Fine Art Logistics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.35 Billion |

| Market Size (2031) | USD 4.26 Billion |

| Growth Rate (2026 - 2031) | 4.94% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

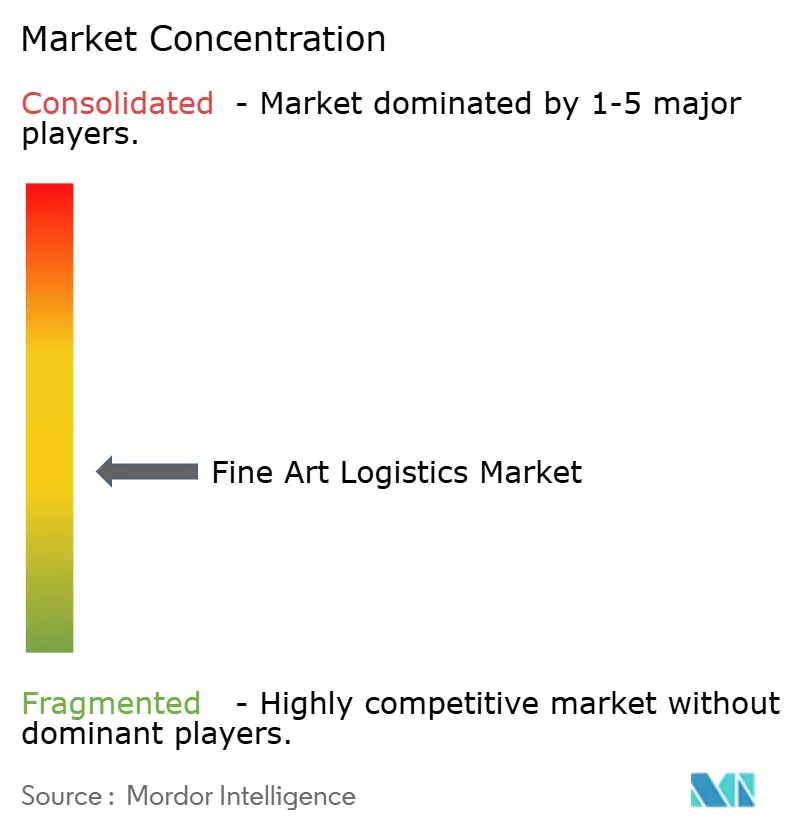

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fine Art Logistics Market Analysis by Mordor Intelligence

The Fine art logistics market is expected to increase from USD 3.22 billion in 2025 to USD 3.35 billion in 2026 and reach USD 4.26 billion by 2031, growing at a CAGR of 4.94% over 2026-2031.

Structural change is underway as hybrid live-plus-digital auctions tighten shipment windows, while duty-free freeports in Singapore, Hong Kong, Geneva, and Dubai multiply inter-continental transfer points. Transportation continues to anchor revenue, yet technology-rich value-added services from IoT-enabled climate monitoring to blockchain provenance tools are expanding more quickly, moving the Fine art logistics market toward integrated, stewardship-oriented contracts. Clients are willing to pay premiums for providers that align with higher insurance thresholds, sustainable fuel programs, and increasingly complex customs regimes. Cost headwinds from jet-fuel swings and sanctions compliance encourage scale advantages, driving consolidation among firms able to invest in smart packaging and regional freeport footprints.

Key Report Takeaways

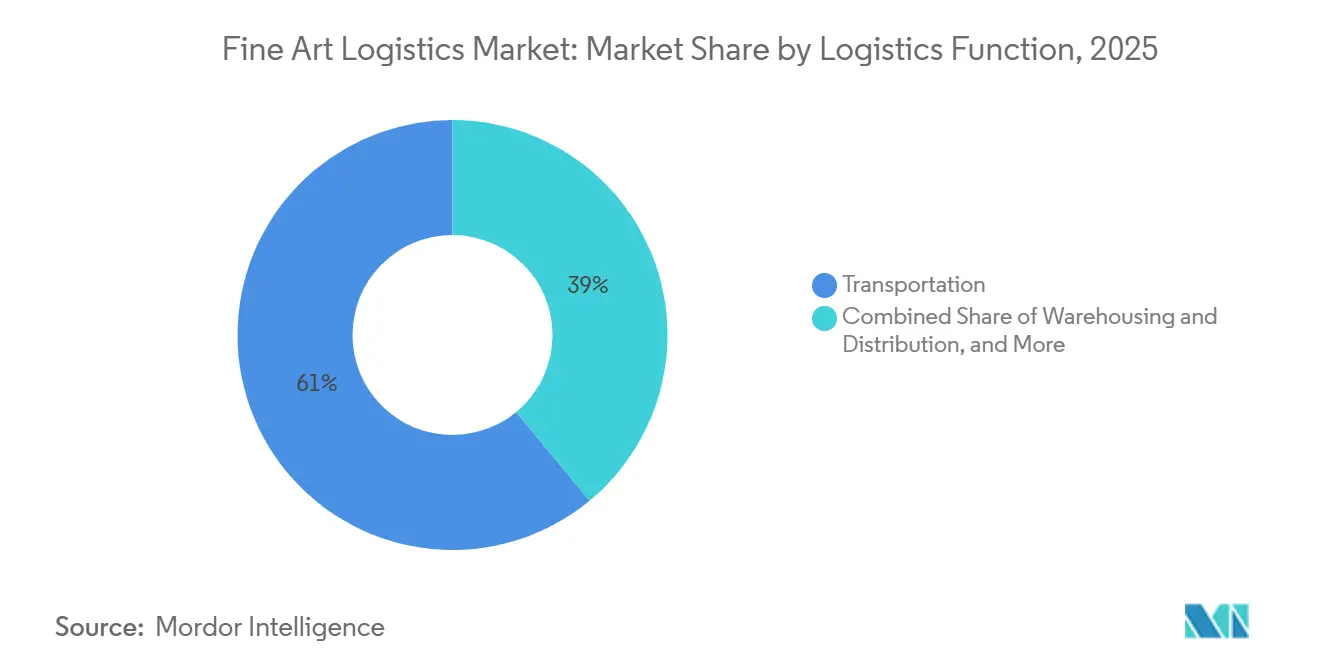

- By logistics function, transportation led with 60.39% of the Fine art logistics market share in 2025, whereas value-added services are projected to expand at a 5.45% CAGR through 2031.

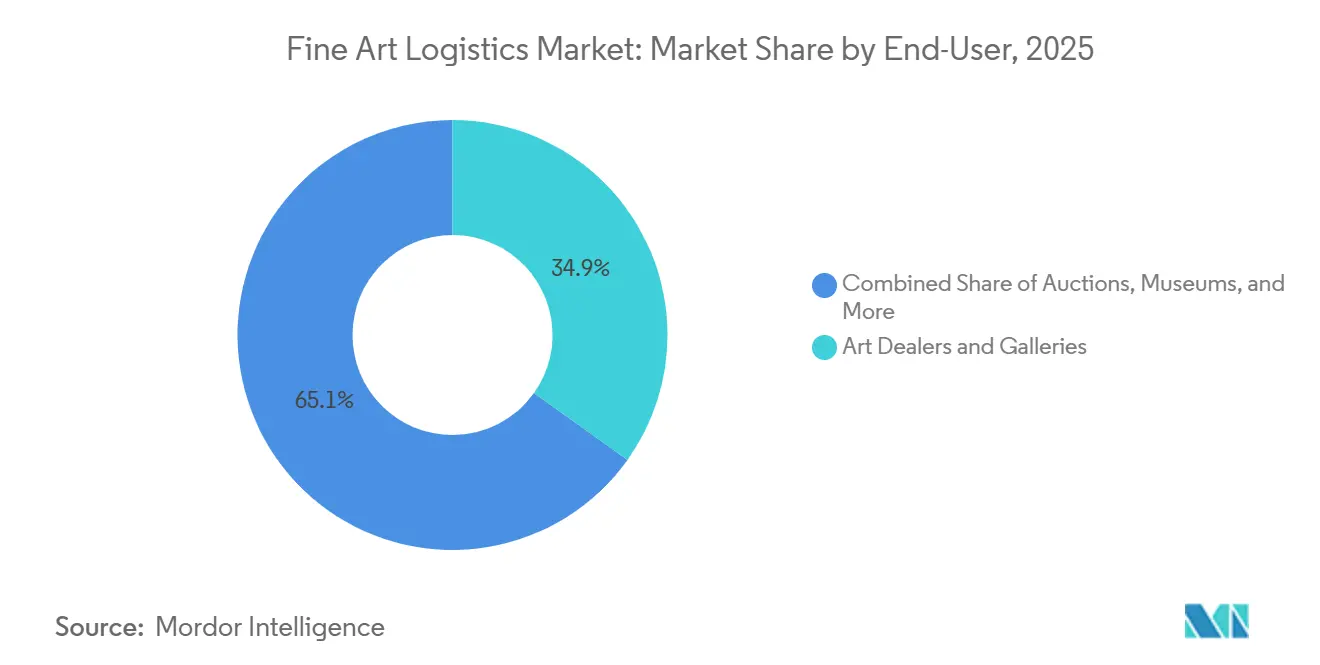

- By end user, art dealers and galleries held 34.87% of the Fine art logistics market size in 2025, while private collectors recorded the fastest 6.08% CAGR over 2026-2031.

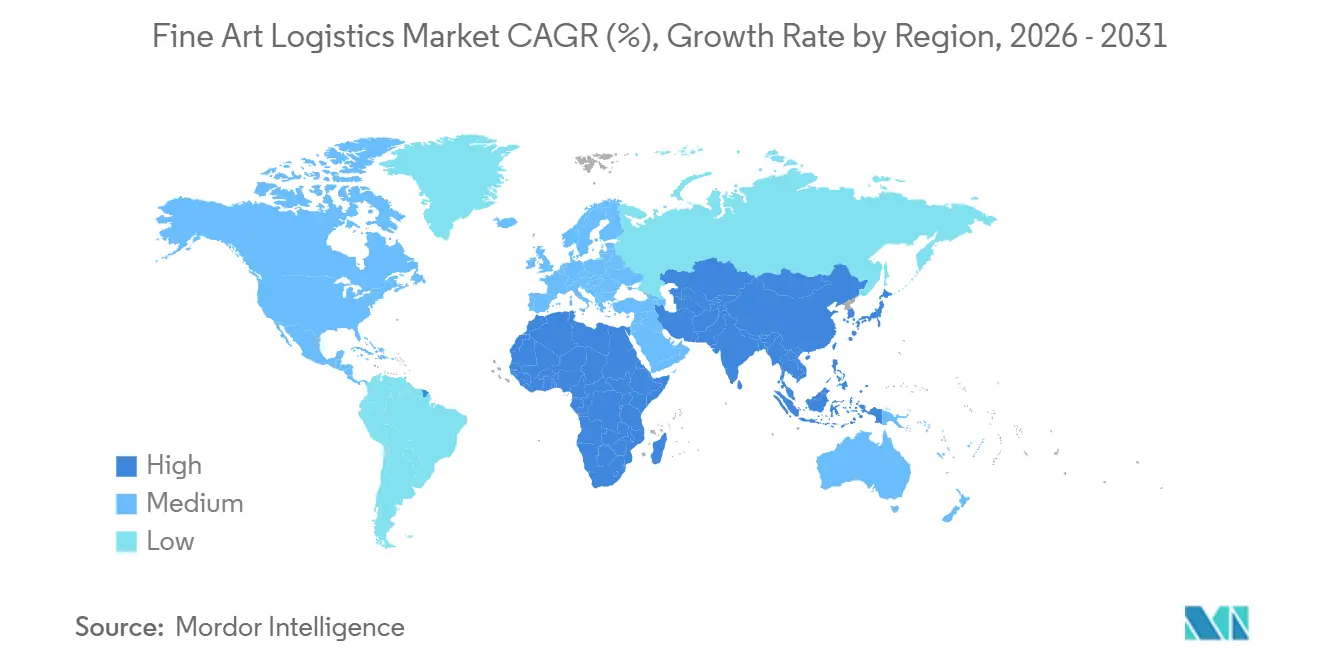

- By geography, North America accounted for 42.14% of the Fine art logistics market share in 2025; Asia-Pacific is forecast to grow at a 5.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Fine Art Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hybrid live-plus-digital auction formats intensify just-in-time shipment volumes | +1.1% | Global, concentrated in major auction hubs | Short term (≤ 2 years) |

| Higher insurance coverage thresholds push stakeholders toward specialist providers | +0.9% | North America and Europe, expanding to APAC | Medium term (2-4 years) |

| Expansion of duty-free art freeports in Europe and GCC amplifies inter-continental flows | +0.8% | Europe, GCC, and Asia-Pacific hubs | Medium term (2-4 years) |

| IoT-enabled climate-monitoring crates create pull for smart-logistics vendors | +0.6% | Global, early adoption in premium segments | Long term (≥ 4 years) |

| Demand for bio-marine-fuel shipping lanes spurs sustainable ocean transport | +0.4% | Europe and North America, expanding globally | Long term (≥ 4 years) |

| Fractional-ownership platforms require rotating custody and micro-fulfilment models | +0.3% | North America and APAC, concentrated in tech-forward markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Hybrid Live-Plus-Digital Auction Formats Intensify Just-In-Time Shipment Volumes

Auction houses now synchronize in-person previews with global online bidding. Artworks must reach preview venues ahead of streaming schedules, pass digital fingerprint checks, and depart for buyers within days, compressing the traditional three-week auction cycle into less than 10 days[1] “Working and touring in Europe: guidance for visual arts, the art market and museums,” UK Government, gov.uk . Remote 3-D scanning lets bidders view high-resolution twins, yet the physical object still travels to meet pre-sale condition reporting standards. Broader bidder reach increases post-sale cross-border shipments, shifting fine art logistics market capacity toward agile, multi-modal routing. Compliance layers tied to passports, visas, and customs declarations add paperwork that specialist providers embed into turnkey auction logistics packages.

Higher Insurance Coverage Thresholds Push Stakeholders Toward Specialist Providers

Underwriters now insist on larger “nail-to-nail” limits after several high-profile loss events, driving stakeholders toward logistics firms with pre-vetted Lloyd’s agreements[2]“ICEFAT organisation and standards for fine art transport,” International Exhibition and Fine Art Transporters, icefat.org . Enhanced due-diligence requires sanctions screening and anti-money-laundering reporting before pick-up. Premium providers offer bundled coverage that accelerates policy issuance, creating a tiered supply landscape where smaller carriers handle lower-value regional moves. The added paperwork favors firms that maintain 24-hour specialist claims desks and digital audit trails.

Expansion of Duty-Free Art Freeports in Europe and GCC Amplifies Inter-Continental Flows

Geneva, Luxembourg, Singapore, and Dubai freeports allow indefinite, tax-deferred storage. Logistics specialists now stage artwork in a “hub-and-spoke” pattern, rotating it through multiple bonded zones before final sale, without triggering VAT or import duties. Providers are investing in on-site climate vaults and x-ray screening near freeports to shorten transfer chains. GCC cultural funding is turning Dubai and Abu Dhabi into preferred staging points for South Asian and African collectors, widening trade lanes and lifting Fine art logistics market demand for Middle Eastern expertise.

IoT-Enabled Climate-Monitoring Crates Create Pull for Smart-Logistics Vendors

Smart crates equipped with temperature, humidity, and shock sensors stream data to mobile dashboards, enabling curators to intervene mid-route. When paired with blockchain ledgers, every micro-climate reading becomes an immutable entry that insurers accept as evidence. Museums increasingly mandate IoT telemetry for outbound loans, effectively excluding carriers that cannot supply real-time condition reports. Providers market stand-alone monitoring subscriptions to galleries, adding annuity revenue on top of transport fees and nudging the Fine art logistics market toward service-led differentiation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile jet-fuel and bunker prices inject cost unpredictability | -0.6% | Global, particularly impacting long-haul routes | Short term (≤ 2 years) |

| Geopolitical sanctions heighten export-licence and compliance complexity | -0.5% | Global, concentrated in sanctioned jurisdictions | Medium term (2-4 years) |

| Shortage of museum-grade sustainable packing substrates slows green transition | -0.4% | Global, acute in specialized conservation markets | Long term (≥ 4 years) |

| Stricter anti-illicit-antiquities checks prolong provenance documentation cycles | -0.3% | Europe & North America, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Jet-Fuel and Bunker Prices Inject Cost Unpredictability

Energy-price swings translate into surcharges that outpace annual logistics budgets, squeezing margins when contracts lock prices months ahead. Larger providers hedge fuel exposure through futures and pass-through clauses, widening the gap with smaller rivals. The volatility accelerates consolidation as acquisition candidates seek the balance-sheet muscle required to weather cost spikes.

Geopolitical Sanctions Heighten Export-License and Compliance Complexity

Heightened scrutiny of Russian, Iranian, and Syrian transactions forces carriers to run daily restricted-party screening and seek special export licences. Documentation mistakes can lead to seizure, reputational damage, and insurer withdrawal, prompting clients to favor providers with in-house legal teams. Real-time compliance software has become a compulsory investment for any firm chasing international Fine art logistics market exposure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Logistics Function: Transportation Scale Meets Value-Added Sophistication

Transportation captured 60.39% of fine art logistics market share in 2025. Air freight dominates high-value transfers thanks to stringent security and rapid transit times, while bio-marine-fuel sea lanes absorb cost-sensitive exhibition shipments. Road fleets, increasingly electric inside low-emission zones, handle final-mile moves, and rail corridors link European capitals on lower carbon footprints. Warehousing and distribution provide climate-controlled bridges that support multi-stop itineraries. Value-added services are projected to grow faster than the overall fine art logistics market size, reflecting client appetite for bundled regulatory, insurance, and authentication support. IoT sensors, blockchain ledgers, and bespoke risk consulting convert once-transactional shipping jobs into multi-year stewardship contracts.

Value-added services are expected to grow the fastest with 5.45% CAGR over the forecast period. Technology investment is reshaping price structures. Smart-box leasing, online booking portals, and API connectivity with auction catalogues compress manual touchpoints. Firms that can demonstrate real-time chain-of-custody data command premiums, while those limited to legacy vans and paper manifests compete on thin margins. The divergence reinforces a two-speed Fine art logistics market, where digitally enabled providers expand EBITDA and acquisition multiples, and undigitized carriers face revenue stagnation.

By End User: Gallery Volumes Contrast with Collector Growth Trajectory

Art dealers and galleries contributed 34.87% of 2025 market share, reflecting frequent exhibition rotations and art-fair attendance. Their predictable shipping patterns allow load pooling, improving asset utilization. Auction houses cluster demand around catalog deadlines, testing rapid-response capacity each season. Museums require meticulous temperature and vibration control, often specifying packaging down to screw material to meet loan agreements aligned with ICEFAT standards[3]“ICEFAT organisation and standards for fine art transport,” International Exhibition and Fine Art Transporters, icefat.org.

Private collectors are the fastest-growing customer group, advancing at a 6.08% CAGR. Rising global wealth, fractional ownership apps, and social-media visibility of private loans drive higher service expectations. White-glove delivery, in-residence hanging, and discrete insurance administration are now table stakes. Logistics providers bundle long-term storage with concierge-style handling, converting episodic shipments into annuity income streams. Corporate collections, foundations, and digital-art platforms fall into an “others” category that demands hybrid physical-digital custody, spurring development of NFT vaults linked to climate-controlled rooms.

Geography Analysis

North America generated 42.14% of 2025 revenue, anchored by New York and Los Angeles auction ecosystems. Dense collector bases support year-round moves, while well-defined customs procedures and bonded warehouses lower regulatory friction. United States museums maintain strict conservation standards, driving premium demand for IoT-equipped crates and GPS-tracked vehicles.

Europe remains the historic crossroads of fine art trade, yet post-Brexit paperwork has lengthened UK-EU transfers, nudging some volume toward Luxembourg and Geneva freeports. Continental rail networks enable lower-carbon intra-EU routes, and strong insurer presence in London retains underwriting talent essential to the Fine art logistics market. EU regulations mandating carbon disclosure from 2027 will likely accelerate adoption of bio-fuel and electric fleets[4]“The art market sector from January 2021: guidance,” UK Government Department for Culture, Media and Sport, gov.uk.

Asia-Pacific is the fastest-growing region, expanding at a 5.55% CAGR to 2031. Hong Kong and Singapore freeports underpin tax-efficient storage, while China’s Tier-1 cities host a surging ultra-high-net-worth population. Government cultural investments in Seoul, Tokyo, and Sydney spur museum expansion, driving import flows of Western masterpieces and outbound touring shows of Asian modernists. Providers that combine Mandarin-speaking couriers with Western conservation credentials gain share.

Competitive Landscape

Competition is moderate, with the five largest operators controlling roughly 45% of global revenue. Reputation barriers, insurer approval lists, and expensive climate vaults deter new entrants. Recent M&A DHL-CRYOPDP and Horus Finance-Andera Partners signals investor appetite for specialty verticals. Technology is a clear battleground: IoT telemetry, blockchain provenance, and customer portals separate premium from commodity tiers.

Strategic partnerships proliferate. Airlines dedicate secure cool-rooms for art pallets, while shipping lines test track-and-trace boxes powered by satellite IoT. Providers court insurers by presenting granular environmental datasets, shortening claims cycles and lowering premiums. Sustainability positions also matter; carriers with verified SAF or bio-marine fuel pathways win museum tenders tied to Paris-aligned targets.

Regional specialists survive by offering ultra-high-touch services hand-carried paintings, overnight cell phone updates to collectors, and multilingual courier escorts. Some partner with global networks for inter-continental legs, creating hybrid ecosystems that extend market reach without heavy capex.

Fine Art Logistics Industry Leaders

Gander & White

Helu-Trans

Hasenkamp

Yamato Transport Co., Ltd.

DHL Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Convelio secured fresh capital and entered a strategic alliance with Phillips. The partners will open a New York storage site in Sep 2026 and add three more facilities worldwide by 2029, extending joint coverage to New York and Hong Kong and aligning logistics capacity with major auction channels.

- February 2026: Crozier signed a year-long agreement with Frieze to handle logistics for all 2026 fairs in the United States and Europe, locking in multi-event revenue and deepening ties with galleries that exhibit at several Frieze shows each season.

- January 2026: UOVO purchased Vault Fine Art Services in Central Texas, expanding its national art-storage and handling network. The deal follows UOVO’s Aug 2025 entry into the Midwest through the Artpack Detroit acquisition, reflecting a step-by-step growth plan in the United States.

- January 2026: DIETL acquired Delaware Freeport, Delaware National Art Company, Techno Export, and Registrar Technologies, integrating storage, crating, customs, and software assets across key markets in the United States. The move complements DIETL’s earlier expansion to Dubai via The Rock-It Company, creating a linked United States–Middle East logistics platform.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the fine art logistics market as every fee-based service that packs, climate-controls, stores, insures, moves across borders, installs, and de-installs paintings, sculptures, antiques, photographs, and other collectible works. We track revenue earned by specialist carriers and warehouse operators that employ trained art handlers, bespoke crating, bonded facilities, and art-specific insurance.

Scope exclusion: parcel couriers moving mass-produced décor items and transactions limited to digital-only NFTs sit outside this analysis.

Segmentation Overview

- By Logistics Function

- Transportation

- Road

- Air

- Sea and Inland Waterways

- Rail

- Warehousing and Distribution

- Value-added Services (Labelling, Kitting, Consulting)

- Transportation

- By End Users

- Art Dealers and Galleries

- Auction Houses

- Museums

- Art Fairs

- Private Collectors

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Peru

- Chile

- Argentina

- Rest of South America

- Asia Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

- Middle East And Africa

- United Arab of Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East And Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts spoke with art-fair organizers in Basel and Miami, specialist underwriters in London, and logistics managers at auction houses across Asia-Pacific. The conversations refined service-intensity ratios, average crate life, and the share of works now moved below five degrees Celsius, closing gaps left by desk work.

Desk Research

We began with public records that pin down physical flows. Customs code SITC 8997, UN Comtrade trade statistics, and the annual Art Basel-UBS art-sales survey rebuilt cross-border volumes, while museum footfall from the Association of Art Museum Directors, FAA valuable-cargo tonnage, and Lloyd's loss ratios signaled storage load and risk premia. Our team then pulled carrier filings in D&B Hoovers, news in Dow Jones Factiva, and Volza shipment ledgers to benchmark revenue. Industry journals and patent abstracts showed uptake of IoT trackers, anti-vibration crates, and low-carbon packaging. These sources are illustrative; many other open and paid repositories informed and validated our work.

Market-Sizing & Forecasting

We start top-down with global art-trade and auction proceeds, multiplying them by the validated service-intensity ratios. Select bottom-up roll-ups of twenty publicly reporting fine-art carriers test the totals. Five signals, touring-exhibition count, high-net-worth population growth, air-freight rate index, climate-controlled warehouse capacity, and digital-art sales penetration feed a multivariate regression that projects 2025-2030 values and fills missing years with three-year moving averages.

Data Validation & Update Cycle

Each draft passes two analyst reviews. Outputs are matched against new auction receipts, cargo tonnage, and carrier earnings every quarter before the annual refresh, and material shocks trigger interim updates so clients always receive the latest view.

Why Mordor's Fine Art Logistics Baseline Carries Proven Reliability

Published values often diverge because scope choices, currency timing, and refresh rhythm differ.

Key gap drivers include whether installation and insurance fees are blended, if subcontract revenue is double counted, and how rapid online art-sale growth is captured.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.88 B (2025) | Mordor Intelligence | |

| USD 5.45 B (2024) | Global Consultancy A | Includes heritage-goods logistics and insurance payouts |

| USD 4.45 B (2024) | Industry Journal B | Uses provider revenue sums without removing subcontract duplication |

Our disciplined scoping, interview-tested variables, and annual refresh cadence give decision-makers a balanced, transparent baseline they can trace and reproduce.

Key Questions Answered in the Report

How large is the Fine art logistics market in 2026?

It is projected at USD 3.35 billion, on track toward USD 4.26 billion by 2031.

What is the expected CAGR for Fine art logistics through 2031?

The market is forecast to expand at 4.94% between 2026 and 2031.

Which region is growing fastest for Fine art logistics services?

Asia-Pacific leads with a 5.55% CAGR, supported by Singapore and Hong Kong freeports and expanding collector bases.

Which customer group shows the highest growth momentum?

Private collectors, boosted by fractional ownership platforms, are advancing at a 6.08% CAGR through 2031.

What technologies differentiate leading Fine art logistics providers?

IoT-enabled climate-monitoring crates, blockchain provenance systems, and sustainable fuel programs are key differentiators.

How are sustainability goals influencing transport choices?

Clients increasingly select bio-marine-fuel sea lanes and SAF-powered air routes, rewarding providers that verify carbon reductions.

Page last updated on: