GitOps And Infrastructure As-a-Code (IaC) Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

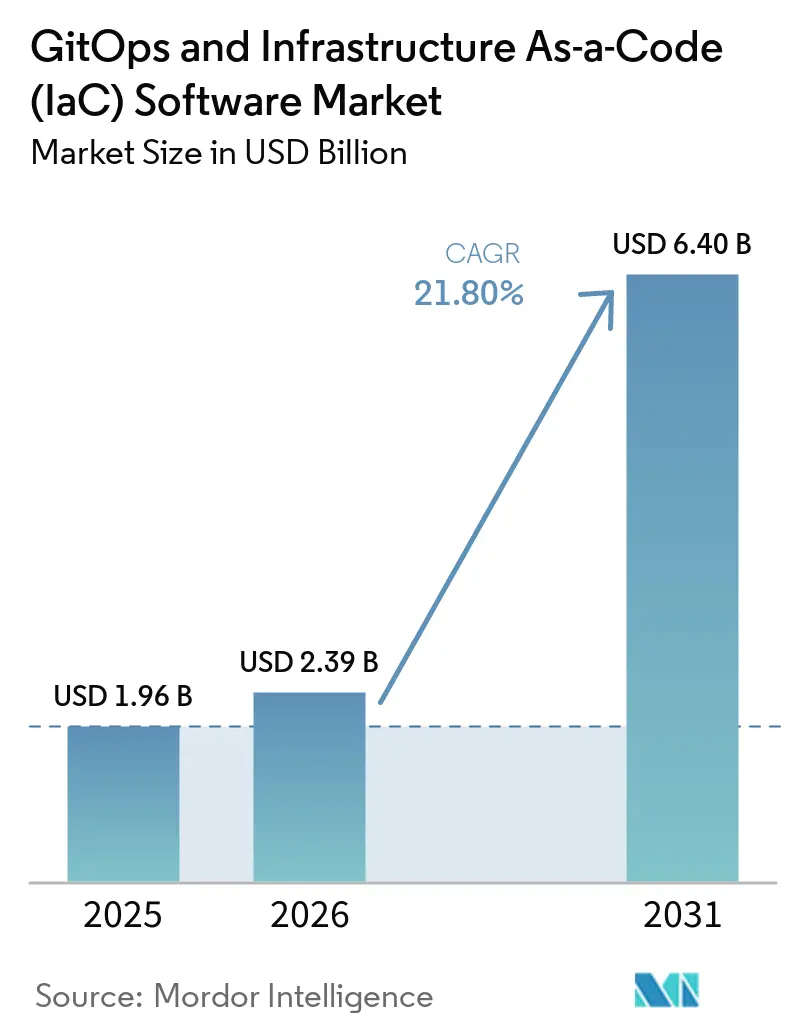

| Market Size (2026) | USD 2.39 Billion |

| Market Size (2031) | USD 6.40 Billion |

| Growth Rate (2026 - 2031) | 21.80% CAGR |

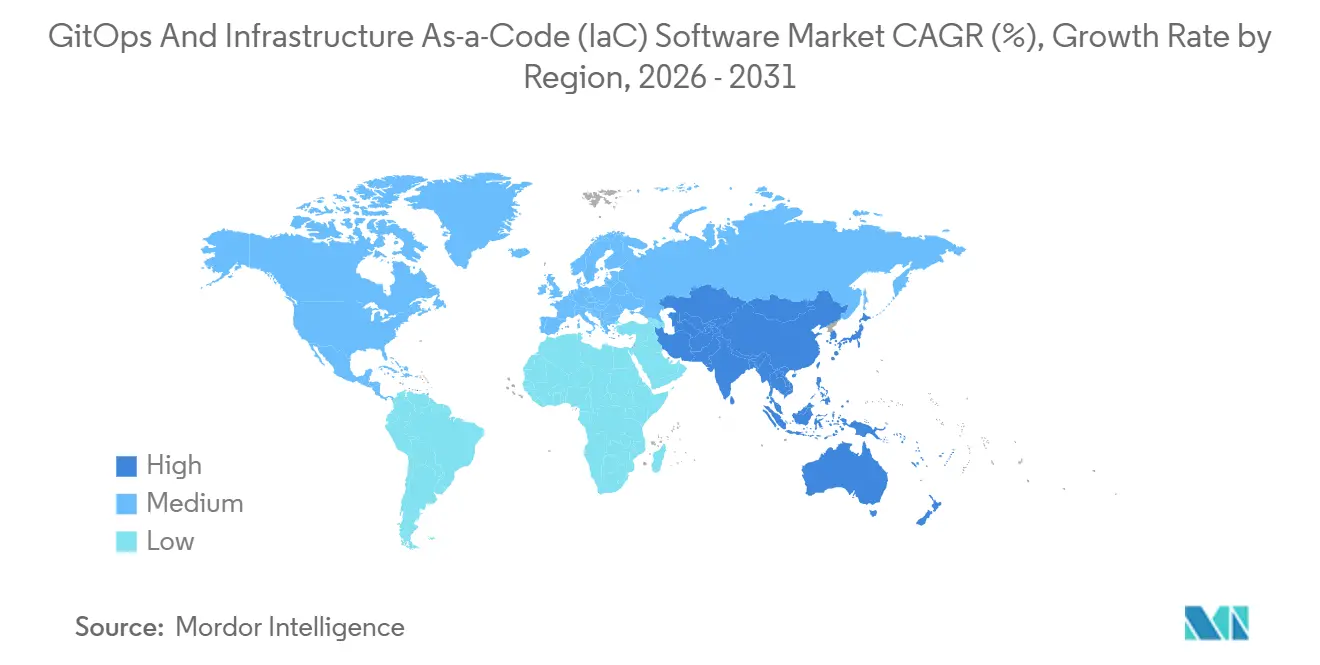

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

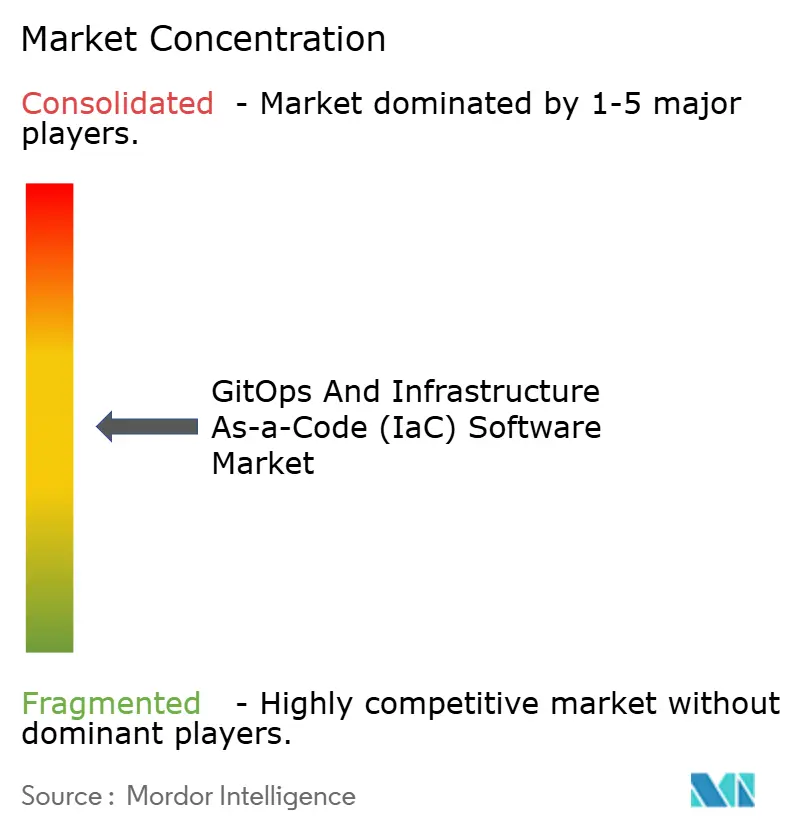

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

GitOps And Infrastructure As-a-Code (IaC) Software Market Analysis by Mordor Intelligence

The GitOps and Infrastructure as Code software market size is expected to increase from USD 1.96 billion in 2025 to USD 2.39 billion in 2026 and reach USD 6.40 billion by 2031, growing at a CAGR of 21.8% over 2026-2031. Demand is rising as enterprises embed declarative infrastructure patterns into production workflows, riding on Kubernetes adoption that already exceeds 82% of cloud-native environments.[1]Cloud Native Computing Foundation, “CNCF End User Survey Finds Argo CD as Majority Adopted GitOps Solution for Kubernetes,” cncf.io Competitive intensity remains high because open-source controllers such as ArgoCD and Flux dominate cluster adoption while commercial backers experiment with monetization models. Managed offerings from hyperscale clouds are accelerating uptake among small and medium enterprises by masking Kubernetes complexity. At the same time, highly-regulated sectors are standardizing on hybrid GitOps deployments to balance compliance with SaaS agility, a pattern reinforced by the first FedRAMP-authorized IaC orchestration platform in 2025.

Key Report Takeaways

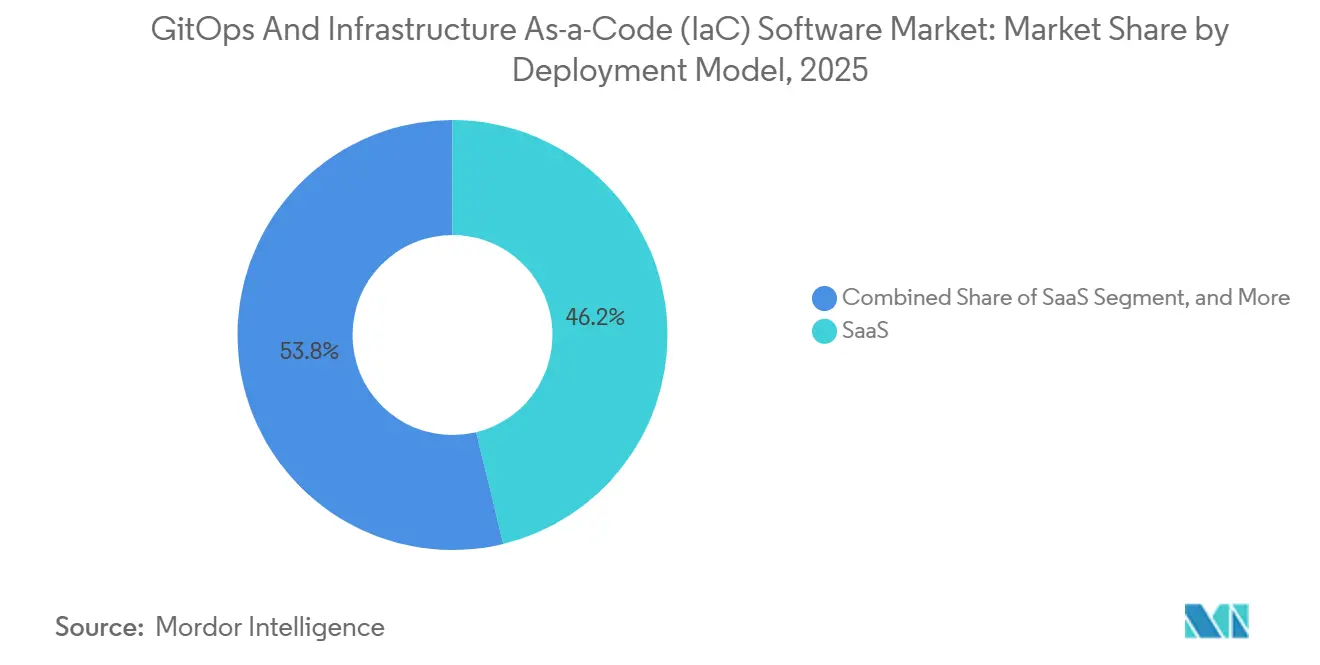

- By deployment model, solutions commanded 46.2% revenue share in 2025 in the itOps and Infrastructure as Code market, while hybrid deployment is projected to expand at a 24.2% CAGR through 2031.

- By organization size, large enterprises held 57.9% of the GitOps and Infrastructure as Code market share in 2025; small and medium enterprises are poised to advance at a 25.4% CAGR to 2031.

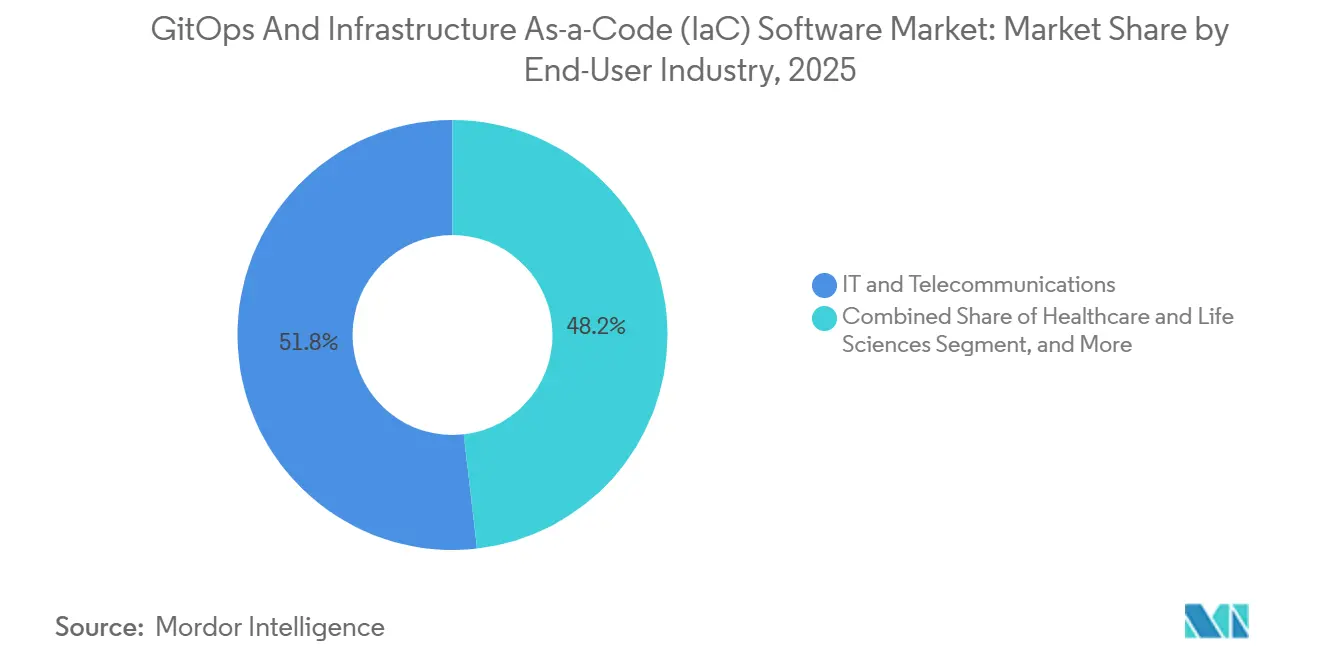

- By end-user industry, IT and telecommunications captured 24.3% share of the GitOps and Infrastructure as Code market size in 2025, whereas healthcare and life sciences are forecast to grow at a 22.6% CAGR.

- By cloud environment, public cloud deployments accounted for 71.8% of the GitOps and Infrastructure as Code market in 2025 revenue and are set to increase at a 23.6% CAGR over 2026-2031.

- By geography, North America led with 33.6% revenue share of the GitOps and Infrastructure as Code market in 2025, while Asia-Pacific is expected to record the fastest 25.8% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global GitOps And Infrastructure As-a-Code (IaC) Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-native adoption by enterprises | +5.2% | Global, strongest in North America and Asia-Pacific | Medium term (2-4 years) |

| Shift toward DevSecOps pipelines | +4.8% | Global, especially regulated industries in North America and Europe | Medium term (2-4 years) |

| Rise of multi-cloud and hybrid-cloud strategies | +4.1% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Growing compliance automation needs in regulated industries | +3.6% | North America and Europe, spillover to Asia-Pacific | Medium term (2-4 years) |

| Open-source community acceleration around GitOps controllers | +2.4% | Global | Long term (≥ 4 years) |

| Demand for immutable infrastructure in edge computing | +1.7% | Asia-Pacific core, manufacturing hubs worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cloud-Native Adoption by Enterprises

Kubernetes reached production adoption in 82% of cloud-native organizations by 2025, anchoring GitOps as the de facto delivery mechanism for containerized workloads. Financial institutions exemplify this shift: Morgan Stanley runs Flux across more than 500 clusters, embedding GitOps directly into core trading infrastructure. In telecommunications, NTT DOCOMO cut 5G core build time by 80% by pairing GitOps with AI-driven automation on AWS. Graduation of ArgoCD and Flux from the CNCF imparted enterprise-grade trust through extensive security audits and scalability tests. Consequently, 97% of ArgoCD users now operate the tool in production, and 42% manage more than 500 applications per instance.

Shift Toward DevSecOps Pipelines

Regulated enterprises are moving security checks inside declarative pipelines, reducing manual review cycles. Pulumi’s December 2025 release added unified state management for Terraform and OpenTofu, enabling consolidated policy-as-code enforcement.[2]Pulumi, “Pulumi for All Your IaC — Including Terraform and HCL,” pulumi.com GitLab version 18.7 introduced secret validity scanning, detecting expired credentials before deployment. European banks accelerated adoption to satisfy DORA requirements, with Intesa Sanpaolo reporting a 70% cut in audit prep time using Cisco’s GitOps-backed fabric controller.[3]Cisco, “Intesa Sanpaolo Achieves DORA Compliance with Cisco Nexus Dashboard Fabric Controller,” cisco.com PCI-DSS automation blueprints have emerged, codifying payment‐card controls as immutable infrastructure. Secrets management still lags because many teams rely on manual key rotation, highlighting the need for integrated vault solutions.

Rise of Multi-Cloud and Hybrid-Cloud Strategies

Enterprises filed 200% more multi-cloud orchestration requests in 2025, aiming to avoid vendor lock-in and optimize pricing. Declarative compositions combining Crossplane with Terraform now provision Red Hat OpenShift clusters consistently across AWS and Azure. An Indian fintech lowered cloud spend by 40% by dynamically shifting workloads between AWS and Azure under a GitOps-governed configuration baseline. Alibaba Cloud’s ACK One added GitOps capabilities for hybrid and edge estates, targeting Asia-Pacific enterprises balancing on-premises sovereignty with cloud agility. Despite these advances, teams still juggle multiple declarative languages, Terraform, Bicep, and Deployment Manager, before unifying them in CI/CD, increasing complexity.

Growing Compliance Automation Needs in Regulated Industries

FedRAMP authorization for Spacelift in September 2025 unlocked U.S. federal demand for SaaS-hosted IaC orchestration with air-gapped agents. GitLab’s compliance center now produces automated DORA and EU Cyber Resilience Act reports straight from merge requests. Cisco’s AI PODs for healthcare integrate ArgoCD to preserve HIPAA-compliant audit trails while automating Kubernetes upgrades. Japanese retailers used ArgoCD with Helm to achieve zero-downtime holiday releases, proving that compliance automation also boosts operational resilience. Persistent gaps remain because auditors still request manual attestations, prompting a surge in third-party reporting tools that translate Git commit history into regulator-friendly formats.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skills gap in Git-centric workflows | -2.8% | Global, intense within SME segments | Short term (≤ 2 years) |

| Security concerns over pipeline secrets management | -2.1% | Global, especially regulated sectors | Medium term (2-4 years) |

| Toolchain fragmentation and interoperability issues | -1.6% | Global, acute in multi-cloud estates | Long term (≥ 4 years) |

| Limited ROI visibility for large legacy environments | -1.2% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skills Gap in Git-Centric Workflows

A 2024 U.K. task-force survey showed 41% of SMEs deem DevOps too complex and 35% lack adequate talent.[4]UK Government, “SME Digital Adoption Taskforce Report,” gov.ukEven organizations already using GitOps struggle: environment promotion emerged as the top operational headache in the July 2025 CNCF survey, with many teams scripting ad-hoc workflows. Managed ArgoCD on EKS, launched November 2025, cuts installation and upgrade toil, narrowing the skill gap for SMEs. Platform engineering teams further reduce friction by exposing self-service deployment portals that hide Git concepts, though this approach demands dedicated engineers and initial investment. Universities are now embedding Kubernetes and GitOps into curricula, suggesting the constraint will ease over the next two to three years.

Security Concerns Over Pipeline Secrets Management

Secrets leakage still threatens supply chains. Pulumi warns that plain-text secrets persist in Git history even after rotation, a risk magnified when repositories are forked. Flux mitigates this with native SOPS encryption, but teams must manage encryption keys and update policies at scale. ArgoCD typically pairs with External Secrets Operator or HashiCorp Vault, adding moving parts and new failure modes. HashiCorp introduced dynamic provider credentials via Vault Secrets in January 2025, yet adoption remains limited to organizations already operating Vault clusters. Regulators now incorporate automated secrets rotation into DORA and PCI-DSS updates, pushing enterprises toward vault-centric patterns, but full rollout requires fresh budget and cultural change.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Hybrid Configurations Capture Air-Gapped Compliance Demand

Hybrid patterns address the dual need for SaaS agility and on-premises control. Solutions captured 46.2% of 2025 revenue, illustrating a preference for integrated toolchains that wrap GitOps controllers with policy engines. The hybrid segment is forecast to register a 24.2% CAGR, outpacing pure SaaS, as regulated entities deploy SaaS control planes while running execution agents inside air-gapped virtual private clouds to protect classified data. FedRAMP clearance for Spacelift and the managed ArgoCD add-on from AWS exemplify how vendors are productizing this architecture. Large banks still favor self-hosted control planes to meet zero-trust mandates, but rising operating costs steer them toward partially hosted dashboards that offload upgrades and patches. The GitOps and Infrastructure as Code software market size for hybrid deployments is projected to expand in tandem with confidential computing trends that mandate in-country processing while permitting centralized governance.

Second-generation platforms now bundle compliance packs, drift detection, and policy-as-code templates, making them appealing to aerospace and defense contractors. In the public sector, procurement rules increasingly require proof that SaaS providers support privatized execution modes, propelling hybrid demand. Across manufacturing, edge clusters running Flux benefit from thin-footprint agents but still connect to central policy hubs, confirming that an endpoint-agnostic control plane is crucial. As a result, the GitOps and Infrastructure as Code software market continues to blur the once-rigid lines between deployment categories, leaving flexibility, not location, as the prime buying criterion.

By Cloud Environment: Public Cloud Dominates as Native Integrations Mature

Public cloud deployments represented 71.8% of 2025 revenue and are forecast to progress at a 23.6% CAGR. Native integrations drive momentum: AWS offers a one-click ArgoCD add-on, Azure bundles Flux into AKS, and Google ships Anthos Config Management. Private clouds remain prominent in finance and healthcare, where data residency pushes workloads onto self-hosted OpenShift clusters. Hybrid control planes now straddle both worlds, with Alibaba Cloud’s ACK One orchestrating on-premises clusters in the same GitOps workflow as public cloud resources.

Flux’s microcontroller architecture suits resource-constrained edge nodes, signaling that the GitOps and Infrastructure as Code software market share for on-premises deployments will not evaporate but will reposition toward edge and sovereign-cloud projects. Cross-plane reconciles multi-cloud state as custom Kubernetes resources, trimming the overhead of writing provider-specific IaC scripts. As public clouds commoditize managed GitOps, differentiation shifts to compliance features, latency-sensitive edge support, and AI-assisted rollout strategies.

By End-User Industry: Healthcare Leaps Ahead on HIPAA-Compliant GitOps

IT and telecommunications dominated 24.3% of 2025 spending, a testament to microservices adoption and 5G roll-outs. Yet healthcare and life sciences are on track for a 22.6% CAGR as they embrace validated GitOps pipelines for software-as-medical-device updates. HIPAA regulations historically forced manual approvals, but declarative pipelines now create immutable audit logs, shortening release cycles from weeks to hours. Banks also deepen adoption to meet real-time change tracking mandated by DORA. Retailers look to GitOps for zero-downtime holiday promotions, while manufacturers run edge clusters that conform to IEC 62443, locking in the GitOps and Infrastructure as Code market share at factory floors.

Across government, FedRAMP-cleared SaaS control planes have significantly streamlined the procurement process, eliminating one of the primary barriers to adoption. While defense agencies continue to operate offline clusters due to security and operational requirements, recent bid solicitations have increasingly mandated support for declarative rollbacks, ensuring greater flexibility and reliability in operations. These developments have collectively driven horizontal adoption across various sectors, enabling the GitOps and Infrastructure as Code industry to cater to both green-field digital-native organizations and brown-field legacy estates. This dual penetration highlights the growing relevance of these technologies in modernizing infrastructure management and aligning with evolving operational demands.

By Organization Size: SMEs Accelerate as Managed Services Lower Barriers

Large enterprises retained 57.9% revenue share in 2025 because they operate hundreds of clusters and possess specialized platform engineering teams. However, SMEs are forecast to post a 25.4% CAGR, closing the gap as managed GitOps services hide complexity. AWS managed ArgoCD automates upgrades and disaster recovery, allowing ten-person DevOps squads to match enterprise-grade resilience without hiring Kubernetes experts. Usage-based pricing from Harness and Spacelift resonates with cost-sensitive startups by linking spend to deployment frequency rather than node count.

Community support also matters; open-source documentation and Slack channels now provide step-by-step guides for first-time adopters, further reducing onboarding friction. Meanwhile, enterprises keep scaling: 25% of ArgoCD instances connect to more than 20 clusters, and the GitOps and Infrastructure as Code market size tied to enterprise licenses still grows in absolute terms. The two tiers, therefore, converge on similar tooling, though buying cycles diverge; enterprises demand multi-year enterprise agreements and vendor road-maps, whereas SMEs prioritize immediate cost efficiency and out-of-the-box defaults.

Geography Analysis

North America controlled 33.6% of global revenue in 2025, buoyed by hyperscale cloud penetration and stringent DevSecOps mandates across banking and healthcare. FedRAMP-cleared SaaS platforms such as Spacelift widened federal uptake, and Harness leveraged its December 2025 USD 240 million funding to accelerate go-to-market across Fortune 500 accounts. Early adopters like Morgan Stanley and Capital One now treat GitOps as core infrastructure, validating enterprise maturity. Canada mirrors U.S. trends, while Mexican telecoms pilot GitOps for 5G roll-outs.

Asia-Pacific is the fastest-growing region, projected at a 25.8% CAGR. Japan’s Tokyo Gas achieved a 30% cost reduction by combining ArgoCD with service mesh for hybrid workloads. Chinese state-owned enterprises deploy Flux in sovereign clouds to honor data localization laws, and Alibaba Cloud embeds GitOps in ACK One to manage multi-cluster estates. India’s fintech community capitalizes on multi-cloud arbitrage, shifting workloads between AWS and Azure for pricing efficiency. Australia and New Zealand exhibit strong uptake in banking and government digitization projects.

Europe demonstrates robust growth driven by regulatory compliance. For instance, Intesa Sanpaolo achieved a 70% reduction in audit times by implementing automation aligned with the Digital Operational Resilience Act (DORA). This success is motivating other financial institutions across Germany and France to adopt similar strategies. The Middle East and Africa, along with South America, are emerging markets showing significant potential. These regions are witnessing growing interest as hyperscale cloud providers establish local data centers. The presence of these data centers not only reduces latency but also addresses compliance challenges, enabling businesses to operate more effectively within local regulatory frameworks. This development is expected to drive further adoption of advanced technologies and foster growth in these regions.

Competitive Landscape

The market exhibits a moderately fragmented structure, with open-source solutions maintaining a significant presence. ArgoCD leads the market with a significant share of cluster adoption, while Flux holds a smaller but notable portion, underscoring the dominance of open-source platforms. Despite Weaveworks ceasing operations in 2024 due to challenges in monetizing open-core models, the Flux community remains robust, supported by active community stewardship. Consolidation trends are evident, as demonstrated by Harness, which has raised substantial funding and achieved impressive annual recurring revenue (ARR), positioning its AI-driven platform as a comprehensive everything after code solution. Similarly, Spacelift’s recent funding round and FedRAMP clearance target U.S. government and other regulated industries, signaling a strategic focus on compliance-driven verticals.

Hyperscale cloud providers are increasingly embedding GitOps as managed services to secure workloads within their ecosystems. For instance, AWS offers managed ArgoCD, Azure integrates Flux extensions, and Google markets Anthos Config Management. HashiCorp, now under IBM’s ownership, plans to discontinue its Terraform free tier by March 2026, prompting a surge in interest for alternatives such as Pulumi, env0, and OpenTofu. Pulumi has responded to this shift by introducing first-class HCL support and offering migration credits, positioning itself as a universal Infrastructure-as-Code (IaC) broker. This strategic move highlights the growing competition among IaC providers as they aim to capture market share in a rapidly evolving landscape.

Emerging tools are addressing unmet needs in environment promotion, driving innovation within the market. Solutions like Kargo and Codefresh GitOps Promoter are gaining traction, reflecting the demand for more specialized tools to streamline deployment processes. These developments indicate a dynamic market environment where innovation continues to thrive, fueled by the need for enhanced efficiency and compliance. As the market evolves, the interplay between open-source platforms, managed services, and emerging tools will shape the competitive landscape, offering opportunities for growth and differentiation.

GitOps And Infrastructure As-a-Code (IaC) Software Industry Leaders

HashiCorp Inc.

GitLab Inc.

Red Hat Inc.

Amazon Web Services Inc.

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: GitLab launched GitLab Duo Agent Platform GA, introducing agentic AI workflows and usage-based pricing via GitLab Credits.

- December 2025: Harness closed a USD 240 million Series E round led by Goldman Sachs at a USD 5.5 billion valuation.

- December 2025: GitLab released version 18.7, bringing secret validity checks and enhanced pipeline reports to GA.

- December 2025: HashiCorp announced the HCP Terraform free tier will end on 31 Mar 2026 and introduced monorepo support.

Global GitOps And Infrastructure As-a-Code (IaC) Software Market Report Scope

The GitOps and Infrastructure as Code Software Market Report is Segmented by Deployment Model (SaaS, Self-Hosted, Hybrid), Organization Size (Small and Medium Enterprises, Large Enterprises), End-User Industry (IT and Telecommunications, Banking Financial Services and Insurance, Healthcare and Life Sciences, Retail and E-Commerce, Manufacturing, Government and Public Sector, Other End-User Industries), Cloud Environment (Public Cloud, Private Cloud), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

The GitOps and Infrastructure-as-Code (IaC) Software Market refers to software tools and platforms that enable automated infrastructure provisioning and application deployment using code-based configurations and version control systems. IaC solutions define and manage infrastructure through machine-readable scripts, while GitOps tools extend this approach by using Git repositories as the single source of truth for continuous deployment and operations.

| SaaS |

| Self Hosted |

| Hybrid |

| Small and Medium Enterprises SMEs |

| Large Enterprises |

| IT and Telecommunications |

| Banking Financial Services and Insurance BFSI |

| Healthcare and Life Sciences |

| Retail and E Commerce |

| Manufacturing |

| Government and Public Sector |

| Other End User Industries |

| Public Cloud |

| Private Cloud |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Deployment Model | SaaS | |

| Self Hosted | ||

| Hybrid | ||

| By Organization Size | Small and Medium Enterprises SMEs | |

| Large Enterprises | ||

| By End User Industry | IT and Telecommunications | |

| Banking Financial Services and Insurance BFSI | ||

| Healthcare and Life Sciences | ||

| Retail and E Commerce | ||

| Manufacturing | ||

| Government and Public Sector | ||

| Other End User Industries | ||

| By Cloud Environment | Public Cloud | |

| Private Cloud | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the GitOps and Infrastructure as Code software market?

The market stands at USD 2.39 billion in 2026 and is projected to reach USD 6.40 billion by 2031.

Which deployment model is growing fastest?

Hybrid deployments are forecast to expand at a 24.2% CAGR through 2031 as organizations blend SaaS agility with air-gapped compliance.

Why are healthcare firms adopting GitOps rapidly?

HIPAA-compliant GitOps patterns cut release times while providing immutable audit logs, driving a 22.6% CAGR in healthcare and life sciences.

How are hyperscale clouds influencing adoption?

AWS, Azure, and Google offer managed GitOps add-ons that eliminate setup overhead, boosting public cloud share to 71.8% of 2025 revenue.

What security challenge still hinders GitOps rollouts?

Secrets management remains a primary concern because plain-text credentials can leak through Git history, necessitating vault-integrated workflows.

Which region will grow quickest over the next five years?

Asia-Pacific is expected to post the fastest 25.8% CAGR, propelled by digital transformation programs in Japan, China, and India.

Page last updated on: