Qatar Dairy Products Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

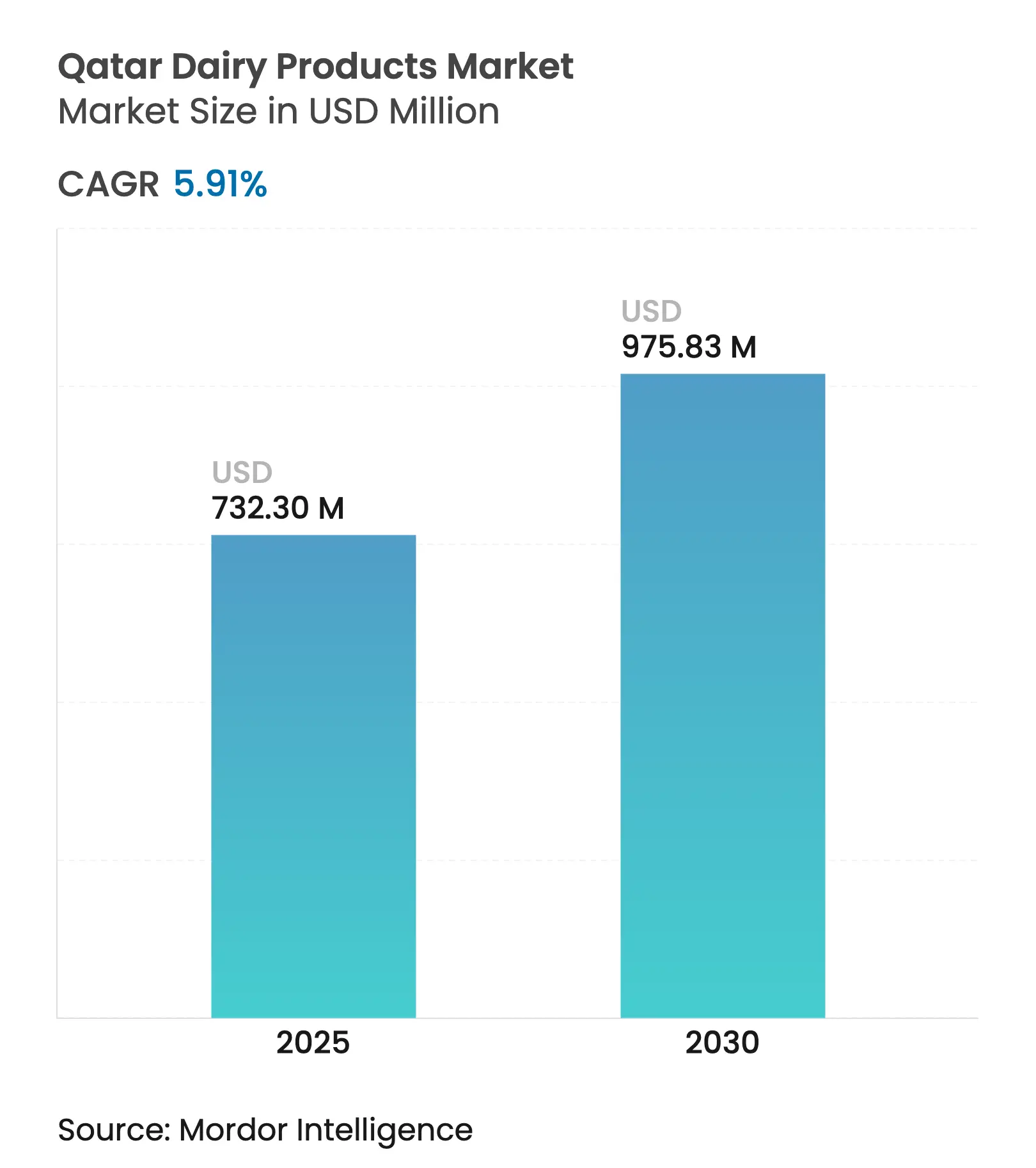

| Market Size (2025) | USD 732.30 Million |

| Market Size (2030) | USD 975.83 Million |

| Growth Rate (2025 - 2030) | 5.91 % CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Qatar Dairy Products Market Analysis by Mordor Intelligence

The Qatar dairy products market size reached USD 732.30 million in 2025 and is expected to grow to USD 975.83 million by 2030, at a CAGR of 5.91%. The market growth is supported by demographic shifts, government policies, and changing consumer preferences. Qatar's growing population, with a high proportion of expatriates, continues to drive increased per-capita dairy consumption and demand for diverse dairy products. The government's focus on domestic dairy production and self-sufficiency has helped Qatar develop into a regional dairy production center, with investments in farming technology, processing facilities, and supply chain infrastructure. The market shows increasing demand for premium, organic, and functional dairy products, reflecting the preferences of Qatar's affluent and health-conscious consumers. The adoption of climate control systems, automated milking, and precision farming technologies improves operational efficiency in Qatar's challenging climate. The regulatory environment maintains product quality and safety standards, benefiting companies that implement strict quality control measures.

Key Report Takeaways

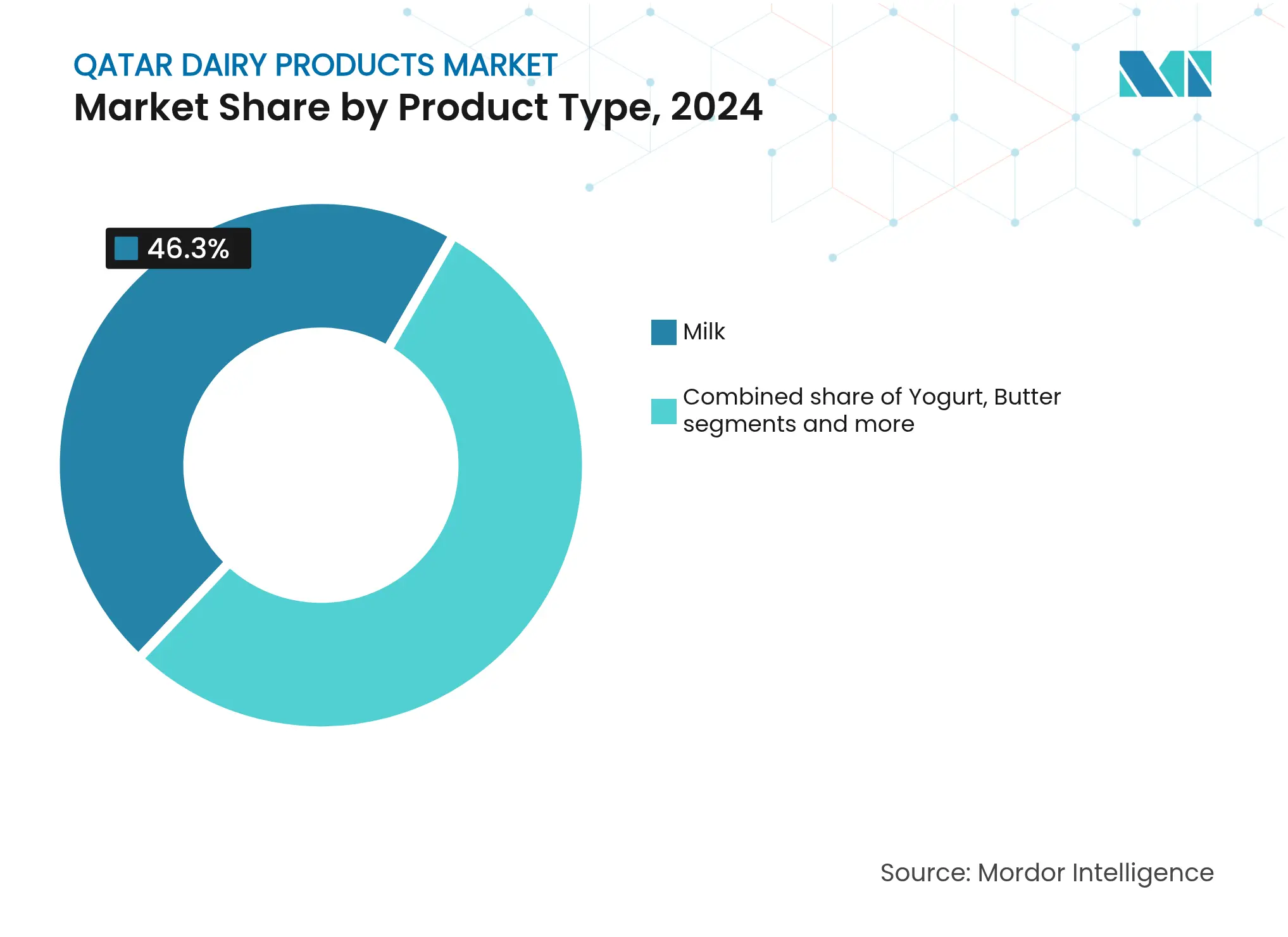

- By product category, milk led with 46.30% of Qatar dairy products market share in 2024, while yogurt is forecast to post the highest growth at a 6.93% CAGR through 2030.

- By source, cow milk dominated at 81.21% of Qatar dairy products market size in 2024, whereas camel milk is projected to advance at an 8.82% CAGR over 2025–2030.

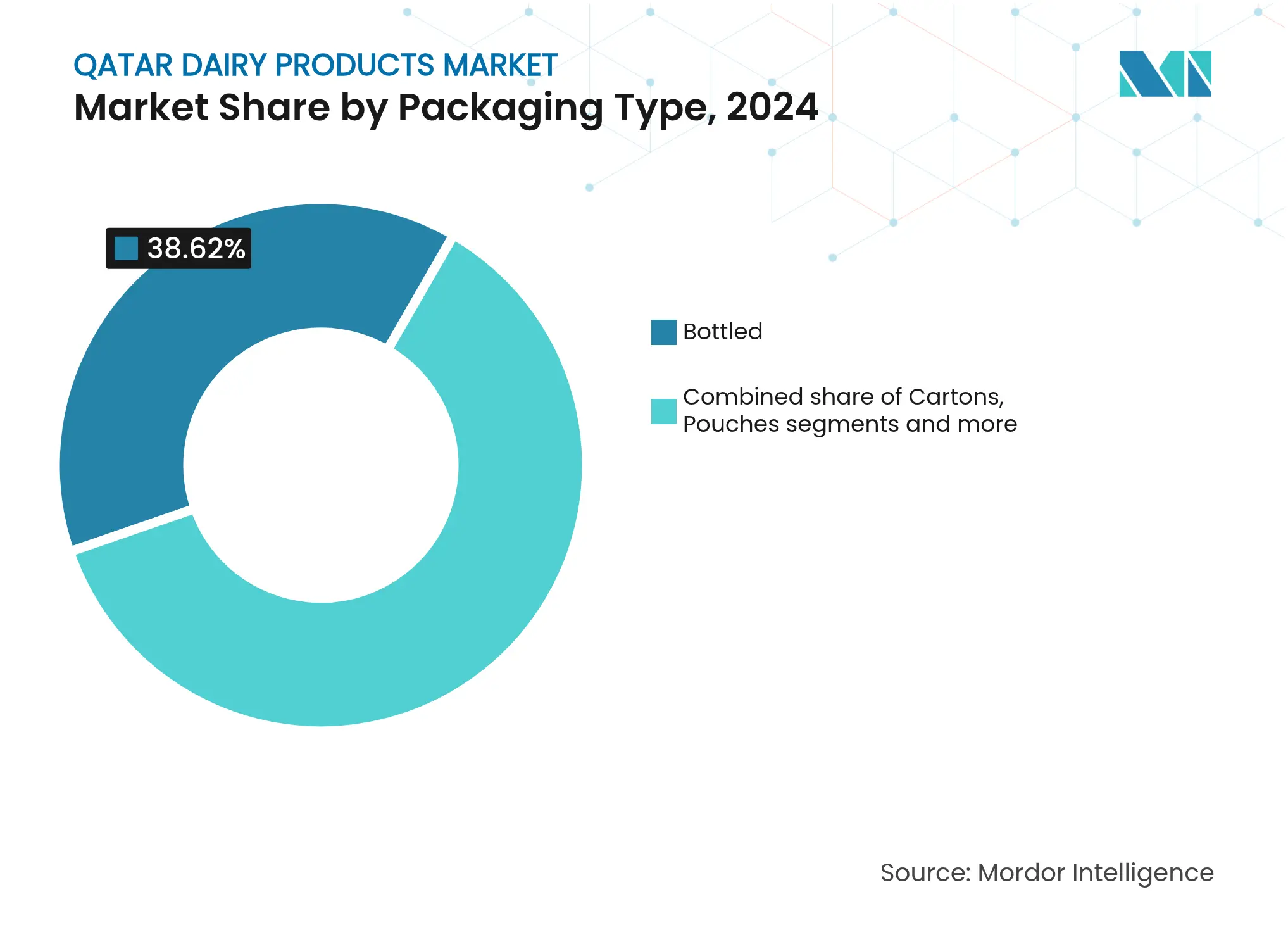

- By packaging type, bottled formats captured 38.62% share in 2024, and tubs & cups are expected to register the fastest expansion at a 7.53% CAGR through 2030.

- By distribution channel, off-trade outlets accounted for 76.28% of Qatar dairy products market share in 2024, while on-trade sales are set to grow at an 8.01% CAGR to 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Qatar Dairy Products Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising per-capita dairy consumption driven by population growth & expat demographics Rising per-capita dairy consumption driven by population growth & expat demographics | +1.7% | National, concentrated in Doha metropolitan area | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+1.7% | Geographic Relevance:National, concentrated in Doha metropolitan area | Impact Timeline:Medium term (2-4 years) |

Health Consciousness & Demand for Nutrition-Rich Options Health Consciousness & Demand for Nutrition-Rich Options | +1.6% | National, with premium segments in urban centers | Long term (≥ 4 years) | |||

Increasing Availability of Organic Dairy Products Increasing Availability of Organic Dairy Products | +0.8% | Qatar-wide, early adoption in Doha and Al Rayyan | Medium term (2-4 years) | |||

Government initiatives for domestic dairy self-sufficiency Government initiatives for domestic dairy self-sufficiency | +1.4% | National, with major production facilities expansion | Long term (≥ 4 years) | |||

Product Innovation & Diversification support the market growth Product Innovation & Diversification support the market growth | +1.0% | Qatar-wide, concentrated in premium retail segments | Medium term (2-4 years) | |||

Adoption of Advanced Dairy Farming Technologies Adoption of Advanced Dairy Farming Technologies | +0.7% | National, focused on major production facilities | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Rising Per-Capita Dairy Consumption Driven by Population Growth and Expat Demographics

Qatar's increasing per-capita dairy consumption is primarily driven by significant population growth and diverse expatriate demographics. According to the Ministry of Foreign Affairs, Qatar's population reached approximately 3.1 million in 2024, showing substantial growth due to economic opportunities and infrastructure development that attract expatriates [1]Source: Ministry of Foreign Affairs, "Key Facts and Information", https://mofa.gov.qa. The expatriate community, which forms the majority of the population, brings varied dietary preferences that increase the demand for diverse dairy products. The combination of population growth, high internet penetration, and urbanization creates a modern retail environment that improves access to dairy products, contributing to higher per-capita consumption. The expanding population, particularly working-age expatriates, directly influences increased consumption of fresh milk, yogurt, cheese, and value-added dairy products. A young and diverse consumer base that embraces both traditional and new dairy products further supports market growth.

Health Consciousness and Demand for Nutrition-Rich Options

Qatar's high-income demographic exhibits pronounced health consciousness, which generates substantial demand for functional and premium dairy products with enhanced nutritional properties. The affluent consumer base demonstrates a clear preference for health benefits over cost considerations, establishing a robust market for probiotic yogurts, organic milk, and specialized dairy formulations. Government-initiated health programs systematically increase public awareness regarding nutrition's fundamental role in preventing lifestyle diseases prevalent in Gulf nations. Camel milk products demonstrate increasing market penetration due to their distinct nutritional composition, specifically elevated vitamin C content and documented anti-inflammatory properties, attracting consumers seeking evidence-based traditional health solutions. These established consumer preferences facilitate premium pricing structures and stimulate product innovation within Qatar's dairy market.

Government Initiatives for Domestic Dairy Self-Sufficiency

Government initiatives for domestic dairy self-sufficiency drive the Qatar Dairy Products Market. Qatar has invested in developing its local dairy industry to reduce import dependence and ensure a stable supply of fresh dairy products. These initiatives include expanding dairy farming infrastructure, implementing climate-controlled barns and automated milking systems, and establishing new enterprises. The government focuses on strengthening supply chains, promoting research in dairy production, and encouraging private sector participation to increase domestic capacity. The State of Qatar's National Food Security Strategy 2030, launched in December 2024, demonstrates these efforts. This strategy aims to strengthen the nation's food security by prioritizing self-sufficiency in key sectors, including dairy. It outlines specific targets to increase local production capacity, improve resource management, and enhance innovation to meet growing demand driven by population growth and evolving consumer preferences.

Adoption of Advanced Dairy Farming Technologies

The dairy farming sector in Qatar necessitates technological implementation to enhance operational efficiency and product quality standards. Baladna's operational facilities incorporate comprehensive cooling systems, automated milking infrastructure, and precision-based nutrition management systems to sustain production levels. The implementation of IoT sensor networks and data analytics systems facilitates the systematic monitoring of animal health parameters, environmental conditions, and production metrics, thereby optimizing operational efficiency while ensuring adherence to animal welfare protocols. The integration of systematic feed management protocols enables consistent production quality that aligns with international standards. The technological infrastructure in processing and packaging operations ensures product safety and longevity. These technological investments establish significant market entry barriers while positioning Qatar as a significant participant in contemporary dairy farming operations within the regional market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Limited Agricultural Land and Harsh Climate Limited Agricultural Land and Harsh Climate | -1.0% | National, affecting all production facilities | Long term (≥ 4 years) | (~) % Impact on CAGR Forecast:-1.0% | Geographic Relevance:National, affecting all production facilities | Impact Timeline:Long term (≥ 4 years) |

High Operational Costs and Resource Scarcity High Operational Costs and Resource Scarcity | -0.9% | Qatar-wide, concentrated in production operations | Medium term (2-4 years) | |||

Stringent Regulatory & Quality Standards Stringent Regulatory & Quality Standards | -0.6% | National, affecting all market participants | Medium term (2-4 years) | |||

Consumer concerns over carbon footprint of desert dairy farming Consumer concerns over carbon footprint of desert dairy farming | -0.5% | Qatar-wide, concentrated in premium segments | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Limited Agricultural Land and Harsh Climate

Geographic constraints significantly impede Qatar's dairy farming expansion capabilities. The nation's limited territorial expanse of 11,586 square kilometers substantially restricts large-scale dairy operations, necessitating the implementation of intensive production methodologies and advanced technological systems to maintain production volumes. The critical issue of water scarcity compels Qatar to rely extensively on desalination processes for agricultural requirements, resulting in elevated operational costs and environmental implications. The region's arid climate conditions mandate the utilization of energy-intensive cooling infrastructure and climate-controlled facilities, substantially increasing operational expenditure compared to temperate regions. These geographical limitations necessitate the importation of essential components, including feed materials and breeding stock, thereby establishing supply chain dependencies and price volatility that impact operational viability.

High Operational Costs and Resource Scarcity

Resource limitations in Qatar generate operational expenditures substantially exceeding global benchmarks, impacting profit margins and market accessibility throughout dairy operations. Energy expenditures for climate control infrastructure represent a significant cost element, particularly during summer periods when cooling requirements intensify for livestock maintenance and product preservation. The nation's reliance on imported agricultural inputs, including forages, grains, and nutritional supplements, incorporates transportation expenses and foreign exchange fluctuation risks into operational costs. Qatar's elevated wage structure further augments expenses, specifically for specialized agricultural personnel essential in contemporary dairy facilities. This financial framework advantages large-scale operations through operational efficiencies while establishing significant barriers to entry for small-scale producers and new market entrants.

Segment Analysis

By Product Type: Milk Dominance Drives Market Foundation

Milk dominates the Qatar Dairy Products Market with a 46.30% market share in 2024, supported by government initiatives and the country's focus on food security. Local producers, particularly Baladna, have established dairy farming and processing facilities that now fulfill over 95% of Qatar's fresh milk demand, reducing import reliance. Consumer health awareness has increased demand for organic, fortified, and lactose-free milk varieties, while modern production technologies have improved product quality and shelf life through methods like UHT processing.

Yogurt represents the market's fastest-growing segment, projected to grow at a CAGR of 6.93% through 2030. This growth stems from increased consumer demand for health-focused products, including probiotic-rich, organic, and additive-free options. The segment's expansion includes new product developments such as Greek-style yogurts and diverse flavor offerings. Consumer preference for local and sustainable dairy products has strengthened, while artisanal and specialty yogurt products have gained popularity through modern retail and e-commerce channels. In 2023, Baladna expanded its product range by introducing Greek yogurt variants, shredded Kashkaval cheese, and long-life juices in mango nectar and cocktail flavors.

Note: Segment shares of all individual segments available upon report purchase

By Source: Cow Milk Leadership with Camel Innovation Potential

Cow milk constitutes 81.21% of Qatar's dairy products market in 2024. This market leadership is attributed to established supply chain infrastructure, sustained consumer preference, and comprehensive applications across fluid milk, cheese, butter, and yogurt products. Governmental initiatives supporting local dairy farming operations, implementation of advanced production technologies, and optimized processing capabilities reinforce cow milk's market position. The product's established consumer acceptance, nutritional composition, and extensive dairy applications maintain its fundamental role in Qatar's dairy market.

Camel milk demonstrates substantial growth potential with a projected CAGR of 8.82% through 2030. This expansion is attributed to heightened recognition of its nutritional properties, including superior vitamin and mineral composition, and reduced allergenicity compared to cow milk. Regional preferences and Gulf cultural heritage influence consumer demand for camel milk. According to official data from the Livestock Affairs Department at the Ministry of Municipality, the camel population reached 94,299 in 2024, representing 8% of livestock, indicating substantial investment in camel farming as a sustainable dairy source [2]Source: Ministry of Municipality, "Qatar’s livestock sector sees strong growth in 2024", https://www.mme.gov.qa/.

By Packaging Type: Sustainability Drives Innovation

Bottled packaging constitutes 38.62% of the market share in 2024, reflecting Qatar's sophisticated retail environment's preference for premium presentation and product visibility. This packaging format facilitates premium pricing strategies and corresponds with Qatar's quality-oriented market dynamics, compensating for elevated production costs. The tubs and cups packaging segment demonstrates significant market expansion at 7.53% CAGR through 2030, attributed to the growth in yogurt product categories and increasing consumer requirements for portion-controlled products.

Carton packaging retains its market presence in long-life products and bulk segments, while pouch packaging serves value-oriented consumers and institutional purchasers. The evolution of packaging formats corresponds with Qatar's National Vision 2030, which emphasizes environmental sustainability and circular economy implementation. Advanced packaging technologies facilitate extended product preservation and enhanced protection in Qatar's high-temperature climate conditions, optimizing distribution efficiency and minimizing food waste. Organizations investing in environmentally sustainable packaging solutions and innovative designs effectively address consumer convenience requirements while maintaining environmental considerations.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: Retail Dominance with Hospitality Recovery

Off-trade channels account for 76.28% market share in Qatar's dairy products sector in 2024, driven by the country's robust retail infrastructure and changing consumer preferences. Modern retail formats, including hypermarkets and supermarkets, lead this distribution landscape through a combination of international retailers and established local chains serving Qatar's diverse consumer population. The growth of online retail channels has transformed the off-trade segment. Qatar's digital infrastructure, with 2.68 million internet users and a 99% internet penetration rate at the beginning of 2023, according to the International Trade Administration, supports the expansion of e-commerce platforms and delivery services [3]Source: International Trade Administration (ITA), "Qatar Country Commercial Guide", https://www.trade.gov. This digital accessibility allows consumers to purchase various dairy products, from basic items to premium offerings, through online platforms with home delivery options.

The on-trade segment, while representing a smaller share, is projected to grow at a CAGR of 8.01% through 2030, driven by Qatar's expanding hospitality and foodservice industries. The country's position as a destination for international events, including sports tournaments and conferences, increases dairy product demand across restaurants, cafes, hotels, and catering services. This growth has prompted suppliers to develop specialized product lines with bulk packaging options and premium ingredients for foodservice customers. The continuous development of hospitality infrastructure and event-hosting capabilities further supports the expansion of the on-trade segment.

Geography Analysis

Qatar's compact geography creates concentrated market dynamics, with the Doha metropolitan area accounting for the majority of dairy consumption. As the country's economic and population center, Doha houses approximately 82% of Qatar's population, enabling efficient distribution and market penetration according to the World Population Review. Northern regions, including Al Rayyan and Al Khor, benefit from proximity to major dairy production facilities, while southern areas serve industrial and tourism-related demand. Qatar's location in the Arabian Gulf facilitates trade connections with regional markets, supporting dairy product imports and exports.

Qatar's infrastructure, including cold chain facilities, ports, and transportation networks, ensures efficient dairy product distribution and quality maintenance. The country's position as a regional business hub attracts international dairy companies seeking access to Middle East markets. Government investments in logistics infrastructure and free trade zones support both international trade and domestic production. The concentration of economic activity generates distribution and marketing efficiencies while enabling effective regulatory oversight and quality control.

Qatar's economic diversification initiatives create opportunities for dairy market growth through tourism, manufacturing, and services sector development. Development projects and international events generate temporary demand increases while providing long-term infrastructure benefits for the dairy sector. The country's trade agreements and diplomatic relationships strengthen import capabilities and support export opportunities for domestic producers. Qatar's political stability and economic fundamentals provide favorable conditions for dairy industry investment and expansion.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Competitive Landscape

Market Concentration

Qatar's dairy products market operates with moderate concentration, positioning itself as a regional dairy hub. While international companies like Danone, Nestlé, and Alra Foods maintain significant market presence through established distribution networks and diverse product portfolios, local producers hold the competitive advantage, particularly in fresh dairy categories. This advantage stems from government support, infrastructure investments, and vertical integration strategies. Baladna demonstrates this local dominance by providing over 95% of Qatar's fresh milk needs through its facilities, which house more than 24,000 Holstein cows.

Market players differentiate themselves through technological investments, including climate control systems, automated milking technologies, and precision farming techniques. These innovations help overcome Qatar's challenging environmental conditions while optimizing productivity, reducing costs, and enhancing animal welfare.

The market shows significant potential in premium segments, including organic dairy, functional products, and specialty formulations that target Qatar's affluent and health-conscious consumers. The regulatory framework influences market competition through quality standards and compliance requirements, benefiting established companies that maintain strict quality assurance protocols and international certifications.

Qatar Dairy Products Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: B.Laban opened its second branch in Qatar. The new location operates on Furousiya Street in Al Muaither, Doha, offering desserts including ice cream.

- February 2025: LuLu Qatar launched a showcase of British dairy products in partnership with the Agriculture and Horticulture Development Board (AHDB) and the Department of Business and Trade (DBT). The initiative expands LuLu's product portfolio of premium offerings in Qatar's retail market.

- February 2023: Baladna, Qatar's primary food and dairy producer, has formed a strategic partnership with The Bel Group, a global cheese and snack manufacturer. The partnership will begin with the production of The Laughing Cow cheese products.

Table of Contents for Qatar Dairy Products Industry Report

1. INTRODUCTION

- 1.1Study Assumptions and Market Definition

- 1.2Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Rising per-capita dairy consumption driven by population growth & expat demographics

- 4.2.2Health consciousness and demand for nutrition-rich options

- 4.2.3Increasing availability of organic dairy products

- 4.2.4Government initiatives for domestic dairy self-sufficiency

- 4.2.5Product innovation and diversification support the market growth

- 4.2.6Adoption of advanced dairy farming technologies

- 4.3Market Restraints

- 4.3.1Limited agricultural land and harsh climate

- 4.3.2High operational costs and resource scarcity

- 4.3.3Stringent regulatory and quality standards

- 4.3.4Consumer concerns over carbon footprint of desert dairy farming

- 4.4Value / Supply-Chain Analysis

- 4.5Regulatory Landscape

- 4.6Technological Outlook

- 4.7Porter's Five Forces Analysis

- 4.7.1Threat of New Entrants

- 4.7.2Bargaining Power of Buyers

- 4.7.3Bargaining Power of Suppliers

- 4.7.4Threat of Substitutes

- 4.7.5Intensity of Competitive Rivalry

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1By Product Type

- 5.1.1Milk

- 5.1.2Yogurt

- 5.1.3Butter

- 5.1.4Cream

- 5.1.5Ice-cream and Frozen Desserts

- 5.1.6Other Product Types

- 5.2By Source

- 5.2.1Cow Milk

- 5.2.2Camel Milk

- 5.2.3Goat and Sheep Milk

- 5.3By Packaging Type

- 5.3.1Bottled

- 5.3.2Cartons

- 5.3.3Pouches

- 5.3.4Tubs and Cups

- 5.3.5Other Packaging Types

- 5.4By Distribution Channel

- 5.4.1On-Trade

- 5.4.2Off-trade

- 5.4.2.1Supermarkets/Hypermarkets

- 5.4.2.2Convenience/ Grocery Stores

- 5.4.2.3Online Retail Stores

- 5.4.2.4Other Distribution Channels

6. COMPETITIVE LANDSCAPE

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1Baladna

- 6.4.2Dandy Company Limited

- 6.4.3Arla Foods amba

- 6.4.4Danone S.A.

- 6.4.5Nestle S.A.

- 6.4.6Gulf Food Production

- 6.4.7Ghadeer Dairy

- 6.4.8Al Maha

- 6.4.9Groupe Lactalis

- 6.4.10Yasar Holding AS

- 6.4.11Almarai Co.

- 6.4.12Al Rawabi Dairy Co.

- 6.4.13FrieslandCampina

- 6.4.14Fonterra Co-operative Group

- 6.4.15Parmalat Middle East

- 6.4.16Kuwait Danish Dairy Co.

- 6.4.17Marmum Dairy Farm

- 6.4.18Al Ain Dairy

- 6.4.19Meggle Group

- 6.4.20Emirates Industry for Camel Milk & Products (Camelicious)

7. MARKET OPPORTUNITIES AND FUTURE OUTLOOK

Qatar Dairy Products Market Report Scope

Dairy products or milk products are a type of food produced from or containing the milk of mammals, most commonly cattle, water buffaloes, goats, sheep, and camels. The market studied has been segmented by product type and distribution channel. By product type, the market is segmented into cheese, milk, yogurt, butter, cream, and other product types. By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, online retail stores, and other distribution channels. For each segment, the market sizing and forecasts have been done on the basis of value (USD million).