Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.52 Billion |

| Market Size (2031) | USD 1.94 Billion |

| Growth Rate (2026 - 2031) | 5.06% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Feed Enzymes Market Analysis by Mordor Intelligence

The feed enzymes market size is projected to increase from USD 1.45 billion in 2025 to USD 1.52 billion in 2026 and reach USD 1.94 billion by 2031, growing at a CAGR of 5.06% over 2026-2031. Mandatory restrictions on in-feed antibiotics across major producing countries have accelerated demand for carbohydrase and phytase products that unlock latent feed energy while keeping residue levels within regulatory limits. Parallel methane-reduction rules in dairy and beef systems are broadening the enzyme user base beyond monogastric animals. Procurement teams are focusing on conversion efficiency as grain markets remain volatile, which increases the return on incremental gains in digestibility. Consolidation among feed mills is tilting bargaining power toward a handful of integrators, intensifying price pressure on suppliers and spurring a shift toward bundled, precision-nutrition services that embed enzymes with data analytics.

Key Report Takeaways

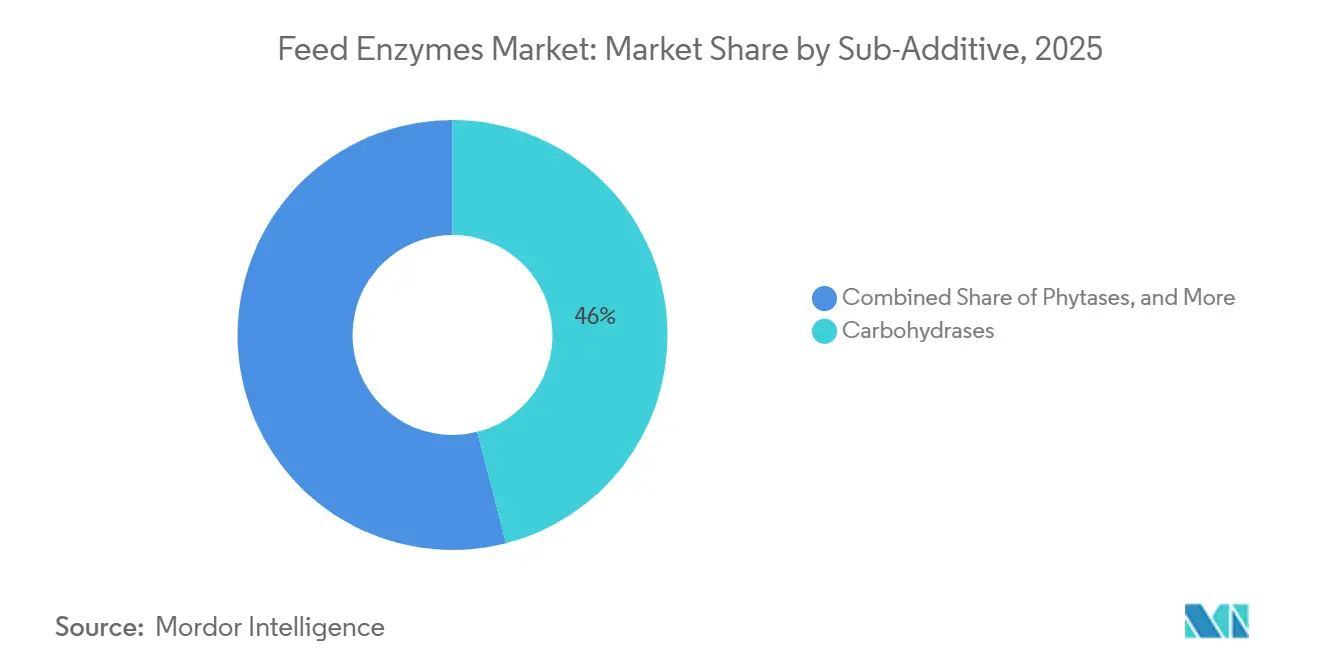

- By sub-additive, carbohydrases led with a 46.0% of the feed enzymes market share in 2025, and are projected to accelerate at a 5.1% CAGR through 2031.

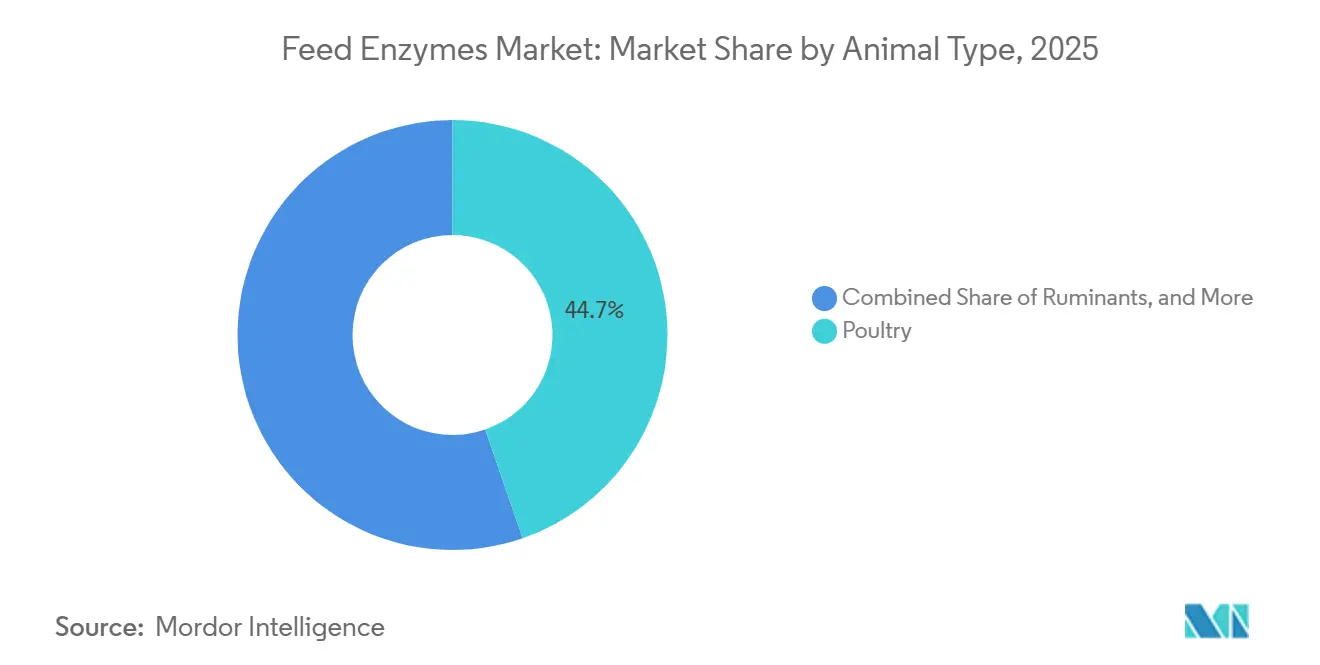

- By animal, poultry accounted for 44.7% of the feed enzymes market size in 2025, while ruminants are positioned to climb at a 5.2% CAGR to 2031.

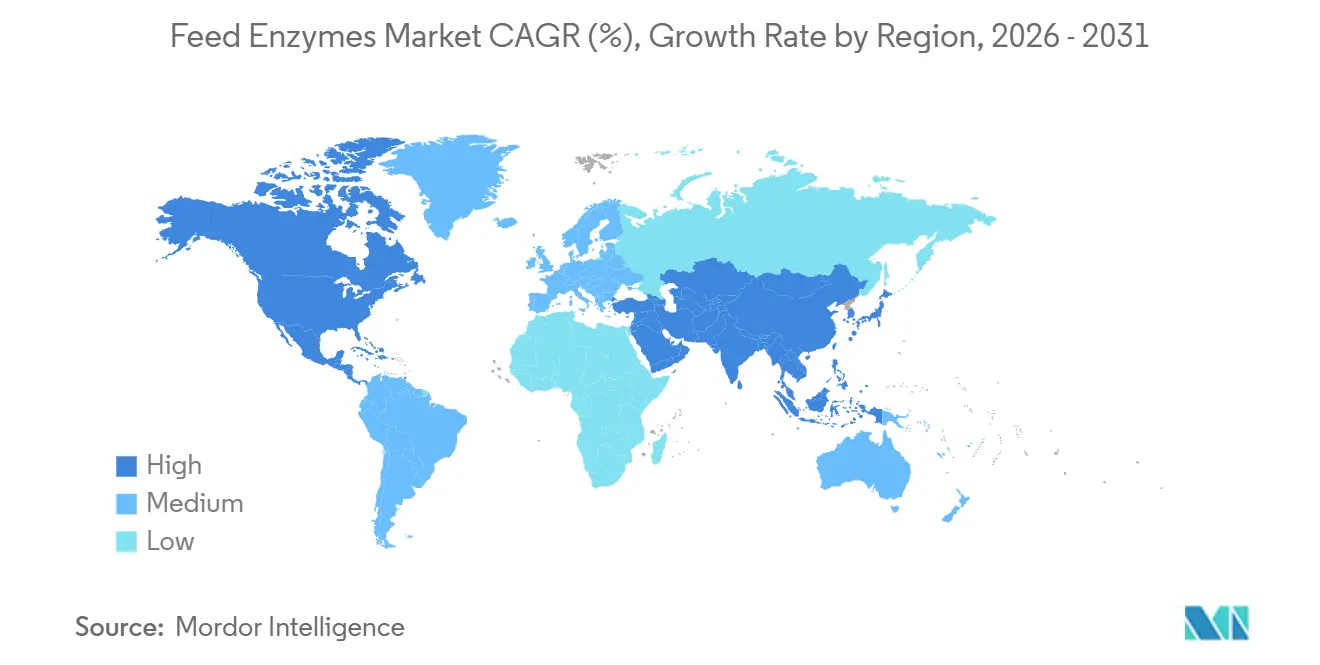

- By geography, Asia-Pacific captured 31.6% of 2025 revenue, whereas North America is forecast to register a 4.7% CAGR between 2026 and 2031.

- Market concentration remains moderate, with the top five companies, BASF SE, Archer Daniels Midland Company, Kerry Group Plc, Elanco Animal Health Incorporated, and International Flavors and Fragrances Inc., collectively accounting for a majority share of the market in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Feed Enzymes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Antibiotic Growth-Promoter Ban Accelerating Enzyme Adoption | +1.0% | European Union, China, Southeast Asia, and South America | Medium term (2-4 years) |

| Escalating Animal Protein Demand in Emerging Economies | +1.1% | India, Indonesia, Vietnam, Philippines, Middle East, and Africa | Long term (≥ 4 years) |

| Feed-Mill Cost Focus Boosting Conversion-Efficiency Solutions | +0.6% | North America, European Union, Brazil, and Argentina | Short term (≤ 2 years) |

| Aquaculture Expansion in Tropical Regions | +0.5% | Vietnam, Indonesia, Thailand, Ecuador, and Chile | Medium term (2-4 years) |

| Genomics-Guided Custom Enzyme Cocktails | +0.2% | North America, and European Union | Long term (≥ 4 years) |

| Retailer Carbon-Footprint Label Mandates | +0.3% | European Union, United States, United Kingdom, Netherlands, and California | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Antibiotic Growth-Promoter Ban Accelerating Enzyme Adoption

The phase-out of antibiotic growth promoters has shifted nutritional strategy from pharmaceutical intervention to enzyme-driven nutrient release. China removed all growth-promoting antibiotics from commercial rations in 2020, immediately expanding the addressable monogastric feed volume for phytase and xylanase[1]Source: European Medicines Agency, “Antimicrobial Resistance,” EMA.europa.eu. Regulation 2019/6 banned routine prophylactic use across the European Union in 2022, followed by the 2024 update to the United States Food and Drug Administration’s Veterinary Feed Directive that requires veterinary oversight for any medically significant antibiotic in feed. Producers initially experienced lower daily weight gain, yet fieldwork published by the European Federation of Animal Science shows that strategic enzyme inclusion can recover up to 80% of lost performance. India and Brazil are moving toward similar bans by 2027 and 2028, respectively, cementing enzymes as a core efficiency lever rather than an optional additive.

Escalating Animal Protein Demand in Emerging Economies

Rising disposable incomes and rapid urbanization are driving increased per-capita meat consumption, particularly poultry, in Asia and Sub-Saharan Africa. From 2020 to 2025, poultry production in Southeast Asia grew at an annual rate of 4.2%, surpassing the global average[2]Source: Food and Agriculture Organization and Organisation for Economic Cooperation and Development, “Agricultural Outlook 2024-2034,” FAO.org. This growth is attributed to rising demand for affordable protein sources and improvements in poultry farming practices. In 2025, India’s broiler production reached 5.2 million metric tons, highlighting cost inefficiencies that enzymes can address by enhancing energy release from corn-soy diets. Enzymes such as phytase and protease are increasingly being used to improve feed efficiency and reduce production costs. In Indonesia, feed usage for tilapia and catfish rose to 2.1 million metric tons in 2025, with phytase adoption reaching 35% of feed formulations, driven by stricter regulations aimed at reducing phosphorus discharge. This regulatory push is part of broader environmental sustainability efforts in the aquaculture sector. In the Middle East, freight costs of USD 40–60 per metric ton for imported grains amplify the economic benefits of improved digestibility, driving enzyme adoption in countries such as Egypt, Saudi Arabia, and the United Arab Emirates.

Feed-Mill Cost Focus Boosting Conversion-Efficiency Solutions

Feed costs constitute approximately two-thirds of total poultry production expenses and over half of swine production costs, making even small improvements in feed conversion ratios financially significant. In the United States, broiler integrators reduced the average feed conversion ratio from 1.88 in 2020 to 1.82 in 2025, with enzyme inclusion contributing to a 0.03-0.05 point improvement. This reduction highlights the growing importance of feed efficiency in reducing overall production costs. In the European Union, feed mills face additional challenges under the Farm to Fork strategy, which aims to reduce antimicrobial use by 50% by 2030, driving the adoption of non-pharmaceutical solutions. The strategy has further accelerated the shift toward sustainable feed practices. Cargill, Incorporated, reported an increase in the inclusion of enzymes in its North American poultry diets in 2025 compared to 2022, indicating a significant shift toward enzyme-focused formulations. Economic models indicate that an enzyme cost of eight to twelve cents per metric ton often yields net feed savings of fifty cents to one dollar, demonstrating the significant return on investment for producers.

Retailer Carbon-Footprint Label Mandates

Supermarket chains are incorporating Scope 3 emissions into supplier scorecards, indirectly incentivizing the use of enzymes that reduce methane and nitrous oxide emissions per unit of animal protein. Carrefour’s Act for Food program in France will mandate beef and dairy suppliers to report enteric methane intensity by 2026. This initiative aims to enhance transparency and encourage suppliers to adopt sustainable practices. Similarly, Tesco in the United Kingdom and Walmart in the United States have established comparable targets to address emissions in their supply chains. The European Union’s Carbon Border Adjustment Mechanism, set to begin in 2026, will impose taxes on carbon-intensive meat imports, further driving the need for emission reductions. Lifecycle studies conducted by Wageningen University indicate that improved feed efficiency through enzyme use can reduce methane emissions by 2-4%, offering a quantifiable, albeit indirect, compliance pathway. These measures collectively highlight the growing emphasis on reducing agricultural emissions and aligning with global sustainability goals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Raw-Material Costs | -0.8% | Global, highest in Middle East, North Africa, and Japan | Short term (≤ 2 years) |

| Lengthy and Complex Regulatory Approvals | -0.5% | European Union, China, and India | Long term (≥ 4 years) |

| Thermal Instability in Pelleted Feed | -0.4% | North America, and European Union | Medium term (2-4 years) |

| Feed-Mill Consolidation Reducing Supplier Leverage | -0.6% | North America, European Union, Brazil, and China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Raw-Material Costs

Corn futures experienced fluctuations, creating a range that complicated enzyme contract negotiations established months earlier. The significant price swings in corn futures created uncertainty for buyers and sellers, making it challenging to lock in stable agreements. Soybean meal prices ranged from USD 350 to USD 420 per short ton due to drought concerns in South America, further contributing to market instability. This level of volatility has led some mills to delay enzyme purchases and adopt least-cost formulations, which prioritize cost savings over performance. In response, suppliers have introduced flexible pricing tied to grain benchmarks; however, this approach shifts margin risk upstream and adds complexity to budgeting processes, requiring mills and suppliers to adapt their financial strategies accordingly.

Lengthy and Complex Regulatory Approvals

Obtaining feed additive clearances requires 18 to 36 months for toxicology and efficacy trials. Regulatory bodies such as the European Food Safety Authority (EFSA), the Chinese Ministry of Agriculture and Rural Affairs (MARA), and India’s Food Safety and Standards Authority (FSSAI) increased data requirements in 2024. These stricter regulations have significantly increased the cost of a global roll-out to USD 0.5-1.0 million per enzyme, encompassing expenses for comprehensive testing, documentation, and compliance processes[3]Source: European Food Safety Authority, “Feed Additive Applications,” EFSA.europa.eu. This financial burden includes conducting extensive toxicology studies to ensure safety, efficacy trials to validate performance, and meeting the detailed documentation standards required by each regulatory authority. Smaller innovators face challenges in meeting these costs, which have slowed the introduction of new modes of action and limited the pace of innovation in the feed-additive market. As a result, the market is increasingly dominated by larger players with the resources to navigate these regulatory hurdles, further widening the gap between established companies and emerging innovators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub-Additive: Carbohydrases Dominate Value Capture

Carbohydrases were the largest sub-additive segment, accounting for 46.0% of the feed enzymes market size in 2025, benefiting from broad compatibility with wheat and corn rations. The segment is forecast to expand at a 5.1% CAGR through 2031 as xylanase and beta-glucanase in poultry starter and grower diets unlock non-starch polysaccharides that would otherwise pass undigested, improving metabolizable energy by up to one hundred kilocalories per kilogram. Phytases driven by phosphorus discharge limits in the European Union and the United States. Proteases, lipases, and amylases collectively accounted for the remaining share, though next-generation protease launches aimed at crude-protein reduction are outpacing their base, indicating room for a mix shift within the overall feed enzymes market.

Growth momentum within the sub-additive category points to thermostable phytases and multi-carbohydrase complexes tailored for viscous barley diets. Advancements in protein engineering are beginning to deliver enzymes that retain more than 85% activity after pelleting, easing a key efficacy concern for mills using high-temperature conditioners. As these variants scale, suppliers project pricing to normalize, preserving margin while widening the addressable feed enzymes market.

By Animal Type: Ruminants Provide the Fastest Upside

Poultry were the largest animal type and accounted for 44.7% of the feed enzymes market share in 2025, reflecting the sector’s scale and tight conversion economics. Broiler integrators already embed enzymes in more than 85% of starter and grower feeds; incremental growth will mainly come from higher dosing precision rather than volume expansion. Policy incentives are sharpening the ruminant value proposition. New Zealand’s levy on enteric methane above sector benchmarks and Canada’s USD 110 million dairy investment fund both recognize enzyme supplementation as an eligible mitigation step.

The ruminant segment is the fastest-growing segment and projected to grow at a 5.2% CAGR to 2031, outpacing monogastric categories as dairy and beef growers adopt cellulase-xylanase blends to comply with methane-reduction mandates. Enzyme packages that improve fiber digestibility are delivering half- to one-liter daily milk gains in intensive European Union systems, validating the economics for wider adoption and expanding the feed enzymes market share captured by ruminant formulations. Feedlot tests in the United States Corn Belt indicate that fiber-degrading complexes can cut finishing days by 3 to 5, a material cash-flow benefit when multiplied across 25 million head annually. These signals support a sustained shift in the feed enzymes industry toward specialized ruminant solutions.

Geography Analysis

Asia-Pacific was the largest geography and accounted for 31.6% of the feed enzymes market share in 2025, anchored by China’s 700 million metric tons compound feed output and India’s rapidly expanding broiler industry. China’s blanket antibiotic ban transformed 260 million metric tons of poultry and swine rations overnight, making enzyme inclusion a structural feature rather than a discretionary choice. India’s penetration remains below 50% due to fragmented mill capacity, but targeted government extension programs are improving technical awareness, which should boost adoption. Southeast Asian aquaculture hubs, especially Vietnam and Indonesia, add further upside as enzyme-supplemented feeds become a prerequisite for environmental permitting.

North America is projected to post the fastest CAGR of 4.7% through 2031, driven by tightening broiler conversion benchmarks and regulatory moves to cut dairy methane emissions. United States Department of Agriculture data shows commercial broiler placements rising 2.3% year-over-year in 2025, heightening the search for margin inside starter and grower diets. Canada’s Dairy Farm Investment Program subsidizes enzyme purchases, linking financial support directly to greenhouse gas reductions. Mexico, while smaller, is accelerating enzyme intake as peso-denominated corn prices hover near multi-year highs, pushing feed formulators toward higher nutrient extraction efficiency.

Europe is projected to grow at a moderate pace, as the penetration of poultry and swine rations already exceeds 90%. Growth in this region will primarily depend on innovation rather than volume, with a focus on multi-substrate blends and precision-dosed ruminant enzymes to address stricter nitrate and phosphorus regulations. The increasing emphasis on sustainability and environmental compliance is also driving the adoption of advanced enzyme solutions in the region. In South America, led by Brazil, the widespread adoption of enzymes in broiler feeds is supported by strong integrator structures and export-oriented production. Aquaculture and beef sectors present untapped opportunities for growth, with rising demand for protein and expanding export markets creating favorable conditions for enzyme adoption. The Middle East and Africa remain underdeveloped due to limitations in feed mill scale and currency risks. Nevertheless, ongoing government initiatives aimed at protein security, coupled with increasing investments in feed production infrastructure, could create growth opportunities beyond 2028.

Competitive Landscape

Market concentration is moderate, with the top five companies, BASF SE, Archer Daniels Midland Company, Kerry Group Plc, Elanco Animal Health Incorporated, and International Flavors and Fragrances Inc. collectively holding a majority of market share in 2025. The January 2024 merger between Novozymes and Chr. Hansen Holding A/S formed Novonesis, a biosolutions leader with significant revenue and the capacity to cross-sell enzymes with microbial products. DSM-Firmenich AG’s January 2025 divestiture of its animal nutrition unit to Advent International introduced private equity discipline into a portfolio that already held established phytase and protease lines, foreshadowing aggressive pricing or bolt-on acquisition moves.

BASF SE surprised the market in October 2025 by announcing a strategic review of its Nutrition and Care division. If the German chemical major exits, an 8-10% global share could shift to an emerging-market player or another financial sponsor, likely raising the competitive temperature. Meanwhile, vertically integrated agribusinesses such as Cargill, Incorporated, and Archer Daniels Midland Company are building domestic enzyme plants or partnering with regional specialists to secure supply and internalize margin.

Second-tier innovators are targeting technical pain points. Adisseo SAS received European Food Safety Authority (EFSA) clearance in July 2024 for a next-gen phytase that retains 90% activity after pelleting at 90 °C, allowing a 20% price premium over standard offerings. Indian-headquartered Advanced Enzyme Technologies and Infinita Biotech are commercializing thermostable variants at lower cost positions, positioning themselves to capture share in Asia and Africa as local regulatory barriers ease. Strategic themes revolve around three axes, including thermostability, precision nutrition platforms, and geographic localization. Players without these capabilities risk margin compression as buyer consolidation accelerates. Financial sponsors are projected to continue rolling up regional producers to build scale, while multinational ingredient houses weigh make-or-buy decisions for enzyme capacity.

Feed Enzymes Industry Leaders

BASF SE

Archer Daniels Midland Company

Kerry Group Plc

Elanco Animal Health Incorporated

International Flavors and Fragrances Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Kemin Industries, Inc. has acquired CJ Youtell Biotech, the enzymes and fermentation subsidiary of CJ Bio, based in Seoul, South Korea. This acquisition enhances Kemin's presence in the enzyme market, particularly in segments such as animal feed and aquaculture. By integrating CJ Youtell Biotech's expertise in enzymes and fermentation, Kemin Industries, Inc. aims to strengthen its product portfolio and expand its global reach in these markets.

- June 2025: DSM-Firmenich AG, a company specializing in nutrition, health, and beauty, has completed the sale of its stake in the Feed Enzymes Alliance to its partner Novozymes, a global biosolutions company, for USD 1.79 billion. This transaction marks a significant step for DSM-Firmenich AG in refining its strategic focus on core business areas, while Novozymes strengthens its position in the biosolutions market through this acquisition.

- April 2025: Novus International, Inc. introduced its CIBENZA XCEL Xylanase enzyme feed additive in India to improve nutrient utilization and gut health in poultry. The product aims to enhance feed efficiency amid fluctuating ingredient costs. The enzyme breaks down soluble and insoluble xylans, facilitating optimized energy release for producers.

Global Feed Enzymes Market Report Scope

Feed enzymes are natural protein-based biocatalysts incorporated into animal diets to facilitate the breakdown of complex, anti-nutritional, or indigestible components into smaller, absorbable nutrients. Their use improves nutrient digestibility, enhances feed conversion ratio (FCR), and minimizes environmental waste by increasing the utilization of carbohydrates, proteins, and phosphorus.

The feed enzymes market report is segmented by sub-additive, including carbohydrases, phytases, and other enzymes, by animal type, including aquaculture, poultry, ruminants, swine, and other animals, and by geography, including North America, South America, Europe, Asia Pacific, the Middle East, and Africa. The market forecasts are provided in terms of value in USD and volume in metric tons.

By Sub-Additive

| Carbohydrases |

| Phytases |

| Other Enzymes |

By Animal Type

| Aquaculture | Fish |

| Shrimp | |

| Other Aquaculture Species | |

| Poultry | Broiler |

| Layer | |

| Other Poultry Birds | |

| Ruminants | Beef Cattle |

| Dairy Cattle | |

| Other Ruminants | |

| Swine | |

| Other Animals |

By Geography

| North America | Canada |

| Mexico | |

| United States | |

| Rest of North America | |

| Europe | France |

| Germany | |

| Italy | |

| Netherlands | |

| Russia | |

| Spain | |

| United Kingdom | |

| Rest of Europe | |

| Asia-Pacific | Australia |

| China | |

| India | |

| Indonesia | |

| Japan | |

| Philippines | |

| South Korea | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific | |

| South America | Argentina |

| Brazil | |

| Chile | |

| Rest of South America | |

| Middle East | Iran |

| Saudi Arabia | |

| Turkey | |

| Rest of Middle East | |

| Africa | Egypt |

| Kenya | |

| South Africa | |

| Rest of Africa |

| By Sub-Additive | Carbohydrases | |

| Phytases | ||

| Other Enzymes | ||

| By Animal Type | Aquaculture | Fish |

| Shrimp | ||

| Other Aquaculture Species | ||

| Poultry | Broiler | |

| Layer | ||

| Other Poultry Birds | ||

| Ruminants | Beef Cattle | |

| Dairy Cattle | ||

| Other Ruminants | ||

| Swine | ||

| Other Animals | ||

| By Geography | North America | Canada |

| Mexico | ||

| United States | ||

| Rest of North America | ||

| Europe | France | |

| Germany | ||

| Italy | ||

| Netherlands | ||

| Russia | ||

| Spain | ||

| United Kingdom | ||

| Rest of Europe | ||

| Asia-Pacific | Australia | |

| China | ||

| India | ||

| Indonesia | ||

| Japan | ||

| Philippines | ||

| South Korea | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| South America | Argentina | |

| Brazil | ||

| Chile | ||

| Rest of South America | ||

| Middle East | Iran | |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | Egypt | |

| Kenya | ||

| South Africa | ||

| Rest of Africa | ||

Market Definition

- FUNCTIONS - For the study, feed additives are considered to be commercially manufactured products that are used to enhance characteristics such as weight gain, feed conversion ratio, and feed intake when fed in appropriate proportions.

- RESELLERS - Companies engaged in reselling feed additives without value addition have been excluded from the market scope, to avoid double counting.

- END CONSUMERS - Compound feed manufacturers are considered to be end-consumers in the market studied. The scope excludes farmers buying feed additives to be used directly as supplements or premixes.

- INTERNAL COMPANY CONSUMPTION - Companies engaged in the production of compound feed as well as the manufacturing of feed additives are part of the study. However, while estimating the market sizes, the internal consumption of feed additives by such companies has been excluded.

| Keyword | Definition |

|---|---|

| Feed additives | Feed additives are products used in animal nutrition for purposes of improving the quality of feed and the quality of food from animal origin, or to improve the animals’ performance and health. |

| Probiotics | Probiotics are microorganisms introduced into the body for their beneficial qualities. (It maintains or restores beneficial bacteria to the gut). |

| Antibiotics | Antibiotic is a drug that is specifically used to inhibit the growth of bacteria. |

| Prebiotics | A non-digestible food ingredient that promotes the growth of beneficial microorganisms in the intestines. |

| Antioxidants | Antioxidants are compounds that inhibit oxidation, a chemical reaction that produces free radicals. |

| Phytogenics | Phytogenics are a group of natural and non-antibiotic growth promoters derived from herbs, spices, essential oils, and oleoresins. |

| Vitamins | Vitamins are organic compounds, which are required for normal growth and maintenance of the body. |

| Metabolism | A chemical process that occurs within a living organism in order to maintain life. |

| Amino acids | Amino acids are the building blocks of proteins and play an important role in metabolic pathways. |

| Enzymes | Enzyme is a substance that acts as a catalyst to bring about a specific biochemical reaction. |

| Anti-microbial resistance | The ability of a microorganism to resist the effects of an antimicrobial agent. |

| Anti-microbial | Destroying or inhibiting the growth of microorganisms. |

| Osmotic balance | It is a process of maintaining salt and water balance across membranes within the body's fluids. |

| Bacteriocin | Bacteriocins are the toxins produced by bacteria to inhibit the growth of similar or closely related bacterial strains. |

| Biohydrogenation | It is a process that occurs in the rumen of an animal in which bacteria convert unsaturated fatty acids (USFA) to saturated fatty acids (SFA). |

| Oxidative rancidity | It is a reaction of fatty acids with oxygen, which generally causes unpleasant odors in animals. To prevent these, antioxidants were added. |

| Mycotoxicosis | Any condition or disease caused by fungal toxins, mainly due to contamination of animal feed with mycotoxins. |

| Mycotoxins | Mycotoxins are toxin compounds that are naturally produced by certain types of molds (fungi). |

| Feed Probiotics | Microbial feed supplements positively affect gastrointestinal microbial balance. |

| Probiotic yeast | Feed yeast (single-cell fungi) and other fungi used as probiotics. |

| Feed enzymes | They are used to supplement digestive enzymes in an animal’s stomach to break down food. Enzymes also ensure that meat and egg production is improved. |

| Mycotoxin detoxifiers | They are used to prevent fungal growth and to stop any harmful mold from being absorbed in the gut and blood. |

| Feed antibiotics | They are used both for the prevention and treatment of diseases but also for rapid growth and development. |

| Feed antioxidants | They are used to protect the deterioration of other feed nutrients in the feed such as fats, vitamins, pigments, and flavoring agents, thus providing nutrient security to the animals. |

| Feed phytogenics | Phytogenics are natural substances, added to livestock feed to promote growth, aid in digestion, and act as anti-microbial agents. |

| Feed vitamins | They are used to maintain the normal physiological function and normal growth and development of animals. |

| Feed flavors and sweetners | These flavors and sweeteners help to mask tastes and odors during changes in additives or medications and make them ideal for animal diets undergoing transition. |

| Feed acidifiers | Animal feed acidifiers are organic acids incorporated into the feed for nutritional or preservative purposes. Acidifiers enhance congestion and microbiological balance in the alimentary and digestive tracts of livestock. |

| Feed minerals | Feed minerals play an important role in the regular dietary requirements of animal feed. |

| Feed binders | Feed binders are the binding agents used in the manufacture of safe animal feed products. It enhances the taste of food and prolongs the storage period of the feed. |

| Key Terms | Abbreviation |

| LSDV | Lumpy Skin Disease Virus |

| ASF | African Swine Fever |

| GPA | Growth Promoter Antibiotics |

| NSP | Non-Starch Polysaccharides |

| PUFA | Polyunsaturated Fatty Acid |

| Afs | Aflatoxins |

| AGP | Antibiotic Growth Promoters |

| FAO | The Food And Agriculture Organization of the United Nations |

| USDA | The United States Department of Agriculture |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms