EMEA Secondary Macronutrients Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

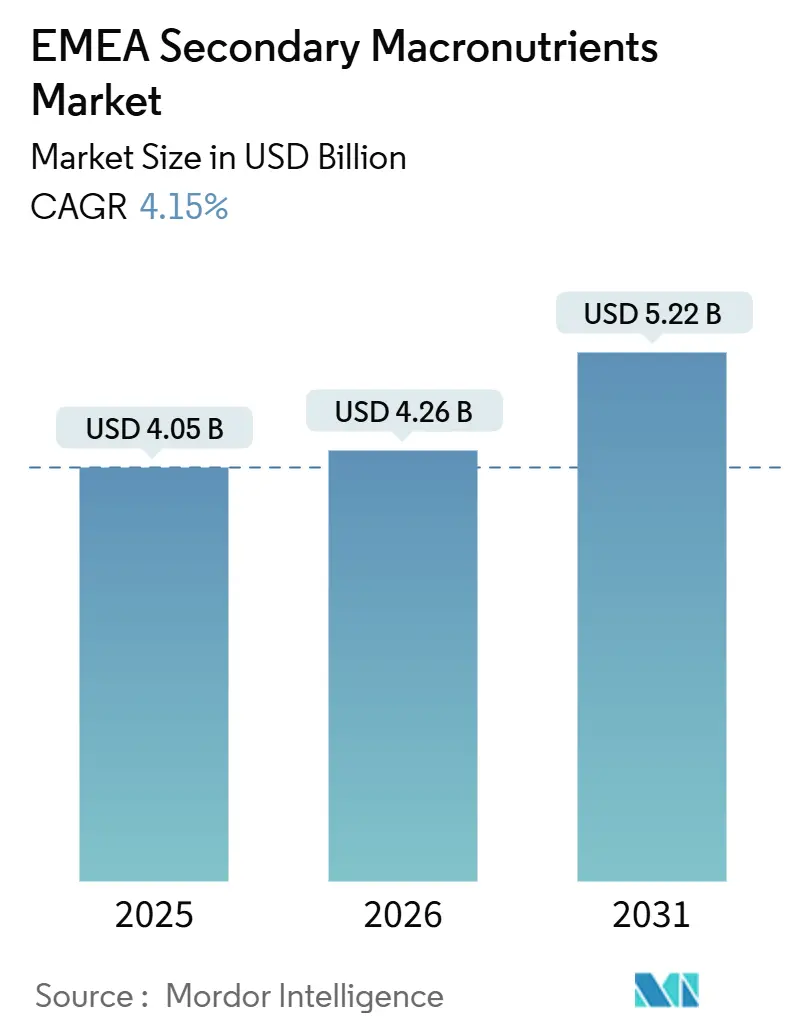

| Base Year Market Size (2025) | USD 4.05 Billion |

| Market Size (2026) | USD 4.26 Billion |

| Market Size (2031) | USD 5.22 Billion |

| Growth Rate (2026 - 2031) | 4.15% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Europe |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

EMEA Secondary Macronutrients Market Analysis by Mordor Intelligence

The EMEA secondary macronutrients market size was valued at USD 4.05 billion in 2025 and estimated to grow from USD 4.26 billion in 2026 to reach USD 5.22 billion by 2031, at a CAGR of 4.15% during the forecast period (2026-2031). The EMEA secondary macronutrients market is experiencing notable shifts due to an increasing emphasis on sustainable and modern farming practices. Agricultural operations in the region are progressively adopting environmentally conscious methods, influenced by stricter certification and regulatory requirements for fertilizer nutrient products, including both synthetic and alternative inputs. An example of this trend is the approval of products such as polysulfate for wider agricultural use by the European Union and the United States Department of Agriculture, highlighting the industry's adaptation to changing consumer preferences. Growing awareness of soil nutrient health and environmental impact has driven the adoption of balanced plant nutrition management practices, particularly in European countries where regulatory frameworks actively promote sustainable agriculture. Additionally, farmers are increasingly employing precision agriculture techniques, facilitating more targeted and efficient application of secondary macronutrients.

Key Report Takeaways

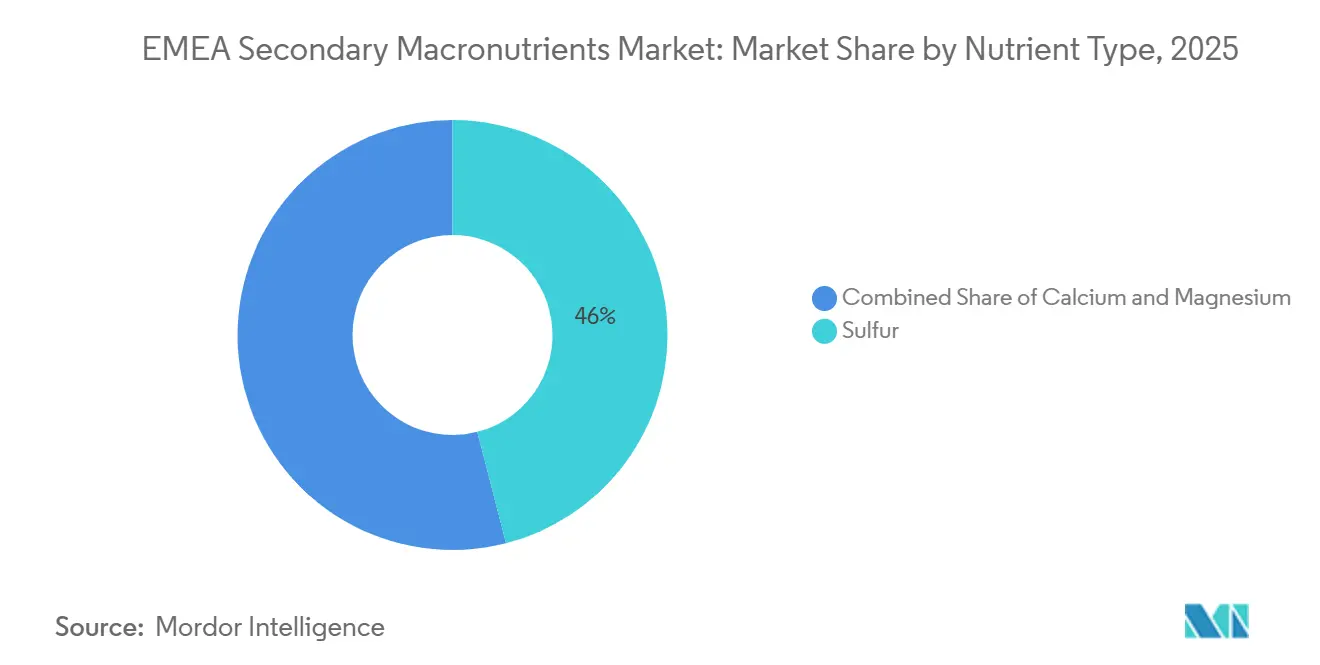

- By nutrient type, sulfur accounted for the largest share, 46.0% of the EMEA secondary macronutrients market size in 2025, while magnesium is the fastest-growing, with a projected CAGR of 6.9% from 2026 to 2031.

- By application method, solid formulations accounted for the largest segment at a 61.0% of the EMEA secondary macronutrients market share in 2025 whereas liquids are the fastest-growing, forecast to expand at an 8.4% CAGR during 2026-2031.

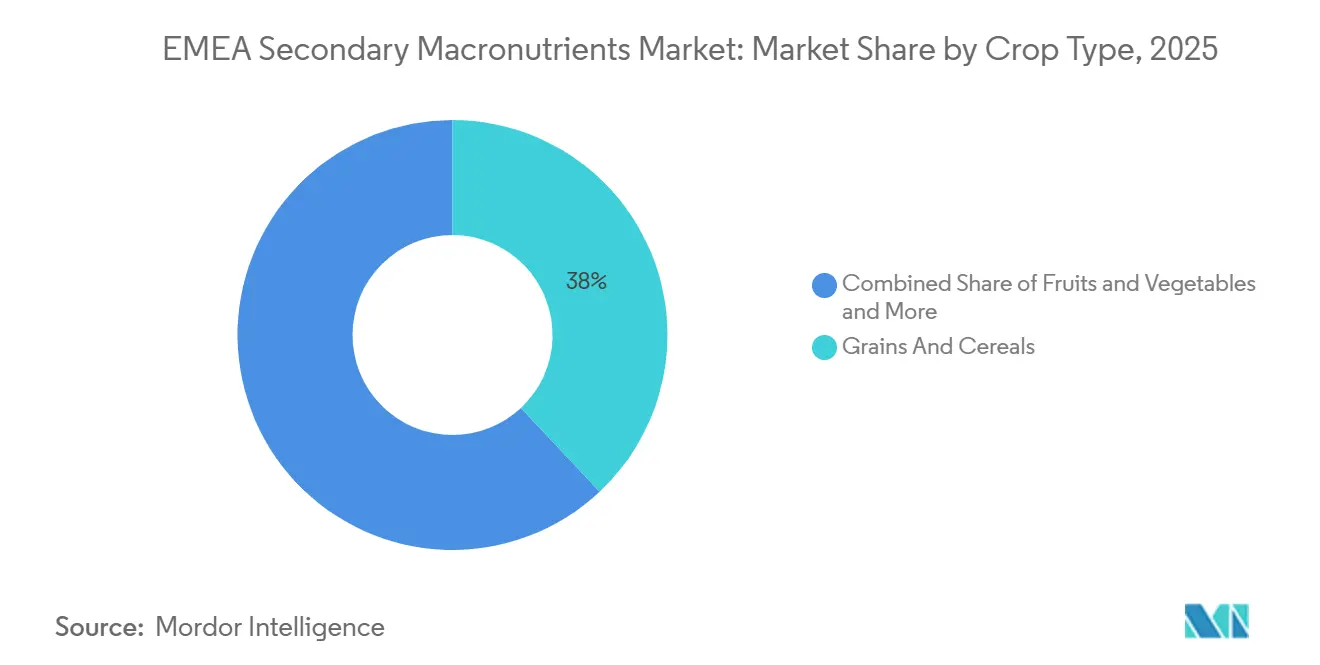

- By crop type, grains and cereals held the largest segment 38.0% EMEA secondary macronutrients market in 2025, yet fruits and vegetables are the fastest-growing, projected to grow at a 7.3% CAGR to 2026-2031.

- By geography, Europe accounted for 54.0% of EMEA secondary macronutrients market in 2025 while the Middle East is the fastest-growing region, set to register a 7.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

EMEA Secondary Macronutrients Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Soil sulfur depletion in high-yield European cereal belts | +1.2% | Germany, France, United Kingdom, and Poland | Medium term (2-4 years) |

| European Union Green Deal pushing balanced fertilization compliance | +0.9% | European Union, and spillover into North Africa exporters | Long term (≥ 4 years) |

| Expansion of controlled-environment agriculture in GCC countries | +1.4% | Saudi Arabia, United Arab Emirates, Kuwait, Qatar, and Oman | Short term (≤ 2 years) |

| Magnesium deficiency issues under LED horticulture lighting | +0.7% | Netherlands, Israel, and United Arab Emirates greenhouse clusters | Medium term (2-4 years) |

| Oil and gas desulfurization creating plentiful low-cost elemental sulfur | +1.0% | Gulf refineries, Europe and Africa import corridors | Short term (≤ 2 years) |

| Digital variable-rate technology boosting site-specific secondary nutrient use | +0.8% | Germany, United Kingdom, and France, pilot sites in South Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

European Union Green Deal Pushing Balanced Fertilization Compliance

The European Commission targets a 20% drop in nutrient losses by 2030, and national regulators have extended compliance auditing to include sulfur, calcium, and magnesium[1]Source: European Commission, “Farm to Fork Strategy,” ec.europa.eu. The February 2026 RENURE amendment lets processed manure qualify as high quality fertilizer, tightening synthetic nitrogen ceilings and raising demand for high-efficiency secondary macronutrients that deliver crop-specific doses without breaching nitrogen caps. Germany now mandates soil tests every six years, steering growers toward calcium ammonium nitrate blends containing 4% magnesium oxide. This policy triad combines cash incentives, legal requirements, and residue scrutiny to accelerate balanced nutrient adoption throughout the EMEA secondary macronutrients market.

Magnesium Deficiency Issues Under LED Horticulture Lighting

Light-emitting diode arrays shift crop physiology and raise magnesium demand. A 2025 study showed diffusive greenhouse covers boosted calcium and magnesium in asparagus spears, and Dutch tomato growers recorded classic magnesium deficiency interveinal chlorosis in older leaves within weeks of converting from high-pressure sodium lamps. Israel increased magnesium guidelines by 15-20% for LED-lit crops. Haifa Group reformulated Magnisal with a higher magnesium-to-nitrogen ratio, and K+S promotes kieserite as a slow-release option for open fields. Because magnesium drives chlorophyll synthesis, quality-minded greenhouse producers see immediate visual gains from balanced feeds, fueling segment acceleration within the EMEA secondary macronutrients market.

Oil and Gas Desulfurization Creating Low-Cost Elemental Sulfur

Oil and gas desulfurization plays a significant role in driving the EMEA secondary macronutrients market by producing large quantities of low-cost elemental sulfur as a byproduct. Strict environmental regulations across Europe, the Middle East, and Africa mandate the removal of sulfur compounds from refineries and natural gas processing plants to reduce emissions, particularly sulfur dioxide. This process, primarily achieved through hydrodesulfurization, enables the recovery of elemental sulfur, which is subsequently utilized in agriculture. The availability of abundant and cost-effective sulfur makes it a valuable input for manufacturing sulfur-based fertilizers, such as ammonium sulfate and gypsum.

Digital Variable-Rate Technology Boosting Site-Specific Use

Digital variable-rate technology is a key driver in the EMEA secondary macronutrients market, facilitating precise, site-specific application of nutrients such as sulfur, calcium, and magnesium. By leveraging GPS mapping, soil testing data, remote sensing, and advanced farm management software, farmers can assess nutrient variability within fields and apply secondary macronutrients only where required and in optimal amounts. This targeted method enhances nutrient use efficiency, minimizes input waste, and improves crop performance, particularly in regions with diverse soil conditions across Europe and parts of Africa.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Preference for NPK bulk blends over standalone secondary nutrients | -0.6% | Sub-Saharan Africa and Eastern Europe | Medium term (2-4 years) |

| Premium pricing for liquid calcium and magnesium formulations | -0.5% | European and Middle Eastern greenhouse hubs | Short term (≤ 2 years) |

| Rising demand for organic produce limiting synthetic fertilizer use | -0.7% | Germany, France, Italy, and spillover to North Africa | Long term (≥ 4 years) |

| Supply-chain volatility for sulfur linked to refining capacity cuts | -0.4% | Europe import corridors and Middle East exports | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Preference for NPK Bulk Blends Over Standalone Secondary Nutrients

The increasing preference for NPK bulk blends over standalone secondary nutrients is limiting the growth of the EMEA secondary macronutrients market. This trend reduces the direct consumption of individual products such as sulfur, calcium, and magnesium. Farmers are opting for blended fertilizers that combine nitrogen (N), phosphorus (P), and potassium (K) with secondary nutrients in a single application. This approach simplifies farming operations, reduces labor costs, and ensures balanced nutrient delivery. Consequently, the demand for separately applied secondary macronutrient products is declining, particularly in large-scale farming systems where efficiency and cost optimization are priorities.

Rising Demand for Organic Produce Limiting Synthetic Fertilizer Use

The increasing demand for organic produce is reducing the use of synthetic fertilizers, thereby constraining the growth of the conventional secondary macronutrients market in the EMEA region. As consumers increasingly prefer chemical-free, sustainably grown food, farmers are adopting organic farming practices that minimize synthetic inputs, such as chemically processed sulfur, calcium, and magnesium fertilizers. This shift has resulted in reduced consumption of conventional secondary macronutrients, especially in European countries with strict organic certification standards. According to "The World of Organic Agriculture in 2025," organically farmed land in Europe remains stable at 19.6 million hectares. Of this, 18.1 million hectares are within the European Union, where organic farming accounts for 11.1% of total agricultural land, compared to 3.9% across the entire continent[2]Source: FiBL, “Europe organic farmland statistics,” fibl.org.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Nutrient Type: Sulfur Dominance Masks Magnesium Momentum

Sulfur held the largest segment, 46.0% of the EMEA secondary macronutrients market size in 2025, reflecting its dual role as protein-synthesis catalyst and soil-pH corrector in alkaline zones across Spain, Morocco, and Egypt. Sulfur's role in enhancing chlorophyll formation and improving nitrogen use efficiency makes it essential for crops like oilseeds and cereals, where its deficiency can adversely affect yield and quality. The widespread sulfur deficiency in intensively cultivated soils across Europe has significantly increased demand for sulfur. Continuous cropping practices and reduced atmospheric sulfur deposition have depleted natural soil sulfur levels, prompting farmers to increasingly adopt sulfur-based fertilizers to restore nutrient balance and sustain soil productivity.

Magnesium is the fastest-growing, projected to grow at a 6.9% CAGR through 2026-2031, driven by LED lighting in greenhouses, which alters magnesium uptake kinetics. Calcium stays pivotal because greenhouse tomatoes and peppers rely on calcium nitrate to prevent blossom-end rot without adding nitrate to already saturated feeding schedules. Together, the three nutrients illustrate a mix of volume stability for sulfur and value-based upside for magnesium and calcium.

By Application Method: Liquid Formulations Gain in Controlled Environments

Solid formulations represented the largest segment, capturing 61.0% of the EMEA secondary macronutrients market share in 2025. This dominance is attributed to their ease of handling, extended shelf life, and compatibility with conventional farming equipment. Granular and powdered forms of sulfur, calcium, and magnesium are commonly applied through broadcasting or blending with bulk fertilizers, making them well-suited for large-scale agricultural operations. Farmers in regions with extensive cereal cultivation often prefer solid fertilizers for their seamless integration into routine soil application practices, which ensure uniform nutrient distribution at lower cost.

Liquids are the fastest-growing, forecast to expand at an 8.4% CAGR through 2026-2031, driven by the increasing adoption of precision agriculture and fertigation systems. Liquid secondary macronutrients enable precise, site-specific application and faster nutrient absorption by plants, making them particularly effective for high-value crops such as fruits and vegetables. Greenhouse growers and drip-irrigated farms in parts of Southern Europe are increasingly utilizing liquid calcium and magnesium solutions to address nutrient deficiencies in real time. This trend toward efficiency, flexibility, and advanced farming techniques is projected to drive significant growth in the liquid segment over the coming years.

By Crop Type: Horticulture Exports Propel Fruits and Vegetables

Grains and cereals held the largest segment, 38.0% of the EMEA secondary macronutrients market in 2025. This dominance is attributed to their extensive cultivation area and the consistent requirement for nutrients such as sulfur, calcium, and magnesium to support high-yield production. Staple crops like wheat, barley, and maize depend on balanced nutrient management to ensure proper growth, protein formation, and yield stability. For instance, sulfur application in wheat is crucial for enhancing grain protein content and baking quality, making secondary macronutrients an essential input for large-scale cereal farming across Europe and parts of Africa.

Fruits and vegetables are the fastest-growing, projected to grow at a 7.3% CAGR to 2026-2031, driven by rising consumer demand for high-quality, nutrient-rich, and fresh produce. These crops are more sensitive to nutrient deficiencies and require precise and frequent application of secondary macronutrients to improve attributes such as size, color, shelf life, and taste. Calcium is critical for preventing disorders like blossom-end rot in tomatoes and for enhancing fruit firmness, encouraging farmers to adopt targeted nutrient solutions. Additionally, the expansion of greenhouse cultivation, drip irrigation, and high-value horticulture in regions such as Southern Europe is further boosting demand for secondary macronutrients in this segment.

Geography Analysis

Europe accounted for 54.0% of EMEA secondary macronutrients market in 2025, driven by advanced agricultural practices, high adoption of precision farming technologies, and stringent regulations promoting balanced nutrient management. Countries such as Germany, France, and Spain have well-established farming systems in which soil testing and targeted fertilizer application are widely practiced, thereby increasing demand for sulfur, calcium, and magnesium. Declining natural sulfur deposition and intensive cropping have made secondary macronutrient supplementation essential for maintaining soil fertility and crop quality.

The Middle East is the fastest growing region, set to register a 7.8% CAGR through 2026-2031, supported by expanding agricultural initiatives, increasing investments in controlled-environment farming, and the availability of low-cost sulfur from oil and gas desulfurization. Countries like Saudi Arabia and the United Arab Emirates are adopting advanced irrigation techniques such as fertigation, which is driving demand for soluble secondary macronutrients. The focus on improving food security and reducing reliance on imports is further accelerating fertilizer usage in the region.

In Africa, the secondary macronutrients market is experiencing steady growth, driven by increasing awareness of soil nutrient deficiencies and efforts to improve agricultural productivity. Many regions in Sub-Saharan Africa have depleted soils lacking essential nutrients such as sulfur and magnesium due to continuous cropping and limited fertilizer use. Governments and international organizations are promoting balanced fertilization practices, encouraging farmers to adopt secondary macronutrients alongside primary nutrients. OCP Group's USD13 billion Green Investment Strategy (2023–2027) aims to increase its fertilizer production capacity from 12 million metric tons to 20 million tons of sustainable products by 2027[3]Source: OCP Group, “Green Investment Program,” ocpgroup.ma.

Competitive Landscape

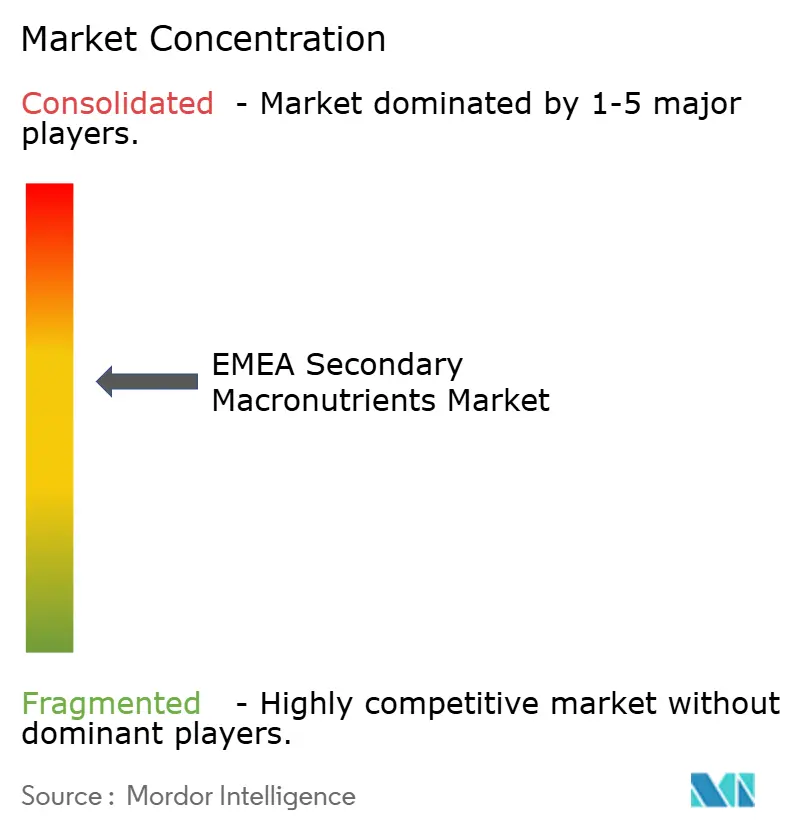

The EMEA secondary macronutrients market is moderately concentrated. Yara International ASA holds a leading position due to its extensive European presence and calcium ammonium nitrate blends that comply with balanced fertilization standards. EuroChem Group AG benefits from its sulfuric acid production capacity in Kazakhstan, offering geographic diversification following disruptions in the Strait of Hormuz. ICL Group leverages UK-mined Polysulphate, which provides four nutrients in a single granule, appealing to precision agriculture practitioners. K+S AG focuses on specialty-coated products that command double-digit premiums, while Haifa Group caters to greenhouse operators with nitrogen-free calcium solutions.

The merger and acquisition landscape has been relatively active, with companies pursuing strategic acquisitions to enhance market presence and expand geographical reach. Additionally, companies are increasingly favoring partnerships and joint ventures, particularly in emerging markets, to mitigate risks while gaining market access and sharing technological expertise.

To maintain and expand market share, incumbent players should prioritize developing innovative product formulations tailored to specific regional crop needs while adhering to sustainability standards. Investment in research and development is essential to create differentiated products, strengthen distribution networks, and foster strong relationships with farming communities. The growing focus on farming and environmental sustainability underscores the need for eco-friendly solutions. Furthermore, advancements in digital technologies and precision agriculture offer opportunities for value-added services and enhanced customer engagement.

EMEA Secondary Macronutrients Industry Leaders

Yara International ASA

EuroChem Group AG

Haifa Group

ICL Group

K+S AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: Africa has pledged to triple the domestic production and distribution of certified quality fertilizers to enhance smallholder farmers' access and boost agricultural productivity, as stated in the Nairobi Declaration during the Africa Fertilizer and Soil Health Summit 2024.

- April 2023: K+S Aktiengesellschaft acquired a 75% stake in the fertilizer business of South Africa-based Industrial Commodities Holdings (Pty) Ltd (ICH). The business now operates as a joint venture under the name Fertiva (Pty) Ltd. This acquisition enhances K+S's fertilizer distribution network in southern and eastern Africa, improving regional access to its specialty fertilizer portfolio, including magnesium- and sulfur-based secondary macronutrient products.

- March 2022: Koch Industries acquired a 50% stake in Jorf Fertilizers Company III (JFC III) from OCP, a leading global fertilizer group and major phosphate miner. This enables OCP and Koch Fertilizer to jointly market JFC III's fertilizers, including secondary macronutrient variants, regionally and globally. The agreement also establishes a strategic partnership, with OCP sourcing ammonia and sulfur from Koch and utilizing Koch's logistics for fertilizer shipments from Morocco.

EMEA Secondary Macronutrients Market Report Scope

Magnesium (Mg), sulfur (S), and calcium (Ca) are considered secondary macronutrients because crops require them in moderate quantities, typically less than primary macronutrients (N, P, and K) but more than micronutrients, and they play essential roles in plant growth and development.

The EMEA Secondary Macronutrients Market report is segmented by nutrient type into sulfur, calcium, and magnesium, by application method into solid and liquid, and by crop type into grains and cereals, pulses and oilseeds, fruits and vegetables, turf and ornamentals, and other crop types. It is also segmented by geography into Europe, the Middle East, and Africa. The market forecasts are provided in terms of value in USD.

| Sulfur |

| Calcium |

| Magnesium |

| Solid |

| Liquid |

| Grains and Cereals |

| Pulses and Oilseeds |

| Fruits and Vegetables |

| Turf and Ornamentals |

| Other Crop Types |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Kuwait | |

| Egypt | |

| Rest of Middle East | |

| Africa | South Africa |

| Morocco | |

| Nigeria | |

| Rest of Africa |

| By Nutrient Type | Sulfur | |

| Calcium | ||

| Magnesium | ||

| By Application Method | Solid | |

| Liquid | ||

| By Crop Type | Grains and Cereals | |

| Pulses and Oilseeds | ||

| Fruits and Vegetables | ||

| Turf and Ornamentals | ||

| Other Crop Types | ||

| By Geography | Europe | Germany |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Kuwait | ||

| Egypt | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Morocco | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the revenue outlook for the EMEA secondary macronutrients market by 2031?

The EMEA secondary macronutrients market is forecast to reach USD 5.22 billion by 2031.

Which nutrient type will grow fastest?

Magnesium is projected to expand at a 6.9% CAGR through 2031 because LED-lit greenhouses raise magnesium uptake needs.

Why are liquid formulations gaining share?

Controlled-environment farms prefer fully soluble calcium and magnesium nitrates that run cleanly through fertigation lines without clogging emitters.

Which region leads growth inside EMEA?

The Middle East is set to record a 7.8% CAGR through 2031, driven by state-funded greenhouse expansion.

Page last updated on: