High-End Accelerometer Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

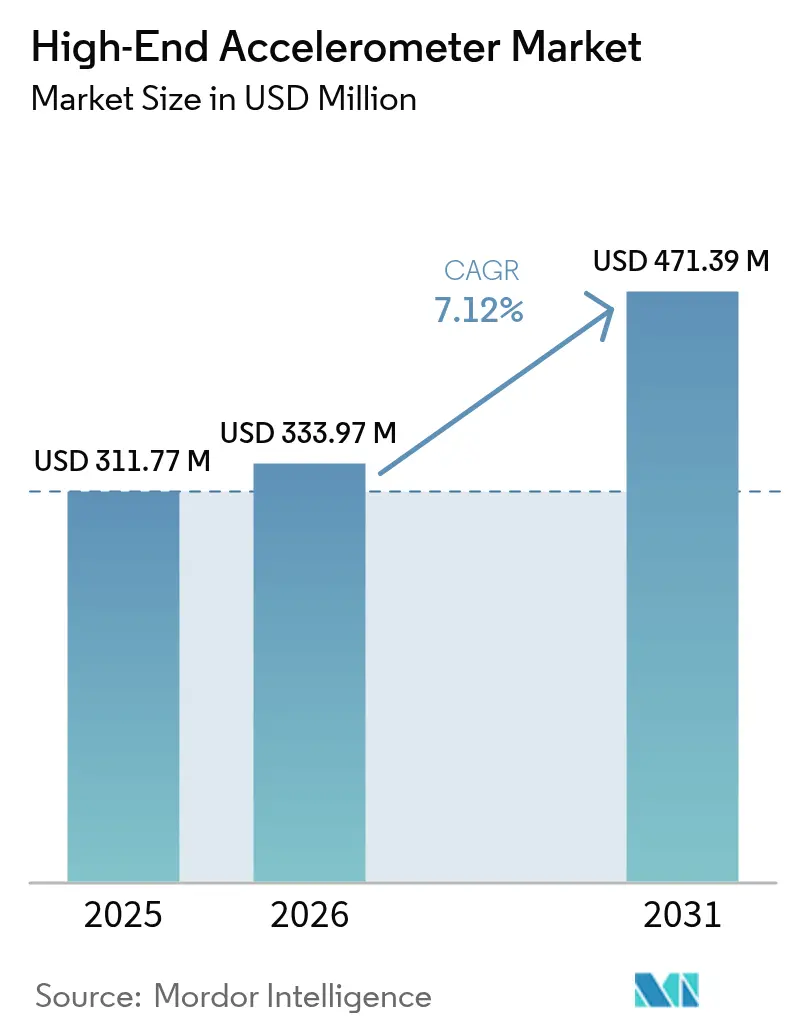

| Market Size (2026) | USD 333.97 Million |

| Market Size (2031) | USD 471.39 Million |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

High-End Accelerometer Market Analysis by Mordor Intelligence

The High-end accelerometer market size was valued at USD 311.77 million in 2025 and estimated to grow from USD 333.97 million in 2026 to reach USD 471.39 million by 2031, at a CAGR of 7.12% during the forecast period (2026-2031). Defense platform upgrades, automotive safety regulations, and the emergence of new low-Earth-orbit (LEO) satellite constellations continue to drive demand for rugged, bias-stable sensors. Lighter, lower-power micro-electro-mechanical systems (MEMS) devices sustain volume leadership, while quartz instruments expand where single-digit micro-g bias stability is mission-critical. Tier-1 suppliers are embedding in-sensor machine-learning blocks to flag vibration anomalies within milliseconds, and the number of shipsets per vehicle is rising as electronic stability control and battery-monitoring functions converge. Export-control frameworks, costly multi-axis calibration, and cybersecurity risks linked to edge AI temper growth, yet do not offset the structural upswing across automotive, defense, and space programs.

Key Report Takeaways

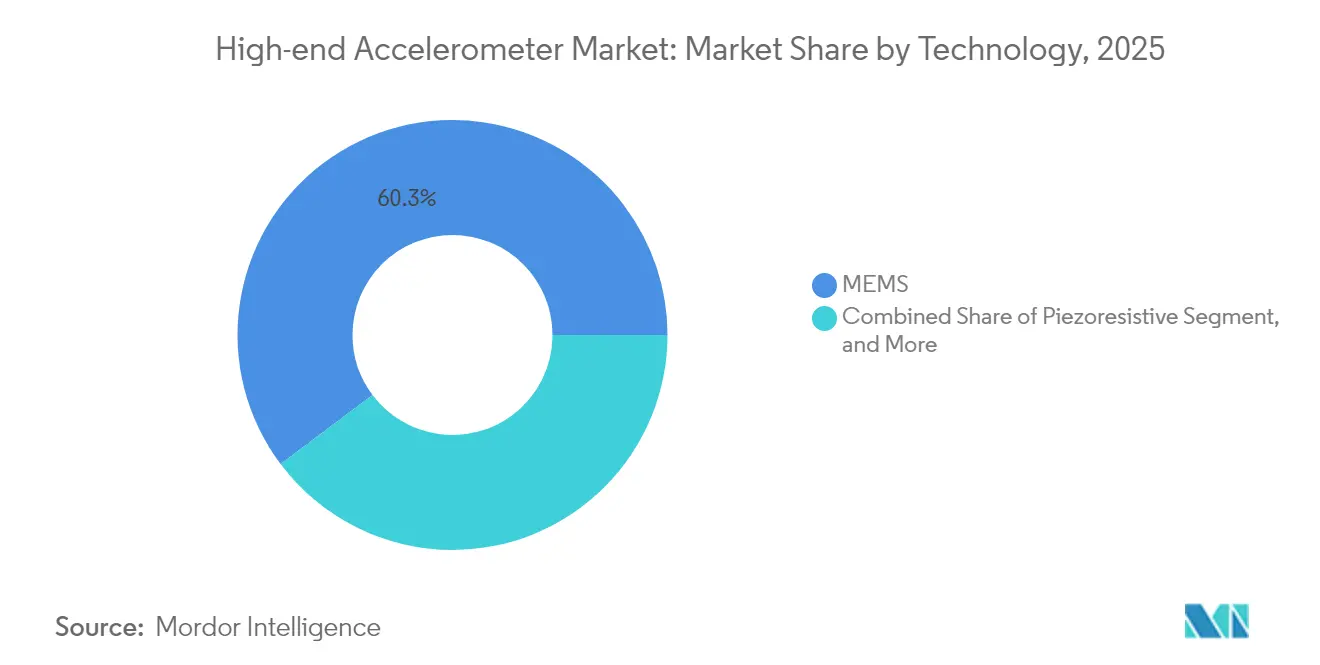

- By technology, MEMS held 60.25% revenue share of the high-end accelerometer market in 2025, while quartz is forecast to grow at a 8.74% CAGR through 2031.

- By axis type, three-axis devices accounted for 60.65% of the 2025 demand in the high-end accelerometer market, whereas six-axis IMU combos are expected to expand at a 8.95% CAGR through 2031.

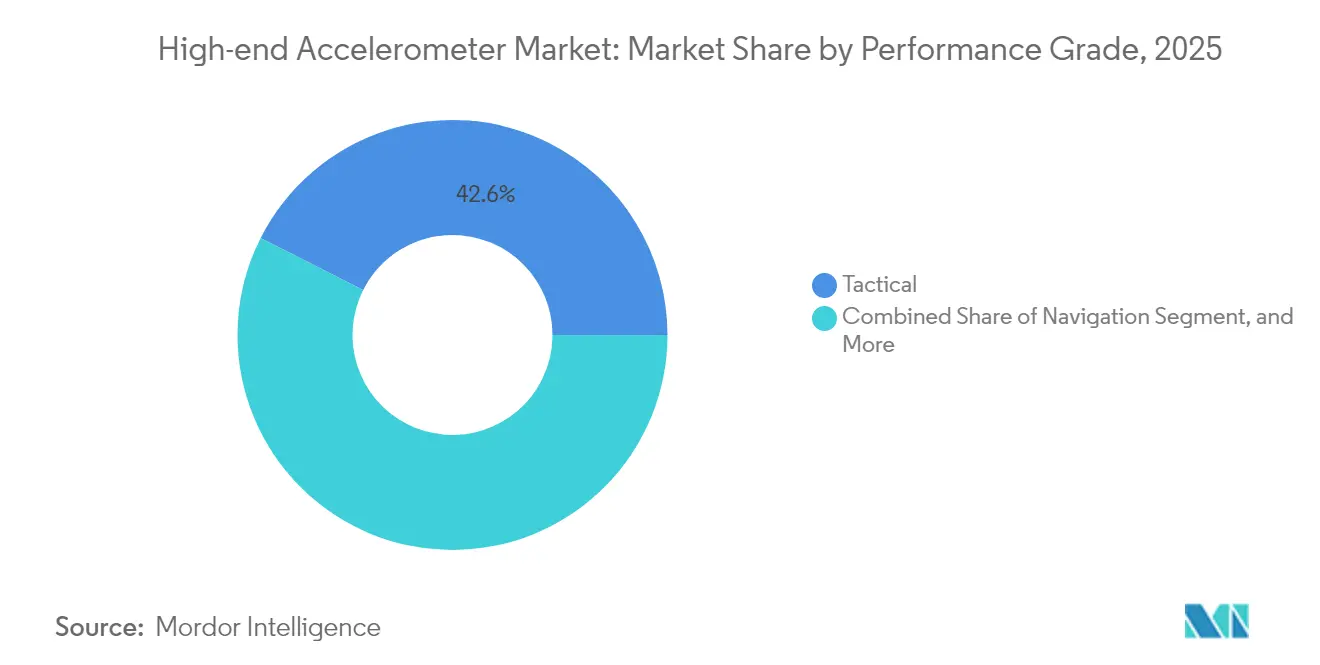

- By performance grade, tactical units captured 42.55% of the 2025 turnover in the high-end accelerometer market, while navigation-grade units are projected to post the fastest 9.02% CAGR.

- By end-use industry, consumer electronics led the high-end accelerometer market in 2025, accounting for 40.45% of the revenue; automotive applications are projected to grow at a 9.55% CAGR.

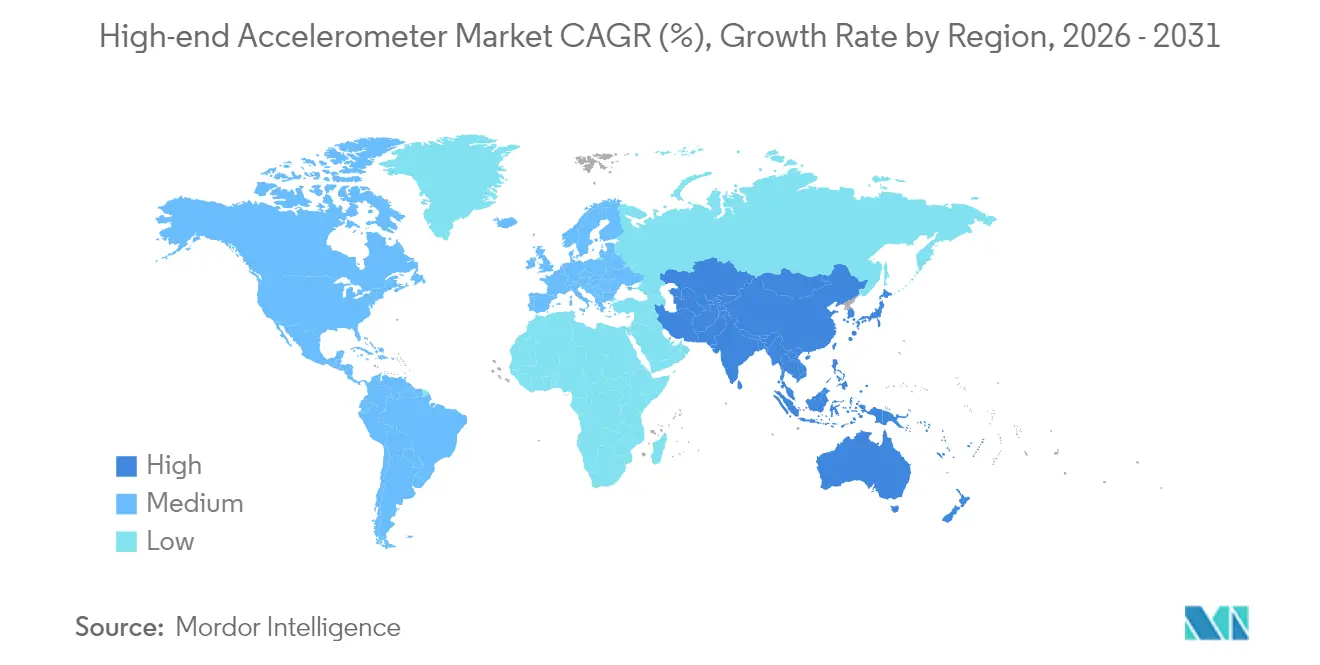

- By geography, North America accounted for 37.80% of the high-end accelerometer market's 2025 sales, while the Asia-Pacific is projected to achieve a 9.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global High-End Accelerometer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising MEMS miniaturization cuts SWaP-C | +1.8% | North America, Asia-Pacific | Medium term (2-4 years) |

| Defense and aerospace modernization budgets | +2.1% | North America, Europe, Middle East | Long term (≥4 years) |

| Automotive ADAS and EV safety mandates | +2.3% | Asia-Pacific core, spillover to Europe and North America | Medium term (2-4 years) |

| Growing demand for predictive-maintenance sensors | +1.2% | Europe and North America industrial hubs | Short term (≤2 years) |

| Quantum-grade bias-stability R&D spillover | +0.6% | North America and Europe research corridors | Long term (≥4 years) |

| LEO-satellite high-G launch requirements | +1.1% | Global, launch activity in U.S., China, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising MEMS Miniaturization Cuts SWaP-C

Areas below 2 mm² and standby currents under 2 µA have unlocked wearable, drone, and battery-monitoring use cases that were previously cost-prohibitive five years ago.[1]Bosch Sensortec, “BMA530 Datasheet,” bosch-sensortec.com Closed-loop sigma-delta cores now deliver 0.1% nonlinearity across ±16 G ranges, rivaling quartz for many mid-grade missions.[2]IEEE Sensors Journal, “Closed-Loop Sigma-Delta MEMS Accelerometers,” ieeexplore.ieee.org The cost per axis in high-volume lines has slipped below USD 0.5; yet, hermetic MEMS parts for tactical roles still command USD 200–500 due to the need for extended burn-in and temperature compensation.

Defense and Aerospace Modernization Budgets

The U.S. Department of Defense increased missile-defense outlays by 12% year over year to USD 33.5 billion in fiscal 2024, securing multi-year demand for inertial subsystems. NATO members reaching the 2% of GDP spending threshold are refreshing artillery fuzes and unmanned aircraft guidance systems. India’s Technology Development Fund set aside INR 10 billion (USD 120 million) to localize high-end accelerometer supply.

Automotive ADAS and EV Safety Mandates

ISO 26262 ASIL-D rules require redundant accelerometers with unlike failure modes, driving sensor counts from two axes per car in 2020 to six or more by 2026. Euro NCAP’s 2025 steering-assist protocol relies on 1 kHz sampling to detect traction loss within 10 ms. China’s draft NEV safety rules would require the addition of rollover detection in 8 million vehicles annually starting from 2026.

Growing Demand for Predictive-Maintenance Sensors

Triaxial arrays flag bearing defects up to six weeks earlier than legacy vibration surveys, cutting downtime that can reach USD 260,000 per hour in semiconductor fabs. Fraunhofer’s energy-harvesting wireless node eliminates the need for battery swaps on remote wind turbine gearboxes. ISO 20816-1 requires a flat frequency response to 10 kHz, favoring piezoelectric stacks in high-speed tool spindles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High calibration and packaging costs | -1.4% | Global, tactical and navigation grades | Medium term (2-4 years) |

| Supply-chain fragility for specialty ASICs | -1.1% | Asia-Pacific foundry nodes | Short term (≤2 years) |

| ITAR/EAR export-license delays | -0.9% | North America and Europe exports | Long term (≥4 years) |

| In-sensor AI cybersecurity risks | -0.5% | Global, critical-infrastructure use | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Calibration and Packaging Costs

Navigation-grade parts require six-position tumble tests across a temperature range of −40 °C to +85 °C, consuming up to 12 hours per unit. Titanium hermetic lids add USD 80–150, yet shield bias drift to within 25 µg over a decade.[3]Analog Devices, “Navigation-Grade IMU Margins,” analog.com The scarcity of ISO/IEC 17025-certified metrologists limits short-term capacity additions.

ITAR/EAR Export-License Delays

Median U.S. approvals stretched to nine months for USML Category VIII accelerometers in fiscal 2024. European dual-use thresholds capture bias stability better than 10 milli-g, inserting 60-day end-user reviews that divert non-allied buyers toward domestic suppliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Quartz Gains in Drift-Sensitive Navigation Roles

Quartz accelerometers are projected to outpace the overall High-end accelerometer market at a 8.74% CAGR during the 2026-2031 period. Their less than 10 µg bias stability keeps submarine and GPS-denied aircraft on course for weeks, supporting fewer than 10 qualified global producers. MEMS maintained a 60.25% High-end accelerometer market share in 2025, driven by consumer and automotive volumes, but it confronts a bias-stability floor near 50 µg due to thermo-mechanical noise. Piezoelectric units dominate vibration monitoring above 10 kHz, while piezoresistive stacks withstand 200 °C downhole environments.

Demand for quartz surged 11% in Honeywell’s QA-3000 line supplying commercial-aircraft reference systems. New closed-loop electronics from Thales reduced wiring by 30% and improved EMI immunity by 15 dB. Emerging autonomous underwater vehicles specify 25 µg drift caps, reinforcing quartz momentum.

By Axis Type: Six-Axis IMU Combos Consolidate Sensor Suites

Three-axis devices led the High-end accelerometer market with a 60.65% share in 2025, but six-axis IMUs are expected to grow faster at a 8.95% CAGR, as automotive Tier-1s consolidate accelerometer–gyroscope packages to reduce harness weight and calibration time. TDK’s ICM-42688 secured design wins on 15 autonomous-vehicle platforms for its 32 kHz synchronous sampling.

Bosch’s BMI323 executes gesture-recognition algorithms internally, reducing the power consumption of always-on wearables by 40%. Two-axis tiltmeter demand persists in construction equipment, trading off the third axis to save 25% of the system cost when roll-pitch data suffice.

By Performance Grade: Navigation-Grade Tracks GPS-Denied Scenarios

Navigation-grade units are expected to expand at a 9.02% CAGR to 2031, outpacing tactical-grade demand, which still represented 42.55% of the High-end accelerometer market in 2025. Sustaining 72-hour missions without GPS and bias stability below 25 µg ensures navigation-grade procurement remains robust in missiles, submarines, and long-endurance UAVs. Strategic-grade sensors with less than10 µg drift remain niche, priced above USD 50,000 per unit, yet underpin NASA’s deep-space SIRU packages.

DARPA’s Micro-PNT program is funding chip-scale atomic clocks and micro-hemispherical gyros that promise to reduce the size of strategic-grade IMUs by 80% within five years.

By End-Use Industry: Automotive Overtakes Consumer on Safety Mandates

Automotive shipments are forecast to grow 9.55% CAGR, overtaking consumer electronics, which held a 40.45% share in 2025. Mandatory electronic stability control and rollover-detection systems lift accelerometer counts to six axes per vehicle by 2026.

Defense and aerospace retain the highest average selling price, albeit only 12% of unit volumes. Industrial machinery installations pay back within six months by preventing downtime, while health-care wearables deploy ultra-low-power MEMS that function for five years on coin cells.

Geography Analysis

North America retained 37.80% of the High-end accelerometer market revenue in 2025, buoyed by USD 1.8 billion in U.S. defense inertial-sensor procurement. Canada earmarked CAD 1.2 billion (USD 880 million) to update CF-18 inertial systems. Mexico’s Guadalajara MEMS cluster expanded 25% in 2024 to support 15.5 million North American vehicle builds.

The Asia-Pacific is set for the fastest 9.05% CAGR through 2031, as China produced 9.5 million EVs in 2024 and is expected to implement mandatory electronic stability control by 2025. Japan’s MEMS Foundry Initiative invested JPY 15 billion (USD 100 million) to lift 8-inch automotive-grade capacity. India attracted USD 450 million under its production-linked incentive scheme for MEMS fabs.

Europe held a 24.00% market share in 2025. German sensor sales reached EUR 3.2 billion (USD 3.4 billion), sustained by mandatory stability and tire-pressure rules. The EU Chips Act allocates EUR 2.5 billion for the expansion of MEMS foundries at STMicroelectronics’ Crolles site. Middle East buyers lengthened delivery cycles to 12 months due to ITAR approvals, nudging Saudi Arabia toward indigenous sourcing.

Regulatory Landscape

High-end accelerometers face a dense compliance stack because they are used in safety-critical automotive systems, dual-use defense and aerospace payloads, and regulated industrial environments. Automotive programs anchor around ISO 26262 (ASIL-focused redundancy and diagnostic coverage), while aerospace deployments commonly require environmental qualification such as RTCA/DO-160 and calibration traceability aligned to NASA metrology guidance (NASA-STD-8739.12A), which supports repeatable multi-axis calibration and documented uncertainty budgets.

Trade and standards updates also shape supplier access and product qualification. China implemented GB/T 45571-2025 in April 2025 to specify technical requirements and test methods for linear accelerometers used across aerospace, aviation, and industrial applications. U.S. export controls and licensing timelines remain a practical constraint for high-performance inertial sensors in defense-relevant categories. For hazardous-area condition monitoring, ATEX/IECEx conformity obligations can add documentation and certification workload alongside performance testing for certain industrial accelerometers.

Value Chain Analysis

The value chain runs from upstream semiconductor and packaging inputs (silicon wafers, specialty ASICs, and hermetic or vacuum packaging materials) through midstream MEMS or quartz device fabrication, to downstream assembly, calibration, and module or IMU integration for automotive, aerospace or defense, and industrial machinery. Automotive-grade qualification cycles of roughly 12-24 months and navigation-grade calibration regimes (including multi-position testing across wide temperature ranges) extend lead times and raise barriers to entry. In turn, metrology capacity constraints increase the importance of ISO/IEC 17025-aligned calibration labs for overall throughput.

On manufacturing, high-grade MEMS wafer capacity stayed tight in 2025, with industry supply-chain discussions citing 85-90% utilization. New capacity build-outs also tend to take 18-24 months, which pushes OEMs and Tier suppliers toward longer-term procurement commitments and tighter coordination with downstream integrators and distributors. Silicon Sensing's expanded distribution arrangement with Althen Sensors and Controls in February 2026 illustrates the emphasis on channel reach and application support for high-spec inertial products. Backend hubs in East Asia remain central for packaging, calibration, and module integration, where turnkey services can shorten program schedules for automotive and industrial customers.

Competitive Landscape

The High-end accelerometer market is moderately fragmented, with the top five suppliers controlling roughly 55% of the 2024 revenue. Analog Devices’ 2024 acquisition of Inertial Sense adds centimeter-level RTK fusion to its IMU stack, illustrating the pivot toward bundled positioning solutions.[4]U.S. Securities and Exchange Commission, “Analog Devices 10-K 2024,” sec.gov Patent activity centers on temperature-compensated storage, with 37% of 2024 USPTO grants focused on inertial bias-drift mitigation.

Niche players, such as Physical Logic and Innalabs, compete on six-month customization cycles, appealing to defense buyers who need rapid form-factor tweaks. Chiplet architectures, which separate analog front ends from digital signal processors, are reducing the cost of tactical-grade IMUs by up to 30%. IEC 62443 cybersecurity certification has emerged as a must-have following the proof-of-concept adversarial vibration attacks that surfaced in 2024.

High-End Accelerometer Industry Leaders

Analog Devices Inc.

Robert Bosch GmbH

Honeywell International Inc.

STMicroelectronics NV

Safran Colibrys SA

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Condition monitoring and predictive maintenance in industrial machinery are a near-term whitespace for high-end accelerometers that combine wide bandwidth with embedded intelligence. In June 2026, STMicroelectronics released the IIS3DWB10IS vibration sensor with an Intelligent Sensor Processing Unit (ISPU 2.0), aimed at industrial vibration with a 10 kHz bandwidth and up to plus/minus 200 g range. The product targets edge inference that reduces reliance on external MCUs and data movement, matching end-user demand for faster anomaly flagging at the sensor node and simpler integration into industrial IoT architectures.

A second opportunity sits in migrating near-navigation-grade MEMS and hardened IMU combinations into autonomous platforms (ground, air, and maritime), where licensing, integration time, and SWaP-C constraints are major gating factors. The shift toward sensors and IMUs that can operate across wider temperature ranges and embed machine-learning cores (for example, STMicroelectronics industrial releases in 2025 with integrated ML capability) supports deployments in harsher environments and battery-powered nodes. At the high end, work tied to space and precision orbital maneuvering continues to reference sub-nano-g sensing research paths, including advanced MEMS architectures and optomechanical concepts, sustaining a pipeline of R&D feeding into premium navigation and science-grade instrument requirements.

Recent Industry Developments

- July 2026: Analog Devices introduced a new MEMS inertial measurement unit targeted at military and rugged applications. The release reinforces ADI's position in higher-assurance inertial platforms where qualification and reliability requirements are more stringent than mainstream automotive and consumer programs. It also supports system suppliers that prefer integrated IMU building blocks over discrete sensor assemblies to shorten integration and test cycles.

- March 2026: Honeywell launched the HGuide i700 inertial measurement unit for unmanned and autonomous platforms, emphasizing commercially available access and reduced export friction for customers. The product positioning addresses a recurring procurement constraint in high-end inertial systems, where licensing and export controls can stretch schedules. It also expands Honeywell's coverage across tactical-to-higher-performance IMU tiers used in drones and robotics.

- January 2026: Bosch Sensortec introduced the BMI5 sensor platform (including BMI560, BMI563, and BMI570) at CES 2026 for premium consumer electronics, with high-volume series production planned to start in Q3 2026. The platform underscores continued performance uplift in volume MEMS, supporting always-on sensing use cases where power and size drive design choices. It also signals manufacturing-scale readiness for higher-spec IMU combinations that can spill into automotive and industrial designs once qualification pathways are completed.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the high-end accelerometer market covers revenues generated from precision accelerometers used to measure acceleration, vibration, shock, and tilt where accuracy, stability, and reliability requirements are stringent across mission and industrial environments.

Scope exclusions: It does not count broader inertial subsystems as a single packaged sale when the accelerometer value cannot be reasonably separated.

Segmentation Overview

- By Technology

- MEMS

- Piezoelectric

- Piezoresistive

- Quartz

- By Axis Type

- One-Axis

- Two-Axis

- Three-Axis

- Six-Axis / IMU Combo

- By Performance Grade

- Industrial

- Tactical

- Navigation

- Strategic

- By End-Use Industry

- Defense and Aerospace

- Automotive

- Industrial Machinery

- Consumer Electronics

- Healthcare

- Other End-Use Industries

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Egypt

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research helped map demand signals and the engineering and regulatory context in which these sensors are bought and qualified. We reviewed public sources such as US Bureau of Labor Statistics (industry output and wage inflation), US Census Bureau trade statistics, Eurostat manufacturing series, and UN Comtrade to understand production patterns and cross-border movement for sensing components.

To keep assumptions anchored, we also used sources such as NASA and ESA public program updates, US DoD budget documents, and SAE and IEEE technical papers that describe performance requirements and test methods that often drive the use of high-grade sensors. Company filings, investor decks, reputable press, and a paid subscription for company financials and news were used to time capacity moves and pricing narratives. This list is illustrative, and many other public documents were cross-checked for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to confirm what buyers consider high-end, how qualification cycles affect shipments, and how pricing typically shifts as volumes scale. We spoke with stakeholders across sensor suppliers, calibration and test ecosystem participants, and procurement and engineering teams from defense, aerospace, industrial machinery, and automotive programs across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 14% | APAC: 37% |

| Mid tier: 54% | Functional/Unit leaders: 29% | EMEA: 37% |

| Smaller Players: 15% | Managers: 57% | Americas: 26% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where aerospace and defense platforms, industrial automation activity, and safety and autonomy feature adoption are used to reconstruct an addressable demand pool for high-grade acceleration sensing. The model is then corroborated with selective bottom-up checks, such as sampled average selling price by performance grade multiplied by estimated shipments, along with channel and tender checks where available, and adjustments are made when the two views do not reconcile.

Inputs that tend to move the numbers include platform build rates and retrofit cycles, navigation and tactical grade qualification timelines, calibration and test spending intensity, export control frictions that impact lead times, and the mix shift between MEMS and quartz or piezoelectric designs. For forecasting, scenario analysis is used so that supply constraints, program timing shifts, and price normalization (as yields improve) can be reflected without forcing a single linear trend. Where company level shipment detail is not visible, gaps are handled with proxy ratios derived from application level demand signals and validated through interviews.

Data Validation & Update Cycle

Validation is done through triangulation across multiple checkpoints, so the modeled value remains consistent with independent signals such as aerospace build schedules, industrial production trends, and defense procurement timing. Outliers are flagged when a regional total moves faster than its linked demand indicators, and then the drivers are reviewed again before sign-off.

A second analyst review is carried out to check arithmetic integrity, unit consistency, and currency conversion timing, followed by a final pass on assumptions that have the biggest impact on the forecast. Reports are refreshed annually, and interim updates are made when material events occur, such as program delays, supply disruptions, or meaningful pricing changes. Before delivery, we recheck recent public updates so clients receive the latest view.

Mordor Intelligence's High End Accelerometer Market Size Compared With Other Published Estimates

Published market sizes for high-end accelerometers often do not match because the underlying definition of what counts as high-end is not consistent, and the included sales channels and end uses can shift the total quickly. Differences also show up when one estimate anchors on a single base year and price point, while another uses a moving price curve and different currency timing.

In this market, the biggest gap drivers are whether multi-sensor IMU bundles are counted at full system value or only the accelerometer portion, how tactical and navigation grade volumes are separated from industrial grade shipments, and whether defense and space program timing is refreshed as new public budgets and launch schedules are released, which is a key reason the 2025 value of USD 311.77 M is positioned as it is by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 311.77 M (2025) | |

| Global Consultancy A | USD 274.40 M (2024) | Uses an earlier base year and a different forecast window, and the page does not clearly state how IMU bundles and calibration related revenue are treated, which can understate the comparable value. |

| Industry Publisher B | USD 285.00 M (2025) | Uses a broader multi-year horizon with limited transparency on performance grade cutoffs, and regional growth assumptions can differ when defense and space program phasing is not refreshed at the same cadence. |

Looking across the three figures, the spread is mainly explained by how tightly the product scope is defined and how consistently pricing and program timing are updated. When IMU system value is not separated from the accelerometer portion, or when high-grade qualification driven demand is blended with general industrial sensors, the total can drift. Our approach keeps the estimate traceable to clear demand indicators and repeatable checks, which makes year to year comparisons easier to defend.

Key Questions Answered in the Report

What CAGR is forecast for the High-end accelerometer market through 2031?

The market is projected to register a 7.12% CAGR from 2026 to 2031.

Which technology segment is expanding the fastest?

Quartz accelerometers are forecast to grow at 8.74% CAGR due to superior bias stability demands.

Why are six-axis IMUs gaining share?

They consolidate accelerometer and gyroscope functions in one package, reducing wiring and calibration cost.

Which region will post the highest growth?

Asia Pacific is expected to expand at 9.05% CAGR, led by China’s EV production boom and regulatory mandates.

How do calibration costs affect price?

Hermetic sealing and multi-temperature tumble testing can exceed 40% of a navigation-grade unit’s bill of materials.

What is driving automotive demand for high-end accelerometers?

ISO 26262 safety rules and rising sensor counts in electronic stability control and battery monitoring are key factors.

Page last updated on: