Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

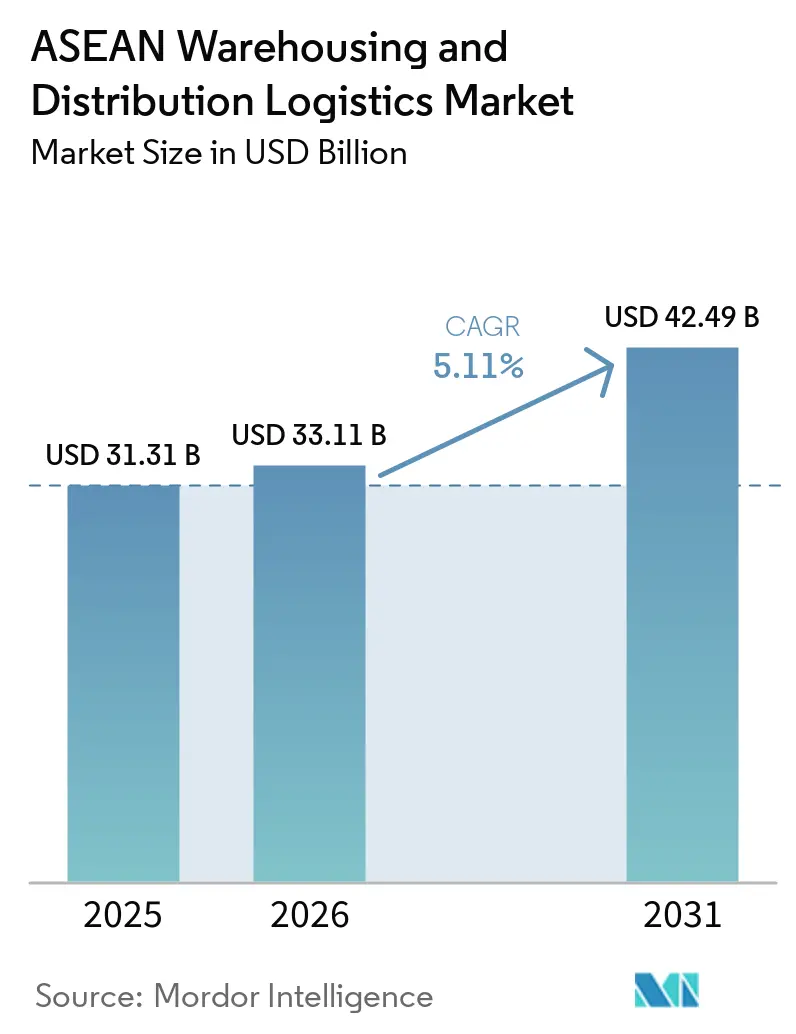

| Base Year Market Size (2025) | USD 31.31 Billion |

| Market Size (2026) | USD 33.11 Billion |

| Market Size (2031) | USD 42.49 Billion |

| Growth Rate (2026 - 2031) | 5.11% CAGR |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

ASEAN Warehousing And Distribution Logistics Market Analysis by Mordor Intelligence

The ASEAN warehousing and distribution logistics market size is expected to grow from USD 31.31 billion in 2025 to USD 33.11 billion in 2026 and is forecasted to reach USD 42.49 billion by 2031 at 5.11% CAGR over 2026-2031.

Expanding foreign direct investment, omnichannel retail adoption, and the China + 1 production pivot are reshaping warehouse footprints from export-weighted hubs into finely segmented, intra-regional networks. Operators are accelerating automation rollouts that synchronize inventory across stores, dark stores, and micro-fulfillment nodes within 15-minute refresh windows, while satellite-enabled IoT removes connectivity barriers in rural locations. Heightened ESG scrutiny is steering facility design toward on-site renewables and natural refrigerants, and vertical automation is compressing land use in congested cities. Competitive intensity has risen as e-commerce majors internalize distribution and technology-led startups introduce warehouse-as-a-service models, forcing traditional 3PLs to scale through acquisitions and specialized investments.

Key Report Takeaways

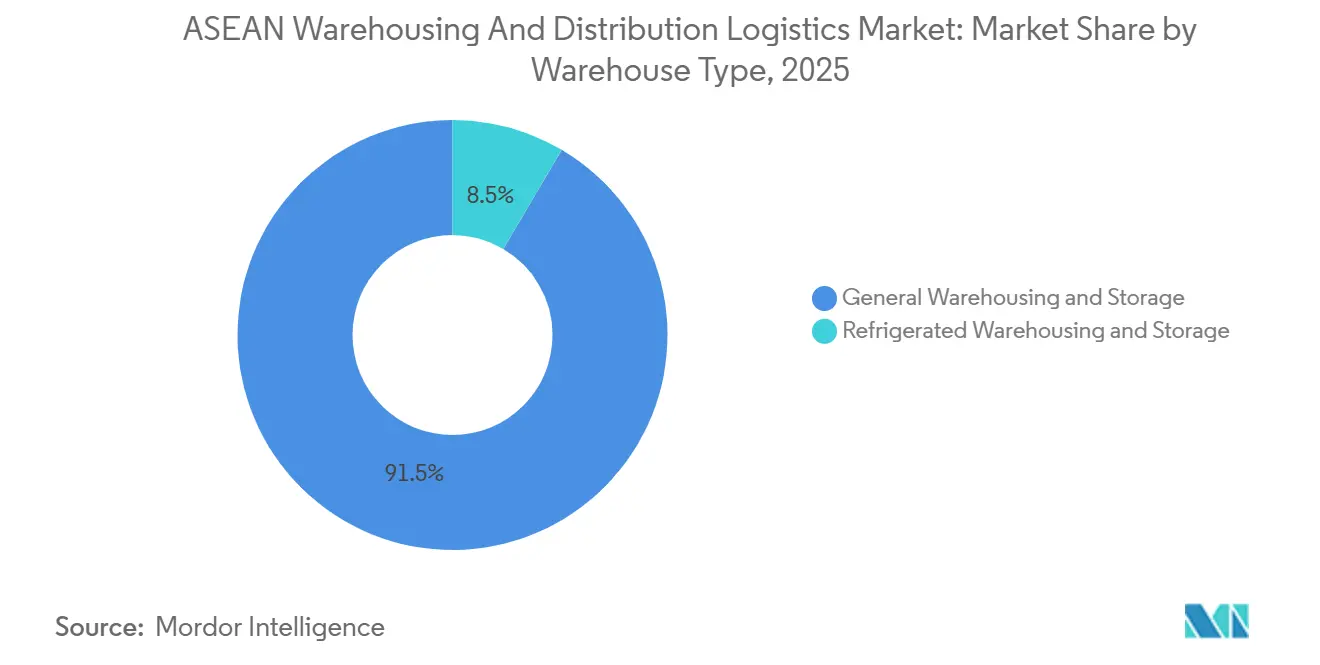

- By warehouse type, general warehousing and storage led with 91.51% of the ASEAN warehousing and distribution logistics market share in 2025; refrigerated warehousing and storage is projected to expand at a 6.09% CAGR through 2031.

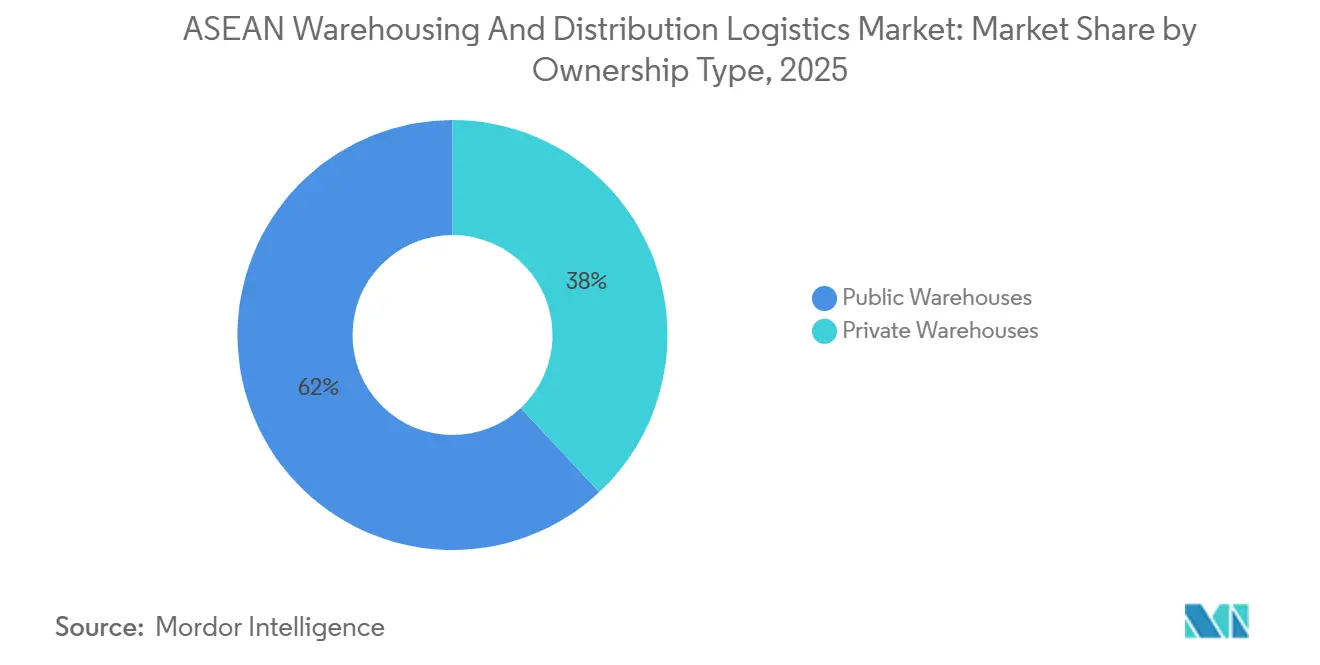

- By ownership, public warehouses accounted for 61.96% of the ASEAN warehousing and distribution logistics market size in 2025, while private facilities recorded the fastest forecast growth at 5.42% CAGR to 2031.

- By end-user industry, e-commerce and retail captured 23.03% market share in 2025; pharmaceutical and healthcare are advancing at a 6.50% CAGR through 2031.

- By country, Indonesia held 20.60% market share of the ASEAN warehousing and distribution logistics market in 2025, and Vietnam is forecast to lead growth at a 5.87% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

ASEAN Warehousing And Distribution Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Omnichannel retail surge demanding real-time inventory orchestration | +1.1% | Indonesia, Thailand, Vietnam, Philippines | Short term (≤ 2 years) |

| China + 1 manufacturing shift amplifying intra-ASEAN distribution flows | +0.9% | Vietnam, Thailand, Malaysia, Indonesia | Medium term (2-4 years) |

| Accelerated 3PL outsourcing by SMEs seeking variable-cost warehousing | +0.7% | All ASEAN member states | Short term (≤ 2 years) |

| Low-Earth-Orbit satellite IoT enabling rural warehouse connectivity | +0.5% | Indonesia, Philippines, rural ASEAN | Medium term (2-4 years) |

| Vertical automated warehousing tackling urban land scarcity | +0.6% | Singapore, Bangkok, Kuala Lumpur, Jakarta | Long term (≥ 4 years) |

| EU CBAM spurring energy-efficient facilities | +0.4% | Vietnam, Thailand, Malaysia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Omnichannel Retail Surge Demanding Real-Time Inventory Orchestration

Retailers now reconcile stock positions across 8-12 fulfillment nodes every 15 minutes to meet buy-online-pickup-in-store and same-day delivery promises. Unified commerce platforms link warehouse management, point-of-sale, and e-commerce systems, driving investments in goods-to-person robotics that cut pick times from 45 minutes to 8 minutes at 99.8% accuracy. Operators offering API-ready platforms command 18-25% price premiums because real-time visibility reduces lost sales by up to 22% while trimming safety stocks in high-velocity categories. Modern trade penetration exceeding 60% of retail sales in Thailand and Indonesia intensifies the need for facilities that process 50,000-100,000 SKUs with sub-hour latency. The premium on orchestration accelerated payback on automation to 3-4 years, compared with 5-6 years before 2024[1]"Retail Foods Annual", FAS, apps.fas.usda.gov/newgainapi/api .

China+1 Manufacturing Shift Amplifying Intra-Asean Distribution Flows

USD 239 billion in manufacturing FDI during 2024 spread production across Vietnam, Thailand, and Indonesia, triggering multi-country inventory pools that consolidate components before final assembly. Centralized regional distribution centers equipped for customs bonding and light kitting now reduce total holding costs by 20-30% while keeping 48-hour delivery promises across ASEAN. RCEP’s cumulative rules of origin further encourage cross-border component flows that rose 7.03% in 2024. Logistics providers respond with hub-and-spoke models anchored in Singapore or Malaysia, with spokes that replenish stores nightly, limiting line-haul routes to 500 kilometers and cutting carbon footprints by 12-15%[2]“Regional Comprehensive Economic Partnership (RCEP) Agreement.” ASEAN. asean.org/wp-content/uploads/2024/10/Regional-Comprehensive-Economic-Partnership-RCEP-Agreement.

Accelerated 3PL Outsourcing by SMEs Seeking Variable-Cost Warehousing

3PL penetration for SMEs jumped from 34% in 2022 to 52% in 2025 as online marketplaces enforce 24-hour fulfillment service-level agreements. Shared facilities offering 10,000-50,000 sq ft on rolling monthly contracts let SMEs avoid 3-5 year leases and USD 2-5 million fit-outs. Providers bundle inventory financing with 60-90 day terms, easing working-capital strain. SMEs report 25-35% reductions in logistics costs after outsourcing storage, picking, and last-mile to scale-driven providers. Cloud-based dashboards give real-time stock views, and mobile apps issue automated replenishment alerts when on-hand units fall below three-day cover, reducing out-of-stocks 18-20%.

Low-Earth-Orbit (LEO) Satellite IoT Enabling Rural Warehouse Connectivity

Starlink’s 150-200 Mbps packages at USD 120 per month replicate urban fiber economics in Indonesia’s outer islands and the Philippines’ provinces, enabling RFID and sensor deployment in remote warehouses. Real-time monitoring curbs inventory shrinkage by 12-18% through geofenced alerts on unauthorized pallet movement and cold-chain temperature drift. Central control towers in Jakarta or Singapore now supervise 20-30 rural sites, pooling data on temperature, humidity, and security for predictive maintenance. Agricultural exporters leverage the visibility to secure certifications for shipments to Japan and South Korea, raising rural facility utilization from 65% to 85% within two seasons.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile power supply and rising electricity tariffs inflating cold-chain OPEX | -0.7% | Indonesia, Philippines, Vietnam | Short term (≤ 2 years) |

| Port congestion and hinterland trucking bottlenecks disrupting throughput | -0.6% | Indonesia, Thailand, Vietnam, Philippines | Short term (≤ 2 years) |

| Slow adoption of ASEAN Single Window 2.0 e-customs harmonization | -0.4% | All ASEAN member states | Medium term (2-4 years) |

| Escalating cyber-attacks on warehouse management and OT systems | -0.3% | Singapore, Thailand, Malaysia, Indonesia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Power Supply and Rising Electricity Tariffs Inflating Cold-Chain OPEX

Power accounts for up to 55% of refrigerated warehouse costs, and 2024-2025 tariff hikes added 8-15% to utility bills in Indonesia and the Philippines. Grid unreliability outside Java and Luzon forces 24/7 diesel generator readiness, doubling energy costs during outages. Vietnam’s USD 0.11 per kWh industrial tariffs prompted operators to install rooftop solar systems that offset 25-30% of power draw, yet high up-front spending strains balance sheets. Temperature excursions caused by brownouts spoil pharmaceuticals, generating 3-5% inventory write-offs annually in vulnerable provinces[3]“The government is proposing a tariff of VND671 (US$0.024) per kWh for surplus power from the rooftop solar panels.” www.pv-tech.org/vietnam-to-buy-power-from-residential-and-commercial-rooftop-solar/ ..

Port Congestion and Hinterland Trucking Bottlenecks Disrupting Throughput

Container dwell times at Tanjung Priok and Manila stretched to 7-14 days in 2024, against 3-5-day global benchmarks, compelling warehouses to hold 15-20% more safety stock and inflating working capital by USD 150-250 million region-wide. Thailand’s Laem Chabang faces gate constraints that cap truck moves at 10,000 daily versus 15,000 demand, while provincial permit regimes in Vietnam fragment long-haul routes. Under-utilized truck capacity, often 45-50% versus 70-75% potential, lifts per-kilometer costs 30-40% and erodes already thin warehouse margins[4]“As of September 2024, PPA records show that yard utilization at its ports is currently at 70%.” Philippine Ports Authority, www.ppa.com.ph/node/18354 ..

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Warehouse Type: Ambient Dominance Masks Cold-Chain Acceleration

General warehousing and storage owned 91.51% of the ASEAN warehousing and distribution logistics market size in 2025, reflecting consumer-electronics, textile, and automotive part flows. Refrigerated warehousing and storage, though only 8.49% of capacity, is rising 6.09% CAGR as vaccine distribution, biologics, and temperature-sensitive foods scale. The ASEAN warehousing and distribution logistics market specialized hubs earn rental rates of USD 12-18 per sq ft monthly, triple ambient space. Hybrid sheds now integrate multi-temperature chambers, letting operators capture 18-22% premiums without separate builds while easing capacity constraints during produce peaks.

Automation lift in ambient warehouses is partly defensive, as e-commerce giants internalize large urban centers, pressuring third-party providers to differentiate through accuracy and throughput. In cold-chain, build-to-suit projects leverage natural refrigerants with 90% lower global-warming potential. DHL’s 8,200 sqm pharma hub in Singapore illustrates how GDP compliance, 2-8 °C redundancy, and 24/7 monitoring create entry barriers and justify long-term anchor leases.

By Ownership: Public Infrastructure Dominates, Private Models Gain Traction

Public warehouses held 61.96% market share in 2025 because SMEs favor pay-as-you-go terms. However, private projects grow 5.42% CAGR as high-velocity operators require bespoke automation, proprietary layouts, and data sovereignty. The ASEAN warehousing and distribution logistics market share of private facilities is projected to grow faster, driven by build-to-suit demand from electronics assemblers and grocery e-tailers. Developers secure 10-15-year leases that de-risk capital outlays, while tenants achieve unit costs 12-18% below multi-client space once volumes exceed 30 turns a year.

Public operators counter with segmented zones, dedicating parts of multi-client sheds to single tenants but preserving flexibility on contract expiry. Technology parity remains challenging, as private owners integrate autonomous mobile robots and vision-guided sorters configured for SKU-specific packaging, reducing labor by 25-35%. Variable-cost economics keep public space relevant for low-turn inventories such as slow-moving spare parts and promotional goods.

By End-User Industry: Healthcare Outpaces Retail Growth

E-commerce and retail contributed 23.03% of the 2025 market share, still the core volume anchor. Yet, pharmaceutical and healthcare warehousing posts 6.50% CAGR through 2031 due to aging populations and higher biologics use. Online-to-offline retailers now demand delivery windows under six hours in tier-one metros, forcing dense urban micro-fulfillment sites to complement regional distribution centers. The ASEAN warehousing and distribution logistics market tied to pharmaceuticals is expected to grow faster as governments extend universal healthcare coverage and biologic therapies proliferate.

Food and beverage cold-chain needs intersect with health drivers, as clean-label products require unbroken 0-4 °C chains verified via blockchain logs for exports to Japan and the EU. Automotive assembly depends on just-in-time parts kitting, especially in Thailand’s Eastern Economic Corridor, sustaining demand for synchronized inventories that feed 2-hour line-side buffers. Renewable-energy equipment and data-center hardware form a nascent but briskly expanding “others” bucket.

Geography Analysis

Vietnam’s logistics economy is projected to grow with 5.87% CAGR, supported by RCEP tariff preferences that lift intra-ASEAN parts movement 7% annually. Government targets of 9-11% logistics share of GDP and top-30 LPI status drive USD 36 billion infrastructure outlays, including new container berths that expanded 2025 seaport volumes 20%. Industrial parks in Bac Ninh and Ho Chi Minh City now standardize 10 m clear heights and 5-ton floor loads, aligning with multinational line-side requirements and pushing warehouse absorption to 95% within nine months of completion.

Indonesia, with 20.60% market share in 2025, matches scale with complexity: 17,000 islands mandate multimodal routing. Java-centric distribution is giving way to regional DCs in Kalimantan and Sulawesi as consumption patterns decentralize. Sislognas policy aims to pare logistics spend from 24% to 17% of GDP by 2030 via toll-road expansion and port digitalization. Tanjung Priok congestion triggered a Cikarang dry-port build-out that shaves two days off import clearance, freeing warehouse capacity near factories and compressing inbound-to-shelf cycles by 15%.

Thailand, Malaysia, and Singapore anchor cross-border flows. Thailand’s USD 18.3 billion Eastern Economic Corridor overhauls highway, seaport, and airport links, slotting bonded warehouses within 10 km of manufacturing zones to secure 4-hour part replenishment. Malaysia leverages Port Klang scale, with Selangor warehouses priced 35% below Singapore but offering comparable ISO-certified quality, drawing regional spare-part hubs. Singapore focuses on high-value segments - pharma, aerospace, semiconductors utilizing eight-story automated sheds that achieve five-fold density and maintain 99.99% inventory accuracy. The Philippines eyes cost reductions to 18% logistics-to-GDP by 2030; the USD 300 million New Cebu container port underpins Visayas warehouse development, easing Luzon congestion.

Competitive Landscape

The market remains moderately fragmented as global 3PLs pursue specialized verticals. GEODIS sealed the Keppel Logistics takeover to deepen its presence in pharmaceutical and e-commerce fulfillment, instantly adding 200,000 sqm capacity. DHL pledged USD 500 million for Asia-Pacific healthcare logistics, opening an 8,200 sq m Singapore facility with 15-minute temperature deviation alerts that meet GDP standards. Vertically integrated e-commerce platforms Shopee, Lazada, and Tokopedia operate more than 120 captive fulfillment centers, limiting third-party share in prime metros but partnering with regional 3PLs in secondary cities.

Startups fuel disruption. Locad’s USD 9 million raise funds an AI-driven fulfillment network providing pay-per-use capacity to SMEs, leveraging cloud WMS to pool inventories across 30 nodes. YCH Group collaborates with government entities on Vietnam SuperPort, combining rail, road, and seaport interfaces to cut transit times on Hanoi-Ho Chi Minh routes by 20%. Technology investments bifurcate the field: large players spend USD 20 million-plus on AutoStore grids and predictive demand engines, while mid-tier firms lag, risking contract erosion.

ESG differentiation grows. Equalbase’s carbon-neutral Penang site gained 95% occupancy six months post-launch, signaling tenant willingness to pay premiums for certified green space. Cyber-resilience emerges as a tender prerequisite; operators now incorporate ISO 27001 compliance and 24/7 security operations centers to reassure multinational customers wary of ransomware downtime.

ASEAN Warehousing And Distribution Logistics Industry Leaders

-

DHL Group

-

CMA CGM Group (including CEVA Logistics)

-

CJ Logistics

-

DSV A/S

-

Linfox Pty Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Nippon Express Logistics (Thailand) Co., Ltd. has upgraded its logistics systems at Don Mueang Airport in Thailand to swiftly and flexibly address diverse logistics needs, including urgent shipments, by expanding hub functions and on-site operations.

- August 2025: Binh Dinh province approved VND 12 trillion (USD 480 million) port investment to raise throughput to 19 million t by 2030, catalyzing hinterland warehouse demand.

- July 2025: J&T Express processed 14 billion parcels in H1 2025 and expanded with 700 service points and 800 line-haul vehicles across Southeast Asia.

- July 2025: Hankyu Hanshin Properties joined Sembcorp to build five warehouses totaling 240,000 sqm in Vietnam’s Dinh Vu Industrial Zone, with completion in winter 2026.

ASEAN Warehousing And Distribution Logistics Market Report Scope

By Warehouse Type (Value)

| General Warehousing and Storage |

| Refrigerated Warehousing and Storage |

By Ownership (Value)

| Private Warehouses |

| Public Warehouses |

By End-User Industry (Value)

| E-commerce and Retail |

| Food and Beverage |

| Pharma and Healthcare |

| Automotive |

| Manufacturing and Engineering Goods |

| Others |

By Geography

| Singapore |

| Thailand |

| Malaysia |

| Vietnam |

| Indonesia |

| Philippines |

| Rest of ASEAN |

| By Warehouse Type (Value) | General Warehousing and Storage |

| Refrigerated Warehousing and Storage | |

| By Ownership (Value) | Private Warehouses |

| Public Warehouses | |

| By End-User Industry (Value) | E-commerce and Retail |

| Food and Beverage | |

| Pharma and Healthcare | |

| Automotive | |

| Manufacturing and Engineering Goods | |

| Others | |

| By Geography | Singapore |

| Thailand | |

| Malaysia | |

| Vietnam | |

| Indonesia | |

| Philippines | |

| Rest of ASEAN |

Key Questions Answered in the Report

What is the projected value of the ASEAN warehousing and distribution logistics market by 2031?

It is forecast to reach USD 42.49 billion by 2031.

How fast will the market grow between 2026 and 2031?

The market is expected to register a 5.11% CAGR during the forecast period.

Which warehouse type is growing the quickest?

Refrigerated warehousing is advancing at a 6.09% CAGR through 2031, driven by pharmaceutical and food-grade demand.

Which country offers the fastest growth opportunity?

Vietnam leads with a projected 5.87% CAGR, supported by strong manufacturing FDI and infrastructure spending.

Why are SMEs outsourcing warehousing to 3PLs?

Outsourcing converts fixed facility costs into variable fees and gives SMEs cloud-based inventory visibility, cutting total logistics expenses by up to 35%.

How is the EU CBAM influencing ASEAN warehouses?

Exporters to Europe now invest in solar roofs and natural refrigerants to lower facility emissions and avoid carbon tariffs that start in 2026.

Page last updated on: