Acceleration And Yaw Rate Sensors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

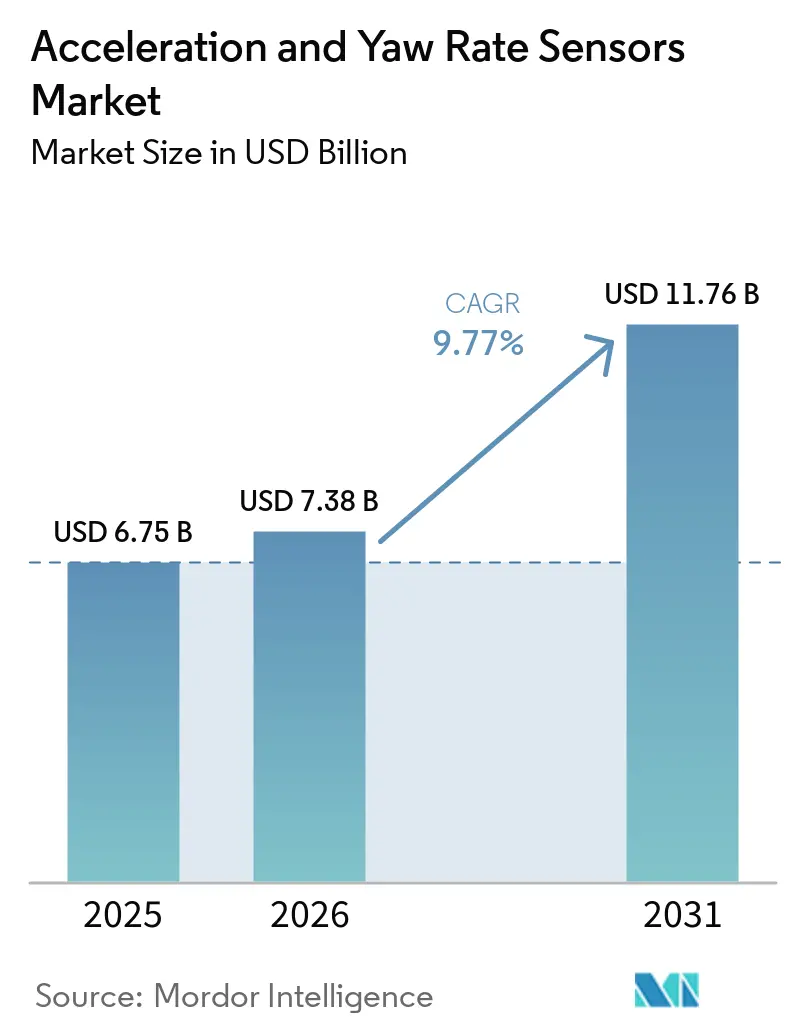

| Market Size (2026) | USD 7.38 Billion |

| Market Size (2031) | USD 11.76 Billion |

| Growth Rate (2026 - 2031) | 9.77% CAGR |

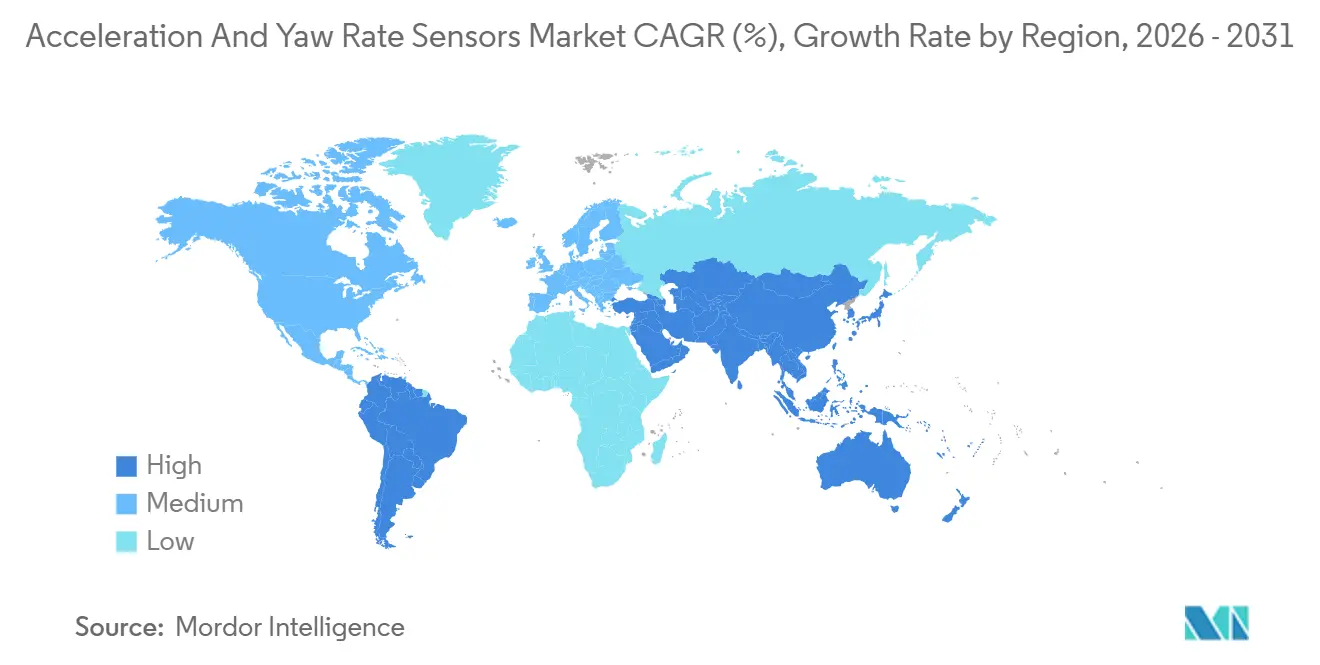

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Acceleration And Yaw Rate Sensors Market Analysis by Mordor Intelligence

The acceleration and yaw rate sensors market size is expected to grow from USD 6.75 billion in 2025 to USD 7.38 billion in 2026 and is forecast to reach USD 11.76 billion by 2031 at 9.77% CAGR over 2026-2031. The acceleration and yaw rate sensors market is still led by automotive demand, but its growth base is widening as industrial robotics, aerospace and defense, and consumer electronics add new use cases for precise inertial sensing. Regulatory changes are raising the minimum sensor content per vehicle platform, which gives suppliers a longer procurement runway as OEMs prepare for future compliance milestones. Demand is also moving toward higher-specification parts because newer braking, lane support, and motion-control functions need better real-time measurement of yaw and lateral acceleration than earlier safety systems required. Competition in the acceleration and yaw rate sensors market is increasingly split between high-volume commodity products that face price pressure and safety-certified, high-precision IMU platforms that still hold pricing strength. This leaves the market with a clear divide, where standard ESC and airbag sensing lines face margin pressure, while navigation-grade and tactical-grade MEMS solutions open new room for backlog growth and supplier differentiation.

Key Report Takeaways

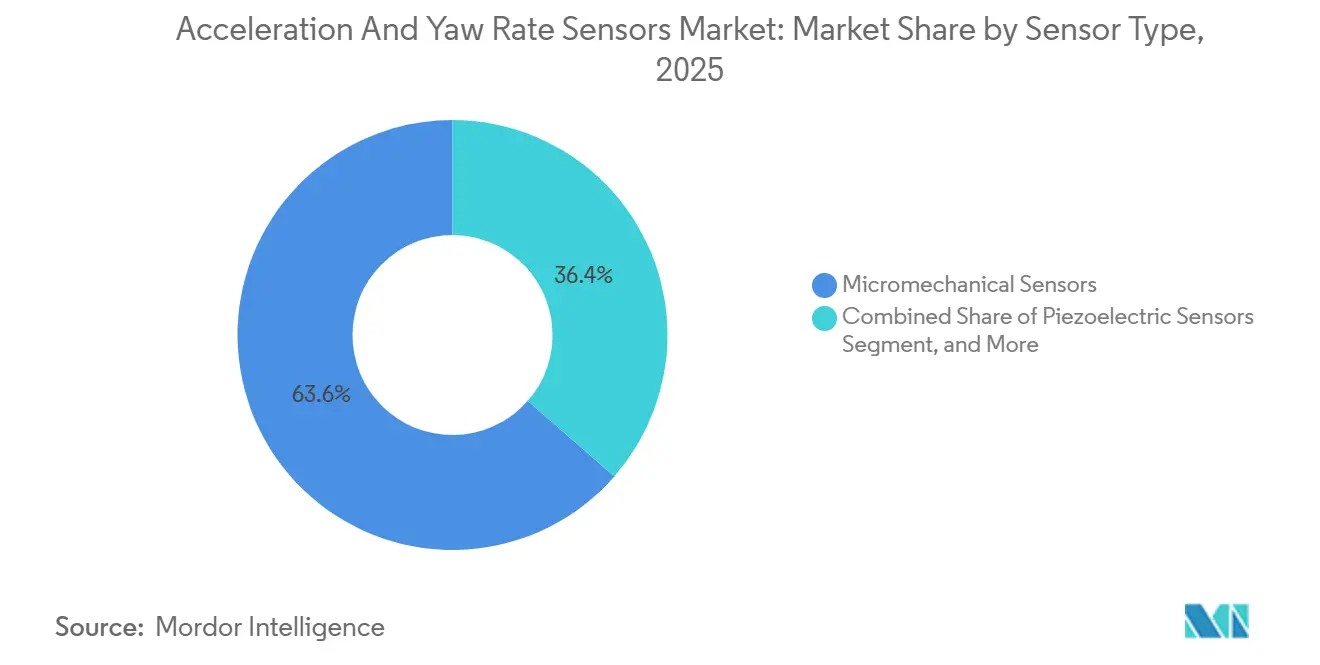

- By sensor type, micromechanical sensors led the acceleration and yaw rate sensors market with 63.56% share in 2025, while piezoelectric sensors are projected to expand at a 10.13% CAGR through 2031.

- By sales channel, OEM fitment held 78.43% of the acceleration and yaw rate sensors market in 2025, while the same channel is also expected to record the fastest growth at a 10.52% CAGR through 2031.

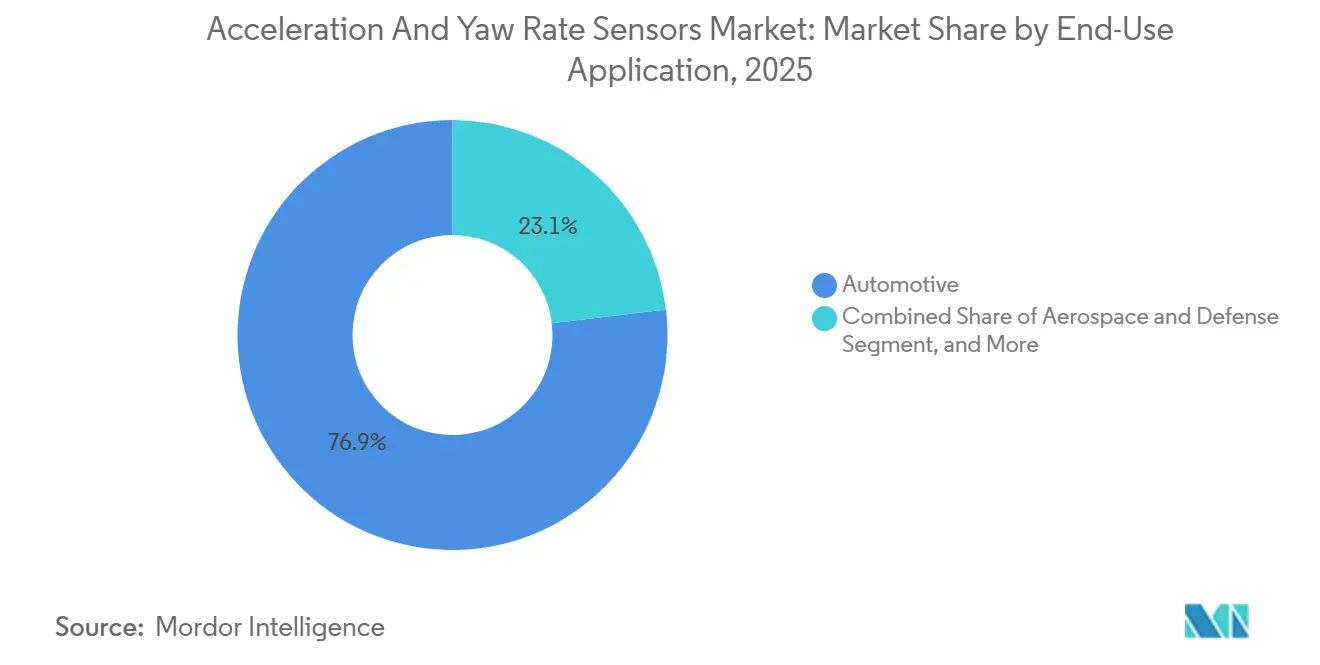

- By end-use application, automotive accounted for 76.85% of the acceleration and yaw rate sensors market in 2025, while industrial and robotics is forecast to advance at a 10.21% CAGR through 2031.

- By geography, North America captured 40.45% of the acceleration and yaw rate sensors market in 2025, while Asia-Pacific is expected to post the highest regional CAGR of 10.41% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Acceleration And Yaw Rate Sensors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Penetration of Electronic Stability Control and ADAS | +2.5% | Global | Short term (≤ 2 years) |

| Higher Sensor Content in Electric and Hybrid Vehicle Ride and Body Control | +1.8% | Global, APAC core, spill-over to North America and EU | Medium term (2-4 years) |

| Adoption of Inertial Sensing in Industrial Robotics and Autonomous Mobile Platforms | +1.4% | APAC core, spill-over to North America and EU | Medium term (2-4 years) |

| Tighter 2026 Safety Assessment Protocols and Functional Safety Requirements | +1.2% | North America and EU | Short term (≤ 2 years) |

| Growing Motion Sensing Content in Software-Defined Vehicle Chassis Architectures | +0.8% | Global | Long term (≥ 4 years) |

| Expansion of Combined IMU Use in GNSS-Denied Vehicle Localization | +0.6% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Penetration of Electronic Stability Control and ADAS

Electronic stability control remains the base application for yaw rate sensors, and its wide fitment across vehicle classes still acts as a dependable volume floor for the acceleration and yaw rate sensors market. U.S. safety rules require ESC across light vehicles and extend related requirements to heavy vehicles, which keeps yaw sensing tied to core vehicle control functions rather than optional features. FMVSS No. 127 added mandatory AEB for light vehicles with a final compliance deadline in September 2029, which creates a multi-year sourcing cycle for sensors that support faster braking decisions.[1]National Highway Traffic Safety Administration, “Federal Motor Vehicle Safety Standards, Automatic Emergency Braking Systems for Light Vehicles - Final Rule,” Federal Register, federalregister.gov That matters because AEB calibration needs yaw rate and lateral acceleration signals with tighter fidelity than older ESC-only layouts. OEMs, therefore, move toward better-performing sensors instead of simply adding more low-cost units. This specification shift raises content value even in mature vehicle categories where unit penetration is already high.

Higher Sensor Content in Electric and Hybrid Vehicle Ride and Body Control

Electric and hybrid platforms add a second demand layer for the acceleration and yaw rate sensors market because ride, body, and torque control functions depend on fast inertial feedback. These vehicles often coordinate torque vectoring and suspension behavior in real time, and that raises the need for IMU update rates of 100Hz or more in production systems. A January 2026 study in Actuators showed that a road-preview semi-active suspension strategy using a body-mounted IMU, wheel acceleration sensors, and wheel-speed sensors maintained strong ride and handling performance under practical sensor limits. That result supports a wider pattern in which OEMs add multi-axis inertial sensing inside EV suspension ECUs instead of removing sensor nodes for cost control. Panasonic Industry’s EWTS5G 6-in-1 device also shows how suppliers are combining 3-axis accelerometers and 3-axis gyroscopes in a compact MEMS package with support up to ASIL D. As EV packaging constraints tighten, suppliers that deliver more sensing functions in smaller footprints gain a clearer path into next-generation platforms.

Adoption of Inertial Sensing in Industrial Robotics and Autonomous Mobile Platforms

Industrial and robotics applications are reshaping the acceleration and yaw rate sensors market because autonomous mobile robots and guided vehicles need inertial feedback between LiDAR and vision updates. IMUs that measure acceleration and yaw rate support SLAM and dead-reckoning functions when external references are momentarily weak or delayed. A 2026 study in PLOS ONE validated a LiDAR-IMU fusion framework for AGVs in dynamic factory settings and showed stable localization through iterative closest-point processing with intermittent IMU aiding. Suppliers are also tailoring products to this use case, and STMicroelectronics’ ISM330BX combines a machine learning core with low-power sensor fusion for demanding industrial environments. The number of IMUs per robot is rising as heavier AMRs and humanoid platforms adopt redundant sensor layouts for fault tolerance. Safety frameworks such as IEC 61508 and the operating needs of collaborative robots support that redundancy trend and add unit demand beyond simple robot fleet growth.

Tighter 2026 Safety Assessment Protocols and Functional Safety Requirements

The 2026 Euro NCAP protocol revision raises the performance bar for the acceleration and yaw rate sensors market because OEMs now face broader and more realistic ADAS testing conditions. Euro NCAP described the update as its largest restructuring since 2009 and expanded evaluation into Safe Driving, Crash Avoidance, Crash Protection, and Post-Crash Safety.[2]Euro NCAP, “Euro NCAP Announces 2026 Protocol Changes To Tackle Modern Driving Risks,” Euro NCAP, euroncap.com The revised Crash Avoidance stage covers new urban scenarios involving powered two-wheelers, cyclists, and pedestrians, which increases the need for better yaw and lateral acceleration measurement under fast response conditions. Euro NCAP also added on-road evaluation across multiple European countries, which shifts attention from closed-track calibration to repeatable real-world behavior. At the same time, Japan’s passenger car AEB requirements and China’s smart-vehicle access framework tighten the same performance direction across major production regions. These converging standards narrow OEM flexibility to use lower-grade inertial sensors and shorten the upgrade cycle between ECU generations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthy Automotive Qualification and ASIL Validation Cycles | -1.3% | Global | Short term (≤ 2 years) |

| Price Pressure From Sensor Commoditization in High-Volume Platforms | -0.9% | Global | Medium term (2-4 years) |

| MEMS and ASIC Capacity Bottlenecks for Automotive-Grade Supply | -0.5% | APAC core, spill-over to North America | Short term (≤ 2 years) |

| Calibration, Cybersecurity, and Redundancy Burdens in Safety-Critical Integration | -0.4% | North America and EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lengthy Automotive Qualification and ASIL Validation Cycles

Automotive-grade devices in the acceleration and yaw rate sensors market must pass both reliability qualification and functional safety review before OEMs accept them into a platform program. This process often runs for 18 to 36 months and requires evidence for each safety mechanism inside the sensor integrated circuit. The burden grows further at ASIL D, where suppliers must show fault detection coverage above 99% across operating temperatures from -40 °C to 125 °C. Bosch Semiconductors positions its SMI980 for ASIL D automotive applications, while TDK InvenSense positions the IAM-20685HP to ISO 26262:2018 ASIL B requirements, and both examples show how much pre-revenue development effort is needed before design-in can begin.[3]Bosch Semiconductors, “SMI980, High Performance Inertial Sensor For ADAS Systems,” Bosch Semiconductors, bosch-semiconductors.com Smaller specialist vendors face an added hurdle when they depend on outside foundries and must match customer design-freeze dates with long validation cycles. That timing mismatch slows the pace at which newer sensing architectures can convert technical readiness into booked revenue.

Price Pressure from Sensor Commoditization in High-Volume Platforms

Price pressure remains a real brake on the acceleration and yaw rate sensors market because mature accelerometers used in airbag and basic ESC functions are now treated as commodity parts in large vehicle programs. Annual cost-down negotiations are common in the automotive supply chain, and mature MEMS lines face steady pricing pressure even when unit volumes rise. As production methods improve, lower-cost suppliers can enter mainstream programs with standard sensing elements that are good enough for less demanding functions. This narrows the revenue pool available to established Western and Japanese suppliers in passenger-car platforms, even while regulatory mandates lift the number of sensors per vehicle. The underlying problem is simple: more sensors in a car do not guarantee more revenue if average selling prices fall faster than content expands. Suppliers are responding by moving toward software-enabled sensing modules with calibrated outputs and embedded fusion algorithms, where differentiation is harder to copy than in a bare MEMS die.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sensor Type: Micromechanical Dominance Offset by Piezoelectric Momentum

Micromechanical sensors held 63.56% of the acceleration and yaw rate sensors market size in 2025, which keeps MEMS as the clear volume leader across automotive safety and control applications. That position rests on long-running wafer-level process gains, batch manufacturing scale, and deep integration into ESC, airbag, and ADAS control units. The product breadth of Bosch Semiconductors, STMicroelectronics, and TDK InvenSense reflects that installed base, with automotive-grade MEMS lines spanning ASIL B to ASIL D and accelerometer ranges from low-g comfort sensing to high-g crash detection.[4]STMicroelectronics, “ISM330BX, 6-Axis IMU With Embedded AI And Sensor Fusion For Industrial Applications,” STMicroelectronics, st.com Capacitive sensors continue to hold a useful position where high resolution and low noise matter more than scale, especially in inertial navigation and structural testing tasks. Other architectures, including resonant MEMS and thermopile-based formats, serve narrower industrial measurement roles inside the acceleration and yaw rate sensors industry.

Piezoelectric sensors are the fastest-growing type in the acceleration and yaw rate sensors market, with a projected 10.13% CAGR from 2026 to 2031. Their main advantage is strong high-frequency vibration performance, an area where capacitive MEMS designs become less effective above the upper end of many standard bandwidth ranges. Kistler’s KiVibe Miniature launch in July 2025 showed how PiezoStar crystal technology and custom ASIC electronics can fit triaxial IEPE sensing into a 6 × 6 mm package that weighs 0.9 g. That product direction fits satellite structural testing, PCB vibration analysis, and lightweight aerospace platforms where both mass and signal quality matter. The ISO 16063 family is increasingly visible in procurement language for this part of the acceleration and yaw rate sensors market, which supports demand for specialized piezoelectric solutions in advanced test environments.

By Sales Channel: OEM Fitment as the Structural Backbone

OEM fitment accounted for 78.43% of the acceleration and yaw rate sensors market share in 2025, which shows how tightly these sensors are embedded inside vehicle electronic architecture and factory-built industrial robot systems. The channel dominates because safety-certified inertial sensing is usually released through formal OEM engineering cycles rather than through open replacement channels. ASIL validation and AEC-Q100 qualification make like-for-like aftermarket substitution difficult when system-level safety integrity must be preserved. That constraint becomes even stronger as software-defined vehicle designs add more inertial sensor nodes to a single platform and require each position to be validated as part of one safety case. For that reason, OEM integration remains the commercial backbone of the acceleration and yaw rate sensors industry.

OEM fitment is also the fastest-growing sales channel in the acceleration and yaw rate sensors market, with a 10.52% CAGR from 2026 to 2031. That unusual overlap between the largest and fastest-growing channel reflects how new safety requirements add sensing content through factory programs instead of aftermarket demand. In robotics and industrial systems, the same channel logic applies when IMUs are built directly into robot joint controllers and AMR navigation modules during platform manufacturing. Vendors such as VectorNav Technologies, Xsens Technologies, and SBG Systems are positioned around this design-in model with compact OEM-focused modules and integrated navigation capabilities. The aftermarket remains relevant in heavy commercial fleets, but it is still more tied to maintenance cycles than to large-scale architecture change across the acceleration and yaw rate sensors industry.

By End-Use Application: Automotive Anchors Revenue While Robotics Accelerates Growth

Automotive represented 76.85% of the acceleration and yaw rate sensors market in 2025, which made it the clear anchor for revenue across passenger cars, light commercial vehicles, heavy commercial vehicles, and off-highway platforms. Passenger cars remain the largest sub-segment by unit volume because ESC is mandatory and ADAS content continues to rise with compliance and rating requirements. Light commercial vehicles are also taking on more sensing content as fleet operators use telematics and lane-support functions to improve route safety and reduce insurance costs. Heavy commercial vehicles must meet ESC requirements that depend on yaw rate and side-slip estimation, which creates a hardware profile that differs from many passenger-car programs. Off-highway vehicles are becoming a more visible use case as agricultural and construction equipment adopt hybrid GNSS-IMU guidance and terrain-adaptive stability control.

Industrial and robotics is the fastest-growing end-use segment in the acceleration and yaw rate sensors market, with a projected 10.21% CAGR through 2031. The International Federation of Robotics reported a new record for global robot installations in 2024, and logistics and warehousing accounted for much of the added deployment base. As SLAM and multi-sensor fusion become standard, redundant IMU nodes are appearing more often in payload-heavy AMRs and humanoid robots, which raises sensor content per platform instead of only per fleet. ISO 3691-4 also keeps pressure on navigation sensor performance for driverless industrial trucks, while aerospace and defense continue to support a steady revenue layer for rugged, high-precision IMUs. Consumer electronics remain smaller within the acceleration and yaw rate sensors industry because mass-market smartphones and wearables source from broader commodity MEMS pools rather than the specialty suppliers emphasized here.

Geography Analysis

North America held 40.45% of the acceleration and yaw rate sensors market share in 2025, supported by dense federal safety mandates and a defense procurement base that values tactical-grade inertial performance. The United States combines ESC requirements, future AEB compliance work, and defense programs that demand high dynamic range sensing, which keeps the regional mix weighted toward premium specifications. VectorNav reinforced that positioning in March 2026 by introducing 90G and 250G accelerometer ranges and 4000°/sec gyroscope capability across its Tactical Series for high-G mission profiles. Canada’s autonomous vehicle testing activity and Mexico’s role in automotive manufacturing add further support to the acceleration and yaw rate sensors market across the region.

Asia-Pacific is the fastest-growing region in the acceleration and yaw rate sensors market, with a 10.41% CAGR from 2026 to 2031. China’s scale in EV production and its smart-vehicle homologation direction are pushing OEMs to source both local and imported inertial sensing solutions for intelligent connected vehicle programs. MEMSIC Semiconductor’s portfolio for ESC, electronic parking brake, and active suspension shows that domestic supply depth is rising alongside vehicle production volume. Japan remains important for precision manufacturing, and Panasonic Industry’s EWTS5G reflects how local suppliers pair compact integration with automotive safety requirements. South Korea, India, and ASEAN are adding incremental demand through tier-1 automotive manufacturing, two-wheeler expansion, commercial vehicle production, and electronics localization.

Europe remains structurally significant in the acceleration and yaw rate sensors market because Germany’s OEM base continues to raise per-vehicle sensing content in response to evolving ADAS evaluation requirements. The United Kingdom, France, Italy, and Spain also support demand through product safety alignment, EV adoption, and rising logistics robot deployment across industrial settings. South America is smaller, but Brazil’s automotive production and Argentina’s agricultural machinery base still create a credible demand floor for inertial sensing adoption. The Middle East and Africa are the earliest-stage regional tier, and initial demand is centered on autonomous inspection and logistics robots tied to Gulf Cooperation Council investment in smart mobility and infrastructure. Compliance frameworks such as IEC 60812 and ISO 26262 are increasingly written into procurement language across Europe and GCC markets, which raises the minimum quality bar for all suppliers.

Competitive Landscape

The acceleration and yaw rate sensors market is fragmented, with precision inertial specialists competing against larger MEMS producers that focus on scale and cost. Silicon Sensing Systems, SBG Systems, VectorNav Technologies, and Xsens Technologies form a visible specialty tier, and they compete through proprietary sensing architectures, calibration depth, and navigation-grade module design. Their approach is to capture value at the module level by combining sensing elements with fusion software, temperature compensation, and GNSS integration instead of relying only on component sales. Safran Colibrys adds another strong position in high-reliability applications, and its MS1000 series shows how aerospace heritage continues to matter in tactical-grade accelerometer supply.

Patent activity and product releases show where the acceleration and yaw rate sensors market is moving at the high-performance end. In March 2026, Kongsberg Discovery and Silicon Sensing presented a north-seeking MEMS gyroscope that reached navigation-grade performance without GNSS or magnetometer aiding, which directly challenges larger and more expensive fiber-optic or ring-laser systems in surveying, defense, and offshore energy applications. The same development highlights a broader substitution path, because tactical-grade MEMS platforms now compete for work that once sat almost entirely with FOG-class hardware. SBG Systems also expanded this part of the market in March 2026 with the Stellar-40 INS, which combined a tactical-grade IMU, GNSS receiver, and sensor fusion software in a compact, rugged enclosure for defense, robotics, and UAV use. VectorNav’s March 2026 high-G product expansion and its Dallas facility increase point to another competitive pattern, suppliers are preparing for higher-volume defense and autonomy programs, rather than staying in purely niche production

A notable white space in the acceleration and yaw rate sensors market sits at the intersection of sensing and cybersecurity, where hardware-level attestation of sensor data still appears underdeveloped. That gap matters more as ISO 21434 and IEC 62443 expectations spread through automotive and industrial integration programs, and customers ask for trusted data paths rather than only accurate measurements. Emerging Chinese vendors focused on AMRs are also entering the industrial IMU segment with cost-competitive designs, which increases pressure on incumbent Western and Japanese suppliers in the mid-price tier. The result is a two-track market where commodity lines face compression, while suppliers that combine functional safety, fusion software, and compact packaging retain stronger negotiating leverage.

Acceleration And Yaw Rate Sensors Industry Leaders

ACEINNA Inc.

Advanced Navigation Pty Ltd.

ASC GmbH

CTS Corporation

DIS Sensors B.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: SBG Systems unveiled the Stellar-40 INS, a modular and scalable inertial navigation system integrating a tactical-grade IMU, GNSS receiver, and advanced sensor fusion algorithms within a compact rugged enclosure. Commercial availability is expected in June 2026. The system implements a three-level vibration mitigation approach, sensor-level isolation, resonance-free enclosure, and structural isolation, and supports dead-reckoning continuity in GNSS-denied environments, positioning SBG Systems to compete for defense, robotics, and UAV navigation contracts that previously required larger FOG-based systems.

- March 2026: Kongsberg Discovery AS and Silicon Sensing Systems Ltd. unveiled a tactical-grade north-seeking MEMS gyroscope, achieving navigation-grade angular performance from Silicon Sensing's SGH03 vibrating-ring MEMS architecture. The solid-state unit operates without GNSS or magnetometer aiding, meeting size, weight, power, and cost constraints for unmanned aerial, surface, and subsea systems. The collaboration was initiated via a strategic agreement in June 2025 and reached its milestone target within a nine-month development cycle.

- March 2026: VectorNav Technologies introduced 90G and 250G accelerometer ranges and 4000°/sec gyroscope capability across its VN-110 IMU and VN-210/VN-310 INS product families, targeting defense contractors operating interceptors, missiles, and hypersonic platforms where conventional inertial sensors fail under high-dynamic flight phases. VectorNav simultaneously announced a new 100,000 sq. ft. production facility expansion in Dallas to support high-volume programs.

- February 2026: NXP Semiconductors formally transitioned its MEMS sensor product portfolio, including automotive safety accelerometers such as the NXLS95 and NXLS96 families, to STMicroelectronics, consolidating automotive MEMS sensor supply and signaling a significant shift in the tier-1 supplier landscape.

Global Acceleration And Yaw Rate Sensors Market Report Scope

The Acceleration and Yaw Rate Sensors Market Report is Segmented by Sensor Type (Micromechanical Sensors, Piezoelectric Sensors, Capacitive Sensors, and Other Sensor Types), Sales Channel (OEM Fitment, Aftermarket Replacement), End-Use Application (Automotive (Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Off-Highway Vehicles), Aerospace and Defense, Industrial and Robotics, Consumer Electronics, Other End-Use Applications), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Micromechanical Sensors |

| Piezoelectric Sensors |

| Capacitive Sensors |

| Other Sensor Types |

| OEM Fitment |

| Aftermarket Replacement |

| Automotive | Passenger Cars |

| Light Commercial Vehicles | |

| Heavy Commercial Vehicles | |

| Off-Highway Vehicles | |

| Aerospace and Defense | |

| Industrial and Robotics | |

| Consumer Electronics | |

| Other End-Use Applications |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of the Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Sensor Type | Micromechanical Sensors | ||

| Piezoelectric Sensors | |||

| Capacitive Sensors | |||

| Other Sensor Types | |||

| By Sales Channel | OEM Fitment | ||

| Aftermarket Replacement | |||

| By End-Use Application | Automotive | Passenger Cars | |

| Light Commercial Vehicles | |||

| Heavy Commercial Vehicles | |||

| Off-Highway Vehicles | |||

| Aerospace and Defense | |||

| Industrial and Robotics | |||

| Consumer Electronics | |||

| Other End-Use Applications | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of the Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current and forecast value of the global acceleration and yaw rate sensors sector?

The sector was valued at USD 6.75 billion in 2025 and is expected to reach USD 11.76 billion by 2031, advancing at a 9.77% CAGR over 2026-2031.

Which end-use category contributes the most revenue?

Automotive remains the main revenue base, accounting for 76.85% of total demand in 2025 because ESC, AEB, and broader ADAS functions continue to expand sensor content per vehicle.

Which sensor technology is growing the fastest?

Piezoelectric sensors are projected to record the fastest growth at a 10.13% CAGR through 2031, supported by demand in high-frequency vibration, aerospace testing, and lightweight platforms.

Why is OEM fitment so dominant in this field?

OEM fitment held 78.43% share in 2025 because ASIL validation and AEC-Q100 qualification keep most safety-critical sensor procurement inside formal design-in cycles rather than open aftermarket channels.

Which region is expanding the fastest through 2031?

Asia-Pacific is expected to post the highest regional CAGR at 10.41%, driven by EV production in China, precision manufacturing in Japan, and wider localization of intelligent vehicle programs across the region.

What is changing competition among suppliers?

Competition is separating into commodity MEMS lines that face price pressure and specialist IMU platforms that gain value from safety certification, fusion software, compact packaging, and rising FOG substitution opportunities.

Page last updated on: