Feed Fats And Proteins Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 13 Billion |

| Market Size (2031) | USD 15.10 Billion |

| Growth Rate (2026 - 2031) | 7.15% CAGR |

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

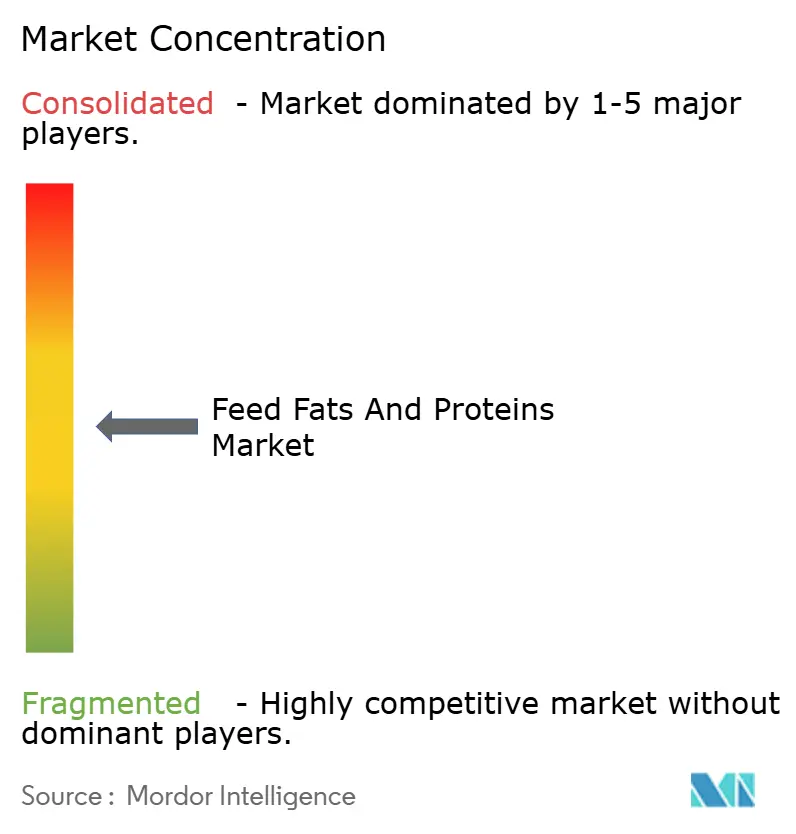

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Feed Fats And Proteins Market Analysis by Mordor Intelligence

The feed fats and proteins market size is projected to increase from USD 12.30 billion in 2025 to USD 13.00 billion in 2026 and reach USD 15.10 billion by 2031, growing at a CAGR of 7.15% over 2026-2031. Renewable-diesel expansion is creating a steady flow of discounted tallow and distillers' corn oil that compounders blend into livestock rations. Southeast Asian aquafeed producers are demanding high-PUFA lipids to support shrimp and finfish growth, while poultry integrators across North America and the European Union are turning to specialty medium-chain triglyceride and omega-3 blends that maintain feed-conversion efficiency after antibiotics are removed[1]Source: U.S. Environmental Protection Agency, “Renewable Fuel Standard Program: Standards for 2026-2027,” EPA.gov. Competitive pressure is also rising as low-carbon fuel standards in California and Canada divert animal fats away from feed channels, squeezing margins for mills without supply contracts.

Key Report Takeaways

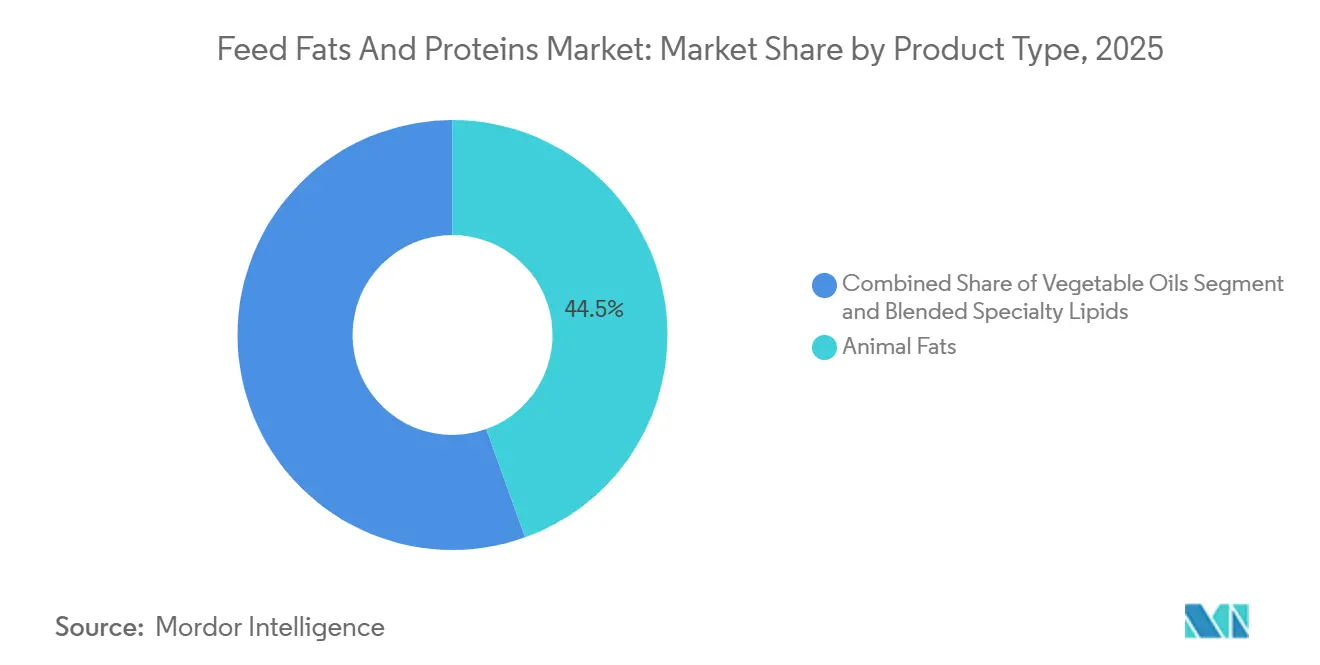

- By product type, animal fats led the largest segment, with 44.5% of the feed fats and proteins market share in 2025, while blended specialty lipids are the fastest growing segment, and will post the highest CAGR at 9.8% through 2026-2031.

- By form, liquid fats and oils hold the largest segment, commanded 56.0% of the feed fats and proteins market size in 2025, and are the fastest-growing segment, projected to expand at an 8.6% CAGR to 2026-2031.

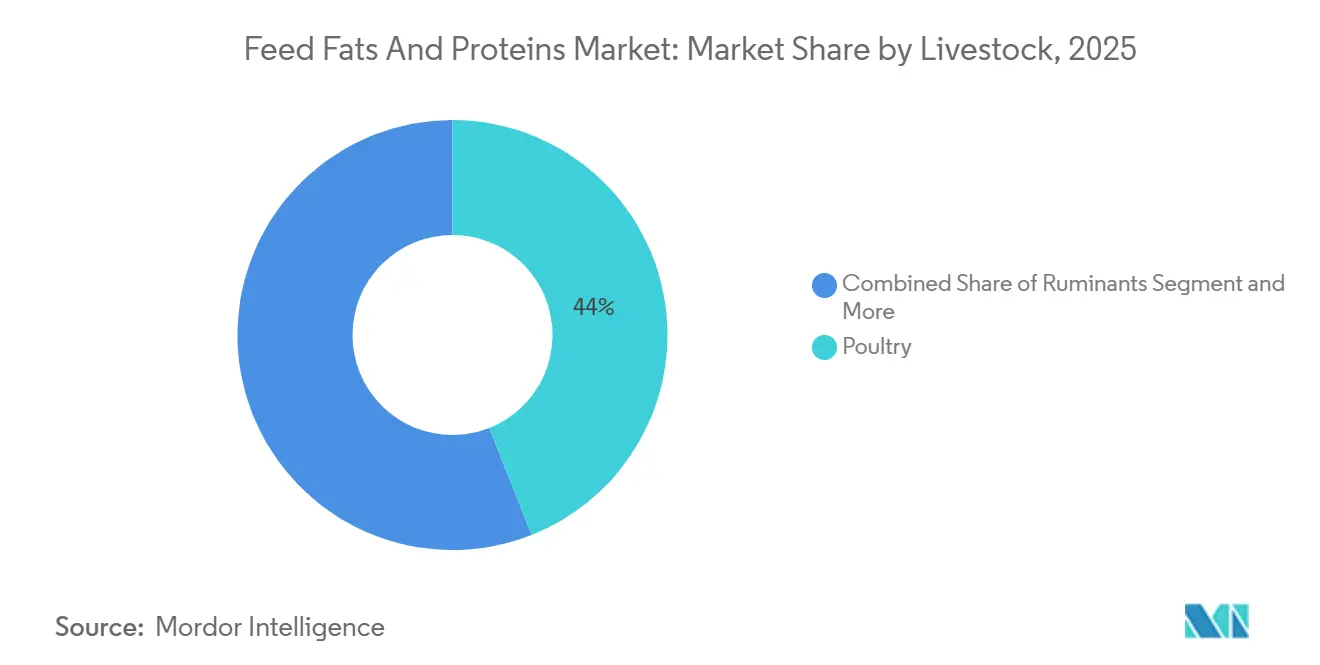

- By livestock, poultry accounted for the largest segment, with 44.0% of the feed fats and proteins market size in 2025, while aquaculture is the fastest-growing segment, forecast to advance at a 10.4% CAGR to 2026-2031.

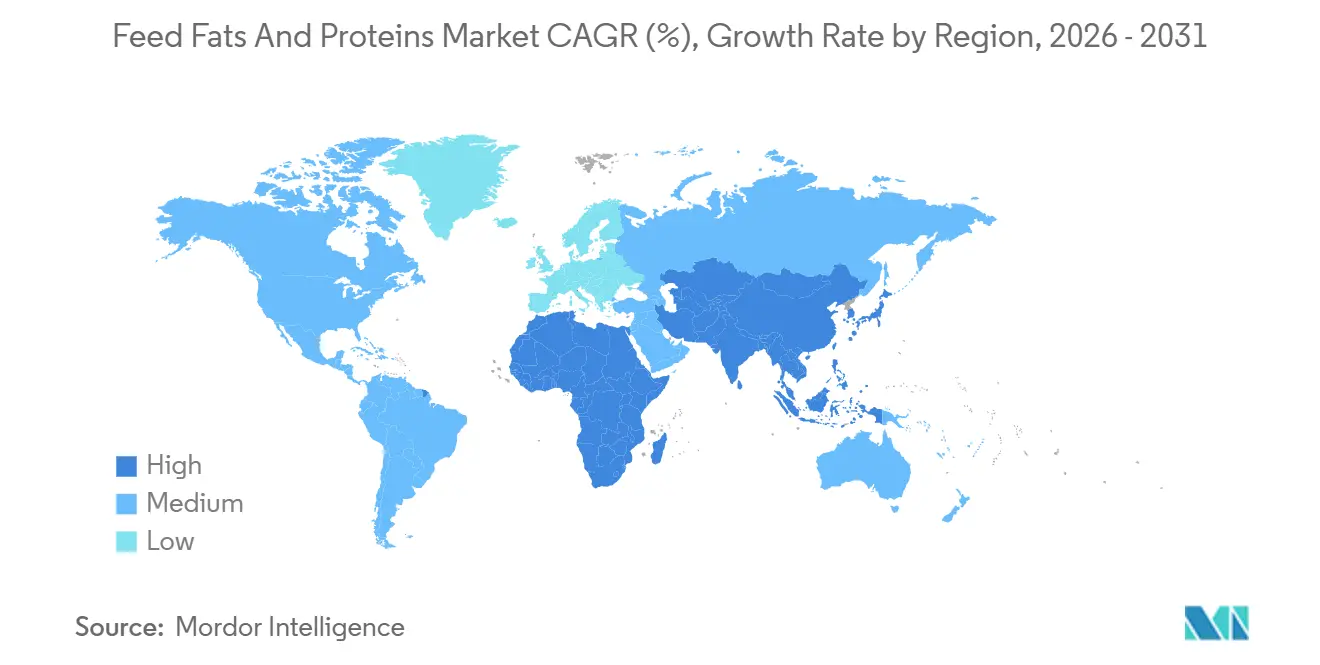

- By geography, Asia-Pacific is the largest region, with 34.2% of the feed fats and proteins market share in 2025, and Africa is the fastest-growing region, projected to log the highest regional CAGR at 7.2% through 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Feed Fats And Proteins Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surplus animal-fat by-products from renewable-diesel plants | +1.8% | North America core, and spill-over to South America | Medium term (2-4 years) |

| Specialty lipid blends that reduce antibiotic reliance | +1.5% | Global, the European Union, and North America are leading the adoption | Long term (≥4 years) |

| Aquafeed milling expansion in Southeast Asia | +1.2% | Asia-Pacific core, and spill-over to South America | Medium term (2-4 years) |

| Mandatory deforestation-free soy sourcing spurring alternative fats | +0.9% | Europe is dominant, and global compliance is emerging | Short term (≤2 years) |

| Rising demand for energy-dense poultry and swine rations | +1.1% | Global, intensive systems in Asia-Pacific and North America | Long term (≥4 years) |

| Blockchain-enabled rendering traceability, unlocking new premiums | +0.4% | North America and the European Union early adopters | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Surplus Animal-Fat By-Products from Renewable-Diesel Plants

Surplus animal-fat by-products from renewable diesel plants are becoming a significant driver of the feed fats and proteins market. The rise in renewable diesel production has increased the availability of animal by-products, which are now being effectively used as cost-efficient, nutrient-dense components in animal feed formulations. This approach not only promotes sustainability by minimizing waste but also helps stabilize the supply of feed ingredients. The Environmental Protection Agency’s 2026-2027 Renewable Fuel Standard fixed biomass-based diesel at 3.6 billion gal, locking in demand for feedstocks while guaranteeing steady coproduct availability.

Specialty Lipid Blends That Reduce Antibiotic Reliance

Global poultry and swine producers are eliminating antibiotic growth promoters, while functional lipids have emerged as viable substitutes. ADM and Berg+Schmidt GmbH & Co.KG (Stern-Wywiol Gruppe) precision blends that combine lauric acid with encapsulated omega-3s, offering integrators a premium solution that aligns with retailer antibiotic-free pledges. These specialty lipid blends not only support animal health but also contribute to sustainable farming practices by reducing reliance on antibiotics, a demand increasingly sought by consumers and regulatory bodies worldwide.

Aquafeed Milling Expansion in Southeast Asia

The growth of aquafeed milling in Southeast Asia is playing a crucial role in market expansion. The rapidly developing aquaculture industry in the region has led to increased demand for high-quality feed, prompting investments in aquafeed production capacity. Consequently, the demand for feed fats and proteins continues to grow, further bolstering the overall market. Peer-reviewed work showed that medium-chain triglycerides and monoacylglycerols improve feed-conversion ratios by up to 5% by limiting pathogenic bacterial loads in broilers. The growing focus on sustainable aquaculture practices has encouraged the adoption of innovative feed solutions, ensuring the long-term viability of the aquafeed industry in the region.

Mandatory Deforestation-Free Soy Sourcing Spurring Alternative Fats

The European Union Deforestation Regulation, effective from December 2024, mandates documentation proving that soy and palm were cultivated on non-deforested land. In response, major crushers have invested in satellite-based traceability systems. Many European buyers are increasingly opting for domestically produced rapeseed and sunflower oils, which pose minimal deforestation risks. This shift has reduced energy density in broiler and swine diets, thereby influencing the Feed Fats and Proteins Market by altering the composition of feed formulations. The regulation is expected to further influence sourcing strategies, with a stronger focus on sustainability and supply chain traceability. The growing preference for local oilseeds may drive higher domestic production, potentially altering the dynamics of the regional oilseed market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility of tallow and poultry fat | -1.3% | Global, North America, and the Asia-Pacific are the most exposed | Short term (≤2 years) |

| Trade barriers on rendered products after disease outbreaks | -0.8% | Asia-Pacific core, and global spill-over | Medium term (2-4 years) |

| Consumer backlash against animal-based feed ingredients | -0.5% | Europe and North America are dominant | Long term (≥4 years) |

| Photo-oxidation losses in high-Polyunsaturated Fatty Acids (PUFA) liquid fats during storage | -0.3% | Global, tropical regions most affected | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Consumer Backlash Against Animal-Based Feed Ingredients

A rising cohort of European pet-food buyers questions the sustainability of rendered animal inputs, pressuring brands to trial algal and insect oils even though scale and cost remain constraints. This sentiment could spill into mainstream livestock channels if marketing claims around “plant-based” meat continue to gain traction. This changing consumer sentiment extends beyond the pet-food segment and could influence the broader livestock feed market. If sustainability-focused marketing in the human food industry continues to grow, similar expectations may emerge in animal nutrition. Feed producers may face increased regulatory scrutiny and demands for reformulation, driving the industry toward innovative yet cost-effective alternatives to traditional animal-derived inputs.

Photo-Oxidation Losses in High-Polyunsaturated Fatty Acids (PUFA) Liquid Fats During Bulk Storage

Aquafeed producers in tropical ports report rapid increases in peroxide value when bulk fish oil is exposed to direct sunlight, cutting shelf life and requiring antioxidant fortification. Encapsulation mitigates but does not eliminate the challenge, adding to formulators' costs. Encapsulation technologies have also been introduced to provide a protective barrier that slows oxidative degradation. These measures increase formulation and processing costs, creating economic challenges for feed manufacturers. Striking a balance between product stability and cost-efficiency remains a critical issue, especially as demand for high-quality aquafeed grows in climate-sensitive regions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Rendered Fats Lead, Specialty Blends Accelerate

Animal fats led the largest segment, with 44.5% of the feed fats and proteins market share in 2025, as renderers supplied cost-effective tallow and poultry fat to integrators. This dominance is largely due to their widespread availability as by-products of the meat processing and rendering industries, making them a cost-effective and sustainable option for feed formulations. Animal fats also provide a high calorific value, enhancing the energy density of feed and contributing to improved weight gain and feed conversion ratios in livestock. Their established supply chains and compatibility with existing feed processing systems strengthen their position, particularly in price-sensitive markets.

Blended specialty lipids are the fastest-growing segment and will post the highest CAGR of 9.8% through 2026-2031. These products are formulated by combining various fat sources, such as vegetable oils and marine oils, with functional additives to achieve customized nutritional profiles. Their increasing adoption is driven by the emphasis on precision nutrition, which optimizes feed for specific species, growth stages, and health outcomes. In aquaculture, blended lipids enhance omega-3 content and promote fish health, while in poultry and swine, they improve immunity, gut health, and overall productivity.

By Form: Liquid Dominates, Dry Meals Serve Niche Applications

Liquid fats and oils hold the largest segment, commanded 56.0% of the feed fats and proteins market size in 2025, and are the fastest-growing segment, projected to expand at an 8.6% CAGR to 2026-2031. This growth is driven by rising demand for high-performance, energy-rich feed, particularly in intensive farming systems. In aquaculture, liquid oils such as fish oil and vegetable oils are critical for providing essential fatty acids, including omega-3s, which are necessary for growth and health. Technological advancements in storage, stabilization, and application methods, such as improved antioxidant systems and controlled dosing, are also facilitating their increased adoption. Despite challenges related to oxidation and storage stability, ongoing innovations and the growing need for efficient feed solutions are projected to support robust growth in this segment.

Mills favor spray-applied soybean oil and tallow because automated systems meter precise inclusion levels without harming pellet integrity. Extruded aqua diets also rely on liquid fish oil and algal concentrates to uniformly distribute omega-3s. Dry meals and powders occupy niche uses where shelf stability and dust control are paramount. Encapsulated fat powders protect polyunsaturated fatty acids from oxidation, an advantage for premium pet-food recipes marketed on stable shelf life.

By Livestock: Poultry Leads, Aquaculture Surges

Poultry accounted for the largest segment, with 44.0% of the feed fats and proteins market size in 2025, owing to broiler diets that include 3-4% fat for rapid weight gain. This dominance is attributed to the high global demand for poultry meat and eggs, which are among the most affordable and widely consumed sources of animal protein. Poultry production systems are highly intensive and require energy-dense, nutritionally balanced feed, making fats and proteins essential components. Additionally, shorter production cycles and more efficient feed conversion ratios in poultry further drive strong, consistent demand for feed inputs.

Aquaculture is the fastest-growing segment, forecast to advance at a 10.4% CAGR to 2026-2031. This rapid growth is driven by rising global demand for seafood and the depletion of wild fish stocks, accelerating the shift toward farmed fish and shrimp. Aquafeed requires high-quality lipids and proteins, particularly those rich in omega-3 fatty acids, to support optimal growth, health, and product quality. Advancements in aquafeed formulations, along with increasing investments in aquaculture infrastructure, especially in the Asia-Pacific and South America, are further driving the demand for specialized feed fats and proteins in this segment.

Geography Analysis

Asia-Pacific is the largest region, with 34.2% of the feed fats and proteins market share in 2025. This dominance is driven by the region’s large and rapidly expanding livestock and aquaculture industries, particularly in countries such as China, India, Vietnam, and Indonesia. In 2025, China’s aim to cut soybean-meal inclusion to 10% by 2030 forces mills to secure alternative proteins and raise fat levels to maintain energy density, stimulating imports of poultry fat and canola oil[3]Source: China Ministry of Agriculture and Rural Affairs, “Soybean Meal Reduction Plan,” moa.gov.cn. Rising population, increasing disposable incomes, and growing demand for animal protein are key factors supporting feed production in the region. Additionally, the strong presence of feed manufacturers, availability of raw materials, and continued investments in commercial farming and aquafeed infrastructure further reinforce Asia-Pacific’s leading position in the market.

Africa is the fastest-growing region, projected to log the highest regional CAGR of 7.2% through 2026-2031. This growth is mainly driven by rising urbanization, increasing protein consumption, and the gradual modernization of livestock and poultry farming practices. Both governments and private entities are investing in improving feed quality and supply chains to boost agricultural productivity. While the market remains less developed than in more established regions, growing awareness of balanced animal nutrition and the expansion of commercial farming are projected to sustain demand for feed fats and proteins in Africa.

South America is projected to experience steady growth in the coming years, driven by evolving oilseed processing dynamics and biofuel policies. In Brazil, robust soybean crushing activity has enhanced the availability of soybean meal and related by-products, bolstering feed production. In North America, market growth is supported by the expansion of renewable diesel production, which produces substantial volumes of animal fat and other lipid coproducts. These by-products are increasingly used in feed applications due to their cost-effectiveness and availability.

Competitive Landscape

The feed fats and proteins market is experiencing moderate growth, with major companies such as Cargill, Incorporated, Archer-Daniels-Midland Company, Darling Ingredients, Bunge Global SA, and Wilmar International Limited holding a significant share of global revenue in 2025. These companies leverage integrated rendering, crushing, and distribution capabilities to address the increasing demand in the livestock and aquaculture sectors. They are actively refining their fat-sourcing strategies to manage fluctuations in biofuel demand while ensuring access to advanced lipid technologies. Additionally, several firms are expanding their proprietary fat-processing platforms to meet functional and species-specific nutritional requirements.

Technological innovation is becoming a core component of leading companies' portfolios. Cargill, Incorporated and ADM are investing in precision nutrition tools, including fat-modulation technologies, to enhance feed conversion efficiency and energy yield in both monogastric and ruminant animals. BASF SE and DSM-Firmenich are focusing on lipid-based functional additives, supported by research and development in feed efficiency and gut health. Key players are also specializing in medium-chain triglycerides and encapsulated lipid formats, while Adisseo (Bluestar) and Evonik Industries are integrating lipid nutrition with amino acid balancing and gut microbiome optimization.

Leading companies are expanding their market presence through regional partnerships, rendered-fat sourcing networks, and specialty lipid formulations. They are also adapting to a changing regulatory landscape, where transparency, feed safety, and environmental impact assessments are gaining prominence. The FDA’s Animal Food Ingredient Consultation pathway, which facilitates the approval of novel lipids, provides opportunities for firms with strong scientific expertise and compliance infrastructure to secure early-mover advantages. Companies that combine large-scale raw-material-handling capabilities with innovation in lipid functionality are projected to drive the next phase of competitive growth in the feed fats and proteins market.

Feed Fats And Proteins Industry Leaders

Cargill, Incorporated

Darling Ingredients

Bunge Global SA

Wilmar International Limited

Archer-Daniels-Midland Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Cargill, Incorporated’s facility in Scotland achieved Aquaculture Stewardship Council (ASC) certification, signifying responsible sourcing and processing of ingredients, including fats, for the aquafeed industry, and enhancing traceability and sustainability standards.

- August 2024: Bunge’s North American refined and specialty oils division is launching a new deoiled soybean lecithin line (powdered and granulated), adjacent to its Bellevue, Ohio, plant. These functional fats enhance feed digestibility and pellet stability.

- February 2024: Cargill, Incorporated, deepened its collaboration with fermentation-tech company ENOUGH to advance production and commercialization of a sustainable fungal protein with a complete amino acid profile. Cargill is also integrating its fat formulations and plant-based ingredients to develop new monogastric feed and alternative-protein applications.

Global Feed Fats And Proteins Market Report Scope

Feed fats and proteins are nutritional components incorporated into animal feed to supply energy, essential fatty acids, and proteins necessary for the growth, reproduction, and overall health of livestock, poultry, and aquaculture species. The feed fats and proteins market report is segmented by product type (animal fats, vegetable oils, and blended specialty lipids), by form (dry meals and powders, and liquid fats and oils), by livestock (poultry, swine, ruminants, aquaculture, and pet food), and by geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The market forecasts are provided in terms of value (USD).

| Animal Fats |

| Vegetable Oils |

| Blended Specialty Lipids |

| Dry Meals and Powders |

| Liquid Fats and Oils |

| Poultry |

| Swine |

| Ruminants |

| Aquaculture |

| Pet Food |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Product Type | Animal Fats | |

| Vegetable Oils | ||

| Blended Specialty Lipids | ||

| By Form | Dry Meals and Powders | |

| Liquid Fats and Oils | ||

| By Livestock | Poultry | |

| Swine | ||

| Ruminants | ||

| Aquaculture | ||

| Pet Food | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected value of the feed fats and proteins market by 2031?

The market is forecast to reach USD 15.10 billion by 2031, growing at a 7.15% through 2026-2031 CAGR.

Which livestock segment is expected to grow fastest through 2031?

Aquaculture, with a projected 10.4% CAGR through 2026-2031, is set to outpace poultry, swine, and ruminants.

How is the Europe Union Deforestation Regulation shaping fat sourcing?

It pushes European feed mills toward rapeseed and sunflower oils that carry lower deforestation risk and are easier to certify.

Which region currently leads demand?

Asia-Pacific led largest region, with 34.2% of the feed fats and proteins market share in 2025.

Page last updated on: