Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

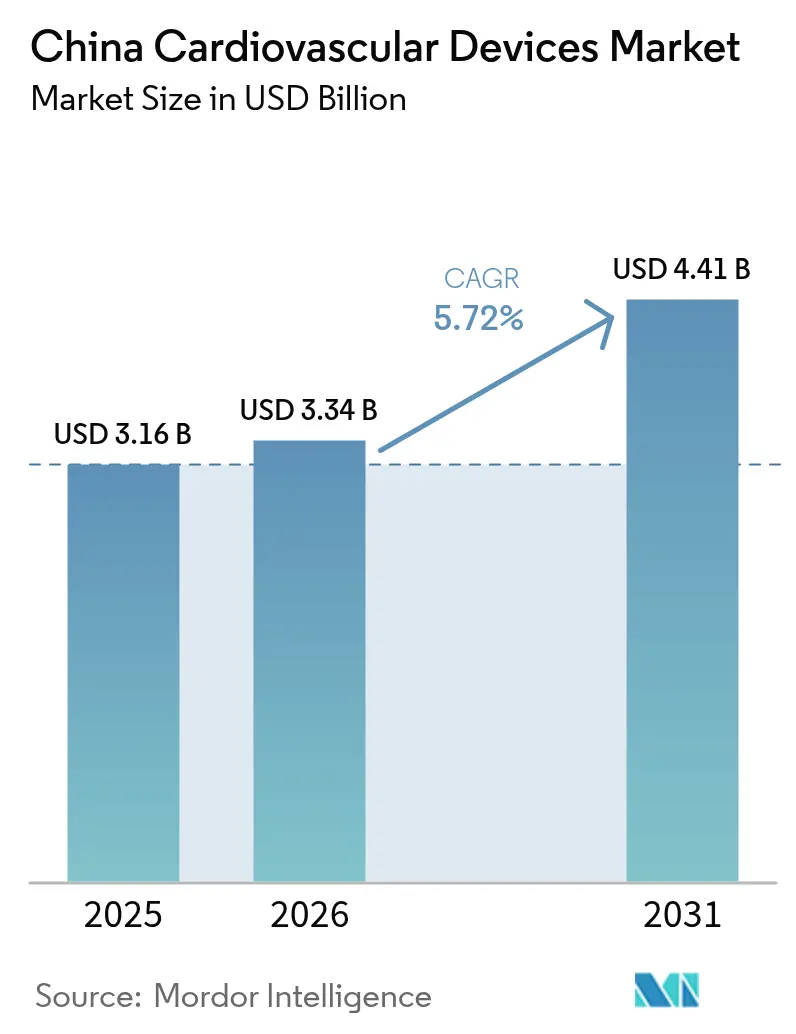

| Base Year Market Size (2025) | USD 3.16 Billion |

| Market Size (2026) | USD 3.34 Billion |

| Market Size (2031) | USD 4.41 Billion |

| Growth Rate (2026 - 2031) | 5.72% CAGR |

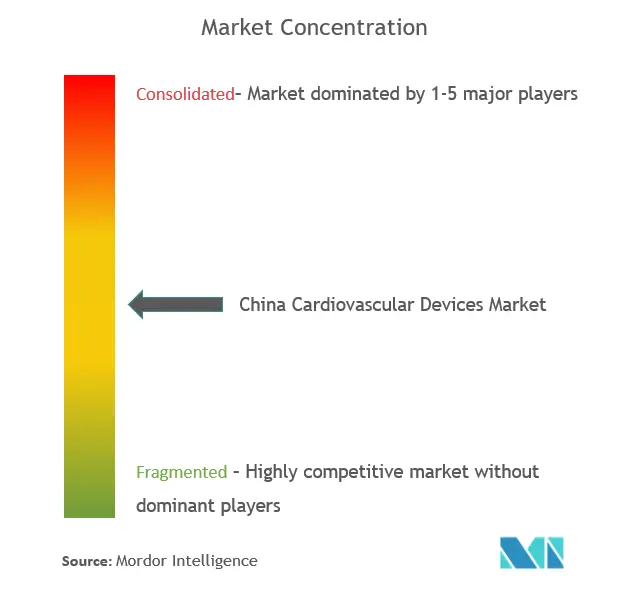

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Cardiovascular Devices Market Analysis by Mordor Intelligence

The China cardiovascular devices market size is expected to grow from USD 3.16 billion in 2025 to USD 3.34 billion in 2026 and is forecast to reach USD 4.41 billion by 2031 at 5.72% CAGR over 2026-2031. Rising life expectancy, an estimated 330 million cardiovascular patients, and the policy tilt of “Healthy China 2030” continue to lift procedure volumes and the uptake of both interventional and monitoring technologies . Price compression sparked by volume-based procurement (VBP) on coronary stents triggered a 95% price fall yet lifted overall stent usage by nearly 10%, illustrating how cost reform can amplify device penetration. Domestic producers are capitalising on these reforms, aided by “Made in China 2025,” which targets 70% local production of mid- to high-end cardiovascular equipment by 2025 . Simultaneously, China’s expanding chest-pain-center network has cut median door-to-balloon times from 117.7 minutes to 46.9 minutes, adding momentum to advanced imaging, guidewire, and emergency monitoring demand.

Key Report Takeaways

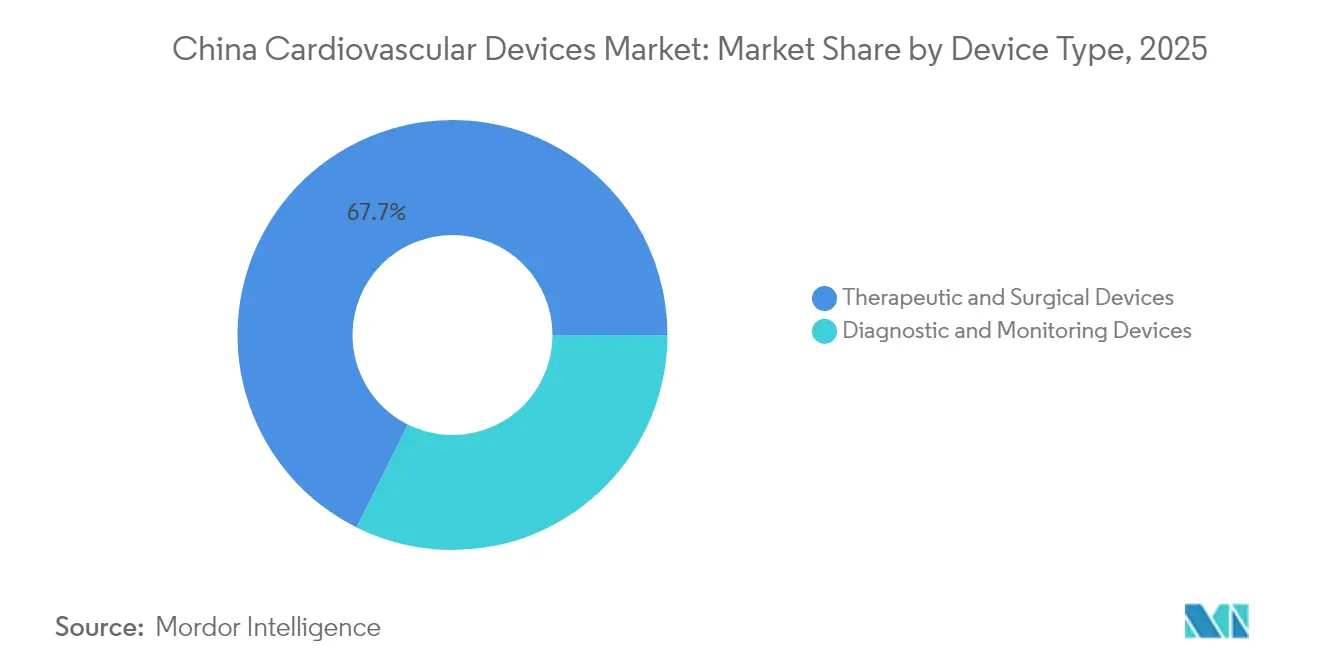

- By device type, Therapeutic and Surgical Devices led with 67.65% of the China cardiovascular devices market share in 2025, while Diagnostic and Monitoring Devices are projected to log the fastest 6.87% CAGR through 2031.

- By application, Coronary Artery Disease commanded 46.05% of the China cardiovascular devices market size in 2025, whereas Structural and Congenital Heart Defects are set to expand at a 7.02% CAGR to 2031.

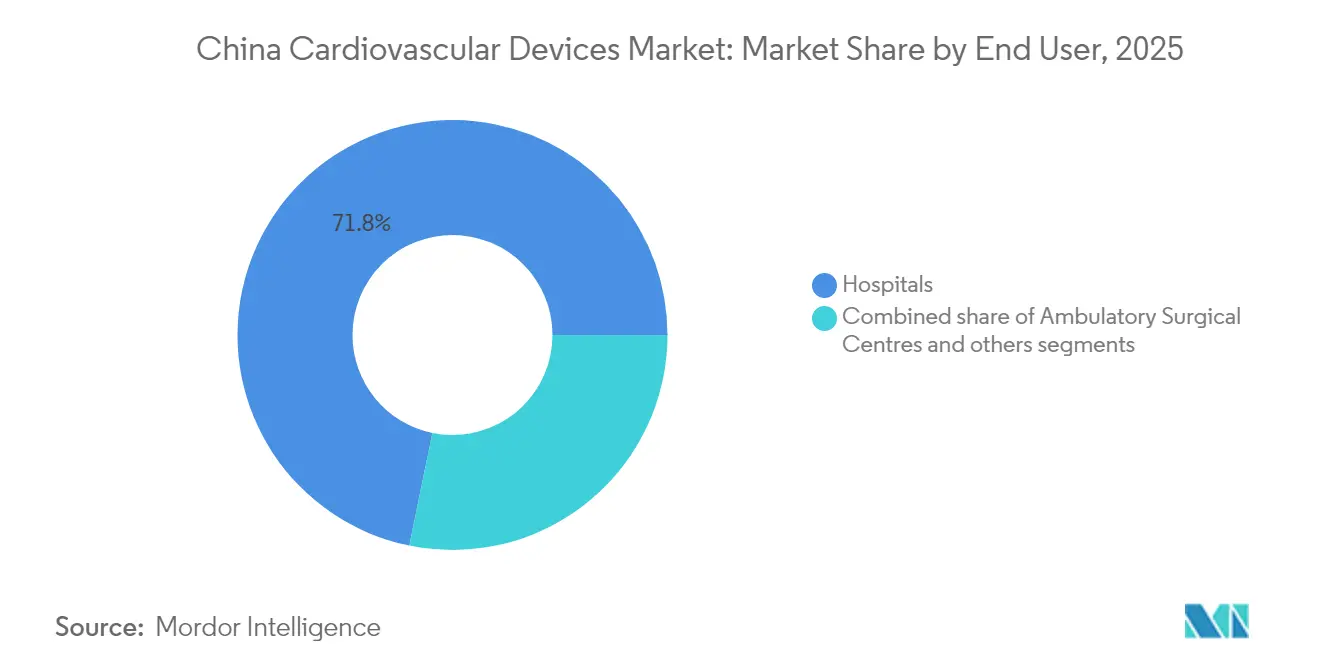

- By end-user, hospitals and cardiac centers retained 71.78% share of the China cardiovascular devices market in 2025, but home-care settings are forecast to grow at a 6.67% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Cardiovascular Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Expansion of China's Chest-Pain Centers Accrediting Advanced Interventional Device Adoption | +1.2% | National, with concentration in urban centers | Medium term (2-4 years) |

| Government "Made in China 2025" Initiatives Boosting Domestic Cardiovascular Device Innovation | +1.8% | National | Long term (≥ 4 years) |

| Rising Prevalence of Atrial Fibrillation in Aging Chinese Population Elevating Demand for CRM Devices | +1.4% | National, with higher impact in Eastern provinces | Long term (≥ 4 years) |

| National Volume-Based Procurement (VBP) for Drug-Eluting Stents Triggering High-Volume Domestic Production | +0.9% | National | Short term (≤ 2 years) |

| Accelerated Conditional Approval Pathway for Breakthrough Cardiovascular Implants by NMPA | +0.7% | National | Medium term (2-4 years |

| Source: Mordor Intelligence | |||

Rapid expansion of China’s chest-pain centers accrediting advanced interventional device adoption

The national roll-out of chest-pain centers has shortened door-to-balloon intervals to as low as 46.9 minutes, driving stronger uptake of high-performance guidewires, drug-eluting stents, and intravascular imaging systems . Integration of artificial-intelligence triage further lifted primary PCI rates within 90 minutes from 24.47% to 60.41% and pushed connected ECG platforms that cut 30-day mortality from 4.14% to 2.73% . National standards maintained by the Chinese Cardiovascular Association make performance metrics public, prompting county-level hospitals to standardise product choices toward devices demonstrating clinical efficiency. This standardisation increases procurement predictability and compresses time-to-tender for domestic innovators aligned with evidence-based protocols. As the program expands into central and western provinces, device makers that couple competitive pricing with proven clinical outcomes are positioned to capture incremental volumes within the China cardiovascular devices market.

Government “Made in China 2025” initiatives boosting domestic cardiovascular device innovation

The industrial policy goal of 70% domestic supply for mid- to high-end cardiovascular equipment has redirected capital into research pipelines, with leading local firms dedicating 11-14% of sales to R&D, well above the global med-tech average. Resulting product launches span coronary bifurcation stents, pulsed-field ablation systems, and magnetic levitation pumps, all cleared through the National Medical Products Administration’s (NMPA) innovation channel. While foreign brands still dominate complex heart-valve segments, Chinese entrants now match global peers in many delivery-system and polymer-coating technologies, shifting procurement in provincial tenders toward locally registered SKUs. Industry stakeholders expect the localisation push to permeate peripheral vascular and electrophysiology niches by 2027, reinforcing the structural tilt of the China cardiovascular devices market toward home-grown solutions.

Rising prevalence of atrial fibrillation in an aging population elevating demand for cardiac rhythm management devices

China houses an estimated 330 million cardiovascular patients, and atrial fibrillation prevalence continues climbing alongside median age. Regulatory clearance of the country’s first pulsed-field ablation (PFA) platform in 2024 offers an alternative to thermal ablation, aided by MANIFEST-17K data showing only 0.98% major complications . Remote rhythm-monitoring wearables captured abnormal beats in 95.9% of obstructive-sleep-apnea cases, highlighting mobile-health’s synergy with clinic-based CRM devices . Multidisciplinary AF clinics benefit from AI-enhanced diagnostics that stratify stroke risk and optimise anticoagulation, broadening device intervention points. Collectively, these developments underpin sustained CRM segment expansion within the China cardiovascular devices market.

Accelerated conditional approval pathway for breakthrough cardiovascular implants by NMPA

In 2023 the NMPA accepted 13,260 medical-device applications and approved 12,213, up 25.4% year on year [1]Source: National Medical Products Administration, “Regulatory Information,” nmpa.gov.cn. Priority review shortened time-to-market for devices such as the mag-lev MoyoAssist ventricular-assist system and the Symplicity Spyral renal-denervation catheter. Domestic and foreign applicants alike leverage rolling submissions and real-world evidence pilots, though local manufacturing still confers procurement advantages. Faster clearance accelerates revenue capture and heightens innovation turnover across the China cardiovascular devices market

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price Erosion due to Ongoing VBP Rounds on High-Value Consumables | -0.6% | National | Short term (≤ 2 years) |

| Capacity Bottlenecks in Qualified Cath Labs Outside Top-Tier Cities | -0.5% | Central and Western regions | Medium term (2-4 years) |

| Clinical Talent Shortage for TAVR and Left Atrial Appendage Closure Procedures | -0.8% | National, with greater impact in lower-tier cities | Medium term (2-4 years) |

| Heightened Post-Market Surveillance Scrutiny on Imported Implantables | -0.4% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Price erosion due to ongoing VBP rounds on high-value consumables

Successive VBP extensions from stents to pacemakers, defibrillators, and valves have saved CNY 260 billion across three years but crimped average selling prices and gross profit margins for premium lines. Multinationals face tougher trade-offs between margin retention and share maintenance, while domestic firms rely on scale economics to protect bottom lines. Although higher volumes cushion revenue, the short-run impact is negative for top-line growth, moderating the overall China cardiovascular devices market CAGR.

Capacity bottlenecks in qualified cath labs outside top-tier cities

Only about 100 hospitals perform TAVR, mainly in coastal megacities, leaving populous inland provinces underserved. Hybrid OR build-outs need heavy capital and trained staff, delaying roll-out for complex structural procedures. Government grants under “Healthy China 2030” aim to bridge gaps, yet the medium-term pace of capacity expansion remains gradual, curbing market breadth in central and western clusters.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Domestic innovation disrupts traditional hierarchies

Therapeutic and Surgical Devices contributed 67.65% of the China cardiovascular devices market in 2025, buoyed by 2,200 annual coronary interventions at leading centers and VBP-induced volume surges. The cardiac-rhythm-management niche accelerated after NMPA cleared MicroPort Sorin’s new pacing lead in February 2025, underscoring local progress in hermetic sealing and lead-coil metallurgy. Intravascular lithotripsy, renal denervation, and next-gen drug-coated balloons form the emerging wave, with localisation tipping cost-of-goods lower than imports. Over the forecast period, domestic innovators are expected to keep displacing foreign incumbents across mid-complexity implants, reinforcing the primacy of this category within the China cardiovascular devices market.

Diagnostic and Monitoring Devices are projected to expand at a 6.87% CAGR through 2031. AI-enabled ECG analytics integrated into smart wearables bring early detection into homes, while hospital chest-pain networks still buy high-throughput CT and MRI scanners for triage optimisation. Cardiac-biomarker assays backed by local reagent makers support rapid rule-out protocols, serving the 330 million strong patient pool . Cloud-native data platforms align with the NMPA’s revised cybersecurity guidance, helping vendors secure faster approval for software-as-medical-device modules. Given rising chronic-disease management at home, connected diagnostics should keep edging wallet share away from purely interventional SKUs, adding depth to the China cardiovascular devices market size.

By Application: Structural heart defects emerge as growth frontier

Coronary Artery Disease remained the largest indication with 46.05% share in 2025, supported by better acute-coronary-syndrome pathways that lowered 30-day mortality to 4.53%. Dedicated bifurcation stents, imaging-guided PCI, and bioresorbable scaffolds are expanding quickly and enjoy rapid regulatory clearance, reflecting convergence between domestic quality systems and global best practice. As urbanisation and risk-factor prevalence persist, procedure counts should continue rising, anchoring the China cardiovascular devices market size for this application.

Structural and Congenital Heart Defects are forecast to post a 7.02% CAGR, the fastest among clinical segments. Transcatheter heart valves spearhead growth: Jenscare’s Ken-Valve and LuX-Valve Plus target tricuspid and aortic lesions, with design tweaks suited to Chinese anatomical profiles. Clinical-talent shortfalls keep procedure volumes below potential, yet training alliances and tele-proctoring are easing diffusion. As devices migrate from tertiary hubs to provincial centers, adoption velocity should accelerate, adding incremental weight to the China cardiovascular devices market share of structural indications.

By End-User: Home care settings disrupt hospital dominance

Hospitals and cardiac centers controlled 71.78% of the China cardiovascular devices market in 2025, largely due to DRG-linked reimbursement that bundles implants within inpatient episodes. Over 96 TAVR cases were handled at single top-tier sites last year, evidencing procedural concentration. Despite this grip, payment reforms and digital-health incentives are nudging providers toward ambulatory and post-discharge monitoring pathways, slightly diluting hospital hold going forward.

Home care and remote programs are slated for a 6.67% CAGR, driven by smartphone penetration and AI-supported triage that shortens clinic queues. Portable ECG patches, cloud-linked blood-pressure cuffs, and app-based medication reminders enable chronic-care decentralisation. Pilot data show virtual consultations reduce follow-up visits by 18% and maintain anticoagulation adherence above 85%, outlining clear efficiency gains for payers. These shifts support a steady rise in the China cardiovascular devices market contribution from consumer-oriented form factors.

Geography Analysis

Regional disparities define market opportunity contours. Eastern provinces cluster chest-pain centers that clock door-to-balloon times as low as 51 minutes, driving dense demand for PCI catheters and drug-eluting stents . Around 100 hospitals now offer TAVR, mainly along the coast, underpinning a geographically skewed China cardiovascular devices market share for structural products.

Central and western provinces display rising adoption curves as provincial health budgets fund cath-lab builds and tele-cardiology links. In Ningxia, chest-pain-center adoption cut 3-year mortality from 11.86% to 8.55%, shining light on latent device needs . Tele-ECG and remote diagnosis shrink onset-to-wire intervals, providing footholds for cost-efficient monitoring and imaging solutions. Government equalisation grants are earmarked for 200 additional cath-lab certifications by 2027, which will broaden the China cardiovascular devices market base beyond first-tier cities.

Manufacturing footprints follow similar geography. Shanghai positions itself as a medical-AI capital by 2027, hosting several cardiovascular-robotics pilots. Procurement rules that restrict imports in public tenders drive both multinationals and local start-ups to set up plants in Jiangsu and Guangdong, accelerating supply-chain localisation. As domestic assembly scales, lead times fall and after-sales networks tighten, reinforcing regional loyalty and enlarging the total China cardiovascular devices market.

Regulatory Landscape

China cardiovascular device regulation is overseen by the National Medical Products Administration (NMPA), with technical review led by the Center for Medical Device Evaluation (CMDE), and the strictest controls apply to Class III implantables used in interventional cardiology. For drug-device combination products, the NMPA uses a primary mode of action approach to decide whether the product follows a medical-device or drug registration pathway, and filing requires early attribute definition.

Oversight has been tightening across the product life cycle through targeted supervision and clearer review expectations for higher-risk categories. In April 2026, the NMPA published its 2026 National Inspection Plan for Medical Devices, which included coronary vascular stents, peripheral vascular stents, and drug-coated balloon dilatation catheters, reinforcing quality-compliance readiness for manufacturers supplying volume-driven procurement channels. In parallel, CMDE Announcement No. 14 of 2026 laid out the 2026-2027 guideline development plan, pointing to more product-specific registration guidance for cardiovascular interventional technologies and a higher bar for evidence packages, consistency in type testing, and post-market controls.

Competitive Landscape

Competition intensifies as domestic R&D spend rises. MicroPort, Lepu Medical, and Venus Medtech funnel 11-14% of revenue into innovation, spawning home-grown iterations of drug-coated balloons and renal-denervation systems . Local players now meet or exceed global standards in coating durability, polymer science, and delivery-shaft flexibility, shrinking multinationals’ technology premium. Policies favouring local provenance further tip tenders in their favour.

Multinationals recalibrate. Medtronic localised production and secured renal-denervation approval in 2024, preserving relevance in hypertension therapy . Johnson & Johnson’s deal to buy Shockwave Medical broadens intravascular lithotripsy access for heavily calcified lesions, a growing need in Chinese patient profiles . Boston Scientific divested its vascular business to refocus on higher-margin rhythm management, signalling portfolio optimisation under pricing pressure.

Innovation keeps reshaping the chessboard. NMPA cleared the first domestic PFA catheter for atrial-fibrillation ablation in 2024, potentially leapfrogging thermal approaches on safety. Mag-lev pumps, bioresorbable scaffolds, and AI-driven decision-support suites are next-wave differentiators. Companies that blend local evidence with cost-efficient engineering stand best positioned to capture share in the evolving China cardiovascular devices market.

China Cardiovascular Devices Industry Leaders

Abbott Laboratories

Boston Scientific Corporation

Medtronic PLC

Lepu Medical Technology(Beijing)Co.,Ltd.

Terumo Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Tender reform and clinical-network buildout create whitespace in cost-efficient interventional portfolios and imaging-guided procedure workflows. The second round of volume-based procurement for coronary stents in May 2026 broadened the product mix by introducing drug-eluting stainless steel stents alongside drug-eluting alloy stents, and it set a procurement cycle through June 30, 2029. That longer cycle provides manufacturers a wider planning window for capacity, localization, and service coverage tied to predictable demand. It also favors players that can sustain stable supply, meet inspection-driven quality requirements, and tailor SKU strategies for differentiated materials and specifications within capped-price frameworks.

A second opportunity is in precision-guided cath lab workflows and hospital standardization programs, where procurement increasingly links to measurable clinical efficiency. As chest-pain-center performance systems expand and door-to-balloon times improve in the market context, demand concentrates around devices that shorten procedure time and support faster decision-making, including intravascular imaging catheters, advanced guidewires, and connected emergency monitoring. At the same time, NMPA and CMDE actions in 2026 around inspection priorities and guideline planning for cardiovascular interventional products increase the payoff for companies that invest early in compliant clinical evidence and manufacturing controls, especially domestic manufacturers building higher-end portfolios across stents, drug-coated balloons, electrophysiology, and imaging-adjacent categories.

Recent Industry Developments

- June 2026: Medtronic announced a strategic investment in CardioACC, a Shenzhen-based company with an NMPA-approved intracardiac echocardiography (ICE) system (approved in 2025), and outlined plans to integrate ICE into Medtronic’s Affera mapping and ablation workflow. The move strengthens procedure-imaging integration for electrophysiology in China and increases competitive intensity around platform-based ablation ecosystems.

- June 2025: Lepu Medical reported NMPA certification for its FireyZip radiofrequency ablation catheter. This expands Lepu’s therapeutic electrophysiology toolkit and supports broader domestic participation in arrhythmia interventions as hospitals seek price-performance alternatives under tightening procurement and budget discipline.

- May 2024: Medtronic secured NMPA clearance for the Symplicity Spyral renal-denervation platform for hypertension therapy in China. The approval broadened the addressable interventional landscape beyond coronary disease and created a regulatory and clinical reference point for catheter-based hypertension treatments.

Research Methodology Framework and Report Scope

Segmentation Overview

- By Device Type

- By Product Type

- Diagnostic & Monitoring Devices

- ECG Systems

- Remote Cardiac Monitor

- Cardiac MRI

- Cardiac CT

- Echocardiography / Ultrasound

- Fractional Flow Reserve (FFR) Systems

- Therapeutic & Surgical Devices

- Coronary Stents

- Drug-Eluting Stents

- Bare-Metal Stents

- Bioresorbable Stents

- Catheters

- PTCA Balloon Catheters

- IVUS/OCT Catheters

- Cardiac Rhythm Management

- Pacemakers

- Implantable Cardioverter Defibrillators

- Cardiac Resynchronization Therapy Devices

- Heart Valves

- TAVR/TAVI

- Mechanical Valves

- Tissue/Bioprosthetic Valves

- Ventricular Assist Devices

- Artificial Hearts

- Grafts & Patches

- Other Cardiovascular Surgical Devices

- Coronary Stents

- Diagnostic & Monitoring Devices

- By Application

- Coronary Artery Disease

- Arrhythmia & Conduction Disorders

- Heart Failure & Cardiomyopathy

- Structural & Congenital Heart Defects

- Peripheral Vascular Disease

- By End User

- Hospitals & Cardiac Centres

- Ambulatory Surgical Centres

- Cardiology/EP Clinics

- Home-care & Remote Monitoring Programs

- By Product Type

Key Questions Answered in the Report

What is the current value of the China cardiovascular devices market?

The market is valued at USD 3.34 billion in 2026 and is forecast to reach USD 4.41 billion by 2031.

Which device category leads market revenue?

Therapeutic and Surgical Devices make up 67.65% of total revenue as of 2025.

Which segment is growing fastest?

Diagnostic and Monitoring Devices are projected to advance at a 6.87% CAGR through 2031.

How is policy affecting pricing?

Volume-based procurement cut stent prices by 95% and is extending to pacemakers, valves, and defibrillators, reshaping pricing across categories.

Page last updated on: