Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

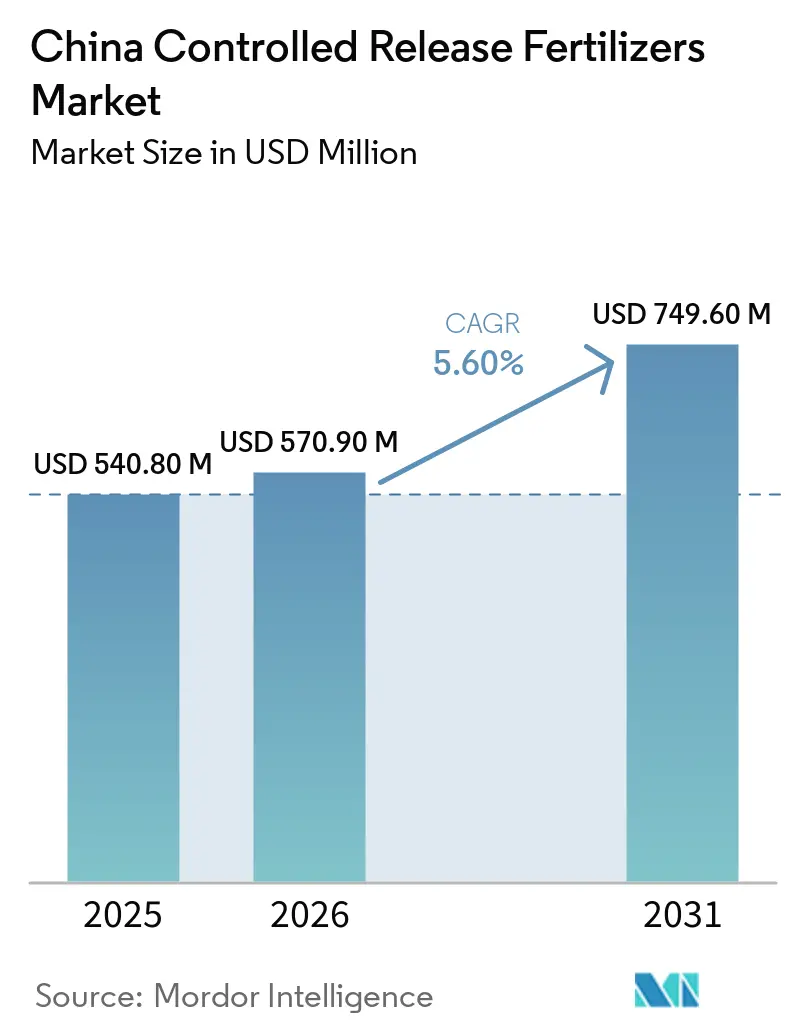

| Base Year Market Size (2025) | USD 540.80 Million |

| Market Size (2026) | USD 570.90 Million |

| Market Size (2031) | USD 749.60 Million |

| Growth Rate (2026 - 2031) | 5.60% CAGR |

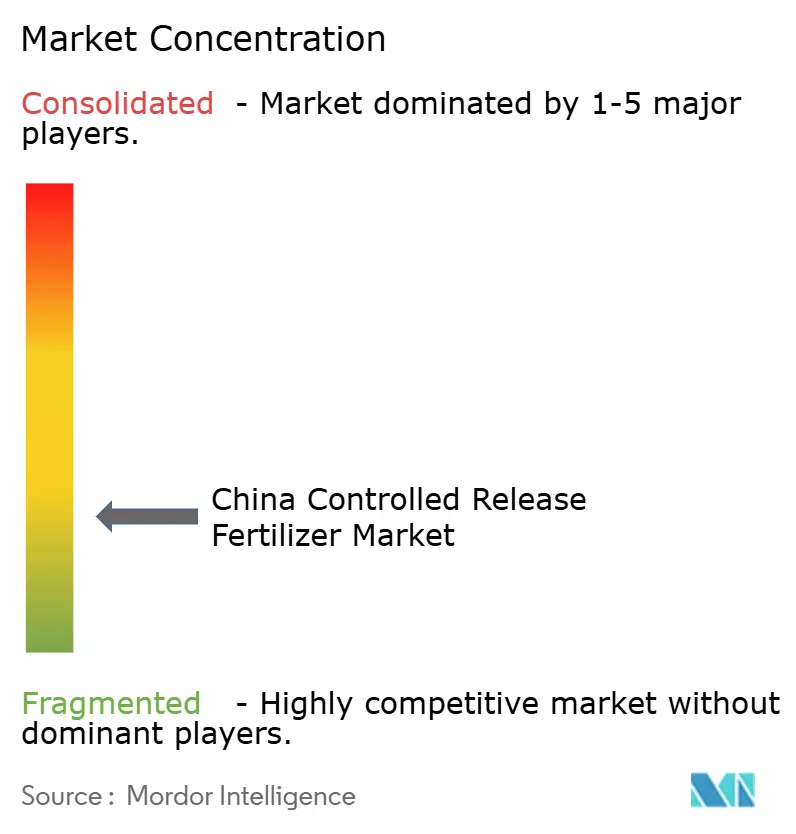

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Controlled Release Fertilizers Market Analysis by Mordor Intelligence

The China controlled release fertilizers market size was valued at USD 540.80 million in 2025 and is estimated to grow from USD 570.90 million in 2026 to USD 749.60 million by 2031, at a CAGR of 5.60% during the forecast period (2026-2031). Rising labor costs, stricter nutrient runoff regulations, and expanding eco-subsidies position the China-controlled release fertilizer market as a core enabler of the country’s precision agriculture ambitions. Polymer coatings maintain technological leadership due to reliable release profiles that improve nitrogen use efficiency by 15-20% compared with conventional urea, directly supporting national carbon-neutrality goals. Strong government support mitigates concerns about premium pricing, while e-commerce penetration improves rural access to products and accelerates adoption among smallholders. The China-controlled release fertilizer market also benefits from China’s greenhouse modernization drive, which increases demand for low-touch nutrition solutions tailored to high-value crops

Key Report Takeaways

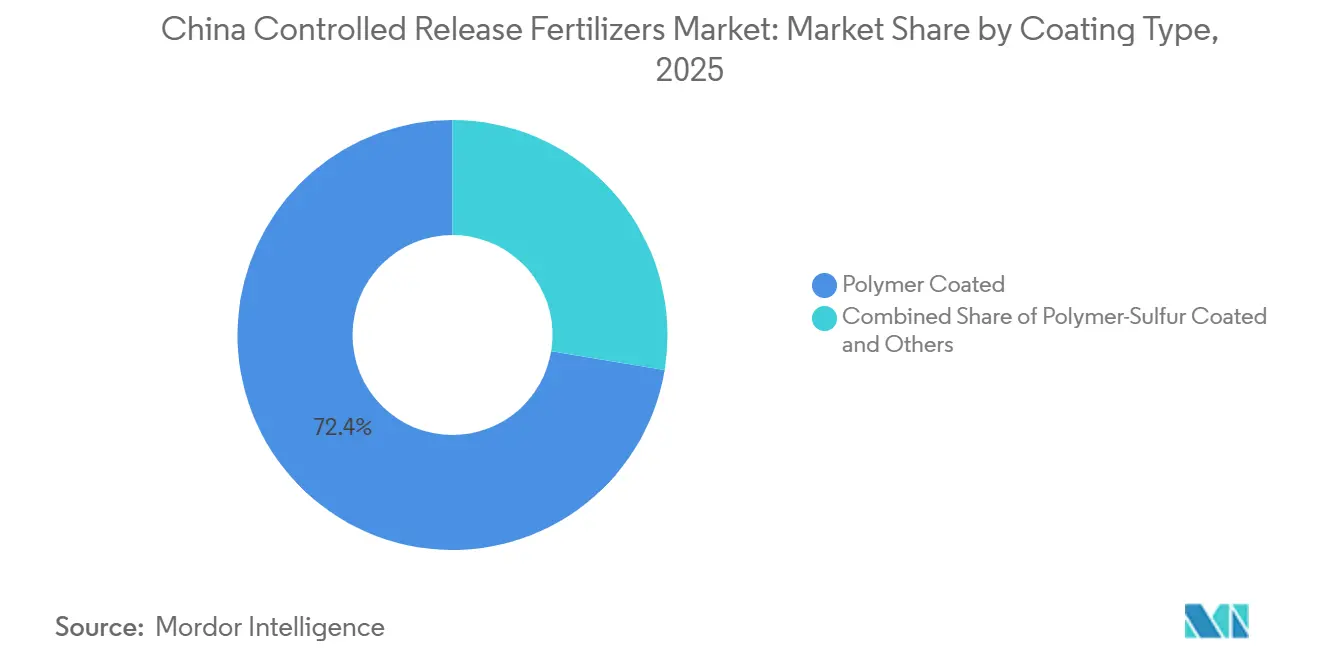

- By coating type, polymer-coated products held the largest China controlled release fertilizers market share, accounting for 72.4% in 2025, while polymer sulfur-coated products are projected to be the fastest-growing segment, expanding at a CAGR of 6.2% through 2031.

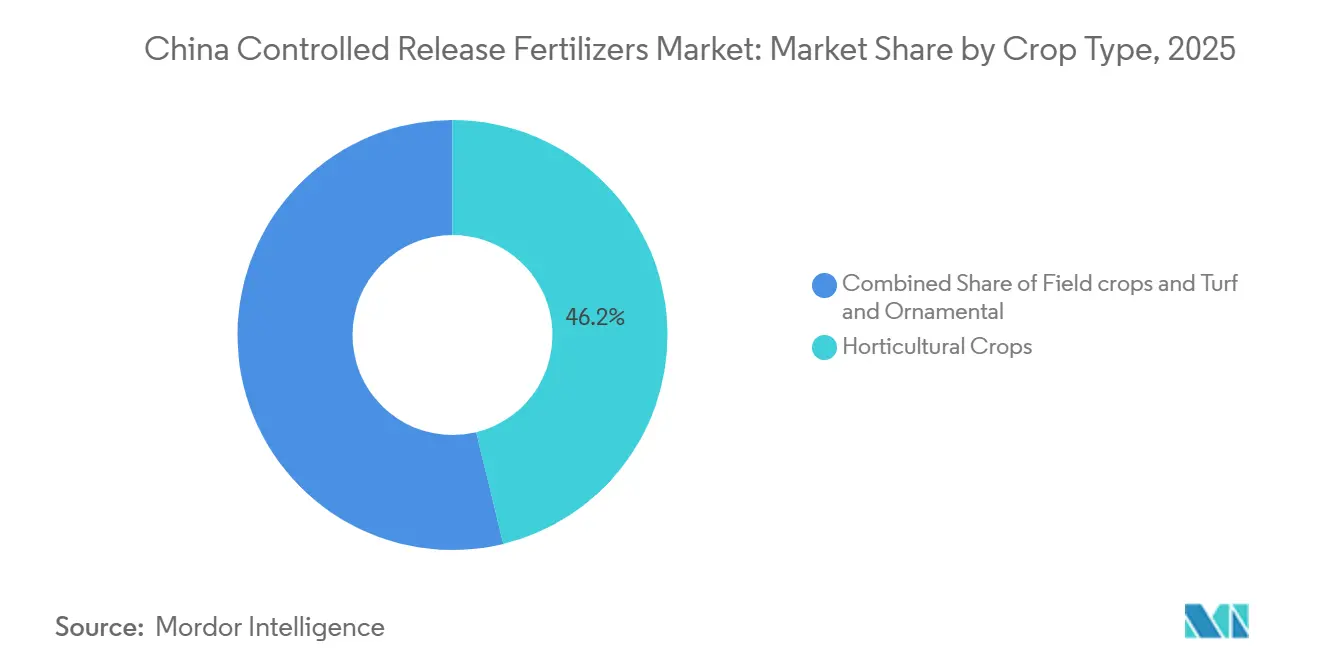

- By crop type, horticultural crops accounted for the largest China controlled release fertilizers market size in 2025, contributing 46.2% of total market revenue, whereas field crops are projected to expand the fastest, at a CAGR of 5.8% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Controlled Release Fertilizers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government eco-subsidies for efficiency fertilizers | +1.2% | National, with early gains in Jiangsu, Shandong, and Hebei | Medium term (2-4 years) |

| Rising labor costs driving mechanized, low-touch nutrition | +1.8% | National, strongest in East and Central China | Short term (≤ 2 years) |

| Tighter nutrient-runoff regulations | +1.0% | Taihu Basin, Bohai Sea region, Yellow River watershed | Long term (≥ 4 years) |

| Smart-fertigation demand for steady nutrient release | +0.9% | Xinjiang, Inner Mongolia, Northeast China | Medium term (2-4 years) |

| Carbon-credit pilots rewarding nitrogen-use efficiency | +0.7% | Pilot provinces: Hubei, Fujian, Guangdong | Long term (≥ 4 years) |

| E-commerce platforms expanding rural product access | +0.6% | Rural areas nationwide, led by Pinduoduo penetration | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government Eco-Subsidies for Efficiency Fertilizers

Central government subsidies under the Ministry of Agriculture and Rural Affairs' 2025+ framework reimburse 30% of controlled-release fertilizer costs for certified eco-farms, creating a direct economic incentive that narrows the price gap with conventional fertilizers. This policy intervention addresses the primary adoption barrier while advancing China's agricultural sustainability objectives. The subsidy mechanism operates through provincial agricultural bureaus, with Jiangsu Province leading implementation by covering over 2 million mu of rice paddies in 2024[1]Source: Ministry of Agriculture and Rural Affairs, “Agricultural Subsidy Programs 2025,” MOA.GOV.CN. The program's expansion to additional provinces in 2025 creates a multiplier effect where early adopters demonstrate yield improvements of 5-6%, encouraging neighboring farms to transition. Compliance requirements under the Green Food certification system ensure that subsidized farms maintain nutrient use efficiency standards, creating a self-reinforcing cycle of sustainable practices adoption.

Rising Labor Costs Driving Mechanized, Low-Touch Nutrition

Agricultural labor costs exceeding CNY 180 per day (USD 25) in major farming regions force growers to adopt mechanized, low-maintenance fertilization regimes where controlled-release products reduce application frequency from 3-4 times to once per season. This labor arbitrage creates compelling economics for CRF adoption, particularly in rice and corn production systems where manual broadcasting represents 15-20% of total production costs. Northeast China's large-scale farming operations demonstrate the clearest adoption patterns, with mechanized transplanting systems incorporating slow-release fertilizers achieving 25% labor cost reductions compared to conventional split applications. The trend accelerates as rural-urban migration continues, with agricultural employment declining 3% annually while remaining workers command premium wages. Smart application equipment manufacturers like Lovol and Zoomlion integrate CRF-compatible systems into their machinery offerings, creating technology lock-in effects that sustain demand growth.

Tighter Nutrient-Runoff Regulations

Implementation of strengthened GB 3838-2002 water quality standards caps nitrate runoff in sensitive watersheds, including Taihu Basin and Bohai Sea region, with enforcement penalties reaching CNY 500,000 (USD 69,000) for non-compliant agricultural operations. These regulations create regulatory pull for controlled release technologies that reduce nitrogen leaching by 40-50% compared to conventional fertilizers. The Taihu Basin's designation as a critical water protection zone requires farms to demonstrate nutrient use efficiency improvements, with controlled-release fertilizers qualifying for streamlined compliance certification. Provincial environmental protection bureaus conduct quarterly monitoring of agricultural runoff, with non-compliant operations facing production restrictions. This regulatory framework transforms controlled-release fertilizers from optional efficiency tools to compliance necessities, particularly for operations within 500 meters of water bodies where stricter standards apply.

Smart-Fertigation Demand for Steady Nutrient Release

IoT-enabled fertigation systems deployed across Xinjiang's cotton fields and Inner Mongolia's potato production require consistent nutrient release profiles that match crop uptake curves, creating technical specifications that favor controlled release formulations over conventional fertilizers. These precision agriculture systems monitor soil nutrient levels in real-time, with controlled-release fertilizers providing the steady nutrient supply needed for automated irrigation scheduling. Xinjiang Production and Construction Corps reports 12% yield improvements when combining drip irrigation with polymer-coated fertilizers compared to conventional fertigation approaches. Technology integration creates switching costs where farmers invest in compatible equipment and training, establishing long-term demand relationships with CRF suppliers. Smart agriculture action plans for 2024-2028 target 40% adoption of precision fertilization technologies, with controlled release products positioned as enabling technologies for digital farming systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium price gap versus conventional bulk NPK | -1.4% | National, the strongest impact in Central and Southwest China | Short term (≤ 2 years) |

| Limited public R&D funding for specialty coatings | -0.8% | National research institutions, university programs | Long term (≥ 4 years) |

| Pending micro-plastic coating legislation | -0.6% | National, with stricter enforcement in coastal provinces | Medium term (2-4 years) |

| Polymer-feedstock price volatility | -0.9% | Manufacturing hubs in Shandong, Jiangsu, and Hebei | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Premium Price Gap Versus Conventional Bulk NPK

Controlled-release fertilizers command 2-3 times the price of conventional bulk NPK, creating affordability barriers for smallholder farmers who operate on margins below 10% of revenue and lack access to agricultural credit for premium inputs. This price differential becomes particularly constraining during commodity price downturns when farmers prioritize cost reduction over efficiency gains. China's 200 million smallholder farming households, averaging 0.6 hectares per operation, struggle to justify CRF premiums without demonstrated yield improvements exceeding 15% [2]Source: National Bureau of Statistics, “Agricultural Census Data 2024,” STATS.GOV.CN. Regional price sensitivity varies significantly, with Central and Southwest China showing the highest resistance due to lower crop values and limited mechanization. Fertilizer cooperatives and bulk purchasing programs provide partial solutions, but coverage remains limited to 30% of eligible farms, constraining market penetration in price-sensitive segments.

Polymer-Feedstock Price Volatility

Raw material costs for polymer coatings, particularly EVA and polyurethane resins, experienced 28% price swings in 2024 due to petroleum price volatility and supply chain disruptions, creating margin pressure for CRF manufacturers and pricing uncertainty for farmers planning seasonal purchases. This volatility stems from China's dependence on imported polymer feedstocks, with domestic production meeting only 60% of coating material demand. Manufacturers struggle to maintain stable pricing contracts with distributors when input costs fluctuate monthly, leading to shortened contract terms and reduced farmer adoption confidence. The constraint intensifies during peak application seasons when demand surges coincide with global polymer market tightness. Strategic inventory management and long-term supply contracts provide partial hedging, but smaller CRF producers lack the scale to secure favorable feedstock arrangements, creating competitive disadvantages that limit market development.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Polymer-Coated Products Lead, Polymer Sulfur-Coated Expands Rapidly

The polymer-coated fertilizer segment dominates the Chinese controlled-release fertilizer market, commanding about 72.4% market share in 2025. This segment's prominence stems from its superior ability to regulate nutrient release through tailored coating characteristics, thickness, and material ratios aligned with specific crop needs. Within this category, polymer-coated urea fertilizer has emerged as the leading variant, particularly valued for its nitrogen efficiency and potential to reduce nitrogen fertilizer use by 30% to 40%.

Polymer sulfur-coated products are projected to be the fastest-growing coating type, with a projected CAGR of 6.2% through 2031. This growth is driven by lower coating costs and the ability to provide extended nutrient release for broad-acre crops. Additionally, polymer-coated fertilizers maintain a strong market position due to increasing adoption in horticultural and ornamental crops, where precise nutrient-release requirements and environmental considerations are essential. Advancements in coating technologies and materials continue to enhance the market by enabling manufacturers to optimize yields while addressing environmental sustainability.

By Crop Type: Horticultural Precision Drives Growth

Horticultural crops accounted for the largest China controlled-release fertilizers market size in 2025, contributing 46.2% of total market revenue. This dominance is attributed to the intensive production of fruits, vegetables, flowers, and other high-value crops that require precise nutrient management. The segment benefits from the increasing adoption of controlled-release fertilizers in protected cultivation systems, where priorities include nutrient-use efficiency, crop quality, and environmental performance. While turf and ornamental crops account for a smaller China controlled-release fertilizers market share, they continue to generate demand, driven by urban landscaping projects, public parks, and ornamental plant nurseries.

Field crops are projected to be the fastest-growing crop segment, expanding at a CAGR of 5.8% through 2031. This growth is supported by China's grain security objectives and the expanding use of controlled-release fertilizers in rice, corn, and wheat production. Adoption is particularly notable in major grain-producing provinces such as Heilongjiang, Hunan, and Jiangxi, where timed-release fertilizers help reduce overall fertilizer consumption while maintaining crop yields. A single application of these fertilizers can supply nutrients throughout the growing season, providing labor savings and enhancing nutrient-use efficiency for large-scale farming operations.

Geography Analysis

East China leads market development with the highest adoption rates and technological sophistication, driven by intensive agricultural systems in Jiangsu, Zhejiang, and Shandong provinces, where high crop values justify controlled-release fertilizer premiums. The region's proximity to manufacturing centers and advanced distribution networks creates favorable economics for CRF adoption, with farmers accessing technical support and financing options unavailable in remote regions. Jiangsu Province's mechanized rice transplanting program covering over 6 million mu demonstrates the region's leadership in precision agriculture adoption, with controlled-release fertilizers integrated into automated planting systems .

Central China, encompassing Henan, Hubei, and Hunan provinces, shows strong growth potential driven by grain production modernization and government subsidies targeting food security objectives. The region's large-scale farming operations increasingly adopt controlled-release fertilizers for corn and rice production, with Henan Province's 10 million-hectare grain production area representing a significant market opportunity. Water quality protection initiatives in the Yangtze River basin create regulatory drivers for CRF adoption, with controlled release technologies helping farmers comply with nutrient runoff limitations while maintaining productivity.

South China's subtropical climate and intensive cropping systems create unique opportunities for controlled release fertilizers, particularly in Guangdong and Guangxi provinces, where year-round production cycles demand consistent nutrient supply. The region's fruit and vegetable production benefits from extended-release formulations that reduce application frequency in high-rainfall environments where conventional fertilizers face leaching losses. Southwest China, including Sichuan and Yunnan provinces, represents an emerging market where mountainous terrain and smallholder farming systems challenge traditional fertilizer distribution, creating opportunities for controlled release products that reduce application labor requirements.

Competitive Landscape

The Chinese controlled-release fertilizer market exhibits a fragmented structure with top players including Hebei Woze Wufeng Biological Technology Co., Ltd, Grupa Azoty S.A. (Compo Expert), Hebei Sanyuanjiuqi Fertilizer Co., Ltd., and Zhongchuang Xingyuan Chemical Technology co, ltd, characterized by the strong presence of domestic manufacturers alongside international players. Local companies leverage their deep understanding of regional agricultural practices and established distribution networks to maintain competitive positions, while global players bring advanced technologies and international expertise. The market demonstrates a balanced mix of specialized fertilizer manufacturers and diversified agricultural input companies, with domestic players particularly strong in serving the field crops segment.

Strategic patterns reveal technology-driven differentiation where companies invest heavily in coating innovations and application-specific formulations to command premium pricing and customer loyalty. Patent filings in biodegradable coatings and precision release mechanisms indicate industry focus on environmental sustainability and performance optimization.

The competitive landscape shows limited consolidation activity, with companies primarily focusing on organic growth strategies rather than mergers and acquisitions. Market participants are increasingly emphasizing vertical integration to control quality and costs throughout the value chain. The presence of both state-owned enterprises and private companies creates a dynamic competitive environment, with different players adopting varied approaches to market penetration and customer engagement. International companies often enter the market through joint ventures or partnerships with local players to navigate regulatory requirements and establish market presence.

China Controlled Release Fertilizers Industry Leaders

Hebei Woze Wufeng Biological Technology Co., Ltd

Grupa Azoty S.A. (Compo Expert)

Hebei Sanyuanjiuqi Fertilizer Co., Ltd.

Zhongchuang xingyuan chemical technology co.ltd

ICL Group Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Kingenta Ecological Engineering Group had significantly expanded its nationwide controlled-release fertilizer demonstration and promotion efforts, with its bio-based coated CRF technology having won a national innovation award in June 2024.

- December 2024: Kingenta Ecological Engineering Group announced a strategic partnership with China Agricultural University to develop next-generation biodegradable coating technologies for controlled-release fertilizers. The collaboration includes a CNY 50 million (USD 7 million) research investment over 3 years, focusing on chitosan and PLA-based coating systems that address environmental concerns about polymer residues.

China Controlled Release Fertilizers Market Report Scope

The China Controlled Release Fertilizers Market is Segmented by Coating Type (Polymer Coated, Polymer-Sulfur Coated, and Others) and by Crop Type (Field Crops, Horticultural Crops, and Turf and Ornamental). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons)

Coating Type

| Polymer Coated |

| Polymer-Sulfur Coated |

| Others |

Crop Type

| Field Crops |

| Horticultural Crops |

| Turf & Ornamental |

| Coating Type | Polymer Coated |

| Polymer-Sulfur Coated | |

| Others | |

| Crop Type | Field Crops |

| Horticultural Crops | |

| Turf & Ornamental |

Market Definition

- MARKET ESTIMATION LEVEL - Market Estimations for various types of fertilizers has been done at the product-level and not at the nutrient-level.

- NUTRIENT TYPES COVERED - Urea & Complex

- AVERAGE NUTRIENT APPLICATION RATE - This refers to the average volume of nutrient consumed per hectare of farmland in each country.

- CROP TYPES COVERED - Field Crops: Cereals, Pulses, Oilseeds, and Fiber Crops Horticulture: Fruits, Vegetables, Plantation Crops and Spices, Turf Grass and Ornamentals

| Keyword | Definition |

|---|---|

| Fertilizer | Chemical substance applied to crops to ensure nutritional requirements, available in various forms such as granules, powders, liquid, water soluble, etc. |

| Specialty Fertilizer | Used for enhanced efficiency and nutrient availability applied through soil, foliar, and fertigation. Includes CRF, SRF, liquid fertilizer, and water soluble fertilizers. |

| Controlled-Release Fertilizers (CRF) | Coated with materials such as polymer, polymer-sulfur, and other materials such as resins to ensure nutrient availability to the crop for its entire life cycle. |

| Slow-Release Fertilizers (SRF) | Coated with materials such as sulfur, neem, etc., to ensure nutrient availability to the crop for a longer period. |

| Foliar Fertilizers | Consist of both liquid and water soluble fertilizers applied through foliar application. |

| Water-Soluble Fertilizers | Available in various forms including liquid, powder, etc., used in foliar and fertigation mode of fertilizer application. |

| Fertigation | Fertilizers applied through different irrigation systems such as drip irrigation, micro irrigation, sprinkler irrigation, etc. |

| Anhydrous Ammonia | Used as fertilizer, directly injected into the soil, available in gaseous liquid form. |

| Single Super Phosphate (SSP) | Phosphorus fertilizer containing only phosphorus which has lesser than or equal to 35%. |

| Triple Super Phosphate (TSP) | Phosphorus fertilizer containing only phosphorus greater than 35%. |

| Enhanced Efficiency Fertilizers | Fertilizers coated or treated with additional layers of various ingredients to make it more efficient compared to other fertilizers. |

| Conventional Fertilizer | Fertilizers applied to crops through traditional methods including broadcasting, row placement, ploughing soil placement, etc. |

| Chelated Micronutrients | Micronutrient fertilizers coated with chelating agents such as EDTA, EDDHA, DTPA, HEDTA, etc. |

| Liquid Fertilizers | Available in liquid form, majorly used for application of fertilizers to crops through foliar and fertigation. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms