Market Overview

| Study Period | 2018 - 2031 |

|---|---|

| Market Size (2026) | USD 8.76 Billion |

| Market Size (2031) | USD 10.78 Billion |

| Growth Rate (2026 - 2031) | 4.24% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

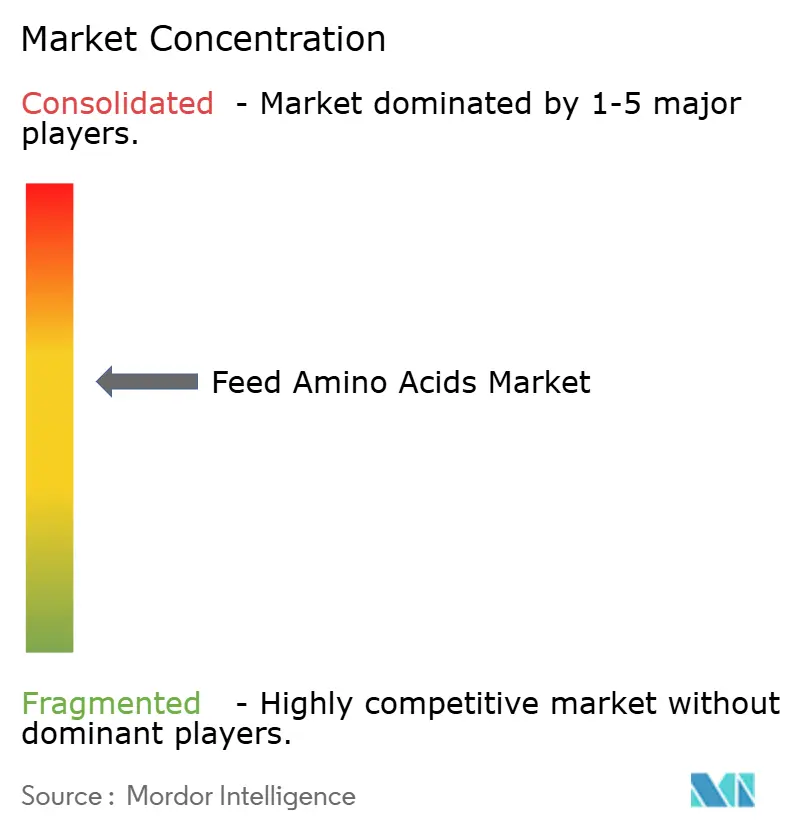

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Feed Amino Acids Market Analysis by Mordor Intelligence

The feed amino acids market size is expected to grow from USD 8.40 billion in 2025 to USD 8.76 billion in 2026 and is forecast to reach USD 10.78 billion by 2031 at 4.24% CAGR over 2026-2031. The growth reflects rising global demand for animal protein, tighter environmental rules that favor low-protein diets supplemented with synthetic amino acids, and steady advances in precision fermentation technologies. Market participants also benefit from robust investments in digital nutrition tools that fine-tune amino acid inclusion rates, improve feed conversion ratios, and cut nitrogen excretion. Competitive strategies focus on capacity expansions in cost-advantaged regions, while strict trade enforcement actions reshape supply chains and encourage locally diversified sourcing. The feed amino acids market continues to gain momentum as integrators align climate targets, consumer expectations, and profitability goals.

Key Report Takeaways

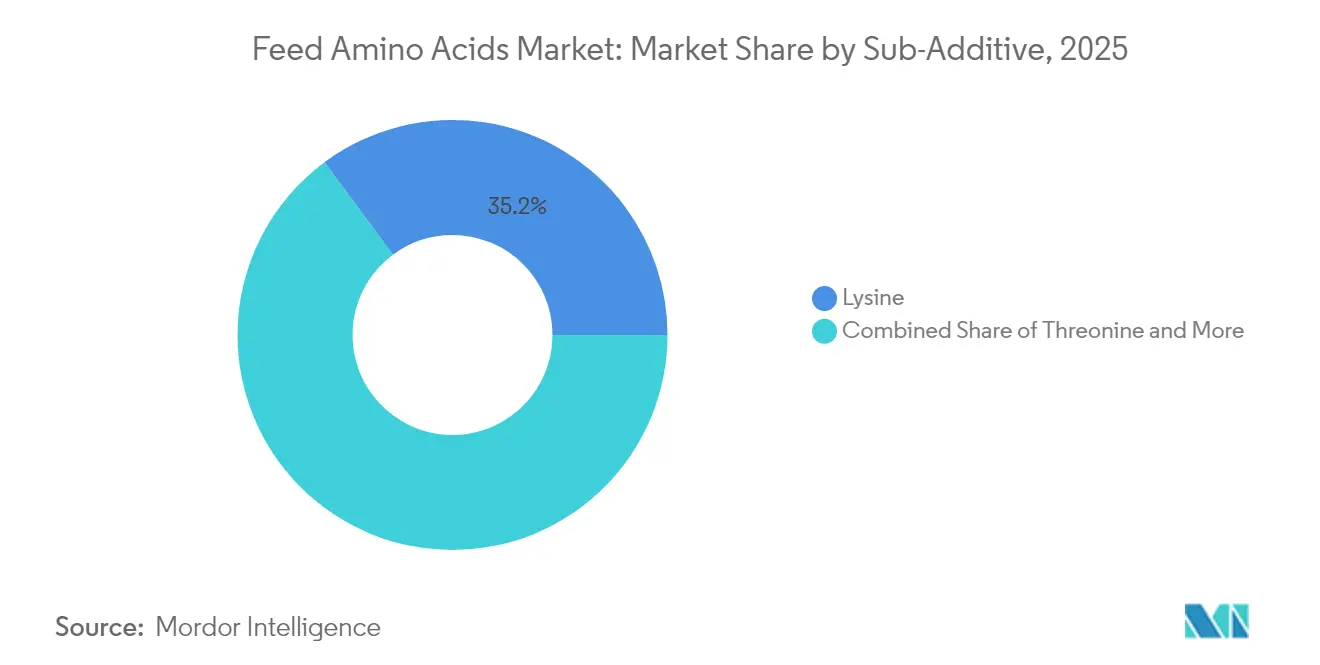

- By sub-additive, lysine led with 35.15% revenue share in 2025, while tryptophan is projected to grow at a 5.08% CAGR through 2031.

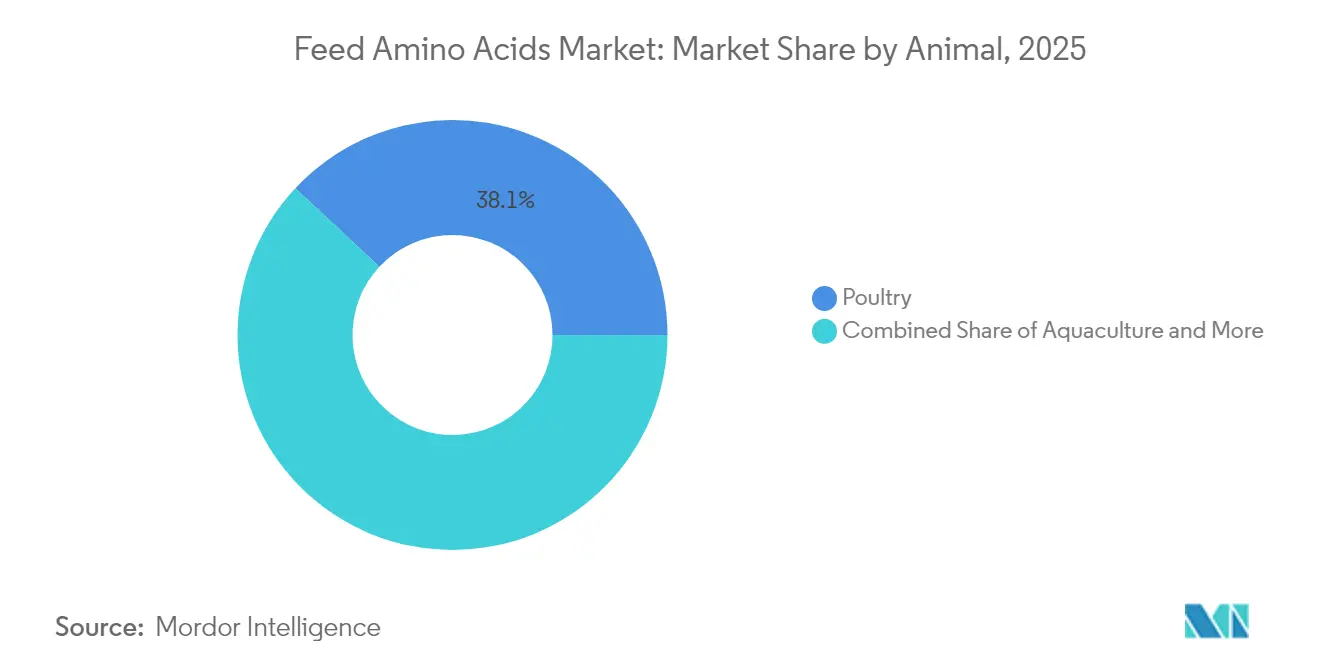

- By animal, poultry accounted for 38.05% of the feed amino acids market size in 2025, while aquaculture is projected to grow at a 4.29% CAGR to 2031.

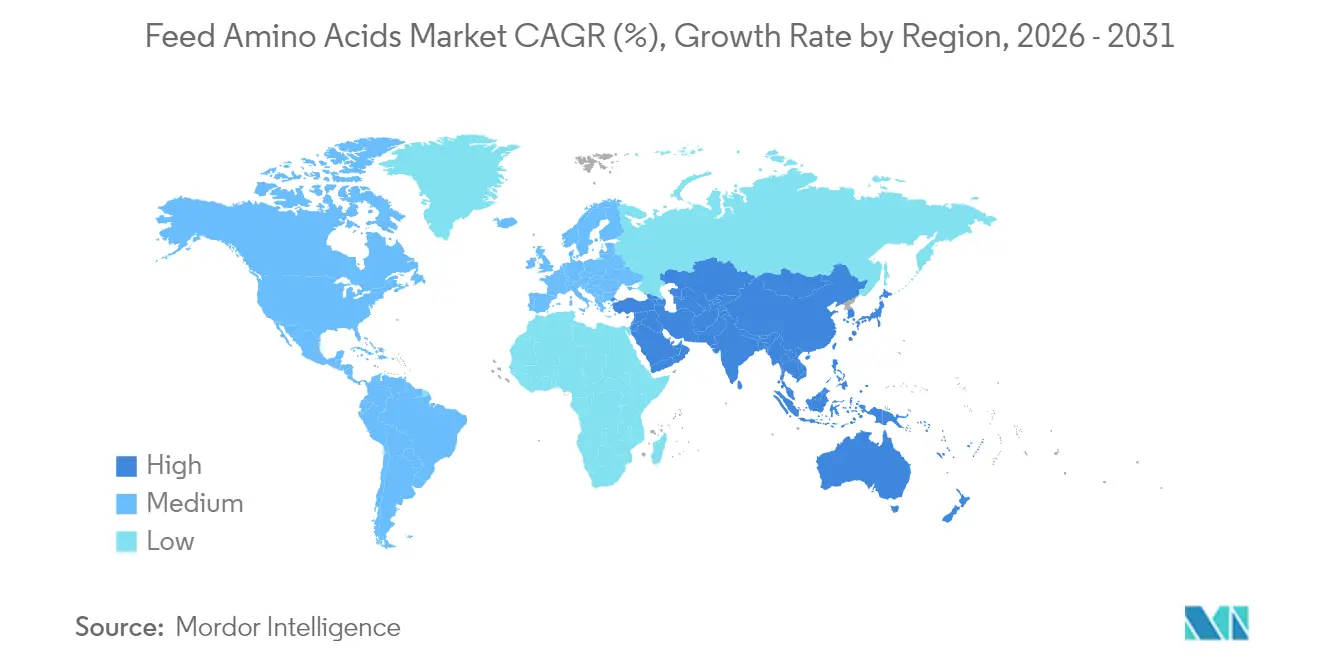

- By geography, Asia-Pacific commanded 30.15% share of the feed amino acids market size in 2025, while it Middle East is projected to grow at a 3.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Feed Amino Acids Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global meat and dairy demand | +1.8% | Global, with the strongest impact in Asia-Pacific and Africa | Medium term (2-4 years) |

| Regulatory push toward reduced crude-protein diets | +1.5% | Europe and North America primarily, expanding to the Asia-Pacific | Short term (≤ 2 years) |

| Cost-efficient fermentation technologies scaling in Asia | +1.2% | Asia-Pacific core, spill-over to global markets | Long term (≥ 4 years) |

| Ban on antibiotic growth promoters intensifying precision nutrition | +1.0% | Global, with early adoption in Europe and North America | Medium term (2-4 years) |

| Scope 3 emission targets adopted by integrators | +0.8% | North America and Europe, expanding globally | Long term (≥ 4 years) |

| Gene-edited cereal varieties with higher lysine content | +0.3% | North America and South America initially | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Meat and Dairy Demand

Escalating animal protein consumption, particularly in emerging economies, is fundamentally reshaping feed formulation strategies toward amino acid-centric approaches. Global meat production is projected to increase by 15% through 2030, with poultry leading growth at 18% and aquaculture expanding by 23% over the same period[1]Source: Food and Agriculture Organization, “The State of Food Security and Nutrition in the World 2024,” fao.org. This demand surge coincides with land and water resource constraints that necessitate higher feed conversion efficiency, positioning amino acids as critical tools for maximizing protein output per unit of feed input. The shift is most pronounced in Asia-Pacific markets, where rapid urbanization and rising incomes drive per-capita protein consumption increases of 3-5% annually. Feed manufacturers are responding by reformulating traditional high-crude-protein diets with targeted amino acid supplementation that reduces total protein requirements while maintaining or improving animal performance outcomes.

Regulatory Push Toward Reduced Crude-Protein Diets

Environmental regulations targeting nitrogen emissions from livestock operations are compelling feed manufacturers to embrace low-crude-protein formulations supplemented with synthetic amino acids. The European Union's Farm to Fork Strategy mandates 50% reduction in nutrient losses by 2030, directly impacting feed formulation practices across member states [2]Source: European Commission, “Farm to Fork Strategy,” europa.eu. Similar regulatory frameworks are emerging in North America, where state-level nitrogen management programs in California, Iowa, and North Carolina require livestock operations to demonstrate reduced environmental impact through improved feed efficiency. These regulations create a compliance-driven demand for amino acid supplementation that enables protein reduction without compromising animal performance. The regulatory influence extends beyond direct mandates, as voluntary sustainability commitments by major integrators increasingly incorporate amino acid-based strategies to achieve Scope 3 emission reduction targets.

Cost-Efficient Fermentation Technologies Scaling in Asia

Breakthrough fermentation technologies developed in China and Southeast Asia are dramatically reducing amino acid production costs while improving product quality and consistency. Advanced strain engineering techniques have increased lysine fermentation yields by 25-30% since 2023, while novel downstream processing methods reduce energy consumption by 15-20% compared to traditional approaches. Chinese manufacturers are leveraging these technological advances to expand global market share, particularly in cost-sensitive segments where price competitiveness determines adoption rates. The technology transfer is occurring through joint ventures and licensing agreements that enable established Western producers to integrate Asian innovations into their manufacturing processes. This technological convergence is anticipated to reduce global amino acid prices by 8-12% through 2028, accelerating adoption in price-sensitive markets while maintaining profitability for efficient producers.

Ban on Antibiotic Growth Promoters Intensifying Precision Nutrition

The global phase-out of antibiotic growth promoters is creating sustained demand for amino acid-based nutrition strategies that maintain animal performance without antimicrobial intervention. As per the World Health Organization, over 70 countries have implemented or announced restrictions on antibiotic use in livestock production, with major markets including the United States, European Union, and China leading the transition. This regulatory shift necessitates more sophisticated feed formulation approaches that optimize amino acid profiles to support immune function and growth performance. The transition is particularly challenging in intensive production systems where antibiotic growth promoters previously masked suboptimal nutrition, creating opportunities for amino acid suppliers to provide technical support and specialized formulations. Research demonstrates that balanced amino acid supplementation can achieve 85-95% of antibiotic growth promoter performance benefits while supporting regulatory compliance and consumer acceptance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile corn and dextrose prices | -1.2% | Global, with the strongest impact in North America and South America | Short term (≤ 2 years) |

| Anti-dumping probes on Chinese amino acids | -0.8% | North America and Europe primarily | Medium term (2-4 years) |

| Environmental limits on sulfate discharge in major producing hubs | -0.6% | Asia-Pacific and Europe | Medium term (2-4 years) |

| Limited efficacy of unprotected amino acids in ruminants | -0.4% | Global, with a focus on dairy-intensive regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Corn and Dextrose Prices

Feedstock price volatility significantly impacts amino acid production economics, particularly for fermentation-based processes that rely heavily on corn-derived dextrose as a primary carbon source. In 2025, corn prices have fluctuated between USD 4.29-4.58 per bushel over the past 2 months, directly impacting variation in amino acid production costs[3]Source: United States Department of Agriculture, “Agricultural Prices,” nass.usda.gov. This volatility is exacerbated by weather-related supply disruptions, biofuel demand competition, and export policy changes that create unpredictable cost structures for amino acid manufacturers. The impact is most severe for lysine and threonine production, where feedstock costs represent 35-45% of total manufacturing expenses. Producers are responding through feedstock diversification strategies, including alternative carbon sources and geographic supply chain optimization, but these adaptations require significant capital investment and operational restructuring.

Anti-Dumping Probes on Chinese Amino Acids

Trade enforcement actions targeting Chinese amino acid imports are reshaping global supply dynamics and creating price premiums in protected markets. The United States imposed anti-dumping duties ranging from 63.17% to 190.71% on Chinese lysine imports in 2024, while the European Union initiated similar investigations covering threonine and tryptophan. These measures reflect concerns about below-cost pricing that undermines domestic production capacity and market competition. The trade actions are forcing importers to diversify supply sources toward higher-cost producers in Europe, North America, and other Asian countries, creating supply chain disruptions and price increases of 20-35% for affected products. The regulatory influence extends beyond direct trade measures, as ongoing investigations create uncertainty that complicates long-term supply agreements and investment planning.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sub-Additive: Lysine Dominance Challenged by Specialty Amino Acid Growth

Lysine maintains its commanding 35.15% market share in 2025, reflecting its fundamental role as the first limiting amino acid in corn-soybean meal diets that dominate global feed formulations. The segment's established position is supported by mature fermentation technologies and competitive pricing that enable widespread adoption across poultry, swine, and aquaculture applications.

Tryptophan emerges as the fastest-growing segment at 5.08% CAGR through 2031, driven by increasing recognition of its dual functionality in protein synthesis and behavioral modification. Research demonstrates that tryptophan supplementation reduces aggressive behavior in group-housed animals while improving feed conversion efficiency, creating value propositions that justify premium pricing.

By Animal: Aquaculture Leads Growth While Poultry Maintains Volume Leadership

Poultry maintains its position as the largest animal segment with 38.05% market share in 2025, reflecting the sector's intensive production systems and well-established amino acid supplementation practices. The segment benefits from decades of research optimizing amino acid profiles for broiler growth and layer productivity, creating standardized formulation approaches that facilitate widespread adoption.

Aquaculture emerges as the fastest-growing segment at 4.29% CAGR, driven by the sector's rapid expansion and increasing adoption of amino acid-balanced formulations that improve feed conversion efficiency in fish and shrimp production. The segment's growth is supported by regulatory frameworks in major producing regions that mandate sustainable feed practices and environmental impact reduction. The regulatory influence includes Food and Drug Administration guidelines for aquaculture feed additives and European regulations on sustainable aquaculture practices that promote amino acid supplementation over fishmeal dependency.

Geography Analysis

Asia-Pacific commands 30.15% market share in 2025, anchored by China's dual role as the world's largest producer and consumer of feed amino acids. The region's dominance stems from established fermentation infrastructure, cost-competitive manufacturing capabilities, and intensive livestock production systems that drive domestic consumption. China, Thailand, Vietnam, and Indonesia represent rapidly growing consumption markets driven by expanding aquaculture and poultry sectors. India emerges as a significant growth driver within the region, with amino acid consumption increasing 12-15% annually as the country's livestock sector modernizes and adopts commercial feeding practices.

Europe holds a significant market share, characterized by mature markets with stringent regulatory frameworks that prioritize environmental sustainability and animal welfare considerations. The region's consumption patterns favor premium amino acid products with enhanced bioavailability and reduced environmental impact, supporting higher pricing levels that offset volume constraints. North America accounts for a prominent share of global consumption, driven by large-scale livestock operations that utilize sophisticated nutrition management systems and regulatory requirements that mandate environmental impact reduction through improved feed efficiency.

The Middle East represents the fastest-growing regional market at 3.42% CAGR, supported by government food security initiatives and expanding livestock production capacity in Saudi Arabia, UAE, and Iran. Africa follows with significant growth, driven by population growth, urbanization, and increasing animal protein consumption that necessitates more efficient livestock production systems. The regulatory influence in these emerging markets includes government subsidies for modern livestock facilities and import policies that favor amino acid supplementation over traditional protein sources.

Competitive Landscape

The feed amino acids market exhibits moderate concentration, with the top five players including Evonik Industries AG, IFF(Danisco Animal Nutrition), SHV (Nutreco NV), Archer Daniels Midland Co, and Adisseo, creating a competitive environment that balances scale advantages with innovation opportunities. Market leaders leverage integrated production capabilities and global distribution networks to maintain cost competitiveness while investing in next-generation fermentation technologies and application-specific formulations.

The recent investments in precision fermentation and sustainable production methods position the market leaders to capitalize on regulatory trends favoring environmental performance. Competitive strategies increasingly emphasize technological differentiation through enhanced bioavailability, targeted delivery systems, and application-specific formulations that address evolving customer requirements.

Companies are investing in digital platforms that provide real-time nutrition optimization and technical support services, creating value-added relationships that extend beyond commodity product sales. The regulatory influence includes ISO certification requirements, environmental compliance standards, and quality assurance protocols that favor established players with robust technical capabilities and regulatory expertise.

Feed Amino Acids Industry Leaders

Evonik Industries AG

IFF(Danisco Animal Nutrition)

SHV (Nutreco NV)

Adisseo

Archer Daniels Midland Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: Evonik Industries expanded its EUR 150 million (USD 162 million) methionine production capacity at its Singapore facility by 40%, targeting growing Asian aquaculture demand and positioning the company to capture market share from Chinese competitors facing trade restrictions.

- October 2022: The partnership between Evonik and BASF allowed Evonik certain non-exclusive licensing rights to OpteinicsTM, a digital solution to improve comprehension and reduce the environmental impact of the animal protein and feed industries.

- September 2022: The new 180,000-ton liquid methionine plant of Adisseo in Nanjing, China, started production. The facility is one of the largest global liquid methionine production capacities that boosted the penetration of liquid methionine manufactured by the company in the global market.

Global Feed Amino Acids Market Report Scope

Lysine, Methionine, Threonine, Tryptophan are covered as segments by Sub Additive. Aquaculture, Poultry, Ruminants, Swine are covered as segments by Animal. Africa, Asia-Pacific, Europe, Middle East, North America, South America are covered as segments by Region.By Sub-Additive

| Lysine |

| Methionine |

| Threonine |

| Tryptophan |

| Others |

By Animal

| Aquaculture | By Sub Animal | Fish |

| Shrimp | ||

| Other Aquaculture Species | ||

| Poultry | By Sub Animal | Broiler |

| Layer | ||

| Other Poultry Birds | ||

| Ruminants | By Sub Animal | Beef Cattle |

| Dairy Cattle | ||

| Other Ruminants | ||

| Swine | ||

| Other Animals |

By Geography

| Africa | By Country | Egypt |

| Kenya | ||

| South Africa | ||

| Rest of Africa | ||

| Asia-Pacific | By Country | Australia |

| China | ||

| India | ||

| Indonesia | ||

| Japan | ||

| Philippines | ||

| South Korea | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| Europe | By Country | France |

| Germany | ||

| Italy | ||

| Netherlands | ||

| Russia | ||

| Spain | ||

| Turkey | ||

| United Kingdom | ||

| Rest of Europe | ||

| Middle East | By Country | Iran |

| Saudi Arabia | ||

| Rest of Middle East | ||

| North America | By Country | Canada |

| Mexico | ||

| United States | ||

| Rest of North America | ||

| South America | By Country | Argentina |

| Brazil | ||

| Chile | ||

| Rest of South America |

| By Sub-Additive | Lysine | ||

| Methionine | |||

| Threonine | |||

| Tryptophan | |||

| Others | |||

| By Animal | Aquaculture | By Sub Animal | Fish |

| Shrimp | |||

| Other Aquaculture Species | |||

| Poultry | By Sub Animal | Broiler | |

| Layer | |||

| Other Poultry Birds | |||

| Ruminants | By Sub Animal | Beef Cattle | |

| Dairy Cattle | |||

| Other Ruminants | |||

| Swine | |||

| Other Animals | |||

| By Geography | Africa | By Country | Egypt |

| Kenya | |||

| South Africa | |||

| Rest of Africa | |||

| Asia-Pacific | By Country | Australia | |

| China | |||

| India | |||

| Indonesia | |||

| Japan | |||

| Philippines | |||

| South Korea | |||

| Thailand | |||

| Vietnam | |||

| Rest of Asia-Pacific | |||

| Europe | By Country | France | |

| Germany | |||

| Italy | |||

| Netherlands | |||

| Russia | |||

| Spain | |||

| Turkey | |||

| United Kingdom | |||

| Rest of Europe | |||

| Middle East | By Country | Iran | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| North America | By Country | Canada | |

| Mexico | |||

| United States | |||

| Rest of North America | |||

| South America | By Country | Argentina | |

| Brazil | |||

| Chile | |||

| Rest of South America | |||

Market Definition

- FUNCTIONS - For the study, feed additives are considered to be commercially manufactured products that are used to enhance characteristics such as weight gain, feed conversion ratio, and feed intake when fed in appropriate proportions.

- RESELLERS - Companies engaged in reselling feed additives without value addition have been excluded from the market scope, to avoid double counting.

- END CONSUMERS - Compound feed manufacturers are considered to be end-consumers in the market studied. The scope excludes farmers buying feed additives to be used directly as supplements or premixes.

- INTERNAL COMPANY CONSUMPTION - Companies engaged in the production of compound feed as well as the manufacturing of feed additives are part of the study. However, while estimating the market sizes, the internal consumption of feed additives by such companies has been excluded.

| Keyword | Definition |

|---|---|

| Feed additives | Feed additives are products used in animal nutrition for purposes of improving the quality of feed and the quality of food from animal origin, or to improve the animals’ performance and health. |

| Probiotics | Probiotics are microorganisms introduced into the body for their beneficial qualities. (It maintains or restores beneficial bacteria to the gut). |

| Antibiotics | Antibiotic is a drug that is specifically used to inhibit the growth of bacteria. |

| Prebiotics | A non-digestible food ingredient that promotes the growth of beneficial microorganisms in the intestines. |

| Antioxidants | Antioxidants are compounds that inhibit oxidation, a chemical reaction that produces free radicals. |

| Phytogenics | Phytogenics are a group of natural and non-antibiotic growth promoters derived from herbs, spices, essential oils, and oleoresins. |

| Vitamins | Vitamins are organic compounds, which are required for normal growth and maintenance of the body. |

| Metabolism | A chemical process that occurs within a living organism in order to maintain life. |

| Amino acids | Amino acids are the building blocks of proteins and play an important role in metabolic pathways. |

| Enzymes | Enzyme is a substance that acts as a catalyst to bring about a specific biochemical reaction. |

| Anti-microbial resistance | The ability of a microorganism to resist the effects of an antimicrobial agent. |

| Anti-microbial | Destroying or inhibiting the growth of microorganisms. |

| Osmotic balance | It is a process of maintaining salt and water balance across membranes within the body's fluids. |

| Bacteriocin | Bacteriocins are the toxins produced by bacteria to inhibit the growth of similar or closely related bacterial strains. |

| Biohydrogenation | It is a process that occurs in the rumen of an animal in which bacteria convert unsaturated fatty acids (USFA) to saturated fatty acids (SFA). |

| Oxidative rancidity | It is a reaction of fatty acids with oxygen, which generally causes unpleasant odors in animals. To prevent these, antioxidants were added. |

| Mycotoxicosis | Any condition or disease caused by fungal toxins, mainly due to contamination of animal feed with mycotoxins. |

| Mycotoxins | Mycotoxins are toxin compounds that are naturally produced by certain types of molds (fungi). |

| Feed Probiotics | Microbial feed supplements positively affect gastrointestinal microbial balance. |

| Probiotic yeast | Feed yeast (single-cell fungi) and other fungi used as probiotics. |

| Feed enzymes | They are used to supplement digestive enzymes in an animal’s stomach to break down food. Enzymes also ensure that meat and egg production is improved. |

| Mycotoxin detoxifiers | They are used to prevent fungal growth and to stop any harmful mold from being absorbed in the gut and blood. |

| Feed antibiotics | They are used both for the prevention and treatment of diseases but also for rapid growth and development. |

| Feed antioxidants | They are used to protect the deterioration of other feed nutrients in the feed such as fats, vitamins, pigments, and flavoring agents, thus providing nutrient security to the animals. |

| Feed phytogenics | Phytogenics are natural substances, added to livestock feed to promote growth, aid in digestion, and act as anti-microbial agents. |

| Feed vitamins | They are used to maintain the normal physiological function and normal growth and development of animals. |

| Feed flavors and sweetners | These flavors and sweeteners help to mask tastes and odors during changes in additives or medications and make them ideal for animal diets undergoing transition. |

| Feed acidifiers | Animal feed acidifiers are organic acids incorporated into the feed for nutritional or preservative purposes. Acidifiers enhance congestion and microbiological balance in the alimentary and digestive tracts of livestock. |

| Feed minerals | Feed minerals play an important role in the regular dietary requirements of animal feed. |

| Feed binders | Feed binders are the binding agents used in the manufacture of safe animal feed products. It enhances the taste of food and prolongs the storage period of the feed. |

| Key Terms | Abbreviation |

| LSDV | Lumpy Skin Disease Virus |

| ASF | African Swine Fever |

| GPA | Growth Promoter Antibiotics |

| NSP | Non-Starch Polysaccharides |

| PUFA | Polyunsaturated Fatty Acid |

| Afs | Aflatoxins |

| AGP | Antibiotic Growth Promoters |

| FAO | The Food And Agriculture Organization of the United Nations |

| USDA | The United States Department of Agriculture |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms