Online Board Games Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.72 Billion |

| Market Size (2031) | USD 3.52 Billion |

| Growth Rate (2026 - 2031) | 5.29% CAGR |

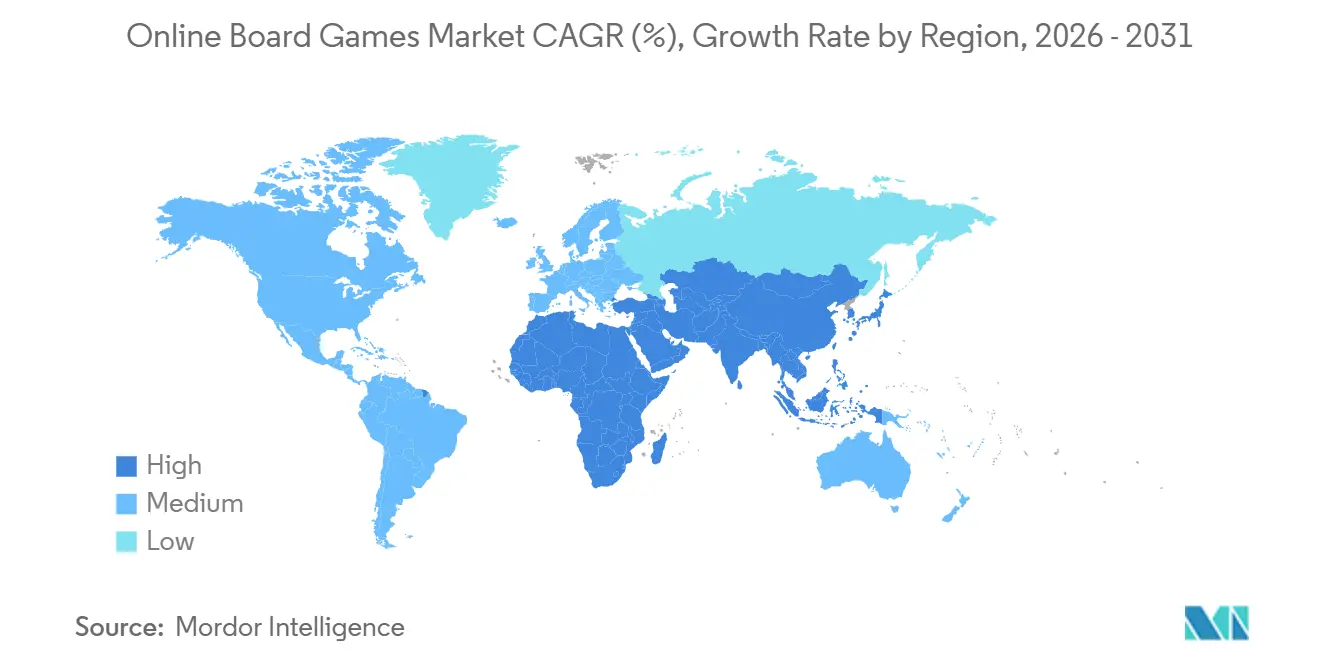

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Online Board Games Market Analysis by Mordor Intelligence

The online board games market size is projected to expand from USD 2.28 billion in 2025 and USD 2.72 billion in 2026 to USD 3.52 billion by 2031, registering a 5.29% CAGR between 2026 to 2031. Always-connected play, generative-AI scenario creation, and carbon-neutral blockchain ownership are shifting the revenue base from one-time sales to subscriptions and secondary-market royalties. Infinite procedural campaigns lower content-production costs and extend user engagement, encouraging publishers to bundle ongoing access into predictable monthly plans. Carbon-efficient proof-of-stake protocols allow NFT-backed pieces and boards to trade peer-to-peer with low fees, adding perpetual royalty income. Asia-Pacific leads adoption, supported by smartphone penetration and national policies that prioritize local intellectual property, while Middle East investment funds accelerate infrastructure and studio acquisitions. Platform holders such as Netflix and Amazon integrate controller-based titles into living-room screens, broadening addressable audiences beyond mobile.

Key Report Takeaways

- By platform, mobile captured 70.63% of online board games market share in 2025; console and smart-TV deployments are advancing at a 5.84% CAGR through 2031.

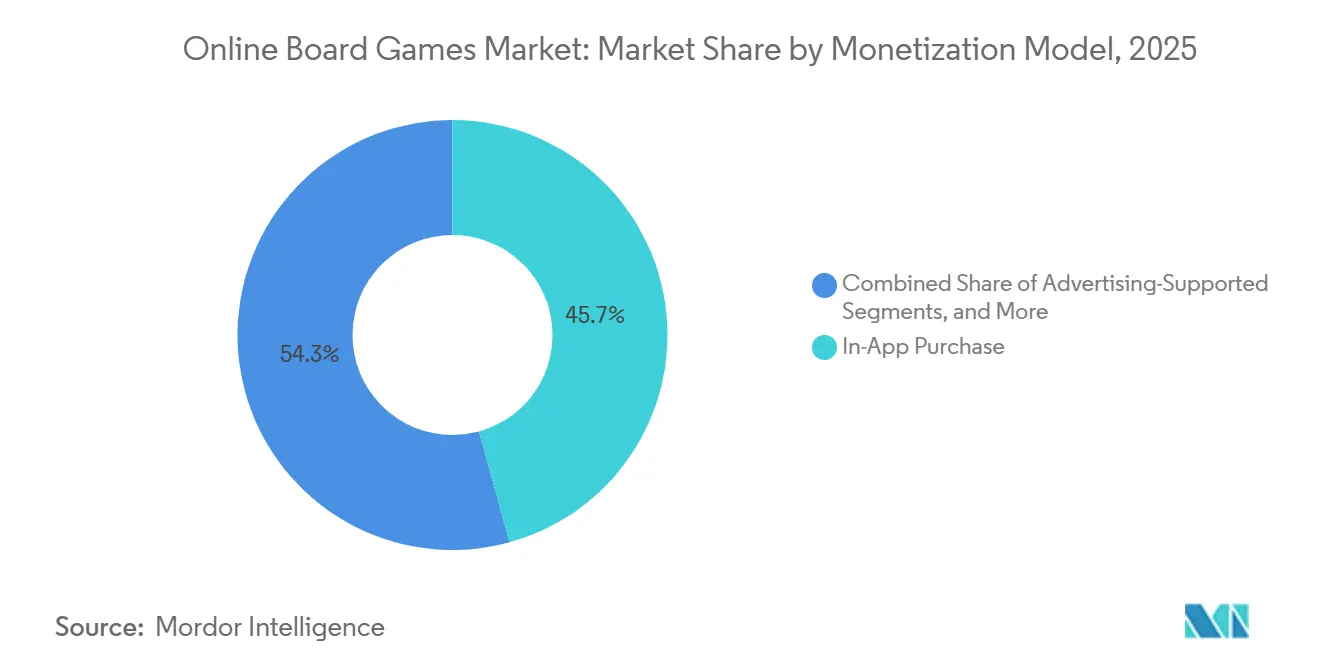

- By monetization model, in-app purchases led with 45.72% of revenue in 2025, whereas subscription and season-pass models are expanding at a 5.57% CAGR to 2031.

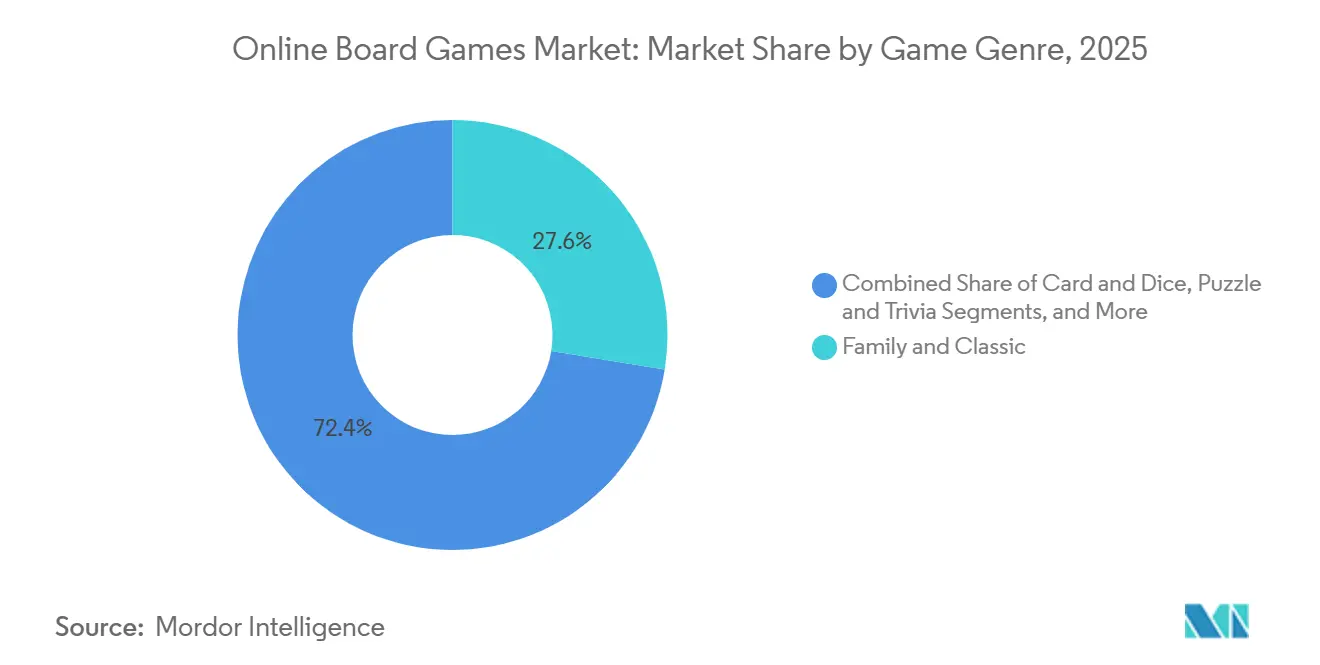

- By genre, family and classic titles held 27.57% of revenue in 2025, while RPG and adventure conversions are projected to post the fastest 6.01% CAGR.

- By player mode, multiplayer accounted for 63.81% of revenue in 2025 and is forecast to grow at a 6.17% CAGR, the quickest among mode segments.

- By geography, Asia-Pacific retained 34.53% of 2025 revenue, and the Middle East is poised for the highest regional growth at a 5.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Online Board Games Market Trends and Insights

Drivers Impact Analysis*

| Driver | (+ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration of Generative-AI dungeon-master modules creating infinitely replayable board scenarios | +0.9% | Global, with early adoption in North America and Asia-Pacific | Medium term (2-4 years) |

| NFT-backed ownership of digital board assets unlocking secondary-market monetization streams | +0.7% | North America, Europe, Middle East | Long term (≥4 years) |

| Voice-controlled gameplay adoption among visually-impaired users broadening total addressable market | +0.4% | Global, particularly North America and Europe | Medium term (2-4 years) |

| Cross-IP mash-ups featuring streaming-series franchises in limited-time board events | +0.8% | Global, with highest impact in North America and Asia-Pacific | Short term (≤2 years) |

| Carbon-neutral blockchain protocols easing environmental concerns around on-chain board gaming | +0.5% | Europe, North America | Long term (≥4 years) |

| 5G-driven latency reduction enabling synchronous multiplayer on-the-go | +1.0% | Asia-Pacific core, spill-over to Middle East and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Integration Of Generative-AI Dungeon-Master Modules Creating Infinitely Replayable Scenarios

Large language models now fabricate coherent board narratives on demand, trimming design labor by roughly 60% and turning finite campaigns into evergreen services. Publishers who previously shipped 20 to 30 scripted levels now deploy generative engines that produce millions of permutations, converting board games from finite products into infinite services. This shift favors subscription monetization over one-time purchases, as players perceive ongoing value from algorithmically refreshed content. Smaller studios gain parity because narrative depth now scales with compute rather than payroll. The competitive field, therefore, widens even as compliance questions around AI-generated intellectual property remain unresolved.[1]Microsoft Research, “WHAM: World Model for Hierarchical Action Models,” microsoft.com

NFT-Backed Ownership Of Digital Board Assets Unlocking Secondary-Market Monetization

Carbon-neutral layer-2 protocols mint and trade board pieces with negligible fees, letting players capture resale value and granting publishers a 5%-10% royalty on every secondary sale. However, regulatory scrutiny is intensifying; the European Union's Markets in Crypto-Assets Regulation mandates disclosure of environmental impact and consumer-protection safeguards, raising compliance costs for smaller developers. Immutable X processed more than 50 million such transactions in 2024 without gas charges, illustrating the scale possible when energy costs and environmental objections disappear.[2]Immutable X, “Carbon-Neutral NFT Transactions,” immutable.com

Voice-Controlled Gameplay Broadening Access For Visually Impaired Players

Natural-language interfaces narrate board states, accept spoken moves, and clarify rules, opening play to an estimated 2.2 billion people with vision impairment. A 2024 study published in the ACM Conference on Human Factors in Computing Systems found that voice-controlled chess interfaces improved move accuracy by 40% among visually impaired participants compared to tactile boards.[3]ACM Conference Proceedings, “Voice-Controlled Chess Interfaces for Visually Impaired Users,” dl.acm.orgPublishers embedding these tools also qualify for accessibility grants and public-sector procurement that require Section 508 compliance. The incremental development cost is modest-typically under USD 50,000 for voice-API integration-yet adoption remains uneven, as many studios prioritize features that appeal to the majority sighted demographic.

5G-Driven Latency Reduction Enabling Synchronous Multiplayer On The Go

Standalone 5G cut round-trip times below 10 milliseconds in live operator trials, making synchronous board turns feasible during commutes. SoftBank and Ericsson recorded a 90% latency drop versus 4G, while T-Mobile’s U.S. rollout posted similar figures. Developers that optimize for portrait-mode one-handed play now reach urban riders who previously defaulted to asynchronous titles. Publishers are redesigning user interfaces to accommodate one-handed play and portrait orientation, optimizing for subway riders who cannot deploy tablets. The competitive implications are stark: developers who fail to optimize for 5G will cede market share to mobile-first studios that treat cellular connectivity as the primary distribution channel.

Restraints Impact Analysis*

| Restraint | ( ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory clampdown on loot-box mechanics aligning them with gambling laws | -0.6% | Europe (Belgium, Netherlands, UK), with spillover to North America | Short term (≤2 years) |

| Bandwidth-throttling policies on ad-supported traffic in emerging markets reducing play quality | -0.4% | Asia-Pacific (India, Indonesia), Africa | Medium term (2-4 years) |

| Rising cyber-bullying incidents in multiplayer board lobbies triggering parental backlash | -0.3% | Global, with highest impact in North America and Europe | Short term (≤2 years) |

| Open-source board-game AIs cannibalizing premium puzzle titles via free GitHub distribution | -0.5% | Global, particularly North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Clampdown On Loot Boxes

Belgium and the Netherlands already ban randomized rewards, and the United Kingdom is drafting similar rules that force odds disclosure and spending caps. Publishers pivot to deterministic season passes, but average revenue per paying user falls 15%-25% as the variable-ratio reinforcement loop disappears. Smaller studios lacking the resources to redesign monetization systems face existential risk, while incumbents like Electronic Arts and Activision Blizzard have absorbed compliance costs and repositioned loot boxes as "surprise mechanics" in jurisdictions with ambiguous statutes. The regulatory trajectory suggests that loot-box bans will expand to additional markets, compressing margins across the industry.

Bandwidth-Throttling Policies On Ad-Supported Traffic

Telecom regulators in India and Indonesia permit carriers to charge for priority routing, relegating free-to-play video ads to slower lanes. Session drops during ad playback prompt uninstalls and raise customer-acquisition costs. Developers compress creatives or pre-cache video but still face 10%-20% higher operating expense.[4]Telecom Regulatory Authority of India, “Differential Pricing Frameworks 2024,” trai.gov.in The long-term solution may involve hybrid monetization that combines lightweight ads with microtransactions, but this approach risks alienating price-sensitive users who gravitate toward ad-supported models precisely because they avoid upfront payments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Monetization Model: Subscriptions Reshape Revenue Predictability

In-app purchases delivered 45.72% of 2025 revenue, yet subscription and season-pass plans are set to expand at 5.57% CAGR, the fastest among models. Warmachine’s digital pass converted 22% of its base in the first year, demonstrating that bundled perks and constant content refresh shift spend from episodic to recurring. Flick Solitaire launched a three-tier season-pass system in 2025-free, premium at USD 4.99 per month, and ultimate at USD 9.99 per month-that gates exclusive card backs and daily challenges behind paywalls, generating 35% higher lifetime value than one-time purchasers.

Apple’s privacy rules lowered ad-targeting accuracy, pushing eCPM down and crowding screens with more ads, so diversification across revenue streams now hedges volatility. Paid-up-front apps languish in the single digits because freemium trials dominate discovery. Netflix’s inclusion of board titles inside its video subscription signals that recurring access, not individual SKU sales, will anchor future online board games market growth.

By Platform: Console And Smart-TV Deployments Accelerate

Mobile owned 70.63% of 2025 spending, but console and smart-TV formats will climb at a 5.84% CAGR as households pivot to living-room play. Netflix launched 40 mobile games in 2024 and expanded to smart-TV interfaces in 2025, embedding titles like Oxenfree and Into the Breach into its streaming app to keep subscribers engaged between content releases Netflix Investor Letter Q4 2024. Amazon's Fire TV integrated Xbox Cloud Gaming in 2024, enabling subscribers to play board-game adaptations like Catan and Ticket to Ride on television screens without purchasing dedicated consoles.

Tablets claim mid-teen share for family game nights. Meanwhile, PCs serve deep-strategy fans, though their growth lags the shift toward handheld and big-screen casual sessions. Cross-platform progression, where players start on phones and finish on TVs, is emerging as a core retention feature despite raising QA spend up to 40%.

By Game Genre: RPG Conversions Lead The Tabletop Renaissance

Family classics such as Monopoly, Scrabble, and Ludo accounted for 27.57% of 2025 income, underscoring the pull of nostalgia. However, RPG and adventure board conversions are expanding at 6.01% CAGR through 2031, the fastest rate among genre segments, as the success of Baldur's Gate 3-which sold 15 million copies and won Game of the Year in 2023-validated demand for rules-heavy digital tabletop experiences.

Strategy and abstract titles remain evergreen due to competitive ladders, while card-and-dice games rely on event-driven tournaments and cosmetic sales. The genre fragmentation reflects divergent player motivations: family games prioritize accessibility and nostalgia, RPG conversions cater to min-maxers, and strategy titles reward pattern recognition and long-term planning.

By Player Mode: Multiplayer Dominance Reflects Social Imperative

Multiplayer captured 63.81% of 2025 spend and will rise at 6.17% CAGR as synchronous play cements community stickiness. Voice chat, ranked ladders, and cross-device lobbies deepen engagement. Player-versus-player formats dominate competitive genres like chess and card games, where ranked ladders and leaderboards provide extrinsic motivation, while co-op and team-play modes appeal to households seeking shared entertainment experiences

Single-player AI modes serve onboarding and low-bandwidth niches but face free open-source competition such as Stockfish and Leela Chess Zero. Turn-based asynchronous loops cater to working adults seeking flexible session lengths, preserving relevance within the online board games industry.

Geography Analysis

Asia-Pacific generated 34.53% of 2025 revenue, powered by China’s preference for homegrown IP, Japan’s commuter gaming culture, and India’s 400 million-player base supported by sub-USD 100 smartphones. Tencent met new real-name and minor play-time limits via biometric verification, sustaining reach within the online board games market. Bandwidth throttling, however, undercuts ad-funded models in India and Indonesia.

North America accounted for roughly 28% of 2025 spend thanks to high ARPU and console-to-mobile crossover adoption. State-level fragmentation around loot-box rules complicates compliance, yet sizable discretionary income still enables robust virtual-goods demand. Canada’s mandatory French localization for Quebec elevates production budgets but unlocks a lucrative bilingual cohort.

Europe supplied about 22% of revenue. GDPR limits behavioral advertising and accelerates subscription uptake, while Belgium and the Netherlands enforce outright loot-box bans. The Middle East, led by Saudi Arabia’s USD 38 billion Savvy Games Group program, is the fastest-growing territory, with a 5.98% CAGR, as the region builds studios and esports venues. Africa remains nascent due to sub-10 Mbps average speeds, but M-Pesa mobile money in Kenya and South Africa enables microtransactions where credit cards are scarce. South America sits in low single-digit share; Brazil’s macro volatility tempers dollar-denominated growth even as player numbers climb.

Competitive Landscape

The online board games market remains fragmented; the top five publishers-Zynga, Tencent, Scopely, Hasbro, and Nintendo-controlled an estimated 35% of 2025 revenue. Zynga cross-promotes Words With Friends and Poker to cut acquisition costs 40%. Tencent embeds mini-board games in WeChat, bypassing app store fees and reaching 600 million monthly players. Scopely’s Monopoly GO! crossed USD 3 billion lifetime revenue by aligning limited-time boards with real-world holidays.

Large incumbents lean on franchise licensing to leverage built-in fan bases, while independents emphasize accessibility and procedural content. Hasbro’s Universes Beyond brings Magic: The Gathering and Warhammer into Dungeons and Dragons digital scenarios to cross-pollinate communities. Voice-interface startups target visually impaired gamers, and blockchain-native studios monetize perpetual royalties on secondary trades. Microsoft’s 2024 patent for real-time difficulty adjustment hints at adaptive AI as the next moat.

Open-source AI chess engines erode premium single-player revenue, so differentiation now centers on social features, cosmetics, and cross-device convenience. Compliance agility likewise shapes advantage as publishers navigate divergent loot-box policies, data-privacy mandates, and sustainability disclosures across regions.

Online Board Games Industry Leaders

Zynga Inc.

Tencent Holdings Ltd.

Scopely (MONOPOLY GO!)

Supercell OY

PLR Worldwide Sales Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Aloft, the cozy skybound survival adventure game, has launched its latest update Gliders & Gales. The update introduces expanded glider customization with dozens of new options, including new patterns, shapes, fabrics, trails, and oculi with upgrades.

- January 2026: Mantic Games relaunched , The Walking Dead: All Out War in a new way with 3D-printing technology, and the ways in which many modern tabletop gamers collect, build, and play

- January 2025: Scopely reported Monopoly GO! surpassing USD 3 billion cumulative revenue within 24 months.

- December 2024: Netflix extended its gaming catalog to smart-TV platforms in 50 countries, debuting controller-compatible board games,

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the online board games market as all revenue generated when classic or native tabletop titles are played through connected digital applications, mobile, browser, or PC client, where matchmaking, rule enforcement, and payments are handled online. Titles range from chess portals to app-based conversions of modern Euro games.

Scope exclusion: Physical retail sales of boxed games without any digital gameplay component lie outside this assessment.

Segmentation Overview

- By Monetisation Model

- Advertising-Supported

- In-App Purchase (Virtual Goods/Boosters)

- Paid-App Purchase (Premium)

- Subscription/Season-Pass

- By Platform

- Mobile (Smartphone)

- Tablet

- PC / Browser

- Console and Smart-TV

- By Game Genre

- Strategy and Abstract (Chess, Go, Xiangqi)

- Card and Dice (Uno, Yahtzee, Poker)

- Family and Classic (Monopoly, Scrabble, Ludo)

- Puzzle and Trivia

- RPG and Adventure Board Conversions

- By Player Mode

- Multiplayer (Real-time/Turn-based)

- PvP

- Co-op/Team-play

- Single-Player (AI)

- Multiplayer (Real-time/Turn-based)

- By Geography

- North America

- United States

- Canada

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Rest of Asia-Pacific

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Kenya

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed mobile publishers, independent designers, ad-tech vendors, and community moderators across North America, Europe, and fast-growing Asia Pacific hubs. These conversations clarified lifetime value assumptions, regional ARPU spreads, and typical MAU-to-payer conversion ratios, enabling us to fine-tune preliminary desk findings.

Desk Research

We start by pooling publicly available datasets from authorities such as the UN Broadband Commission, ITU, and national telecom regulators for internet and smartphone penetration, which anchor the addressable user base. Trade bodies, International Mobile Gaming Association, Entertainment Software Association, and the German Games Industry Association, supply yearly download and revenue snapshots. Financial filings of key publishers, app-store rankings, and ad-network CPM trackers fill pricing and monetization gaps. Paid repositories like D&B Hoovers and Dow Jones Factiva help our analysts validate company level scale and cross-check news on licensing deals. This list is illustrative; several additional sources inform data verification and narrative context.

Market-Sizing & Forecasting

We deploy a top-down device penetration build, translating active smart-device counts into a playable population and then applying observed gamer participation and payer ratios. Results are sense-checked through selective bottom-up roll-ups of leading platform revenues and sampled average selling price multiplied by volume data. Key variables like monthly active users, in-app purchase ARPU, paid-ad fill rates, smartphone penetration, and average session duration feed a multivariate regression model; this shapes our 2025-2030 trajectory. Where platform disclosures are partial, gaps are prorated by regional download shares before being validated against expert feedback.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated variance flags, senior analyst reconciliation, and final sign-off. The model refreshes each year, with off-cycle updates triggered by material events such as policy shifts in major app stores. A fresh data sweep is undertaken before every client delivery.

Why Mordor's Online Board Games Baseline Earns Trust

Published figures often diverge because firms vary in scope, data freshness, and revenue attribution choices. Ad inventory inclusion, currency conversion timing, and whether hybrid physical-digital sales are counted can swing totals noticeably.

Key gap drivers include: some studies lump paid offline boxed sets with digital revenue; others extrapolate global totals from limited app-store panels; refresh cycles longer than two years miss rapid MAU swings when app-store privacy rules change. Our disciplined segmentation, annual refresh, and dual-source payer ratios keep estimates grounded.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.27 B (2025) | Mordor Intelligence | - |

| USD 2.19 B (2024) | Regional Consultancy A | Relies on survey panels, limited app-store coverage |

| USD 13.6 B (2023) | Global Consultancy B | Aggregates broader digital board and card games, counts physical-digital hybrids |

| USD 2.30 B (2024) | Trade Journal C | Uses publisher press releases without payer conversion validation |

In summary, the disciplined scoping and recurring updates that underpin Mordor's figures give decision-makers a balanced, transparent baseline that traces directly to measurable user activity and monetization levers.

Key Questions Answered in the Report

How fast will revenue from subscriptions grow?

Subscription and season-pass plans are on track to rise at a 5.57% CAGR between 2026 and 2031, the quickest pace among monetization models.

Which region is the quickest riser?

The Middle East is projected to log a 5.98% CAGR through 2031, outpacing all other territories due to large-scale sovereign investment.

Why are RPG board conversions surging?

Successful digital adaptations such as Dungeons and Dragons campaigns demonstrate pent-up demand for deep rulesets, leading the genre to a 6.01% CAGR outlook.

Will loot-box bans cut overall spending?

Short-term revenue dips of 15%–25% are expected where random rewards are restricted, but publishers are offsetting with deterministic season passes and cosmetics.

How large is multiplayer’s share today?

Multiplayer modes represented 63.81% of 2025 revenue and hold the strongest growth trajectory at a 6.17% CAGR through 2031.

Page last updated on: