Advanced Glycation End Products Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

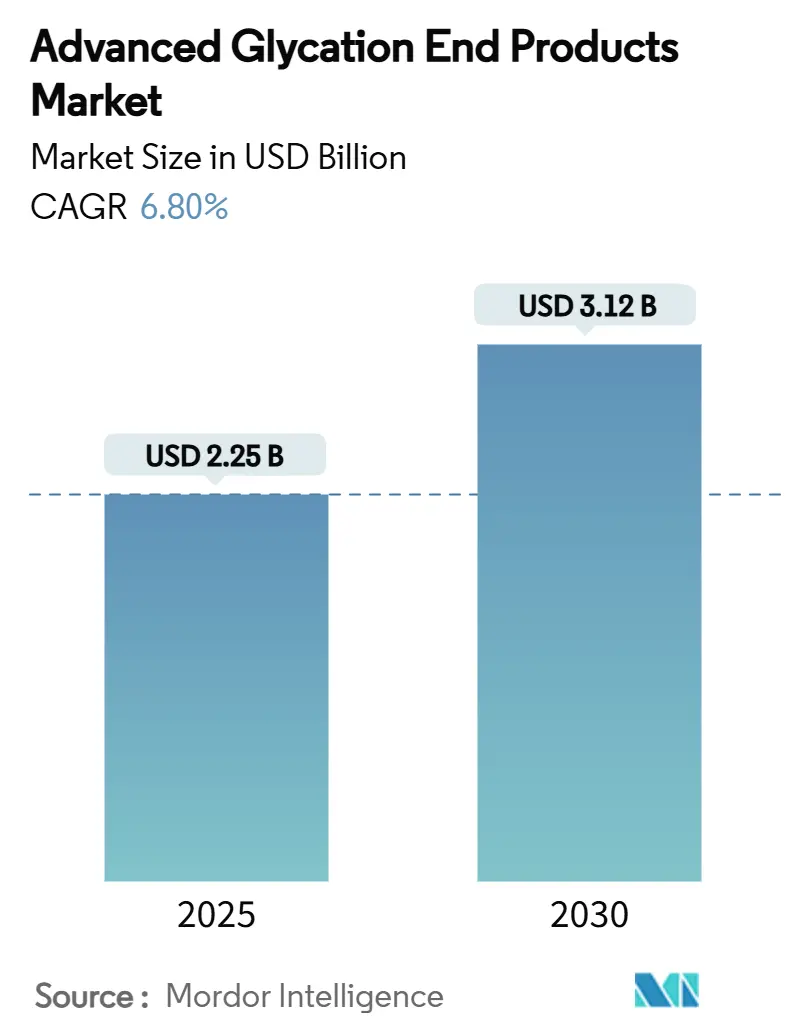

| Market Size (2025) | USD 2.25 Billion |

| Market Size (2030) | USD 3.12 Billion |

| Growth Rate (2025 - 2030) | 6.80% CAGR |

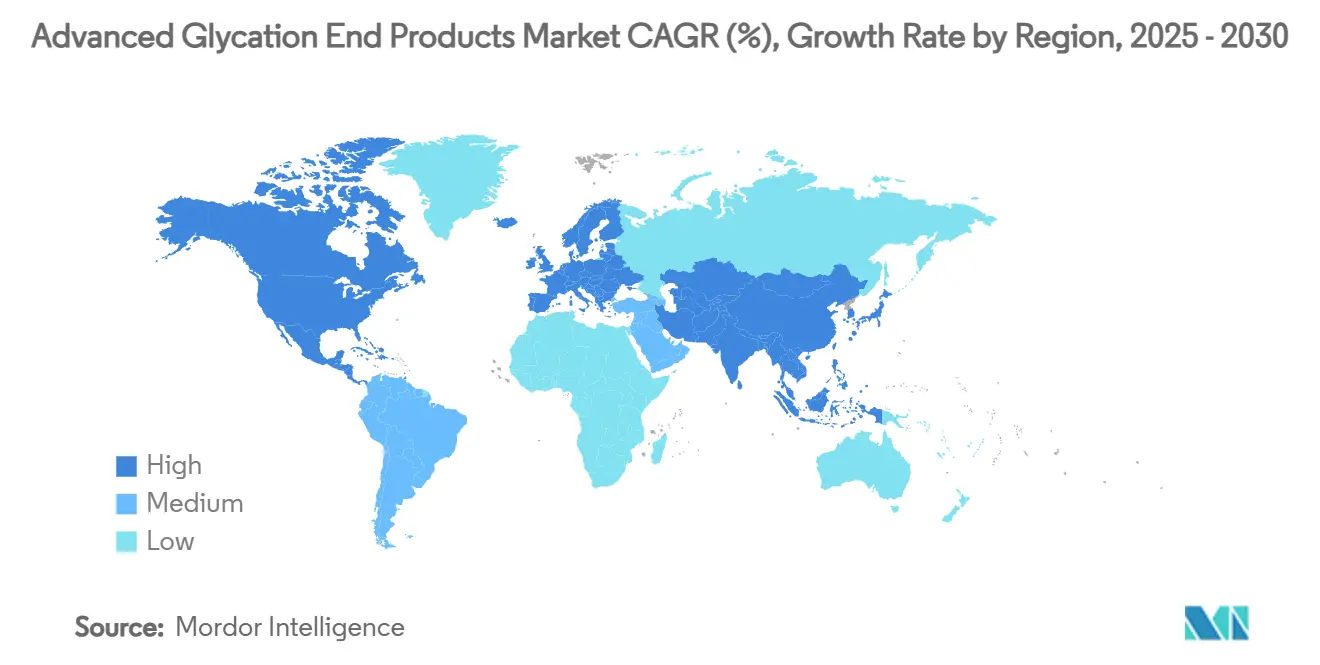

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Advanced Glycation End Products Market Analysis by Mordor Intelligence

The Advanced Glycation End Products market size is valued at USD 2.25 billion in 2025 and is forecast to reach USD 3.12 billion by 2030, reflecting a 6.8% CAGR during the period. Steady expansion rests on the growing recognition of AGEs as reliable biomarkers and therapeutic targets across metabolic, cardiovascular, and neurodegenerative disorders, which drives laboratory demand for highly standardized reference materials. Analytical breakthroughs that offer ten-fold sensitivity gains, together with a visible shift from fluorescence-based to non-fluorescent measurement protocols, enable laboratories to quantify individual AGE species with greater precision. Regulatory momentum in food safety and novel foods assessments broadens commercial testing demand, while the appetite for point-of-care AGE readers creates an adjacent opportunity set for calibration standards and low-volume reagent kits. Supply chain constraints around animal-derived proteins persist, yet the emergence of recombinant production systems reduces variability and enhances lot-to-lot consistency. Together, these trends keep competitive entry barriers moderately high and preserve healthy pricing discipline across the Advanced Glycation End Products market.

Key Report Takeaways

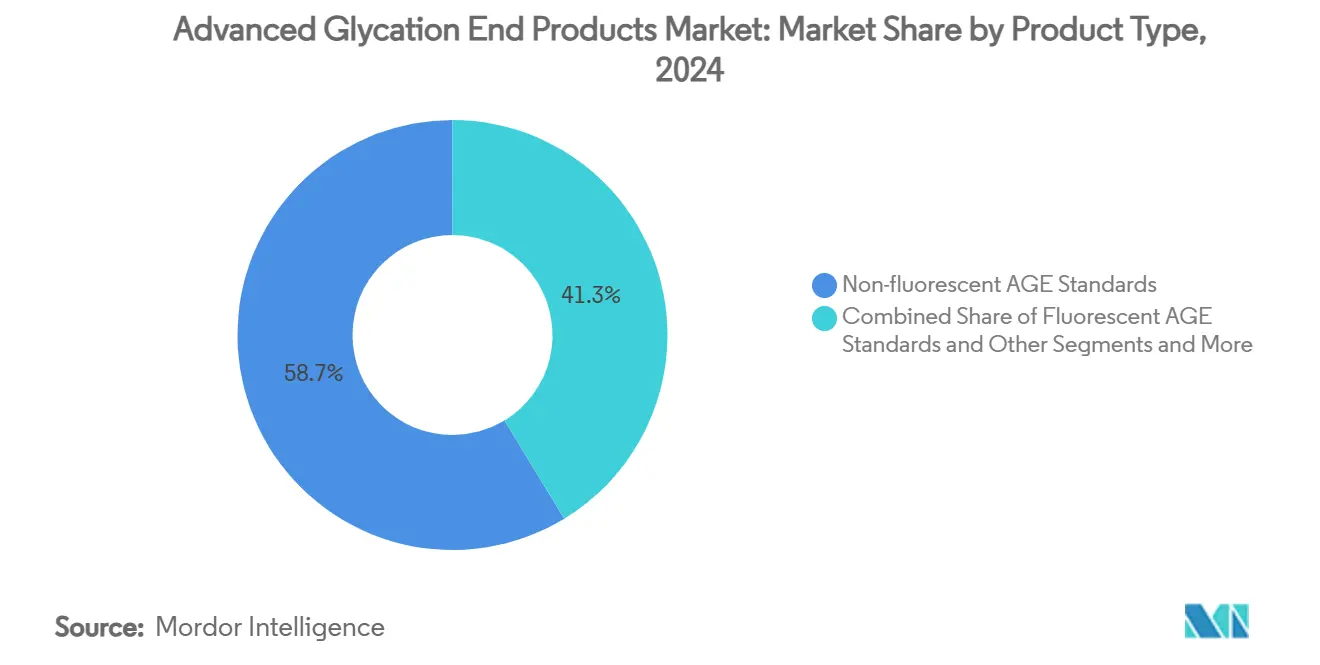

- By product type, non-fluorescent AGE standards held 58.7% of the Advanced Glycation End Products market share in 2024, whereas the “Others” subset is expected to advance at an 11.8% CAGR through 2030.

- By application, diabetes-complication research commanded 22.8% of the Advanced Glycation End Products market size in 2024, while neurodegenerative disease research carries the fastest growth outlook at 12.6% to 2030.

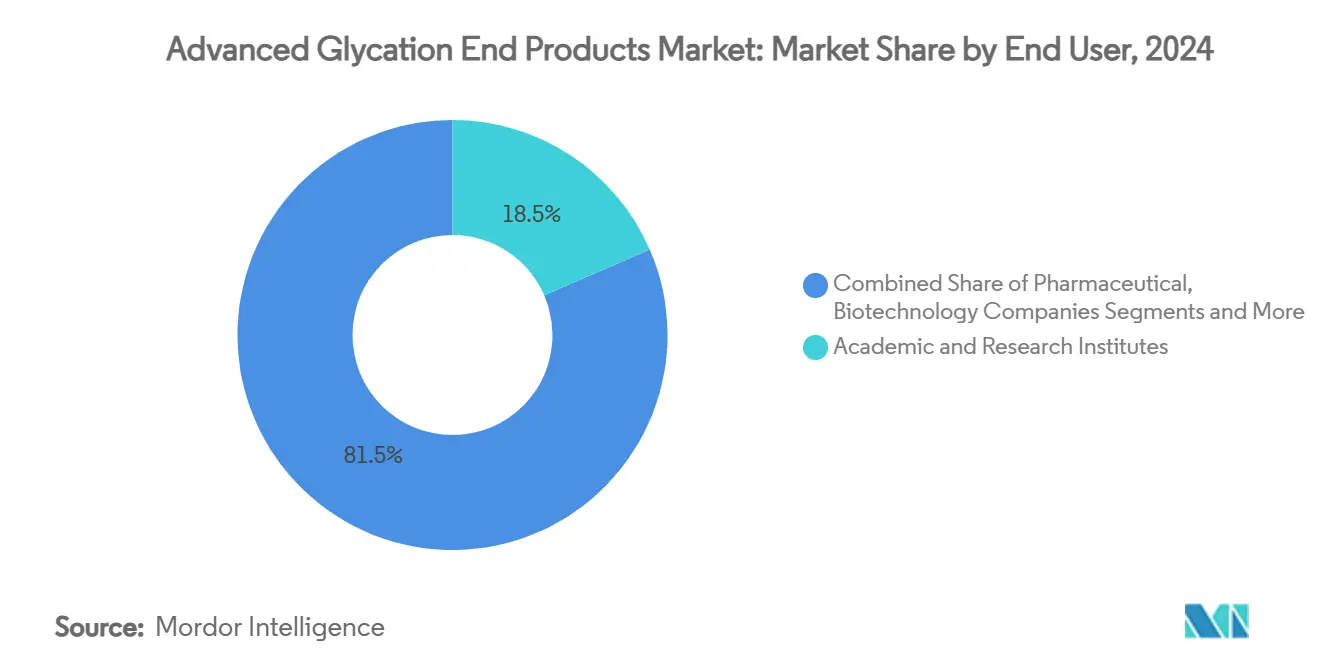

- By end user, academic and research institutes captured 18.5% share of the Advanced Glycation End Products market size in 2024; pharmaceutical and biotechnology companies record the strongest CAGR at 10.9% through 2030.

- By geography, North America led with 36.8% of the Advanced Glycation End Products market share in 2024, whereas Asia Pacific is forecast to expand at an 8.4% CAGR over the same horizon.

Global Advanced Glycation End Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global diabetes prevalence | +1.80% | Global, concentrated in Asia Pacific and North America | Long term (≥ 4 years) |

| Growing R&D funding for AGE-linked chronic diseases | +1.20% | North America and EU, spill-over to Asia Pacific | Medium term (2–4 years) |

| Expansion of AGE testing in food-safety and labeling programs | +0.90% | EU core, expanding to North America | Medium term (2–4 years) |

| Advances in minimally-invasive fluorescence devices | +1.10% | Global, early adoption in developed markets | Short term (≤ 2 years) |

| Emerging EU limits on AGEs in clinical nutrition and infant formula | +0.70% | EU, with harmonization to other regions | Long term (≥ 4 years) |

| Surge in anti-glycation cosmetic formulations needing standards | +0.50% | Global, led by Asia Pacific and North America | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Global Diabetes Prevalence

Diabetes affects AGE formation rates and therefore anchors long-term demand for reference standards. Research programs on diabetic complications already absorb 22.8% of the Advanced Glycation End Products market.[1]Krishna Adeshara, “Protein Glycation Products Associate With Progression of Kidney Disease and Incident Cardiovascular Events in Individuals With Type 1 Diabetes,” Cardiovascular Diabetology, biomedcentral.com NIDDK earmarked USD 7.5 million in 2024 for Diabetes Research Centers and a further USD 29.5 million for TrialNet coordination in 2025, both of which mandate harmonized AGE assays. A population-based study of 77,143 adults showed skin autofluorescence predicts cardiovascular mortality, encouraging clinicians to integrate AGE screening in routine risk assessment. These observations persuade pharmaceutical sponsors to include AGE endpoints in clinical trials, which multiplies demand for high-purity calibrants. As screening shifts from reactive diabetes management to proactive cardiometabolic monitoring, the Advanced Glycation End Products market secures a durable expansion path.

Growing R&D Funding for AGE-Linked Chronic Diseases

Independent of glycemic control, AGEs are implicated in neurodegeneration, renal decline, and systemic aging. BioAge Labs secured USD 550 million from Novartis in 2024 to pursue age-modifying drug targets, with program protocols calling for validated AGE assays at every site. The National Institutes of Health allocated USD 29.5 million to TrialNet, insisting on uniform biomarker panels that include key AGE species.[2]National Institutes of Health, “Coordinating Center for Type 1 Diabetes TrialNet (U01 Clinical Trial Required),” nih.gov Chiba University’s clinical study on nicotinamide riboside in Werner syndrome likewise required bespoke AGE quantification methods. Funding concentration in North American and European hubs magnifies regional reagent consumption and cements technology leadership. As research scopes broaden from single indications to multi-pathway aging biology, laboratories demand a wider catalog of standards that fuels incremental revenue across the Advanced Glycation End Products market.

Expansion of AGE Testing in Food-Safety & Labeling Programs

The EU’s 2025 novel-foods guidance obliges manufacturers to document the AGE formation potential during processing.[3]European Food Safety Authority, “Navigating Novel Foods: What EFSA’s Updated Guidance Means for Safety Assessments,” efsa.europa.eu Dietary surveys reveal 2.7-fold variation in AGE intake based on cooking techniques, a gap that regulators address by encouraging standardized assays for methylglyoxal-derived AGEs. Commission Regulation (EU) 2023/915 codifies maximum contaminant levels, making laboratory AGE tests part of compliance workflows. Food producers adopt AGE analytics for label claims, generating a fresh buyer cohort that previously sat outside biomedical research. The structural broadening of end markets underpins a multi-year lift in sales for suppliers able to translate biomedical expertise into accredited food-testing kits within the Advanced Glycation End Products market.

Advances in Minimally-Invasive Fluorescence Devices

Portable AGE readers based on skin autofluorescence reduce sample-handling complexity and widen the user base beyond specialist labs. Near-infrared multispectral sensors achieve 9.98% glucose accuracy and offer an architecture that can accommodate AGE wavelengths, setting the stage for real-time metabolic monitoring. Fluorescence lifetime imaging microscopy further enables cellular-level AGE mapping, adding spatial-omics value to pre-clinical workflows. These hardware gains democratize AGE measurement and create spill-over demand for miniaturized reference materials and calibration slides. Suppliers that bundle standards with device-specific software extensions are positioned to capture emergent revenue pools inside the Advanced Glycation End Products market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lack Of Clinical Standardization For AGE Biomarkers | -1.40% | Global, particularly affecting regulatory approval pathways | Long term (≥ 4 years) |

| High Cost Of Advanced Analytical Instrumentation | -0.80% | Emerging markets and smaller research institutions | Medium term (2-4 years) |

| Supply Bottlenecks For High-Purity Non-Fluorescent AGE Reagents | -0.60% | Global, with acute impact on specialized research applications | Short term (≤ 2 years) |

| Ethical Issues With Animal-Derived AGE-Modified Proteins | -0.40% | EU and North America, with regulatory spillover effects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lack of Clinical Standardization for AGE Biomarkers

Although FDA guidance on laboratory-developed tests clarified overarching requirements in 2024, no consensus exists on which AGE species merit routine clinical measurement. Studies show that carboxymethyl-lysine, pentosidine, and methylglyoxal-lysine dimer exert different pathological weights, yet reference ranges remain undefined across diverse populations. This uncertainty discourages physicians from adopting AGE tests as diagnostic criteria and restrains payer reimbursement. Pharmaceutical developers hesitate to select AGE endpoints for pivotal trials without regulator-endorsed cut-offs, slowing companion reagent sales. Until harmonized clinical guidelines emerge, market growth relies more heavily on research rather than diagnostic channels inside the Advanced Glycation End Products market.

High Cost of Advanced Analytical Instrumentation

High-resolution mass spectrometers and ultra-high-performance LC systems are essential for comprehensive AGE profiling, yet acquisition prices often top USD 1 million per unit. Operating costs rise further due to service contracts and specialist labour. Budget constraints press hardest on emerging markets and mid-tier universities, forcing them to outsource testing to contract research organizations. The capital hurdle concentrates adoption within well-funded centers and slows diffusion in price-sensitive regions. Although recombinant reagents promise lower consumable costs, total assay economics remain dominated by instrument depreciation, limiting overall expansion of the Advanced Glycation End Products market in undercapitalized geographies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Growing Sophistication Drives Non-Fluorescent Adoption

Non-fluorescent standards controlled 58.7% of the Advanced Glycation End Products market in 2024, reflecting their capacity to eliminate auto-fluorescence interference and to quantify individual AGE adducts with single-ppm resolution. Researchers turn to isotope-labeled carboxyethyl-lysine and methylglyoxal derivatives to calibrate LC-MS methods that map precise AGE burden at the tissue level. Fluorescent calibrants retain utility for high-throughput screens and legacy protocols but register slower growth as labs migrate toward LC-MS platforms.

The “Others” cluster, covering recombinant sRAGE constructs and hybrid nano-labels, is projected to rise at an 11.8% CAGR to 2030, outpacing the core. Morinaga Bio Science Research Institute’s biotin-sRAGE, launched in 2025, illustrates how genetically modified silkworm expression improves lot consistency and mitigates animal-derived supply risk. As vendors pair recombinant proteins with synthetic linkers, product lines blur classical boundaries and fuel incremental demand. This evolution sustains high single-digit growth for the Advanced Glycation End Products market even as top-line prices gradually compress.

By Application: Neurodegeneration Emerges as the Fastest Mover

Diabetes-complication research accounted for 22.8% of the Advanced Glycation End Products market share in 2024, anchored by well-funded cardiovascular and renal studies. Trial protocols routinely measure AGEs alongside HbA1c to capture long-term glycemic damage.

Neurodegenerative disease research now advances at a 12.6% CAGR through 2030, propelled by mounting data that links AGEs to amyloid aggregation and synaptic loss in Alzheimer’s and Parkinson’s disease. Funding injections from foundations such as The Michael J. Fox Foundation amplify demand for brain-targeted AGE assays. Cardiovascular and renal fields maintain steady uptake, while food and nutrition testing grows from a modest base on the back of EU regulatory mandates. Collectively, application diversification cushions the Advanced Glycation End Products market against cyclical funding swings in any single disease area.

By End User: Pharmaceutical Entry Re-Shapes Demand Patterns

Academic centers held an 18.5% share of the Advanced Glycation End Products market in 2024, underscoring their historical leadership in mechanistic research. These institutions remain anchor customers for broad catalog products and exploratory reagents.

Pharmaceutical and biotechnology firms, however, will post a 10.9% CAGR to 2030 as they embed AGE endpoints into drug-discovery and biomarker-stratification programs. BioAge Labs’ portfolio of NLRP3 inhibitors and senolytics exemplifies the translational uptake that pulls reagents into regulated bioanalytical testing workflows. Diagnostic laboratories account for consistent baseline consumption, while contract research organizations act as multipliers by servicing sponsors that lack in-house AGE expertise. This swing toward commercial therapeutic development reinforces revenue visibility for suppliers operating in the Advanced Glycation End Products market.

Geography Analysis

North America claimed 36.8% of the Advanced Glycation End Products market in 2024, buoyed by federal research outlays and early adoption of LC-MS platforms. Funding from NIDDK and NIH underwrites multicenter trials that stipulate harmonized calibrants, giving vendors predictable volume flows. The FDA’s structured pathway for laboratory-developed tests provides regulatory clarity, encouraging diagnostic firms to codify AGE kits. Leading suppliers such as Thermo Fisher expand instrument installed bases through next-generation mass spectrometers that promise ten-fold sensitivity gains, locking in aftermarket reagent sales.

Europe maintains a strong presence thanks to stringent food-safety legislation and mature pharmaceutical research networks. EFSA’s updated novel-foods guidance and Regulation (EU) 2023/915 compel food laboratories to quantify AGE levels, injecting recurrent demand outside core biomedical sectors. Cross-border initiatives, including Novartis’ USD 550 million collaboration with BioAge Labs, reinforce biomarker standardization across clinical sites and stimulate higher-grade reagent consumption.

Asia Pacific is the fastest expanding region with an 8.4% CAGR through 2030, driven by a dual effect of rising diabetes prevalence and growing biotechnology investment. China scales GMP-grade reagent manufacturing, narrowing historic cost gaps with Western providers, while Japan leverages advanced analytical know-how to develop high-fidelity fluorescence devices. South Korea’s partnership between KAIST and MilliporeSigma exemplifies how academic–industry tie-ups accelerate local assay development. India and Southeast Asian economies add incremental upside as public-health agencies prioritize metabolic disease surveillance, ensuring sustained order inflows into the Advanced Glycation End Products market.

Competitive Landscape

Moderate fragmentation prevails as technical complexity restricts commodity-style entry. Thermo Fisher Scientific and Merck KGaA (MilliporeSigma) retain leadership by bundling instruments, consumables, and validation services. Thermo Fisher’s Stellar mass spectrometer, introduced in 2024, provides 10× quantitative sensitivity, elevating lower-limit detection for methylglyoxal-derived AGEs and reinforcing instrument-linked reagent pull-through. Specialty houses such as Cell Biolabs and Cayman Chemical focus on niche AGE derivatives, while Randox embeds AGE measurements into multi-analyte chemistry panels that target hospital labs.

Strategic routes center on academic consortia and technology licensing. MilliporeSigma’s alliances with KAIST and The Michael J. Fox Foundation grant early visibility into emerging disease models that require bespoke AGE standards. Recombinant protein innovators, typified by Morinaga Bio Science Research Institute, challenge incumbents by eliminating animal-derived inputs and securing supply resilience. Price competition remains contained because validation costs and quality-system overheads create natural floor pricing.

However, geographic manufacturing diversification in China and India could gradually compress margins over the coming decade. Overall, differentiation hinges on assay-specific performance data, regulatory dossiers, and end-to-end customer support across the Advanced Glycation End Products market.

Advanced Glycation End Products Industry Leaders

Merck KGaA

Thermo Fisher Scientific Inc.

Abcam plc

Cell Biolabs Inc.

Diagnoptics Technologies BV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: Morinaga Bio Science Research Institute launched Biotin-sRAGE recombinant reagent produced in genetically modified silkworms, offering enhanced stability for AGE binding studies.

- January 2025: BioAge Labs discontinued azelaprag due to liver enzyme findings and nominated BGE-102 as its next clinical candidate.

- September 2024: Asahi Kasei Pharma agreed to transfer its diagnostics business, including metabolic reagents, to Nagase & Co. effective July 2025, aiming to boost healthcare growth.

Global Advanced Glycation End Products Market Report Scope

| Fluorescent AGE Standards & Reagents |

| Non-fluorescent AGE Standards & Reagents |

| Others |

| Diabetes Complications Research |

| Cardiovascular & Renal Disease Research |

| Neurodegenerative Disease Research |

| Oncology Research |

| Food & Nutrition Studies |

| Academic & Research Institutes |

| Pharmaceutical & Biotechnology Companies |

| Diagnostic Laboratories |

| Food & Beverage Testing Labs |

| Contract Research Organizations |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Fluorescent AGE Standards & Reagents | |

| Non-fluorescent AGE Standards & Reagents | ||

| Others | ||

| By Application | Diabetes Complications Research | |

| Cardiovascular & Renal Disease Research | ||

| Neurodegenerative Disease Research | ||

| Oncology Research | ||

| Food & Nutrition Studies | ||

| By End User | Academic & Research Institutes | |

| Pharmaceutical & Biotechnology Companies | ||

| Diagnostic Laboratories | ||

| Food & Beverage Testing Labs | ||

| Contract Research Organizations | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the Advanced Glycation End Products market in 2025?

The Advanced Glycation End Products market size stands at USD 2.25 billion in 2025.

What CAGR is projected for this market to 2030?

The market is forecast to register a 6.8% CAGR between 2025 and 2030.

Which product segment leads in revenue contribution?

Non-fluorescent AGE standards contribute the largest share at 20.7% in 2024.

Which application area is growing fastest?

Neurodegenerative disease research is projected to expand at 12.6% annually through 2030.

Which region shows the highest growth rate?

Asia Pacific is set to grow the quickest with an anticipated 8.4% CAGR over 2025-2030.

What factor most constrains widespread diagnostic adoption of AGE testing?

The lack of globally harmonized clinical reference ranges for AGE biomarkers hinders routine diagnostic integration.

Page last updated on: