Market Overview

| Study Period | 2017 - 2030 |

|---|---|

| Market Size (2025) | USD 402.5 Billion |

| Market Size (2030) | USD 541.20 Billion |

| Growth Rate (2025 - 2030) | 6.10% CAGR |

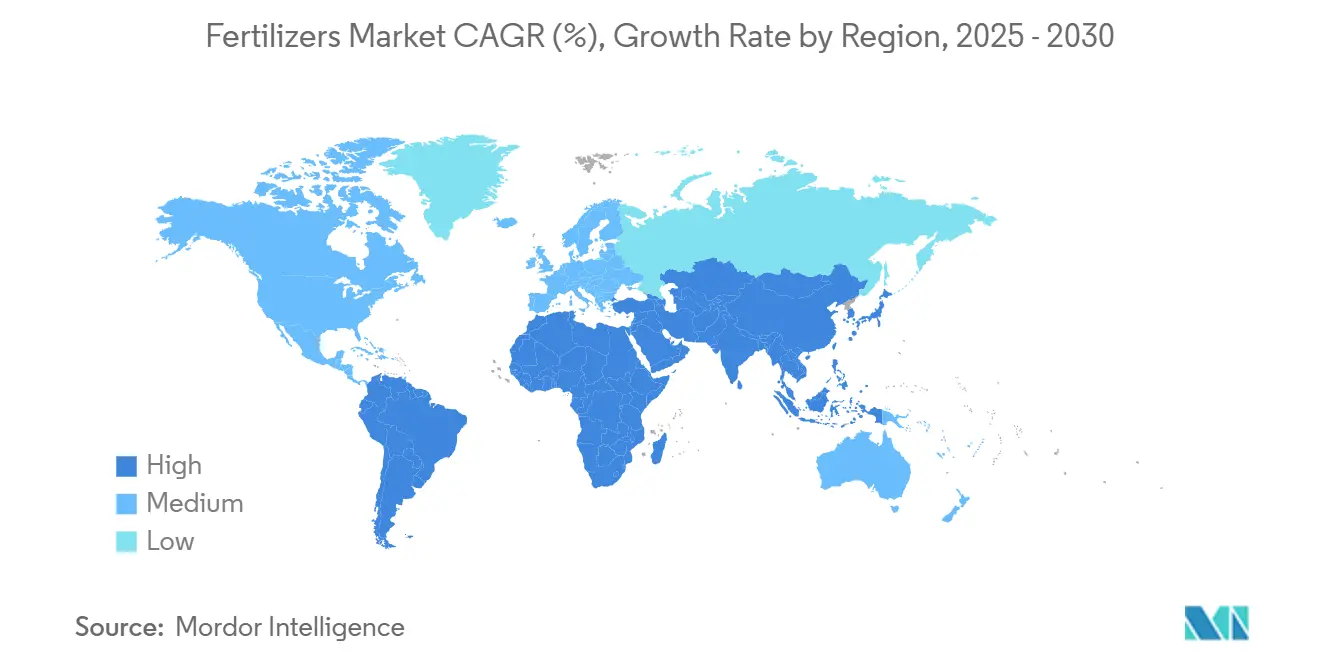

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

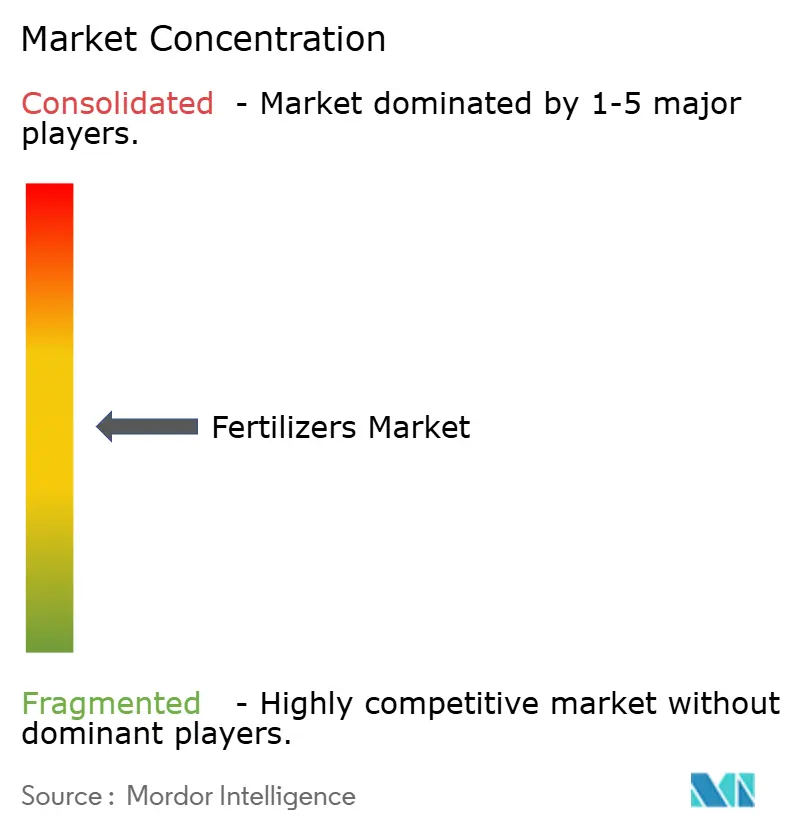

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fertilizers Market Analysis by Mordor Intelligence

The fertilizers market size is valued at USD 402.5 billion in 2025 and is forecast to reach USD 541.2 billion by 2030, reflecting a 6.1% CAGR over the period. Demand is advancing as precision agriculture technologies link data analytics with nutrient management, while specialty formulations such as controlled-release coatings extend nutrient availability and curb losses. Regional capacity additions in natural-gas-advantaged areas lower production costs and shift global trade flows, even as volatile feedstock pricing in Europe compresses margins. Government climate-smart policies spur the adoption of enhanced-efficiency fertilizers, and digitized dealer networks in emerging economies ease last-mile distribution. Carbon-credit incentives for green ammonia production create new revenue streams that reposition fertilizer companies as decarbonization partners rather than commodity suppliers.

Key Report Takeaways

- By type, straight fertilizers accounted for 73.9% of the fertilizers market share in 2024 and are projected to grow at a CAGR of 6.1% through 2030.

- By form, conventional fertilizers held 88.5% revenue share of the fertilizers market size in 2024, and specialty fertilizers are projected to post the quickest 6.2% CAGR to 2030.

- By application mode, soil application accounted for 89% share of the fertilizers market in 2024, whereas fertigation is forecast to grow at a 6.3% CAGR.

- By crop type, field crops held an 82% share of the fertilizers market in 2024, while horticultural crops are projected to expand at a 7.1% CAGR through 2030.

- By geography, Asia-Pacific captured a 43.8% share of the fertilizers market in 2024, while the Middle East and Africa are set to surge at a 7.3% CAGR through 2030.

Global Fertilizers Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Fertilizer Demand from Precision-Agriculture Projects | +1.2% | North America and Europe | Medium term (2–4 years) |

| Transition to Climate-Smart Nutrient-Management Policies | +0.9% | European Union and North America | Long term (≥ 4 years) |

| Rapid Adoption of Specialty and Slow-Release Formulations | +1.4% | Asia-Pacific | Short term (≤ 2 years) |

| Capacity Expansions in Low-Cost Natural-Gas Regions | +1.0% | Middle East, Russia, and North America | Medium term (2–4 years) |

| Digitization of Dealer Networks in Emerging Economies | +0.8% | Asia-Pacific and Africa | Medium term (2–4 years) |

| Carbon-Credit Incentives for Green Ammonia Production | +0.8% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Surge in Fertilizer Demand from Precision-Agriculture Projects

Variable-rate application hardware, yield-monitoring sensors, and drone imagery allow growers to tailor nutrient programs to within-field variability, boosting demand for fertilizers that can be metered precisely through equipment retrofits. Companies such as CF Industries Holdings, Inc. and Nutrien Ltd. now bundle remote sensing services with fertilizer supply, creating stickier customer relationships [1] “Precision Agriculture Adoption Patterns,” United States Department of Agriculture, usda.gov. Retailers report double-digit increases in tonnage linked to prescription maps that reduce overlaps and missed spots, translating to higher overall nutrient uptake efficiency even when absolute application volumes fall. The model shifts revenues from pure ton sales toward outcome-based service fees, a trend most visible among corn and soybean growers in the United States.

Transition to Climate-Smart Nutrient-Management Policies

The European Commission’s Farm to Fork strategy caps synthetic nitrogen use per hectare and rewards enhanced-efficiency fertilizers that cut nitrous oxide emissions [2] “Farm to Fork Strategy Key Facts,” European Commission, ec.europa.eu. Similar targets in Canada and select U.S. states tighten allowable nitrate runoff, prompting growers to adopt nitrification inhibitors and urease-inhibitor-coated urea that limit volatilization. Such policies lift the premium segment of the fertilizers market, especially for urea treated with dual inhibitors that can document up to 30% emissions savings in field trials.

Rapid Adoption of Specialty and Slow-Release Formulations

High-value fruit, vegetable, and greenhouse crops benefit from controlled-release fertilizers (CRF) that match nutrient release to phenological stages. Sulfur-coated and polymer-coated granules cut application labor by half in many horticultural operations, offsetting higher per metric ton prices. Demand spikes are strongest in southeastern China, Spain, and California, where water scarcity drives fertigation investments.

Digitization of Dealer Networks in Emerging Economies

Mobile-based platforms in India and Nigeria now enable smallholders to conveniently order micro-pouches of water-soluble nutrients and receive tailored, location-specific soil test recommendations. These digital tools enhance accessibility, transparency, and input efficiency. Apps continuously log transaction and usage data, which upstream manufacturers analyze to refine stocking decisions, forecast demand trends, and optimize logistics, ultimately shrinking working capital requirements and improving profitability in fragmented, underserved rural fertilizer markets.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Feedstock Prices (Natural Gas, Phosphate Rock) | -1.8% | Europe and Asia-Pacific | Short term (≤ 2 years) |

| Regulatory Caps on Nitrogen Usage in Europe | -0.7% | Europe | Medium term (2–4 years) |

| Growing Organic Farming Acreage | -0.5% | North America and Europe | Long term (≥ 4 years) |

| Supply-Chain Bottlenecks in Potash Logistics | -0.9% | Import-dependent Regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Feedstock Prices (Natural Gas, Phosphate Rock)

Benchmark gas prices in Europe tripled during early 2024, driving ammonia shutdowns and forcing spot imports into fertilizer-deficient regions. Phosphate rock costs surged on Moroccan export levies, squeezing margins for diammonium phosphate (DAP) and monoammonium phosphate (MAP) producers in India.

Growing Organic-Farming Acreage

Growing organic-farming acreage continues to restrain fertilizer market growth [3]“Organic Survey Results 2024,” United States Department of Agriculture, usda.gov. As more farmers adopt organic practices, demand for synthetic NPK fertilizers declines, replaced by composts, manures, and microbial biofertilizers emphasizing soil health and sustainability. This shift also reduces dependence on chemical fertilizers, driven by government incentives, eco-conscious consumers, and certification standards promoting environmentally friendly nutrient management practices.

Segment Analysis

By Type: Specialty Uptake Accelerates within Commodity Dominance

Straight fertilizers accounted for 73.9% of the fertilizer market size in 2024 and are projected to grow at a 6.1% CAGR through 2030. Nitrogenous products, led by urea, dominated revenue due to high nitrogen content and favorable cost-to-nutrient ratios. Phosphatic fertilizers like DAP and MAP advanced on balanced-fertilization programs in India and Southeast Asia, while MOP benefited from South American soybean expansion. Micronutrients, particularly zinc and boron, recorded the fastest growth, aided by soil testing and government extension programs. Specialty formulations, including sulfur- and polymer-coated urea, reduced leaching, and secondary macronutrients regained relevance in intensively cropped soils.

Complex fertilizers are experiencing increased adoption as subsidy disparities decrease, making them more accessible to farmers. Multi-nutrient blends cater to crop-specific requirements, ensuring optimal nutrient supply for various crops, while also addressing environmental concerns related to nitrogen overuse, such as soil degradation and water contamination. Developments in nano-encapsulation and biodegradable coatings have significantly enhanced nutrient uptake efficiency and sustainability by reducing nutrient loss and minimizing environmental impact, thereby supporting the market's growth potential.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Form: Controlled-Release Formulations Redefine Value

Conventional fertilizers accounted for 88.5% of the fertilizers market share in 2024. While traditional granular products continue to dominate volumes, specialty formulations are increasingly reshaping the market’s value composition, with specialty fertilizers projected to achieve the fastest 6.2% CAGR through 2030. Controlled-release fertilizers extend nutrient availability over 90–120 days, aligning with crop uptake cycles and lowering labor costs.

Slow-release fertilizers (SRF) are finding niches in golf courses and municipal turf, where consistent greening without burn is essential. Liquid fertilizers are gaining adoption among precision sprayer fleets, while water-soluble powders enhance fertigation efficiency in greenhouse vegetable production.

By Application Mode: Fertigation Outpaces Legacy Broadcast

By application mode, soil application accounted for 89% of the fertilizers market in 2024, whereas fertigation is forecast to grow at a 6.3% CAGR through 2030. Broadcast soil application continues to dominate tonnage, providing a cost-effective method for large-scale cereal and staple crops. However, fertigation is emerging as the fastest-growing segment, as drip and pivot irrigation systems allow growers to deliver nutrients precisely alongside water, improving nutrient-use efficiency and reducing losses.

Foliar sprays offer targeted in-season corrections, particularly for micronutrients, and their adoption is rising in high-value specialty fruit orchards, where visual quality premiums justify additional applications. The shift toward precision application methods is also supported by digital agronomy tools, remote sensing, and variable-rate nutrient delivery systems, helping farmers optimize crop nutrition and overall yields while minimizing environmental impact.

By Crop Type: Field Staples Drive Volume, Horticulture Drives Margin

By crop type, field crops held an 82% share of the fertilizers market in 2024. Cereal crops such as corn, wheat, and rice account for the bulk of nutrient demand due to large acreage, ensuring the fertilizers market remains heavily volume-driven. These crops primarily rely on conventional granular fertilizers to meet high nutrient requirements efficiently and cost-effectively.

Horticultural crops, while projected to expand at a 7.1% CAGR through 2030, increasingly adopt premium specialty formulations, raising average selling prices and supporting value growth. Turf and ornamental crops, though representing a smaller share, benefit from controlled-release fertilizers and urban greening mandates, resulting in higher per-acre spends. This combination of volume-driven field crops and high-value horticultural applications continues to shape market dynamics and innovation priorities.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

Asia-Pacific anchored the fertilizers market in 2024, accounting for 43.8% of global revenue. China’s eco-efficiency programs trim over-application yet still require approximately 50 million metric tons of annual nutrients, while India’s nutrient-based subsidy ensures farmer affordability remains a priority. Southeast Asian rice producers expand urea deep-placement pilots that reduce losses and improve yields. Collectively, these dynamics sustain the region’s dominant market position, with moderate growth projected across conventional and specialty fertilizers.

The Middle East and Africa are anticipated to record the fastest regional CAGR of 7.3% through 2030. Nigeria’s Presidential Fertilizer Initiative has revived dormant blending plants, raising domestic NPK uptake. Kenya and Ethiopia deploy mobile soil labs that recommend customized blends, stimulating micronutrient demand. Several Middle Eastern countries are expanding nitrogen and phosphate fertilizer capacities to serve both domestic and export markets. However, logistics gaps persist, and consistent subsidy funding remains a critical success factor.

North America and Europe contribute to steady but slower growth. Large-scale North American farms integrate satellite imagery and real-time weather data into application planning, boosting enhanced-efficiency fertilizers with measurable Return on Investment (ROI). Europe emphasizes environmental compliance, favoring nitrification-inhibitor-treated urea and organic conversions, which modestly temper total tonnage growth. South American soybean frontiers in Brazil and Argentina sustain high potash demand, though reliance on Canadian and Russian supply chains exposes importers to freight volatility.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The top five suppliers, Nutrien Ltd., CF Industries Holdings, Inc., Yara International ASA, The Mosaic Company, and ICL Group Ltd., accounted for a substantial revenue share in 2024, reflecting a moderately concentrated market. These companies utilize vertically integrated operations encompassing mining, production, and retail to ensure access to feedstocks and customers. Their vertical integration allows them to control critical aspects of the supply chain, from raw material extraction to final product distribution, providing a competitive advantage in terms of cost efficiency and market reach.

Strategic thrusts now revolve around sustainability and digital solutions. Nutrien Ltd. rolled out a grower-facing app that links soil test results with tailored nutrient plans, while CF Industries Holdings, Inc. is investing in green ammonia initiatives that capture carbon credits.. Yara International ASA collaborates with Microsoft on an artificial-intelligence platform that parses satellite imagery to deliver in-season recommendations.

Mid-tier innovators such as Haifa Group and Coromandel International Ltd. differentiate through specialty formulations, water-soluble grades for hydroponics, and micronutrient-infused NPKs for soil-specific deficiencies. Regional firms exploit proximity advantages, OCP Group extends Morocco’s phosphate dominance through value-added MAP downstream, and Acron Group tailors nitrate solutions to Eastern European cereals.

Fertilizers Industry Leaders

CF Industries Holdings, Inc.

ICL Group Ltd

Nutrien Ltd.

The Mosaic Company

Yara International ASA

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- November 2024: Haifa Group introduced new water-soluble fertilizer formulations specifically designed for greenhouse cucumber production, targeting the Netherlands and Belgian growers.

- July 2024: ICL Group Ltd completed the acquisition of specialty fertilizer assets from a regional competitor for USD 45 million, expanding its controlled-release fertilizer portfolio in Mediterranean markets. The transaction includes manufacturing facilities and distribution networks in Spain and Italy.

- June 2024: OCP Group commissioned a USD 1.8 billion phosphate processing complex in Morocco with 1.2 million metric tons annual capacity.

Global Fertilizers Market Report Scope

Complex, Straight are covered as segments by Type. Conventional, Speciality are covered as segments by Form. Fertigation, Foliar, Soil are covered as segments by Application Mode. Field Crops, Horticultural Crops, Turf & Ornamental are covered as segments by Crop Type. Asia-Pacific, Europe, Middle East & Africa, North America, South America are covered as segments by Region.Type

| Complex | ||

| Straight | Micronutrients | Boron |

| Copper | ||

| Iron | ||

| Manganese | ||

| Molybdenum | ||

| Zinc | ||

| Others | ||

| Nitrogenous | Ammonium Nitrate | |

| Anhydrous Ammonia | ||

| Urea | ||

| Others | ||

| Phosphatic | Diammonium Phosphate (DAP) | |

| Monoammonium Phosphate (MAP) | ||

| Single Super Phosphate (SSP) | ||

| Triple Super Phosphate (TSP) | ||

| Others | ||

| Potassic | Muriate of Potash (MoP) | |

| Sulfate of Potash (SoP) | ||

| Others | ||

| Secondary Macronutrients | Calcium | |

| Magnesium | ||

| Sulfur | ||

Form

| Conventional | |

| Speciality | Controlled Release Fertilizer (CRF) |

| Liquid Fertilizer | |

| Slow Release Fertilizer (SRF) | |

| Water Soluble |

Application Mode

| Fertigation |

| Foliar |

| Soil |

Crop Type

| Field Crops |

| Horticultural Crops |

| Turf and Ornamental |

Geography

| Asia-Pacific | Australia |

| Bangladesh | |

| China | |

| India | |

| Indonesia | |

| Japan | |

| Pakistan | |

| Philippines | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific | |

| Europe | France |

| Germany | |

| Italy | |

| Netherlands | |

| Russia | |

| Spain | |

| Ukraine | |

| United Kingdom | |

| Rest of Europe | |

| Middle East and Africa | Nigeria |

| Saudi Arabia | |

| South Africa | |

| Turkey | |

| Rest of Middle East and Africa | |

| North America | Canada |

| Mexico | |

| United States | |

| Rest of North America | |

| South America | Argentina |

| Brazil | |

| Rest of South America |

| Type | Complex | ||

| Straight | Micronutrients | Boron | |

| Copper | |||

| Iron | |||

| Manganese | |||

| Molybdenum | |||

| Zinc | |||

| Others | |||

| Nitrogenous | Ammonium Nitrate | ||

| Anhydrous Ammonia | |||

| Urea | |||

| Others | |||

| Phosphatic | Diammonium Phosphate (DAP) | ||

| Monoammonium Phosphate (MAP) | |||

| Single Super Phosphate (SSP) | |||

| Triple Super Phosphate (TSP) | |||

| Others | |||

| Potassic | Muriate of Potash (MoP) | ||

| Sulfate of Potash (SoP) | |||

| Others | |||

| Secondary Macronutrients | Calcium | ||

| Magnesium | |||

| Sulfur | |||

| Form | Conventional | ||

| Speciality | Controlled Release Fertilizer (CRF) | ||

| Liquid Fertilizer | |||

| Slow Release Fertilizer (SRF) | |||

| Water Soluble | |||

| Application Mode | Fertigation | ||

| Foliar | |||

| Soil | |||

| Crop Type | Field Crops | ||

| Horticultural Crops | |||

| Turf and Ornamental | |||

| Geography | Asia-Pacific | Australia | |

| Bangladesh | |||

| China | |||

| India | |||

| Indonesia | |||

| Japan | |||

| Pakistan | |||

| Philippines | |||

| Thailand | |||

| Vietnam | |||

| Rest of Asia-Pacific | |||

| Europe | France | ||

| Germany | |||

| Italy | |||

| Netherlands | |||

| Russia | |||

| Spain | |||

| Ukraine | |||

| United Kingdom | |||

| Rest of Europe | |||

| Middle East and Africa | Nigeria | ||

| Saudi Arabia | |||

| South Africa | |||

| Turkey | |||

| Rest of Middle East and Africa | |||

| North America | Canada | ||

| Mexico | |||

| United States | |||

| Rest of North America | |||

| South America | Argentina | ||

| Brazil | |||

| Rest of South America | |||

Need A Different Region or Segment?

Customize Now

Market Definition

- MARKET ESTIMATION LEVEL - Market Estimations for various types of fertilizers has been done at the product-level and not at the nutrient-level.

- NUTRIENT TYPES COVERED - Primary Nutrients: N, P and K, Secondary Macronutrients: Ca, Mg and S, Micronutients: Zn, Mn, Cu, Fe, Mo, B, and Others

- AVERAGE NUTRIENT APPLICATION RATE - This refers to the average volume of nutrient consumed per hectare of farmland in each country.

- CROP TYPES COVERED - Field Crops: Cereals, Pulses, Oilseeds, and Fiber Crops Horticulture: Fruits, Vegetables, Plantation Crops and Spices, Turf Grass and Ornamentals

| Keyword | Definition |

|---|---|

| Fertilizer | Chemical substance applied to crops to ensure nutritional requirements, available in various forms such as granules, powders, liquid, water soluble, etc. |

| Specialty Fertilizer | Used for enhanced efficiency and nutrient availability applied through soil, foliar, and fertigation. Includes CRF, SRF, liquid fertilizer, and water soluble fertilizers. |

| Controlled-Release Fertilizers (CRF) | Coated with materials such as polymer, polymer-sulfur, and other materials such as resins to ensure nutrient availability to the crop for its entire life cycle. |

| Slow-Release Fertilizers (SRF) | Coated with materials such as sulfur, neem, etc., to ensure nutrient availability to the crop for a longer period. |

| Foliar Fertilizers | Consist of both liquid and water soluble fertilizers applied through foliar application. |

| Water-Soluble Fertilizers | Available in various forms including liquid, powder, etc., used in foliar and fertigation mode of fertilizer application. |

| Fertigation | Fertilizers applied through different irrigation systems such as drip irrigation, micro irrigation, sprinkler irrigation, etc. |

| Anhydrous Ammonia | Used as fertilizer, directly injected into the soil, available in gaseous liquid form. |

| Single Super Phosphate (SSP) | Phosphorus fertilizer containing only phosphorus which has lesser than or equal to 35%. |

| Triple Super Phosphate (TSP) | Phosphorus fertilizer containing only phosphorus greater than 35%. |

| Enhanced Efficiency Fertilizers | Fertilizers coated or treated with additional layers of various ingredients to make it more efficient compared to other fertilizers. |

| Conventional Fertilizer | Fertilizers applied to crops through traditional methods including broadcasting, row placement, ploughing soil placement, etc. |

| Chelated Micronutrients | Micronutrient fertilizers coated with chelating agents such as EDTA, EDDHA, DTPA, HEDTA, etc. |

| Liquid Fertilizers | Available in liquid form, majorly used for application of fertilizers to crops through foliar and fertigation. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF