Accelerometer Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 3.77 Billion |

| Market Size (2031) | USD 5.14 Billion |

| Growth Rate (2026 - 2031) | 6.41% CAGR |

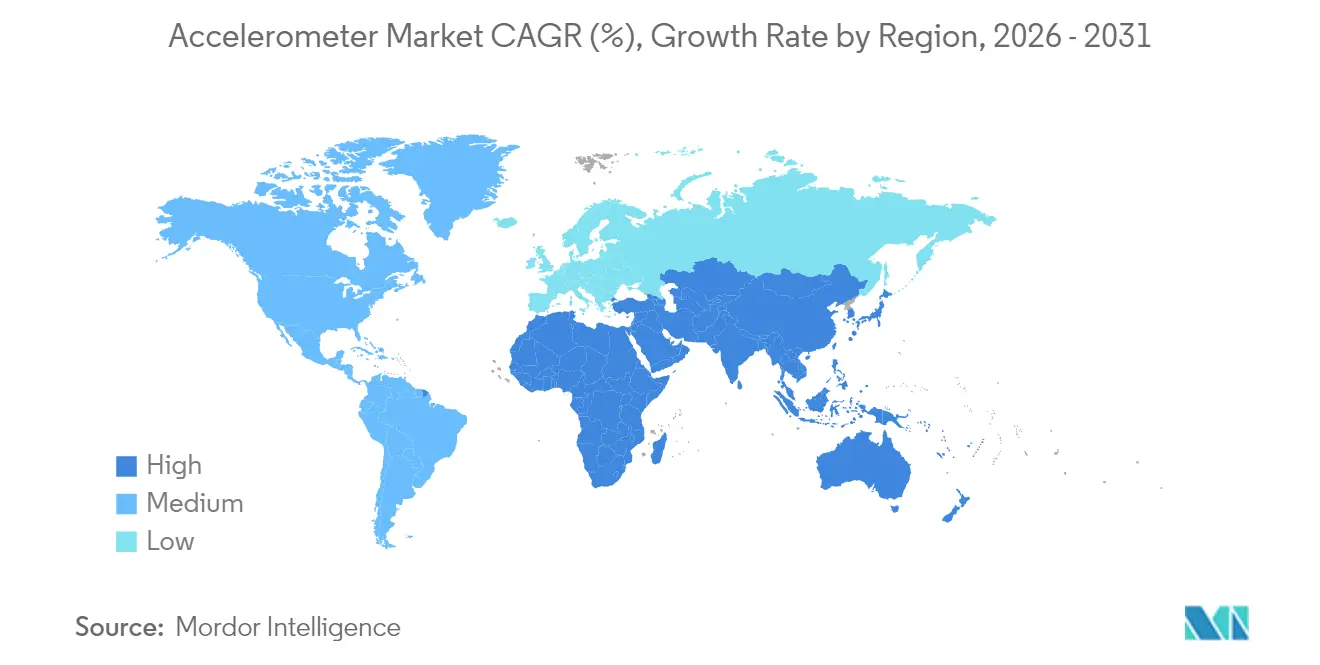

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Accelerometer Market Analysis by Mordor Intelligence

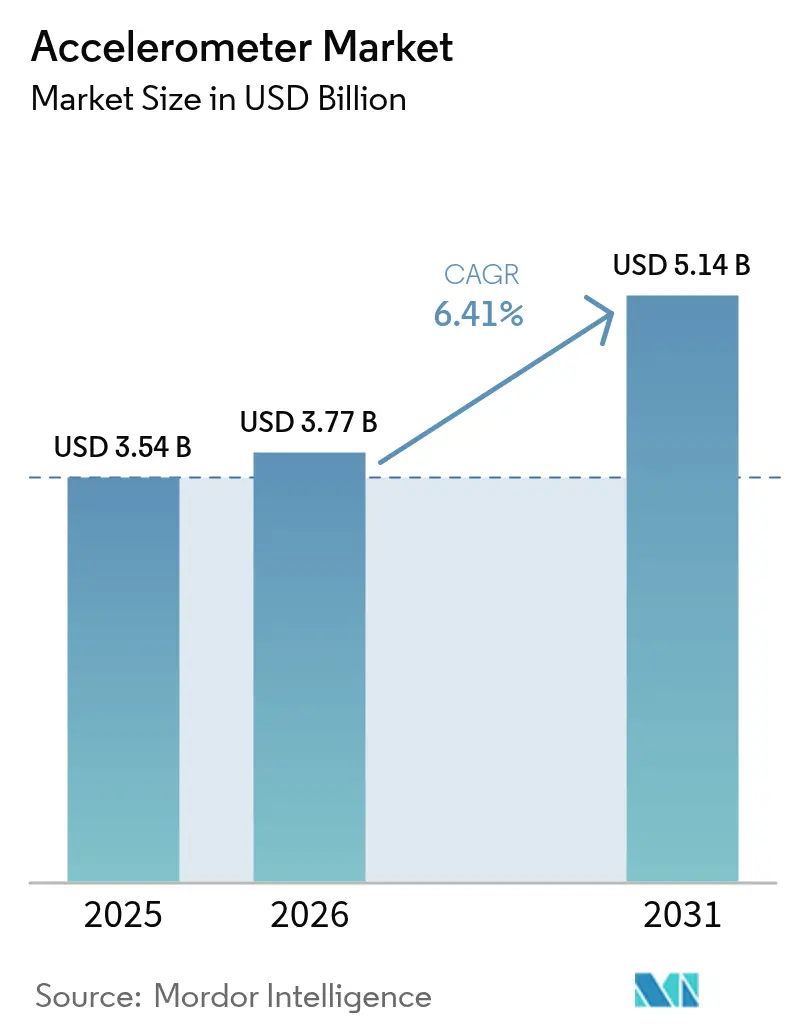

The accelerometer market size is expected to grow from USD 3.54 billion in 2025 to USD 3.77 billion in 2026 and is forecast to reach USD 5.14 billion by 2031 at 6.41% CAGR over 2026-2031. Demand scales with the sensor’s increasingly critical role in consumer devices, automotive safety systems and industrial monitoring. Continuous MEMS miniaturization lowers system cost while enabling integration into space-constrained products, and AI-enhanced on-chip processing now lets accelerometers deliver real-time insights at the edge. Tier-1 automotive suppliers are embedding high-g variants in ADAS sensor-fusion suites, while precision-grade piezoelectric devices sustain differentiated value in aerospace and defense niches. Supply-side risks include lingering 8-inch MEMS wafer constraints and price compression in commoditized consumer segments, but design wins in healthcare wearables and renewable-energy infrastructure keep the overall growth outlook intact.

Key Report Takeaways

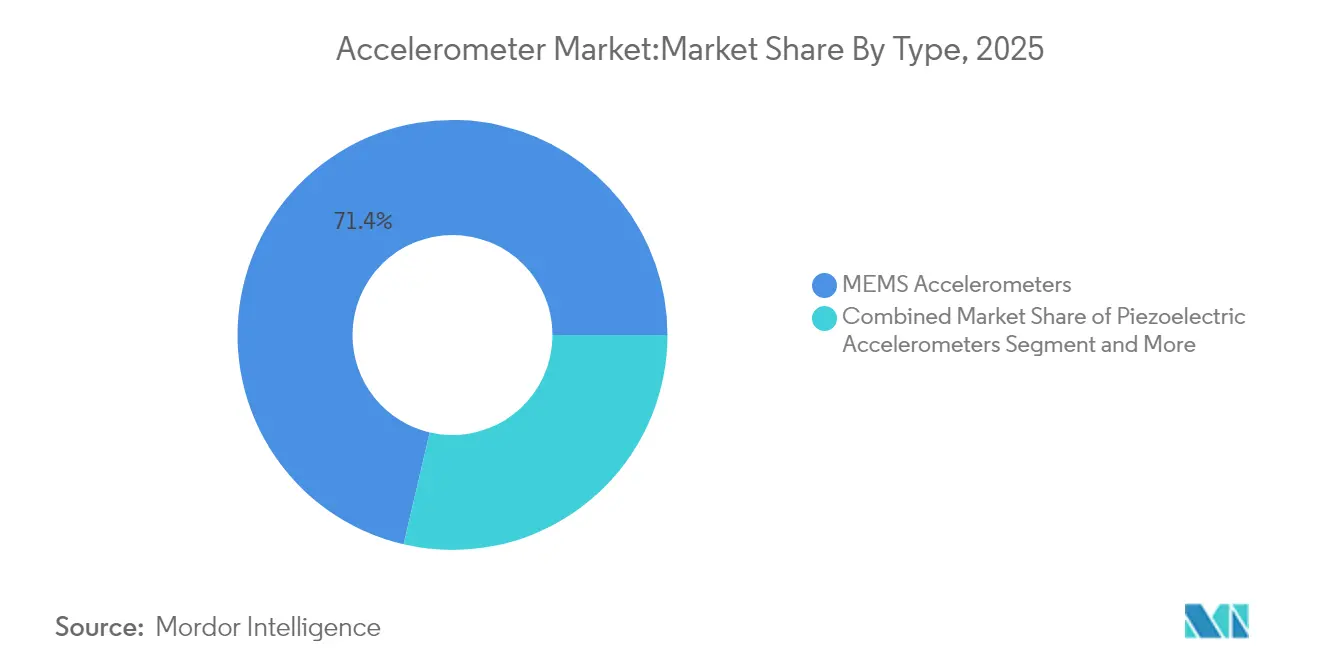

- By product type, MEMS devices held 71.35% of accelerometer market share in 2025, while piezoelectric designs are set to post the highest 7.42% CAGR through 2031.

- By dimension, 3-axis units led with 63.90% revenue share in 2025; 6-axis and higher combo IMUs are projected to expand at 8.05% CAGR to 2031.

- By end user, consumer electronics accounted for 37.20% of the accelerometer market size in 2025, whereas healthcare applications are advancing at an 8.21% CAGR to 2031.

- By performance grade, consumer-grade sensors captured 45.30% of 2025 revenue, yet navigation-grade components are forecast to grow the fastest at 8.46% CAGR.

- By region, Asia-Pacific commanded 46.10% of global revenue in 2025; the Middle East & Africa region is on course for the strongest 8.33% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Accelerometer Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ )% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| MEMS miniaturization and cost reduction | 1.80% | Global with APAC manufacturing concentration | Medium term (2-4 years) |

| Consumer electronics and wearables boom | 1.50% | Global, led by North America and APAC | Short term (≤ 2 years) |

| Automotive ADAS / safety integration | 1.20% | North America & Europe regulatory push, APAC production | Medium term (2-4 years) |

| Industry-4.0 condition monitoring uptake | 0.90% | Europe & North America, expanding to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

MEMS Miniaturization and Cost Reduction

Third-generation MEMS processes now fabricate sub-millimeter proof-mass structures that cut die size and power draw without degrading noise density. Bosch’s miniature 2024 accelerometer series exemplifies how wafer-level chip-scale packaging lowers material cost while sustaining ±2 g to ±16 g dynamic range. [1]Andreas Schmid, “Accelerometers Overview,” Bosch Sensortec, bosch-sensortec.com Larger 300 mm MEMS fabs promise further scale economies, allowing OEMs to allocate tighter bill-of-materials budgets to additional sensing functions. STMicroelectronics’ LIS2DUXS12 integrates a machine-learning core enabling event classification at microwatt levels, removing the need for a companion MCU and shrinking board footprint. [2]Mouser Electronics, “STMicroelectronics LIS2DUXS12 Smart Accelerometer,” Mouser Electronics, mouser.com As foundries migrate to larger wafers, average selling prices decline and unlock latent demand in cost-sensitive IoT nodes, reinforcing the growth loop for the accelerometer market.

Consumer Electronics and Wearables Boom

Smartphones, earbuds and fitness trackers remain volume engines, but 2025 design roadmaps reveal an accelerating pivot toward medical-grade wearables that require sub-30 μg/√Hz noise floors and continuous operation for multi-day battery life. Analog Devices’ ADXL380 targets true-wireless earbuds with dual signal paths so a single sensor supports both active-noise-cancellation feedback and head-gesture recognition. In medical devices, AI-inference embedded in the sensor offloads cloud processing, enabling fall-detection wearables certified under IEC 60601-1 for hospital use. Higher-value clinical applications ease margin pressure and expand the accelerometer market into regulated healthcare channels that favor quality over lowest price.

Automotive ADAS / Safety Integration

Crash detection is now table stakes; 2025 vehicle platforms incorporate multi-axis accelerometer clusters to monitor chassis vibration and infer road profile in real time. Upcoming UNECE R157 phases mandate Level 3 automated-lane keeping in Europe, boosting demand for redundant inertial data streams that enhance camera-radar fusion accuracy. Knowles’ V2S200D exploits body-panel vibrations to localize emergency-vehicle sirens, offering a solid-state alternative to membrane microphones for exterior sound sensing. Tier-1 suppliers are standardizing digital SPI interfaces with self-diagnostic bit-error checks, folding cybersecurity and functional-safety requirements into next-generation accelerometer specifications. These upgrades reinforce the accelerometer market’s position in safety-critical automotive architectures.

Industry-4.0 Condition Monitoring Uptake

Vibration-based predictive maintenance cuts unplanned outage costs that exceed USD 50 billion annually in heavy industry. PCB Piezotronics’ new low-noise triaxial models deliver 60 μg/√Hz performance, enabling early fault detection in gearboxes and turbines. Edge AI routines running on PSoC-6 microcontrollers now process FFT spectra locally, reducing data sent over constrained LPWAN links and containing operating costs. Waste-heat energy-harvesting modules extend sensor lifetimes beyond 10 years, permitting deployment in ATEX-classified zones where battery replacement is impractical. The resulting ROI accelerates adoption, enlarging the industrial slice of the accelerometer market.

Restraints Impact Analysis*

| Restraint | ( ~ )% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price pressure & commoditization | −1.1% | Global, most acute in consumer devices | Short term (≤ 2 years) |

| Accuracy limits vs. piezoelectric high-g | −0.6% | Worldwide aerospace & defense demand | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Pressure and Commoditization

In smartphones the bill-of-materials allotment for inertial sensing shrank by nearly 30% between 2022 and 2024, pushing suppliers to differentiate with embedded ML cores and lower power-suspend modes. Kionix’s KX224 series sells below USD 0.30 at million-piece volumes, underscoring deteriorating average selling prices for legacy parts. Vendors invest in automated calibration to recoup margin; however, factory-trim routines raise capex and erode benefit. The imbalance confines many competitors to break-even PandL positions, tempering near-term revenue expansion for the accelerometer market.

Accuracy Limits vs. Piezoelectric High-G

MEMS capacitive structures struggle to maintain linearity beyond ±200 g, whereas piezoelectric stacks preserve accuracy beyond ±5,000 g, a necessity for missile guidance and spacecraft vibration testing. Defense primes therefore continue sourcing piezoelectric or quartz-flexure assemblies despite higher part cost. Research at the University of Colorado Boulder showed atom-interferometer prototypes that outperform both MEMS and piezoelectric solutions, hinting at a potential technology leap over the next decade. [3]Strain D., “Quantum Navigation Device Measures Acceleration in 3D,” Phys.org, phys.org This ceiling limits MEMS penetration in ultra-high-performance niches and caps pricing power in the premium band of the accelerometer market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: MEMS Dominance Faces Precision Challenges

MEMS devices captured 71.35% accelerometer market share in 2025 owing to unmatched cost-performance balance. Volume manufacturing on 200 mm wafers combined with wafer-level packaging positions MEMS at the heart of smartphones, wearables and automotive ECUs. Piezoelectric units, while representing a smaller base, advance at 7.42% annually as defense and aerospace operators demand sub-1 µg bias stability and radiation tolerance. Piezoresistive and capacitive variants serve niche industrial uses where shock survivability or ultra-low power trumps absolute precision.

MEMS leadership rests on integration advantages. STMicroelectronics’ sensor-hub architecture merges a digital machine-learning core and FIFO buffers directly on the die, trimming external component count. Still, when g-range, temperature extremes or bias stability exceed MEMS limits, designers revert to piezoelectric stacks.

By Dimension: Multi-Axis Integration Drives Complexity

The trend toward full-six-degree-of-freedom measurement places 3-axis accelerometers at 63.90% revenue share in 2025. OEMs prefer unified X-Y-Z readings to support gesture recognition and vibration diagnostics with minimal sensor fusion overhead. Meanwhile, combo IMUs embedding 6-axis or 9-axis capability demonstrate an 8.05% growth trajectory, driven by drones, AR/VR headsets and robotics, where synchronized gyro-accelerometer data simplifies algorithm tuning. Single-axis devices persist in tilt switches and automotive airbag triggers, but share steadily erodes.

Collins Aerospace’s SiIMU02 illustrates the premium end of multi-axis integration, achieving near-fiber-optic gyro accuracy in a palm-sized MEMS assembly. For mid-tier consumer products, suppliers consolidate accelerometer, gyroscope and sometimes magnetometer on a single ASIC with programmable digital filters. This convergence compresses PCB area and bill-of-materials cost, ensuring the accelerometer market maintains momentum as application complexity rises.

By End User: Healthcare Emerges as Growth Engine

Consumer electronics retained 37.20% of global revenue in 2025; yet price erosion caps segmental growth at a mid-single-digit pace. Conversely, healthcare deployments deliver the highest 8.21% CAGR as hospitals adopt motion-analysis wearables for post-operative mobility tracking and sleep-stage monitoring. Inertial Labs’ tactical-grade IMU, originally designed for defense, now appears in robotic-surgery arms, underscoring cross-industry technology migration. Industrial end users embed accelerometers in motors and pumps to flag early vibration anomalies, validating ROI for predictive maintenance installations and elevating sensor ASPs.

Regulatory emphasis on remote patient monitoring and reimbursement for tele-health fosters sustained purchasing of high-accuracy, medically certified devices. Suppliers bundling secure firmware update support and IEC 62304 compliance stand to capture premium margins as clinical use cases scale.

By Performance Grade: Navigation Precision Commands Premium

Consumer grade sensors dominate unit volumes at 45.30% 2025 share, but revenue gravitas shifts toward navigation-grade and above, where ASPs are an order of magnitude higher. The accelerometer market share for navigation-grade products is expected to rise to 18.45% by 2031 as autonomous driving and precision-agriculture fleets specify <50 µg bias stability levels. Inertial Labs delivers 1 deg/hr gyro bias within a MEMS pack, narrowing a gap traditionally held by fiber-optic gyros. Space-grade parts remain a specialist pocket: Northrop Grumman’s LR-500 QMG IMU targets small-satellite constellations with ±0.05 deg/hr class drift, but quantities remain limited.

Tier-2 automakers gradually migrate from consumer to industrial-grade accelerometers as over-the-air software updates require tighter performance margins across the vehicle lifetime. This up-spec trend inflates blended ASP even where unit growth moderates, supporting the accelerometer market’s value expansion.

Geography Analysis

Asia-Pacific controlled 46.10% of global revenue in 2025, anchored by China’s consumer-electronics export base and a dense 8-inch MEMS foundry footprint. Shenzhen-headquartered MEMSIC recorded triple-digit growth after focusing capacitor-type accelerometers on domestic smartphone OEMs. Japan and South Korea contribute high-reliability variants for automotive and industrial sectors, while Taiwan’s pure-play foundries support contract manufacturing. The region’s accelerometer market will expand at a steady 6.08% CAGR, although wafer-capacity constraints and rising labor costs temper upside.

The Middle East and Africa represents the fastest 8.33% CAGR through 2031 as Saudi Arabia’s Vision 2030 stimulus funds local semiconductor initiatives and scales renewable-energy assets requiring turbine vibration monitoring. Wind farms across Egypt and Morocco adopt triaxial accelerometers to meet ISO 10816 predictive-maintenance benchmarks. Regional public-private partnerships with European sensor makers expedite technology transfer, accelerating indigenous production and lifting the local accelerometer market trajectory.

North America holds a strong second position driven by automotive ADAS mandates and an advanced industrial IoT install base. Adoption of Industry-4.0 maintenance strategies across oil and gas, chemicals and metals drives demand for rugged, hazardous-area-rated accelerometers. Europe trails marginally yet enjoys higher average selling prices as OEMs prioritize quality and functional safety. EU funding for Horizon Europe robotics projects further stimulates precision-grade sensor uptake, reinforcing regional participation in the accelerometer market.

Regulatory Landscape

Accelerometers used in vehicles, industrial equipment, and connected wearables increasingly fall under safety, durability, and product-security compliance regimes that affect qualification cost and time-to-market. In Japan, the Japanese Industrial Standards Committee revised JIS C 5400:2026 (July 2026) to require AEC-Q100 Grade 1 vibration durability testing for industrial MEMS accelerometers used across automotive and industrial IoT supply chains, effectively extending automotive-style stress screening deeper into industrial sensing programs.

Trade and market-access rules also influence landed cost and sourcing strategies for MEMS sensors and adjacent semiconductor content. In the United States, a 25% ad valorem tariff on certain semiconductors and derivative products under Section 232 took effect January 15, 2026, making accurate product classification and bill-of-materials structuring more consequential for global shipments of accelerometer-based electronics. For connected devices that embed inertial sensors, national technical regulations can indirectly shape accelerometer demand through device certification gates, such as Indonesia's KEPMEN KOMDIGI No. 569/2025, which became fully effective on January 19, 2026 for 4G LTE and 5G NR devices and added mandatory compliance requirements for specified bands.

Value Chain Analysis

The accelerometer value chain runs from upstream silicon and packaging inputs to sensor design and fabrication, module assembly and calibration, and then distribution via OEM direct supply, tier-1 integrators, and global electronics channels. Upstream dependencies include MEMS wafers, ASICs, packaging substrates, and specialized processes such as wafer-level packaging and deep reactive-ion etching. These inputs support high-volume MEMS production concentrated in China, Taiwan, and South Korea, while higher-precision piezoelectric and servo-accelerometer manufacturing remains more anchored in Germany, Japan, and the United States. Lead times for custom-qualified MEMS sensors and ASICs can extend into 10 to 30 weeks when substrates or fab capacity tighten, and qualification cycles for safety-critical applications (automotive, aerospace, industrial) commonly run 6 to 24 months. This dynamic raises barriers for new entrants and slows supplier substitution.

Downstream, more value is captured through calibration software, embedded intelligence, and application-level integration, rather than discrete component sales alone. Recent partner moves show tighter coupling between inertial sensing providers and robotics or autonomous driving stacks: in April 2026, ASENSING and JOYNEXT partnered to integrate high-precision positioning and attitude measurement with domain controllers for L2+ to L4 autonomous driving, and DAISCH announced cooperation agreements in April 2026 to integrate IMU solutions into intelligent cleaning robots and to collaborate on embodied-AI IMU motion-perception technology. These collaborations reflect accelerometers and IMUs being designed and qualified as part of broader motion-perception subsystems, which in turn shapes specifications, lifecycle support, and sourcing decisions across the chain.

Competitive Landscape

Competition is moderate, with the top five suppliers controlling an estimated 58% of 2024 revenue. Analog Devices, Bosch and STMicroelectronics leverage in-house MEMS fabs and deep system-integration know-how to secure multi-year supply agreements with smartphone and automotive OEMs. Bosch pushes a platform strategy, sharing common ASIC cores across pressure, gyro and accelerometer families to spread RandD spend. STMicroelectronics differentiates via embedded machine-learning cores that shorten customers’ time-to-AI deployment. Analog Devices emphasizes ultra-low noise density and radiation-hardened variants for aerospace orbiters.

Specialists pursue vertical niches. PCB Piezotronics extends piezoelectric lines into differential-output models for aero-engine testing. Inertial Labs packages tactical-grade MEMS IMUs for defense unmanned platforms, capturing share where size-weight-power trump fiber-optic performance. Disruptive contenders in quantum sensing, often university spin-outs, targeting sub-nano-g resolution, threaten long-term incumbent positions though commercial readiness remains distant. Overall, product roadmaps converge on embedded intelligence, cybersecurity hardening and self-calibration—capabilities likely to re-order leadership standings as the accelerometer market matures.

Accelerometer Industry Leaders

Analog Devices Inc.

Robert Bosch GmbH

STMicroelectronics

TDK InvenSense

Honeywell International Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term opportunity is industrial and automotive-adjacent MEMS accelerometers that can pass more stringent durability and qualification screens while retaining small form factor and low power. The July 2026 revision of JIS C 5400:2026 by the Japanese Industrial Standards Committee, which mandates AEC-Q100 Grade 1 vibration testing for industrial MEMS accelerometers, creates a compliance-driven whitespace for suppliers with automotive-style reliability infrastructure and for OEMs seeking standardized, audit-ready sensor qualifications across factories, vehicles, and industrial IoT deployments.

Another opportunity is expanding navigation and autonomy use cases where inertial sensing is sourced as a resilience layer rather than a commodity motion input, particularly in degraded GNSS environments and robotics localization stacks. In June 2026, Safran Electronics & Defense announced the MS500 closed-loop, ITAR-free MEMS accelerometer positioned for high-precision navigation, supporting demand for sovereign and export-friendly inertial components in defense and critical infrastructure programs. On the application side, autonomous mobile robots and automated guided vehicles increasingly rely on sensor fusion (IMU plus vision/LiDAR) for SLAM-based localization, and industrial-grade MEMS accelerometers with high output data rates in compact LGA packages are being positioned for robotics and condition monitoring. This supports higher-value design-ins where calibration stability and edge processing features differentiate suppliers from price-compressed consumer segments.

Recent Industry Developments

- July 2026: Analog Devices announced the release of a new MEMS inertial measurement unit, expanding its inertial sensing lineup for applications needing tightly integrated motion measurement. The launch supports higher-value designs where system designers prefer pre-integrated inertial building blocks over discrete sensors to shorten validation cycles and improve robustness at the edge.

- November 2025: STMicroelectronics released the ISM6HG256X three-in-one motion sensor that combines low-g and high-g accelerometer ranges with a gyroscope for industrial IoT use. By bringing 16g and 256g sensing into one package, STMicroelectronics addressed condition monitoring and shock-event capture with fewer components, which helps OEMs reduce board area and simplify firmware and calibration.

- April 2024: STMicroelectronics introduced the LSM6DSV32X 6-axis inertial module with a 32g accelerometer range and edge-AI oriented features. The module broadened IMU choices for intensive movement analysis in wearables and IoT, reinforcing the trend toward on-sensor intelligence and higher dynamic range in compact inertial platforms.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the global revenues generated from accelerometers sold as components or devices that measure linear acceleration or vibration and output an electrical signal, across major end-use industries and regions.

Scope exclusions: We exclude sensor modules where gyroscopes or magnetometers are the dominant element, since those are tracked under separate motion-sensing categories.

Segmentation Overview

- By Type

- MEMS Accelerometers

- Piezoelectric Accelerometers

- Piezoresistive Accelerometers

- Capacitive Accelerometers

- Thermal and Other Types

- By Dimension

- 1-Axis

- 2-Axis

- 3-Axis

- 6-Axis and Above (Combo IMUs)

- By End User

- Consumer Electronics

- Automotive

- Aerospace and Defense

- Industrial and Manufacturing

- Healthcare and Medical Devices

- Other End Users

- By Performance Grade

- Consumer Grade

- Industrial Grade

- Tactical Grade

- Navigation Grade

- Space Grade

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- APAC

- China

- Japan

- India

- South Korea

- Taiwan

- Southeast Asia

- Rest of APAC

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with building the demand context for accelerometers and the supply context for sensor manufacturing, because each side explains a different piece of the total value. We typically pull macro and electronics-production signals from sources such as the World Bank, OECD datasets, and UN Comtrade for trade flows, which helps confirm shipment direction by region.

To keep assumptions grounded, we also refer to public standards and technical references (including IEEE publications), patent databases to gauge design activity, and public filings and investor decks to understand product mix and the pricing commentary that appears in earnings materials. In parallel, we use paid subscriptions for company financials and intelligence, news and financials, and patent coverage, which helps cross-check coverage gaps when public disclosures are thin. These sources are not exhaustive, and we use other public and paid references as needed to collect, validate, and clarify data points throughout the work.

Primary Interviews and Surveys

Primary work is used to translate desk assumptions into workable sizing inputs, especially around typical selling prices, axis mix shifts, and how design wins convert into volumes over time. We interview and survey stakeholders across component suppliers, module integrators, and downstream buyers, and we keep coverage balanced across APAC, EMEA, and the Americas so regional demand patterns are not generalized.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 12% | APAC: 39% |

| Mid tier: 59% | Functional/Unit leaders: 39% | EMEA: 35% |

| Smaller Players: 16% | Managers: 49% | Americas: 26% |

Market-Sizing & Forecasting

The sizing model uses both top-down and bottom-up logic. First, we reconstruct a top-down demand pool by tying accelerometer use to electronics and vehicle build activity, then applying adoption and content assumptions by device category that were validated through expert calls. Next, we run selective bottom-up checks so the totals are not driven by a single macro series, using sampled ASP times volume math, channel checks on mix, and supplier roll-ups where disclosures allow it.

We keep inputs practical and repeatable, so the model relies on variables such as smartphone and wearable shipments, vehicle production trends (particularly safety and stability feature penetration), industrial automation activity, unit ASP movement by grade, and the split of 1-axis versus multi-axis demand. Where bottom-up checks show gaps (for example, private-company revenue splits), we fill missing pieces using peer benchmarks and then adjust back to the demand pool to keep the final number consistent. Forecasts are developed using scenario analysis, supported by expert consensus on the input variables, and then converted into a single base-case trajectory that aligns with observed shipment cycles and pricing patterns.

Data Validation & Update Cycle

Validation is done in layers so the output does not rely on one data source or one assumption. Analysts compare model totals against independent signals, such as trade direction, end-market shipment growth, and expected ASP bands, and then investigate variances that look unusually high or low before sign-off.

A second review step is applied to both the calculations and the logic, and we re-contact experts when a key input shifts materially or when a reported metric conflicts with field feedback. Reports are refreshed annually, with interim updates when a major event changes pricing, supply, or demand. Before delivery, a final pass is completed to ensure the latest public data and market signals are reflected in the numbers.

Mordor Intelligence's Global Accelerometers Market Market Size Compared With Other Published Estimates

Published market values for accelerometers can appear far apart because firms often use different base years, currency timing, and definitions of what counts as an accelerometer sale versus a broader motion-sensing package. Differences also show up when forecasts assume faster price erosion, or when unit growth is increased based on optimistic adoption curves.

Some published estimates appear to include a wider motion-sensing electronics spend that folds in adjacent sensor packages and related modules, which expands the value pool. In Mordor Intelligence, the sizing is tied to accelerometers as the primary sensing element, and totals are checked back to end-market shipment signals and realistic ASP bands before the value is finalized.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.77 B (2026) | |

| Industry Research Firm A | USD 3.38 B (2025) | Uses an earlier base year and a different forecast window, and the mix appears to lean more toward high-volume consumer use cases, which can understate pricing for industrial and automotive grades. |

| Global Consultancy B | USD 8.65 B (2026) | Likely counts a broader spend around accelerometer-related modules and system-level sensing content, which expands the scope beyond standalone accelerometer revenues and lifts the total market value. |

The spread across the figures is mostly explained by scope breadth and how pricing and mix are handled in the base year. When the market is kept tied to accelerometer revenues and then cross-checked against shipment indicators and plausible ASP ranges, the resulting size is easier to reproduce and simpler to audit year over year.

Key Questions Answered in the Report

What is the current size of the accelerometer market?

The accelerometer market stands at USD 3.77 billion in 2026 and is projected to reach USD 5.14 billion by 2031.

Which accelerometer technology type dominates global revenue?

MEMS accelerometers lead with 71.35% 2025 market share thanks to cost-effective high-volume manufacturing.

Which end-user segment is growing the fastest?

Healthcare applications are expanding at an 8.21% CAGR as medical wearables adopt high-precision motion tracking.

Why are piezoelectric accelerometers still relevant?

They deliver superior accuracy beyond ±1,000 g and excel in aerospace and defense environments where MEMS devices face performance limits.

What geographic region shows the strongest growth outlook?

The Middle East and Africa is forecast to grow at 8.33% CAGR through 2031, supported by semiconductor initiatives and renewable-energy projects.

How are suppliers differentiating in a price-pressured environment?

Leading vendors embed on-sensor machine-learning cores, improve power efficiency and integrate self-diagnostics to sustain margins and win design slots.

Page last updated on: