Market Overview

| Study Period | 2020 - 2031 |

|---|---|

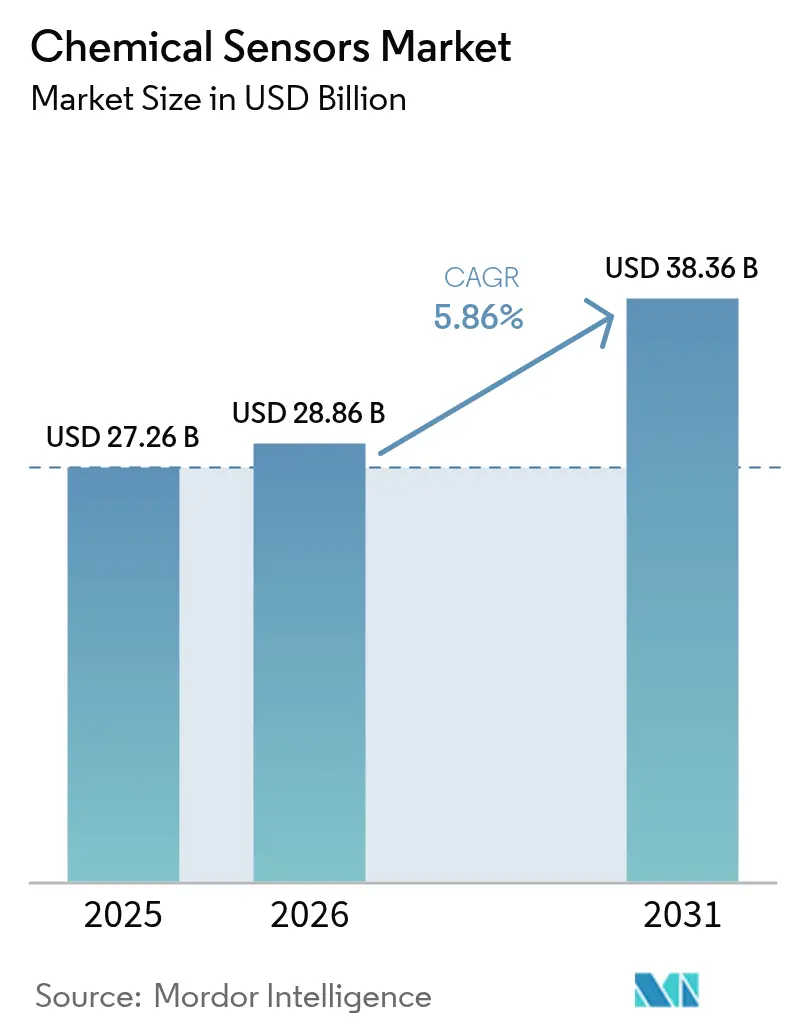

| Market Size (2026) | USD 28.86 Billion |

| Market Size (2031) | USD 38.36 Billion |

| Growth Rate (2026 - 2031) | 5.86% CAGR |

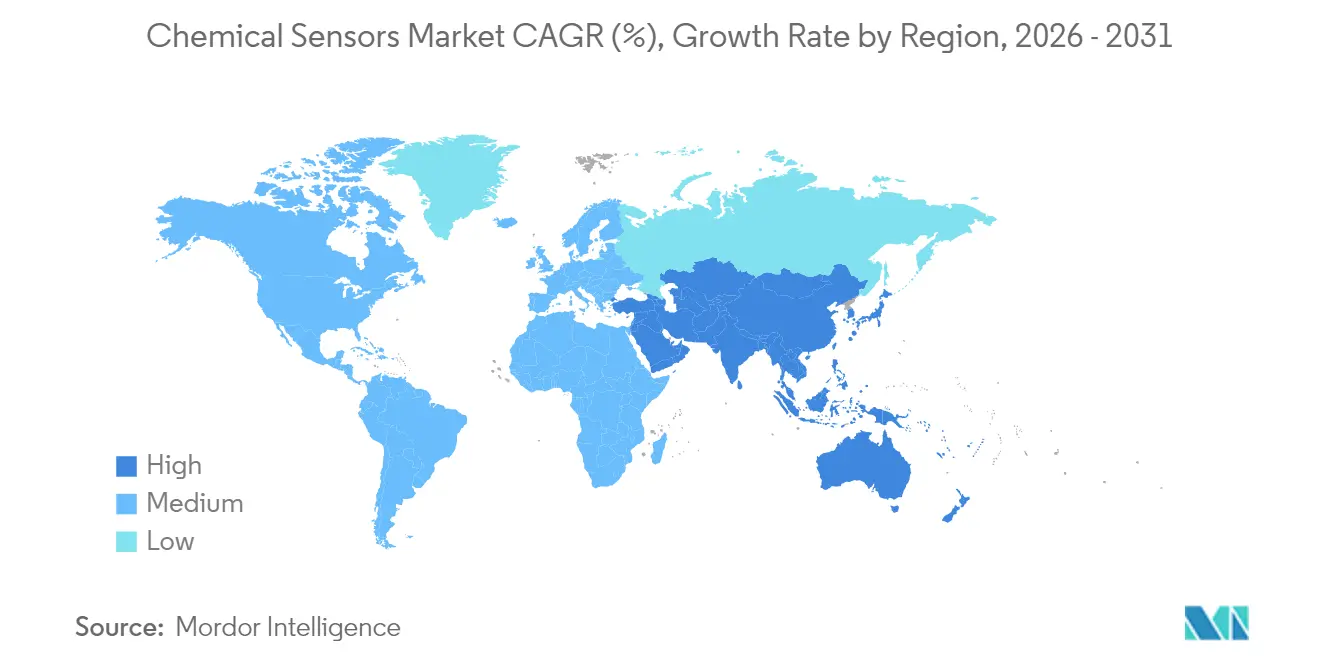

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chemical Sensors Market Analysis by Mordor Intelligence

The chemical sensors market size in 2026 is estimated at USD 28.86 billion, growing from 2025 value of USD 27.26 billion with 2031 projections showing USD 38.36 billion, growing at 5.86% CAGR over 2026-2031. Sweeping air-quality laws, miniaturized biosensing in point-of-care devices, and hydrogen safety regulations are raising global demand. Electrochemical platforms still dominate toxic-gas detection because they achieve parts-per-million accuracy at low power draw. Optical architectures, particularly non-dispersive infrared carbon dioxide monitors, are gaining traction as replacements for catalytic beads in confined spaces. Investment in automated refineries and battery gigafactories continues to favor multi-sensor modules that combine combustible, oxygen, and toxic gas channels on a single board. Meanwhile, printed and flexible sensors are transitioning from pilot-scale to high-volume roll-to-roll lines, bringing sub-USD1 wireless tags within reach for food-safety and athletic-performance markets.

Key Report Takeaways

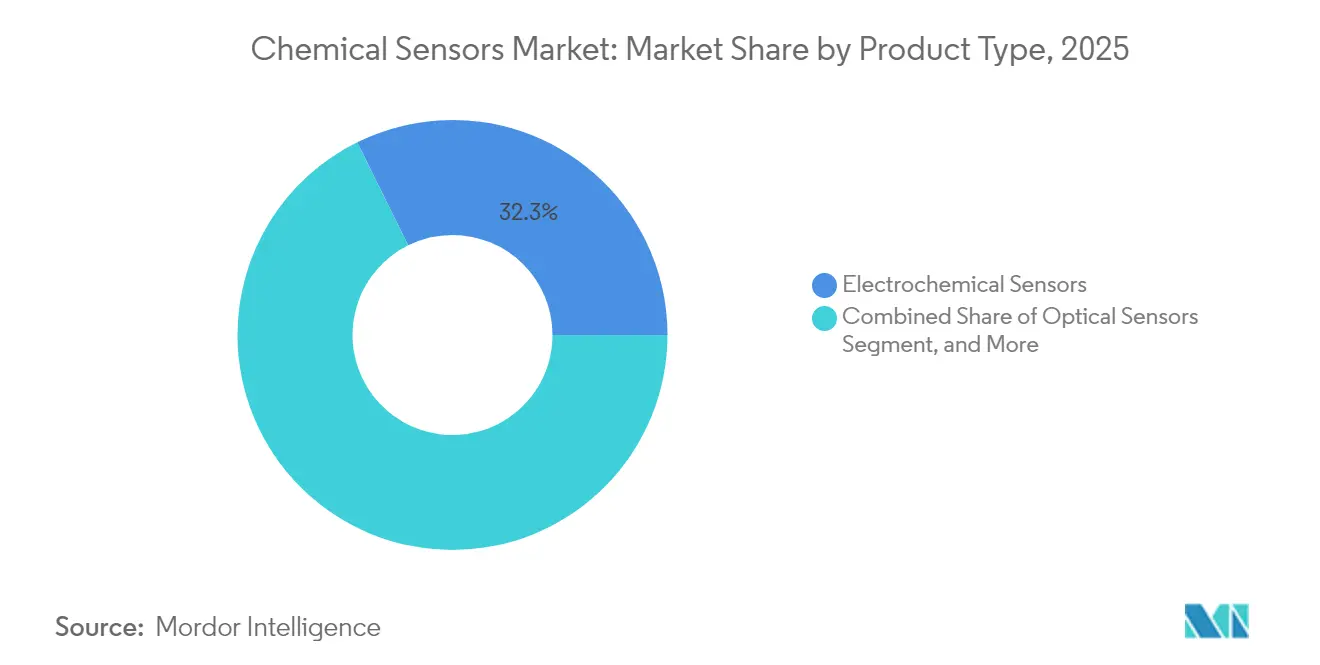

- By product type, electrochemical sensors led with a 32.31% share of the chemical sensors market in 2025, while optical sensors are expected to advance at a 6.98% CAGR to 2031.

- By technology, MEMS-based sensors led with a 27.02% share of the chemical sensors market in 2025, while printed/flexible sensors are expected to advance at a 6.86% CAGR to 2031.

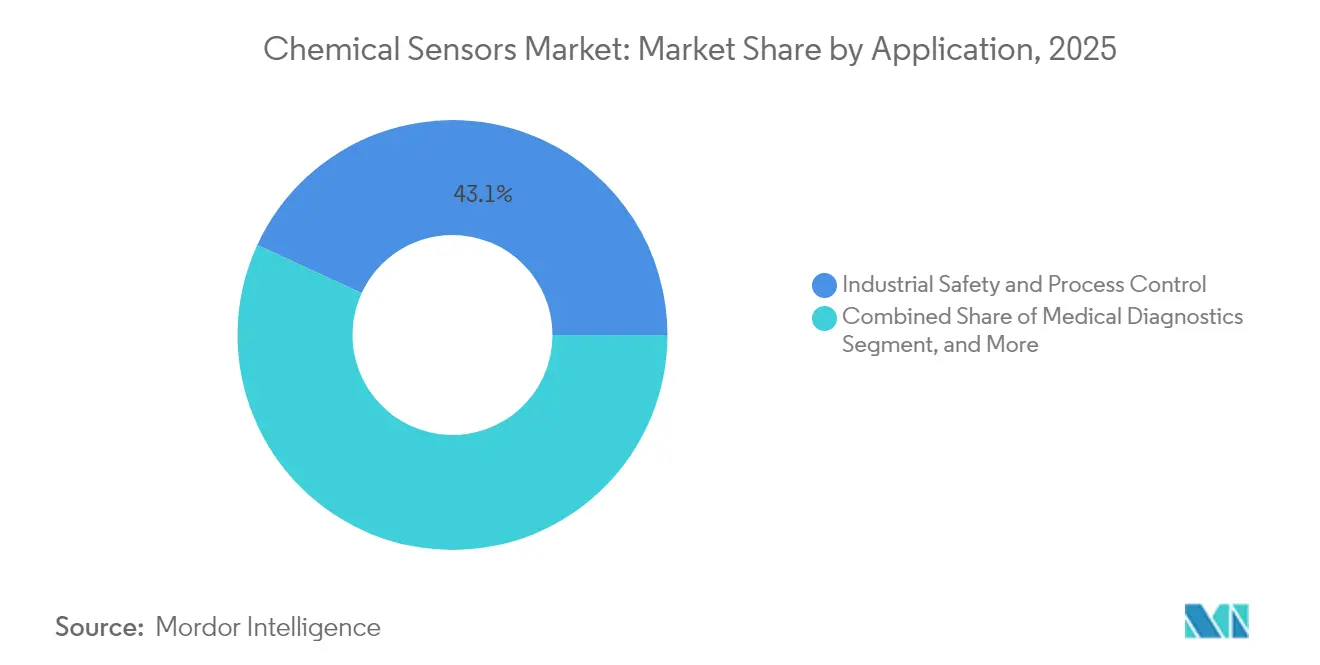

- By application, industrial safety and process control accounted for a 43.12% share of the chemical sensors market in 2025, and medical diagnostics is expected to expand at a 7.12% CAGR through 2031.

- By analyte phase, gas phase accounted for 61.44% share of the chemical sensors market in 2025, and liquid-phase sensing is projected to grow at a 6.63% CAGR between 2026 and 2031.

- By geography, North America held 46.55% share of the chemical sensors market in 2025, while the Asia-Pacific region is forecast to log the fastest CAGR of 6.88% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Chemical Sensors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Environmental Regulations Driving Demand For Industrial Gas Detection | +1.8% | Global, with early enforcement in EU and North America | Medium term (2-4 years) |

| Growing Adoption Of Miniaturized Electrochemical Sensors In Medical Diagnostics | +1.5% | North America, Europe, and urban Asia-Pacific | Short term (≤ 2 years) |

| Expansion Of Industrial Automation And Process Safety Systems | +1.2% | Global, concentrated in manufacturing hubs across Asia-Pacific and North America | Medium term (2-4 years) |

| Emergence Of Flexible Printed Chemical Sensors For Disposable IoT Devices | +0.9% | North America, Europe, and Japan | Long term (≥ 4 years) |

| Integration Of Chemical Sensors Into Hydrogen Infrastructure Safety Systems | +0.7% | Europe, Japan, South Korea, and select North American corridors | Long term (≥ 4 years) |

| Rapid Proliferation Of Indoor Air Quality Mandates In Commercial Real Estate | +0.6% | North America, Europe, and urban centers in China and India | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Environmental Regulations Driving Demand For Industrial Gas Detection

Revisions to the U.S. National Ambient Air Quality Standards in 2024 lowered the annual PM2.5 limit, obliging facilities to install multi-gas monitors that stream electrochemical sulfur-dioxide and nitrogen-dioxide data in real time.[1]U.S. Environmental Protection Agency, “National Ambient Air Quality Standards,” epa.gov The European Union amended its Industrial Emissions Directive the same year, forcing chemical plants over 100 tonnes throughput to publish near-continuous volatile-organic-compound readouts. China expanded its ambient network to 1,800 stations by mid-2025 and each site runs ozone, carbon-monoxide, and nitrogen-oxides cells that collectively created a USD 400 million procurement pool. India’s Central Pollution Control Board mandated Source Emission Monitoring Systems for thermal plants, which spurred a 31% YoY spike in sensor shipments during early 2025. Refineries swapping catalytic-bead elements for infrared heads have cut false alarms by 40% and doubled calibration intervals, reinforcing this regulatory tailwind.

Growing Adoption Of Miniaturized Electrochemical Sensors In Medical Diagnostics

The U.S. FDA cleared seven new point-of-care electrochemical platforms in 2024 that shrink form factors under 15 mm, opening hospital and at-home use cases. Abbott’s FreeStyle Libre posted USD 5.3 billion revenue in 2024, up 21% YoY, underscoring reimbursement-led diffusion of amperometric glucose oxidase stacks. Sensirion introduced a 10 mm-square carbon-dioxide cell in March 2025 that fits ventilator circuits at one-third the cost of infrared alternatives. Europe’s In Vitro Diagnostic Regulation tightened detection-limit rules in May 2024, prompting nanostructured electrodes that drop lactate thresholds below 1 µM.[2]European Commission, “Industrial Emissions Directive,” ec.europa.eu Screen-printed sweat-lactate patches launched for endurance athletes in 2024 and already measure 2-25 mM ranges on the fly.

Expansion Of Industrial Automation And Process Safety Systems

Siemens logged EUR 9.2 billion (USD 10.4 billion) in process-automation orders during fiscal 2024 as factories inserted gas-detection nodes into distributed-control networks. Honeywell earmarked USD 300 million for a Mexicali expansion in January 2025 aimed at hydrogen-fluoride and silane monitoring for gigafactories. ISA published a 2024 technical report that sets safety-integrity levels for hydrogen stations, requiring dual electrochemical sensors with sub-10-second response.[3]International Society of Automation, “ISA-84.00.07 Gas Detection,” isa.org Yokogawa added AI-driven drift analytics to its CENTUM VP platform in 2024, cutting unscheduled downtime at LNG terminals by 25%. OSHA’s proposed confined-space rule will replace single-gas units with four-gas ensembles across utilities and construction sites.

Emergence Of Flexible Printed Chemical Sensors For Disposable IoT Devices

MIT researchers demonstrated sub-USD 0.10 printed ammonia films in 2024 that pave the way for single-use soil probes and cold-chain labels. PARC licensed its printed volatile-organic-compound patents to consumer-electronics OEMs, bringing USD 2-sensors into smart thermostats. The U.S. Department of Defense funded stretchable nerve-agent patches for uniforms, demanding detection in under 15 seconds. Thin Film Electronics shipped 2.3 million near-field tags with integrated ammonia sensors for protein spoilage testing, a 140% YoY leap. ISO published durability test rules that require printed devices to survive 10,000 bends, accelerating wearables commercialization.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Calibration And Maintenance Costs Limit Adoption In Cost-Sensitive Industries | -0.8% | Global, particularly acute in South America, Africa, and Southeast Asia | Short term (≤ 2 years) |

| Sensor Drift And Limited Lifespan Affect Long-Term Reliability | -0.6% | Global, with heightened impact in harsh industrial environments | Medium term (2-4 years) |

| Supply Chain Bottlenecks For Specialty Electrochemical Catalysts | -0.4% | Global, concentrated in platinum-group metal sourcing | Short term (≤ 2 years) |

| Data Governance Concerns Slowing Deployment Of Cloud-Connected Sensors | -0.3% | Europe, North America, and regulated sectors globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Calibration And Maintenance Costs Limit Adoption In Cost-Sensitive Industries

Field calibration every 90-180 days costs USD 150-300 per instrument and quickly eclipses hardware outlays over a five-year run. A 2024 survey of 340 food processors pegged annual upkeep at USD 18,000 per site, 2.8 times capex, discouraging broader coverage. Warehousing operators running net margins below 5% favor handheld spot checks over continuous monitors because service contracts strain budgets. NFPA eased residential carbon-monoxide detector intervals to seven-year cycles in 2025, but industrial units remain on quarterly schedules, cementing this cost divide.

Sensor Drift And Limited Lifespan Affect Long-Term Reliability

Electrochemical oxygen cells drift 0.3% per month at room temperature but quadruple under 40 °C humidity, forcing replacement within three years. A Singapore HVAC study found 18% of 1,200 metal-oxide units wandered out of spec in 18 months, triggering costly false alarms. Honeywell reported field hydrogen-sulfide sensors saw service life shorten from 36 to 22 months when exposed to >50 ppm spikes. IEC’s 2024 accelerated-aging rule now requires <15% signal loss after 1,000 hours at double concentration, raising the R&D bar for next-gen electrodes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Electrochemical Platforms Anchor Safety While Optical Architectures Gain Share

Electrochemical cells captured 32.31% of 2025 revenue and remain the preferred route for hydrogen-sulfide, carbon-monoxide, and nitrogen-dioxide alarms in refineries and wastewater plants. Optical devices are expanding at a 6.98% CAGR through 2031 as operators migrate toward non-dispersive infrared heads that extend maintenance intervals beyond 24 months.

Catalytic-bead sensors, once a staple for combustible gas, are slipping below 17.60% share because intrinsic-safety rules encourage ignition-free optics. Semiconductor metal-oxide devices, now 21.70% of demand, dominate budget indoor-air applications where sub-USD 5 price points matter. Infrared spectroscopy upgrades in natural-gas pipeline inspection push parts-per-billion methane detection and are a key reason optical traction is accelerating. U.S. methane-reduction incentives add a USD 280 million annual pull for these modules. Electrochemical single-gas badges still rule personal protective gear because electrolyte depletion drives repeat sales and predictable replacement cycles, keeping the chemical sensors market robust in consumables revenue.

By Technology: MEMS Integration Trims Cost While Printed Sensors Target Disposables

MEMS variants delivered 27.02% of 2025 revenue by slipping sensing elements and mixed-signal ASICs onto 5 mm silicon dies. Wafer-level packaging slashes assembly overhead and has pulled retail air-quality monitors under USD 50. Printed and flexible formats are logging a 6.86% CAGR as roll-to-roll gravure drops unit cost to USD 0.10 for single-use biosensing strips, opening new frontiers in athletics and decentralized medicine.

CMOS-integrated units, currently 18.70% share, add on-chip calibration that pares bill-of-materials by 30%. Infrared blocks represent about 20.80% of demand, serving HVAC, incubators, and greenhouses where optical lifetime exceeds a decade. Surface-acoustic-wave lines, roughly 12.80% share, stay in niche defense roles for chemical warfare agent alerts, but standardization work on shock and vibration tests is making them more attractive in transport safety. ISO 27891 now requires MEMS gas chips to survive 1,500 g shock with no drift, a hurdle most mainline suppliers have cleared, shoring up confidence in automotive and industrial buyers.

By Application: Industrial Safety Leads While Medical Diagnostics Posts Fastest Expansion

Industrial safety and process control generated 43.12% of 2025 revenue thanks to mandatory multi-gas arrays in confined spaces and continuous emission systems on petrochemical stacks. Medical diagnostics is registering the fastest 7.12% CAGR as payers expand coverage for continuous glucose monitoring and emergency departments adopt point-of-care lactate cards.

Environmental monitoring contributes 15.80% by value through city air-quality grids and water-utility discharge testing. Automotive exhaust and cabin air modules, about 11.70% share, march toward real-time nitrogen-oxides reporting to meet Euro 7 and China 7 rules. Oil and gas upstream and refining uses, now 10.80% of turnover, rely on waterproof electrochemical hydrogen-sulfide cells at wellheads and flare stacks to keep OSHA exposure within 10 ppm. Defense contracts, 5.90% share, focus on trace explosives and warfare agents, reinforcing demand for high-sensitivity surface-acoustic-wave and colorimetric papers. The transition toward value-based healthcare makes remote metabolic monitoring a reimbursable necessity, sustaining double-digit biosensor shipments.

By Analyte Phase: Gas Detection Dominates Revenue While Liquid Sensing Gains From Water Quality Mandates

Gas detection holds 61.44% of 2025 sales, underpinned by industrial-safety badges, ambient air stations, and hydrogen infrastructure diagnostics. Liquid-phase probes are growing at 6.63% CAGR because utilities must track lead, nitrate, and phosphate at tighter thresholds after the 2024 U.S. drinking-water rule update.

Solid-phase sensing, 7.90% share, remains the tool of analytical labs checking soil contamination or tablet dissolution. New hydrogen codes stipulate electrochemical or catalytic detection at 1,000 ppm within one second, intensifying gas-cell R&D. The European Drinking Water Directive inserted per- and polyfluoroalkyl substances at nanogram levels, fueling aptamer-based electrochemical innovations. Aquaculture pilots show dissolved-oxygen and ammonia telemetry cuts fish mortality by up to 18%, indicating another vector for liquid-phase upside in the chemical sensors market.

Geography Analysis

North America generated 46.55% of 2025 revenue, a lead built on strict OSHA confined-space laws and Medicare expansion that added 3.2 million glucose-monitoring beneficiaries. The 2024 PM2.5 standard drove a USD 340 million sensor retrofit wave, and Canada earmarked CAD 180 million (USD 133 million) to extend ozone and particulate networks into remote communities.

Europe contributed 27.98% of sales; its shift to Euro 7 exhaust norms mandates ±10% accuracy across -40-85 °C, generating steady orders for electrochemical and solid-state stacks. Germany carved EUR 500 million (USD 565 million) for hydrogen stations that each need redundant sub-second detectors, while the United Kingdom cut the formaldehyde limit to 0.3 ppm, spurring upgrades across laboratories.

Asia-Pacific is projected to outpace all regions at a 6.88% CAGR through 2031. China’s 1,800-node air network and factory VOC rules, India’s Source Emission Monitoring rollout, and Japan’s hydrogen-fuel road map combine to unlock multi-billion-dollar tenders. South Korea’s semiconductor VOC law adds another USD 85 million annual pull. Middle East and Africa and South America remain smaller slices but are moving toward national gas-pipeline safety laws that hinge on infrared methane trackers, creating long-tail opportunities for local integrators.

Competitive Landscape

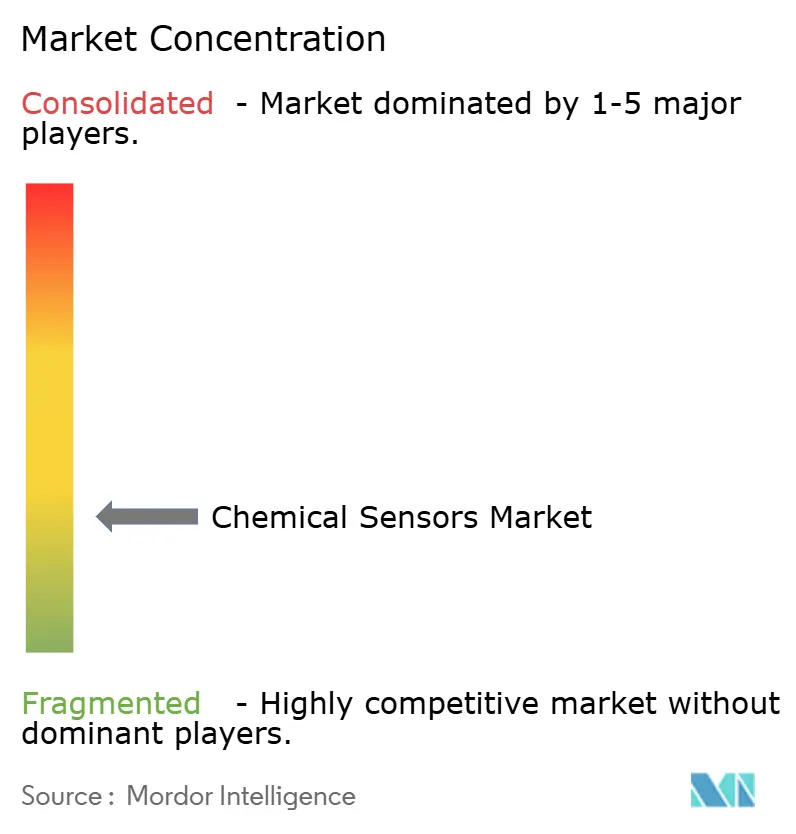

Most of 2024's revenue was attributed to the top five suppliers, confirming moderate fragmentation. Incumbents manage end-to-end verticals, including electrochemical cell winding, MEMS wafer runs, and infrared optics, which enables gross margins above 45%.

Honeywell’s USD 300 million Mexicali buildout will push volumes for gigafactory hydrogen-fluoride arrays, while Siemens folded Sensirion’s industrial gas line into its SIMATIC platform following a EUR 85 million (USD 96 million) deal. Software-led calibration is the new differentiator: AI drift compensation extends service intervals to 180 days and trims ownership cost for budget-sensitive warehouses. Alphasense filed 14 patents in 2024 on nanostructured electrodes that sharpen detection limits by an order of magnitude.

Cloud partnerships also rose; Sensirion added native hooks into AWS IoT Core and Azure IoT Hub so customers mine sensor fleets for predictive insights. Regulation acts as both a moat and a catalyst for firms with in-house IECEx and IVDR labs onboard, new analytes faster, yet niche specialists can win on turnaround speed for third-party test services. Overall, strategic emphasis is tilting toward hydrogen safety, indoor-air mandates, and medical biosensing.

Chemical Sensors Industry Leaders

Alphasense Limited

Figaro Engineering Inc.

Membrapor AG

Sensirion AG

Aeroqual Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Bosch Sensortec launched mass production of a MEMS formaldehyde sensor line at its Dresden 300 mm fab, targeting smart-home and automotive cabin-air applications with unit costs below USD 3.

- August 2025: Alphasense Limited rolled out a cloud-based predictive-calibration suite that extends field maintenance intervals for electrochemical toxic-gas sensors from 90 days to 180 days, with pilot deployments across 12 European chemical plants.

- March 2025: Sensirion AG started commercial shipments of its 10 mm × 10 mm miniaturized electrochemical CO₂ sensor, delivering an initial lot of 50,000 units to three ventilator and anesthesia equipment OEMs.

- January 2025: Honeywell International began construction of its USD 300 million Mexicali, Mexico expansion, adding fully automated assembly lines for hydrogen-fluoride, ammonia, and silane detectors to serve battery gigafactories and semiconductor fabs.

Global Chemical Sensors Market Report Scope

The Chemical Sensors Market Report is Segmented by Product Type (Electrochemical Sensors, Optical Sensors, Pellistor/Catalytic Bead Sensors, Semiconductor Sensors, Other Product Type), Technology (CMOS-Integrated Sensors, MEMS-Based Sensors, NDIR and Infrared Sensors, SAW and Acoustic Sensors, Printed/Flexible Sensors), Application (Industrial Safety and Process Control, Environmental Monitoring, Medical Diagnostics, Automotive Emissions and Cabin Air, Oil and Gas Exploration and Refining, Homeland Security and Defense, Other Application), Analyte Phase (Gas Phase, Liquid Phase, Solid Phase), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

By Product Type

| Electrochemical Sensors |

| Optical Sensors |

| Pellistor/Catalytic Bead Sensors |

| Semiconductor Sensors |

| Other Product Type |

By Technology

| CMOS-Integrated Sensors |

| MEMS-Based Sensors |

| NDIR and Infrared Sensors |

| SAW and Acoustic Sensors |

| Printed/Flexible Sensors |

By Application

| Industrial Safety and Process Control |

| Environmental Monitoring |

| Medical Diagnostics |

| Automotive Emissions and Cabin Air |

| Oil and Gas Exploration and Refining |

| Homeland Security and Defense |

| Other Application |

By Analyte Phase

| Gas Phase |

| Liquid Phase |

| Solid Phase |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Product Type | Electrochemical Sensors | ||

| Optical Sensors | |||

| Pellistor/Catalytic Bead Sensors | |||

| Semiconductor Sensors | |||

| Other Product Type | |||

| By Technology | CMOS-Integrated Sensors | ||

| MEMS-Based Sensors | |||

| NDIR and Infrared Sensors | |||

| SAW and Acoustic Sensors | |||

| Printed/Flexible Sensors | |||

| By Application | Industrial Safety and Process Control | ||

| Environmental Monitoring | |||

| Medical Diagnostics | |||

| Automotive Emissions and Cabin Air | |||

| Oil and Gas Exploration and Refining | |||

| Homeland Security and Defense | |||

| Other Application | |||

| By Analyte Phase | Gas Phase | ||

| Liquid Phase | |||

| Solid Phase | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current Chemical Sensor Market size?

The Chemical Sensor Market size is USD 28.86 billion in 2026 and is projected to register a CAGR of 5.86% during the forecast period (2026-2031)

Who are the key players in Chemical Sensor Market?

Smiths Detection Inc., General Electric Co., MSA Safety Incorporated, Pepperl+Fuchs Group and Honeywell International Inc. are the major companies operating in the Chemical Sensor Market.

Which is the fastest growing region in Chemical Sensor Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Chemical Sensor Market?

In 2025, the North America accounts for the largest market share in Chemical Sensor Market.

What years does this Chemical Sensor Market cover?

The report covers the Chemical Sensor Market historical market size for years: 2019, 2020, 2021, 2022, 2023, 2024 and 2025. The report also forecasts the Chemical Sensor Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: