Wearable Health Sensors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.09 Billion |

| Market Size (2031) | USD 4.16 Billion |

| Growth Rate (2026 - 2031) | 14.78% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wearable Health Sensors Market Analysis by Mordor Intelligence

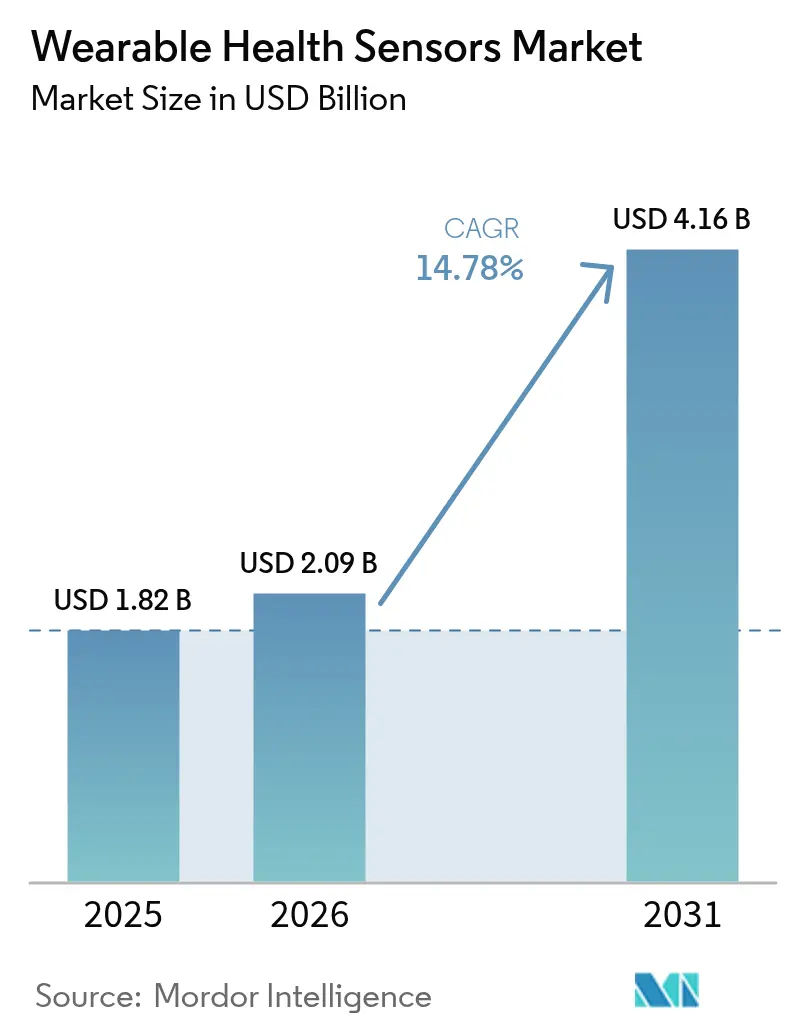

The wearable health sensors market size was valued at USD 1.82 billion in 2025 and estimated to grow from USD 2.09 billion in 2026 to reach USD 4.16 billion by 2031, at a CAGR of 14.78% during the forecast period (2026-2031). Demand is shifting from episodic care toward continuous monitoring as payers and providers see clear cost savings from early intervention. Miniaturized sensors paired with Bluetooth Low Energy, LTE-M, and NB-IoT keep power draw low while moving clinical-grade data into secure cloud platforms. North American adoption benefits from Remote Patient Monitoring (RPM) reimbursements, while cost breakthroughs in printed bio-patches expand use in Europe and Asia. Competitive activity centers on non-invasive glucose detection, skin-tone agnostic optical sensing, and hybrid MEMS-optical stacks that raise accuracy without harming battery life. Partnerships between silicon vendors and device brands are accelerating time-to-market for multi-parameter wearables across consumer, clinical, and industrial settings.

Key Report Takeaways

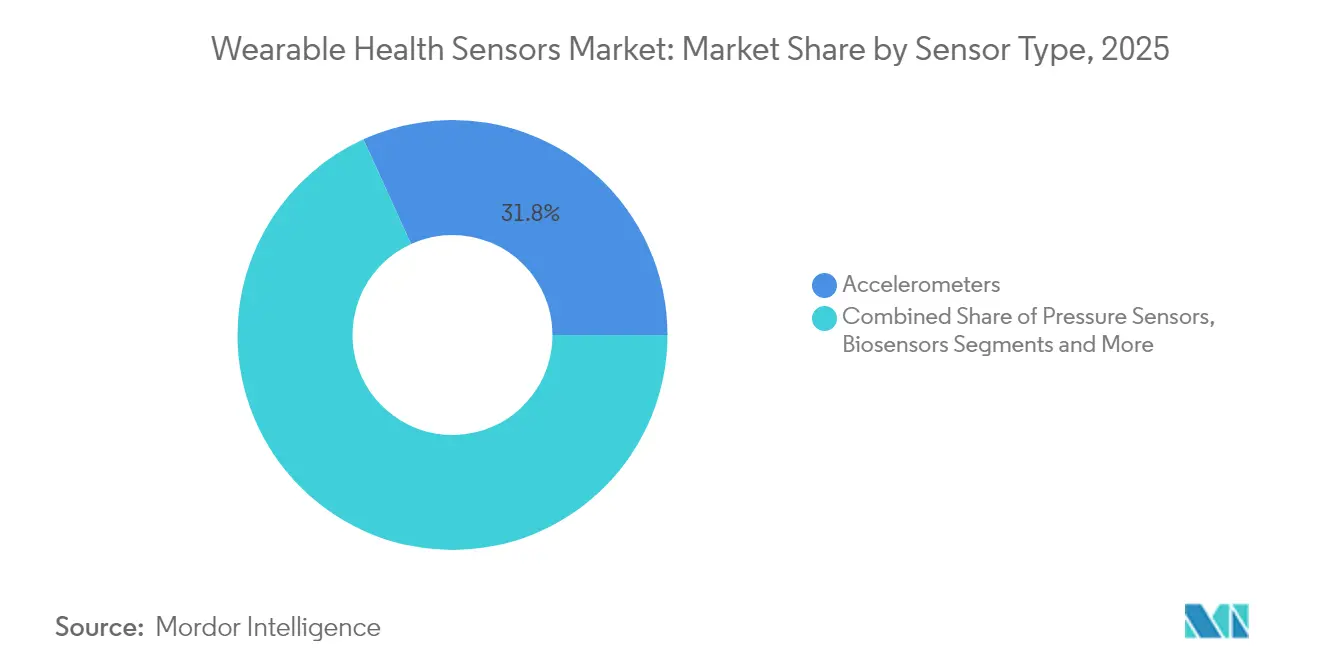

- By sensor type, accelerometers and inertial MEMS led with 31.80% of the wearable health sensors market share in 2025; optical/PPG sensors post the fastest 15.28% CAGR to 2031.

- By body placement, wrist-worn devices held 44.20% revenue share in 2025, while smart textiles expand at 15.05% CAGR through 2031.

- By application, remote patient monitoring and elderly care captured 38.10% of the wearable health sensors market size in 2025 and grow at 14.78% CAGR to 2031.

- By end user, home-healthcare agencies register the highest 25.10% CAGR to 2031, overtaking consumer channels in growth speed.

- By connectivity, BLE continued to dominate with 60.20% share in 2025 as cellular modules post a 14.35% CAGR on autonomy needs.

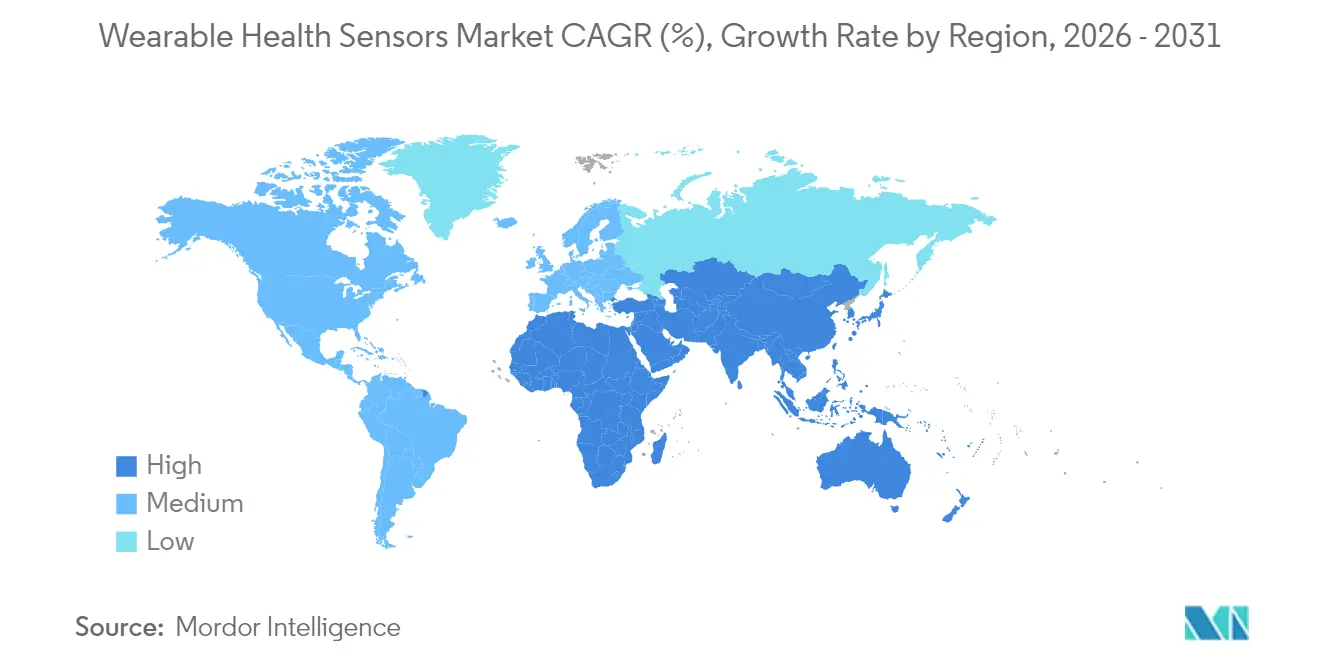

- Regionally, North America accounted for 38.20% of 2025 revenues, whereas Asia-Pacific records the strongest 13.72% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Wearable Health Sensors Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| FDA-Reimbursed Remote Patient Monitoring Codes Accelerating U.S. Prescription-Grade Wearables | +3.5% | North America, with spillover to Europe | Medium term (2-4 years) |

| National Chronic-Disease Screening Mandates in Asia Driving Continuous BP / CGM Kits | +2.8% | Asia-Pacific, particularly China, Japan, and India | Medium term (2-4 years) |

| Scale-up of Printed Flexible Bio-Patches in EU Cutting Unit Cost Below US$1 | +1.9% | Europe, with global adoption following | Long term (≥ 4 years) |

| AI-Enabled Injury-Prevention Wearables Adopted by Elite Sports Leagues | +1.4% | North America, Europe | Short term (≤ 2 years) |

| Worker-Safety Heat-Strain Programs in GCC Oil and Gas Operations | +1.2% | Middle East, with adoption in other high-temperature industrial environments | Medium term (2-4 years) |

| Venture Funding Surge in Non-invasive Glucose Optical Sensors | +2.1% | Global, with initial concentration in North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

FDA-reimbursed Remote Patient Monitoring codes accelerating U.S. prescription-grade wearables

RPM billing simplification that cut mandatory capture from 16 to 12 days per 30-day cycle unlocked a USD 5.1 billion annual device pool. Providers now receive up to USD 1,400 per patient yearly, funding enterprise-grade sensor platforms over retail gadgets. Major health systems formed dedicated RPM teams, expanding procurement pipelines for validated patches and smartwatches that feed EHR dashboards. Hospital readmission rates for chronic patients have fallen 30%, reinforcing payer support.[1]U.S. Department of Health and Human Services, “Billing for Remote Patient Monitoring,” Telehealth.HHS.gov, telehealth.hhs.gov

National chronic-disease screening mandates in Asia driving continuous BP and CGM kits

China earmarked USD 8.7 billion for diabetes and hypertension screening under its latest Five-Year Plan and posts 22.3% annual device demand growth.[2]Vietnam National University, “Hybrid Sensor Integration for Cardiovascular Monitoring,” ScienceDirect, sciencedirect.com Japan mandates yearly cardiovascular checks for citizens older than 40, embedding wearable sensors into universal coverage. These programs create long-run datasets for AI decision support while normalizing at-home diagnostics across the region.

Scale-up of printed flexible bio-patches in the EU cutting unit cost below USD 1

European printed-electronics lines grew capacity 340% since 2023, pushing disposable bio-patch cost below USD 1. Healthcare providers now deploy single-use sensors for post-operative monitoring at prices comparable with traditional dressings. Biodegradable e-textiles lose 48% weight after four months in soil, easing hospital waste concerns.[3]Marzia Dulal, “Sustainable E-Textiles: Biodegradable Wearables Reduce Waste,” TechXplore, techxplore.com

AI-enabled injury-prevention wearables adopted by elite sports leagues

Teams integrate multi-sensor modules with real-time biomechanics analytics to flag fatigue indicators before injuries occur, trimming player downtime by 26%. Premium budgets accelerate R&D that later migrates to consumer and clinical devices, extending the innovation runway for advanced sensor manufacturers.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| EU MDR Class IIa SaMD Post-Market Surveillance Delays | -2.1% | Europe, with global impact for multinational manufacturers | Medium term (2-4 years) |

| Battery Energy-Density Limits in Ultra-Miniature Patches | -1.8% | Global | Long term (≥ 4 years) |

| PPG Accuracy Gaps on Dark Skin Tones—Recalls in Africa/Caribbean | -1.2% | Africa, Caribbean, with global reputational impact | Short term (≤ 2 years) |

| Data-Sovereignty Compliance Costs in Brazil and Colombia | -0.8% | Latin America, particularly Brazil and Colombia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU MDR Class IIa SaMD post-market surveillance delays

Average clearance for analytical wearables rose from 7 to 19 months, lifting compliance expense 280% for startups. Many postpone EU launches or pivot to wellness labeling, slowing regional access to clinical-grade wearables and prompting consolidation as small firms seek scale to absorb regulatory overhead.

Battery energy-density limits in ultra-miniature patches

Commercial batteries plateau near 300 Wh/L, well below the 500 Wh/L needed for week-long multi-parameter monitoring in coin-cell footprints. Designers trade feature breadth for runtime, delaying form-factor migration from wrists to skin-tight patches. Incremental gains of 8-10% per year leave space for disruptive solid-state or on-body energy harvesting solutions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sensor Type: MEMS Dominates While Optics Accelerates

Accelerometers and inertial MEMS sensors command 31.80% of the market share in 2025, establishing themselves as the foundation of the wearable health sensors ecosystem due to their versatility in tracking movement patterns across multiple body locations. These sensors have evolved beyond simple step counting to enable sophisticated gait analysis and fall detection algorithms that are particularly valuable in elderly care applications. Optical/PPG sensors are projected to grow at the fastest rate of 15.28% from 2026-2031, driven by their expanding capabilities beyond heart rate monitoring to include blood oxygen saturation, blood pressure estimation, and even early-stage glucose monitoring applications. Temperature sensors have found renewed importance in continuous fever monitoring systems, while pressure sensors are increasingly deployed in smart footwear for diabetic foot ulcer prevention.

The integration of multiple sensor types within single devices represents a significant market evolution, with hybrid magnetic and optical sensor combinations showing particular promise for improved cardiovascular monitoring. Recent research from Vietnam National University demonstrates that combining these sensor types can overcome the limitations of optical sensors in detecting subtle cardiovascular abnormalities, potentially enabling earlier intervention for conditions like atrial fibrillation. Biosensors (electrochemical) are gaining traction in specialized applications like sweat analysis for hydration monitoring, while position and proximity sensors enable contextual awareness that improves the accuracy of other sensor readings by accounting for body position and movement artifacts.

By Body Placement: Wrist Dominance Challenged by Smart Textiles

Wrist-worn devices maintain their market leadership with 44.20% share in 2025, benefiting from consumer familiarity, established form factors, and the ability to house multiple sensor types in a single accessible location. The strategic advantage of this placement lies in its balance between user acceptance and sensor accuracy, with major players like Apple and Samsung leveraging their smartwatch platforms to introduce increasingly sophisticated health monitoring capabilities. Smart clothing and textiles are experiencing the fastest growth at 15.05% CAGR (2026-2031), as innovations in flexible electronics and conductive materials enable seamless integration of sensors into everyday garments without compromising comfort or washability.

Chest patches and skin-adhesive sensors are gaining prominence in clinical applications, offering continuous monitoring capabilities for patients with chronic conditions while maintaining a discreet profile. The University of British Columbia has developed a low-cost piezo-resistive sensor that can be embedded in textiles to monitor human movements, including heart rates and temperatures, and is washable and durable. Headgear and eyewear placements are finding specialized applications in neurological monitoring and augmented reality health interfaces, while footwear sensors provide unique insights into gait patterns and weight distribution that are particularly valuable for diabetic care and athletic performance analysis. The emerging category of implantable and ingestible sensors represents the frontier of the market, offering unprecedented monitoring precision but facing significant regulatory and user acceptance challenges.

By Application: Remote Monitoring Leads While Mental Health Accelerates

Remote patient monitoring and elderly care applications dominate the market with 38.10% share in 2025, reflecting the growing emphasis on aging-in-place solutions and the management of chronic conditions outside traditional healthcare settings. This application segment has benefited from healthcare system initiatives to reduce hospitalization costs, with remote monitoring demonstrating the ability to reduce hospital readmissions by up to 30% for chronic condition patients. Mental health and stress tracking applications are projected to grow at the fastest rate of 18.25% CAGR (2026-2031), as wearable sensors evolve beyond physical parameters to monitor physiological indicators of psychological states.

Chronic disease management applications, particularly for diabetes and cardiovascular conditions, represent a critical market segment where wearable sensors are increasingly integrated into standard care protocols. Recent innovations in this space include the direct pairing of the Apple Watch with the Dexcom G7 continuous glucose monitor, eliminating the need for smartphone intermediation and enhancing the user experience. Sports and fitness performance applications continue to drive consumer adoption, with elite sports organizations implementing sophisticated monitoring systems that track multiple physiological parameters to optimize training and prevent injuries. Worker safety and environmental exposure monitoring represent an emerging application area, particularly in industries with high heat stress risks, where wearable sensors can provide early warning of dangerous physiological conditions.

By End User: Consumer Dominance Shifting Toward Healthcare

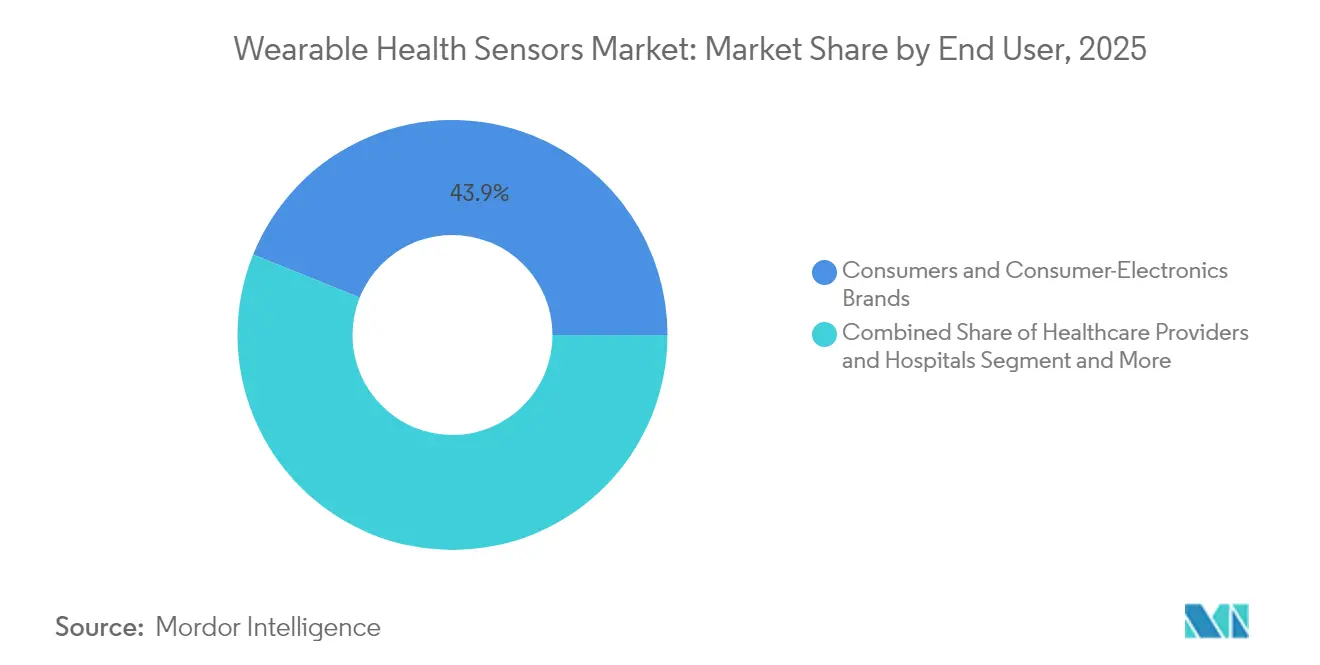

Consumers and consumer electronics brands account for 43.90% of the market share in 2025, reflecting the current dominance of fitness trackers and smartwatches in the wearable health sensors landscape. This segment benefits from established retail channels, consumer familiarity with wearable devices, and the integration of health monitoring features into mainstream consumer electronics products. The strategic significance of this segment extends beyond direct sales, as it serves as the primary channel for introducing new sensor technologies to the broader market before they migrate to specialized healthcare applications.

Home healthcare agencies are experiencing the most rapid growth at 25.10% CAGR (2026-2031), driven by the increasing shift toward home-based care delivery and the integration of remote monitoring into standard care protocols. This growth is supported by healthcare system initiatives to reduce hospitalization costs, with remote monitoring enabling earlier intervention for deteriorating conditions and reducing emergency department visits. A study by the Bipartisan Policy Center found that RPM services can reduce hospital readmissions by 38% for heart failure patients, creating a compelling economic case for adoption by home care providers. Healthcare providers and hospitals are increasingly implementing wearable sensor programs for post-discharge monitoring, while sports teams and fitness centers utilize advanced sensor systems for performance optimization and injury prevention. Military and first responder applications represent a specialized segment where environmental and physiological monitoring capabilities are integrated into existing equipment to enhance operational safety.

By Connectivity Technology: BLE Dominance with Cellular Growth

Bluetooth Low Energy (BLE) maintains its position as the dominant connectivity technology for wearable health sensors, offering an optimal balance between power efficiency and data transmission capabilities for most consumer applications. The strategic advantage of BLE lies in its universal smartphone compatibility, enabling wearable devices to leverage the processing power and connectivity of companion devices rather than incorporating these capabilities directly. Recent advancements in BLE security protocols, particularly LE Secure Connections using Elliptic Curve Diffie-Hellman (ECDH), have addressed previous vulnerabilities that limited adoption in sensitive healthcare applications.

Cellular connectivity, particularly LTE-M and NB-IoT, is gaining traction in applications requiring autonomous operation without smartphone tethering, such as elderly monitoring systems and remote patient care. This growth is supported by declining module costs and power consumption improvements that make cellular viable for a wider range of wearable form factors. Wi-Fi connectivity remains relevant for home-based applications where power constraints are less severe, while NFC/RFID technologies enable novel interaction models and passive sensing applications. Ultra-Wideband (UWB) technology is emerging as a significant innovation in the space, offering precise location tracking capabilities that enhance the contextual awareness of health monitoring systems, particularly in institutional settings where spatial information provides valuable clinical context.

Geography Analysis

North America led the wearable health sensors market with 38.20% revenue share in 2025. Widespread RPM reimbursement, high per-capita health spending, and ecosystem depth spur institutional demand. CMS allows providers to bill roughly USD 1,400 each year per monitored chronic patient, turning devices from consumer novelties into clinical assets. Canada expands telehealth to remote provinces, while Mexico’s social security system pilots diabetes CGM subsidies.

Asia-Pacific records the fastest 13.72% CAGR through 2031. China’s national screening budgets drive bulk procurement of continuous BP cuffs and glucose sensors, while local semiconductor fabricators scale optical chipsets. Japan’s super-aged society integrates fall and arrhythmia patch kits into community clinics. India’s middle class adopts mid-range fitness bands, and government primary-care centers test wearable vitals kiosks. South Korea leverages foundry expertise to supply MEMS and ASIC cores for global brands.

Europe contributes a significant slice yet faces MDR headwinds. Germany and France reimburse digital therapeutics that pass DiGA or PACTe portals, encouraging heart failure and COPD monitoring pilots. Printed-electronics hubs in Germany, the Netherlands, and the UK reduce patch cost, helping hospitals justify disposable sensors. However, MDR post-market rules slow Class IIa software deployments, leading several startups to prioritize United States release first. The Middle East accelerates adoption within oil and gas labor programs, while African uptake depends on addressing PPG accuracy in darker skin populations and connectivity gaps.

Competitive Landscape

Competition blends consumer electronics giants, medical device incumbents, semiconductor suppliers, and focused startups. Apple and Samsung wield platform stickiness and integrate silicon, software, and services, breaking ground on non-invasive glucose spectrometry. Dexcom partners with Apple for direct CGM-watch pairing, sidestepping smartphones and cementing cross-ecosystem utility. TE Connectivity and STMicroelectronics supply ultra-thin pressure and combo IMU sensors that shrink form factors for textile embedding.

Accuracy across all skin tones emerges as a differentiator. Valencell’s recalibrated PPG engines cut errors on Fitzpatrick Types V-VI by 68%, positioning the firm as a preferred module supplier for diversity-conscious payers. Regulatory capability also shapes rivalry; Medtronic’s strong compliance infrastructure speeds global launch of maternity CGM indications, whereas smaller innovators sometimes reclassify as wellness to dodge EU MDR.

Strategic capital flows focus on optical absorption spectroscopy and photothermal approaches for needle-free glucose assays. Venture funding hit USD 1.2 billion in 2024, drawing semiconductor fabs into co-development deals. Patent races in hybrid MEMS-optical stacks intensify, as combined sensor suites deliver redundancy that secures clinical accuracy and supports payer acceptance.

Wearable Health Sensors Industry Leaders

Apple Inc.

Alphabet Inc. (Fitbit)

STMicroelectronics N.V.

Analog Devices Inc.

Texas Instruments Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: The UK National Health Service confirmed reimbursement for prescribed wearable sensors in diabetes and heart failure care pathways, opening a nationwide procurement round.

- March 2025: Oura and Dexcom closed a USD 75 million investment agreement to stream glucose trends into smart rings, unifying metabolic and sleep metrics.

- May 2025: Apple reported milestone progress in optical glucose spectroscopy for the Apple Watch, paving the way for future non-invasive diabetes management.

- April 2025: Samsung secured FDA clearance for sleep-apnea detection on Galaxy Watches, marking the first mass-market smartwatch with the feature.

Global Wearable Health Sensors Market Report Scope

Sensors used for tracking and finding information related to fitness, health, location, etc., that are integrated in a wearable device or technology are called wearable sensors. These sensors are integrated into accessories, wearables, cloth, etc., using wireless devices that allow biological and physiological sensing to measure, monitor, and diagnose blood pressure, heart rate, and other metabolic activities. The studied market is segmented by Types, such as Pressure Sensors, Temperature Sensors, and Position Sensors, among different End-user Industries such as Healthcare, Consumer Electronics, and Sports/Fitness in various geographies.

The market sizes and forecasts are provided in terms of value (USD million) for all the above segments. The impact of COVID-19 on the market and impacted segments are also covered under the scope of the study. Further, the disruption of the factors affecting the market's expansion in the near future has been covered in the study regarding drivers and restraints.

| Pressure Sensors |

| Temperature Sensors |

| Accelerometers / Inertial MEMS |

| Optical / PPG Sensors |

| Biosensors (Electro-chemical) |

| Gyroscopes and Magnetometers |

| Position and Proximity Sensors |

| Others |

| Wrist-wear |

| Headgear and Eyewear |

| Chest Patches and Skin-Adhesive |

| Footwear and In-Shoe |

| Smart Clothing / Textiles |

| Implantable and Ingestible Sensors |

| Vital-Signs Monitoring |

| Chronic-Disease Management (Diabetes, CVD) |

| Sports and Fitness Performance |

| Remote Patient Monitoring and Elderly Care |

| Mental-Health and Stress Tracking |

| Worker Safety and Environmental Exposure |

| Healthcare Providers and Hospitals |

| Consumers and Consumer-Electronics Brands |

| Sports Teams / Fitness Centers |

| Military and First Responders |

| Home-care Agencies |

| Bluetooth / BLE |

| Wi-Fi |

| NFC / RFID |

| Cellular (LTE-M / NB-IoT) |

| Ultra-Wideband (UWB) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Nordics | Sweden |

| Norway | ||

| Denmark | ||

| Finland | ||

| Western Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Eastern Europe | Poland | |

| Russia | ||

| Rest of Eastern Europe | ||

| Middle East | GCC (Saudi Arabia, UAE, Qatar, Kuwait, Bahrain, Oman) | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN (Indonesia, Malaysia, Thailand, Vietnam, Philippines, Singapore) | ||

| Rest of Asia-Pacific | ||

| By Sensor Type | Pressure Sensors | ||

| Temperature Sensors | |||

| Accelerometers / Inertial MEMS | |||

| Optical / PPG Sensors | |||

| Biosensors (Electro-chemical) | |||

| Gyroscopes and Magnetometers | |||

| Position and Proximity Sensors | |||

| Others | |||

| By Body Placement / Form Factor | Wrist-wear | ||

| Headgear and Eyewear | |||

| Chest Patches and Skin-Adhesive | |||

| Footwear and In-Shoe | |||

| Smart Clothing / Textiles | |||

| Implantable and Ingestible Sensors | |||

| By Application | Vital-Signs Monitoring | ||

| Chronic-Disease Management (Diabetes, CVD) | |||

| Sports and Fitness Performance | |||

| Remote Patient Monitoring and Elderly Care | |||

| Mental-Health and Stress Tracking | |||

| Worker Safety and Environmental Exposure | |||

| By End User | Healthcare Providers and Hospitals | ||

| Consumers and Consumer-Electronics Brands | |||

| Sports Teams / Fitness Centers | |||

| Military and First Responders | |||

| Home-care Agencies | |||

| By Connectivity Technology | Bluetooth / BLE | ||

| Wi-Fi | |||

| NFC / RFID | |||

| Cellular (LTE-M / NB-IoT) | |||

| Ultra-Wideband (UWB) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Nordics | Sweden | |

| Norway | |||

| Denmark | |||

| Finland | |||

| Western Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Netherlands | |||

| Eastern Europe | Poland | ||

| Russia | |||

| Rest of Eastern Europe | |||

| Middle East | GCC (Saudi Arabia, UAE, Qatar, Kuwait, Bahrain, Oman) | ||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN (Indonesia, Malaysia, Thailand, Vietnam, Philippines, Singapore) | |||

| Rest of Asia-Pacific | |||

Key Questions Answered in the Report

How large is the wearable health sensors market in 2026 and how fast will it grow?

The market stands at USD 2.09 billion in 2026 and is projected to expand to USD 4.16 billion by 2031, reflecting a 14.78% CAGR.

Which sensor category is growing the fastest?

Optical/PPG sensors grow at a 15.28% CAGR between 2026 and 2031 as algorithms unlock new parameters such as blood pressure and early glucose signals.

Why is Asia-Pacific the fastest-growing region?

Government-funded chronic disease screening, rising healthcare spending, and local semiconductor capacity drive a 13.72% CAGR in Asia-Pacific.

What reimbursement policies support adoption in North America?

U.S. Medicare RPM codes allow billing of roughly USD 1,400 per patient per year for remote monitoring, accelerating prescription-grade wearable rollout.

What technical hurdle limits ultra-miniature patches?

Battery energy density remains near 300 Wh/L, below the 500 Wh/L needed for week-long multi-parameter sensing, constraining smaller form factors.

How are companies addressing accuracy gaps on darker skin tones?

Module suppliers recalibrate optical paths and multi-wavelength LEDs; Valencell’s latest PPG engine cuts error rates by 68% on Fitzpatrick Types V-VI.

Page last updated on: