Europe Automotive Semiconductor Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

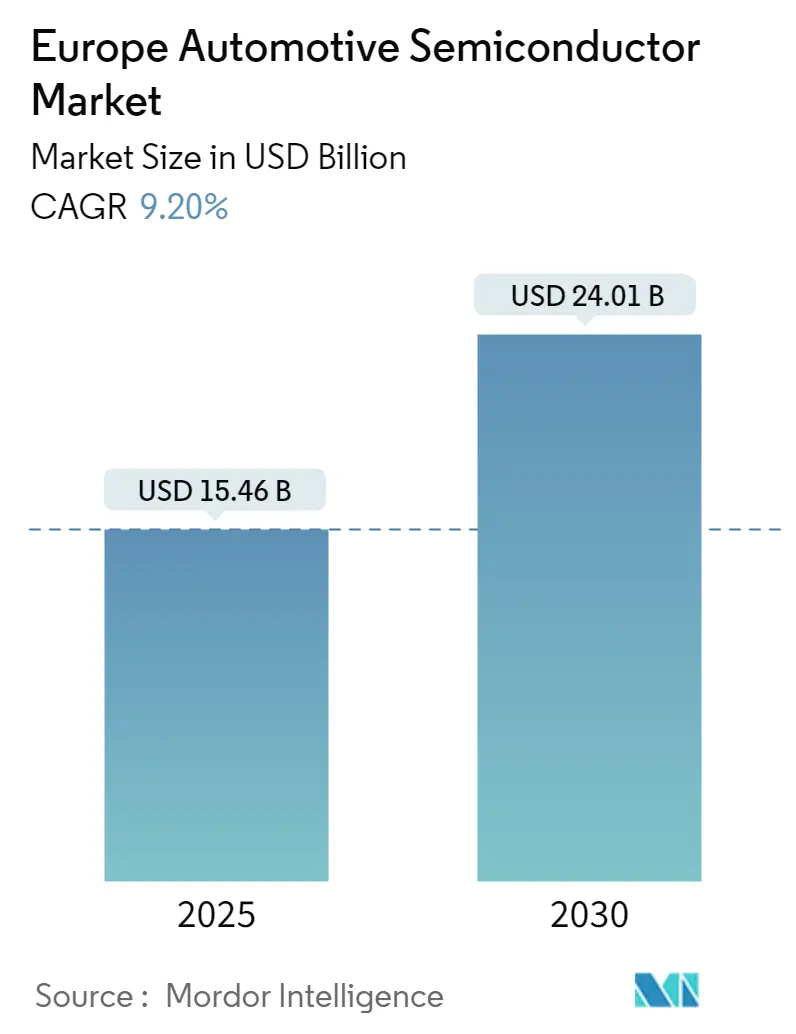

| Market Size (2025) | USD 15.46 Billion |

| Market Size (2030) | USD 24.01 Billion |

| Growth Rate (2025 - 2030) | 9.20% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Automotive Semiconductor Market Analysis by Mordor Intelligence

The Europe Automotive Semiconductor Market size is estimated at USD 15.46 billion in 2025, and is expected to reach USD 24.01 billion by 2030, at a CAGR of 9.2% during the forecast period (2025-2030).

The European automotive semiconductor landscape is undergoing a transformative phase, marked by significant investments in domestic manufacturing capabilities. A landmark development occurred in August 2023 when industry leaders Robert Bosch GmbH, TSMC, NXP Semiconductors NV, and Infineon Technologies AG announced their joint investment in the European Semiconductor Manufacturing Company (ESMC) in Dresden, Germany. This initiative, aligned with the European Chips Act, aims to establish a 300mm fab facility with a monthly production capacity of 40,000 wafers on advanced process technologies, creating approximately 2,000 direct high-tech professional jobs. The facility's construction is scheduled to commence in the second half of 2024, with production targeted for late 2027.

The industry is witnessing rapid technological advancement in semiconductor manufacturing processes and applications. In March 2024, the UK government demonstrated its commitment to semiconductor innovation by introducing a significant EUR 16.6 million investment, primarily focused on developing automotive chips for high-energy applications, particularly in electric vehicles. This investment aligns with the broader European strategy to enhance domestic semiconductor capabilities and reduce dependency on external suppliers. The region's semiconductor sales have shown consistent performance, maintaining steady levels between USD 4.4-4.8 billion monthly from July 2023 to January 2024, reflecting the market's stability and growth potential.

Strategic partnerships and collaborations are reshaping the industry's competitive landscape. In February 2024, Analog Devices Inc. established a crucial partnership with TSMC through its subsidiary in Japan, strengthening the region's semiconductor manufacturing capabilities. Similarly, in April 2024, ZF Friedrichshafen AG and Wolfspeed Inc. announced plans for a joint European R&D center in the Nuremberg Metropolitan Region, focusing on advancing Silicon Carbide automotive power electronics. These collaborations are instrumental in developing next-generation automotive semiconductor technologies and establishing robust supply chains within Europe.

The market is increasingly aligned with sustainability goals and electric vehicle adoption trends. According to the World Economic Forum, European roads are projected to host approximately 40 million electric vehicles by 2030, a significant increase from the current 8 million EVs. This transition is supported by various initiatives, including the European Green Deal and national programs aimed at reducing carbon emissions. In response to this trend, semiconductor manufacturers are developing specialized solutions for electric vehicle applications, particularly in power management, battery systems, and charging infrastructure, demonstrating the industry's commitment to supporting sustainable transportation solutions through electric vehicle semiconductor innovations.

Worldwide, activity is shaped by contributions from multiple regions, with Europe representing one of the more structurally developed among them. The global report on automotive semiconductor market by Mordor Intelligence reflects how these regional layers combine into a single system.

Europe Automotive Semiconductor Market Trends and Insights

Increasing Vehicle Production and Adoption of EVs

The automotive semiconductor market in Europe is experiencing substantial growth driven by increasing vehicle production across major manufacturing countries. According to the International Organization of Motor Vehicle Manufacturers (OICA), Germany maintained its position as Europe's largest automobile manufacturer, producing approximately 4.1 million vehicles in 2023, while France recorded production of 1.5 million motor vehicles in the same year, with 68.2% being passenger cars. This robust production environment has created a strong demand for automotive electronics across various applications, from basic control units to advanced power management systems.

The transition towards electric vehicles (EVs) has emerged as a significant driver for semiconductor demand, with manufacturers requiring more sophisticated power management and control systems. This trend is evidenced by the growing EV adoption in key markets like Germany, where new electric car registrations increased from 470,559 in 2022 to 524,219 in 2023, according to the Kraftfahrt-Bundesamt (KBA). The semiconductor industry is responding to this demand through strategic initiatives, as demonstrated by Infineon Technologies AG and GlobalFoundries' January 2024 agreement on the supply of AURIX TC3x 40 nanometer automotive microcontroller and power management solutions, securing production capacity through 2030 to support the growing EV market.

Growing Demand for Advanced Safety and Comfort Systems Augmented by Government Regulations

The increasing integration of advanced safety features and comfort systems in vehicles, supported by stringent European regulations, is driving significant demand for automotive semiconductors. These components are crucial in implementing essential safety systems such as anti-lock braking systems (ABS), electronic stability control (ESC), and advanced driver-assistance systems (ADAS). The semiconductor technology enables real-time data processing and precise control, enhancing vehicle stability and preventing accidents through features like rapid brake pressure modulation and selective braking control for individual wheels.

The European Union's commitment to road safety through initiatives like 'Vision Zero,' which aims to eliminate road fatalities by 2050, has created a regulatory environment that mandates the incorporation of advanced safety technologies. This regulatory framework has led to the mandatory implementation of various ADAS semiconductor features and safety systems in new vehicles, driving the demand for sophisticated semiconductor solutions. The industry is responding with innovations in sensor technology, vision systems, and AI chips, enabling vehicles to better perceive their surroundings and make intelligent decisions in real-time. For instance, German semiconductor companies are developing advanced sensors and microcontrollers specifically designed for automotive safety applications, while also focusing on enhancing comfort features through improved infotainment systems and connected car technologies.

Segment Analysis: By Vehicle Type

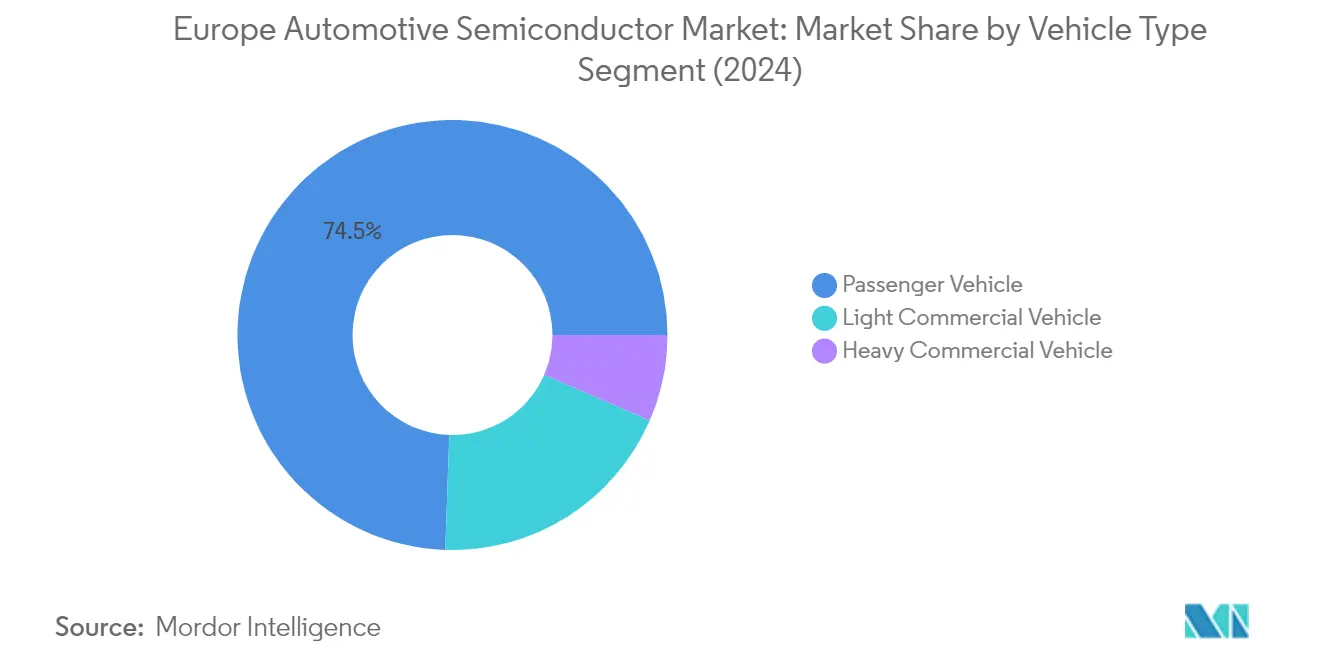

Passenger Vehicle Segment in Europe Automotive Semiconductor Market

The passenger vehicle segment dominates the European automotive semiconductor market, commanding approximately 74% of the market share in 2024. This significant market position is driven by the increasing integration of advanced electronic systems in modern passenger vehicles, particularly in premium and luxury car segments. The segment's growth is further bolstered by stringent European regulations mandating advanced safety features and the rising adoption of electric vehicles. Major European automotive manufacturers like BMW, Volkswagen, and Mercedes-Benz are incorporating more sophisticated semiconductor components in their passenger vehicles, particularly for applications such as advanced driver assistance systems (ADAS), infotainment systems, and powertrain control. The segment's robust performance is also supported by the growing consumer demand for connected car features and autonomous driving capabilities in passenger vehicles.

Heavy Commercial Vehicle Segment in Europe Automotive Semiconductor Market

The heavy commercial vehicle segment is emerging as the fastest-growing segment in the European automotive semiconductor market, projected to grow at approximately 12% CAGR from 2024 to 2029. This remarkable growth is primarily driven by the increasing electrification of commercial vehicles and the implementation of stringent emission regulations across Europe. The segment is witnessing substantial technological advancements, particularly in fleet management systems, telematics, and autonomous driving capabilities. European commercial vehicle manufacturers are increasingly investing in semiconductor-intensive technologies to enhance vehicle efficiency, safety, and connectivity. The adoption of electric powertrains in heavy commercial vehicles is creating additional demand for power semiconductors, battery management systems, and other electronic components. Furthermore, the integration of advanced driver assistance systems and safety features in commercial vehicles is contributing significantly to the segment's growth trajectory.

Remaining Segments in Vehicle Type

The light commercial vehicle segment represents a significant portion of the European automotive electronics market, bridging the gap between passenger vehicles and heavy commercial vehicles. This segment is experiencing substantial transformation with the integration of advanced telematics systems, fleet management solutions, and electrification initiatives. Light commercial vehicles are increasingly incorporating sophisticated semiconductor components for applications such as delivery optimization, route planning, and vehicle diagnostics. The segment is also witnessing growing adoption of advanced safety features and driver assistance systems, particularly in urban delivery vehicles. European manufacturers are focusing on developing more efficient and connected light commercial vehicles to meet the evolving needs of last-mile delivery and urban logistics operations.

Segment Analysis: By Application

Safety Segment in Europe Automotive Semiconductor Market

The safety segment has emerged as the dominant force in the European automotive semiconductor market, commanding approximately 26% of the market share in 2024. This significant market position is driven by the increasing integration of advanced safety features in modern vehicles, including airbag deployment systems, anti-lock braking systems (ABS), and stability control mechanisms. The segment's growth is further bolstered by stringent European safety regulations mandating the implementation of various safety technologies in vehicles. The introduction of new safety features like intelligent speed assistance, drowsiness detection, and advanced driver monitoring systems has significantly contributed to the segment's dominance. European automakers are increasingly focusing on incorporating sophisticated safety semiconductors to enhance vehicle safety systems, particularly in response to the EU's Vision Zero initiative aimed at reducing road fatalities.

Power Electronics Segment in Europe Automotive Semiconductor Market

The automotive power electronics segment is experiencing the most rapid growth in the European automotive semiconductor market, with a projected growth rate of approximately 11% during the forecast period 2024-2029. This exceptional growth is primarily driven by the increasing adoption of electric vehicles (EVs) and hybrid vehicles across Europe. The segment's expansion is supported by technological advancements in wide bandgap materials like Gallium Nitride (GaN) and Silicon Carbide (SiC), which are revolutionizing power management in automotive applications. The surge in demand for efficient power conversion and management systems, particularly in electric powertrains, battery management systems, and charging infrastructure, is fueling this growth. European manufacturers are increasingly investing in automotive power electronics solutions to enhance vehicle efficiency and meet stringent emission regulations, while the rising focus on sustainable transportation continues to drive innovation in this segment.

Remaining Segments in Application Segmentation

The other significant segments in the European automotive electronics market include body electronics, comfort/entertainment units, chassis, and other applications. The body electronics segment plays a crucial role in vehicle control systems and diagnostic functions, while the comfort/entertainment unit segment focuses on enhancing user experience through advanced infotainment systems and connectivity solutions. The chassis segment contributes to vehicle stability and control systems, incorporating sophisticated semiconductor solutions for improved performance. Other applications encompass various automotive functions including telematics, instrument clusters, and lighting systems. Each of these segments contributes uniquely to the overall market dynamics, driven by increasing vehicle electrification, connectivity requirements, and the growing demand for advanced automotive features.

Competitive Landscape

Top Companies in Europe Automotive Semiconductor Market

The European automotive semiconductor market features prominent players including NXP Semiconductors, Infineon Technologies, Renesas Electronics, STMicroelectronics, Toshiba Electronic Devices, Texas Instruments, Robert Bosch, Micron Technology, ON Semiconductor, Analog Devices, and ROHM Company Limited. These companies are driving innovation through substantial investments in research and development, particularly focusing on electric vehicles, autonomous driving technologies, and advanced driver assistance systems. The industry witnesses continuous product launches and technological advancements, with companies developing specialized solutions for vehicle electrification, power management, and connectivity features. Strategic partnerships and collaborations have become increasingly common, especially in developing next-generation semiconductor solutions and establishing regional manufacturing capabilities. Companies are also expanding their production capacities and strengthening their supply chain networks to address the growing demand from European automotive manufacturers, while simultaneously focusing on sustainability and energy-efficient solutions.

Market Dominated by Global Technology Leaders

The European automotive semiconductor landscape is characterized by a mix of global technology conglomerates and specialized semiconductor manufacturers, with established players maintaining significant market presence through their extensive product portfolios and strong relationships with automotive OEMs. The market structure shows moderate consolidation, with major players leveraging their technological expertise and manufacturing capabilities to maintain their competitive positions. These companies have established robust distribution networks and maintain close partnerships with automotive manufacturers, tier-1 suppliers, and technology providers across Europe.

The industry has witnessed significant merger and acquisition activities, particularly focused on strengthening technological capabilities and expanding market presence. Companies are actively pursuing strategic acquisitions to enhance their product offerings, gain access to new technologies, and strengthen their position in emerging segments like electric vehicles and autonomous driving. The market also sees increasing collaboration between semiconductor manufacturers and automotive companies, leading to joint development initiatives and long-term supply agreements, particularly in addressing the growing demand for advanced automotive electronics solutions in modern vehicles.

Innovation and Adaptability Drive Market Success

Success in the European automotive semiconductor market increasingly depends on companies' ability to innovate and adapt to rapidly evolving technological requirements. Incumbent players are focusing on developing specialized solutions for electric vehicles, enhancing their research and development capabilities, and establishing strong partnerships with automotive manufacturers. Companies are also investing in advanced manufacturing facilities and adopting Industry 4.0 practices to improve operational efficiency and maintain quality standards. The ability to provide comprehensive solutions, including software integration and support services, has become crucial for maintaining market leadership.

Market contenders are gaining ground by focusing on niche applications, developing innovative solutions for specific automotive applications, and establishing strategic partnerships with regional automotive manufacturers. The industry faces moderate end-user concentration, with major automotive manufacturers wielding significant influence over semiconductor specifications and supply chains. While substitution risk remains low due to the specialized nature of automotive chips, regulatory requirements, particularly regarding safety standards and environmental regulations, continue to shape product development and market strategies. Companies are also increasingly focusing on sustainability initiatives and developing eco-friendly semiconductor solutions to align with European environmental regulations and customer preferences.

Europe Automotive Semiconductor Industry Leaders

NXP Semiconductors NV

Infineon Technologies AG

STMicroelectronics NV

Robert Bosch GMBH

Texas Instruments Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2024: Infineon Technologies AG, a prominent player in power systems and IoT, announced that it is strengthening its outsourced backend manufacturing footprint in Europe and revealed a multi-year partnership with Amkor Technology Inc., a significant semiconductor packaging and test service provider. The companies have agreed to operate a dedicated packaging and test center at Amkor's manufacturing site in Porto. The operations are anticipated to begin in the first half of 2025. With this long-term agreement, Infineon and Amkor are likely to strengthen their partnership further, extending the classical Outsourced Semiconductor Assembly and Test (OSAT) business model.

- February 2024: Infineon Technologies AG announced that Infineon and Honda Motor Co. Ltd signed a memorandum of understanding to build a strategic collaboration. Honda selected Infineon as a semiconductor partner to align future technology and product roadmaps. Infineon will support Honda with technologies that facilitate competitive and advanced vehicles. The technical support would focus on the area of power semiconductors, advanced driver assistance systems, and E/E architectures, where both parties would collaborate on new architecture concepts.

Europe Automotive Semiconductor Market Report Scope

For market estimation, we have tracked the revenue generated from the sale of automotive semiconductors offered by different market players for a diverse range of applications. The market trends are evaluated by analyzing the investments made in product innovation, diversification, and expansion. Furthermore, the advancements in electric vehicles, miniaturization of automotive electronics, advanced driver-assistance systems (ADAS), and connected cars are also crucial in determining the growth of the market.

The European automotive semiconductor market is segmented by vehicle type (passenger vehicle (discrete, optoelectronics. sensors and actuators, logic, memory, analog IC, micro), light commercial vehicle (discrete, optoelectronics. sensors and actuators, logic, memory, analog IC, micro), and heavy commercial vehicle (discrete, optoelectronics. sensors and actuators, logic, memory, analog IC, micro)), application (chassis, power electronics, safety, body electronics, comfort/entertainment, and other applications), and country (Germany, France, Italy, and Rest of Europe). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Passenger Vehicle | Discrete |

| Optoelectronics | |

| Sensors and Actuators | |

| Logic | |

| Memory | |

| Analog IC | |

| Micro | |

| Light Commercial Vehicle | Discrete |

| Optoelectronics | |

| Sensors and Actuators | |

| Logic | |

| Memory | |

| Analog IC | |

| Micro | |

| Heavy Commercial Vehicle | Discrete |

| Optoelectronics | |

| Sensors and Actuators | |

| Logic | |

| Memory | |

| Analog IC | |

| Micro |

| Chassis |

| Power Electronics |

| Safety |

| Body Electronics |

| Comfort/Entertainment Unit |

| Other Applications |

| United Kingdom |

| Germany |

| France |

| Italy |

| Vehicle Type | Passenger Vehicle | Discrete |

| Optoelectronics | ||

| Sensors and Actuators | ||

| Logic | ||

| Memory | ||

| Analog IC | ||

| Micro | ||

| Light Commercial Vehicle | Discrete | |

| Optoelectronics | ||

| Sensors and Actuators | ||

| Logic | ||

| Memory | ||

| Analog IC | ||

| Micro | ||

| Heavy Commercial Vehicle | Discrete | |

| Optoelectronics | ||

| Sensors and Actuators | ||

| Logic | ||

| Memory | ||

| Analog IC | ||

| Micro | ||

| Application | Chassis | |

| Power Electronics | ||

| Safety | ||

| Body Electronics | ||

| Comfort/Entertainment Unit | ||

| Other Applications | ||

| Country | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

Key Questions Answered in the Report

How big is the Europe Automotive Semiconductor Market?

The Europe Automotive Semiconductor Market size is expected to reach USD 15.46 billion in 2025 and grow at a CAGR of 9.20% to reach USD 24.01 billion by 2030.

What is the current Europe Automotive Semiconductor Market size?

In 2025, the Europe Automotive Semiconductor Market size is expected to reach USD 15.46 billion.

Who are the key players in Europe Automotive Semiconductor Market?

NXP Semiconductors NV, Infineon Technologies AG, STMicroelectronics NV, Robert Bosch GMBH and Texas Instruments Inc. are the major companies operating in the Europe Automotive Semiconductor Market.

What years does this Europe Automotive Semiconductor Market cover, and what was the market size in 2024?

In 2024, the Europe Automotive Semiconductor Market size was estimated at USD 14.04 billion. The report covers the Europe Automotive Semiconductor Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Europe Automotive Semiconductor Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: