Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

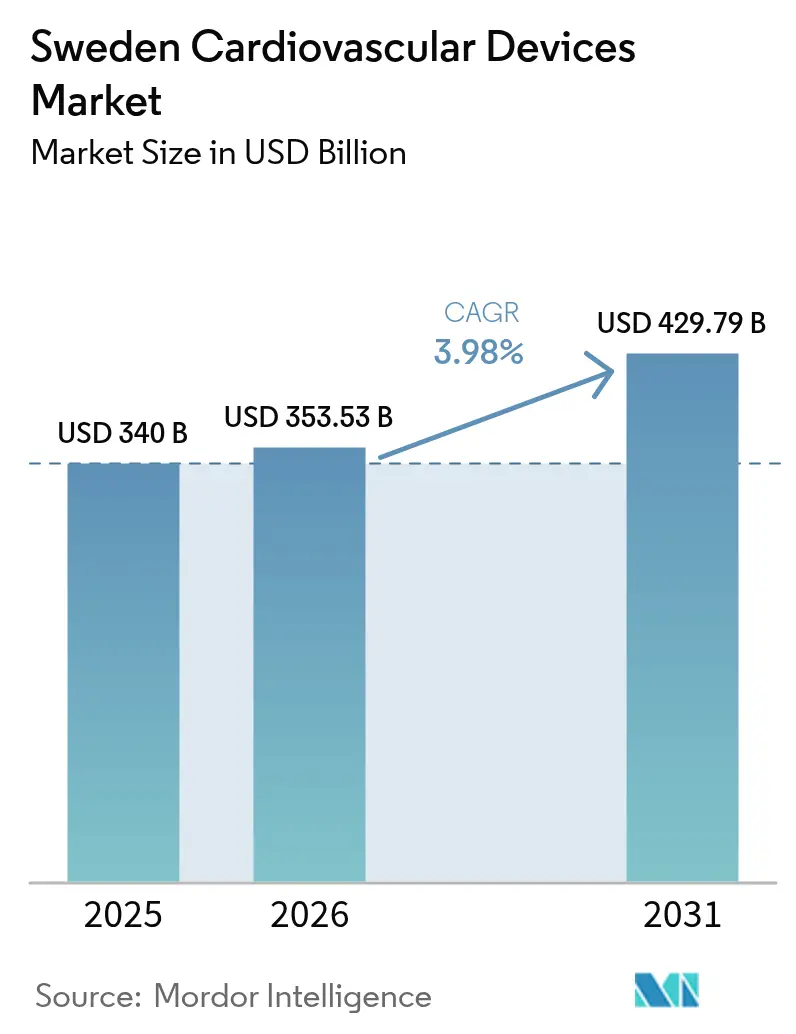

| Base Year Market Size (2025) | USD 340 Billion |

| Market Size (2026) | USD 353.53 Billion |

| Market Size (2031) | USD 429.79 Billion |

| Growth Rate (2026 - 2031) | 3.98% CAGR |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sweden Cardiovascular Devices Market Analysis by Mordor Intelligence

The Sweden cardiovascular devices market size is expected to grow from USD 340 million in 2025 to USD 353.53 million in 2026 and is forecast to reach USD 429.79 million by 2031 at 3.98% CAGR over 2026-2031. Robust digital health infrastructure, high life expectancy and rigorous value-based reimbursement continue to shape the cardiovascular devices market, steering manufacturers toward clinically proven, cost-effective solutions that align with Sweden’s evidence-based medicine objectives. Growth momentum is further sustained by the 20.5% share of citizens aged 65+and rising procedural volumes for minimally invasive therapies. Diagnostic and monitoring technologies, empowered by artificial intelligence and remote connectivity, are expanding faster than legacy interventional categories as Region Stockholm moves toward its goal of 50% digital healthcare delivery by2030. In parallel, Sweden’s early readiness for EU Medical Device Regulation (MDR) has limited supply disruption compared with peer markets while encouraging new-generation product introductions that meet elevated clinical evidence standards.

Key Report Takeaways

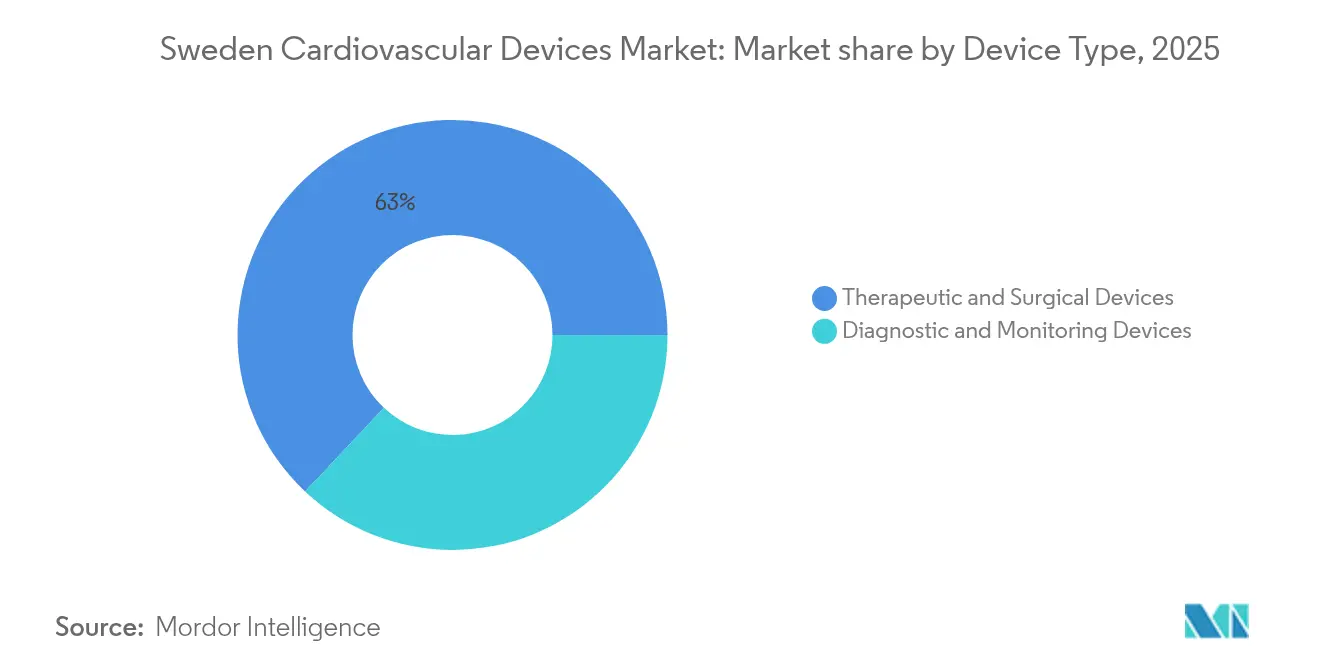

- By device type: Therapeutic and surgical systems commanded 62.98% of the cardiovascular devices market share in 2025, whereas diagnostic and monitoring platforms are advancing at a 5.55% CAGR through 2031.

- By application: Coronary artery disease retained 41.10% share of the cardiovascular devices market size in 2025, while structural heart disease posts the fastest 6.15% CAGR through 2031.

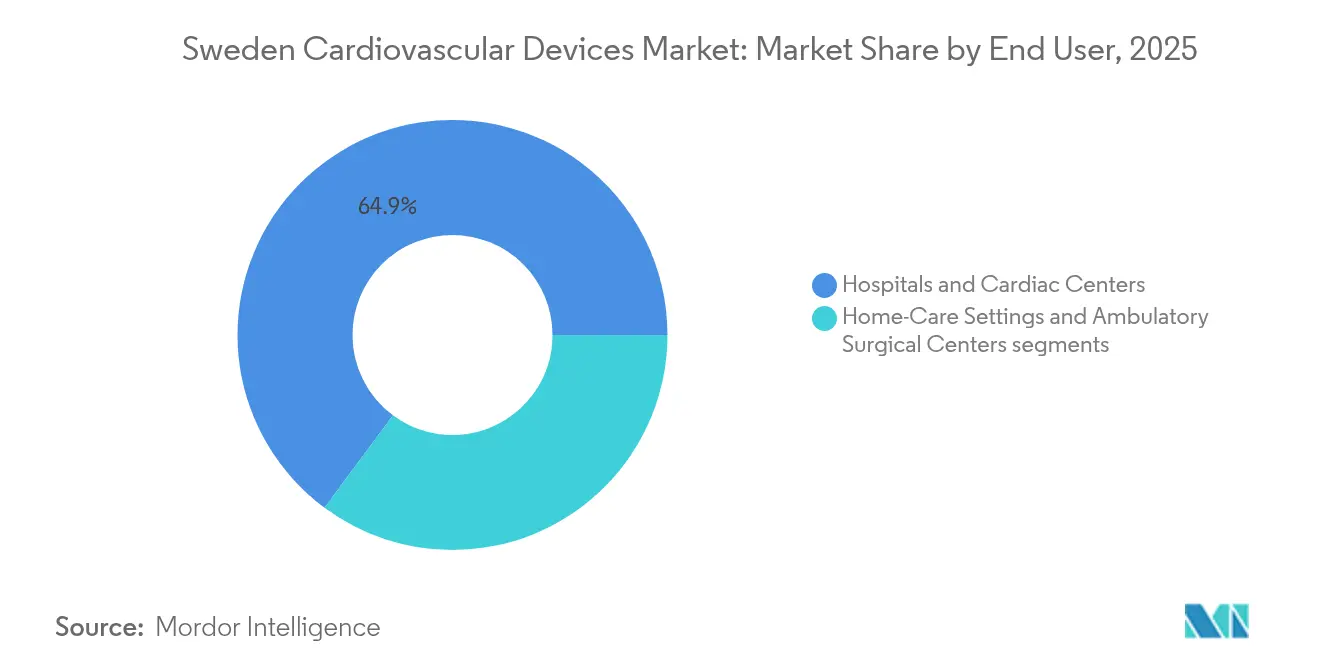

- By end user: Hospitals and cardiac centers held 64.85% of total 2025 revenue, whereas ambulatory surgical centers record the highest projected growth at 7.6% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Sweden Cardiovascular Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of cardiovascular disease & ageing population | 1.30% | Sweden national, with regional variations | Long term (≥ 4 years) |

| National registries enabling real-world evidence adoption | 0.90% | Sweden national, aligned with Nordic cooperation | Medium term (2-4 years) |

| Rapid hospital shift to minimally-invasive & transcatheter procedures | 1.00% | Sweden national, led by university hospitals | Medium term (2-4 years) |

| Government incentives for digital health & remote cardiac monitoring | 0.80% | Sweden national, piloted in Region Stockholm | Short term (≤ 2 years) |

| Green procurement mandates driving OEM sustainability innovation | 0.60% | Sweden national, EU-wide implications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of cardiovascular disease & ageing population

Cardiovascular disease accounts for one-quarter of Swedish mortality, with ischemic heart disease and stroke topping the list among seniors 65 + . The population segment aged 80 + is forecast to rise from 5.2% to 7.1% by 2030, prompting the National Board of Health and Welfare to estimate a 40% jump in cardiovascular interventions over the same horizon. Higher-than-European-average atrial fibrillation prevalence underpins demand for alternatives to oral anticoagulants, such as left atrial appendage (LAA) closure implants that gained selective reimbursement in late 2024. Sweden’s exhaustive registries—Patient Register, Cause of Death Register and SWEDEHEART—supply longitudinal real-world evidence that validates device effectiveness and informs procurement criteria. Taken together, a growing elderly cohort, strong epidemiologic tracking and universal access mandate continued expansion of the cardiovascular devices market.

National registries enabling real-world evidence adoption

The SWEDEHEART platform captures data from every catheterization laboratory and surgical center, tracking more than 200,000 procedures yearly and offering unmatched transparency for device outcomes. Registry-based randomized trials such as TASTE have validated the feasibility of large-scale pragmatic evidence generation without exorbitant costs, shortening the path to reimbursement in Sweden and abroad. Alignment with EuroHeart widens cross-border data harmonization, enhancing the export potential of Sweden-generated evidence for CE-marked products lakemedelsverket.se. TLV routinely references registry findings for value assessments, giving manufacturers that conduct Swedish trials a competitive edge in the cardiovascular devices market. As real-world data continues to inform clinical guidelines, registry infrastructure strengthens Sweden’s appeal as a development hub.

Rapid hospital shift to minimally-invasive & transcatheter procedures

Transcatheter aortic valve replacement volumes jumped 25% in 2024, and all seven university hospitals now use TAVR as first-line therapy in appropriate cases. Region Stockholm’s same-day discharge model for cardiac catheterizations has cut episode-of-care costs by 30% while maintaining comparable safety results, bolstering political and payer support for minimally invasive workflows . National guidelines drafted by the National Board of Health and Welfare favor percutaneous techniques following pharmacoeconomic evaluations that demonstrate reduced ICU stays and rehospitalization rates socialstyrelsen.se. Concentrated surgical expertise at Karolinska, Sahlgrenska and Skåne facilitates structured training, helping regional hospitals replicate best practice and fueling decentralized growth across the cardiovascular devices market. Ongoing participation in European transcatheter registries cements Sweden’s leadership in procedural innovation.

Government incentives for digital health & remote cardiac monitoring

The central government has allocated SEK 2 billion to digital health infrastructure, specifically encouraging cardiovascular solutions that curb hospitalizations government.se. Region Stockholm’s pilot for remote heart failure monitoring decreased admissions by 20% and has since been rolled out nationally under a unified reimbursement code, widening market access for qualified platforms regionstockholm.se. The Medical Products Agency’s fast-track route for software as a medical device trimmed average approval timelines by six months, positioning Sweden as an early-adopter environment for AI-enabled diagnostics lakemedelsverket.se. Harmonized electronic health record standards through the National Patient Summary make data integration straightforward, speeding provider uptake of connected devices. Government backing, streamlined approvals and interoperable IT architecture together reinforce the strategic importance of digital cardiovascular monitoring within the cardiovascular devices market.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU MDR transition increasing time-to-market & costs | -0.70% | Sweden as EU member state | Medium term (2-4 years) |

| Centralised regional tenders squeezing device prices | -0.40% | Sweden national, SKR coordination | Short term (≤ 2 years) |

| Limited reimbursement for novel LAA & wearable devices | -0.50% | Sweden national, TLV evaluation framework | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EU MDR Transition Increasing Time-to-market & Costs

Swedish manufacturers report 15-20% higher compliance expenditure for Class III cardiovascular products under EU MDR, eroding margins for niche devices. Although the Medical Products Agency engaged early with notified bodies, capacity bottlenecks have added 4-6 months to average approval cycles, delaying commercial launches and risking product withdrawals in low-volume categories. Smaller importers struggle to meet extensive clinical data requirements, constricting portfolio diversity in the cardiovascular devices market. Healthcare regions voice concern that certain specialized implants may disappear from procurement lists, potentially disrupting continuity of care. While Sweden participates in EU-wide coordination to clarify grey areas, lingering compliance uncertainty tempers investment in high-risk device R&D.

Limited reimbursement for novel LAA & wearable devices

TLV applies rigorous cost-effectiveness thresholds before granting broad coverage, and evidence demands for novel LAA systems exceed those for pharmaceuticals due to the expectation of demonstrable superiority over anticoagulation therapy. Interim regional funding pathways create patchy access and frustrate uniform adoption, limiting near-term revenue potential even after CE marking. Wearables face assessment via legacy device frameworks that may not capture preventive value, slowing listing decisions despite favorable clinical readouts. Manufacturers must therefore generate Sweden-specific budget-impact models, lengthening market entry timelines and bifurcating launch strategies between professional and consumer channels. Conservative reimbursement patterns, although designed for fiscal prudence, create headwinds for products focused on lifestyle modification rather than acute intervention.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Type: Therapeutic Leadership Amid Digital Transformation

Therapeutic and surgical systems accounted for 62.98% of the cardiovascular devices market in 2025, underpinned by Sweden’s advanced cardiac surgery programs and mature reimbursement infrastructure that rewards long-term outcome data. The cardiovascular devices market size for therapeutic systems is projected to expand in line with a strong 3.92% CAGR as Karolinska’s 400 + annual TAVR caseload sets a Nordic benchmark and attracts regional referrals, supporting higher-value sales of delivery catheters, replacement valves and perfusion equipment. Hospitals prioritize drug-eluting stents, cardiac resynchronization devices and extracorporeal systems with proven cost-utility, a stance that favors established vendors such as Getinge AB, Medtronic and Abbott. Central procurement via SKR strengthens price discipline yet assures predictable demand for technologies that clear TLV’s health-economic hurdle.

Diagnostic and monitoring equipment represent the fastest-growing product class at 5.55% CAGR to 2031, aided by government incentives for remote monitoring, AI-enhanced electrocardiography and wearable sensors. The cardiovascular devices market is witnessing an influx of software-centric entrants leveraging Sweden’s electronic health record interoperability to embed analytics into routine care. Remote heart-failure monitoring platforms, reimbursed since 2024, have spurred regional tenders focusing on data security and integration features rather than hardware price alone. The Medical Products Agency’s six-month rapid-review track for breakthrough software further accelerates rollout, keeping diagnostic vendors firmly on investors’ radar.

By Application: Structural Heart Disease Innovation

Structural heart disease therapies are advancing at a 6.15% CAGR, the fastest among clinical applications, even though coronary interventions still dominate revenue with 41.10% share of the cardiovascular devices market size in 2025. Participation in NOTION and other pan-Nordic aortic and mitral trials provides Swedish centers with first access to next-generation valves and repair systems, bolstering procedure counts at Sahlgrenska and generating early real-world evidence for payers. Increased indications for low-risk patients and streamlined reimbursement approvals for early-adoption programs create a positive feedback loop that sustains growth. Device makers respond by establishing local training centers, highlighted by Karolinska’s SEK 50 million government-funded Nordic hub inaugurated in 2025, which anchors ongoing skill diffusion.

Coronary artery disease maintains market leadership because of Sweden’s dense network of catheterization labs and registry-driven quality benchmarking. SWEDEHEART’s records covering 50,000 annual percutaneous coronary interventions yield granular insights that improve stent selection and procedural protocols ucr.uu.se. Drug-eluting stents permeate 95% of eligible cases, ensuring stable baseline demand despite slowing growth relative to structural heart therapies. The cardiovascular devices market also sees steady momentum in arrhythmia management, where remote monitoring has become standard of care, and in heart-failure implants benefiting from new national guidelines endorsing device-based interventions. Hypertension remains an emerging arena for digital therapeutics as primary care shifts toward proactive management supported by connected blood-pressure monitors.

By End-User: University Hospital Concentration

Hospitals and cardiac centers absorbed 64.85% of cardiovascular device purchases in 2025, reflecting Sweden’s strategy of concentrating complex care at university institutions that act as national referral hubs. The cardiovascular devices market derives two-thirds of its turnover from Karolinska, Sahlgrenska and Skåne, where high case complexity sustains demand for premium heart-lung machines, TAVR kits and mapping systems. Centralized expertise supports uniform protocols and predictable procurement volumes, enabling manufacturers to align service packages and training commitments with long-term framework agreements negotiated at regional level.

Ambulatory surgical centers are projected to post a 7.6% CAGR through 2031 as same-day discharge models migrate from Region Stockholm pilots to nationwide rollout. The cardiovascular devices market therefore leans toward compact, single-use or rapidly reprocessable equipment optimized for outpatient settings. Device vendors catering to this segment highlight shorter setup times and integrated digital documentation features that dovetail with Sweden’s paperless workflow mandates. Home monitoring forms a nascent yet promising end-user domain, especially for chronic heart-failure and hypertension management supported by reimbursed telehealth programs.

Geography Analysis

Sweden serves as the Nordic launchpad for cardiovascular devices, pairing early-stage EU MDR compliance with world-class registries that give manufacturers real-world evidence for global filings. Nordic joint-procurement agreements further lower entry barriers by pooling demand with Norway, Denmark and Finland.

Region Stockholm represents roughly 25% of the population yet an outsized share of device revenue thanks to Karolinska University Hospital, abundant digital-health start-ups and proactive remote-monitoring budgets. Västra Götaland, anchored by Sahlgrenska, dominates structural-heart volumes and draws cross-border patients from western Norway. Skåne capitalizes on its Øresund corridor ties to Denmark, while sparsely populated northern counties lean on tele-cardiology, helicopter EMS and rugged devices built for harsh climates.

Internationally, Getinge AB exports nine in ten locally made systems, and multinationals exploit Sweden’s data-rich environment for FDA and PMDA post-market studies getinge.com. Initiatives like the Nordic Trial Alliance expand registry cohorts and amplify Sweden’s influence in value-based procurement across Europe.

Competitive Landscape

The cardiovascular devices market in Sweden exhibits moderate concentration: multinational leaders dominate high-revenue therapy classes yet domestic suppliers hold significant share in niche surgical technologies and services. Getinge AB anchors the national ecosystem with heart-lung machines and perfusion disposables widely specified by university hospitals, bolstered by a SEK 1.2 billion acquisition in March 2025 that broadened its cardiac-surgery suite getinge.com. Medtronic, Abbott and Boston Scientific vie for coronary and structural heart franchises, differentiating less on unit price and more on registry-documented outcomes and device longevity to satisfy TLV’s stringent cost-utility thresholds. Framework agreements negotiated through SKR prevent price outliers yet assure volume security for selected suppliers, encouraging multiyear service and training commitments aligned with national guidelines. Competitive positioning is increasingly shaped by digital competencies. Swedish start-ups and established imaging vendors capitalize on the Medical Products Agency’s expedited avenue for breakthrough software, enabling first-to-market AI ECG algorithms or cloud-based hemodynamic analytics. Interoperability with the National Patient Summary is a procurement prerequisite, screening out solutions reliant on proprietary data silos. Vendors that package hardware, analytics and telehealth support under a single service contract enjoy advantages as regions seek turnkey solutions that minimize IT integration burden. Sustainability considerations also influence tender scoring: Swedish Medtech guidelines encourage carbon-light manufacturing, reusable instrument loops and transparent lifecycle reporting, tilting awards toward brands capable of documenting environmental impact reductions.

Strategic moves during 2024-2025 highlight the dynamic landscape. Medtronic expanded its Uppsala engineering center to co-develop cryoablation catheters with local clinicians, whereas Abbott partnered with Region Stockholm to pilot sensor-based heart-failure monitoring in primary care clinics. Boston Scientific entered a memorandum with Sahlgrenska University Hospital to train Scandinavian physicians on WATCHMAN Flex implantation following TLV reimbursement acceptance. These collaborative models reinforce Sweden’s profile as a launchpad and knowledge hub within the wider cardiovascular devices market.

Sweden Cardiovascular Devices Industry Leaders

Cardinal Health

Medtronic

Boston Scientific Corporation

Biotronik

Abbott Laboratories

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Region Stockholm extended remote cardiac monitoring reimbursement to all 21 healthcare regions, targeting a 15% drop in heart-failure hospitalizations and annual savings of SEK 200 million.

- September 2024: SWEDEHEART surpassed 2 million patient records, reinforcing Sweden’s leadership in outcomes research. undefined

- Jan 2025: Karolinska University Hospital opened a Nordic transcatheter heart-valve training center with SEK 50 million in government support.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the Swedish cardiovascular devices market as the total annual revenue generated inside Sweden from equipment meant to diagnose, monitor, or treat heart and vascular conditions, including electro-cardiography systems, implantable rhythm-management hardware, vascular catheters, stents, valves, ventricular assist devices, and artificial hearts. Accessories sold with these products, such as lead wires, delivery sheaths, and guidewires, are also counted.

Scope exclusion: over-the-counter consumer wearables and general imaging scanners not labeled for cardiovascular use are left outside the model.

Segmentation Overview

- By Device Type

- Diagnostic & Monitoring Devices

- ECG Systems

- Remote Cardiac Monitors

- Cardiac MRI

- Cardiac CT

- Echocardiography / Ultrasound

- Fractional Flow Reserve (FFR) Systems

- Therapeutic & Surgical Devices

- Coronary Stents

- Drug-Eluting Stents

- Bare-Metal Stents

- Bioresorbable Stents

- Catheters

- PTCA Balloon Catheters

- IVUS / OCT Catheters

- Cardiac Rhythm Management Devices

- Pacemakers

- Implantable Cardioverter Defibrillators

- Cardiac Resynchronization Therapy Devices

- Heart Valves

- TAVR / TAVI

- Mechanical Valves

- Tissue / Bioprosthetic Valves

- Ventricular Assist Devices

- Artificial Hearts

- Grafts & Patches

- Other Cardiovascular Surgical Devices

- Coronary Stents

- Diagnostic & Monitoring Devices

- By Application

- Coronary Artery Disease

- Arrhythmia

- Heart Failure

- Structural Heart Disease

- Hypertension

- Others

- By End-User

- Hospitals & Cardiac Centers

- Home-Care Settings

- Ambulatory Surgical Centers

Detailed Research Methodology and Data Validation

Primary Research

Discussions with cardiologists in Stockholm and Gothenburg, catheter-lab managers across several county councils, and Swedish distributors enabled us to stress-test utilization rates, average selling prices, and EU MDR transition timelines. Follow-up e-surveys with home-monitoring nurses and payor advisers confirmed uptake assumptions for remote cardiac telemetry and TAVI kits.

Desk Research

We began by mapping Sweden's device portfolio using open sources such as the Swedish Medical Products Agency's implant registries, SWEDEHEART outcome database, Eurostat trade codes, and OECD health expenditure dashboards, supplemented by peer-reviewed journals in the European Heart Journal and targeted press releases. Company 10-Ks, Swedish procurement tenders, and clinical-trial filings filled unit-price and pipeline-volume gaps. To enrich financial signals, our team pulled manufacturer revenue splits from D&B Hoovers and screened local news flows through Dow Jones Factiva. The sources cited illustrate our approach; dozens more helped verify data and wording.

Market-Sizing & Forecasting

A top-down reconstruction pairs import-export values (HS codes 9018.90, 9021.90), domestic production, and replacement-cycle estimates, which are then benchmarked against bottom-up snapshots built from sampled device volumes multiplied by interviewed ASPs. Key variables, like procedure volumes from SWEDEHEART, aging-population growth (65+ cohort), public procurement price ceilings, EU MDR compliance costs, and tele-monitoring penetration, drive the model. Multivariate regression combined with scenario analysis projects 2025-2030 demand; where supplier roll-ups under-report niche segments, interpolation from neighbor Nordics bridges gaps.

Data Validation & Update Cycle

Outputs face variance checks versus hospital billing statistics and Prevex price indices before any sign-off. Two analysts review anomalies, and Mordor refreshes each dataset annually, issuing interim corrections when material events, such as regulatory shifts or major tender awards, arise. A final pre-publication sweep ensures clients receive the freshest view.

Why Mordor's Sweden Cardiovascular Devices Baseline Stands Up to Scrutiny

Published numbers often clash because firms select different device baskets, price points, and refresh cadences.

Key gap drivers include inclusion of general imaging gear by some publishers, untreated currency conversions, and single-channel import extrapolations that miss domestic refurbishment flows. Mordor's baseline reports the 2025 market at USD 0.34 billion, grounded in procedure-linked demand and verified ASPs, while others diverge for the reasons summarized below.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 0.34 bn (2025) | Mordor Intelligence | - |

| USD 0.71 bn (2023) | Regional Consultancy A | Bundles imaging systems, no bottom-up cross-check |

| USD 0.33 bn (2025) | Industry Journal B | Relies chiefly on customs data, excludes remote telemetry devices |

Taken together, the comparison highlights that when device scope, pricing discipline, and annual refreshes align, as in Mordor's approach, results converge toward a balanced, decision-ready baseline that clients can audit and reproduce with confidence.

Key Questions Answered in the Report

What is the current size of Sweden’s cardiovascular devices market?

The market stands at USD 353.53 million in 2026 and is projected to reach USD 429.79 million by 2031, reflecting a 3.98% CAGR.

Which device category generates the most revenue in Sweden?

Therapeutic and surgical systems lead with 62.98% of 2025 revenue, driven by transcatheter aortic valve replacements, drug-eluting stents and cardiac rhythm management devices.

Which clinical application is growing the fastest?

Structural heart disease treatments are advancing at a 6.15% CAGR through 2031, outpacing all other application areas.

Why do manufacturers choose Sweden for early-stage European trials?

Sweden’s early EU MDR compliance, extensive registries such as SWEDEHEART and efficient reimbursement reviews create a low-risk environment for first-in-human studies.

How is digital health influencing market growth?

Government investment of SEK 2 billion and nationwide reimbursement for remote cardiac monitoring are propelling a 5.55% CAGR in diagnostic and monitoring devices.

Page last updated on: