Photoelectric Sensor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.16 Billion |

| Market Size (2031) | USD 3.05 Billion |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Photoelectric Sensor Market Analysis by Mordor Intelligence

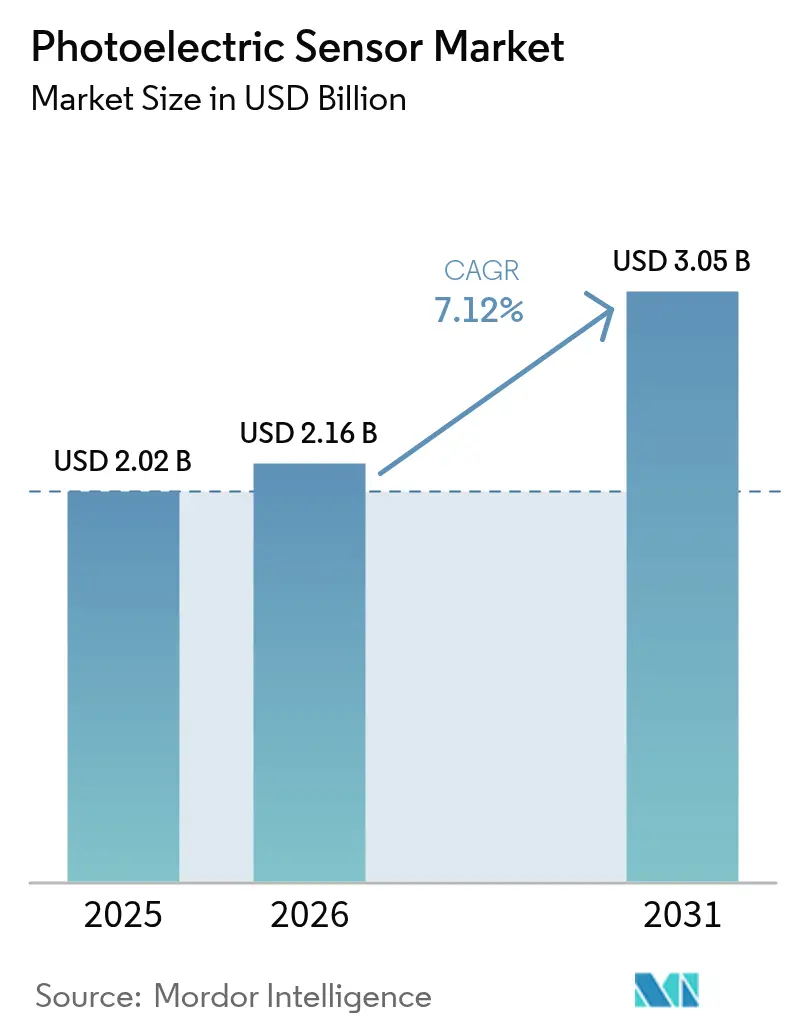

The photoelectric sensor market size is expected to grow from USD 2.02 billion in 2025 to USD 2.16 billion in 2026 and is forecast to reach USD 3.05 billion by 2031 at 7.12% CAGR over 2026-2031. This growth reflects a global pivot toward hyper-automated production lines that rely on precise object detection and positioning. Wider access to government tax credits for smart-factory retrofits, rapid Industry 4.0 rollouts, and declining prices for high-power laser emitters are reinforcing demand. Industrial users also benefit from AI-enabled self-calibration that cuts maintenance labour requirements by close to 30%, pushing total cost of ownership down. Quality-driven sectors such as food, beverage, and pharmaceuticals now view safety-rated photoelectric sensors as non-negotiable, particularly after the introduction of the new IEC 61496-5 standard.

Key Report Takeaways

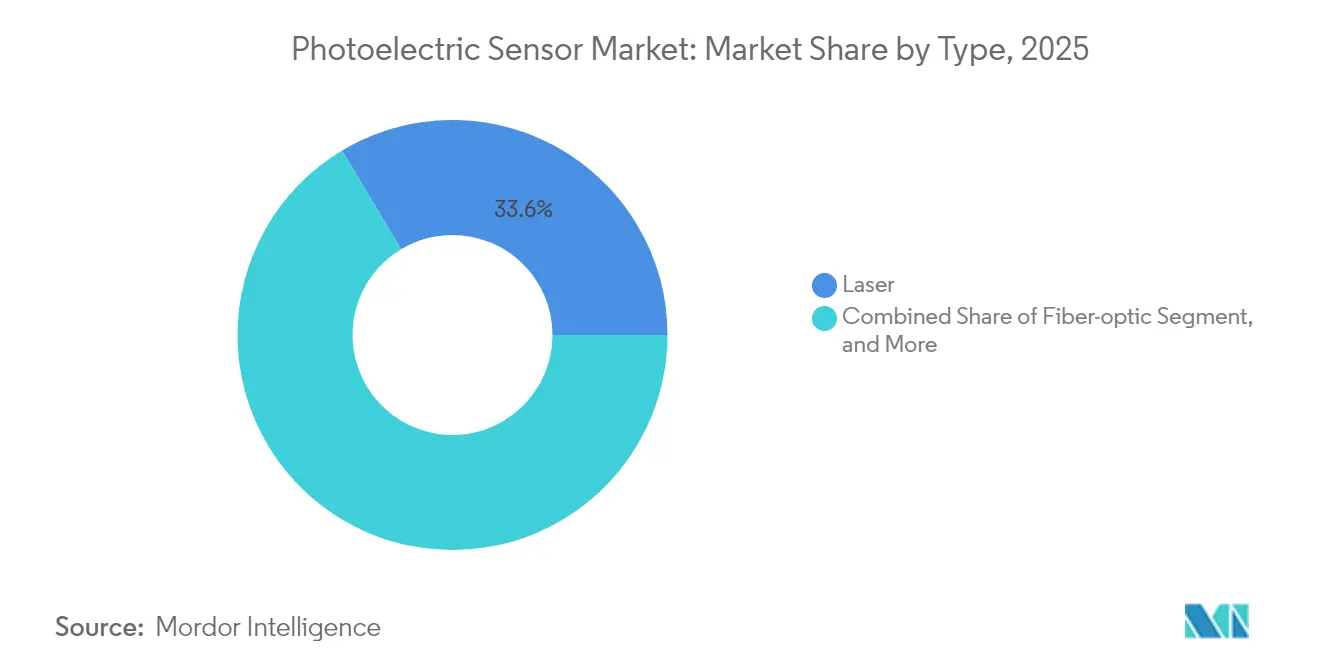

- By product category, laser sensors held a 33.58% photoelectric sensor market share in 2025 while background-suppression sensors are set to grow at a 10.05% CAGR from 2026-2031.

- By detection technology, through-beam solutions commanded 40.62% of the photoelectric sensor market size in 2025, whereas background-suppression will lead growth.

- By housing style, cylindrical units captured 44.32% photoelectric sensor market share in 2025 while PCB-mount devices are forecast to expand at 10.62% CAGR through 2031.

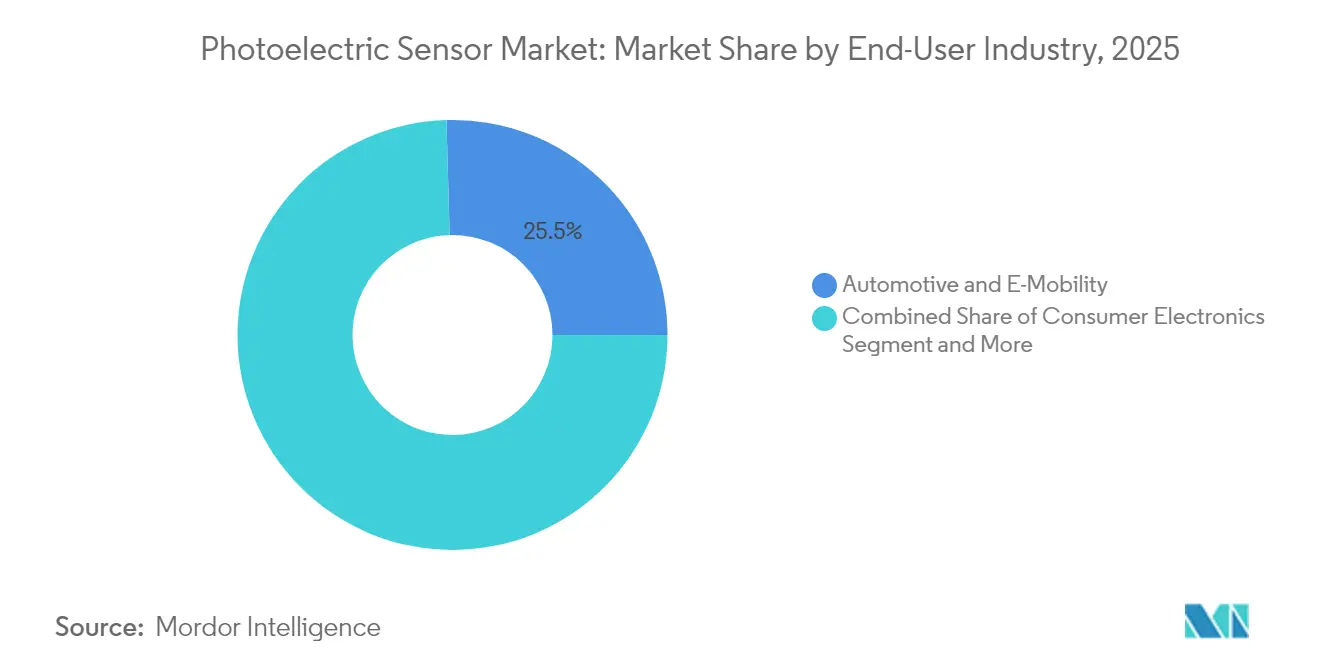

- By end-user industry, automotive and e-mobility represented 25.45% of the photoelectric sensor market size in 2025; pharmaceuticals and medical devices will grow fastest at 11.88% CAGR to 2031.

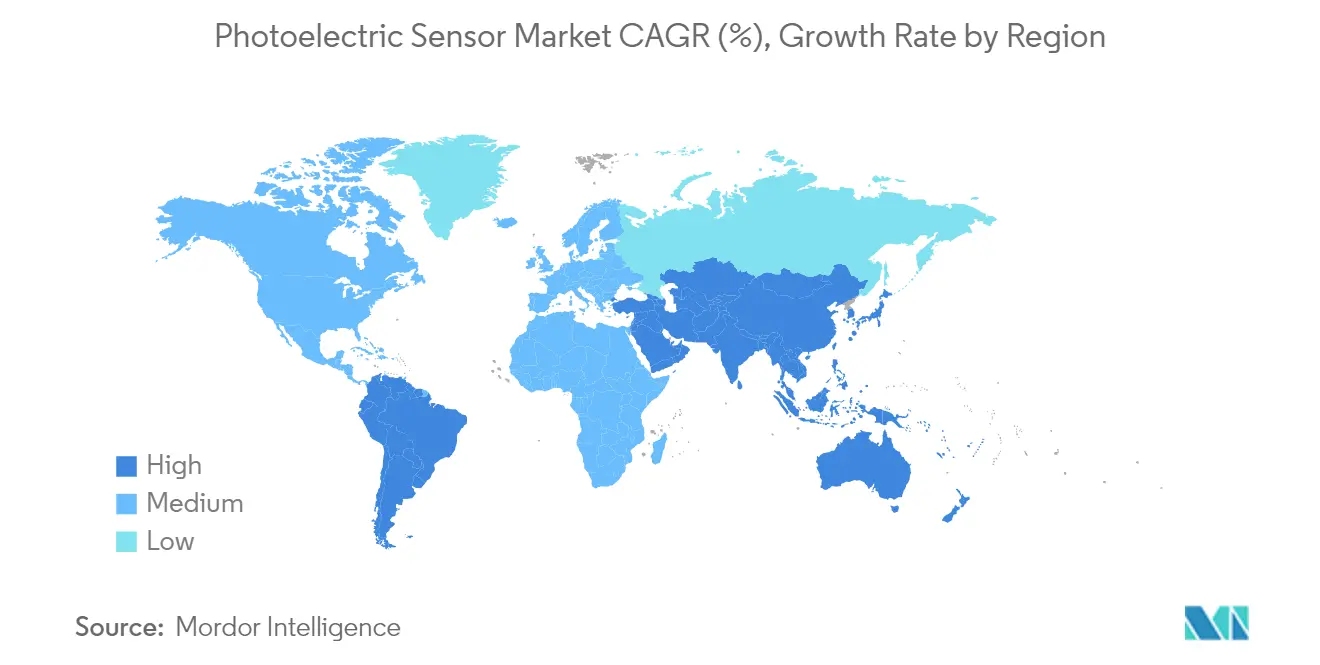

- By geography, APAC led with 47.40% revenue share in 2025 while the Middle East is projected to register a 13.12% CAGR for 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Photoelectric Sensor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated deployment of Industry 4.0 production lines | 1.80% | Global, with APAC and Europe leading adoption | Medium term (2-4 years) |

| Government tax-credit programmes for smart-factory retrofits | 1.20% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Falling ASP of high-power red-laser emitters | 0.90% | Global manufacturing hubs | Long term (≥ 4 years) |

| Rapid shift to zero-defect packaging lines in F&B | 1.10% | Global, concentrated in developed markets | Medium term (2-4 years) |

| New IEC 61496-5 safety-rated photoelectric standards | 0.70% | Global, mandatory compliance regions first | Short term (≤ 2 years) |

| AI-enabled self-calibration reducing maintenance labour | 1.00% | Advanced manufacturing economies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerated Deployment of Industry 4.0 Production Lines

Factories are weaving dense networks of smart sensors that feed real-time data into edge controllers and cloud platforms, allowing predictive maintenance routines that slash unplanned downtime by as much as 30%. Photoelectric sensors furnish high-frequency positional feedback to robotic arms and conveyor systems, permitting adaptive control that limits waste and energy consumption. The IO-Link protocol has become a de-facto digital interface, making it possible to stream diagnostic parameters straight into ERP dashboards. Line installers in APAC report payback periods of less than 18 months on sensor upgrades because higher uptime compensates for initial hardware costs. Broader availability of “plug-and-produce” photoelectric devices further reduces commissioning effort, helping small and mid-size manufacturers adopt industrial automation.

Government Tax-Credit Programmed for Smart-Factory Retrofits

The United States continues to expand federal RandD credits and allows accelerated depreciation for automation hardware under Section 179D. Similar stimulus measures in the European Union funnel up to 20% of project spending into cash rebates when firms add energy-efficient, safety-rated sensors. Germany’s BMBF-funded “Fusion 2040” programme set aside EUR 650 million to support integrated sensor platforms for advanced manufacturing. Local authorities in South Korea and Singapore follow suit with grant schemes that reimburse employee training tied to digital transformation. These incentives are bringing forward purchase decisions and supporting multi-line retrofits that might otherwise have been delayed.

Falling ASP of High-Power Red-Laser Emitters

Recent advances in gallium arsenide nano-ridge technology enable 780 nm diodes to achieve 71% wall-plug efficiency, bringing unit prices down by more than 15% in two years. Manufacturers now fabricate III-V light sources directly on 300 mm silicon wafers, unlocking semiconductor-style economies of scale. Hydrogen plasma passivation also boosts slope efficiency in blue laser diodes, widening application boundaries to opaque and reflective targets. As device costs slide, laser-based photoelectric sensors enter mainstream packaging, logistics, and mobile-robot platforms, opening addressable market segments that once belonged solely to infrared units.

Rapid Shift to Zero-Defect Packaging Lines in F and B

Food processors implement 100% inspection regimes to comply with global safety codes. High-speed photoelectric arrays inspect bottle caps and seals at rates exceeding 3,000 units per minute, recording dimensional data for every SKU batch. Hyperspectral extensions validate chemical composition, eliminating contamination events that previously triggered costly recalls. Machine-learning classifiers residing at the edge re-tune light thresholds on the fly, preserving detection reliability during changeovers and across ambient lighting fluctuations. The resulting waste reduction improves margins and supports corporate sustainability targets, strengthening the business case for extensive sensor deployments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Uptake of low-cost 3D ToF cameras in short-range picking | -0.80% | Global, concentrated in logistics and e-commerce | Medium term (2-4 years) |

| High replacement rate in wash-down environments | -0.50% | Food processing and pharmaceutical regions | Short term (≤ 2 years) |

| Volatile gallium-arsenide spot prices | -0.60% | Global semiconductor supply chains | Short term (≤ 2 years) |

| Fragmented OEM interface protocols | -0.40% | Global, affecting system integration | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Uptake of Low-Cost 3D ToF Cameras in Short-Range Picking

Time-of-flight arrays such as Teledyne’s 832 × 600-pixel Hydra3D now deliver sub-millimetre depth accuracy and run at 416 fps, letting robotic cells identify irregular loads in chaotic bins. Their falling price narrows the gap with premium photoelectric sensors in logistics and warehouse operations. The ability to perceive full point clouds gives integrators freedom to cut sensor counts. Nonetheless, photoelectric sensors remain ahead in high-speed pass-fail detection on conveyor belts, keeping displacement risk confined to specific 3D-vision use cases.

Volatile Gallium-Arsenide Spot Prices

China refines roughly 98% of global gallium, the core feedstock for many laser diodes. Export controls introduced in 2024 sent spot rates soaring 150% within six months. The US Geological Survey projects that a 30% supply disruption would shave USD 602 billion off US GDP. Sensor manufacturers now secure multi-year contracts, increase recycled content, or explore alternative emitter materials like GaAsP quantum wells. While mitigation efforts are advancing, material volatility continues to raise bill-of-materials risk and slows price reductions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Laser Dominance Driven by Precision Demands

Laser photoelectric sensors commanded a 33.58% photoelectric sensor market share in 2025, reflecting their unrivalled accuracy and long sensing ranges. The segment is forecast to record a 8.95% CAGR, raising the laser photoelectric sensor market size for this segment to USD 1.13 billion by 2031. Price erosion in high-power red-laser dies makes these devices viable even in cost-sensitive production cells. Automotive power-train lines deploy self-contained CMOS laser units with 500 mm detection distance to confirm gear-wheel seating. Fiber-optic variants secure positions in welding booths where electromagnetic noise threatens conventional electronics. The proliferation of IO-Link-enabled models means line operators collect live signal strength and contamination alarms for predictive cleaning schedules. Parallel structured light innovations offer multi-beam coverage that improves detection through dust, reducing false trips.

Emerging retro-reflective array sensors blend easy setup with wide beam reach, useful in carton-forming machines and palletizers. Miniaturization progresses each quarter as gallium arsenide nano-ridge emitters shrink optical packages and trim thermal loads. Suppliers introduce stainless-steel IP69K housings that withstand caustic wash-down cycles in dairy filling rooms. Combined, these advances underpin strong forward momentum and keep the laser category at the centre of the photoelectric sensor market.

By Detection Technology: Background-Suppression Gains Momentum

Through-beam devices held 40.62% revenue in 2025, forming the backbone of high-speed press lines and canning operations. They remain favoured where open mounting is possible and total reliability is paramount. Background-suppression sensors will outpace rivals at 10.05% CAGR, enlarging their photoelectric sensor market size from USD 548 million in 2026 to USD 885 million by 2031. Their optical design isolates the target within a narrow distance window, preventing false positives from conveyors or enclosures. Robotics integrators specify these sensors on automated guided vehicles for docking accuracy within ±1 mm. Retro-reflective versions support space-restricted conveyors that permit only one-sided mounting, retaining their simplicity with their installation simplicity.

Ongoing R&D focuses on ASIC-driven adaptive thresholds that let background-suppression units learn surface finishes and compensate for ambient light drift. IO-Link channels expose hysteresis parameters to the PLC, letting control engineers fine-tune detection curves without manual potentiometer twists. Diffuse sensors survive where ambient light is stable, serving cost-oriented packaging OEMs that bundle sensors into entry-level machines. Across detection technologies, artificial intelligence algorithms increasingly prune false signals and report contaminant buildup, raising system reliability in dusty, high-speed settings.

By End-User Industry: Pharmaceuticals Lead Growth Trajectory

Automotive and e-mobility manufacturing controlled 25.45% of the photoelectric sensor market size in 2025, driven by stringent tolerance tracking and growing electric vehicle volumes. Over 450 sensors outfit a single battery-pack assembly line to verify cell orientation and presence. Pharmaceuticals and medical devices will register a 11.88% CAGR, reflecting rigorous inspection mandates under GMP and FDA Title 21. Vision inspection systems leveraging background-suppression sensors count up to 3,000 tablets each minute while logging serialisation codes. Food and beverage plants continue to demand IP69K devices that handle caustic sodium hydroxide wash-downs. Consumer electronics suppliers employ mini-PCB sensors to confirm camera lens insertion at sub-millimetre accuracy.

The pharmaceutical surge is intensified by a global shift to continuous manufacturing, where zero-defect output is mandatory. Multi-spectrum photoelectric sensors authenticate pill coating thickness, a task formerly requiring batch sampling. Hyperspectral overlays verify active ingredient distribution, aligning with real-time release testing strategies. These use cases add momentum and revenue, making healthcare the prime engine of incremental growth for the photoelectric sensor market.

By Housing/Mounting Style: Miniaturization Drives PCB-Mount Growth

Cylindrical M8–M30 bodies held 44.32% of the photoelectric sensor market in 2025 because their threaded barrels simplify retrofit installation in existing brackets. Miniature PCB-mount sensors will expand at 10.62% CAGR, reflecting accelerated pull from compact electronic assembly lines and mobile-robot makers. Integration teams value tiny footprints that hide within gripper jaws or pick-and-place heads, freeing exterior space for vision cameras and cables. Rectangular housings remain popular where mechanical alignment jigs lock onto square faces, such as bottling lines. Slot and fork formats detect labels and textile edges at high rates.

Material science advances bring new IP69K-rated plastics that shrug off chemical detergent wash-downs in meat processing. Stainless steel casings now receive PEEK window inserts that resist scratching while passing FDA rules. Quick-disconnect M12 connectors reduce swap times and enhance uptime. The availability of uniform mounting adapters allows device interchangeability across brands, cutting engineering hours during line upgrades. All factors combined cement a healthy growth outlook for compact and rugged housing categories inside the photoelectric sensor market.

Geography Analysis

APAC controlled 47.40% of revenue in 2025 as China, Japan, and South Korea invested heavily in intelligent factories. Government incentives, especially China’s “Made in China 2025” programme, repay up to 50% of capital expenses on smart equipment, accelerating sensor adoption. Domestic robot makers embed photoelectric detection in pick-and-place modules for smartphone assembly. Japan’s precision machinery builders rely on high-end laser models that discern micron-level edges on semiconductor wafers.

The Middle East will grow fastest at 13.12% CAGR. Saudi Arabia’s Vision 2030 supports fresh metal-processing and chemical complexes that specify Industry 4.0 connectivity from day one. Emerson’s 13,000 m² Dammam hub now manufactures control systems with integrated measurement instrumentation, including photoelectric sensors. UAE smart-city pilots deploy outdoor-rated retro-reflective sensors to automate parking guidance and waste-handling chutes, opening non-industrial revenue channels.

North America and Europe post steady gains as reshoring of critical supply chains and sustainability mandates drive upgrades. US food processors increase inline inspection to meet FSMA regulations. German automotive OEMs embrace predictive maintenance on assembly lines, embedding IO-Link sensors that stream diagnostics into MES platforms. South America and Africa remain nascent but rising industrial wages push firms to install basic automation, presenting long-term potential for cost-competitive diffuse sensors.

Competitive Landscape

The landscape remains moderately concentrated. Omron, Keyence, SICK, and Banner Engineering collectively hold close to 45% revenue through broad portfolios and strong channel coverage. These leaders pivot toward AI-embedded firmware and cloud hooks that enrich aftermarket services. SICK and Endress+Hauser formed a joint venture in 2024 to merge sensor strength with process analytics, creating a one-stop shop for flow and gas measurement solutions. Omron’s new South Carolina plant broadens US footprint and reduces lead times for custom sensor variants.

Midsize challengers exploit niches in harsh-environment sensing and miniaturised optics. Coherent’s high-efficiency CW lasers supply many start-ups that package ultracompact photoelectric heads. Zebra’s 2024 purchase of Photoneo injected 3D vision know-how, permitting integrated solutions that compete against time-of-flight cameras in logistics. Market consolidation continues as distributors such as Graybar Canada absorb regional players to gain application engineering talent. Certification around IEC 61496-5 tightens entry barriers, advantaging firms with in-house safety labs.

Emerging players experiment with gallium-free emitters to bypass supply constraints and differentiate on sustainability metrics. Partnerships with IIoT platforms such as Siemens MindSphere and PTC ThingWorx allow sensor vendors to monetize data services. Competitive intensity is expected to remain moderate, with price pressures offset by value-added software and predictive maintenance offerings.

Photoelectric Sensor Industry Leaders

Omron

Keyence

Sick AG

Schneider Electric

Panasonic

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Chart Industries and Flowserve announced an all-stock merger creating a USD 19 billion enterprise value company with USD 300 million cost synergies.

- June 2025: Applied Industrial Technologies acquired IRIS Factory Automation to bolster material handling workflows that rely on machine vision.

- June 2025: Crane Company agreed to buy Precision Sensors and Instrumentation from Baker Hughes for USD 1.06 billion to expand aerospace and nuclear sensing portfolios.

- April 2025: Hamamatsu Photonics unveiled the InGaAs camera C16741-40U for near-infrared inspection at Automate 2025.

Global Photoelectric Sensor Market Report Scope

A photoelectric sensor is an equipment that is used to discover the distance, absence, or presence of an object by using a light transmitter. It consists of an emitter and receiver for emitting light and receiving light. Photoelectric sensors detect objects, changes in surface conditions, and other items through a variety of optical properties.

| Laser |

| Fiber-optic |

| LED/Infra-red |

| Retro-reflective Array |

| Through-beam |

| Retro-reflective |

| Diffuse |

| Background-suppression |

| Cylindrical (M8-M30) |

| Rectangular / Cubic |

| Slot / Fork |

| Miniature PCB-mount |

| Consumer Electronics |

| Automotive and E-Mobility |

| Food and Beverages |

| Packaging Machinery OEMs |

| Pharmaceuticals and Medical Devices |

| Building and Smart Infrastructure |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type | Laser | |

| Fiber-optic | ||

| LED/Infra-red | ||

| Retro-reflective Array | ||

| By Detection Technology | Through-beam | |

| Retro-reflective | ||

| Diffuse | ||

| Background-suppression | ||

| By Housing / Mounting Style | Cylindrical (M8-M30) | |

| Rectangular / Cubic | ||

| Slot / Fork | ||

| Miniature PCB-mount | ||

| By End-user Industry | Consumer Electronics | |

| Automotive and E-Mobility | ||

| Food and Beverages | ||

| Packaging Machinery OEMs | ||

| Pharmaceuticals and Medical Devices | ||

| Building and Smart Infrastructure | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the photoelectric sensor market?

The photoelectric sensor market stood at USD 2.16 billion in 2026 and is projected to hit USD 3.05 billion by 2031.

Which region dominates revenue in the photoelectric sensor market?

APAC led with 47.40% revenue share in 2025 due to extensive manufacturing automation in China, Japan, and South Korea.

Which detection technology will grow fastest through 2031?

Background-suppression sensors will post a 10.05% CAGR between 2026 and 2031, outpacing other detection methods.

Why are laser photoelectric sensors gaining share?

Falling prices for high-power red-laser emitters and superior precision make laser sensors attractive for automotive, packaging, and electronics applications.

How are government incentives affecting adoption?

Tax credits and grants in the United States, European Union, and parts of APAC reduce upfront costs for Industry 4.0 retrofits, accelerating sensor deployment.

What is the biggest end-user growth opportunity?

Pharmaceutical and medical device manufacturers will expand sensor use at 11.88% CAGR as stringent inspection requirements drive 100% production monitoring.

Page last updated on: