Feed Plant-based Protein Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

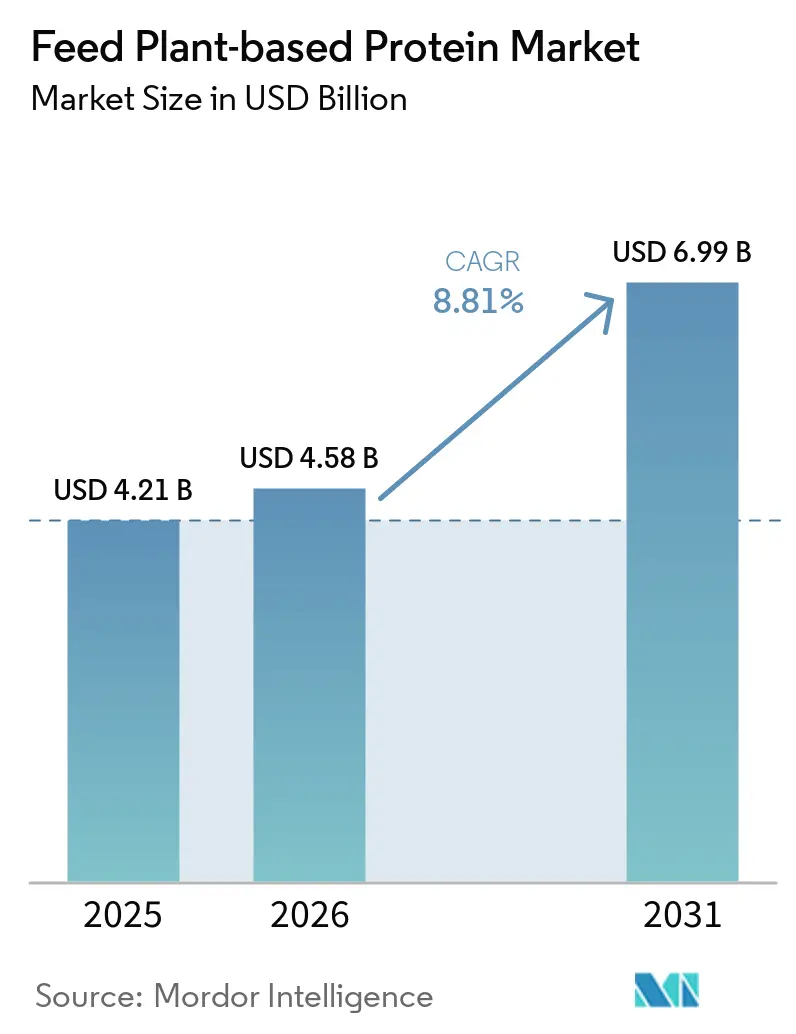

| Market Size (2026) | USD 4.58 Billion |

| Market Size (2031) | USD 6.99 Billion |

| Growth Rate (2026 - 2031) | 8.81% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Feed Plant-based Protein Market Analysis by Mordor Intelligence

The plant-based feed protein market was valued at USD 4.21 billion in 2025 and is projected to grow from USD 4.58 billion in 2026 to USD 6.99 billion by 2031, registering a CAGR of 8.81% between 2026 and 2031. The market growth is supported by rising demand for sustainable and cost-effective protein alternatives in animal nutrition, increasing adoption of plant-derived feed ingredients across livestock and aquaculture sectors. According to the Federal Reserve Bank of St. Louis, fishmeal prices rose from USD 1,625 per metric ton in November 2025 to over USD 2,010 per metric ton in February 2026. This price increase has improved the economic feasibility of using soy, pea, and wheat proteins in feed formulations. Feed costs, which account for nearly half of total animal production expenses, are encouraging nutrition teams to focus on protein sources that optimize cost, digestibility, and supply reliability. The market is further supported by increased investments from major processors, who are expanding production capacity for soy, sunflower, and pea proteins to achieve economies of scale and diversify raw material options. Regulatory compliance, amino acid balancing, and climate-related crop risks are projected to benefit suppliers with diversified sourcing and advanced processing capabilities. Conversely, smaller formulators may experience margin pressures due to rising traceability costs.

Key Report Takeaways

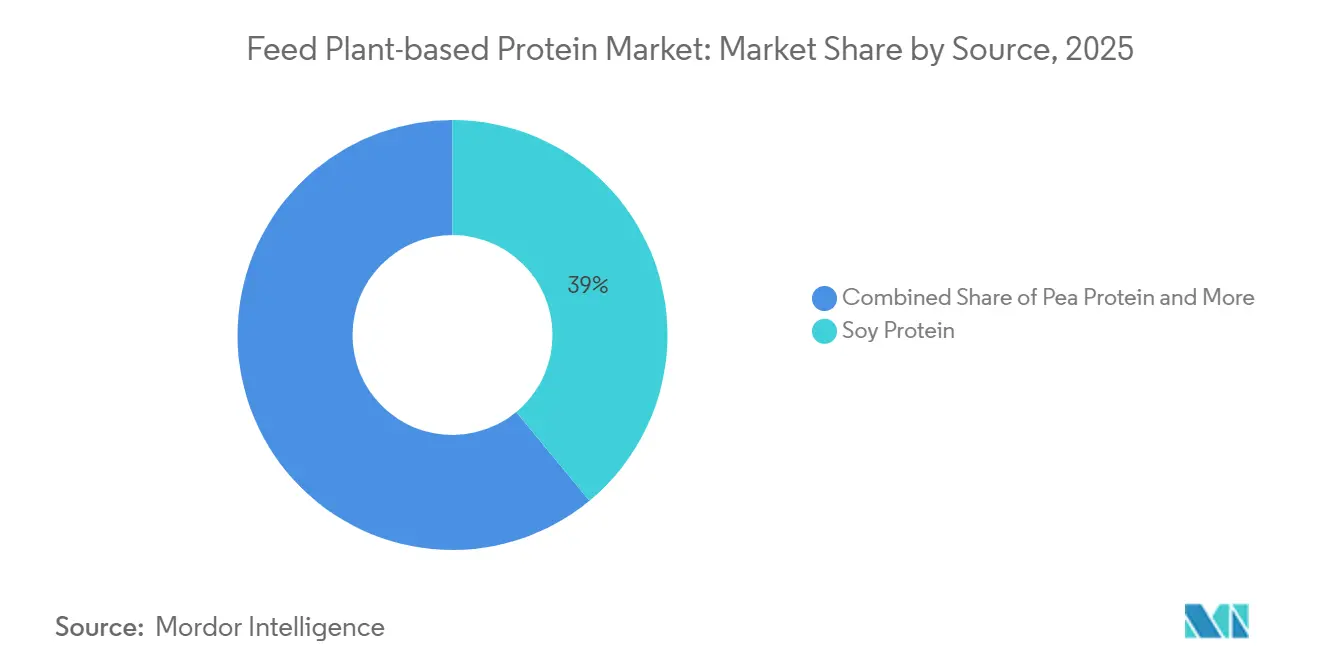

- By source, the feed plant-based protein market share for the soy protein segment accounted for the largest 39.0% in 2025, while the feed plant-based protein market size for the pea protein segment is projected to grow at the fastest 11.8% CAGR from 2026 to 2031.

- By livestock, the feed plant-based protein market share for the poultry segment held the largest 41.1% in 2025, while the feed plant-based protein market size for the aquaculture segment is forecast to grow at the fastest 9.7% CAGR from 2026 to 2031.

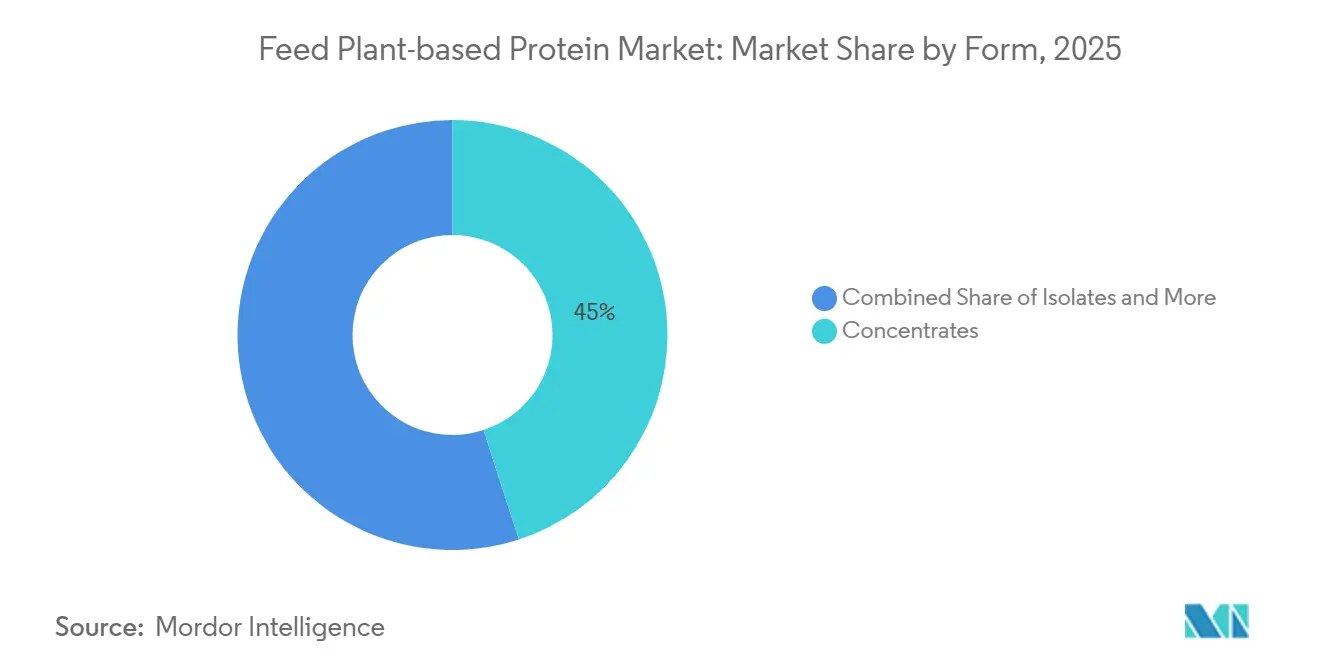

- By form, the feed plant-based protein market share for concentrates accounted for the largest 45.0% in 2025, while the feed plant-based protein market size for isolates is projected to grow at the fastest 10.6% CAGR from 2026 to 2031.

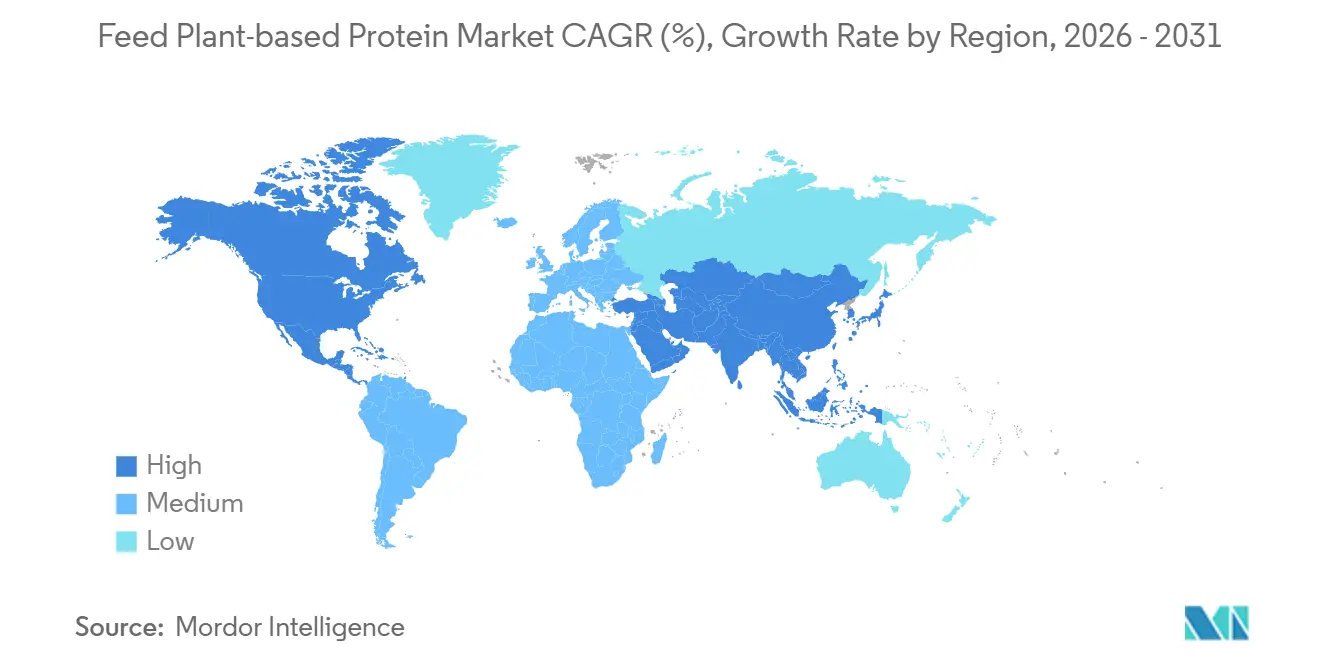

- By geography, the feed plant-based protein market share for North America held the largest 37.1% in 2025, while the feed plant-based protein market size for Asia-Pacific is forecast to grow at the fastest 8.9% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Feed Plant-based Protein Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for sustainable animal nutrition | +2.5% | Global | Long term (≥ 4 years) |

| Cost volatility in fishmeal and animal proteins | +2.0% | Global, with concentration in Asia-Pacific and South America | Short term (≤ 2 years) |

| Processing innovations enhancing digestibility | +1.5% | North America, Europe, and Asia-Pacific | Medium term (2-4 years) |

| Aquaculture feed capacity expansion | +1.2% | Asia-Pacific core, spill-over to South America and Africa | Medium term (2-4 years) |

| Corporate carbon-reduction commitments | +0.8% | North America and Europe | Long term (≥ 4 years) |

| Functional health benefits for antibiotic-free feeds | +0.6% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Sustainable Animal Nutrition

Rising demand for sustainable animal nutrition is supporting growth in the plant-based feed protein market because feed manufacturers and livestock producers are increasingly prioritizing lower-emission and traceable protein ingredients. According to Donau Soja, 54% of European Union soy intake complied with the European Feed Manufacturers' Federation Soy Sourcing Guidelines in 2025 [1]Source: Donau Soja, “European Soy Monitor 2025,” donausoja.org. This shift reflects stronger adoption of certified and sustainably sourced plant proteins across commercial feed supply chains. Feed producers are increasingly incorporating soy, pea, and wheat proteins into livestock and aquaculture formulations to align with sustainability targets, procurement standards, and carbon-reduction strategies within global animal nutrition systems.

Cost Volatility in Fishmeal and Animal Proteins

Cost fluctuations in fishmeal and animal proteins are driving increased demand for plant-based feed proteins, as feed manufacturers seek more cost-effective and stable protein alternatives for livestock and aquaculture diets. According to the Organisation for Economic Co-operation and Development and the Food and Agriculture Organization, Agricultural Outlook 2025-2034, global oilseed meal usage in aquaculture is projected to grow by 37%, reaching 11 million metric tons by 2034, while fishmeal usage is anticipated to increase by only 16% during the same period[2]Source: Organisation for Economic Co-operation and Development and Food and Agriculture Organization, “OECD-FAO Agricultural Outlook 2025-2034,” fao.org. This trend highlights the rising adoption of soy, pea, and wheat proteins in feed formulations, as producers focus on cost efficiency, supply reliability, and reducing reliance on marine-based protein sources.

Processing Innovations Enhancing Digestibility

Processing innovations are driving growth in the plant-based feed protein market, as advancements in fermentation and extrusion technologies enhance nutrient digestibility and protein availability in alternative feed ingredients. Research published by the Royal Society of Chemistry in 2025 indicates that thermoextrusion of pea protein isolates increased essential amino acid bioaccessibility from 42% to 59% in isolated form and from 53% to 61% after texturization. These technological advancements enable feed manufacturers to improve nutritional performance while broadening the application of plant-derived proteins in livestock and aquaculture diets. Enhanced digestibility and functional performance are also boosting the commercial viability of pea, soy, and wheat proteins within sustainable animal nutrition systems.

Aquaculture Feed Capacity Expansion

The expansion of aquaculture feed capacity is driving growth in the plant-based feed protein market, as fish and shrimp producers increasingly adopt alternative protein ingredients to enhance supply stability and feed sustainability. According to the Food and Agriculture Organization, aquaculture is projected to account for 56% of total global fisheries and aquaculture production by 2034, driving sustained demand for scalable feed proteins in commercial aquaculture systems. This growth is driving broader use of soy, pea, and wheat proteins in aquafeed formulations, as producers prioritize reliable, cost-efficient alternatives to marine-based proteins. The trend is particularly pronounced in the Asia-Pacific region, where intensive aquaculture production is rapidly expanding.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Amino-acid profile gaps versus animal proteins | -1.5% | Global | Long term (≥ 4 years) |

| Price sensitivity among feed formulators | -1.2% | Asia-Pacific, South America, and Africa | Short term (≤ 2 years) |

| Allergen concerns in soy-dominant rations | -0.8% | South America, North America, and Europe | Long term (≥ 4 years) |

| Climate-induced yield risk for feed crops | -0.7% | Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Amino-Acid Profile Gaps Versus Animal Proteins

Amino acid profile limitations continue to constrain growth in the plant-based feed protein market, as many plant-derived proteins are deficient in methionine and other sulfur-containing amino acids compared to animal-based proteins. Research published in Food and Function by the Royal Society of Chemistry in 2025 indicates that high-temperature texturization processing reduced lysine content in pea protein by up to 23.4%, underscoring the nutritional losses associated with protein processing[3]Source: Royal Society of Chemistry, “Impact of Thermoextrusion on Pea Protein Digestibility and Amino Acid Bioaccessibility,” pubs.rsc.org. These amino acid deficiencies complicate formulation in poultry, swine, and aquaculture diets, particularly for smaller feed manufacturers that lack advanced balancing capabilities and consistent access to supplemental amino acids.

Allergen Concerns in Soy-Dominant Rations

Concerns regarding allergens and antinutritional factors in soy-dominant feed formulations are limiting the growth of the plant-based feed protein market. Soybean-derived ingredients can negatively impact nutrient absorption, digestive efficiency, and overall feed performance in livestock systems. To address these issues, soy-heavy formulations often require additional processes such as fermentation, enzyme treatment, or thermal processing to reduce antinutritional compounds and enhance digestibility. These processes increase production complexity and operational costs for feed manufacturers. Furthermore, they pose formulation challenges in poultry, swine, and aquaculture diets, where maintaining nutrient balance and gut health is essential. Consequently, feed producers are increasingly exploring alternative plant protein sources to reduce reliance on soy-based formulations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Soy Protein Anchors Volume as Pea Protein Reshapes Sourcing Strategy

The feed plant-based protein market share for the soy protein segment accounted for the largest 39.0% in 2025. Soy protein remains the leading ingredient due to the established global soybean processing infrastructure, efficient supply chains, and compatibility with various livestock. Poultry, swine, and aquaculture producers continue to rely on soybean meal and soy concentrates because of their well-defined nutritional profiles, digestibility standards, and cost-effectiveness. Canola and wheat proteins play complementary roles in livestock diets, aiding in amino acid balancing and cost optimization. Additionally, large integrated processors benefit from mature soybean trading networks and the widespread availability of soy across global commercial feed markets.

The feed plant-based protein market size for the pea protein segment is projected to grow at the fastest 11.8% CAGR from 2026 to 2031. Pea protein is gaining traction due to its alignment with non-genetically modified feed programs, lower-emission sourcing strategies, and the diversification of protein sources beyond soy-dependent supply chains. Livestock and aquaculture feed manufacturers are increasingly incorporating pea proteins to enhance formulation flexibility and mitigate risks associated with soybean market fluctuations. Other alternative proteins, such as canola, wheat, fava bean, and lupin, are also gaining prominence in blended formulations, driven by growing emphasis on digestibility, amino acid composition, and sustainability considerations among global commercial feed producers.

By Livestock: Poultry Leads by Scale as Aquaculture Redefines Protein Specification

The feed plant-based protein market share for the poultry segment held the largest 41.1% in 2025. Poultry production remains the primary commercial application for plant-based feed proteins due to the consistently high-volume protein requirements of broiler and layer systems in industrial feed programs. Key ingredients such as soy protein concentrates, soybean meal, and wheat proteins form the foundation of global poultry nutrition systems. Large integrated poultry producers focus on scalable protein sourcing, predictable pricing, and stable digestibility to ensure feed-conversion efficiency and maintain production economics. Additionally, standardized formulation practices in poultry feed support the widespread adoption of plant-based proteins in commercial compound-feed manufacturing worldwide.

The feed plant-based protein market size for the aquaculture segment is forecast to grow at the fastest 9.7% CAGR from 2026 to 2031. Aquaculture producers are increasingly incorporating soy, pea, and wheat proteins into feed formulations due to rising fishmeal prices, sustainability concerns, and feed-security priorities. Shrimp and fish feed manufacturers are also focusing on improving digestibility, amino-acid balancing, and precision feed formulation to enhance production efficiency. While the swine and ruminant sectors remain significant demand centers, particularly for canola meal and blended protein concentrates, aquaculture continues to attract greater innovation. This is driven by the need for scalable and nutritionally efficient protein alternatives in intensive seafood farming globally.

By Form: Concentrates Command Scale as Isolates Drive Premium Value

The feed plant-based protein market share for concentrates accounted for the largest 45.0% in 2025. Concentrates remain the dominant form due to their balanced combination of protein content, cost-effective processing, and suitability for large-scale feed formulation. Commercial livestock producers extensively use concentrates in poultry, swine, and ruminant diets, where moderate protein purity meets commercial requirements. Additionally, concentrates are easier to produce in higher volumes compared to more refined protein forms, enhancing their cost competitiveness in mainstream feed applications. Textured proteins, while occupying a smaller share, are gaining traction in specialty feed formulations, addressing performance targets such as palatability, early-stage nutrition, and improved feed intake.

The feed plant-based protein market size for isolates is projected to grow at the fastest 10.6% CAGR from 2026 to 2031. Isolates are increasingly utilized in aquaculture and young-animal nutrition due to their higher protein purity, enhanced digestibility, and precise amino-acid profiles, which are critical for these applications. Technological advancements in extrusion, fermentation, and protein processing are further enhancing the functional performance and nutrient bioavailability of isolate-based feed ingredients. Premium feed formulations are driving the adoption of isolates, as producers focus on feed efficiency, gut health, and optimized nutrient absorption. This trend is boosting demand for high-value plant proteins in specialized livestock and aquaculture nutrition programs worldwide.

Geography Analysis

The feed plant-based protein market share for North America held the largest 37.1% in 2025. The region's dominance is attributed to the extensive soybean processing, canola crushing, and pea protein manufacturing infrastructure in the United States and Canada. Additionally, the presence of large integrated livestock and poultry industries supports consistent demand for plant-derived feed proteins within industrial feed systems. North America benefits from advanced agricultural logistics, export-oriented oilseed production, and significant feed-manufacturing capacity. Furthermore, growing investments in traceable sourcing and alternative proteins are enhancing regional production capabilities for pea, sunflower, and canola-based feed ingredients in commercial animal nutrition markets.

The feed plant-based protein market size for Asia-Pacific is projected to grow at the fastest 8.9% CAGR from 2026 to 2031. This rapid growth is driven by strong industrial livestock production, aquaculture expansion, and increased adoption of compound feed across countries such as China, India, Vietnam, and Southeast Asia. Europe also continues investing heavily in sustainable protein diversification and lower-emission feed systems supported by regulatory and research initiatives. Meanwhile, South America remains a key player, with Brazil and Argentina serving as major hubs for soybean production and exports. These regions are witnessing growing demand for scalable plant-based proteins as global livestock and aquaculture industries prioritize feed security and sustainable sourcing practices.

The Middle East and Africa currently represent a smaller share of the plant-based feed protein market. However, demand in these regions is increasing as feed security and formal livestock production become more significant. Gulf countries continue to depend heavily on imported plant proteins, highlighting the importance of long-term supply agreements and regional processing partnerships, particularly during periods of commodity market volatility. In Africa, the market remains limited in value, but key livestock-producing countries like Nigeria and South Africa are transitioning toward more industrialized feed formulation systems. Cowpeas present a viable regional protein source due to their nitrogen-fixing properties, drought tolerance, and nutritional benefits, which can be enhanced through processes such as fermentation or sprouting.

Competitive Landscape

The market is moderately fragmented overall, with higher concentration among large commodity processors and global oilseed suppliers. Companies such as Cargill, Incorporated, Archer Daniels Midland Company, Roquette Frères S.A., Wilmar International Limited, and Ingredion Incorporated maintain strong competitive positions through integrated capabilities in origination, crushing, processing, logistics, and feed ingredient supply. Competitive differentiation is increasingly driven by factors such as traceability, sustainable sourcing, protein diversification, and value-added processing, rather than solely by commodity volume. Smaller specialty suppliers compete by focusing on digestibility improvements, young-animal nutrition solutions, and premium plant-protein formulations tailored for specialized livestock applications worldwide.

Strategic investments are increasingly directed toward protein diversification, regional processing capacity, and sustainability compliance within commercial feed supply chains. Major ingredient manufacturers are reducing reliance on soy by investing in processing capabilities for pea, sunflower, canola, and specialty proteins. Traceability standards and deforestation-free sourcing requirements are becoming critical procurement considerations, particularly in the European and North American livestock feed industries. Companies with expertise in managing multi-origin sourcing, ensuring formulation consistency, and meeting regulatory compliance are enhancing their competitive positions in international feed markets. Additionally, research investments in fermentation, extrusion, and digestibility enhancement technologies are improving the performance characteristics of next-generation plant-derived feed proteins globally.

Competitive positioning is increasingly reliant on integrated sourcing capabilities, sustainability compliance, and processing specialization rather than the scale of commodity trading. For instance, Roquette Frères S.A. reported that its Manitoba facility achieved full operating capacity in 2026, with an annual processing capability of 125,000 metric tons of yellow peas. Large suppliers are also prioritizing investments in traceable sourcing, alternative crop proteins, and regional manufacturing expansion to enhance supply chain resilience. Market leadership is distributed across soy, pea, canola, and specialty proteins, as livestock producers increasingly demand diversified and sustainable plant-protein sourcing strategies within global feed systems.

Feed Plant-based Protein Industry Leaders

Cargill, Incorporated

Archer Daniels Midland Company

Roquette Frères S.A.

Wilmar International Limited

Ingredion Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Cargill, Incorporated made a USD 150 million investment to upgrade its sunflower processing facility in Saint-Nazaire, France. The upgrade focuses on transitioning production to high and super-high protein sunflower meal for the animal feed industry. This initiative is supported by the French Agency for Ecological Transition and the France 2030 program.

- March 2026: Bunge Global SA has completed the acquisition of International Flavors and Fragrances Inc.’s soy protein concentrate, lecithin, and soy crush business. This acquisition enhances Bunge's plant-based protein ingredient portfolio for applications in food, feed, and alternative proteins.

- March 2026: Royal Agrifirm Group B.V., acquired Hamlet Protein A/S to enhance its global specialties business in soy-based feed proteins for young animal nutrition. This acquisition broadens Agrifirm’s range of highly digestible plant-based protein ingredients and advanced nutritional solutions for livestock feed applications.

Global Feed Plant-based Protein Market Report Scope

Feed plant-based protein refers to protein ingredients obtained from crops like soy, peas, wheat, and canola, which are included in animal feed formulations. These proteins are utilized in diets for poultry, swine, ruminants, and aquaculture to promote growth, enhance feed efficiency, and offer sustainable alternatives to animal-derived protein sources. The feed plant-based protein market report is segmented by source (soy protein, pea protein, wheat protein, canola protein, and other sources), by livestock (poultry, swine, ruminant, aquaculture, and other livestocks), by form (concentrates, isolates, and textured proteins), and by geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The market forecasts are provided in terms of value (USD).

| Soy Protein |

| Pea Protein |

| Wheat Protein |

| Canola Protein |

| Other Sources |

| Poultry |

| Swine |

| Ruminant |

| Aquaculture |

| Others |

| Concentrates |

| Isolates |

| Textured Proteins |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Source | Soy Protein | |

| Pea Protein | ||

| Wheat Protein | ||

| Canola Protein | ||

| Other Sources | ||

| By Livestock | Poultry | |

| Swine | ||

| Ruminant | ||

| Aquaculture | ||

| Others | ||

| By Form | Concentrates | |

| Isolates | ||

| Textured Proteins | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is driving growth in plant-based feed protein demand through 2031?

Growth is being supported by higher fishmeal prices, rising meat production, broader use of compound feed, and stronger demand for lower-emission protein ingredients. The market size is projected to reach USD 6.99 billion by 2031.

Which livestock segment is expanding fastest for plant-based proteins?

Aquaculture will be the fastest-growing livestock segment, with a projected 9.7% CAGR from 2026 to 2031.

Which region leads current demand and which region is growing fastest?

North America led with the largest 37.1% of market share in 2025 due to strong soybean and pea processing capacity, while Asia-Pacific will forecast to expand fastest at an 8.9% CAGR from 2026 to 2031.

What are the main constraints limiting wider adoption in feed?

The key limits are amino acid gaps versus animal proteins, strong price sensitivity among feed formulators, soy allergen and antinutritional concerns, and climate-driven volatility in crop yields.

Page last updated on: