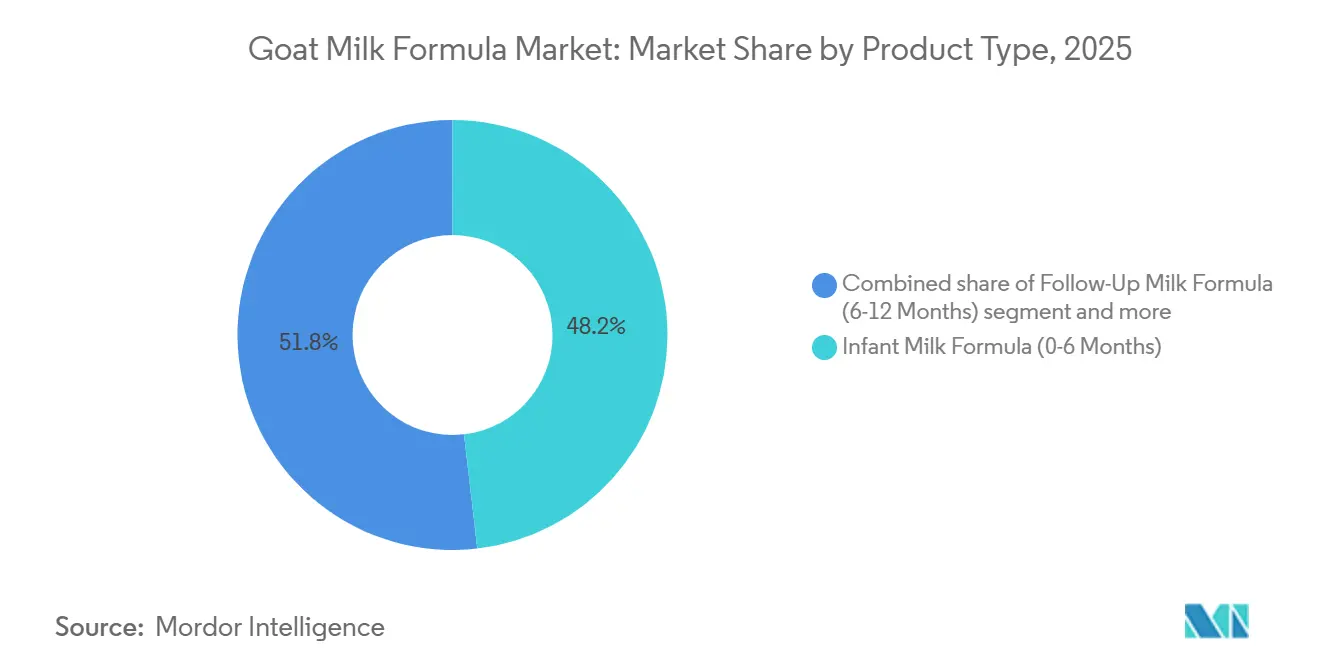

- By product type, infant milk formula commanded 48.17% of 2025 revenue, while growing-up milk formula is projected to advance at a 10.85% CAGR through 2031.

- By form, powder held 78.24% of 2025 volume and liquid ready-to-feed leads growth with an 11.36% CAGR to 2031.

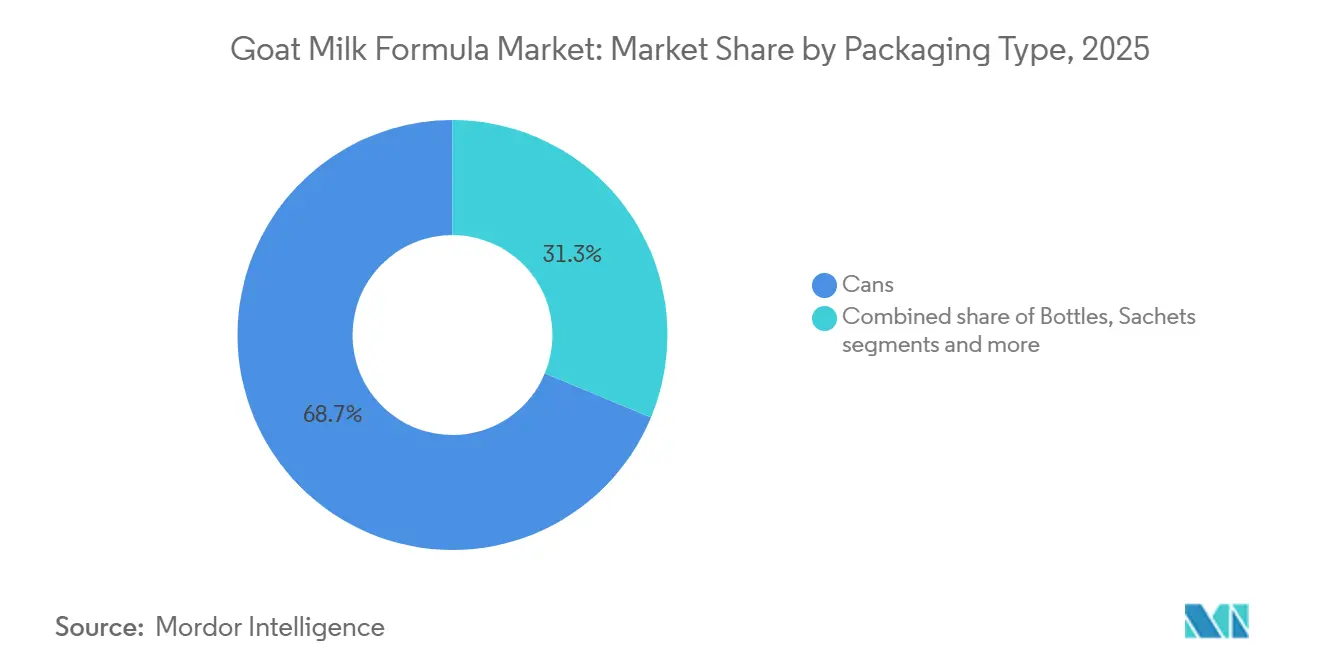

- By packaging type, cans captured 68.74% share in 2025 and sachets are forecast to expand at an 11.74% CAGR during 2026-2031.

- By distribution channel, supermarkets and hypermarkets represented 58.69% of 2025 value, whereas online retail is rising at a 12.14% CAGR through 2031.

- By geography, Asia-Pacific contributed 44.39% of 2025 revenue and the Middle East and Africa region is on track for the fastest 11.67% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Goat Milk Formula Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of cow's milk allergies and lactose intolerance | +2.1% | Global, with concentration in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| High digestibility and nutritional benefits | +1.8% | Global, particularly Asia-Pacific and Middle East markets with digestive-health awareness | Long term (≥ 4 years) |

| Growing parental awareness of hypoallergenic and natural formula benefits | +1.6% | North America, Europe, Australia, and affluent Asia-Pacific urban centers | Medium term (2-4 years) |

| Rising birth rates driving demand for goat milk formula | +0.3% | Middle East and Africa (positive); Asia-Pacific (negative due to China decline) | Long term (≥ 4 years) |

| Increasing preference for organic and clean-label products | +1.4% | Europe, North America, Australia, and premium segments in Asia-Pacific | Medium term (2-4 years) |

| Sustainability of goat farming | +0.9% | Europe (strong regulatory push), North America, and select Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of cow's milk allergies and lactose intolerance

Infants worldwide face challenges with cow's milk protein allergy. However, goat milk formula's cross-reactivity with cow milk proteins restricts its use for those with IgE-mediated allergies. This constraint limits the target population to individuals with non-IgE-mediated sensitivities and lactose intolerance. Cow’s milk allergy (CMA) is one of the most widespread food allergies among infants and young children. In Europe, its prevalence ranges from 0.36% to 4.9%, according to Clinical and Experimental Pediatrics[1]Source: Clinical and Experimental Pediatrics, "Regional differences in diagnosis and management", e-cep.org. Goat milk contains naturally lower levels of alpha-S1-casein and smaller fat globules, which promote faster gastric emptying and reduce regurgitation episodes. These advantages appeal to parents managing functional gastrointestinal disorders rather than true allergies. Supporting its role in infant nutrition, the European Food Safety Authority has confirmed that goat milk protein is an appropriate protein source for infant and follow-on formulas. This approval, based on Delegated Regulation 2016/127, has established a regulatory standard across the European Union.

High digestibility and nutritional benefits

Goat milk contains oligosaccharides at levels approximately five times higher than cow milk. This compositional advantage enhances prebiotic activity and supports a bifidogenic gut microbiota profile in formula-fed infants. The smaller fat globules and distinctive fatty acid composition, featuring higher concentrations of medium-chain triglycerides, promote more efficient lipid absorption. Manufacturers highlight this benefit, particularly in markets where digestive comfort influences purchasing decisions. These findings are especially significant in the Asia-Pacific region, where traditional beliefs about the "heating" and "cooling" properties of foods impact formula preferences. However, the nutritional narrative faces a limitation: goat milk's protein structure is highly similar to that of cow milk. This similarity reduces its effectiveness in managing confirmed cow milk protein allergies. As a result, manufacturers must carefully position their products to avoid making misleading health claims.

Growing parental awareness of hypoallergenic and natural formula benefits

Parents demonstrate strong brand loyalty, influenced by hospital recommendations and the belief that higher prices indicate superior quality. Goat milk formula brands capitalize on this perception by positioning their products at premium price points. Ausnutria's Kabrita brand gained recognition as the first goat milk infant formula to complete an FDA pre-market review, aligning with its U.S. launch in January 2024. The company highlights this regulatory approval in its marketing to support retail prices exceeding USD 40 for an 800-gram canister. Messaging emphasizing "natural" qualities and being "closer to human milk" resonates strongly, particularly in regions where clean-label trends have diminished trust in extensively hydrolyzed and amino acid-based formulas. This is significant, considering that all infant formulas, including goat milk variants, undergo substantial processing and fortification. The challenge lies in maintaining this competitive advantage as cow milk formula manufacturers introduce "gentle" and "comfort" variants that replicate goat milk's digestibility claims without facing similar supply-chain constraints.

Increasing preference for organic and clean-label products

Manufacturers encounter significant challenges in compliance due to differing organic certification requirements across jurisdictions. Holle Baby Food AG, a Swiss company with 85 years of history, obtains goat milk from Demeter-certified biodynamic farms located in Austria, Switzerland, and the Netherlands. While this supply-chain model secures retail premiums, its scalability is restricted by the limited availability of certified goat dairy operations. The European Union's organic regulation (EU 2018/848) requires pasture access and limits synthetic inputs. These regulations, which meet consumer expectations, increase production costs by an estimated 25% to 35% compared to conventional formulas. To address the affordability challenge, sachet packaging formats are gaining traction. These formats lower upfront costs and reduce waste for families concerned about infant tolerance. Although clean-label positioning aligns with sustainability claims, the environmental impact of goat milk production remains a topic of debate. Smaller ruminants produce less methane per animal, but more animals are needed to achieve the same milk output as cows, complicating life-cycle assessments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory complexities across regions | -1.2% | Global, with acute impact in China, United States, and European Union | Short term (≤ 2 years) |

| Competition from cow and plant-based formulas | -1.5% | Global, particularly North America and Europe where plant-based adoption is rising | Medium term (2-4 years) |

| Seasonality and supply chain disruptions | -0.8% | Global, with pronounced effects in regions dependent on New Zealand and European imports | Short term (≤ 2 years) |

| Higher production costs compared to cow's milk formulas | -1.1% | Global, with margin pressure most acute in price-sensitive emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory complexities across regions

China's State Administration for Market Regulation requires manufacturers to file separate applications for each formula variant. This process, which demands extensive documentation, including details on production facilities, ingredient sourcing, and clinical evidence, can take 18 to 24 months to complete. This regulatory system favors established companies with dedicated regulatory teams while creating obstacles for new entrants seeking to launch innovative formulations. In February 2025, the United States Food and Drug Administration addressed a decade-long uncertainty by issuing "no questions" letters for three goat milk GRAS notices (GRN 1211, 1212, 1213). Despite this, manufacturers must still adhere to the Infant Formula Act's nutrient specifications and Current Good Manufacturing Practice regulations, which require facility registration and biannual inspections. Additionally, brands operating in multiple markets face increased landed costs and inventory challenges due to varying labeling requirements. For example, China mandates that Chinese-language labels be printed at the source factory rather than applied after importation.

Competition from cow and plant-based formulas

In January 2025, the U.S. Government Accountability Office revealed that over half of all infant formula sales in the U.S. occur through the Special Supplemental Nutrition Program for Women, Infants, and Children (WIC). This program primarily awards contracts to cow milk formula manufacturers, creating obstacles for the adoption of goat milk formulas. Winning a WIC contract resulted in a 1.7% increase in retail prices for non-WIC consumers, equating to an additional USD 0.30 for a 12-ounce container. Manufacturers raised prices to recover rebate costs, which puts premium-priced goat formulas, excluded from WIC offerings, at a disadvantage. While the European Union limits plant-based formulas to soy isolate and hydrolyzed rice protein, Australia and New Zealand approved pea-rice blends in 2024. Additionally, the International Life Sciences Institute Europe organized a workshop in November 2024 to assess the safety of new plant proteins. These plant-based options appeal to parents concerned about environmental and animal welfare issues, a group that significantly overlaps with the clean-label audience targeted by goat milk formulas. The U.K. Competition and Markets Authority reported that three major manufacturers dominate the infant formula market. This dominance allows cow milk producers to secure favorable retailer shelf space and hospital contracts, forcing goat milk brands to rely on online platforms and specialty retailers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Infant Formula Anchors Revenue, Toddler Segment Accelerates

In 2025, infant milk formula for ages 0-6 months accounted for 48.17% of total revenue. This dominance stems from hospital discharge practices that foster brand loyalty during the crucial neonatal phase, a time when parents are particularly receptive to healthcare provider recommendations. Bubs Australia, in June 2025, submitted a New Infant Formula Submission (NIFS) to the FDA. This move, bolstered by a clinical trial involving 478 infants, underscores the strategic emphasis brands place on obtaining regulatory credentials to influence hospital formulary committees. Meanwhile, the follow-up milk formula for ages 6-12 months acts as a retention tool, enhancing customer lifetime value as infants move to complementary feeding. However, this segment grapples with margin pressures due to competition from retailers' private-label offerings.

Projected to grow at a 10.85% CAGR through 2031, the growing-up milk formula for children over 12 months is witnessing a surge. This growth is fueled by manufacturers' initiatives to market toddler nutrition as a unique category, necessitating specialized formulations, rather than merely an extension of infant feeding. Unlike their 0-12 month counterparts, toddler formulas enjoy a more relaxed regulatory landscape in many regions. This leniency allows brands to stand out with added probiotics, DHA, and claims of boosting immunity. However, a significant hurdle emerges: pediatric guidelines in North America and Europe don't deem toddler formulas as essential nutrition. This oversight exposes the segment to potential regulatory clampdowns, akin to the U.K. Competition and Markets Authority's February 2025 move to broaden advertising restrictions beyond just 6-month formulas.

By Form: Powder Dominates, Liquid Gains in Urban Markets

In 2025, powdered goat milk formula led the market, accounting for 78.24% of the volume share. This dominance is attributed to its cost efficiency, longer shelf life, and compatibility with manufacturing infrastructures originally designed for cow milk production. However, the reconstitution process, mixing the powder with water in precise ratios, can result in preparation errors, causing over- or under-concentration. To address this, regulatory agencies enforce scoop calibration and include water-temperature instructions on labels. Meanwhile, liquid ready-to-feed variants are experiencing significant growth, with an 11.36% CAGR projected through 2031. This growth is driven by urban dual-income households willing to pay a premium for the convenience and reduced contamination risk offered by liquid formats. Nannycare, a U.K.-based brand sourcing goat milk from New Zealand, provides both powder and liquid formats. The liquid variant is particularly targeted for hospital use and travel scenarios where access to clean water or sterilization equipment is limited.

However, the growth of the liquid segment relies heavily on the development of cold-chain logistics, which remain inadequate in many emerging markets. In China, cross-border e-commerce regulations favor shelf-stable powder formats that can endure the 14- to 21-day transit times from Australia and New Zealand. In contrast, liquid formulas require refrigerated shipping and storage, a cost-intensive process that limits their availability to tier-1 cities with advanced retail infrastructures. A January 2025 report from the United States Government Accountability Office revealed that liquid formulas make up a small portion of WIC-contracted products due to their higher per-ounce costs. This cost dynamic reinforces the dominance of powdered formats in the price-sensitive segments served by WIC. To overcome these challenges, manufacturers are exploring ultra-high-temperature (UHT) processing and aseptic packaging. These advancements aim to extend the shelf life of liquid formulas to 12 months without refrigeration, potentially enabling distribution in markets currently constrained by cold-chain limitations.

By Packaging Type: Cans Lead, Sachets Disrupt Affordability Barriers

In 2025, metal cans accounted for 68.74% of the packaging market share due to their excellent oxygen and moisture barrier properties. These attributes are crucial for preserving the oxidation-sensitive lipids and vitamins in goat milk formula. Additionally, the canister format serves as an effective marketing tool. Larger pack sizes, typically between 800 and 900 grams, secure prominent shelf placement and support premium pricing through perceived value, even though their per-gram costs are higher than smaller formats. Holle Baby Food AG's use of recyclable steel cans complies with European Union circular-economy directives but highlights challenges in end-of-life recycling. These challenges stem from the energy-intensive steel production process and the difficulty of separating multi-material lids. Bottles, mainly used for liquid ready-to-feed formats, cater to on-the-go consumption and are particularly popular in hospital settings, where the convenience of single-serve options outweighs cost concerns.

Sachets are experiencing significant growth, with an 11.74% CAGR projected through 2031. Their popularity is driven by their ability to reduce upfront purchase costs and minimize waste for families uncertain about their infant's tolerance to goat milk formula. In emerging markets, single-serve sachets address a key issue: humidity can spoil opened powder cans within days, discouraging bulk purchases. However, sachet packaging has its limitations. It generates higher per-unit material waste and presents recycling challenges due to its multi-layer laminate structures, which current municipal systems cannot separate. Regulatory acceptance of sachets varies across regions. For example, China's packaging standards for infant formula emphasize tamper-evidence and traceability, which sachet formats can meet using QR codes and serialized batch numbers. Conversely, some European markets restrict single-use plastics under extended producer responsibility schemes.

By Distribution Channel: Supermarkets Hold Ground, Online Retail Surges

In 2025, supermarkets and hypermarkets maintained their position as the leading sales channel, contributing 58.69% of total sales. This dominance is attributed to the trust consumers place in physical retail environments, where parents can physically examine and compare products side-by-side before making a purchase decision. These retail formats provide a sense of reliability and transparency, which are critical factors for consumers, particularly when purchasing essential products. In contrast, convenience stores play a supplementary role in the market. They primarily cater to impulse purchases and emergency top-ups, offering quick access to products. However, their limited product assortment and lack of variety restrict their ability to support brand discovery and broader consumer engagement.

Online retail channels are expected to grow at a strong 12.14% CAGR through 2031, driven by China's cross-border e-commerce policies. These policies allow consumers to purchase imported formulas directly from overseas warehouses without needing domestic product registration. This shift in consumer behavior challenges traditional distributor networks and pharmacy chains, which have historically controlled formula access through pharmacist consultations and loyalty programs. Furthermore, increasing internet penetration supports the growth of online sales. By 2025, the International Telecommunication Union (ITU) reported that approximately 6 billion people, or about three-quarters of the global population, were internet users[2]Source: International Telecommunication Union (ITU), "ITU's Facts and Figures 2025", itu.int. However, a January 2025 report from the U.S. Government Accountability Office highlighted a significant constraint. It stated that WIC's single-supplier contracts, which account for over half of U.S. formula purchases, are primarily executed through brick-and-mortar retailers. This reliance imposes a structural limitation on online penetration within the WIC-eligible population.

Geography Analysis

In 2025, Asia-Pacific accounted for 44.39% of the revenue. However, the region's growth story is divided: while China faces a demographic decline, Southeast Asia is experiencing the rise of a growing middle class. Urban parents in China, despite having fewer children, are increasingly focusing on infant nutrition, a trend referred to as premiumization. This is exemplified by Bubs Australia's significant 20% share in China's cross-border e-commerce goat formula market. Online platforms allow brands to bypass traditional distributors and pharmacy gatekeepers, creating a structural shift that favors agile specialists over established multinationals. Japan and South Korea face similar demographic challenges but demonstrate higher per-capita spending on formulas. Conversely, in emerging markets like India and Indonesia, goat milk formula primarily caters to expatriates and affluent consumers due to affordability constraints.

North America and Europe together contributed approximately 35% of the 2025 revenue, with growth driven more by regulatory progress and clean-label trends than by demographic changes. A key development was the U.S. FDA's issuance of "no questions" letters in February 2025 for three goat milk GRAS notices (GRN 1211, 1212, 1213). This critical step removed the final regulatory hurdle for commercialization, enabling Ausnutria's Kabrita to become the first goat milk infant formula to complete the FDA's pre-market review, ahead of its January 2024 launch. Countries such as Germany, France, and the Netherlands, with well-established goat dairy industries, supply raw milk to regional processors. For instance, Holle Baby Food AG sources ingredients from Demeter-certified biodynamic farms located in Austria, Switzerland, and the Netherlands. According to the European Commission, Spain produced 1.1 million tonnes of milk from ewes and goats in 2024, followed by Greece with 0.9 million tonnes and France with 0.8 million tonnes[3]Source: European Commission, "Milk and milk product statistics", ec-europa.eu. However, the European Union's Delegated Regulation 2016/127 enforces strict compositional standards and limits health claims, preventing manufacturers from marketing goat milk formula as hypoallergenic without robust clinical evidence.

The Middle East and Africa are projected to grow at the fastest rate, with a CAGR of 11.67% through 2031. This growth is driven by expatriate populations in Gulf Cooperation Council states, government-supported nutrition programs in Egypt and Morocco, and increasing disposable incomes in urban areas. The UAE and Saudi Arabia show high per-capita formula consumption due to large expatriate communities familiar with goat milk products from their home countries and local populations with higher rates of lactose intolerance. Egypt's government has prioritized infant nutrition as part of broader public health initiatives, driving demand for alternatives that are affordable yet positioned as premium compared to standard cow milk formulas. South Africa's retail infrastructure facilitates the distribution of imported goat milk formulas, though affordability remains a challenge outside metropolitan areas. Despite the region's strong growth potential, regulatory fragmentation poses a significant obstacle. Each country has distinct import and labeling requirements, forcing manufacturers to navigate a complex compliance landscape, which increases both time-to-market and administrative costs.

Competitive Landscape

The goat milk formula market maintains a moderate concentration level, with established players holding competitive advantages through regulatory expertise and robust distribution networks. Market leaders like Ausnutria Dairy Corporation Ltd, Dana Dairy Group, Dairy Goat Co-operative (NZ) Ltd, Kendal Nutricare Ltd, and The Little Oak Company implement vertical integration strategies across the value chain. Specialist producers continue to dominate the goat milk formula market, even as multinational dairy groups show increasing interest in this niche segment. In the first half of 2025, Ausnutria’s Kabrita demonstrated its first-mover advantage and effective e-commerce execution by capturing a significant share of China’s goat milk formula market, including the imported segment. This success highlights the importance of strategic positioning and robust online sales channels in driving market penetration.

In contrast, the broader UK infant formula market is largely controlled by three major conglomerates, Danone SA, Kendal Nutricare, and Nestlé. However, the goat milk formula segment within this market remains fragmented, providing niche brands with the opportunity to maintain pricing power. Holle differentiates itself through its Demeter biodynamic certification, which appeals to environmentally conscious consumers. However, the limited availability of certified milk constrains the company’s production volumes, posing a challenge to scaling operations.

Strategic priorities in the goat milk formula market are increasingly centered on advancing traceability technologies, such as blockchain-based batch tracking, and generating robust clinical data to support product claims. Additionally, precision fermentation startups exploring the production of human lactoferrin represent a potential disruptive force in the industry. However, these innovations face significant hurdles due to underdeveloped regulatory pathways. Consolidation within the sector may accelerate as multinational dairy firms recognize that achieving economies of scale could help mitigate the challenges posed by raw-material seasonality and regulatory compliance costs in the goat milk formula industry.

Goat Milk Formula Industry Leaders

-

Ausnutria Dairy Corporation Ltd

-

Dana Dairy Group

-

Dairy Goat Co-operative (NZ) Ltd

-

Kendal Nutricare Ltd

-

The Little Oak Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Goat milk formula brand, The Little Oak Company, has launched a new facility in Perth, Western Australia. The facility's strategic location reduces transportation distances, lowering emissions and supporting the company's sustainability initiatives.

- February 2025: Kabrita has introduced a goat milk-based infant formula in Canada. As per Kabrita's report, the new formula is crafted from grass-fed goat milk and is enriched with 25 essential vitamins and minerals, such as DHA, ARA, and prebiotics.

- February 2024: Danalac Goat launched its official online store shop.danalac.com, offering European-approved goat milk formula directly to consumers. The store provides a comprehensive range of goat milk formulas.

- January 2024: Kabrita USA introduced a goat-milk infant formula after completing extensive safety evaluations to establish its whey protein concentrate and non-fat dry goat milk as generally recognized as safe (GRAS) for infants.

Global Goat Milk Formula Market Report Scope

Goat milk formula is manufactured to meet the same nutritional standards as cow's milk-based formula, using goat milk as the primary ingredient. The goat milk formula market is segmented by product type, form, packaging type, distribution channel, and geography. By product type, the market is segmented into infant milk formula 0-6 months, follow-up milk formula 6-12 months, and growing-up milk formula 12+ months. By form, the market is segmented into powdered and liquid. By packaging type, the market is segmented into cans, bottles, sachets, and others. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, online retail stores, and other distribution channels. By Geography, the market is segmented into North America, South America, Europe, Asia-Pacific, and Middle East and Africa. For each segment, the market sizing and forecasts were made based on value (USD) and volume (Tons).

| Infant Milk Formula (0-6 Months) |

| Follow-Up Milk Formula (6-12 Months) |

| Growing-Up Milk Formula (12+ Months) |

| Powdered |

| Liquid |

| Cans |

| Bottles |

| Sachets |

| Others |

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Infant Milk Formula (0-6 Months) | |

| Follow-Up Milk Formula (6-12 Months) | ||

| Growing-Up Milk Formula (12+ Months) | ||

| By Form | Powdered | |

| Liquid | ||

| By Packaging Type | Cans | |

| Bottles | ||

| Sachets | ||

| Others | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is revenue growing for goat milk formula between 2026 and 2031?

The category is set to expand at a 9.86% CAGR over 2026-2031, lifting value from USD 9.16 billion to USD 14.66 billion.

Which region is poised to record the quickest growth through 2031?

The Middle East and Africa region is projected to log an 11.67% CAGR, the highest of any geography.

What share did powdered formats hold in 2025?

Powder accounted for 78.24% of global volume, cementing its role as the primary format.

What drives the surge in online sales?

Cross-border e-commerce rules that favor direct import, combined with subscription convenience, are propelling a 12.14% CAGR in online channels.

Page last updated on: