Industrial Gas Regulator Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

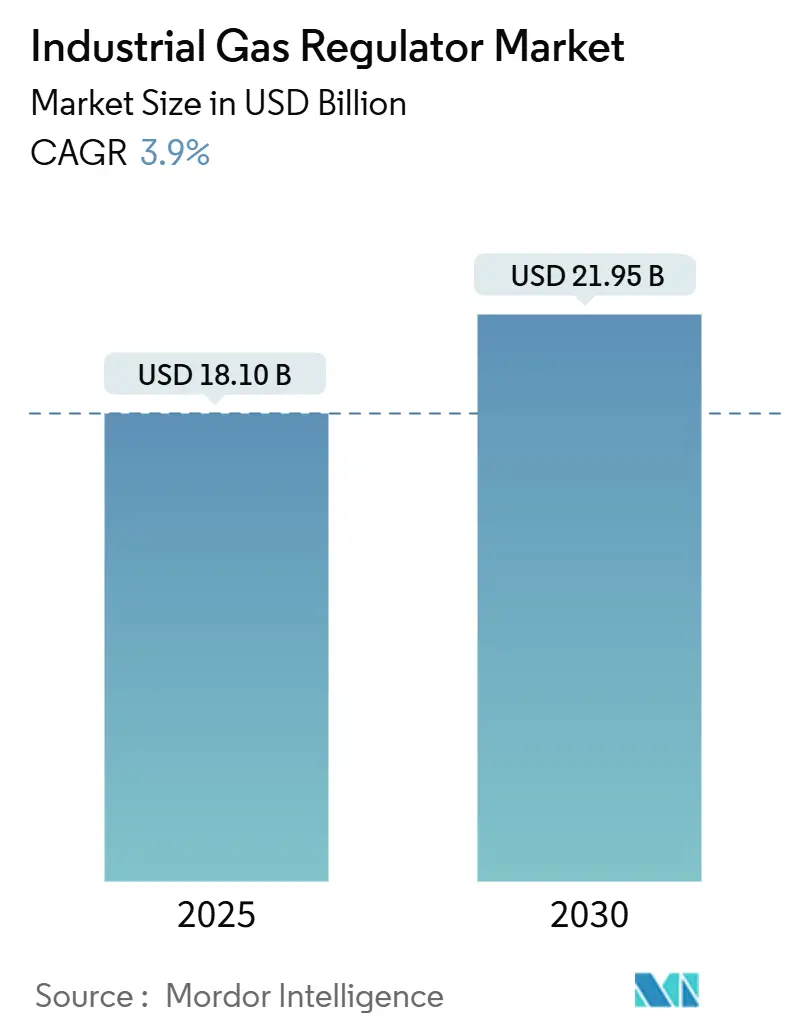

| Market Size (2025) | USD 18.10 Billion |

| Market Size (2030) | USD 21.95 Billion |

| Growth Rate (2025 - 2030) | 3.90% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Industrial Gas Regulator Market Analysis by Mordor Intelligence

The industrial gas regulator market size stood at USD 18.10 billion in 2025 and is projected to reach USD 21.95 billion by 2030, registering a 3.90% CAGR over the period. Growing demand for precise gas flow control across steel decarbonization projects, LNG bunkering terminals, and advanced semiconductor fabs is supporting steady capital outlays despite cyclical spending swings in traditional process sectors. Shipping’s transition toward low-carbon fuels is spurring port authorities to require cryogenic-grade regulators with automated shut-off features, while PFAS-free sealing norms are reshaping component material choices. Capacity additions in green hydrogen electrolyzer farms and on-site nitrogen generation skids are expanding the addressable base for high-pressure and specialty-alloy regulators. Consolidation is picking up as leading automation vendors bolt on pump and compressor specialists to build end-to-end gas flow platforms, illustrated by Honeywell’s USD 2.16 billion Sundyne deal in June 2025.

Key Report Takeaways

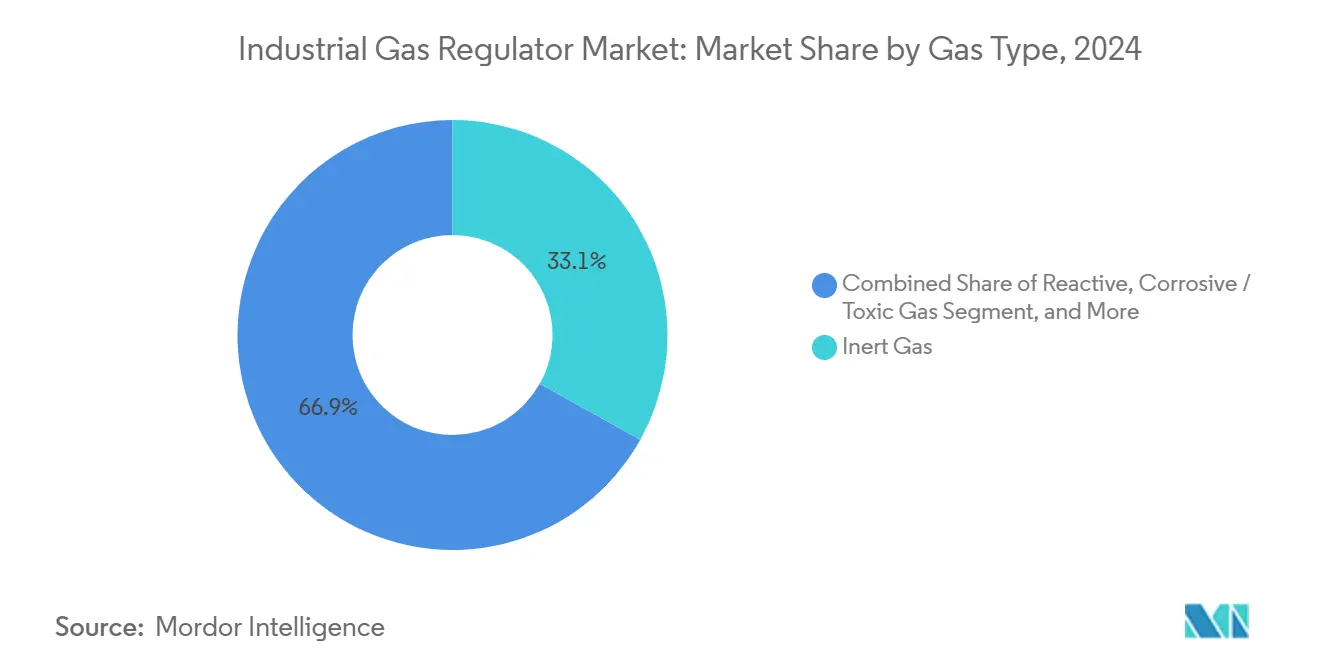

- By gas type, inert gases captured 33.1% of the industrial gas regulator market share in 2024; reactive gases are projected to advance at a 4.9% CAGR through 2030.

- By material, brass products accounted for 45.4% of the industrial gas regulator market size in 2024, whereas high-purity alloys are projected to expand at a 5.2% CAGR to 2030.

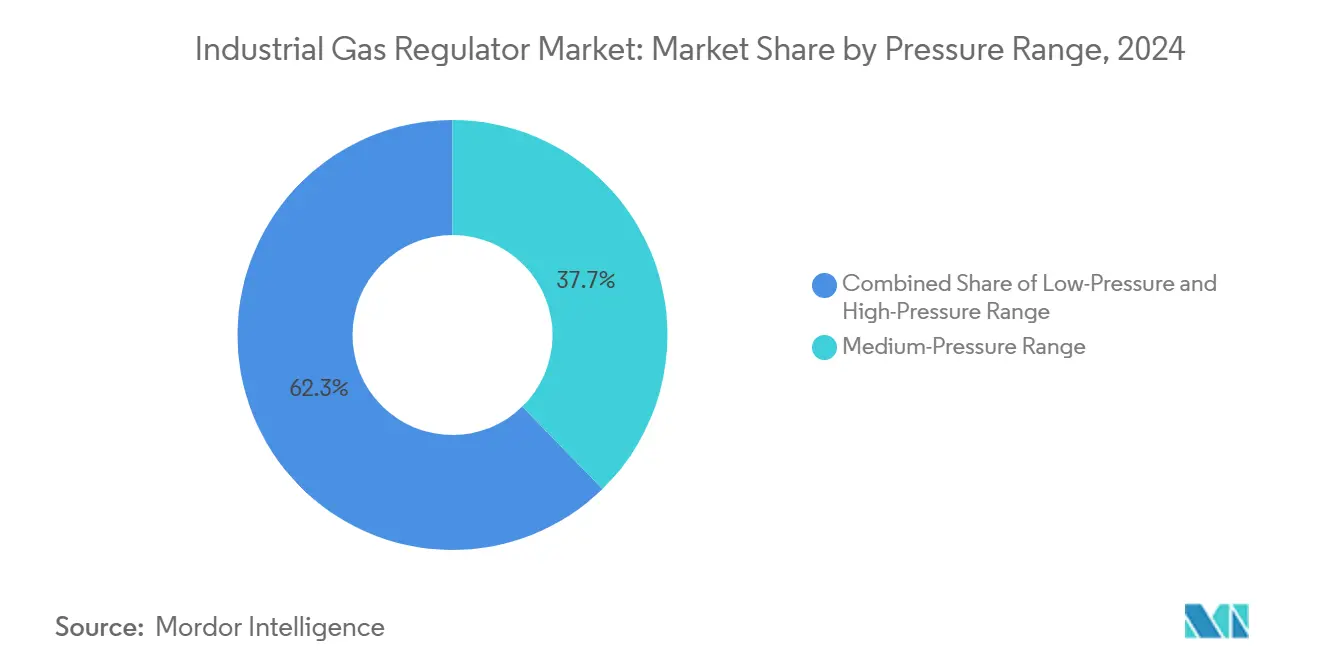

- By pressure range, medium-pressure units commanded 37.7% revenue in 2024, and high-pressure designs are forecast to post a 4.4% CAGR to 2030.

- By end-use, oil and gas operations held 58.9% of the industrial gas regulator market share in 2024, while energy transition projects featuring hydrogen systems are expected to rise at a 5.0% CAGR through 2030.

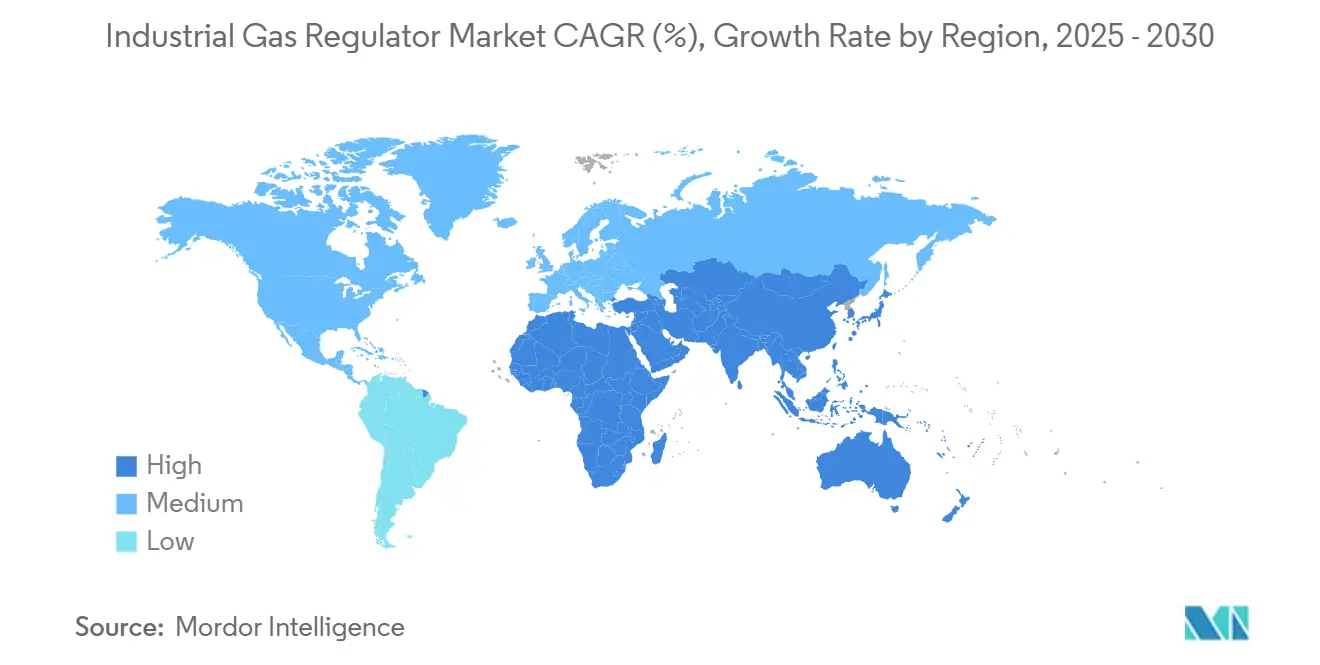

- By geography, the Asia-Pacific region led with 31.70% of 2024 revenue, and the Middle East is expected to record the fastest 5.60% CAGR from 2024 to 2030.

Global Industrial Gas Regulator Market Trends and Insights

Driver Imapct Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Sustainability-Linked Emission Curbs in Steel and Chemicals | +0.8% | Global with concentration in China, India, Europe | Medium term (2-4 years) |

| LNG Bunkering Expansion at Ports | +0.6% | Asia-Pacific, North America, Europe | Medium term (2-4 years) |

| Semiconductor Equipment Capacity Build-Out in Asia | +0.7% | Asia-Pacific core, spill-over to North America | Short term (≤ 2 years) |

| Oil and Gas Brownfield Upgrades (mid-stream compressors) | +0.5% | North America, Middle East, Russia | Long term (≥ 4 years) |

| On-Site Gas Generation Skids | +0.4% | Global, early adoption in North America, Europe | Medium term (2-4 years) |

| Decentralised Green-H₂ Electrolyser Farms | +0.9% | Australia, Saudi Arabia, Europe, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sustainability-Linked Emission Curbs in Steel and Chemicals

New EPA coke-oven norms add USD 4 million annual compliance costs across 11 U.S. facilities, compelling mills to retrofit high-accuracy CO₂, nitrogen, and ammonia regulators that withstand acidic off-gas streams.[1]Source: Federal Register, “National Emission Standards for Hazardous Air Pollutants for Coke Ovens,” federalregister.govEurope’s BAT directive is pushing chemical complexes to deploy corrosion-resistant alloy regulators with PFAS-free diaphragms to monitor sulfuric and nitric flows. Carbon-capture retrofits can cut blast-furnace emissions by up to 45%, creating pull-through demand for ultra-high-purity regulator trains used in solvent recovery units. Asia’s hydrogen-based direct-reduction programs unlock a USD 180 billion decarbonization opportunity by 2050, enlarging the industrial gas regulator market as mills integrate green H₂ distribution skids.

LNG Bunkering Expansion at Ports

Four bunkering methods, truck-to-ship, shore-to-ship, ship-to-ship, and portable-tank transfer, each require cryogenic regulators rated to 315 bar and -162 °C, with flame-arrester interfaces meeting ISO 80079-49.[2]Source: Maritime Administration, “Liquefied Natural Gas Bunkering Study,” maritime.dot.gov Japan’s JFE Engineering won a USD 230 million EPC for Taiwan’s new terminal, underscoring rising Asian demand for marine-grade regulators. Port authorities now mandate the use of IoT-enabled pressure transducers that relay valve status to harbor control rooms, thereby boosting the uptake of smart industrial gas regulator market solutions. North American yards are installing redundant venting lines to comply with NFPA 59A, resulting in increased demand for dual-stage safety regulators.

Semiconductor Equipment Capacity Build-Out in Asia

Intel, TSMC, and Samsung have accelerated fab spending, sending spot helium to USD 14 per m³ and triggering supply security investments in on-site recycle loops that rely on ultra-clean pressure regulators with 5 µin Ra electropolished wetted paths.[3]Source: Amy Nordrum, “Era of Cheap Helium Is Over,” MIT Technology Review, technologyreview.comSub-5 nm nodes need sub-ppb impurity control, leading fabs to specify double-diaphragm stainless steel or Monel regulators with integrated particle filters rated to 0.003 µm. China’s domestic equipment champions are dual-certifying to SEMI S2 and GB standards, expanding the industrial gas regulator industry’s certification workload. Demand peaks before tooling arrives, making automated changeover manifolds critical for uninterrupted gas delivery.

Oil and Gas Brownfield Upgrades (Mid-Stream Compressors)

North American mid-streamers spent USD 10 billion on gas projects in 2024, 67% of which targeted compressor revamps that embed new regulator panels for dual-fuel engines. Phillips 66’s Iron Mesa plant will handle 300 MMcf/d and specifies Class 600 stainless steel regulators with remote actuators for flaring mitigation. Extended 60-week lead times for large compressors are diverting budgets toward retrofit kits, boosting demand for modular regulator skids. Electric drive replacements need precise natural-gas pilot control to avoid methane slip, prompting operators to buy regulators meeting API 614.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Helium Supply Volatility | -0.6% | Global, acute in North America, Asia-Pacific | Short term (≤ 2 years) |

| Cyclical Downturn in Industrial Cap-Ex | -0.4% | North America, Europe, select Asia-Pacific | Medium term (2-4 years) |

| PFAS-free Sealing Mandate Costs | -0.3% | North America, Europe, expanding global | Long term (≥ 4 years) |

| Trade-War Driven Dual-Certification Burden | -0.2% | US-China trade corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Helium Supply Volatility

BLM pipeline outages have cut global output 10%, reducing North American share to an expected 37% by 2025 and doubling lead times for medical MRI regulators.[4]Source: Peak Scientific, “The Continuing Helium Crisis,” peakscientific.com MRI system OEMs are qualifying hydrogen-compatible regulators as back-up, but OSHA 29 CFR 1910.103 imposes tougher ignition controls. Semiconductor fabs are hoarding inventory, forcing regulator makers to finance larger cylinder fleets and carry cash-flow risk. Russian Amur expansion could relieve pressure, yet geopolitical uncertainties keep prices volatile.

Cyclical Downturn in Industrial Cap-Ex

Parker-Hannifin saw an 8.6% North America sales dip in its Diversified Industrial segment despite record 22.1% margins, highlighting uneven project timing. Elevated interest rates and labor shortages delay plant upgrades, steering demand toward MRO spares instead of new regulators. Pneumatics suppliers expect recovery in late 2025 as automation outlays restart, but cautious order patterns temper near-term volume.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Gas Type: Reactive Gases Drive Innovation

Reactive gases reached 4.9% CAGR and are catalyzing material upgrades as hydrogen embrittlement and oxygen ignition risks rise. Emerson’s 2024 launch of the TESCOM HV-7000 hydrogen regulator, rated 700 bar, shows performance thresholds inching upward.[5]Source: Emerson, “New TESCOM HV-7000 Hydrogen Regulator,” emerson.com Inert gases retained a 33.1% share in 2024 by supporting electronics, food packaging, and metal fabrication routines. Corrosive-gas lines, notably for ammonia and SO₂, push uptake of Hastelloy bodies with fluorine-free seats. Specialty calibration mixtures, though niche, command premium prices and demand sub-0.1% flow accuracy, expanding the industrial gas regulator market among analytical-lab suppliers.

Rising helium prices are nudging fabs to nitrogen-purged wafer cooling, redirecting demand from low-pressure helium regulators to medium-pressure nitrogen variants equipped with integrated MFC bypasses. Specialty-blend growth also stems from stricter stack-emission monitoring, requiring multi-component calibration gases that need stainless steel or Monel regulators to avert adsorption. These shifts keep the industrial gas regulator market size expanding steadily across gas-type niches.

By Material: High-Purity Alloys Gain Traction

The industrial gas regulator market size for high-purity alloys is projected to jump from USD 3.5 billion in 2025 to nearly USD 4.5 billion by 2030, equating to a 5.2% CAGR. Brass maintains volume leadership in standard compressed-air and nitrogen circuits; however, PFAS-free gasket mandates are accelerating the switch to stainless steel spring packs and low-sulfur 316L bodies. Semiconductor fabs now dictate <1 ppm total metal contamination, elevating Monel and Nickel 200 regulators into mainstream demand curves.

Price premiums of 40-70% over brass are offset by extended MTBF and compliance advantages under SEMI F20 and ISO 11119-2. In hydrogen refueling, Monel regulators resist hydride formation, making them the de facto choice for 700-bar pump shelters. Exotic-alloy uptake fuels aftermarket opportunities, while scheduled seat replacements necessitate proprietary spares, thereby reinforcing vendor lock-in across the industrial gas regulator market.

By Pressure Range: High-Pressure Applications Accelerate

High-pressure designs (>34 bar) are forecast to add USD 1.2 billion in sales between 2025 and 2030, equal to a 4.4% CAGR. Hydrogen mobility, CNG transport, and offshore CO₂ sequestration all rely on 10,000 psi regulators with double-barrier venting and burst-disc redundancy. Medium-pressure units still hold 37.7% 2024 share thanks to widespread use in general industry.

IoT retrofits are expanding in high-pressure spheres as pipeline operators deploy MEMS strain-gauge modules that relay valve stem travel data. Remote diagnostics slash inspection rounds, cutting OPEX by 15% while raising cybersecurity requirements. Integrated designs bundle relief, check, and filter elements to shorten install footprints, trimming weight on skid packages bound for FPSOs.

By End-Use Industry: Energy Transition Emerges

Oil and gas applications generated 58.9% of the revenue in 2024 through well-pad choke, compressor, and refinery duties. Yet, energy-transition verticals, such as green hydrogen, biogas upgrading, and fuel-cell backup power, are expected to rise 5.0% annually, overtaking electronics by 2029. Saudi Aramco’s USD 7.7 billion Fadhili expansion alone will consume thousands of Class 1500 regulators across dehydration and NGL splitters.

Healthcare needs continue to climb, especially after regional oxygen shortages during the 2024 pandemic spikes, prompting hospitals to commission redundant bulk-O₂ yards with dual-stage brass-free regulators. Food processors are embedding nitrogen flush lines to extend shelf life, a practice that now touches 70% of new packaging installs in Europe. Ultimately, the industrial gas regulator market benefits from both legacy hydrocarbons and emerging decarbonization pathways.

Geography Analysis

Asia-Pacific generated 31.70% revenue in 2024, underpinned by China’s 1,655.6 × 10⁸ m³ LNG imports and EUR 20 billion (USD 23.29 billion) semiconductor FDI inflows. Government incentives in Japan and South Korea for sub-3 nm fabs sustain high-purity alloy regulator demand, while Australia’s USD 127 billion hydrogen pipeline ensures long-cycle project visibility. Production Linked Incentives in India target steel and medical-gas equipment, sending local regulator OEMs on capacity-expansion drives. Stringent JIS and GB standards on cylinder inspection elevate aftermarket refresher cycles, anchoring the industrial gas regulator market in the region.

The Middle East recorded the highest 5.60% CAGR outlook as Saudi Arabia accelerates to 165 bcm gas output by 2030; Fadhili’s capacity hike from 2.5 to 3.8 Bcf/d alone will boost regulator shipments by 18% over baseline. UAE carbon-intensity targets and Qatar’s LNG mega-trains inject high-pressure regulator demand. Local EPCs favor suppliers that can pre-certify to Saudi ARAMCO’s SAMSS 070001 specs, narrowing the vendor pool and supporting premium pricing within the industrial gas regulator market.

North America and Europe remain mature but opportunity-rich. The U.S. midstream’s USD 10 billion 2024 spend creates a steady flow for retrofit kits, especially API 6D-rated regulators with fugitive-emission packing. EU PFAS legislation inflates material costs yet also triggers replacement cycles across refineries. Tariffs from 5–25% on Chinese valve imports raise landed costs, advantaging domestic producers. South America and Africa are nascent, with Brazil’s pre-salt gas and Nigeria’s NLNG Train 7 offering spot project spikes rather than sustained volume.

Mordor Intelligence provides coverage of the industrial gas regulator market across other key regional markets. Detailed country-level analysis extends to United States incorporating local coverage and market participation, as required.

Competitive Landscape

The industrial gas regulator market is moderately fragmented. Emerson, Honeywell, and Parker-Hannifin integrate regulators into broader automation suites and leverage global service networks. Their scale enables multi-year framework agreements with major oil companies and semiconductor manufacturers.

Honeywell’s Sundyne acquisition brings sealless pump expertise, positioning the firm to package compressors and regulators under a unified control layer, while Dover’s 2024 Marshall Excelsior deal strengthened its cryogenic valve lineup. Swagelok and Rotarex defend niche shares via high-purity alloys and cylinder-mounted ring valves, respectively. Start-ups specializing in laser-cut isolation regulators for fuel-cell stacks are capitalizing on design-for-additive-manufacturing trends.

Digitalization is the competitive hinge: vendors embedding Bluetooth Low-Energy pressure sensors see a 12% higher aftermarket contract attachment rate. Partnerships such as SICK–Endress+Hauser bundle gas analyzers with pressure control to offer turn-key emissions-monitoring skids. Barriers include dual certification for U.S.–China trade lanes and PFAS phase-out costs. Market participants that pre-qualify PFAS-free seal materials and achieve ATEX/IECEx dual stamps are winning LNG terminal tenders.

Industrial Gas Regulator Industry Leaders

Emerson Electric Co.

Parker-Hannifin Corporation

Honeywell International Inc.

Cavagna Group S.p.A.

Rotarex S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Honeywell closed its USD 2.16 billion Sundyne acquisition, integrating compressor know-how into its Process Solutions unit.

- May 2025: Phillips 66 began constructing the 300 MMcf/d Iron Mesa gas processing plant in the Permian Basin.

- May 2025: MSA Safety purchased M&C TechGroup for USD 200 million to deepen gas-analysis capabilities.

- April 2025: Saudi Aramco awarded USD 7.7 billion EPC contracts to lift Fadhili Gas Plant to 3.8 Bcf/d throughput.

Global Industrial Gas Regulator Market Report Scope

| Inert (N₂, Ar) |

| Reactive (O₂, H₂) |

| Corrosive / Toxic (Cl₂, NH₃, HCl, SF₆) |

| Specialty and Calibration Blends |

| Brass |

| Stainless Steel |

| High-Purity Alloys (Monel, Hastelloy) |

| Low-Pressure (≤ 0.7 bar) |

| Medium-Pressure (0.7–34 bar) |

| High-Pressure (≥ 34 bar) |

| Oil and Gas |

| Chemicals and Petrochemicals |

| Metals and Mining |

| Healthcare and Life-Sciences |

| Food and Beverage |

| Electronics and Semiconductor |

| Energy Transition (Green-Hydrogen, Fuel-Cells) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Gas Type | Inert (N₂, Ar) | ||

| Reactive (O₂, H₂) | |||

| Corrosive / Toxic (Cl₂, NH₃, HCl, SF₆) | |||

| Specialty and Calibration Blends | |||

| By Material | Brass | ||

| Stainless Steel | |||

| High-Purity Alloys (Monel, Hastelloy) | |||

| By Pressure Range | Low-Pressure (≤ 0.7 bar) | ||

| Medium-Pressure (0.7–34 bar) | |||

| High-Pressure (≥ 34 bar) | |||

| By End-Use Industry | Oil and Gas | ||

| Chemicals and Petrochemicals | |||

| Metals and Mining | |||

| Healthcare and Life-Sciences | |||

| Food and Beverage | |||

| Electronics and Semiconductor | |||

| Energy Transition (Green-Hydrogen, Fuel-Cells) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the industrial gas regulator market in 2025?

The industrial gas regulator market size is valued at USD 18.10 billion in 2025.

Which region leads demand for industrial gas regulators?

Asia-Pacific held 31.70% of 2024 revenue, driven by LNG imports and semiconductor expansion.

How are PFAS regulations affecting material choices?

PFAS-free mandates are shifting demand toward stainless steel and high-purity alloy regulators with alternative sealing technologies.

Which end-use sector shows the highest growth potential?

Energy-transition projects especially green hydrogen electrolyzers are projected to rise at a 5.0% CAGR to 2030.

Page last updated on: