Water and Wastewater Sensors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

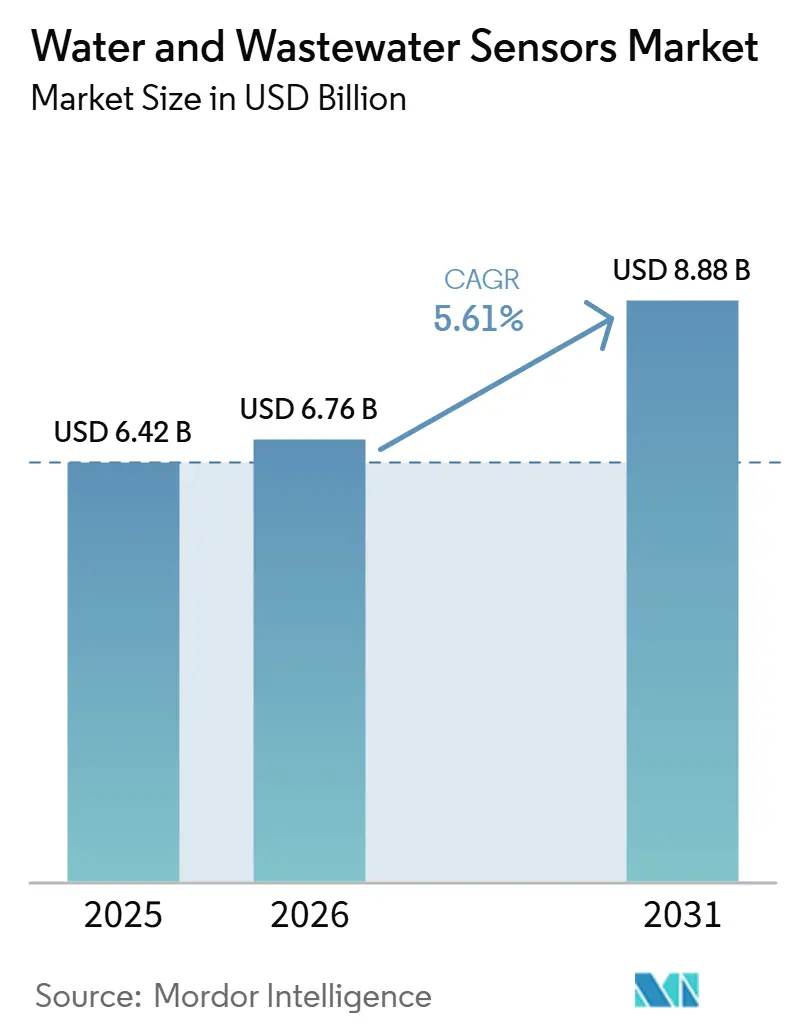

| Market Size (2026) | USD 6.76 Billion |

| Market Size (2031) | USD 8.88 Billion |

| Growth Rate (2026 - 2031) | 5.61% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Water and Wastewater Sensors Market Analysis by Mordor Intelligence

The Water And Wastewater Sensors Market size is projected to expand from USD 6.42 billion in 2025 and USD 6.76 billion in 2026 to USD 8.88 billion by 2031, registering a CAGR of 5.61% between 2026 to 2031.

Growth is being propelled by utilities that are switching from periodic grab sampling to continuous, edge-enabled monitoring, a move that cuts contamination-detection times from days to minutes. Lower bill-of-materials costs for optical and micro-electromechanical-systems (MEMS) parts, the spread of edge artificial intelligence, and tightening global discharge rules collectively reinforce demand. Competitive tactics now center on embedding machine-learning inference in probe housings, letting suppliers promise higher uptime through performance-based contracts. The Asia-Pacific region dominates shipments, yet Africa exhibits the fastest trajectory, as donor-funded smart-metering projects bundle turbidity and conductivity sensors with prepaid billing modules. Headline risks stem from capital-heavy retrofits, a global shortage of calibration talent, and cybersecurity gaps in cloud-connected probes.

Key Report Takeaways

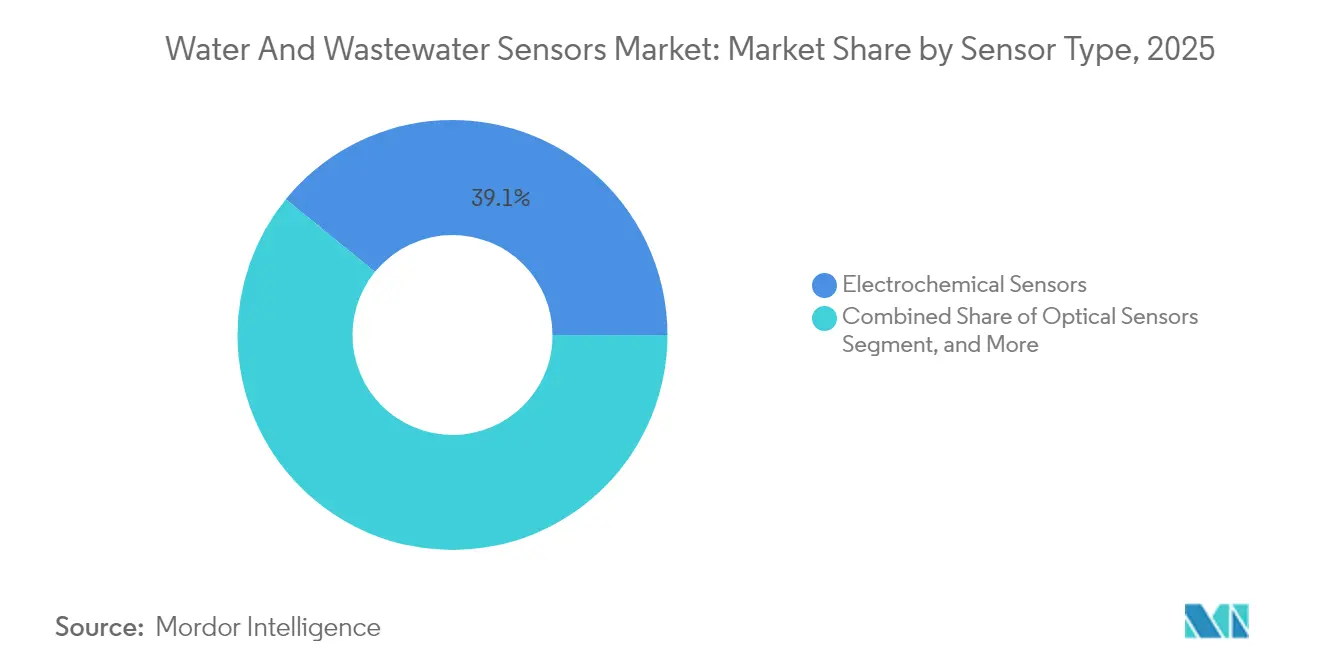

- By sensor type, electrochemical sensors led the water and wastewater sensors market share, accounting for 39.12% of the revenue in 2025. Meanwhile, optical sensors are projected to grow at an 8.31% CAGR through 2031.

- By parameter monitored, pH held 32.55% of the water and wastewater sensors market share in 2025, while dissolved-oxygen probes posted the fastest growth at an 8.61% CAGR to 2031.

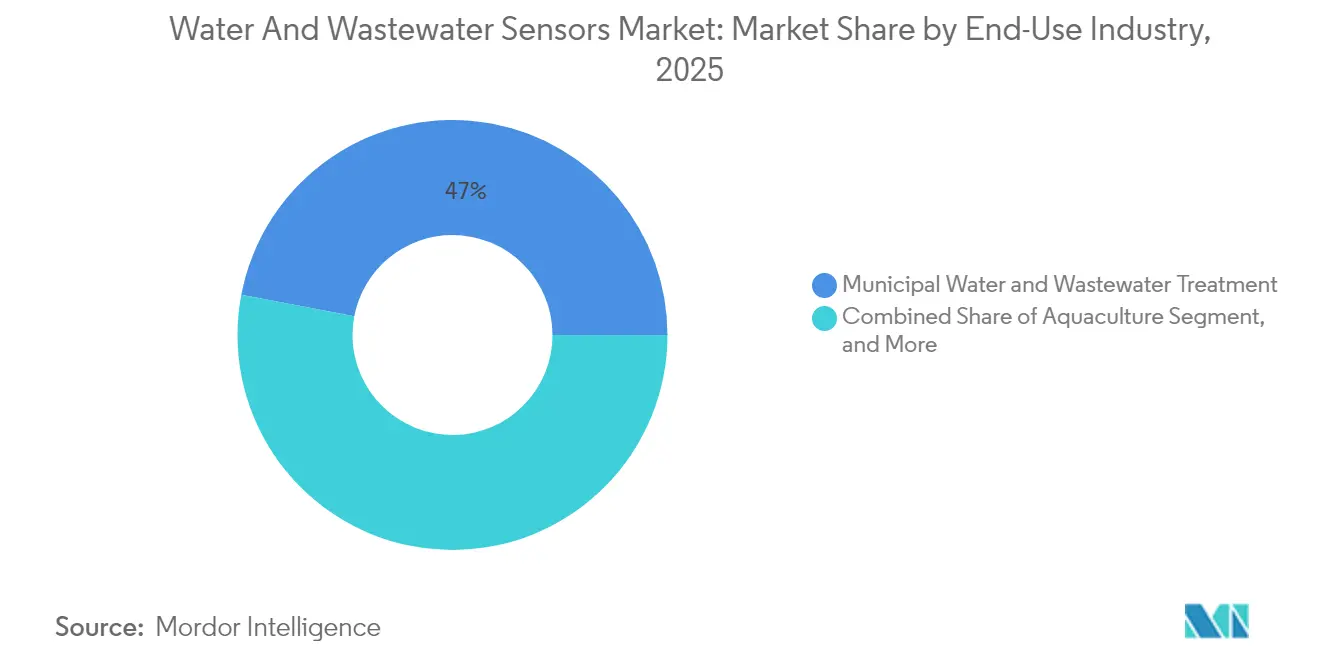

- By end-use industry, municipal water and wastewater treatment captured 47.01% of the water and wastewater sensors market share in 2025, while aquaculture is advancing at an 8.44% CAGR, due to recirculating systems that require real-time oxygen and pH oversight.

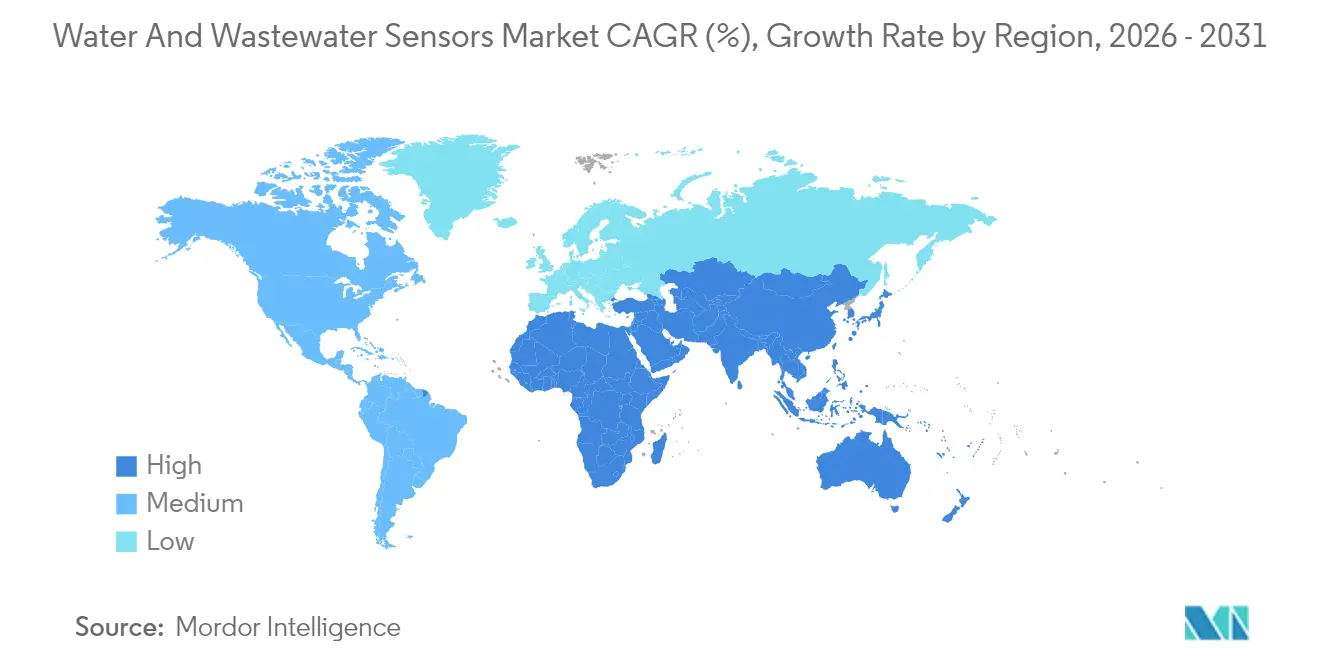

- By geography, the Asia-Pacific region commanded 35.22% of the water and wastewater sensors market share in 2025, and is set to achieve an 8.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Water and Wastewater Sensors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Digitization of Water Utilities | +1.2% | Global with early adoption in North America and Europe | Medium term (2-4 years) |

| Tightening Industrial Discharge Regulations | +1.0% | Asia-Pacific core, expanding into Middle East and Africa | Long term (≥ 4 years) |

| Rapid Expansion of Smart Irrigation Networks | +0.9% | North America, Australia, Middle East | Short term (≤ 2 years) |

| Cost Decline of Optical and MEMS Components | +0.8% | Global | Short term (≤ 2 years) |

| Integration of Edge AI for On-Site Detection | +0.7% | North America, Europe, China | Medium term (2-4 years) |

| Rise of Performance-Based Contracts | +0.6% | Europe, North America with spill-over to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Digitization Of Water Utilities

Continuous sensor networks now feed live data into digital twins, letting operators simulate process changes before rolling them out at full scale. The United States Environmental Protection Agency’s 2024 cybersecurity guidance obliges utilities that deploy networked probes to segment operational and information-technology traffic, raising entry barriers for small municipalities while speeding consolidation.[1]United States Environmental Protection Agency, “Cybersecurity Guidance for Drinking Water Systems,” epa.gov Xylem’s 2023 purchase of Evoqua formed a vertically integrated platform combining probes, managed calibration, and analytics, a blend that utilities prefer because it centralizes accountability. Cloud dashboards provide regional views of turbidity, conductivity, and oxidation-reduction potential; however, Europe’s data-protection laws are prompting the migration of inference workloads from the cloud to local gateways to avoid cross-border data transfers. Edge-embedded analytics reduce latency, shrink bandwidth costs, and cut regulatory complexity, turning the sensor node into the primary decision point. This digitization wave anchors the water and wastewater sensors market as a strategic lever rather than a compliance checkbox.

Tightening Industrial Discharge Regulations

Governments across the Asia-Pacific region have upgraded effluent rules for heavy metals, biochemical oxygen demand, and suspended solids, obliging factories to install multi-parameter probes at their outlet pipes. China now mandates the installation of round-the-clock chemical-oxygen-demand analyzers at every industrial park in the Yangtze River Economic Belt, affecting more than 15,000 facilities.[2]Ministry of Ecology and Environment, “Industrial Discharge Monitoring Requirements,” mee.gov.cn India’s Central Pollution Control Board requires textile and drug plants to log readings every 15 minutes and trigger alarms within 30 seconds. These directives compress decision cycles, forcing the adoption of electrochemical and optical sensors that can run unattended for months. Demand is spilling over to the Middle East, where Saudi Arabia’s utility regulator now requires continuous monitoring of boron and bromide at desalination outlets. Tougher limits underline why the water and wastewater sensors market continues to expand at a healthy pace.

Rapid Expansion of Smart Irrigation Networks

Precision farming is prompting growers to integrate soil-moisture, salinity, and nutrient probes with variable-rate control valves, resulting in up to 30% reduction in water use without compromising yields.[3]United States Department of Agriculture, “Precision Agriculture Water Efficiency,” usda.gov Australia’s Murray-Darling Basin Authority requires telemetry-enabled flow meters before granting allocations, thereby accelerating the adoption of capacitive and time-domain-reflectometry sensors. Middle East initiatives pair field sensors with satellite imagery, giving growers early warnings of stress and triggering automated irrigation cycles. Vendors now supply solar-powered, LoRaWAN-connected units that communicate over kilometers for pennies per month, opening acreage previously beyond cellular networks. The smart-irrigation surge feeds incremental volumes into the water and wastewater sensors market, especially in arid regions where water security drives technology budgets.

Cost Decline Of Optical And MEMS Components

Since 2020, optical dissolved-oxygen probes have seen a 40% reduction in bill of materials, drawing level with electrochemical alternatives in total cost of ownership. High-volume automotive and consumer electronics runs have driven down MEMS pressure sensor pricing, enabling water market suppliers to integrate sub-$1 chips. Hach released a fluorescence turbidity probe in 2024 at 25% below the price of legacy nephelometric units while promising twice the service life. Chinese players, such as those from Hubei Sensorthings, undercut Western incumbents by 30–40%, although questions about long-term drift persist. Altogether, lower prices open the water and wastewater sensors market to utilities in Africa and South America that had long relied on manual test kits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital-Intensive Retrofitting of Legacy Plants | -0.5% | Global, acute in aging infrastructure regions | Medium term (2-4 years) |

| Scarcity of Skilled Calibration Technicians | -0.3% | Africa, South America, rural Asia-Pacific | Long term (≥ 4 years) |

| Data-Security Concerns in Cloud Probes | -0.4% | North America, Europe | Short term (≤ 2 years) |

| Limited Sensor Longevity in High-Salinity Effluents | -0.3% | Middle East, coastal industrial zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Capital-Intensive Retrofitting Of Legacy Plants

Modernizing plants built decades ago often entails power upgrades, communications cabling, and parallel operations while new and old systems overlap, a package that can exceed USD 500,000 for mid-sized utilities. European operators must also translate heritage supervisory control and data acquisition protocols into modern fieldbus standards, which inflates deployment hours. Smaller municipalities cope by rotating shared sensor trailers across multiple sites, yet this compromises continuous oversight and slows incident response. Budget rigidity, therefore, delays adoption and tempers short-term gains in the water and wastewater sensors market.

Scarcity Of Skilled Calibration Technicians

Optical and MEMS probes require specialized reference solutions, firmware updates, and drift checks that differ from those used with traditional membrane electrodes. Sub-Saharan Africa has fewer than 2,000 certified technicians for an installed base exceeding 50,000 probes, forcing utilities to import vendor service teams that book weeks in advance. South American operators sometimes skip quarterly calibrations altogether or reuse expired calibration solutions, which undermines data integrity. Vendors seek to offset the gap with self-calibrating probes, but these add 15–20% to the list price and still require occasional verification. Until training pipelines expand, technician scarcity will moderate growth in the water and wastewater sensors market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sensor Type: Electrochemical Reliability And Optical Upsurge

Electrochemical sensors retained 39.12% of the 2025 revenue, thanks to sub-10-second response times, which are critical for pH and ion-selective electrode control loops. Optical designs are growing at an 8.31% CAGR, primarily because luminescent dissolved-oxygen probes overcome membrane fouling and provide year-long calibration stability. Ultrasonic units address open-channel flow and sludge-blanket depth, avoiding biofouling because no wetted parts intrude. Capacitive probes excel at level detection in oil-water separators, where dielectric contrasts sharpen accuracy. Other niche formats hold less than 5% combined share but solve specialty measures such as ammonia and volatile organic compounds.

Utilities are gravitating toward optical options after tiring of membrane swaps every three to six months in high-solids basins. Yokogawa’s dual-wavelength probe, launched in 2024, counters turbidity interference and stretches calibration to 12 months. Even so, electrochemical cells remain relevant for parts-per-billion trace-metal targets, where stripping voltammetry paired with ion-selective electrodes achieves sensitivities that optical methods cannot. Regulatory alignment with ISO 10530 ensures a durable demand floor, allowing both sensor families to coexist within the water and wastewater sensors market.

By Parameter Monitored: pH Dominance and Dissolved-Oxygen Momentum

pH captured 32.55% of 2025 revenue because corrosion control, coagulation, and biological stability all hinge on constant hydrogen-ion monitoring. Dissolved-oxygen probes are projected to grow at an 8.61% CAGR through 2031, driven by stricter biochemical oxygen demand ceilings that require plants to maintain aerobic conditions around the clock. Turbidity tracking underpins filtration performance and compliance with the Safe Drinking Water Act, while conductivity probes serve as total dissolved solids meters and cooling-tower sentinels. Oxidation-reduction potential sensors fine-tune chlorine dosing and detect early fouling in reverse-osmosis membranes.

Multi-parameter sondes often incorporate temperature chips to compensate for readings, a requirement established by Standard Methods for the Examination of Water and Wastewater. Specialty measures such as chlorophyll a, nitrate, and free chlorine satisfy growing niches in reservoir and aquaculture oversight. Shrimp and salmon farms utilizing biofloc and recirculating systems now base their profitability on milligram-per-liter precision, a trend that highlights why dissolved-oxygen monitoring is the fastest-growing segment within the broader water and wastewater sensors market.

By End-Use Industry: Municipal Bedrock And Aquaculture Sprint

Municipal treatment plants accounted for 47.01% of 2025 spending, primarily due to statutory monitoring at intake, clarification, and discharge points. Aquaculture is racing ahead at an 8.44% CAGR, benefitting from land-based recirculating designs that pack fish at densities tenfold above pond norms yet rely on sensor-based automation to avert hypoxia. Industrial users, from petrochemicals to food processing, adopt probes to avoid fines and recycle water. Environmental agencies deploy portable kits for catchment oversight, with the United States Geological Survey operating 8,000 real-time stations.

Municipal utilities are increasingly offering sensor-as-a-service to neighboring industries, monetizing their calibration expertise and data systems. Meanwhile, large salmon growers in Norway and Chile equip each tank with redundant probes to ensure oxygen accuracy of 0.5 milligrams per liter, a specification that surpasses many legacy electrodes. These dynamics position aquaculture as the fastest-growing demand node in the water and wastewater sensors market.

Geography Analysis

The Asia-Pacific region delivered 35.22% of global revenue in 2025 and continues to combine component manufacturing strength with the largest pool of new installations. China enforces 15-minute reporting intervals at industrial parks along the Yangtze River Economic Belt, cementing a home-market advantage for domestic probe makers. India’s Jal Jeevan Mission deploys turbidity and residual-chlorine probes at village plants, though patchy power and scarce service staff shorten sensor uptimes. Japan focuses on replacing aging sensors from the 1980s, buoying local champions such as Yokogawa.

Africa is forecast to grow, anchored by donor-funded smart-metering programs in Nairobi, Lagos, and Addis Ababa that bundle flow, pressure, turbidity, and conductivity sensors. South Africa mandates continuous monitoring for plants serving more than 10,000 residents, yet funding gaps delay rollouts. Egypt’s new administrative capital features a fully instrumented network that other North African cities now benchmark.

North America and Europe exhibit steady, but slower growth as operators shift their focus toward analytics layers that extract added value from mature hardware fleets. The United States Environmental Protection Agency’s 2024 security rules accelerate upgrades to secure field protocols, favoring vendors with both sensors and cyber-hardened gateways. Germany pilots digital twins that integrate sensor feeds with hydraulic models, trimming unplanned downtime by 30%. The Middle East buys specialized boron analyzers and fouling monitors for desalination trains that supply over 70% of municipal water. South American growth is driven by Brazilian and Argentine farms that utilize soil-moisture networks to meet European sustainability certifications.

Competitive Landscape

The water and wastewater sensors market is moderately concentrated. Xylem, Hach, Endress+Hauser, and ABB collectively command roughly 40–45% of the global market share, but hundreds of regional firms compete for municipal tenders and industrial projects. Tier-1 suppliers pursue end-to-end platforms: Xylem’s USD 7.5 billion acquisition of Evoqua fused probes, treatment gear, and managed services into one invoice. Hach’s Claros software now unites dissolved-oxygen, turbidity, and pH data across multiple plants, delivering automated compliance reports.

Technology is the main battleground. Endress+Hauser patents target self-calibrating optical probes with built-in edge AI, while Yokogawa’s new liquid analyzer supports four sensors and anomaly detection at the gateway. Thermo Fisher introduced a turbidity sensor that verifies calibration in situ without process removal, cutting labor by 50%. Startups such as In-Situ and Aquaread focus on aquaculture, promising milligram-level oxygen accuracy at price points palatable to growers.

Cost disruptors include Chinese entrants like Hubei Sensorthings, exporting cut-rate multi-parameter sondes to Africa and South America. European niche firms, such as Libelium, sell solar-powered buoys that stream sensor data over satellite connections into reservoir dashboards. Compliance with ISO 17025 calibration and IEC 61010 electrical safety remains a gating factor, tilting awards toward incumbents with certified service centers. Overall, rivalry hinges on striking a balance between unit cost, calibration intervals, and predictive analytics in a market where utilities are increasingly outsourcing risk through performance-based contracts.

Water and Wastewater Sensors Industry Leaders

Xylem Inc.

Hach Company

Horiba Ltd.

ABB Ltd.

Yokogawa Electric Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Yokogawa Electric acquires a 30% stake in Norwegian startup BlueSensor AS to integrate high-precision dissolved-oxygen probes for recirculating aquaculture systems into the FLXA analyzer line.

- June 2025: ABB completes a six-month field trial of its optical boron analyzer at Saudi Arabia’s Ras Al Khair desalination complex and announces global production availability for Q4 2025.

- March 2025: Endress+Hauser launches the Memosens 4.0 portfolio, unifying digital communications and edge-AI self-calibration across optical dissolved-oxygen, pH, and conductivity probes for municipal utilities.

- January 2025: Xylem Inc. begins full-scale commercial rollout of the Xylem Vue powered by Idrica platform, adding predictive leak-detection modules optimized for small distribution networks.

Global Water and Wastewater Sensors Market Report Scope

The Water and Wastewater Sensors Market Report is Segmented by Sensor Type (Electrochemical Sensors, Optical Sensors, Ultrasonic Sensors, Capacitive Sensors, Other Sensor Type), Parameter Monitored (pH, Dissolved Oxygen, Turbidity, Conductivity, Oxidation-Reduction Potential (ORP), Temperature, Other Parameter Monitored), End-Use Industry (Municipal Water and Wastewater Treatment, Industrial Water and Wastewater Treatment, Environmental Monitoring Agencies, Aquaculture, Other End-Use Industry), Installation Point (In-Line, Submersible, Handheld or Portable, Remote or IoT-Enabled Units), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). Market Forecasts are Provided in Terms of Value (USD).

| Electrochemical Sensors |

| Optical Sensors |

| Ultrasonic Sensors |

| Capacitive Sensors |

| Other Sensor Type |

| pH |

| Dissolved Oxygen |

| Turbidity |

| Conductivity |

| Oxidation-Reduction Potential (ORP) |

| Temperature |

| Other Parameter Monitored |

| Municipal Water and Wastewater Treatment |

| Industrial Water and Wastewater Treatment |

| Environmental Monitoring Agencies |

| Aquaculture |

| Other End-Use Industry |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Sensor Type | Electrochemical Sensors | ||

| Optical Sensors | |||

| Ultrasonic Sensors | |||

| Capacitive Sensors | |||

| Other Sensor Type | |||

| By Parameter Monitored | pH | ||

| Dissolved Oxygen | |||

| Turbidity | |||

| Conductivity | |||

| Oxidation-Reduction Potential (ORP) | |||

| Temperature | |||

| Other Parameter Monitored | |||

| By End-Use Industry | Municipal Water and Wastewater Treatment | ||

| Industrial Water and Wastewater Treatment | |||

| Environmental Monitoring Agencies | |||

| Aquaculture | |||

| Other End-Use Industry | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large is the global water and wastewater sensors market in 2026?

The water and wastewater sensors market size stands at USD 6.76 billion in 2026 with a forecast value of USD 8.88 billion by 2031.

Which sensor technology is growing fastest in the sector?

Optical dissolved-oxygen probes are expanding at an 8.31% CAGR through 2031 as luminescent designs displace membrane-based electrodes.

Why are utilities investing in IoT-enabled water sensors?

Remote probes reduce field visits, push anomaly detection to the edge, and support distributed assets such as rural wells and elevated tanks.

What segment leads end-use demand today?

Municipal water and wastewater utilities hold 47.01% of revenue given mandatory continuous monitoring at multiple treatment stages.

What is the main hurdle to wider sensor deployment?

Retrofitting legacy plants remains capital-intensive, with upgrade packages often exceeding USD 500 000 for mid-sized facilities.

Page last updated on: