Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

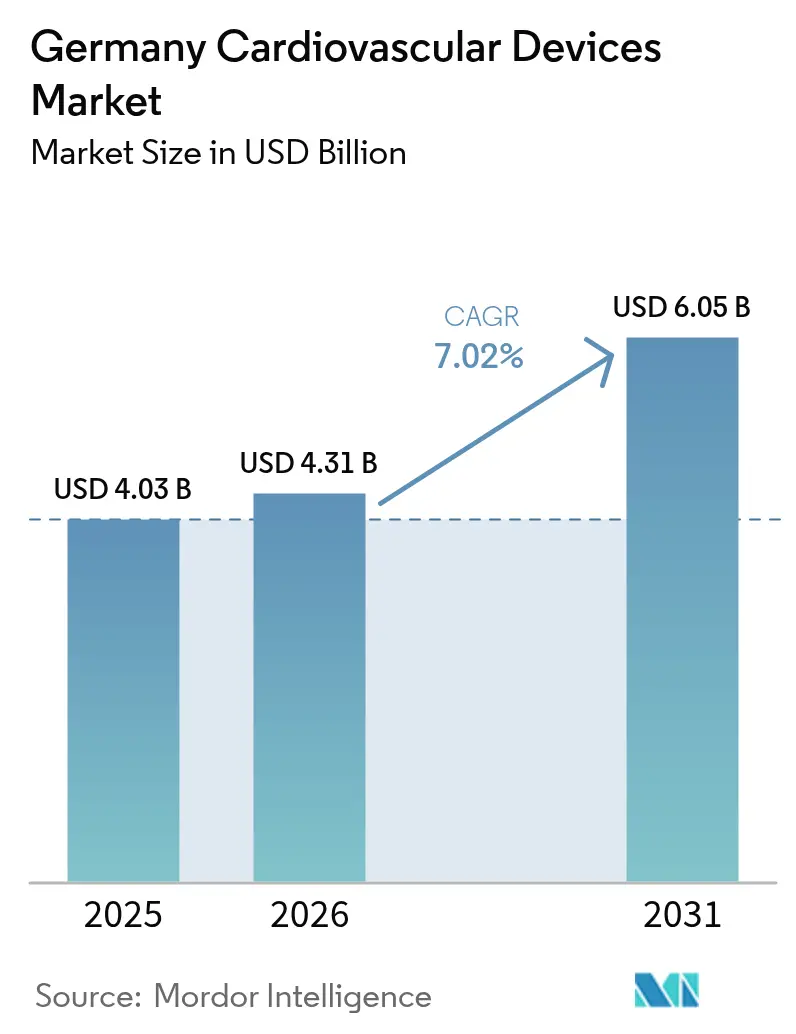

| Base Year Market Size (2025) | USD 4.03 Billion |

| Market Size (2026) | USD 4.31 Billion |

| Market Size (2031) | USD 6.05 Billion |

| Growth Rate (2026 - 2031) | 7.02% CAGR |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Cardiovascular Devices Market Analysis by Mordor Intelligence

The Germany cardiovascular devices market size is expected to grow from USD 4.03 billion in 2025 to USD 4.31 billion in 2026 and is forecast to reach USD 6.05 billion by 2031 at 7.02% CAGR over 2026-2031. Higher procedure volumes, an aging population, and expanding remote-monitoring mandates anchor long-term demand. Hospitals continue to invest in structural-heart and rhythm-management systems as DRG payments favor catheter-based interventions over conservative therapy. At the same time, mandatory telemonitoring of chronic heart-failure patients generates recurring revenue for implantable loop recorders and cloud analytics, turning the Germany cardiovascular devices market into a data-driven services arena. EU-MDR compliance costs eliminate many low-margin SKUs, shifting innovation toward AI-enabled diagnostics, minimally invasive systems, and fully implantable pumps that shorten inpatient stays. Although pharmacological advances temper device uptake in early-stage disease, Germany’s super-aged demographic keeps replacement and upgrade cycles brisk, sustaining a predictable mid-single-digit revenue trajectory through 2030.

Key Report Takeaways

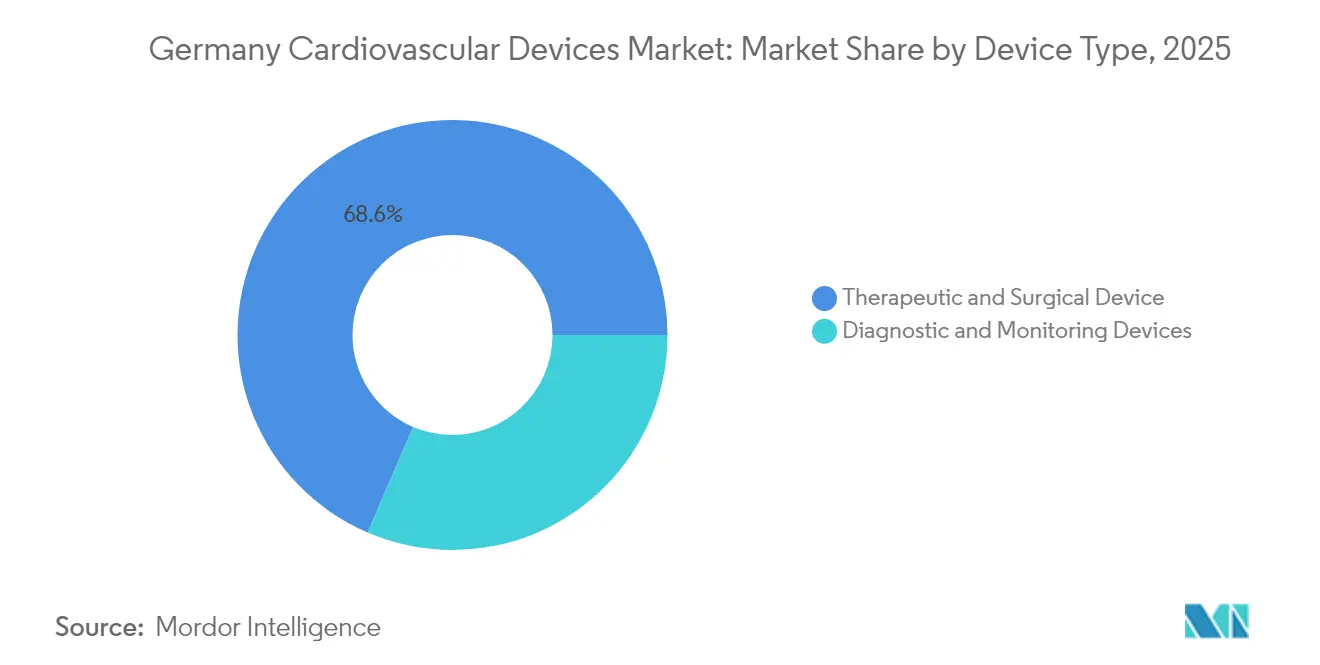

- By device type, Therapeutic and Surgical Devices held 68.55% of the Germany cardiovascular devices market share in 2025; Diagnostic and Monitoring Devices are set to post the highest 6.12% CAGR through 2031.

- By application, Coronary Artery Disease represented 42.70% of revenue in 2025, while Heart Failure is projected to advance at 6.63% CAGR between 2026-2031.

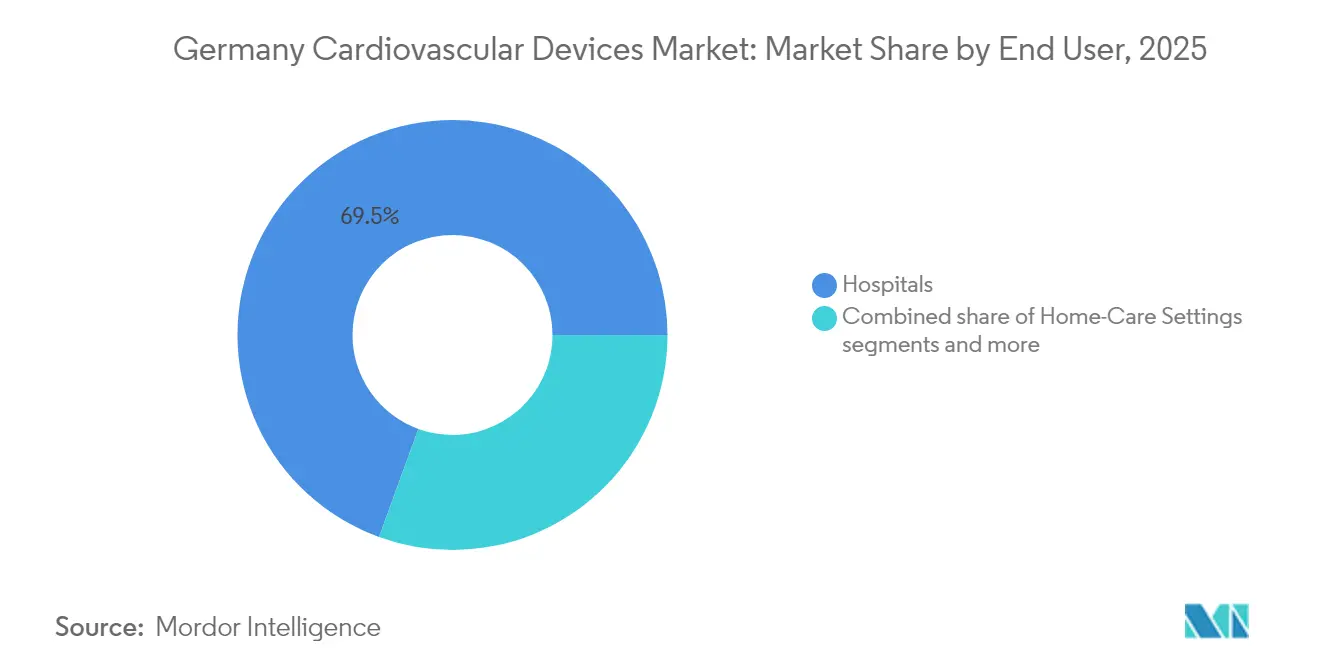

- By end-user, hospitals accounted for 69.45% of spending in 2025; the “Other” segment (ambulatory centers, cardiac clinics, home care) is poised for a 6.85% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Cardiovascular Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Expansion of Reimbursed TAVI & TMVR Procedures Boosting Transcatheter Heart Valve Demand | 2.30% | National, with concentration in university hospitals and specialized cardiac centers | Short term (≤2 yrs) |

| Mandatory Remote Heart-Failure Telemonitoring (G-BA 2022) Accelerating Implantable Loop Recorder Uptake | 1.90% | National, with early adoption in university hospitals and cardiac rehabilitation centers | Medium term (3-4 yrs) |

| Germany's Highest PCI per-Capita in EU Sustaining DES & Guidewire Replacement Cycles | 1.60% | National, with higher impact in regions with dense catheterization laboratory networks | Short term (≤2 yrs) |

| Super-Aged Demographics in Southern & Eastern States Driving Pacemaker & VAD Implant Volumes | 1.40% | Regional, concentrated in Bavaria, Baden-Württemberg, Saxony, and Thuringia | Long term (≥5 yrs) |

| R&D Tax Incentives & MDR Transition Supporting Domestic Innovators (e.g., BIOTRONIK) | 1.10% | National, with concentration in innovation hubs (Berlin, Munich, Hamburg) | Medium term (3-4 yrs) |

| Krankenhaus-Zukunft Act Funding Digital ICU / OR Hemodynamic Monitoring Systems | 2.00% | National, with priority for digitalization in public hospitals | |

| Source: Mordor Intelligence | |||

Rapid Expansion of Reimbursed Cardiovascular Procedures

Germany’s DRG system rewards hospitals for interventional care, lifting procedure counts for transcatheter aortic valve implantation beyond 100,000 cumulative cases. Catheter laboratories continue to replace surgical suites, and reimbursement parity between valve surgery and TAVI compresses payback periods for capital equipment. As 95% of octogenarian patients now receive TAVI, device makers bundle valves with embolic-protection filters to enlarge average selling prices while helping hospitals meet stroke-reduction quality metrics

Mandatory Remote Heart-Failure Telemonitoring

Since 2023, statutory insurers must cover remote telemetry for chronic heart-failure patients, motivating adoption of implantable loop recorders and non-invasive hemodynamic sensors. University centers have established command hubs that analyze continuous data feeds and trigger early outpatient interventions, cutting readmissions and freeing inpatient beds. Vendors offer subscription packages that integrate hardware, analytics dashboards, and reimbursement coding support, encouraging hospitals to migrate from episodic follow-up to always-on monitoring workflows.

Germany’s Highest PCI per-Capita Rate Sustains Drug-Eluting-Stent & Guidewire Replacement Cycles

German cardiologists perform more percutaneous coronary interventions per resident than any other EU nation, a metric tied directly to the country’s dense network of 960+ cath labs and procedure-friendly reimbursement. High procedure throughput leads to rapid inventory turnover for drug-eluting stents (DES) and complex-lesion guidewires, underpinning predictable reorder profiles for suppliers. Domestic firms such as Andramed and Bentley InnoMed win share with balloon-expandable platforms tuned for tortuous anatomies, supporting premium pricing on niche SKUs. Continuous innovation in hydrophilic-coated wires and micro-catheters keeps procedural success rates high, reinforcing physician loyalty to interventional pathways. As cath-lab operators pursue same-day discharge to unlock DRG headroom, demand for fast-healing DES coatings is set to strengthen further.

Krankenhaus-Zukunft Act Spurs Digital ICU/OR Hemodynamic-Monitoring Upgrades

Germany’s federal stimulus allocates EUR 4.3 billion to hospital digitalization, with priority spend on ICU and operating-room connectivity that directly benefits cardiovascular monitoring platforms. Capital grants subsidize AI-enabled hemodynamic monitors, multi-parameter recorders, and interoperable middleware that feed data into electronic health records in real time. Early tenders favour vendors offering cybersecurity certification and MDR-compliant software updates, raising the adoption bar for low-cost imports. Clinical teams report that integrated dashboards shorten response times during high-risk cardiovascular surgeries, improving outcome benchmarks that influence DRG bonuses. Funding is front-loaded through 2026, creating a near-term sales surge and a long-tail maintenance market for analytics subscriptions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

| EU-MDR Post-Market Costs Forcing SMEs to Withdraw Legacy Cardiovascular SKUs | -1.80% | National, with greater impact on SME-concentrated regions (Baden-Württemberg, Bavaria) | Short term (≤2 yrs) |

| DRG Budget Caps Curbing Ventricular Assist Device Implant Adoption Beyond University Centers | -1.20% | National, with higher impact in non-university hospitals and smaller cardiac centers | Medium term (3-4 yrs) |

| Value-Based Procurement Driving Price Erosion in Stents & Balloons | -1.00% | National, with higher impact in regions with centralized procurement systems | Short term (≤2 yrs) |

| Pharmacotherapy Advances (e.g., SGLT2i) Moderating Device Therapy Volumes | -1.30% | National, with higher impact in regions with advanced healthcare systems and research centers | Medium term (3-4 yrs) |

| Source: Mordor Intelligence | |||

EU-MDR Post-Market Costs

The 2021 MDR raised evidence thresholds and introduced intensive post-market surveillance, raising recertification costs by up to 300% for some small firms. With only 43 notified bodies to assess 500,000 devices EU-wide, certification queues stretch into 2026. Many German SMEs drop low-volume catheters rather than fund new trials, consolidating purchasing toward large multinationals and reducing product variety for niche applications.

Pharmacotherapy Advances Moderating Device Demand

European Society of Cardiology guidelines now recommend SGLT2 inhibitors as first-line therapy in heart-failure, deferring some device interventions. Early pharmacologic success curbs immediate demand for pacing or defibrillation, but remote telemetry reveals decompensation earlier, eventually feeding volumes back into device pipelines at later disease stages.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Therapeutic and Surgical Devices Lead by Device Type

Therapeutic and Surgical Devices captured 68.55% Germany cardiovascular devices market share in 2025, boosted by 164 TAVI cases per million residents. Growing reliance on drug-eluting stents, left-atrial appendage occluders, and VADs underscores hospitals’ preference for minimally invasive solutions that shorten intensive-care occupancy. Despite the maturity of percutaneous coronary intervention, high-risk subsets such as calcified lesions sustain demand for lithotripsy catheters reimbursed under new OPS codes.

Diagnostic and Monitoring Devices, although smaller, will expand at 6.12% CAGR to 2031, buoyed by AI-driven ECG analytics and mandatory heart-failure telemonitoring.

By Application: Coronary Stability, Heart-Failure Upsurge

Coronary Artery Disease maintains the largest revenue pool at 42.70% in 2025, sustained by high prevalence among workers retiring after 2025. Hospitals increasingly pair fractional flow reserve wires with balloon-expandable stents from Andramed or Bentley InnoMed to optimize lesion management.

By End-User: Hospital Core, Outpatient Surge

Hospitals delivered 69.45% of 2025 sales, led by university centers that act as reference sites for first-in-human trials. Hybrid-DRG flat fees enacted in 2024 stabilize revenue forecasts, encouraging capital budgeting for integrated cath-lab-operating-room hybrids .

The “Other” segment grows fastest at 6.85% CAGR, as ambulatory surgical centers adopt same-day PCI and home-care services deploy wearable ECG patches. Statutory reimbursement for DiGA apps widens access to mobile arrhythmia detection, embedding the Germany cardiovascular devices market into everyday life.

Geography Analysis

Southern states such as Bavaria and Baden-Württemberg host dense medical-technology clusters around Munich and Stuttgart. Proximity to Fraunhofer institutes and Technical University campuses accelerates prototype iteration, helping regional firms file MDR submissions sooner. These states also generate 34% of national cath-lab procedures, partly because affluent populations seek early elective interventions.

North-Rhine-Westphalia concentrates the highest structural-heart case volume—Cologne, Düsseldorf, and Essen collectively performed over 12,000 TAVI procedures in 2024. Large tertiary hospitals leverage diversified funding streams that combine DRG, teaching grants, and EU research budgets to outfit hybrid theaters. Device vendors treat these centers as launchpads, because published real-world evidence from Rhine-Ruhr regions influences guideline committees.

Eastern regions such as Saxony rely on telecardiology to offset longer travel times to university hospitals. Broadband penetration exceeding 95% enables continuous data uploads from rural heart-failure patients, supporting service contracts between device manufacturers and regional telehealth call centers. Funding from the European Regional Development Fund further subsidizes server infrastructure, positioning the East as a service hub that exports telemetry analytics nationwide.

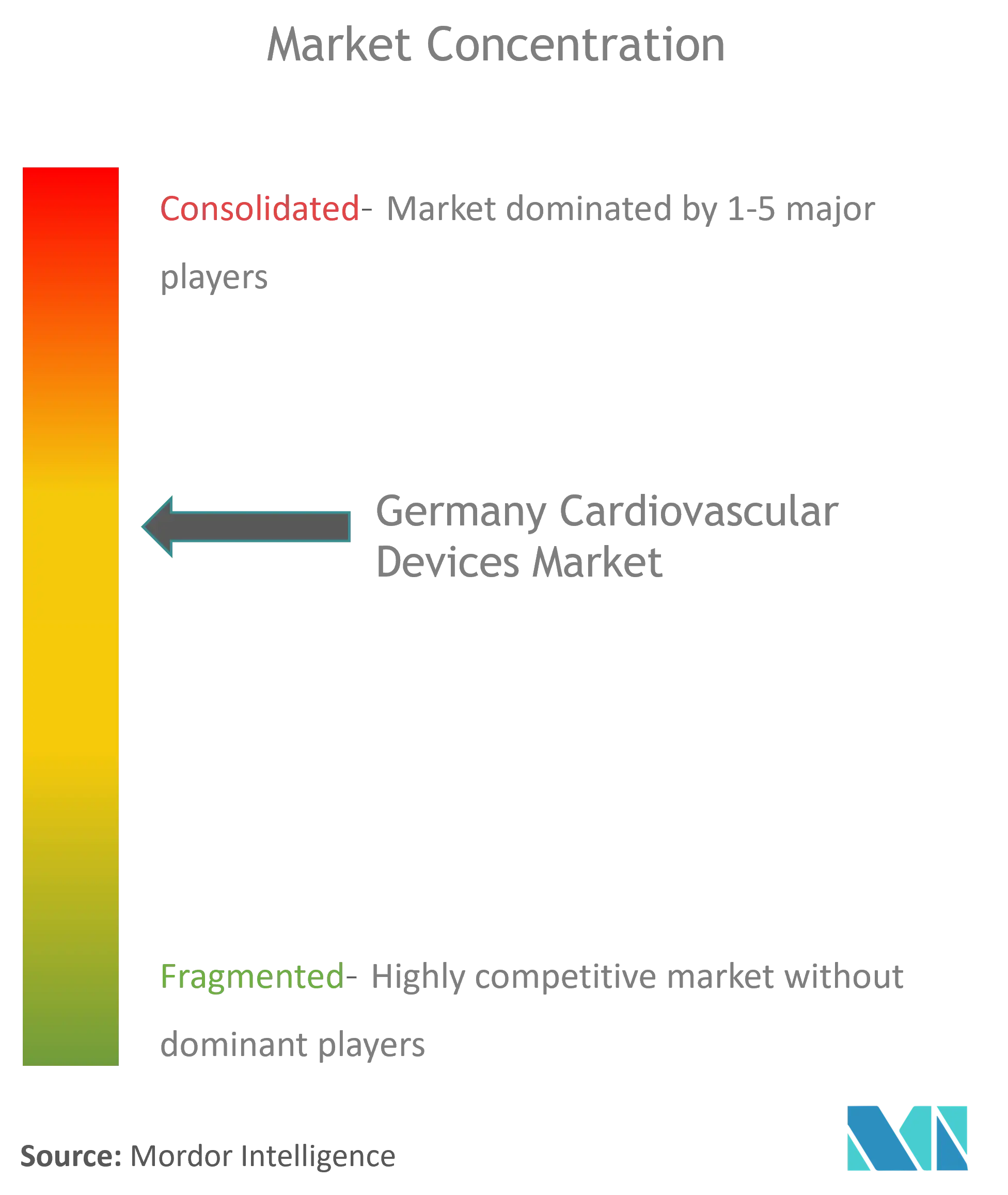

Competitive Landscape

Germany cardiovascular devices industry competition is moderate, with domestic innovators coexisting alongside global majors. BIOTRONIK’s DX platform integrates atrial sensing into single-chamber ICDs, reducing lead count and complication risk. The firm’s Berlin headquarters houses vertical production lines, ensuring supply resilience during MDR-related shortages.

Berlin Heals and Protembis exemplify venture-backed niche specialists. Berlin Heals’ C-MIC device applies bioelectric stimulation to heart-failure ventricles, aiming to avoid life-long pharmacotherapy. Protembis’ ProtEmbo filter addresses cerebral embolic risk during TAVI, aligning with hospitals’ shift toward patient-safety metrics. Both companies leverage German Angel Investors’ tax credits and Fraunhofer project grants to co-fund pivotal trials.

AI-centric disruptors such as LARALAB partner with imaging vendors to embed eligibility algorithms directly into hospital PACS, compressing CT-review time from hours to minutes[2]Source: Edward Plugge, “LARALAB launches REC,” einpresswire.com . Large multinationals increasingly license these algorithms rather than build in-house, intensifying M&A as buyers chase software intellectual property that fortifies their hardware install base.

Germany Cardiovascular Devices Industry Leaders

Abbott Laboratories

Boston Scientific Corporation

Medtronic PLC

Edwards Lifesciences

Cardinal Health Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: In a groundbreaking pilot project, the Ströer media company, along with Hamburg's Herzstädter and Medical Industrie, has installed a defibrillator in a digital media column. This first-of-its-kind initiative in a public space underscores the project's commitment to enhancing emergency response capabilities and supporting HerzretterStadt Hamburg in its life-saving mission.

- August 2024: Heidelberg University Hospital implanted two Carmat Aeson total artificial hearts, extending support for transplant-eligible patients

- May 2024: LARALAB launched ‘REC—Rapid Eligibility Check,’ enabling AI-based screening for mitral and tricuspid interventions

Germany Cardiovascular Devices Market Report Scope

As per the scope of the report, cardiovascular devices are used to diagnose and treat heart disease and related cardiovascular problems. Cardiac Devices offers monitoring services to hospitals and physicians to take care of the patients with the help of the data collected by cardiac monitors. The German Cardiovascular Devices Market is segmented by Device type, Diagnostic and Monitoring Devices (Electrocardiogram, Remote Cardiac Monitoring, and Other Diagnostic and Monitoring Devices), and Therapeutic and Surgical Devices (Cardiac Assist Devices, Cardiac Rhythm Management Device, Catheter, Grafts, Heart Valves, Stents, and Other Therapeutic and Surgical Devices). The report offers the value (in USD million) for the above segments.

By Device Type

| Diagnostic & Monitoring Devices | ECG Systems | |

| Remote Cardiac Monitor | ||

| Cardiac MRI | ||

| Cardiac CT | ||

| Echocardiography / Ultrasound | ||

| Fractional Flow Reserve (FFR) Systems | ||

| Therapeutic & Surgical Devices | Coronary Stents | Drug-Eluting Stents |

| Bare-Metal Stents | ||

| Bioresorbable Stents | ||

| Catheters | PTCA Balloon Catheters | |

| IVUS/OCT Catheters | ||

| Cardiac Rhythm Management | Pacemakers | |

| Implantable Cardioverter Defibrillators | ||

| Cardiac Resynchronization Therapy Devices | ||

| Heart Valves | TAVR/TAVI | |

| Mechanical Valves | ||

| Tissue/Bioprosthetic Valves | ||

| Ventricular Assist Devices | ||

| Artificial Hearts | ||

| Grafts & Patches | ||

| Other Cardiovascular Surgical Devices | ||

By Application

| Coronary Artery Disease |

| Arrhythmia |

| Heart Failure |

| Structural Heart Disease |

| Hypertension |

| Others |

By End User

| Hospitals |

| Home-Care Settings |

| Others |

| By Device Type | Diagnostic & Monitoring Devices | ECG Systems | |

| Remote Cardiac Monitor | |||

| Cardiac MRI | |||

| Cardiac CT | |||

| Echocardiography / Ultrasound | |||

| Fractional Flow Reserve (FFR) Systems | |||

| Therapeutic & Surgical Devices | Coronary Stents | Drug-Eluting Stents | |

| Bare-Metal Stents | |||

| Bioresorbable Stents | |||

| Catheters | PTCA Balloon Catheters | ||

| IVUS/OCT Catheters | |||

| Cardiac Rhythm Management | Pacemakers | ||

| Implantable Cardioverter Defibrillators | |||

| Cardiac Resynchronization Therapy Devices | |||

| Heart Valves | TAVR/TAVI | ||

| Mechanical Valves | |||

| Tissue/Bioprosthetic Valves | |||

| Ventricular Assist Devices | |||

| Artificial Hearts | |||

| Grafts & Patches | |||

| Other Cardiovascular Surgical Devices | |||

| By Application | Coronary Artery Disease | ||

| Arrhythmia | |||

| Heart Failure | |||

| Structural Heart Disease | |||

| Hypertension | |||

| Others | |||

| By End User | Hospitals | ||

| Home-Care Settings | |||

| Others | |||

Key Questions Answered in the Report

How big is the Germany cardiovascular devices market in 2026?

The market stands at USD 4.31 billion.

What growth rate is projected for the Germany cardiovascular devices market through 2031?

A 7.02% CAGR is forecast from 2026-2031.

Which segment grows fastest within the Germany cardiovascular devices market?

Diagnostic and Monitoring Devices will rise at 6.12% CAGR during the forecast period.

Why is mandatory telemonitoring significant for German heart-failure care?

Statutory reimbursement requires remote monitoring for over 3 million patients, driving higher implantable recorder adoption and reducing readmissions.

Page last updated on: