Gas Sensor, Detector And Analyzer Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.21 Billion |

| Market Size (2031) | USD 6.84 Billion |

| Growth Rate (2026 - 2031) | 5.59% CAGR |

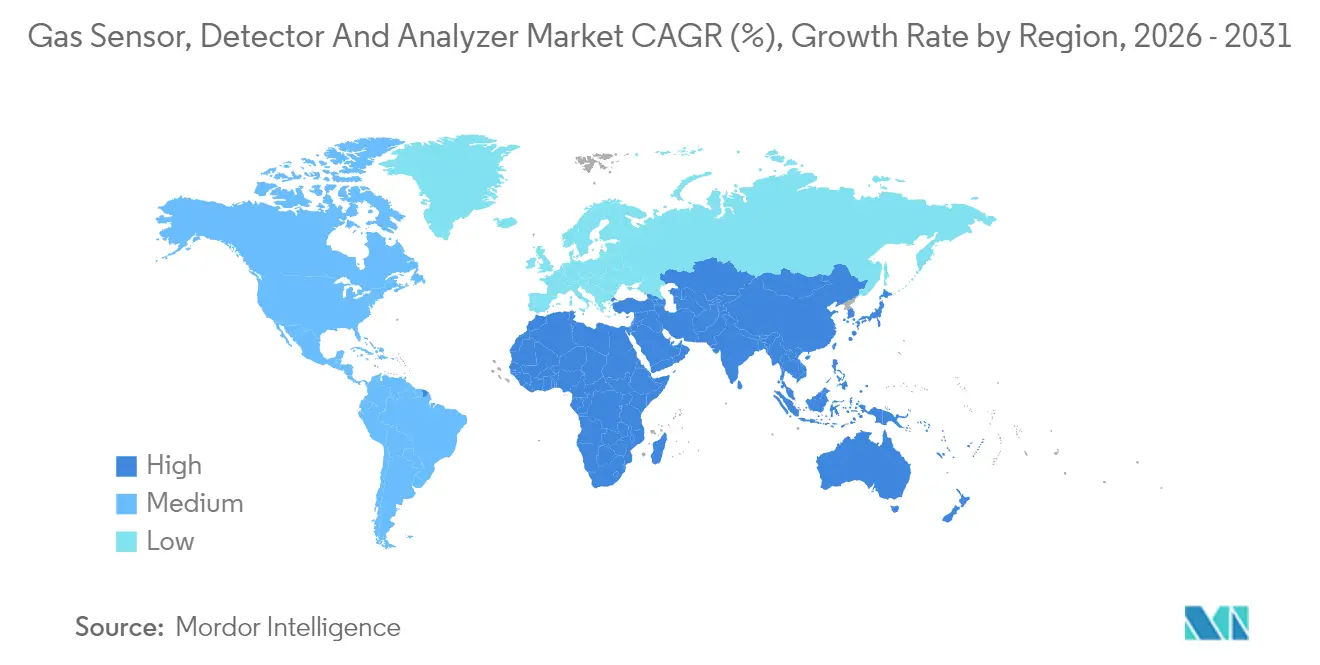

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

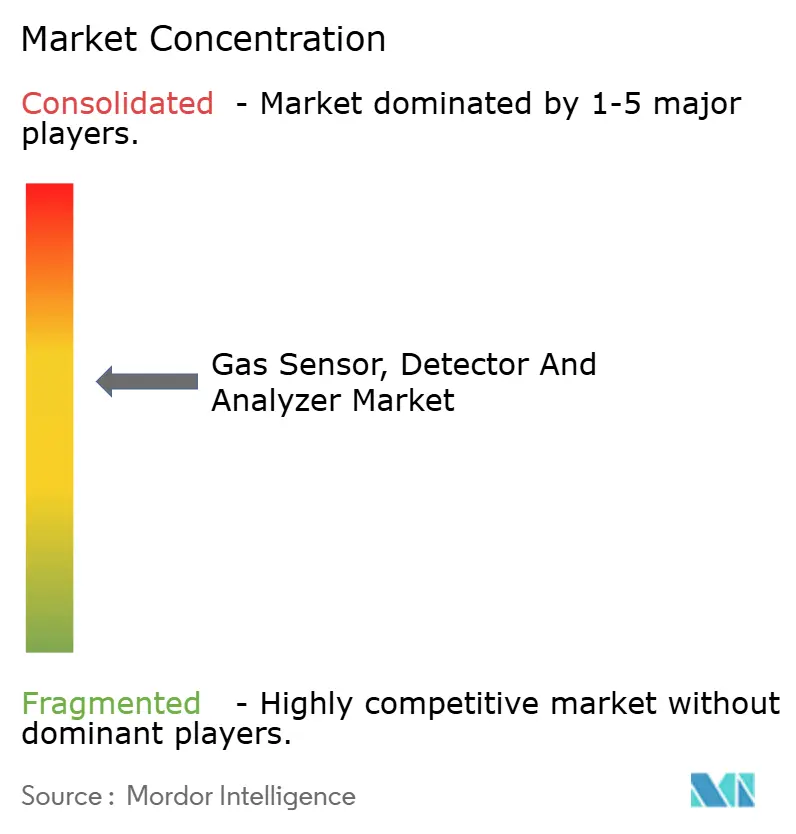

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Gas Sensor, Detector And Analyzer Market Analysis by Mordor Intelligence

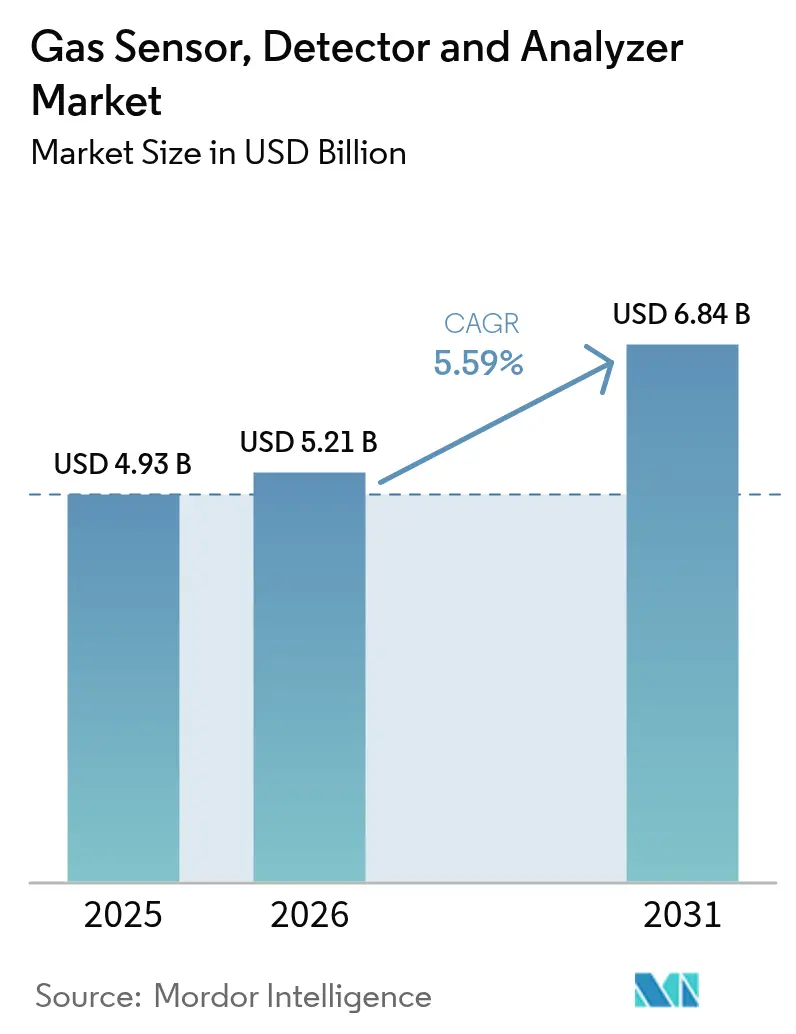

The Gas Sensor, Detector, and Analyzer Market size is expected to grow from USD 4.93 billion in 2025 to USD 5.21 billion in 2026 and is forecast to reach USD 6.84 billion by 2031 at 5.59% CAGR over 2026-2031. Robust enforcement of occupational safety statutes, expanding green hydrogen build-outs, and IoT-centric monitoring architectures collectively underpin this steady trajectory. Momentum is shifting from legacy detectors to miniaturized, multi-parameter sensors that can stream continuous data into analytics platforms. Industrial buyers are increasingly favoring integrated hardware-software bundles that convert raw readings into actionable safety intelligence, which is accelerating the replacement of standalone systems. Supply-side competition, therefore, revolves around sensor selectivity, power efficiency, and secure connectivity rather than basic detection capability. Asia Pacific, led by China and India, remains the pivotal demand engine as regulators align domestic codes with global best practice, while North America and Europe sustain demand through upgrade cycles and tightening emissions limits.

Key Report Takeaways

- By product category, sensors led with a 47.33% share of the gas sensor, detector, and analyzer market in 2025, whereas detectors are projected to register the fastest growth of 6.78% CAGR through 2031.

- By technology, electrochemical modules held 37.08% share of the gas sensor, detector, and analyzer market size in 2025, and semiconductor devices are forecast to expand at 5.66% CAGR during 2026-2031.

- By communication type, wired installations accounted for 68.72% of the revenue in 2025; wireless architectures are expected to grow at a 6.95% CAGR as 5G and LoRaWAN overcome earlier latency and security concerns.

- By end-user industry, the oil and gas sector accounted for 24.31% of the gas sensor, detector, and analyzer size in 2025, while the pharmaceutical industry is poised for a 5.73% CAGR, driven by stringent clean-room validation rules.

- By geography, Asia Pacific captured 35.42% share in 2025 and is projected to log the fastest 5.86% CAGR to 2031 as regional manufacturing scales under harmonized safety mandates.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Gas Sensor, Detector And Analyzer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Safety Awareness Regarding Occupational Hazards | +1.2% | Global, with strongest impact in North America and Europe | Medium term (2-4 years) |

| Proliferation of Handheld Multigas Detectors | +0.8% | Asia Pacific core, spillover to Middle East and Africa | Short term (≤ 2 years) |

| Rising Stringency of Emission Control Regulations | +1.5% | North America and EU, expanding to Asia Pacific | Long term (≥ 4 years) |

| Growing Adoption of IoT-Enabled Gas Monitoring Solutions | +1.1% | Global, led by developed markets | Medium term (2-4 years) |

| Rapid Expansion of Green Hydrogen Production Facilities | +0.7% | Europe and Asia Pacific, emerging in North America | Long term (≥ 4 years) |

| Miniaturization of Photoacoustic Spectroscopy Sensors | +0.3% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Safety Awareness Regarding Occupational Hazards

Rising public scrutiny of workplace fatalities has prompted industrial operators to incorporate continuous detection into their standard operating procedures. OSHA recorded 5,190 worker deaths in 2024, with exposure to gases accounting for 8% of those incidents. Insurance carriers now offer discounts of up to 25% on premiums when certified detection networks are installed, making compliance a direct cost-saving measure. Expanded mandates also reach “non-traditional” settings such as food processing plants, forcing first-time buyers to enter the gas sensor, detector, and analyzer market. Demand therefore shifts from episodic purchase cycles to programmatic rollouts tied to enterprise-wide safety KPIs.

Proliferation of Handheld Multigas Detectors

Portable multigas units have transitioned from specialty gear to first-response essentials following the International Association of Fire Chiefs' endorsement in 2024 for all emergency teams.[1]International Association of Fire Chiefs, “Emergency Response Equipment Standards,” iafc.org Current devices feature six-gas arrays with cross-sensitivity trimmed to below 2%, enabling firefighters and maintenance crews to validate hazards in real-time. Battery life now stretches to 72 hours, eliminating mid-shift downtimes, while GPS and cellular backhauls convert each worker into a mobile sensing node. This behavioral shift supports sustained double-digit unit volumes, especially across fast-growing Southeast Asian construction sectors.

Rising Stringency of Emission Control Regulations

Climate policy reforms are being directly translated into sensor line-item budgets. The European Commission’s 2024 Industrial Emissions Directive sliced permissible NOx thresholds by 40%, obliging power stations to install continuous sampling systems with 95% uptime.[2]European Commission, “Industrial Emissions Directive Amendment,” ec.europa.eu The EPA’s parallel methane rule mandates quarterly surveys of oil and gas assets using optical or equivalent sensors. Because non-compliance fines in the United States average USD 15,625 per violation, operators prioritize certified analyzers capable of parts-per-billion resolution and automated audit trails.

Growing Adoption of IoT-Enabled Gas Monitoring Solutions

Seventy-seven percent of manufacturing sites worldwide now stream detection data into cloud dashboards, up from 52% two years ago, according to the Industrial Internet Consortium.[3]Industrial Internet Consortium, “Connected Manufacturing Survey Report,” iiconsortium.org Edge analytics reduces false alarms by 45% and decreases maintenance call-outs, while encrypted IEC 62443 protocols alleviate cybersecurity concerns. Vendors bundling sensors, gateways, and software analytics therefore realize higher recurring revenue, and this integrative model is steering consolidation moves among tier-one suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Installation and Calibration Costs | -0.9% | Global, most pronounced in emerging markets | Short term (≤ 2 years) |

| Limited Sensor Selectivity Leading to Cross-Sensitivity Errors | -0.6% | Global, particularly affecting multi-gas applications | Medium term (2-4 years) |

| Shortage of Skilled Calibration Technicians in Emerging Economies | -0.4% | Asia Pacific, Middle East, and Africa | Long term (≥ 4 years) |

| Data Security Concerns in Cloud-Connected Detection Networks | -0.3% | Global, concentrated in critical infrastructure sectors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial Installation and Calibration Costs

A full-plant wired detection grid can cost USD 25,000-75,000, and annual calibration contracts add 20-30% to ownership outlays. Forty percent of factories in emerging Asia defer upgrades because budgets are exhausted by other capital projects. Subscription models are gaining traction, trimming entry costs by as much as 70%, yet many small operators still treat gas monitoring as discretionary until regulators intervene.

Limited Sensor Selectivity Leading to Cross-Sensitivity Errors

Electrochemical cells often misclassify gases when humidity and temperature swing, fueling 8-12% false positives per NIST field trials. Every misread forces a work stoppage, so operators remain wary of adopting networked arrays in complex chemical plants. Machine-learning filters improve accuracy but increase device cost and power consumption, constraining deployment in low-margin sectors, such as municipal wastewater treatment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Category: Sensors Drive Integration Flexibility

In value terms, sensors captured 47.33% of the gas sensor, detector, and analyzer market share in 2025, reflecting their plug-and-play compatibility within distributed architectures. The segment is expected to grow at a 6.62% CAGR to 2031, driven by the miniaturization of MEMS detectors that can be embedded directly into machinery panels without requiring structural retrofits. Detectors sustain relevance for confined-space alerts and firefighter kits, whereas analyzers dominate lab and emissions-reporting contexts that demand parts-per-million precision. Manufacturers now collapse these boundaries, offering hybrid modules under IEC 62990 for universal slot-in use, a move expected to reinforce sensor-first design approaches.

Second-generation platforms fold alarms, analytics, and cloud gateways into a single housing, cutting installation hours by 35%. Smaller vendors can now exploit open-standard protocols to sell niche analyzers that integrate seamlessly with tier-one supervisory systems, thereby reducing vendor lock-in concerns. This interoperability steers procurement away from one-off detector orders toward enterprise-wide framework agreements, and the gas sensor, detector, and analyzer market, therefore, inches toward larger average contract values.

By Technology: Semiconductor Innovation Disrupts Electrochemical Dominance

Electrochemical stacks still hold 37.08% of the gas sensor, detector, and analyzer market size because their cost-performance ratio remains favorable in legacy deployments. Nevertheless, semiconductor arrays are driving near-term innovation, with a 5.66% CAGR in operational durability and sub-milliwatt power budgets. Non-dispersive infrared heads maintain a stronghold niche for CO₂ trace detection in food packaging, while paramagnetic loops safeguard oxygen purity in inerting systems. Catalytic beads endure in hydrocarbon environments, where intrinsically safe ratings outweigh selectivity concerns.

Advanced photoacoustic cells, although currently more expensive, offer multi-gas capabilities with compact footprints; patent filings for this class increased by 45% in 2024, underscoring the heightened R&D investments. Regulatory bodies are noticing: the EPA cleared several novel sensor chemistries for mandated leak surveys last year. Consortia expect end users to phase in these solid-state variants as battery life targets extend beyond five years and calibration cycles widen to annual intervals.

By Communication Type: Wireless Gains Despite Security Concerns

Wired backbones still transmit 68.72% of detection data, a figure rooted in industrial mistrust of radio links for life-critical services. Even so, wireless nodes are climbing at 6.95% CAGR as 5G deterministic networks and LoRaWAN low-power profiles demonstrate <100 ms latency. The Federal Communications Commission (FCC) doubled the unlicensed spectrum for industrial IoT in 2024, thereby widening channel availability for dense sensor clusters. Batteries and energy harvesting enable instrumentation in Class I, Division 1 zones where power wiring is cost-prohibitive.

Standards bodies have mitigated cyber risks through certificate-based authentication within WirelessHART and ISA100.11a suites. Vendors add edge-compute chips that quarantine the measurement loop from the corporate network, satisfying CISO audits. Consequently, the addressable gas sensor, detector, and analyzer market expands into brownfield sites that were previously deemed wiring-impossible, particularly within sprawling midstream pipelines.

By End-User Industry: Pharmaceuticals Accelerate Beyond Traditional Markets

Oil and gas remained the largest buyer cohort, accounting for 24.31% of 2025 spending, primarily driven by methane leak surveys and refinery turnarounds. However, pharmaceutical plants now post a 5.73% CAGR as FDA process-validation rules prescribe continuous monitoring to protect drug sterility. Clean-room contracts often bundle hundreds of nodes into a single facility, directing high-margin revenue toward suppliers familiar with Good Manufacturing Practice documentation.

Chemical and petrochemical complexes maintain baseline volumes for combustible-gas arrays, while water utilities implement H₂S and chlorine monitoring to comply with worker-safety regulations. Mining houses embed kits into battery-electric vehicles underground, balancing the risks of explosions against the need for efficient ventilation. Food processors utilize CO₂ probes to verify modified-atmosphere packaging, a niche market growing in tandem with the expansion of plant-based meat manufacturing. Each application incrementally widens the gas sensor, detector, and analyzer market, shifting it from a heavy-industry monopoly to a multi-vertical mainstream.

Geography Analysis

Asia Pacific controlled 35.42% of 2025 revenue and is advancing at a 5.86% CAGR. China enforces GB/T 50493-2024, which compels chemical producers to install multi-point detection networks, while India’s amended Factories Act mandates real-time monitoring in hazardous units. Japanese OEMs, such as Figaro Engineering, export MEMS sensors that reduce power consumption by 30%, thereby accelerating adoption among cost-sensitive Southeast Asian SMEs. South Korea’s shipyards deploy marine-grade detectors resistant to salt spray, and Australia’s underground mines opt for long-range mesh networks to overcome rock-mass RF attenuation.

North America shows replacement-driven stability rather than first-time adoption. OSHA’s confined-space code ensures the health of portable detector volumes, and Canada’s oil-sands operators require ruggedized analyzers capable of operating at -40 °C. Upcoming U.S. methane legislation will enforce quarterly leak surveys, ensuring sustained orders for optical imagers and high-accuracy analyzers. Mexico’s growing automotive clusters are also installing CO and NO₂ arrays in paint-shop ventilation, adding incremental unit sales.

Europe emphasizes near-continuous emissions monitoring. Power generators equipped with NOx scrubbers must verify exhaust levels of less than 15 ppm under the 2024 Industrial Emissions Directive. Germany integrates sensor outputs into Industry 4.0 platforms, feeding predictive maintenance algorithms that prevent furnace trips. The United Kingdom’s offshore wind farms require H₂S monitoring during monopile grouting, while Poland’s copper mines adopt flameproof detectors as production pivots to battery metals. South America, the Middle East, and Africa round out the landscape, with the former driven by copper and lithium projects, and the latter by refinery expansions and gas-powered desalination plants.

Competitive Landscape

The field remains moderately fragmented despite headline acquisitions. Honeywell, Siemens, and Emerson collectively account for roughly 38% of 2024 revenue, yet more than 200 smaller firms serve regional or application-specific niches. Scale players weaponize M and A to fold advanced chemistries into broader automation suites; Siemens’ 2025 takeover of Sensirion’s industrial arm added MEMS arrays that bridge process-control and building-automation sales channels. Honeywell’s USD 180 million plant upgrade earmarks capacity for semiconductor sensors, underscoring a strategic pivot away from purely electrochemical catalogs.

Software capability now differentiates winners. Emerson’s Rosemount 6888 detector bundles edge analytics to flag drift events before calibration expires, and Draeger-Microsoft’s Azure alliance marries detector fleets with AI-driven predictive models. Smaller innovators leverage IEC 62990 interoperability to integrate specialized photoacoustic cells without recreating full monitoring stacks, allowing them to focus on core sensing IP. Patent filings around low-power photoacoustic designs highlight intensifying R&D rivalry, with a 45% rise in 2024, signaling an impending leap in multi-gas handheld performance.

Pricing pressure persists in entry-level SKUs, but high-spec units retain premium margins thanks to stringent certification hurdles. Supply-chain resilience also shapes share: firms owning vertically integrated MEMS fabs can ride component shortages that trip competitors reliant on contract foundries. Overall, the gas sensor, detector, and analyzer market rewards vendors balancing hardware excellence with cloud-grade software, global service footprints, and credible cybersecurity credentials.

Gas Sensor, Detector And Analyzer Industry Leaders

-

Emerson Electric Company

-

Teledyne Technologies Incorporated

-

Siemens Aktiengesellschaft

-

Spectris plc (Servomex Group Limited)

-

Honeywell Analytics Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Honeywell International earmarked USD 180 million to expand its Morristown, New Jersey facility, scaling semiconductor-sensor output for pharmaceutical and hydrogen clients.

- August 2025: Siemens AG closed a USD 95 million purchase of Sensirion’s industrial gas sensor division, bolstering its MEMS portfolio for distributed monitoring.

- July 2025: Emerson Electric rolled out the Rosemount 6888 wireless gas detector line with 5G links and on-device analytics geared toward upstream oil-field deployments.

- June 2025: Teledyne Technologies committed USD 75 million to boost photoacoustic analyzer capacity at its Thousand Oaks, California plant.

Global Gas Sensor, Detector And Analyzer Market Report Scope

Gas analyzers, sensors, and detectors are safety devices used in commercial, medical, industrial, and other industries. These devices continuously analyze and monitor the concentration of gases in different end-user industries, and thus, provide life safety and help avoid fire breakouts.

The Gas Sensor, Detector, and Analyzer Market Report is Segmented by Product Category (Gas Analyzers, Gas Sensors, and Gas Detectors), Technology (Electrochemical, Paramagnetic, and More), Communication Type (Wired, and Wireless), End-User Industry (Oil and Gas, Metals and Mining, Utilities and Power Generation, Pharmaceuticals, Food and Beverage, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Gas Analyzers |

| Gas Sensors |

| Gas Detectors |

| Electrochemical |

| Paramagnetic |

| Zirconia |

| Non Dispersive Infrared |

| Semiconductor |

| Photoionization |

| Catalytic |

| Photoacoustic |

| Other Technology |

| Wired |

| Wireless |

| Oil and Gas |

| Chemicals and Petrochemicals |

| Water and Wastewater Treatment |

| Metals and Mining |

| Utilities and Power Generation |

| Pharmaceuticals |

| Food and Beverage |

| Other End-User Industry |

| North America | United States |

| Canada | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Product Category | Gas Analyzers | |

| Gas Sensors | ||

| Gas Detectors | ||

| By Technology | Electrochemical | |

| Paramagnetic | ||

| Zirconia | ||

| Non Dispersive Infrared | ||

| Semiconductor | ||

| Photoionization | ||

| Catalytic | ||

| Photoacoustic | ||

| Other Technology | ||

| By Communication Type | Wired | |

| Wireless | ||

| By End-User Industry | Oil and Gas | |

| Chemicals and Petrochemicals | ||

| Water and Wastewater Treatment | ||

| Metals and Mining | ||

| Utilities and Power Generation | ||

| Pharmaceuticals | ||

| Food and Beverage | ||

| Other End-User Industry | ||

| By Geography | North America | United States |

| Canada | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the gas sensor market?

It is valued at USD 5.21 billion in 2026 and is projected to reach USD 6.84 billion by 2031.

Which product category commands the largest share?

Sensors hold 47.33% of 2025 revenue thanks to their integration flexibility in distributed monitoring.

Which region is growing the fastest?

Asia Pacific is advancing at a 5.86% CAGR driven by industrial expansion and tighter safety laws.

Why are semiconductor sensors gaining traction?

They offer solid-state reliability, lower power draw, and support for compact multigas designs.

What hinders broader adoption in small plants?

High upfront installation and calibration costs remain the primary barrier, especially in emerging markets.

How are regulations shaping demand?

Stricter emissions and safety mandates in the United States, European Union, and Asia are making continuous monitoring a non-discretionary capital expense.

Page last updated on: