Board Games Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

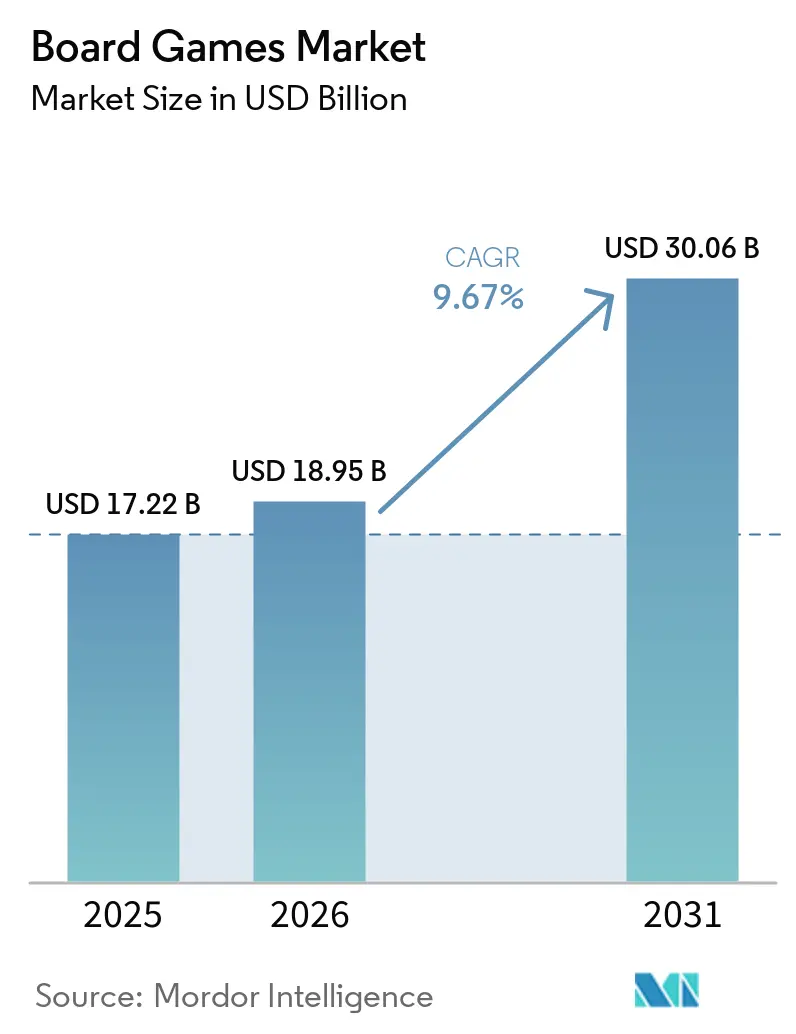

| Market Size (2026) | USD 18.95 Billion |

| Market Size (2031) | USD 30.06 Billion |

| Growth Rate (2026 - 2031) | 9.67% CAGR |

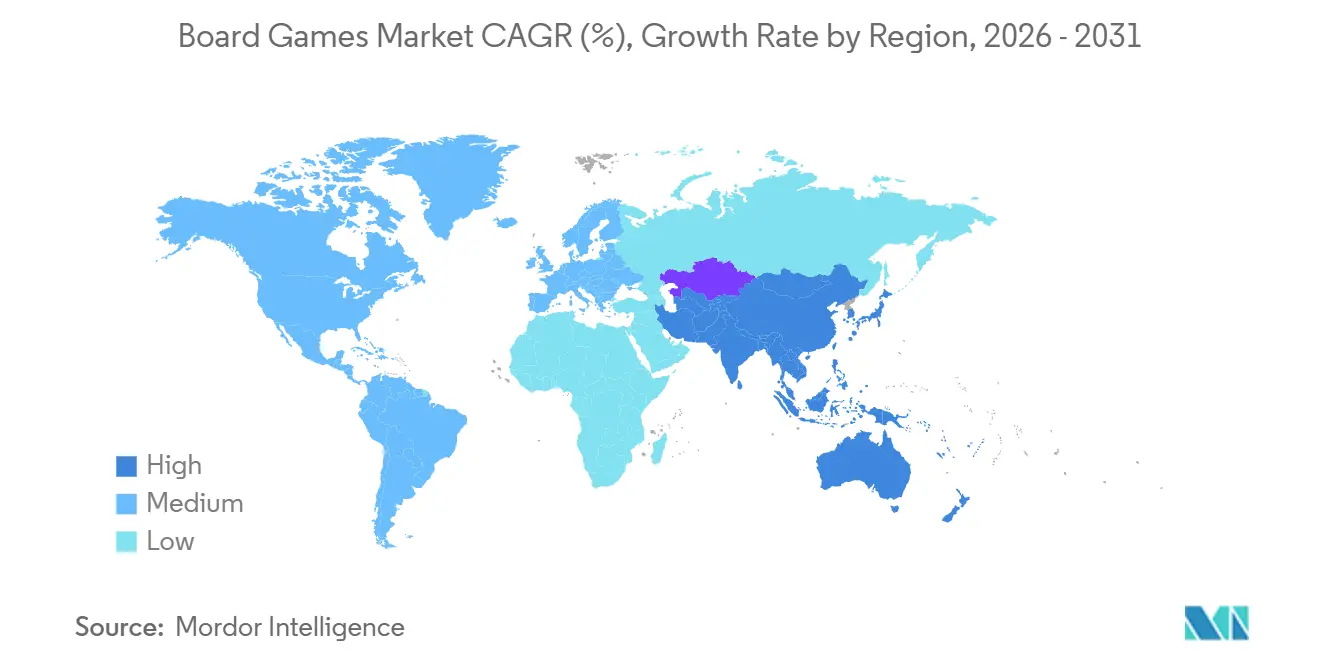

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Board Games Market Analysis by Mordor Intelligence

The Board Games Market size is expected to grow from USD 17.22 billion in 2025 to USD 18.95 billion in 2026 and is forecast to reach USD 30.06 billion by 2031 at a CAGR of 9.67% during 2026-2031. Rising demand for screen-free social entertainment, greater consumer willingness to spend on premium tabletop experiences, and the growing popularity of immersive campaign-based gameplay are accelerating market growth beyond the broader toys and games industry. Strategy and Euro-style games remained the largest revenue-generating category in 2025, while cooperative, legacy, and family games are recording faster adoption as replayability and expansion packs extend product lifecycles and increase consumer spending. Publishers are also broadening their portfolios with licensed intellectual properties, localized editions, and inclusive themes to attract a wider demographic across age groups and regions. In a testament to this trend, the International Chess Federation (FIDE) revealed that in January 2025, China led the pack with its female players achieving an average top 10 rating of 2,482[1]International Chess Federation (FIDE), "Leading chess federations for female players worldwide", ratings.fide.com. Retail channels continue to evolve, with specialty hobby stores driving product discovery, while rapid growth in e-commerce, crowdfunding platforms, and convention-led pre-orders is expanding direct-to-consumer sales. At the same time, established publishers are strengthening their portfolios through acquisitions and licensing partnerships, while independent studios continue introducing innovative titles that sustain category growth and keep consumer interest high.

Key Report Takeaways

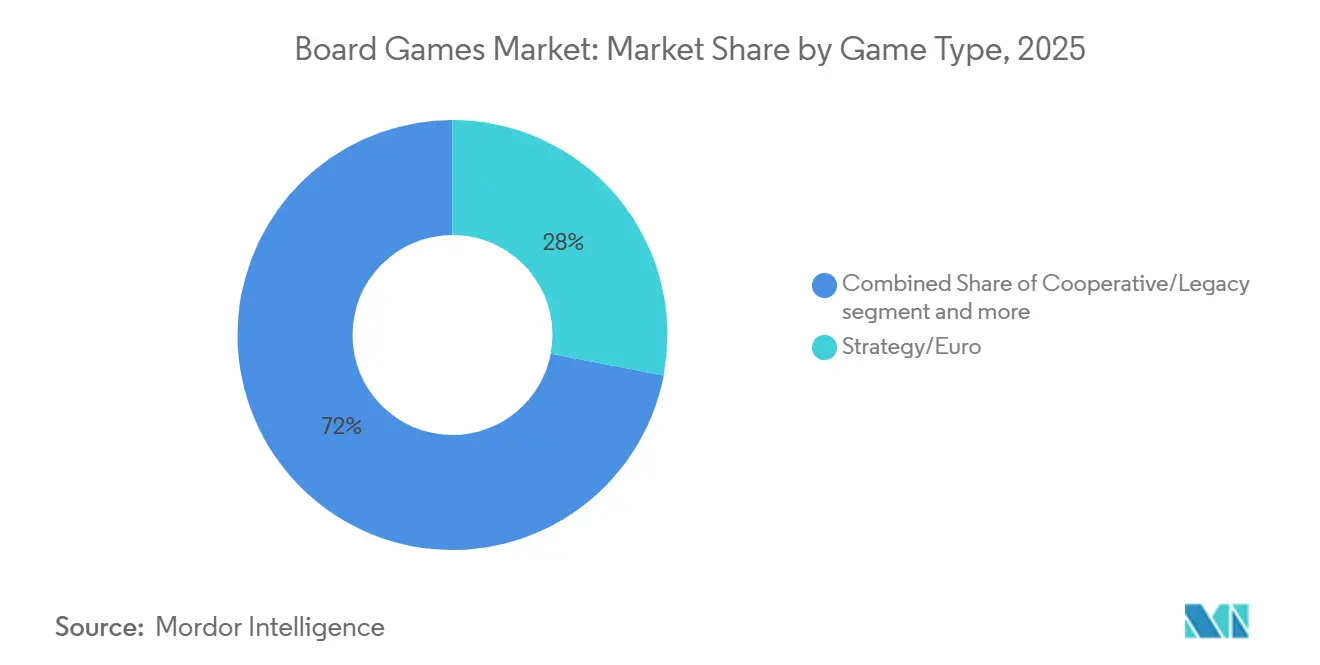

- By game type, Strategy/Euro titles held 28.02% of the board games market share in 2025, while Cooperative and Legacy formats are forecast to register the fastest 10.74% CAGR through 2031.

- By age group, Adults contributed 48.26% of 2025 revenue, but the Children segment is expected to expand at a 10.39% CAGR through 2031.

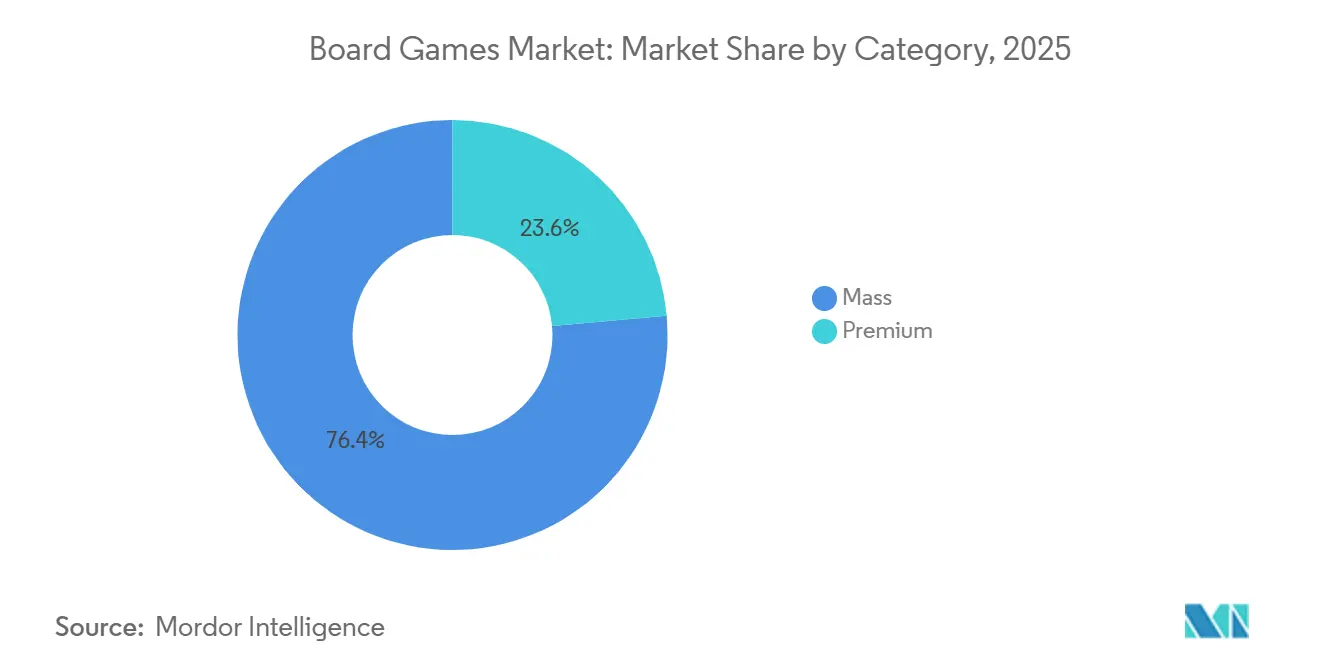

- By category, Mass-market SKUs commanded 76.42% of 2025 sales, whereas Premium collector editions are projected to rise at a 10.85% CAGR to 2031.

- By distribution channel, Specialty stores delivered 37.13% of revenue in 2025, yet Online retail is poised for an 11.28% CAGR through 2031.

- By geography, North America captured 38.41% of the 2025 value; Asia-Pacific is set to post a 10.97% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Board Games Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing interest in offline, screen-free entertainment | +2.1% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Resurgence of analog entertainment | +1.8% | North America, Europe, urban Asia-Pacific | Long term (≥ 4 years) |

| Popularity of board-game cafés and social spaces | +1.5% | North America, Europe, China, Japan, South Korea | Medium term (2-4 years) |

| Crowdfunding-driven democratization of publishing | +1.3% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Eco-friendly production boosting brand affinity | +0.9% | Europe, North America, premium segments in Asia-Pacific | Long term (≥ 4 years) |

| Strong gifting culture around holidays and special occasions | +1.2% | Global, peak in Q4 across all regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing interest in offline, screen-free entertainment

As screen fatigue becomes increasingly prevalent, leisure budgets are being redirected toward analog experiences that not only minimize blue-light exposure but also encourage authentic, face-to-face social interactions. For instance, 27% of U.S. college students felt tired or sleepy within the past seven days as of fall 2025, according to the National College Health Assessment[2]Source: National College Health Assessment, "American College Health Association's National College Health Assessment Fall 2025", acha.org. This growing demand is particularly noticeable among millennials and Gen Z parents. While these generations grew up immersed in digital entertainment, they are now prioritizing hands-on, tactile play experiences for their children. To cater to this shift, publishers are introducing features such as quick-start rules and tutorial videos, which are conveniently accessible through QR codes. These additions aim to reduce the mental effort that has traditionally discouraged casual buyers from engaging with analog games. Furthermore, this trend is self-perpetuating: as households accumulate collections of 5 to 10 game titles, they increasingly organize regular game nights. These gatherings not only establish analog leisure as a norm within their social networks but also significantly enhance word-of-mouth promotion and discovery.

Resurgence of analog entertainment

The resurgence of analog entertainment is creating new growth opportunities for the board games market as consumers increasingly value experiences that deliver creativity, skill development, and shared participation over passive content consumption. Board games are benefiting from this transition by offering high replay value, collectible appeal, and diverse gameplay formats that cater to families, hobby enthusiasts, educational institutions, and corporate team-building activities. Publishers are responding by expanding thematic portfolios through licensed franchises, historical settings, and culturally localized editions that resonate with regional audiences while extending global reach. At the same time, specialty retailers and independent publishers are broadening product availability through exclusive editions and limited-release campaigns, encouraging repeat purchases among collectors. The continued success of crowdfunding platforms has also enabled innovative game mechanics and niche genres to reach commercial scale, strengthening category diversity and reinforcing consumer interest in analog entertainment across both mature and emerging markets.

Popularity of board-game cafés and social spaces

The growing popularity of board game cafés and dedicated social gaming spaces is strengthening demand for board games by providing consumers with low-risk opportunities to discover, learn, and repeatedly engage with new titles before making purchases. Unlike traditional retail stores, these venues function as experiential marketing channels where customers can test strategy, cooperative, family, and party games under guided play sessions, increasing confidence in premium-priced purchases. They also foster local gaming communities through tournaments, themed events, and publisher-led demonstrations, creating sustained engagement beyond one-time transactions. As participation expands, cafés increasingly influence purchasing decisions, driving sales through on-site retail counters and referrals to specialty stores and online channels. Publishers are capitalizing on this trend by deepening collaborations with organized play venues and gaming events. For instance, Ravensburger expanded its partnership with Gen Con in 2025 as a convention co-sponsor, showcasing new tabletop releases such as Horrified: Dungeons & Dragons through immersive demonstrations that strengthened consumer engagement. In 2026, Asmodee partnered with the mental health charity Mind to encourage board game cafés and hobby stores to host community play events, reinforcing cafés as important channels for attracting new players and increasing game participation. These developments are transforming board game cafés from recreational venues into influential ecosystems for product discovery, community building, and long-term market expansion.

Strong gifting culture around holidays and special occasions

The strong gifting culture surrounding holidays, birthdays, and festive celebrations continues to drive board game sales by positioning tabletop games as gifts that deliver shared experiences rather than one-time entertainment. Their broad appeal across children, teenagers, adults, and multigenerational households makes board games a preferred choice during Christmas, Lunar New Year, Diwali, and other seasonal celebrations. Publishers increasingly synchronize product launches and premium editions with these high-demand periods, while retailers expand curated gift assortments, exclusive bundles, and limited-edition offerings to encourage higher consumer spending. In 2025, Goliath Games expanded its portfolio by introducing new family and party board games under licensed entertainment brands, strengthening its presence in seasonal gifting categories across major retail channels. In 2026, Hachette Boardgames UK broadened its distribution portfolio by adding new strategy and family board game publishers, increasing the availability of premium tabletop titles across specialty retailers ahead of key holiday shopping periods. These initiatives improve product visibility during peak gifting seasons, stimulate impulse purchases, and encourage consumers to purchase multiple games for different age groups and occasions, reinforcing holiday gifting as a consistent growth driver for the global board games market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from digital gaming and streaming | -1.4% | Global, most acute in Asia-Pacific and North America | Short term (≤ 2 years) |

| Counterfeit and IP-infringing titles | -0.8% | Asia-Pacific, Eastern Europe, Latin America | Medium term (2-4 years) |

| Localization and translation challenges | -0.6% | Global, critical for Asia-Pacific and South America entry | Medium term (2-4 years) |

| Paper and pulp supply shortages | -1.0% | Global, with acute pressure in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Competition from digital gaming and streaming

Competition from digital gaming and streaming platforms continues to restrain the growth of the global board games market by capturing a larger share of consumers' leisure time and discretionary spending. Mobile games, console titles, subscription gaming services, and video-on-demand platforms offer instant accessibility, frequent content updates, and multiplayer experiences without requiring physical space or coordinated group participation. This convenience is particularly attractive to younger consumers, reducing the frequency of board game purchases and limiting repeat engagement among casual players. Publishers are therefore facing increasing pressure to differentiate physical games through immersive mechanics, premium components, and licensed intellectual properties. Reflecting this competitive landscape, CMON streamlined its product portfolio in 2025 by prioritizing high-performing crowdfunding campaigns and established franchises to improve commercial efficiency amid changing consumer preferences. Likewise, Steamforged Games expanded its portfolio of video game-inspired tabletop titles in 2026, leveraging well-known digital gaming intellectual properties to attract existing gaming communities into the tabletop segment. These developments highlight how digital entertainment is reshaping consumer expectations and intensifying competitive pressure across the global board games market.

Counterfeit and IP-infringing titles

The proliferation of counterfeit and intellectual property (IP)-infringing board games continues to restrain market growth by eroding publisher revenues, weakening brand equity, and reducing consumer confidence in premium tabletop products. Counterfeit games are often sold through unauthorized online marketplaces and informal retail channels at significantly lower prices, while offering inferior materials, incomplete components, and poor print quality that negatively affect the overall gameplay experience. The challenge is particularly pronounced for bestselling strategy, family, and party games, where strong brand recognition makes successful titles frequent targets for imitation. As counterfeit products become more sophisticated, publishers are increasing investments in packaging security, authentication measures, and legal enforcement to protect their intellectual property and preserve consumer trust. Reflecting these efforts, The Op Games expanded its portfolio of officially licensed tabletop games in 2025, strengthening brand protection through exclusive licensing agreements with major entertainment franchises. In 2026, Maestro Media broadened its portfolio of officially licensed board games through new intellectual property partnerships, reinforcing the importance of authorized publishing rights in a market increasingly challenged by counterfeit products. These developments underscore the commercial risks posed by IP infringement across the global board games market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Game Type: Legacy Formats Reshape Engagement Models

Strategy and Euro games accounted for 28.02% of the global board games market revenue in 2025, supported by strong demand for deep gameplay, high replayability, and premium-priced titles among hobby gamers. Publishers continue investing in the segment through new releases and expansions to extend franchise lifecycles. For instance, Czech Games Edition expanded its strategy portfolio in 2025 by launching new editions of Codenames and releasing the Lost Ruins of Arnak: Twisted Paths expansion, while confirming wider multilingual distribution into 2026, reinforcing sustained demand for premium strategy titles.

Cooperative and Legacy games are projected to register a 10.74% CAGR during 2026–2031, driven by increasing consumer preference for campaign-based gameplay, evolving narratives, and long-term replayability. Publishers are expanding investment in story-driven cooperative experiences to attract both hobby gamers and new audiences. For example, CD PROJEKT RED and Go On Board announced The Witcher: Legacy in 2025, a cooperative campaign board game with branching narratives and persistent progression, highlighting continued innovation and commercial momentum within the cooperative and legacy game segment.

By Age Group: Children Segment Accelerates on STEM Demand

In 2025, adults contributed 48.26% of spending, driven by higher disposable incomes and a preference for 90-minute Eurogame sessions. Meanwhile, the children's segment is projected to grow at a strong 10.39% CAGR, as parents and educators increasingly look for screen-free, skill-building tools. In 2024, children under 12 accounted for over 60% of mass-market purchases, with school budgets expanding for products tied to curricula, such as those teaching coding logic and spatial reasoning.

Teenagers, operating within budgets of USD 20 to USD 40, are attracted to social-deduction party games like Werewolf and Secret Hitler. This trend was reinforced by Exploding Kittens' board-game launch at USD 24.99 in July 2025, which secured prominent end-cap placements at Target and Walmart. Adult preferences are diverging: casual players prefer cooperative games under an hour, while hobbyists are investing in multi-season legacy boxes. Publishers are now developing modular rules that adapt in complexity, enabling a single SKU to appeal to players with varying experience levels and optimizing returns on design investments.

By Category: Premium Editions Capture Enthusiast Dollars

Mass-market SKUs, supported by sub-USD 40 price points and broad distribution, are anticipated to contribute 76.42% of 2025 sales. Retail giants allocate 80% of their physical shelf space to these accessible titles, capitalizing on competitive pricing and recognizable intellectual properties to drive impulse purchases. In contrast, premium collector lines are forecasted to achieve a strong 10.85% CAGR, propelled by Kickstarter pre-orders that reduce production risks and attract buyers for high-end products priced between USD 100 and USD 200.

Out-of-print editions from CMON experienced up to a 50% increase in value on the secondary market last year, solidifying the collectibles narrative and attracting additional investment into the segment. Although eco-friendly materials increase unit costs by 10%–20%, they enable higher price points among environmentally conscious consumers. Conventional publishers are exploring “deluxe” mid-tier offerings priced at USD 50–USD 70, aiming to appeal to consumers transitioning from mass-market to premium without incurring the full costs associated with collector-level products.

By Distribution Channel: E-Commerce Erodes Specialty Margins

In 2025, specialty stores contributed 37.13% of the market value by focusing on hand-selling complex titles and hosting demo nights. With a stock depth ranging from 200 to 500 SKUs, these stores provide a discovery experience that big-box chains cannot replicate, while their in-store activities build strong community engagement. At the same time, online revenue is projected to grow at an 11.28% CAGR, driven by Amazon’s notable 29% category growth and direct-to-consumer models that protect publisher margins. Furthermore, the expansion of internet access is strengthening online retail channels. For instance, the International Telecommunication Union (ITU) reported that global internet access increased to 74% in 2025, compared to 71% in 2024[3]Source: International Telecommunication Union (ITU), "Individuals Using the Internet", itu.int.

Hypermarkets and supermarkets primarily focus on family titles priced below USD 30, leveraging aggressive Q4 bundles that account for 40% of their annual sales. Other channels, such as cafés, conventions, and publisher webstores, generate lower-volume but higher-margin revenue and serve as valuable sources for future product insights. Stonemaier’s hybrid model exemplifies this approach, with 60%–70% of its inventory pre-sold on Kickstarter before retail distribution, demonstrating how integrated channel planning can effectively balance cash flow and market reach.

Geography Analysis

In 2025, North America accounted for 38.41% of the global turnover, with the U.S. contributing over 60% of the regional value. Around 1,200 dedicated game shops support a thriving discovery and tournament ecosystem. In early 2026, tariffs on Chinese components, reaching up to 145%, reduced gross margins by 3–5 percentage points. This led to a shift towards nearshoring in Mexico, where wages are 30%–40% lower than in the U.S., and freight lead times have decreased to 10 days. Hasbro reported USD 4.7 billion in revenue for 2025, with Wizards of the Coast contributing USD 2.2 billion, highlighting the effectiveness of a dual analog-digital model that outperforms category averages. USMCA tariff exemptions are driving assembly operations to Monterrey and Toronto, strengthening North America's supply chain resilience.

Asia-Pacific is projected to grow at a 10.97% CAGR through 2031. Although China's growth is hindered by regulatory challenges such as the NPPA content review, which can extend lead times by up to 18 months, rising disposable income continues to drive demand. India is expected to lead regional growth as urban families increasingly adopt board games as an affordable entertainment option, supported by widespread English fluency. Japan and South Korea are becoming key markets for premium collector editions, with conventions in Tokyo and Seoul drawing 30,000–40,000 attendees annually. Rising labor costs in China and geopolitical tensions are prompting publishers to diversify manufacturing to Vietnam and India, enhancing supply-chain flexibility.

Europe recorded moderate growth, led by Germany and the UK. The 2023 Essen Spiel event attracted 162,000 visitors and generated EUR 15 million in sales, reinforcing Germany's position as the hub of Eurogame design. While the EU's Extended Producer Responsibility laws introduce cost pressures, they also provide a competitive advantage for early adopters. South America and the Middle East and Africa collectively contributed less than 10% of global revenue. However, Brazil and the UAE are emerging as key regional players. Brazil benefits from nearshoring trends that reduce lead times to North America, while the UAE's multilingual expatriate population drives demand for premium English-language imports.

Competitive Landscape

In the competitive landscape, a combination of market concentration and continuous innovation defines the dynamics: leading publishers actively rejuvenate timeless titles by leveraging synergies, while a wide range of indie studios consistently introduces innovative and unique concepts. Hasbro, under its "Playing to Win" strategy, has set an ambitious goal of reaching 750 million consumers by 2027. The company is revitalizing its classic brands through digital enhancements and is intensifying its efforts to expand into emerging markets, showcasing a forward-looking approach to growth.

While established players such as Hasbro, Mattel, and Ravensburger maintain a dominant presence, indie publishers like Stonemaier Games, Cephalofair, and CMON are rapidly gaining traction. Platforms such as Kickstarter and Gamefound have significantly disrupted the traditional publishing landscape, enabling niche games to achieve global recognition. These platforms have also fueled a rise in designer-led initiatives, empowering creators to bring their visions to life and connect directly with a global audience.

Digital innovations, from app-assisted gameplay and online platforms to AI-driven features, are seamlessly blending the physical and digital realms. This not only heightens player engagement but also broadens revenue streams. Moreover, leveraging technology can provide a competitive edge. For instance, studios harnessing AI for tasks like rules adjudication can channel those savings into enhancing art and storytelling, amplifying their market appeal. Furthermore, emerging mixed-reality prototypes suggest a future where NFC-equipped miniatures engage with apps for dynamic storytelling, bridging digital content with physical enhancements. Early adopters of these innovations could command significant pricing leverage, enhancing their profit margins in the board games market.

Board Games Industry Leaders

-

Hasbro Inc.

-

Mattel Inc.

-

Asmodee Group

-

Ravensburger AG

-

Spin Master Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Hasbro unveiled its comprehensive “Playing to Win” strategy, targeting expansion from 500 million to 750 million consumers by 2027 with anticipated mid-single-digit revenue growth and improved operating margins.

- March 2025: Hasbro introduced MONOPOLY App Banking and CONNECT 4 Frenzy at the 2025 Toy Fair, demonstrating digital-physical integration strategies that modernize classic games while preserving tactile gameplay elements.

- August 2024: The board game "Rock Hard:1977" debuted, catering to 2–5 players aged 16 and above. Blending strategic planning with a dash of luck, the game unfolds over nine "months," segmented into morning, evening, and after-hours phases. Players can leverage "candy" tokens, which provide risk/reward boosts reminiscent of a vice-fueled momentum.

Global Board Games Market Report Scope

A board game is a type of tabletop game that involves small objects ( game pieces ) that are placed and moved in particular ways on a specially designed, patterned game board. The board games market report is segmented by game type, age group, category, distribution channel, and geography. By game type, the market is segmented into traditional/classics, strategy/euro, card and dice, cooperative/legacy, miniature wargames, educational, and puzzle hybrids. By age group, the market is segmented into children, teenagers, and adults. By category, the market is segmented into mass and premium. By distribution channel, the market is segmented into hypermarkets and supermarkets, specialty stores, online retail stores, and other distribution channels. By geography, the market is segmented into North America, South America, Europe, Asia-Pacific, the Middle East and Africa. For each segment, the market forecasts are provided in terms of value (USD) and volume (units).

| Traditional/Classics |

| Strategy/Euro |

| Card and Dice |

| Cooperative/Legacy |

| Miniature Wargames |

| Educational and Puzzle Hybrids |

| Children |

| Teenagers |

| Adults |

| Mass |

| Premium |

| Hypermarkets and Supermarkets |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Game Type | Traditional/Classics | |

| Strategy/Euro | ||

| Card and Dice | ||

| Cooperative/Legacy | ||

| Miniature Wargames | ||

| Educational and Puzzle Hybrids | ||

| By Age Group | Children | |

| Teenagers | ||

| Adults | ||

| By Category | Mass | |

| Premium | ||

| By Distribution Channel | Hypermarkets and Supermarkets | |

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast will global revenue grow for physical tabletop titles between 2026 and 2031?

It is forecast to rise at a 9.67% CAGR, taking the board games market size from USD 18.95 billion in 2026 to USD 30.06 billion by 2031.

Which gameplay format is poised to be the fastest-growing through 2031?

Cooperative and legacy formats are projected to advance at a 10.74% CAGR as campaign-based storytelling extends player engagement.

What share of 2025 spending came from North America?

North America held 38.41% of global value, with the United States accounting for more than three-fifths of the regional total.

How are tariffs influencing manufacturing footprints?

U.S. duties of up to 145% on Chinese components introduced in early 2026 are pushing publishers to nearshore final assembly to Mexico and expand sourcing in Vietnam.

Page last updated on: