GCC Foodservice Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

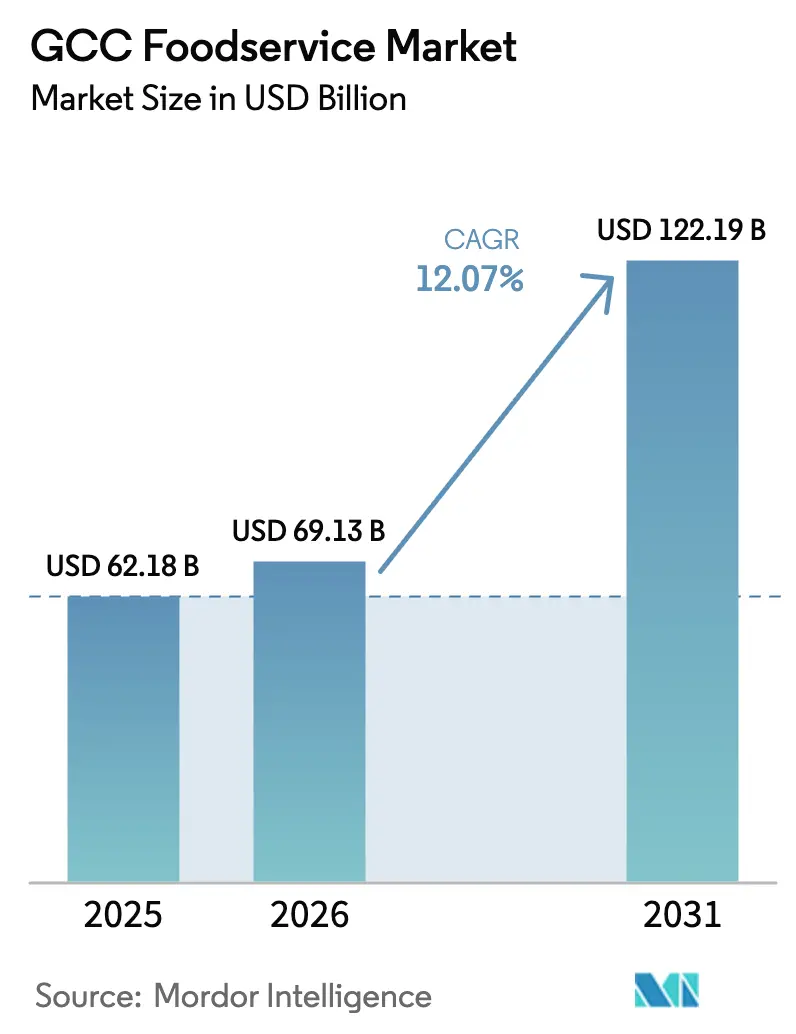

| Base Year Market Size (2025) | USD 62.18 Billion |

| Market Size (2026) | USD 69.13 Billion |

| Market Size (2031) | USD 122.19 Billion |

| Growth Rate (2026 - 2031) | 12.07% CAGR |

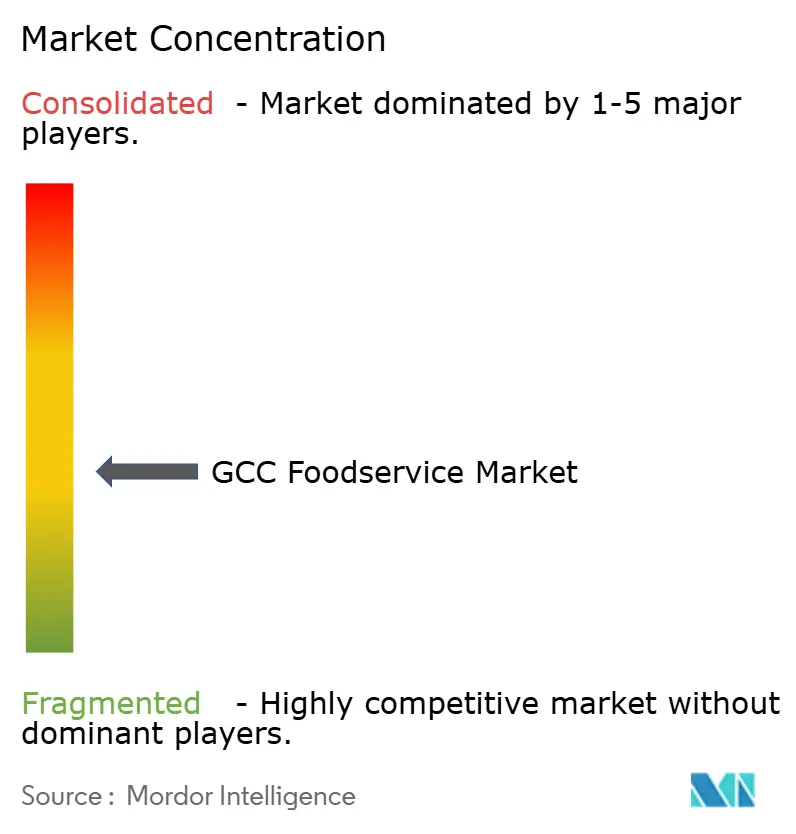

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

GCC Foodservice Market Analysis by Mordor Intelligence

The GCC Foodservice Market size was valued at USD 62.18 billion in 2025 and is estimated to grow from USD 69.13 billion in 2026 to reach USD 122.19 billion by 2031, at a CAGR of 12.07% during the forecast period (2026-2031). Key drivers include substantial investments in mega-tourism hubs, the rise of delivery-first consumer preferences, and labor-nationalization policies that enhance service quality, expanding revenue opportunities across various formats. Saudi Arabia remains a central market, with its Vision 2030 initiative integrating thousands of restaurant seats into mixed-use developments. Concurrently, Kuwait's policy-driven diversification is accelerating the establishment of new outlets. Cloud kitchens are gaining traction as aggregators utilize AI to direct orders to delivery-only platforms, cutting startup costs and reducing turnaround times. Chain operators, supported by centralized procurement and real-time loyalty data, are outperforming independent players but face challenges such as high rents and import-related cost volatility. The adoption of technology, including mobile ordering, predictive inventory systems, and robotics, has shifted from being optional to essential, creating a clear divide between efficient brands and slower adopters.

Key Report Takeaways

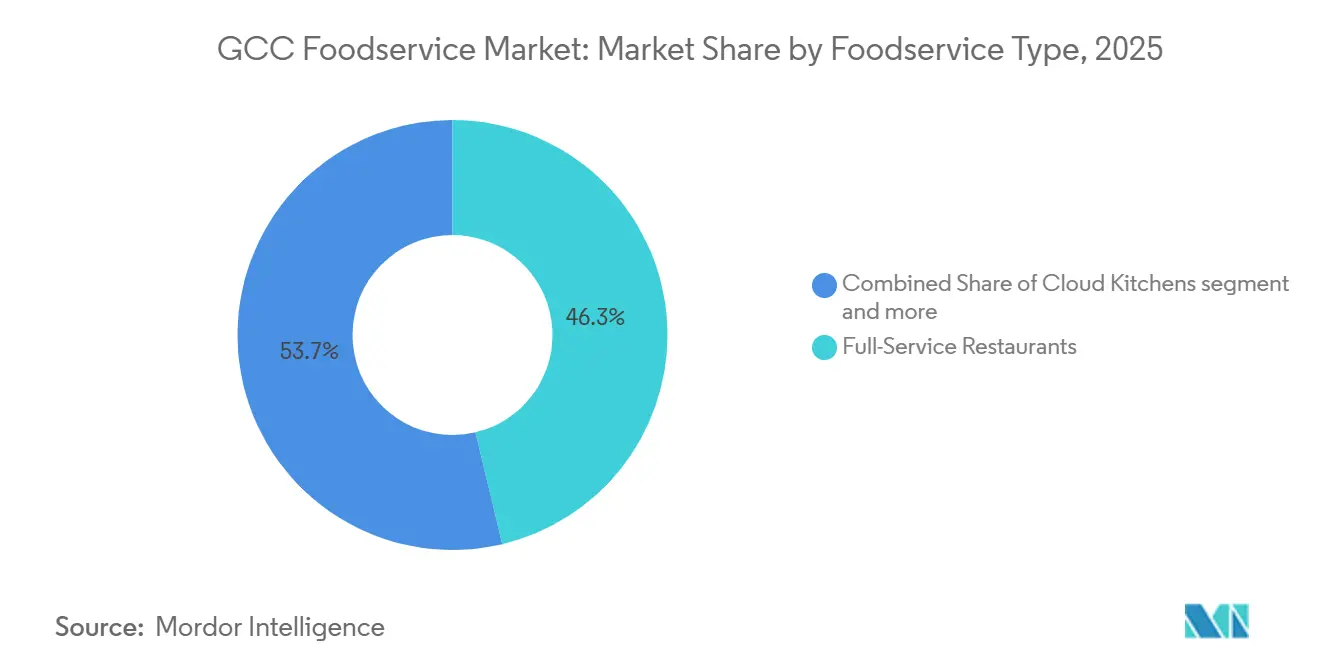

- By foodservice type, full-service restaurants led with 46.29% of GCC Foodservice market share in 2025, yet cloud kitchens are advancing at a 13.24% CAGR through 2031.

- By outlet, independent outlets accounted for 58.73% of the GCC Foodservice market size in 2025, while chained formats are scaling at a 12.84% CAGR.

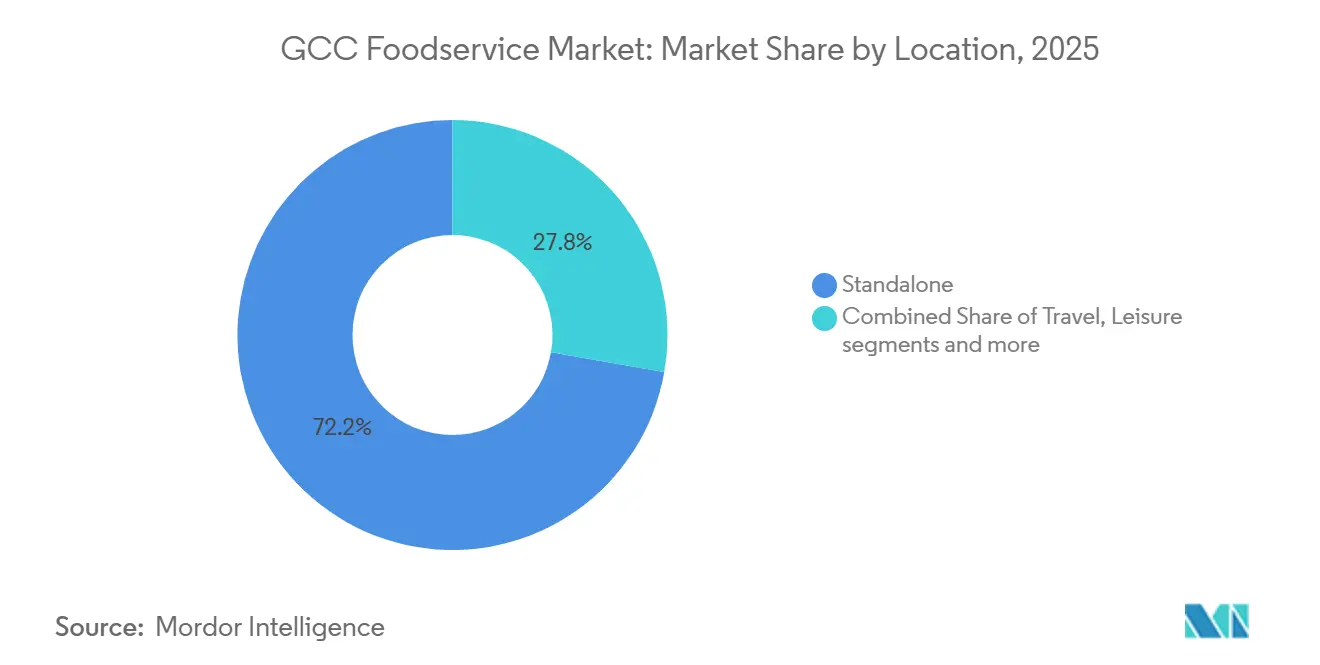

- By location, standalone locations held a 72.24% revenue share in 2025; leisure-anchored venues are forecast to expand at a 13.69% CAGR to 2031.

- By service type, dine-in transactions captured 62.24% of spend in 2025, whereas delivery orders are growing fastest at a 13.78% CAGR.

- By geography, Saudi Arabia commanded 47.27% of regional sales in 2025, and Kuwait is the quickest riser with a 13.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

GCC Foodservice Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of quick-service chains | +2.1% | Saudi Arabia, UAE, Kuwait | Medium term (2-4 years) |

| Rising tourism linked to mega-events (Expo City, Vision 2030) | +3.2% | Saudi Arabia, UAE, Qatar | Long term (≥ 4 years) |

| E-commerce integrations driving cloud-kitchen demand | +1.8% | GCC-wide, strongest in UAE and Saudi Arabia | Short term (≤ 2 years) |

| Growth of healthy/functional menus | +1.3% | UAE, Saudi Arabia, Qatar | Medium term (2-4 years) |

| AI-optimized demand forecasting for inventory cuts | +1.5% | GCC-wide, early adoption in UAE | Short term (≤ 2 years) |

| Digital transformation in restaurants supports the market | +1.9% | GCC-wide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid expansion of quick-service chains

Quick-service restaurant (QSR) networks are rapidly occupying high-traffic corridors, surpassing full-service concepts in obtaining licenses. This trend creates a competitive land-grab environment that benefits franchisees with centralized capital. Americana Restaurants, which operates 2,590 outlets including KFC and Pizza Hut, reported that 44% of its revenue now comes from home delivery. This highlights QSRs' ability to adapt more effectively to off-premise demand compared to traditional dine-in establishments. Kudu Company for Food and Catering, with over 350 branches in Saudi Arabia, has entered into a partnership with Sushi Sushi to open 40 new locations by 2035. This initiative expands Kudu's offerings beyond its core burger-and-chicken menu, catering to health-conscious consumers. In 2024, the Dubai Municipality issued 1,200 new restaurant licenses, an increase of 16 restaurants from 2023[1]Source: Dubai Department of Economy and Tourism, "Annual Dubai Gastronomy Industry Report 2024", dubaidet.gov.ae. This growth indicates both a rise in demand and the municipality's streamlined approval processes, which accelerate market entry for QSR chains.

Rising tourism linked to mega-events (expo city, vision 2030)

Sovereign-backed tourism infrastructure is integrating thousands of restaurant seats into mixed-use destinations, transforming transient visitor flows into consistent foodservice revenue. In 2025, Dubai recorded 19.59 million overnight visitors, reflecting a 5% rise from 2024[2]Source: Dubai Department of Economy and Tourism, "Tourism Performance Report January - December 2025", dubaidet.gov.ae. During the first quarter of 2025, Saudi Arabia experienced a record 9.7% growth in international visitor spending compared to the same period in 2024[3]Source: Ministry of Tourism Saudi Arabia, "Visitor Spending Reaching SAR 49.4 Billion in Q1 2025", mt.gov.sa. As part of Vision 2030, Saudi Arabia aims to attract 150 million visitors by 2030, supported by mega-projects such as NEOM, the Red Sea Project, and Qiddiya, all of which include dedicated hospitality districts. The 2023-24 Riyadh Season, a recurring entertainment festival, attracted substantial attendance, generating over SAR 10 billion in economic impact, with foodservice operators reporting a 30-40% increase in revenue. Expo City Dubai, a permanent district located on the former Expo 2020 site, is planned for expansion by 2031. Oman's Vision 2040 strategy aims to triple tourism receipts, with projects like Muscat Bay and Yiti boosting resort-anchored foodservice capacity.

E-commerce integrations driving cloud-kitchen demand

Delivery platforms have transitioned from intermediaries to key decision-makers, influencing menu design, pricing strategies, and kitchen locations through data-sharing agreements that blur the boundaries between operators and distributors. In 2025, Qatar's Ministry of Public Health introduced licensing guidelines for cloud kitchens. These regulations, requiring separate ventilation systems and real-time health inspections, have increased compliance costs but also enhanced the format's appeal to institutional investors. By mid-2025, Dubai Municipality mandated that all cloud kitchens register under a dedicated "virtual restaurant" category. This initiative improves the tracking of food-safety violations and simplifies enforcement processes. In February 2026, Kuwait implemented delivery platform regulations, capping commission rates at 15%. This measure aims to protect smaller operators, potentially reducing aggregator profit margins while stabilizing restaurant profitability.

Growth of healthy/functional menus

Health-conscious consumers are increasingly demanding transparency in sourcing and macronutrient labeling. Consequently, operators are reformulating core menu items to avoid losing market share to wellness-focused competitors. Menus featuring plant-based and functional ingredients are expanding. For instance, several UAE-based chains have introduced vegan burger lines in response to growing demand for dairy-free and gluten-free options. In 2024, Saudi Arabia's Food and Drug Authority updated its nutritional-labeling regulations, requiring calorie counts on all chain-restaurant menus. This regulation aligns with international best practices and encourages operators to adopt lower-calorie formulations. Alshaya Group, which manages brands such as Starbucks, Shake Shack, and P.F. Chang's in the GCC, reported in its 2025 sustainability brief that 30% of its new menu items now include plant-based proteins or reduced-sugar alternatives. Additionally, cafés are offering functional beverages, including collagen-infused smoothies and adaptogenic teas, reflecting wellness trends that originated in Western markets but are now being localized in the GCC.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High real-estate rents in premium retail zones | -1.4% | UAE (Dubai, Abu Dhabi), Qatar (Doha) | Short term (≤ 2 years) |

| Growing "eat-at-home" preference post-inflation | -1.1% | GCC-wide, most acute in Saudi Arabia and UAE | Medium term (2-4 years) |

| Tightening labor-nationalization quotas | -1.6% | Saudi Arabia, UAE, Kuwait | Medium term (2-4 years) |

| Import-dependent supply-chain volatility | -1.2% | GCC-wide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High real-estate rents in premium retail zones

Landlords in Dubai, Riyadh, and Doha are securing record-high rents from high-traffic corridors, putting pressure on restaurant margins. This trend is compelling operators to either scale down or relocate to less prominent, secondary locations. In 2024, restaurant rents in Riyadh's Olaya district, a prominent commercial hub, increased by 12%, driven by multinational chains competing for prime storefronts as part of Vision 2030 initiatives. Similarly, Doha's Lusail district, supported by World Cup infrastructure, experienced a significant 20% year-on-year rent hike in 2024. This increase forced many independent operators to either exit the market or consolidate into food courts. To adapt, operators are reducing dining spaces and expanding delivery-only kitchen operations. For instance, Americana Restaurants reported that 44% of its revenue now comes from off-premise channels, reducing the need for large front-of-house areas. Additionally, some chains are negotiating revenue-share leases instead of fixed rents, transferring occupancy risks to landlords while limiting potential gains during peak seasons.

Growing "eat-at-home" preference post-inflation

Although headline inflation has moderated, household budgets remain under strain. Consequently, consumers are shifting toward grocery shopping and preparing meals at home instead of dining out. Inflation rates in the GCC peaked at 3-5% in 2023 but eased to 2-3% in 2024. However, food-price indices remain high due to the region's dependence on imports and currency volatility. To address these challenges, UAE supermarket chains such as Carrefour and LuLu Hypermarket introduced meal-kits in 2024. These kits, priced 40-50% lower than restaurant meals, include pre-portioned ingredients and recipe cards, enabling consumers to replicate restaurant-style dishes at home. Quick-service restaurants are also adapting; in 2024, Herfy Food Services launched a "SAR 15 Meal Deal," which bundles a sandwich, fries, and a drink, targeting price-sensitive customers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Foodservice Type: Cloud Kitchens Reshape Off-Premise Economics

In 2025, full-service restaurants accounted for 46.29% of the GCC Foodservice market by strategically enhancing customer experiences. They achieved this by combining appealing ambiance, engaging entertainment options, and multi-course menu offerings, which collectively drove higher check values. Café-bar hybrids have positioned themselves to serve both social gatherings and co-working needs, with mobile ordering now representing over 60% of Starbucks' transactions, showcasing the growing reliance on digital convenience. Quick-service giants, such as Americana, are capitalizing on the increasing demand for delivery services, which now contribute significantly to their overall network sales.

Cloud kitchens are rapidly gaining prominence, recording an impressive 13.24% CAGR. Talabat’s implementation of AI-driven order management systems and Dubai’s introduction of a dedicated licensing category have significantly reduced barriers to market entry, thereby increasing investor confidence. In Qatar, the enforcement of ventilation and inspection regulations has formalized operational standards, making the market more attractive to institutional investors. Additionally, operators are launching virtual brands to generate incremental revenue streams without negatively impacting dine-in sales. This approach is effectively blurring the lines between traditional foodservice formats and creating new opportunities for growth.

By Outlet: Chained Operators Leverage Scale and Data

In 2025, independents achieved a 58.73% revenue share, primarily due to their ability to offer personalized menus and foster strong loyalty within local communities. However, these establishments face significant challenges, including paying 10-15% higher costs for supplies compared to their larger counterparts and frequently lacking access to integrated delivery technology. Although Monsha’at provides grants aimed at facilitating digital upgrades, the process of adhering to labor quota compliance remains a considerable obstacle for many independent operators.

Chained outlets are experiencing substantial revenue growth, with a compound annual growth rate (CAGR) of 12.84%. These chains benefit from economies of scale, which enable centralized procurement, consistent employee training programs, and the use of analytics to drive strategic decision-making. The acquisition of Five Guys by Alamar Foods highlights the increasing demand for premium fast-casual dining experiences with higher ticket sizes. Additionally, global master franchisees are rapidly experimenting with plant-based and low-sugar product lines across hundreds of locations, significantly accelerating the pace of menu innovation and adaptation to evolving consumer preferences.

By Location: Leisure Destinations Capture Experiential Spend

In 2025, standalone locations, including street-level restaurants and suburban outlets, captured 72.24% of the market share. These establishments, serving both residential areas and commuter corridors, enjoy lower rents compared to their mall-anchored or airport-based counterparts. This cost advantage allows them to offer competitive pricing and more spacious dining areas. Furthermore, standalone formats grant operators enhanced flexibility: they can extend operating hours, alter facades, and add drive-through lanes without needing landlord consent or facing common-area limitations. While retail-anchored outlets in shopping malls benefit from consistent foot traffic and longer hours, they grapple with premium rents and reduced autonomy due to mall management oversight. Restaurants within hotels and resorts, catering to both business travelers and tourists, often see boosted revenues through room-service markups and event catering. Meanwhile, concessions at airports and train stations, despite commanding the highest rents, enjoy the highest customer throughput, with travelers frequently paying a 20-30% premium for the sake of convenience.

Leisure-anchored outlets, encompassing theme parks and entertainment districts, are witnessing the fastest expansion in this segment, growing at a 13.69% CAGR from 2026 to 2031. These venues are evolving into destination dining spots, merging culinary experiences with entertainment. A testament to this trend is Qiddiya, a sprawling 366-square-kilometer entertainment project near Riyadh, which, upon completion, will boast over 300 restaurants and cafés, catering to both local and international tourists. Additionally, leisure-anchored formats enjoy higher spending; patrons at theme parks and waterfront venues typically shell out 25-35% more per visit than those at standalone or retail spots, a trend attributed to longer stay durations and fewer nearby dining options.

By Service Type: Delivery Platforms Redefine Mealtime Convenience

In 2025, dine-in services accounted for 62.24% of the market share, highlighting the enduring appeal of experiential dining. Features such as ambiance, social interaction, and multi-sensory engagement justify the premium pricing. To differentiate from delivery-only competitors, operators invest significantly in interior design, live entertainment, and chef-driven menus, creating a unique dining experience that cannot be replicated at home. Meanwhile, takeaway services, which include walk-in pickups and drive-through orders, remain a consistent revenue contributor, particularly for quick-service chains that efficiently optimize kitchen throughput and reduce wait times.

Delivery services are experiencing rapid growth, with a 13.78% CAGR projected from 2026 to 2031, making it the fastest-growing segment. Platforms like Talabat, which reported a Q2 2025 gross merchandise value of USD 2.439 billion, a 32% year-on-year increase, are leading this growth. These platforms leverage AI-driven demand forecasting and dynamic pricing to enhance kitchen utilization and reduce waste. Saudi Arabia's online food delivery market grew at over 30% CAGR between 2020 and 2024, prompting Talabat to collaborate with robotics firm Wings to pilot autonomous last-mile delivery in Dubai. This initiative reduces delivery times and labor costs. In the post-inflation environment, household budgets are prioritizing convenience, with consumers increasingly replacing restaurant meals with delivery orders to save on travel and parking costs. This shift is accelerating the structural growth of the delivery channel.

Geography Analysis

In 2025, Saudi Arabia accounted for 47.27% of the GCC's foodservice revenue, supported by Vision 2030 mega-projects that incorporated thousands of restaurant seats into mixed-use developments. The 2023-24 Riyadh Season, a recurring entertainment festival, attracted 22 million visitors and generated an economic impact exceeding SAR 10 billion (USD 2.67 billion). During this period, foodservice operators reported revenue increases of 30-40%. Saudization mandates, requiring Saudi nationals to fill hospitality roles by 2025, are driving up wage costs. However, these mandates are also improving service quality and reducing employee turnover. To meet compliance requirements, operators are investing in vocational training centers.

Kuwait, despite its smaller population, is projected to achieve the highest growth at a 13.89% CAGR from 2026 to 2031. This growth is driven by National Vision 2035 diversification efforts and a strong dining-out culture, with households allocating 15-20% of their discretionary income to foodservice. The Silk City mega-project, a USD 86 billion initiative on Boubyan Island, is expected to feature over 500 restaurants and cafés, catering to both domestic and regional tourists. In February 2026, Kuwait implemented delivery platform regulations, capping commission rates at 15%. While this move may compress aggregator margins, it is anticipated to enhance restaurant profitability and encourage menu innovation. With over 98% of its population living in urban areas, Kuwait's compact geography and high urbanization rate enable fast delivery times, often within 25 minutes. This logistical advantage allows cloud kitchens to increase order frequency.

The United Arab Emirates, Qatar, Bahrain, and Oman collectively contribute a significant share of the region's foodservice revenue. Each country demonstrates unique growth patterns shaped by tourism infrastructure, regulatory frameworks, and demographic characteristics. Expo City Dubai, a permanent district developed on the former Expo 2020 site, is allocating AED 10 billion (USD 2.72 billion) to expand its area to 180,000 square meters by 2031. This expansion will establish retail and dining hubs designed to serve an estimated 25 million annual visitors. Qatar, leveraging its World Cup legacy, has maintained steady tourist arrivals. The Doha Metro expansion has improved access to dining districts, reducing reliance on private vehicles. Oman's Vision 2040 strategy, which aims to triple tourism revenues, is supported by projects like Muscat Bay and Yiti. These developments are increasing foodservice capacity, targeting long-haul travelers from Europe and Asia. However, regulatory harmonization remains incomplete. Each GCC country enforces distinct food-safety standards, licensing fees, and labor quotas, complicating regional expansion and increasing compliance costs for chains.

Competitive Landscape

The GCC foodservice sector, marked by moderate fragmentation, presents significant opportunities for independent restaurants, regional chains, and emerging cloud-kitchen brands to establish themselves. These players are leveraging localized menus, niche cuisines, and hyper-local delivery models to differentiate themselves in the market. There is a noticeable gap in offerings such as healthy fast-casual formats, plant-based concepts, and ethnic cuisines that are currently underrepresented. To address this demand, several UAE-based chains introduced vegan burger lines in 2024, responding to a reported 20-25% increase in consumer requests for dairy-free and gluten-free options, reflecting a shift in dietary preferences across the region. The major players operating on the market include ALBAIK Food Systems Company SA, Americana Restaurants International PLC, MH Alshaya Co. WLL, Riyadh International Catering Corporation, Herfy Food Service Company, among others.

Technology adoption is becoming a critical factor in determining market leaders. Operators utilizing advanced tools like AI-driven demand forecasting, dynamic pricing strategies, and integrated loyalty programs are achieving 12-15% higher unit economics compared to competitors relying on traditional, manual processes. For example, Talabat integrated machine-learning models into its merchant dashboard in 2025, enabling restaurants to accurately predict hourly order volumes. This capability allowed businesses to optimize preparation schedules, significantly reducing food spoilage and overtime labor costs. Similarly, Kudu Company for Food and Catering launched a proprietary mobile application in 2024, which combined features such as loyalty points, pre-ordering options, and real-time delivery tracking. This innovation led to a 25% increase in repeat customer frequency, showcasing the impact of technology-driven customer engagement.

Cloud-kitchen aggregators are emerging as key disruptors in the sector. These operators manage multiple virtual brands from a single facility, allowing them to test new concepts with minimal capital investment and adapt quickly based on real-time sales data. Regulatory compliance is also becoming a strategic advantage for businesses. For instance, Dubai Municipality's mandate requiring all cloud kitchens to register under a dedicated "virtual restaurant" category by mid-2025 is expected to raise barriers to entry for new players. However, this regulation also legitimizes the cloud-kitchen format, making it more attractive to institutional investors. Additionally, labor-nationalization quotas are accelerating the adoption of automation technologies. In 2024, several UAE-based quick-service restaurant (QSR) outlets deployed self-service kiosks and robotic kitchen assistants, reducing reliance on frontline labor while improving order accuracy and operational efficiency.

GCC Foodservice Industry Leaders

-

ALBAIK Food Systems Company SA

-

Americana Restaurants International PLC

-

MH Alshaya Co. WLL

-

Riyadh International Catering Corporation

-

Herfy Food Service Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Brunch and Cake, an all-day dining chain, opened its sixth location at Palm Jumeirah Mall. The 206-square-meter restaurant, situated on Level 01, serves the brand's signature menu featuring brunch dishes, all-day dining options, and fresh-baked pastries including croissants, cookies, and cakes.

- July 2025: Little Caesars opened its first restaurant in the United Arab Emirates, offering large classic pizzas including pepperoni, veggie, and cheese varieties. The Dubai opening represents a significant step in Little Caesars' international expansion.

- June 2025: Papa John's introduced a Croissant Pizza in the United Arab Emirates, featuring a flaky, buttery croissant-style dough base. The new product combines traditional pizza toppings with a pastry-like crust texture.

- April 2025: Pret A Manger has launched its first outlet in Saudi Arabia, located in the Olaya Towers of Riyadh. This initiative marks a key milestone in the brand's broader expansion strategy across the Gulf Cooperation Council (GCC) region.

GCC Foodservice Market Report Scope

The GCC foodservice market is segmented by foodservice type, outlet, location, and geography. By foodservice type, the market is segmented into café and bars, cloud kitchen, full-service restaurants, and quick service restaurants. By outlet, the market is segmented into chain and independent. By location, the market is segmented into leisure, lodging, retail, standalone, and travel. By service type, the market is segmented into dine-in, takeaway, and delivery. By geography, the market is segmented into the United Arab Emirates, Bahrain, Saudi Arabia, Kuwait, Oman, and Qatar. For each segment, the market forecasts are provided in value (USD).

| Cafe and Bars | By Cuisine | Bars and Pubs |

| Caf� | ||

| Juice/Smoothie/Desserts Bars | ||

| Specialist Coffee and Tea Shops | ||

| Cloud Kitchen | ||

| Full Service Restaurants | By Cuisine | Asian |

| European | ||

| Latin American | ||

| Middle Eastern | ||

| North American | ||

| Other FSR Cuisines | ||

| Quick Service Restaurants | By Cuisine | Bakeries |

| Burger | ||

| Ice Cream | ||

| Meat-based Cuisines | ||

| Pizza | ||

| Other QSR Cuisines |

| Chained Outlets |

| Independent Outlets |

| Leisure |

| Lodging |

| Retail |

| Standalone |

| Travel |

| Dine-in |

| Takeaway |

| Delivery |

| United Arab Emirates |

| Bahrain |

| Saudi Arabia |

| Kuwait |

| Oman |

| Qatar |

| By Foodservice Type | Cafe and Bars | By Cuisine | Bars and Pubs |

| Caf� | |||

| Juice/Smoothie/Desserts Bars | |||

| Specialist Coffee and Tea Shops | |||

| Cloud Kitchen | |||

| Full Service Restaurants | By Cuisine | Asian | |

| European | |||

| Latin American | |||

| Middle Eastern | |||

| North American | |||

| Other FSR Cuisines | |||

| Quick Service Restaurants | By Cuisine | Bakeries | |

| Burger | |||

| Ice Cream | |||

| Meat-based Cuisines | |||

| Pizza | |||

| Other QSR Cuisines | |||

| By Outlet | Chained Outlets | ||

| Independent Outlets | |||

| By Locations | Leisure | ||

| Lodging | |||

| Retail | |||

| Standalone | |||

| Travel | |||

| By Service Type | Dine-in | ||

| Takeaway | |||

| Delivery | |||

| By Geopgraphy | United Arab Emirates | ||

| Bahrain | |||

| Saudi Arabia | |||

| Kuwait | |||

| Oman | |||

| Qatar | |||

Market Definition

- FULL-SERVICE RESTAURANTS - A foodservice establishment where customers are seated at a table, give their order to a server and are served food at a table.

- QUICK SERVICE RESTAURANTS - A foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables.

- CAFES & BARS - A type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars.

- CLOUD KITCHEN - A foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers.

| Keyword | Definition |

|---|---|

| Albacore Tuna | It is one of the smallest species of tuna found in the six distinct stocks known globally in the Atlantic, Pacific, and Indian oceans, as well as the Mediterranean Sea. |

| Angus beef | It is beef derived from a specific breed of cattle indigenous to Scotland. It requires certification from the American Angus Association to receive the "Certified Angus Beef" quality mark. |

| Asian cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Chinese, Indian, Korean, Japanese, Bengali, Southeast Asian, etc. |

| Average Order Value | It is the average value of all orders made by the customers at a foodservice establishment. |

| Bacon | It is salted or smoked meat that comes from the back or sides of a pig. |

| Bars & Pubs | It is a drinking establishment that is licensed to serve alcoholic drinks for consumption on the premises. |

| Black Angus | It is beef derived from a black-hided breed of cows that don't have horns. |

| BRC | British Retail Consortium |

| Burger | It is a sandwich consisting of one or more cooked beef patties, placed inside a sliced bread roll or bun roll. |

| Café | It is a foodservice establishment serving various refreshments (mainly coffee) and light meals. |

| Cafes & Bars | It is a type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars. |

| Cappuccino | It is an Italian coffee drink that is traditionally prepared with equal parts double espresso, steamed milk, and steamed milk foam. |

| CFIA | Canadian Food Inspection Agency |

| Chained Outlet | It refers to a foodservice establishment that shares brands, operates in several locations, has central management, and standardized business practices. |

| Chicken Tender | It refers to chicken meat prepared from the pectoralis minor muscles of a chicken bird. |

| Cloud Kitchen | It is a foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers. |

| Cocktail | It is an alcoholic mixed drink made with either a single spirit or a combination of spirits, mixed with other ingredients such as juices, flavored syrups, tonic water, shrubs, and bitters. |

| Edamame | It is a Japanese dish prepared with soybeans (harvested before they ripen or harden) and cooked in its pod. |

| EFSA | European Food Safety Authority |

| ERS | Economic Research Service of the USDA |

| Espresso | It is a concentrated form of coffee, served in shots. |

| European cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Italian, French, German, English, Dutch, Danish, etc. |

| FDA | Food and Drug Administration |

| Fillet Mignon | It is a cut of meat taken from the smaller end of the tenderloin. |

| Flank Steak | It is a cut of beef steak taken from the flank, which lies forward of the rear quarter of a cow. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Franks | Also known as frankfurter or Würstchen, it is a type of highly seasoned smoked sausage popular in Austria and Germany. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Full service restaurant | It refers to a foodservice establishment where customers are seated at a table, give their order to a server, and are served food at a table. |

| Ghost Kitchen | It refers to a cloud kitchen. |

| GLA | Gross Leasable Area |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Grain-fed beef | It is beef derived from cattle that have been fed a diet supplemented with soy and corn and other additives. Grain-fed cows can also be given antibiotics and growth hormones to fatten them up more quickly. |

| Grass-fed beef | It is beef derived from cattle that have only been fed grass as feed. |

| Ham | It refers to the pork meat taken from the leg of a pig. |

| HoReCa | Hotels, Restaurants and Cafes |

| Independent Outlet | It refers to a foodservice establishment that operates with a single outlet or is structured as a small chain with no more than three locations. |

| Juice | It is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| Latin American | It includes full-service offerings in restaurants that serve cuisines from cultures such as Mexican, Brazilian, Argentinian, Colombian, etc. |

| Latte | It is a milk-based coffee that is made up of one or two shots of espresso, steamed milk, and a thin layer of frothed milk. |

| Leisure | It refers to foodservice offered as a part of a recreation business, such as sports arenas, zoos, movie theaters, and museums. |

| Lodging | It refers to foodservice offerings at hotels, motels, guesthouses, holiday homes, etc. |

| Macchiato | It is an espresso coffee drink with a small amount of milk, usually foamed. |

| Meat-based cuisines | This inlcudes food items like fried chicken, steak, ribs, etc. where meat is the primary ingredient for the dish. |

| Middle Eastern cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Arabic, Lebanese, Iranian, Israeli, etc. |

| Mocktail | It is an non-alcoholic mixed drink. |

| Mortadella | It is a large Italian sausage or luncheon meat made of finely hashed or ground heat-cured pork, which incorporates at least 15% small cubes of pork fat. |

| North American | It includes full-service offerings in restaurants that serve cuisines from cultures such as American, Canadian, Caribbean, etc. |

| Pastrami | It refers to a highly seasoned smoked beef, typically served in thin slices. |

| PDO | Protected Designation of Origin: It is the name of a geographical region or specific area that is recognized by official rules to produce certain foods with special characteristics related to location. |

| Pepperoni | It is an American variety of spicy salami made from cured meat. |

| Pizza | It is a dish made typically of flattened bread dough spread with a savory mixture usually including tomatoes and cheese and often other toppings and baked. |

| Primal cuts | It refers to the major sections of the carcass. |

| Quick service restaurant | It refers to a foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables. |

| Retail | It refers to a foodservice outlet inside a mall. shopping complex or a commercial real estate building, where there are other businesses operating as well. |

| Salami | It is a cured sausage consisting of fermented and air-dried meat. |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Scallop | It is an edible shellfish that is a mollusk with a ribbed shell in two parts. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Self-service kiosk | It refers to a self-order point-of-sale (POS) system through which customers place and pay for their own orders at kiosks, enabling totally contactless and frictionless service. |

| Smoothie | It is a beverage made by placing all the ingredients in a container and processing them together, without removing the pulp. |

| Specialty coffee & tea shops | It refers to a foodservice establishment that serves only various types of tea or coffee. |

| Standalone | It refers to a restaurants that have an independent infrastructure setup and not connected to any other business. |

| Sushi | It is a Japanese dish of prepared vinegared rice, usually with some sugar and salt, accompanied by a variety of ingredients, such as seafood—often raw—and vegetables. |

| Travel | It refers to foodservice offerings such as airplane food, dining on long-distance trains, and foodservice on cruise ships. |

| Virtual Kitchen | It refers to a cloud kitchen. |

| Wagyu Beef | It is beef derived from any of four strains of a breed of black or red Japanese cattle that are valued for their highly marbled meat. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for the market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market size estimations for the forecast years are in nominal terms. Inflation is considered for average order value, and it is forecasted as per predicted inflation rates in the countries.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms